© 2003 mcgraw-hill ryerson limited 14 chapter capital markets mcgraw-hill ryerson©2003 mcgraw-hill...

TRANSCRIPT

© 2003 McGraw-Hill Ryerson Limited

1414Chapt

er

Chapt

er

Capital MarketsCapital Markets

McGraw-Hill Ryerson ©2003 McGraw-Hill Ryerson Limited

Based on:

Terry Fegarty, Gitman et al, Gallagher et al,Prentice Hall Slides

May 10, 2005

© 2003 McGraw-Hill Ryerson Limited

Chapter 14 - Outline

Financial System: Overview Financial Markets:

Capital Markets vs. Money Markets Primary vs. Secondary Markets Organized Exchanges vs. OTC

Financial Intermediaries Deregulation of the Financial Industry

Changes to the Banking System Market Efficiency Summary and Conclusions

PPT 14-2

© 2003 McGraw-Hill Ryerson Limited

Financial System: Overview

Central duty - to acquire funds.

© 2003 McGraw-Hill Ryerson Limited

Financial System: Overview

The Financial System is made up of two groups: suppliers of capital (entities and individuals that

have excess funds), and demanders of capital (entities and individuals

that need funds). The financial system makes it possible for

participants to adjust their holdings of financial assets as their needs change.

This is the liquidity function of the financial system, that is, the system allows funds to flow with ease.

© 2003 McGraw-Hill Ryerson Limited

Financial System: Overview

Along with this movement of funds through the financial system, funds are exchanged for financial products called securities.

The financial system provides the network that brings the two groups (savers & users) together:Financial MarketsFinancial Intermediaries

© 2003 McGraw-Hill Ryerson Limited

Funds Flow: No Intermediation

Markets

Intermediaries

Surplus Units Deficit Units

Markets

Intermediaries

Savers Users

© 2003 McGraw-Hill Ryerson Limited

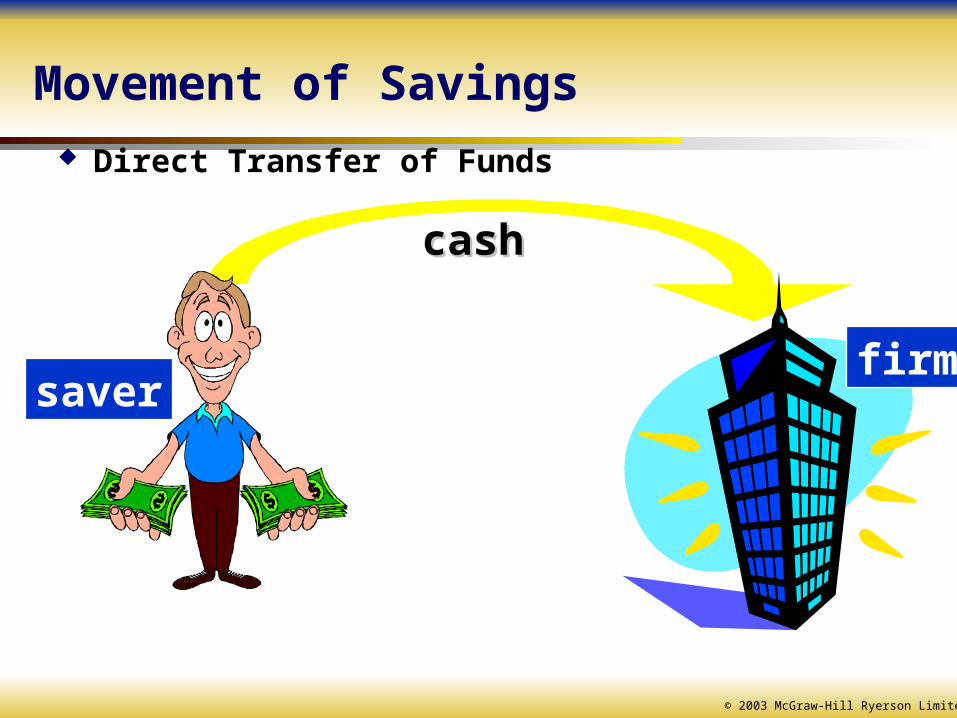

Direct Transfer of Funds

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Direct Transfer of Funds

saver

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Direct Transfer of Funds

saverfirm

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Direct Transfer of Funds

cashcash

saverfirm

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Direct Transfer of Funds

cashcash

securitiessecurities

saverfirm

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Financial Markets

Financial Markets provide a forum where suppliers of funds (savers)

and demanders of funds (users) can transact business.

bring savers and users of funds together to make a fair exchange that brings value to both parties.

Financial transactions can take place in one central location or in a dispersed location.

Example: Toronto Stock Exchange, Nasdaq

© 2003 McGraw-Hill Ryerson Limited

Financial Intermediaries

Financial Intermediaries act as the “grease” that enables the “machinery” of

the financial system to work smoothly. Example: Chartered Banks, Investment Bankers,

Stockbrokers, dealers, etc. Financial Intermediaries accomplish this by:

reducing the cost of bringing borrowers and savers together

bridging borrower’s and lender’s maturity preferences

reducing investment risk through diversification

© 2003 McGraw-Hill Ryerson Limited

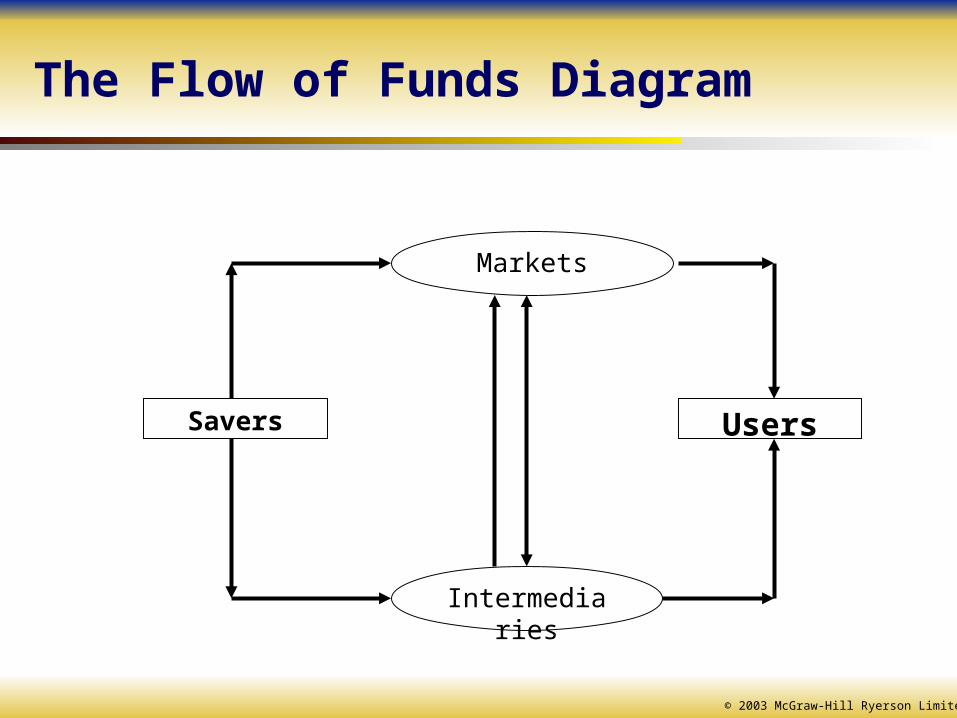

The Flow of Funds Diagram

Markets

Intermediaries

Savers Users

© 2003 McGraw-Hill Ryerson Limited

Fund Flows via Intermediary

Markets

Intermediaries

Savers Users

© 2003 McGraw-Hill Ryerson Limited

Movement of Savings

Indirect Transfer using a Financial Intermediary

© 2003 McGraw-Hill Ryerson Limited

Indirect Transfer using a Financial Intermediary

financialintermediary

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Indirect Transfer using a Financial Intermediary

financialintermediary firm

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Indirect Transfer using a Financial Intermediary

fundsfunds

financialintermediary firm

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Indirect Transfer using a Financial Intermediary

fundsfunds

firmfirmsecuritiessecurities

financialintermediary firm

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Indirect Transfer using a Financial Intermediary

fundsfunds

firmfirmsecuritiessecurities

financialintermediary firm

saver

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Indirect Transfer using a Financial Intermediary

fundsfunds fundsfunds

firmfirmsecuritiessecurities

financialintermediary firm

saver

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Indirect Transfer using a Financial Intermediary

fundsfunds

intermediaryintermediarysecuritiessecurities

fundsfunds

firmfirmsecuritiessecurities

financialintermediary firm

saver

Movement of Savings

© 2003 McGraw-Hill Ryerson Limited

Fund Flows via Market

Markets

Intermediaries

Savers Users

© 2003 McGraw-Hill Ryerson Limited

The Flow of Funds Diagram

Markets

Intermediaries

Savers Users

© 2003 McGraw-Hill Ryerson Limited

Financial Markets: Capital Markets vs. Money Markets

Two Distinct Financial Markets:1. Capital Markets are where L/T securities with maturities

greater than 1 year are traded ex., Common Stock, Preferred Stock, Bonds,

Mortgages, etc.

2. Money Markets are where S/T securities with maturities less than 1 year are traded ex., T-Bills, Commercial Paper, Negotiable Certificate

of Deposits, Bankers’ Acceptances, Eurocurrency

PPT 14-3

© 2003 McGraw-Hill Ryerson Limited

Money Market Securities

Securities traded in the Money Market include: Treasury Bills: Short-term instruments issued by the

Canadian Government that are sold at a discount and pay face value at maturity.

Negotiable Certificates of Deposits (CDs): certificates that can be traded in financial markets and represent amounts deposited at bank that will be repaid at maturity with a specified interest rate.

Commercial Paper: unsecured short-term promissory notes issued by large corporations with strong credit ratings.

Banker’s Acceptances: documents that signify a bank has a guaranteed payment of certain amount at a future date if the original issuer does not pay.

© 2003 McGraw-Hill Ryerson Limited

0

20

40

60

80

100

120

140

160

$ b

illio

ns

Government ofCanada

Treasury Bills

CommercialPaper

Asset-backedSecurities

Bankers'Acceptances

Other

Source: Bank of Canada Banking and Financial Statistics , January 2002, F2 and G6 series.

1991

2001

Figure 14-1 Canadian money market: securities outstanding

PPT 14-4

© 2003 McGraw-Hill Ryerson Limited

Capital Market Securities

Major Securities traded in the Capital Market include: Bonds:

Long-term securities that represent a promise to pay a fixed amount at a future date usually with interest payments made at regular intervals.

Issued by the Canadian Federal, Provincial and Municipal Governments and Corporations.

most widely used form of financing in recent years significant amounts raised abroad

© 2003 McGraw-Hill Ryerson Limited

0

50

100

150

200

250

300

$ b

illio

ns

Government ofCanada

Provincial andMunicipalities

Corporations

Source: Bank of Canada Banking and Financial Statistics , October 2001, G6 and K8 series.

1991

2001

Figure 14-2 Canadian Bond Market: Securities Outstanding (Canadian Dollars)

PPT 14-6

© 2003 McGraw-Hill Ryerson Limited

0

20

40

60

80

100

120

140

160

180

$ b

illio

ns

Government ofCanada

Provincial andMunicipalities

Corporations

Source: Bank of Canada Banking and Financial Statistics , October 2001, K8 series

1991

2001

Figure 14-3Canadian bonds outstanding: foreign currencies

PPT 14-8

© 2003 McGraw-Hill Ryerson Limited

Capital Market Securities

Major Securities traded in the Capital Market include: Shares:

Preferred shares come with fixed dividends and usually no voting

rights. least used of all L/T corporate securities

Common shares may come with dividends, paid at the discretion of the

board, and have voting rights. Common shareholders share in the residual profits of

the firm. Shares of ownership interest in corporations. 23 % of net new financings in 2000 more equity is being raised abroad by Canadian

corporations

© 2003 McGraw-Hill Ryerson Limited

-10

0

10

20

30

40

50

60

$ b

illio

ns

1991 1993 1995 1997 1999 2001Source: Bank of Canada Review, January 2002, F9 series.

Bonds

Preferreds

Common stock

Figure 14-4 Net new corporate financings by type of security

PPT 14-9

© 2003 McGraw-Hill Ryerson Limited

Financial Markets: Primary Vs. Secondary Markets

Both Capital and Money Markets have a Primary Market and a Secondary Market.

Primary Market is the market: that creates and places an initial value on financial

securities. where securities are traded for the first time.

Secondary Market is the market: where previously issued securities are traded among

investors. may occur on an exchange or OTC through your stockbroker.

© 2003 McGraw-Hill Ryerson Limited

Figure 14-10 Secondary Market: Daily trading averages

0

5

10

15

20

25$ b

illio

ns

Source: Investment Dealers Association Reports , July 2001, www.ida.ca

1997

2000

PPT 14-16

© 2003 McGraw-Hill Ryerson Limited

Organized Exchanges

Organized Exchanges operate in a central location where previously issued securities are traded. Exchanges are therefore, 2nd markets.Exchanges like the Toronto Stock Exchange (TSX) are organizations that facilitate the trading of stocks among investors.Corporations arrange for their company shares be listed for a fee on the Exchange so that investors may trade their shares at a designated “Post” or Exchange location.

© 2003 McGraw-Hill Ryerson Limited

Organized Exchanges

New York Stock Exchange (NYSE)

largest and most important market for stocks in world

Toronto Stock Exchange (TSX)

largest and most important market for stocks in Canadasmaller and less significant globally than NYSE

© 2003 McGraw-Hill Ryerson Limited

Table 14-1Global stock markets

Australia Korea

Austria Mexico

Belgium Netherlands

Brazil Norway

Canada Singapore/ Malaysia

Denmark Spain

France Sweden

Germany Switzerland

Hong Kong United Kingdom

Italy United States

Japan

PPT 14-18

© 2003 McGraw-Hill Ryerson Limited

OTC

OTC stands for over the counter. It has no central location unlike Exchanges. It is a network of dealers around the globe who

maintain inventories of securities for sale. Connected through computer terminals and

telephones buy and sell securities which are not listed on a stock

exchange bulk of all bond trading is done OTC

NASDAQ is the best known OTC market and rivals the New York Stock Exchange in trading volumes.

© 2003 McGraw-Hill Ryerson Limited

Financial Intermediaries: Functions/Roles

Financial Intermediaries can assume the following roles:

Investment Bankers - primarily involved in the underwriting of securities.

Brokers – are agents who work on behalf of the investor

Dealers – make a living by buying and reselling securities to others.

© 2003 McGraw-Hill Ryerson Limited

Investment Banking

How do investment bankers help firms issue securities?

Underwriting1 the issue. Distributing the issue. Advising the firm.

1Underwriting refers to the process by which an investment banker (usually in cooperation with other investment banking firms) purchases all the new securities from the issuing company and then resells them to the public.

© 2003 McGraw-Hill Ryerson Limited

Investment Banking -Distribution Methods

Negotiated Purchase Issuing firm selects an investment banker to

underwrite the issue. The firm and the investment banker negotiate the

terms of the offer.

Competitive Bid Several investment bankers bid for the right to

underwrite the firm’s issue. The firm selects the banker offering the highest price.

© 2003 McGraw-Hill Ryerson Limited

Investment Banking - Distribution Methods Best Efforts

Issue is not underwritten. Investment bank attempts to sell the issue for a

commission.

Privileged Subscription Issue is not underwritten also. Investment banker helps market the new issue to a

select group of investors. Usually targeted to current stockholders, employees,

or customers.

© 2003 McGraw-Hill Ryerson Limited

Financial Intermediaries-Underwriting

Direct Sale No investment banker is involved. Issuing firm sells the securities directly to the investing

public.

© 2003 McGraw-Hill Ryerson Limited

Principal Financial Intermediaries

Principal Financial Intermediaries in Canada:Chartered BanksTrust CompaniesCredit UnionsFinance CompaniesInsurance CompaniesMutual Funds CompaniesPension Funds CompaniesBank of Canada

© 2003 McGraw-Hill Ryerson Limited

Principal Financial Intermediaries

Chartered Banks – are financial institutions that exist primarily to lend money to businesses (commercial loans).

Example: Royal Bank, CIBC, TD Trust Companies – like chartered banks, are in business

to take in deposits and lend money, primarily mortgage loans.

Example: TD Canada Trust, BMO Trust, AGF Trust Credit Unions – are member-owned financial institutions.

They pay interest on shares bought by, and collect interest on loans made to the members.

Example: Caisses Populaires

© 2003 McGraw-Hill Ryerson Limited

Principal Financial Intermediaries

Finance Companies are non-bank firms that make short-term and long-term loan

to consumers and businesses. Often serve customers who do not qualify for loans at other

financial institutions. Funds are obtained from banks or by selling Commercial

Paper. Example: Household Finance, Beneficial Finance

Insurance Companies Are firms, for a fee (premiums), will assume risks for their

customers. Will pay beneficiaries of insured person when this person

dies (Life Insurance). Example: Standard Life, RBC Insurance, London Life

© 2003 McGraw-Hill Ryerson Limited

Principal Financial Intermediaries

Mutual Funds Companies Are investment companies that receive money from

individuals for investment in both the money and capital markets.

Professionals manage these money and may have the objective of safety, growth, income, high-risk, liquidity.

Example: AIM Trimark, ING Funds, Standard Life Mutual Funds, Scotia Mutual Funds

Pension Funds Companies Take in funds, usually contributed both by the employee

and the employer, and invest those funds for future payment to the employee.

Example: Altamira Financial Services, Fidelity Investments

© 2003 McGraw-Hill Ryerson Limited

0

200

400

600

800

1000

1200

1400

1600

1800

$ b

illio

ns

Banks

Trusteed

Pension FundsMutual

Funds

Insurance

Companies

Credit Unions/

Caisses Populaires

Trust

Companies

Finance and Savings

Source: Bank of Canada Review, January 2001, C3, D1-D5, series;Statistics Canada, Cataloque 74-001, 2nd Q. 2001.

1991

2001

Figure 14-8 Total assets of financial intermediaries

PPT 14-14

© 2003 McGraw-Hill Ryerson Limited

Deregulation of the Financial Industry

Prior to deregulation in 1987, financial institutions were allowed to operate only in one of the “four pillars”: chartered banks alternate banks (trust companies, credit unions, caisses

populaires) life insurance companies and specialized lending and

saving intermediaries investment dealers

Intense global competition led to major restructuring of the financial industry. These “4 pillars” were dismantled in the 1987 deregulation.

© 2003 McGraw-Hill Ryerson Limited

This led to 1-stop banking where:U.S.-based banks may compete in the Canadian marketBanks may own securities dealersBanks may own insurance companies and sell commercial paperBanks may create mutual fund subsidiariesTrust companies have been taken over by banks or have been reduced in their importance.

Changes to the Banking System

PPT 14-22

© 2003 McGraw-Hill Ryerson Limited

Market Efficiency Market Efficiency refers to the ease, speed and cost of

trading securities.

In an efficient market, securities can be traded easily, quickly, and at low costs.

Markets lacking these qualities are considered inefficient.

The major stock markets are considered efficient because investors can trade thousands of dollars worth of shares in minutes by making a phone call and paying a relatively small commission.

PPT 14-20

© 2003 McGraw-Hill Ryerson Limited

Summary and Conclusions

Capital markets refer to the trading of financial assets with long terms to maturity, including stocks, bonds, and mortgages.Canadian corporations seek funds from both stock and bond markets, Canadian and foreignThe Toronto Stock Exchange (TSX) is the dominant Canadian exchange.Bonds are traded in the Over-The -Counter marketMajor changes in the Canadian financial market include one-stop financial services, more investment banking, and more foreign banks.

PPT 14-23

OK, LET’S RECAP . . .