© 2008 by nelson, a division of thomson canada limited transparency 4.1 finance for non-financial...

TRANSCRIPT

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.1

Finance for Non-Financial ManagersFifth Edition

Slides prepared by

Pierre G. BergeronUniversity of Ottawa

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.2

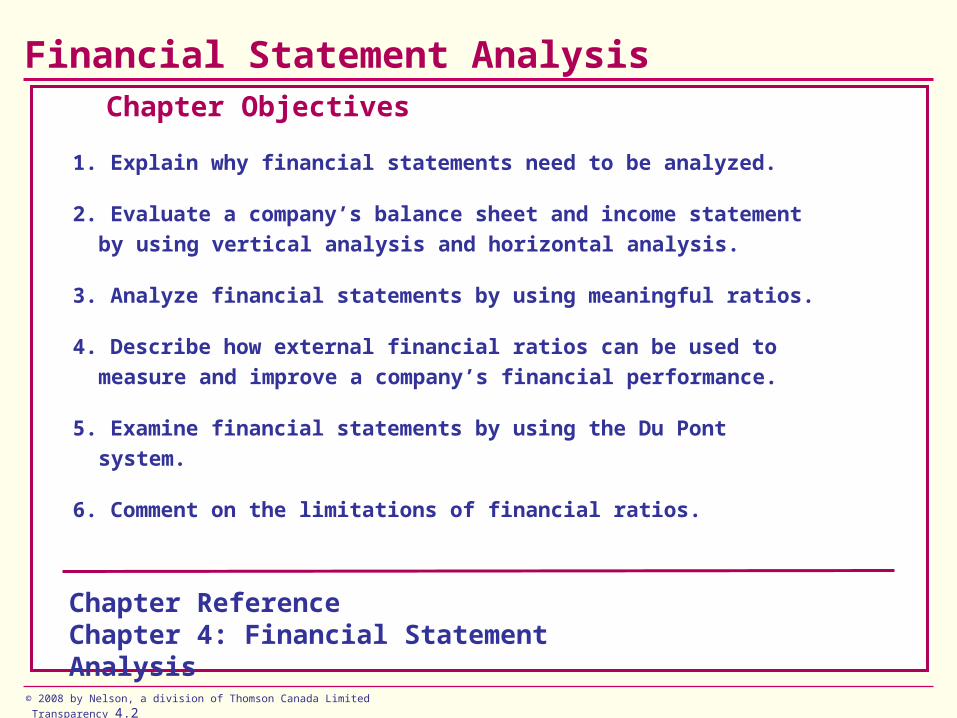

Financial Statement Analysis

Chapter Objectives

1. Explain why financial statements need to be analyzed.

2. Evaluate a company’s balance sheet and income statement by

using vertical analysis and horizontal analysis.

3. Analyze financial statements by using meaningful ratios.

4. Describe how external financial ratios can be used to measure

and improve a company’s financial performance.

5. Examine financial statements by using the Du Pont system.

6. Comment on the limitations of financial ratios.

Chapter ReferenceChapter 4: Financial Statement Analysis

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.3

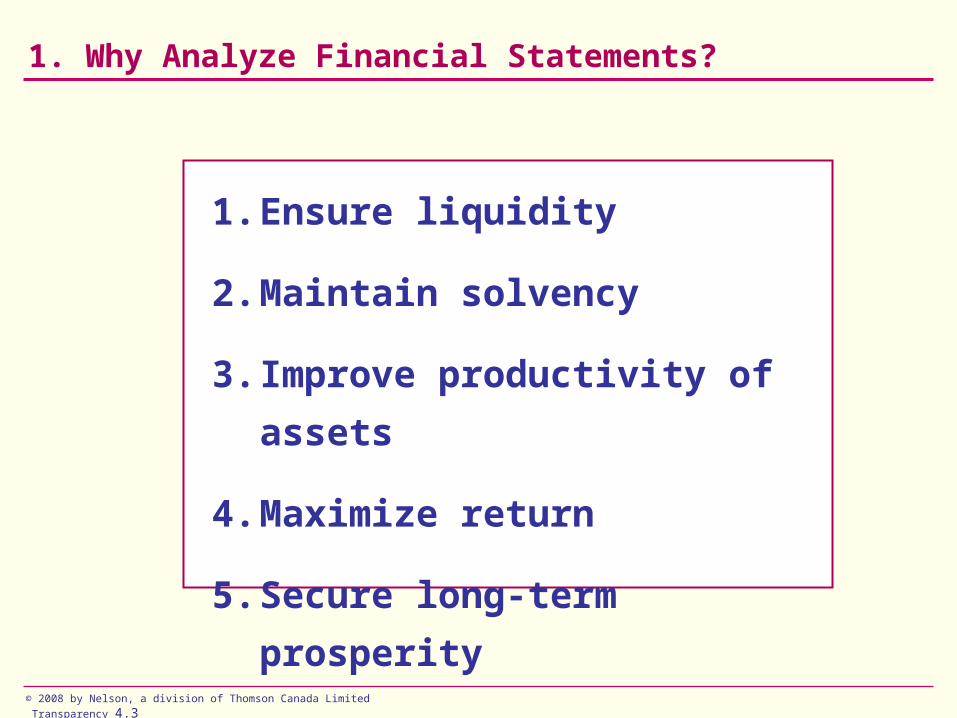

1. Why Analyze Financial Statements?

1. Ensure liquidity

2. Maintain solvency

3. Improve productivity of assets

4. Maximize return

5. Secure long-term prosperity

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.4

2. Modern Industries Ltd. – Vertical Analysis

Sales revenue

Cost of sales

Gross profit

Operating expenses

Salaries

Lease payments

Amortization

Other expenses

Total operating expenses

Income before taxes

Income taxes

Net income

$2,500,000

1,400,000

1,100,000

820,000

20,000

50,000

50,000

940,000

160,000

80,000

$ 80,000

2006 $ % of sales

100.0

56.0

44.0

32.8

0.8

2.0

2.0

37.6

6.4

3.2

3.2

100.0

58.0

42.0

33.2

0.8

1.3

2.1

37.4

4.6

2.3

2.3

2005 $ % of sales

$2,300,000

1,334,000

966,000

763,600

18,000

30,000

48,000

859,600

106,400

53,200

$ 53,200

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.5

Modern Industries Ltd. – Horizontal Analysis

Sales revenue

Cost of sales

Gross profit

Operating expenses

Salaries

Lease payments

Amortization

Other expenses

Total operating expenses

Income before taxes

Income taxes

Net income

$2,500,000

1,400,000

1,100,000

820,000

20,000

50,000

50,000

940,000

160,000

80,000

$ 80,000

$2,300,000

1,334,000

966,000

763,600

18,000

30,000

48,000

859,600

106,400

53,200

$ 53,200

2006 2005

$ 200,000

66,000

134,000

56,400

2,000

20,000

2,000

80,400

53,600

26,800

$ 26,800

Amount of change

8.69

4.95

13.87

7.38

11.10

66.67

4.17

9.35

50.37

50.37

50.37

% of change

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.6

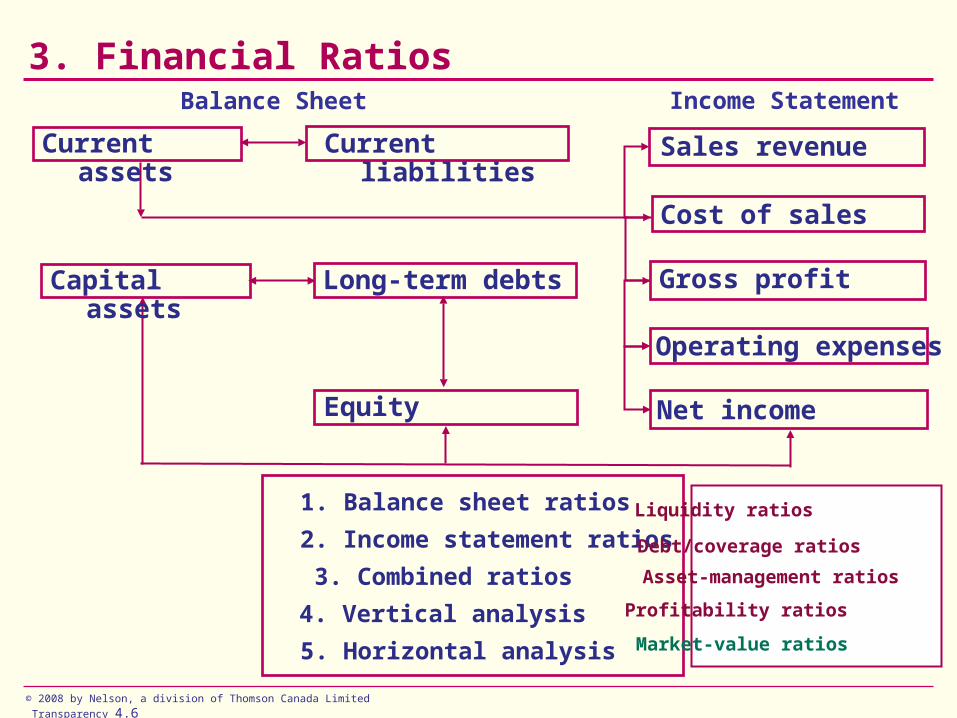

3. Financial Ratios

4. Vertical analysis

Sales revenue

Operating expenses

Cost of sales

Gross profit

Net income

Income Statement

2. Income statement ratios

3. Combined ratios

Current assets Current liabilities

Capital assets Long-term debts

Equity

Balance Sheet

1. Balance sheet ratios

5. Horizontal analysis

Liquidity ratios

Debt/coverage ratios

Asset-management ratios

Profitability ratios

Market-value ratios

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.7

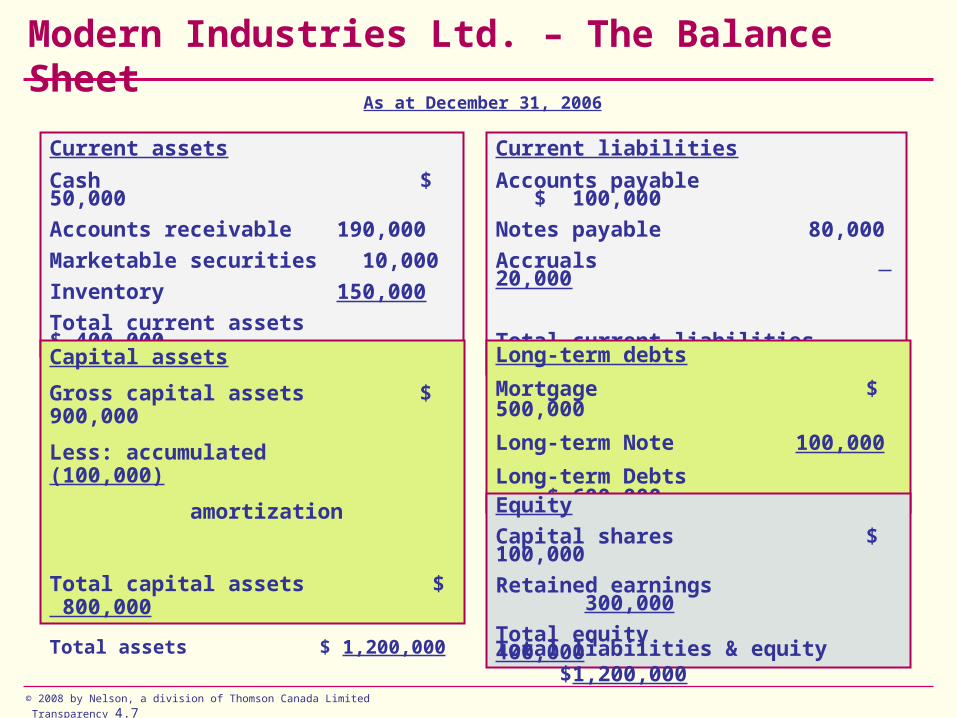

Modern Industries Ltd. – The Balance Sheet

Current assets

Cash $ 50,000

Accounts receivable 190,000

Marketable securities 10,000

Inventory 150,000

Total current assets $ 400,000

Current liabilities

Accounts payable $ 100,000

Notes payable 80,000

Accruals 20,000

Total current liabilities $ 200,000

Capital assets

Gross capital assets $ 900,000

Less: accumulated (100,000)

amortization

Total capital assets $ 800,000

Long-term debts

Mortgage $ 500,000

Long-term Note 100,000

Long-term Debts $ 600,000

Equity

Capital shares $ 100,000

Retained earnings 300,000

Total equity 400,000

Total assets $ 1,200,000 Total liabilities & equity $1,200,000

As at December 31, 2006

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.8

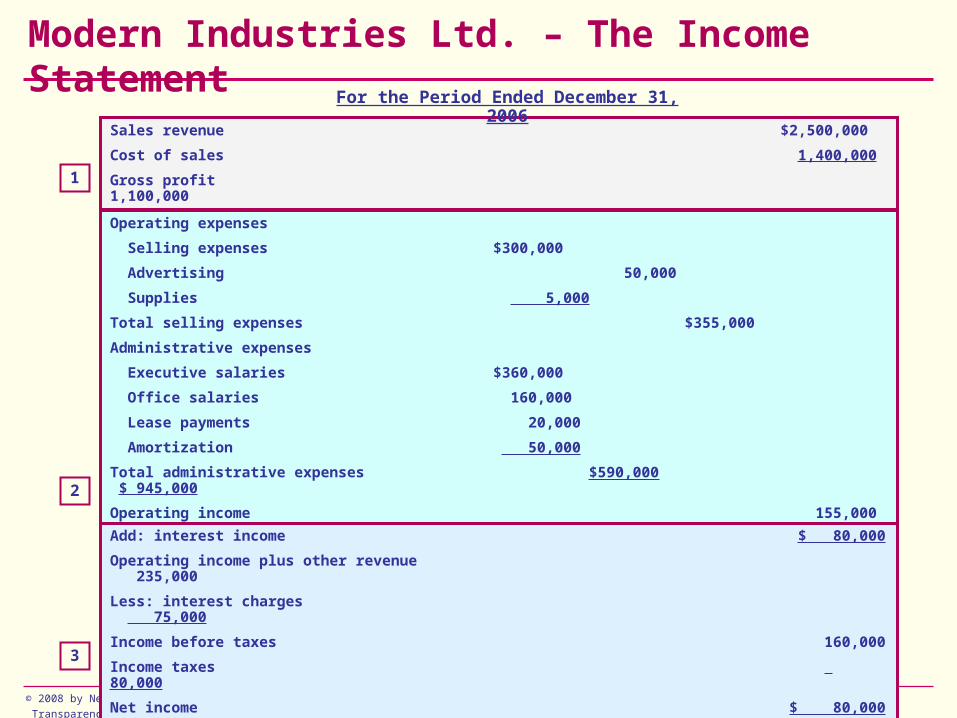

Modern Industries Ltd. – The Income Statement

Sales revenue $2,500,000

Cost of sales 1,400,000

Gross profit 1,100,0001

For the Period Ended December 31, 2006

2

Operating expenses

Selling expenses $300,000

Advertising 50,000

Supplies 5,000

Total selling expenses $355,000

Administrative expenses

Executive salaries $360,000

Office salaries 160,000

Lease payments 20,000

Amortization 50,000

Total administrative expenses $590,000 $ 945,000

Operating income 155,000

3

Add: interest income $ 80,000

Operating income plus other revenue 235,000

Less: interest charges 75,000

Income before taxes 160,000

Income taxes 80,000

Net income $ 80,000

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.9

Categories of Financial Ratios

ratios Indicate a company’s ability to meet its short-term obligations.

Liquidity

ratios Measure the extent to which a business can be financed by debt.

Debt/coverage

ratios Show how effectively management utilizes the assets of a business.

Asset-management

ratios Indicate the management’s overall effectiveness as measured by return on sales, on assets, on equity.

Profitability

• short-term lenders

• everybody

• employees

• Investors (shareholders & long-term lenders)

• managers

• suppliers

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.10

Commonly Used Financial Ratios

LIQUIDITY RATIOS

DEBT/COVERAGE RATIOS

ASSET/MANAGEMENT RATIOS

PROFITABILITY RATIOS

1. Current ratio (times)

2. Quick or acid test ratio (times)

3. Debt-to-total assets (percent)

4. Times-interest-earned (times)

5. Fixed-charges coverage (times)

6. Average collection period (days)

7. Inventory turnover (times)

8. Capital assets turnover (times)

9. Total assets turnover (times)

10. Profit margin on sales (percent)

11. Return on total assets (percent)

12. Return on equity (percent)

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.11

Ratio 1: Current Ratio

Purpose To give a general indication of the ability of a business (borrower) to meet its current obligations.

Current assets Current liabilities

Cash $ 50,000 Accounts payable $100,000

Accounts receivable 190,000 Notes payable 80,000

Marketable securities 10,000 Accruals 20,000

Inventory 150,000

Total current assets $400,000 Total current liabilities $200,000

Current assets

Current liabilities$400,000

$200,000= = 2.0 times

• collateral • growth • cushion

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.12

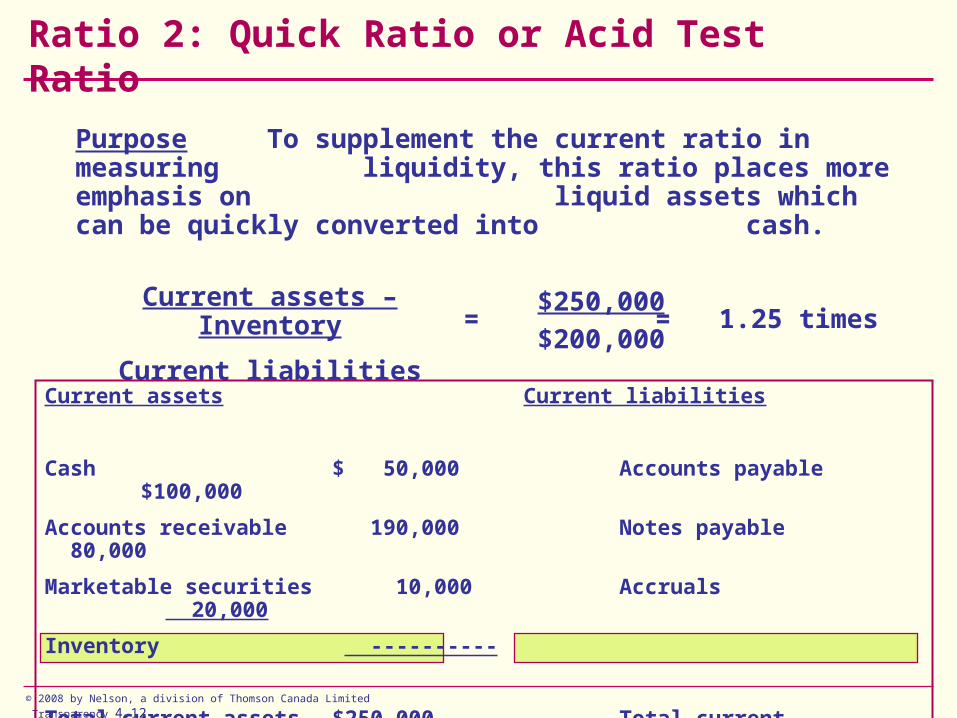

Ratio 2: Quick Ratio or Acid Test Ratio

Purpose To supplement the current ratio in measuring liquidity, this ratio places more emphasis on liquid assets which can be quickly converted into cash.

Current assets Current liabilities

Cash $ 50,000 Accounts payable $100,000

Accounts receivable 190,000 Notes payable 80,000

Marketable securities 10,000 Accruals 20,000

Inventory ----------

Total current assets $250,000 Total current liabilities $200,000

Current assets – Inventory

Current liabilities

$250,000

$200,000= = 1.25 times

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.13

Ratio 3: Debt-to-Total Assets

Purpose Measures the proportion of “all” debts provided by lenders to finance “all” assets.

It is also called debt ratio.

Total current assets $ 400,000 Total current liabilities $ 200,000

Total capital assets 800,000 Total long-term debts 600,000

Total debts 800,000

Equity 400,000

Total assets $ 1,200,000 Total liabilities & equity $ 1,200,000

Total debts

Total assets

$800,000

$1,200,000= = 67 percent

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.14

Applying for a Mortgage

A person in the 40% tax bracket applies for a mortgage

Payment Salary

$ 1,500$ 5,000

= = .30=$ 2,000$ 5,000 = .40

Payment Salary

Mortgage $ 1,500Income taxes $ 2,000Mortgage $ 2,000

Other $ 1,500

Total $ 5,000Other $ 1,000

Total $ 5,000

Income taxes $ 2,000

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.15

Ratio 4: Times-Interest-Earned

Purpose Shows the debt-paying ability of a business or its capacity to service the interest charges.

Sales revenue $ 2,500,000

Cost of sales 1,400,000

Gross profit 1,100,000

Operating expenses

Total selling expenses $ 355,000

Total admin. expenses 590,000 945,000

Operating income 155,000

Add: interest income 80,000

Less: interest charges 75,000 5,000

Income before taxes 160,000

Income taxes 80,000

Net income $ 80,000

Income before taxes + Interest charges

Interest charges$235,000

$75,000= = 3.1 times

•••••

Interest

Principal

Taxes

Dividends

Retained earnings

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.16

Ratio 5: Fixed-Charges-Coverage RatioPurpose Similar to the times-interest-earned ratio except

this ratio includes “all” fixed charges, or the capacity to service the interest charges and other fixed obligations.

Sales revenue $2,500,000Cost of sales 1,400,000Gross profit 1,100,000Operating expensesTotal selling expenses $355,000Total administrative expenses 590,000* 945,000Operating income 155,000Add: interest income 80,000Less: interest charges 75,000 5,000Income before taxes 160,000Income taxes 80,000Net income $ 80,000*Includes $20,000 lease payments

I.B.T. + Interest charges + Lease payments

Interest charges + Lease payments

$255,000

$95,000= = 2.7 times

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.17

Ratio 6: Average Collection Period

Purpose Measures the number of days it takes a business to collect payments after credit sales have been made.

Balance Sheet

Current assets

Accounts receivable $ 190,000

Total current assets $ 400,000

Sales revenue

365

$2,500,000

365= = = $6,849Step 1 Average sales per day

Step 2 Average collection periodAccounts receivable

Average sales per day

$190,000

$6,849= = = 27.7 days

Income Statement

Sales revenue $2,500,000

Cost of sales 1,400,000

Gross profit $ 1,100,000

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.18

Ratio 7: Inventory Turnover

Purpose Shows how long it takes for inventory to turn around or how fast it moves.

Balance Sheet

Current assets

Inventory $ 150,000

Total current assets $ 400,000

Income Statement

Sales revenue $2,500,000

Cost of sales 1,400,000

Gross profit $1,100,000

Cost of sales

Average inventory

$1,400,000

$150,000 = = 9.3 times

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.19

Ratio 8: Capital Assets TurnoverPurpose Measures how intensively a firm’s assets such as

land, buildings, and equipment are working.

Current assets $ 400,000

Net capital assets 800,000

Total assets $ 1,200,000

Sales revenue $ 2,500,000

Cost of sales 1,400,000

Gross profit 1,100,000

Total op. expenses 945,000

Operating income 155,000

Other income 5,000

Income before taxes 160,000

Income taxes 80,000

Net income $ 80,000

Sales revenue

Net capital assets

$2,500,000

$800,000= = 3.1 times

Income Statement Balance Sheet

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.20

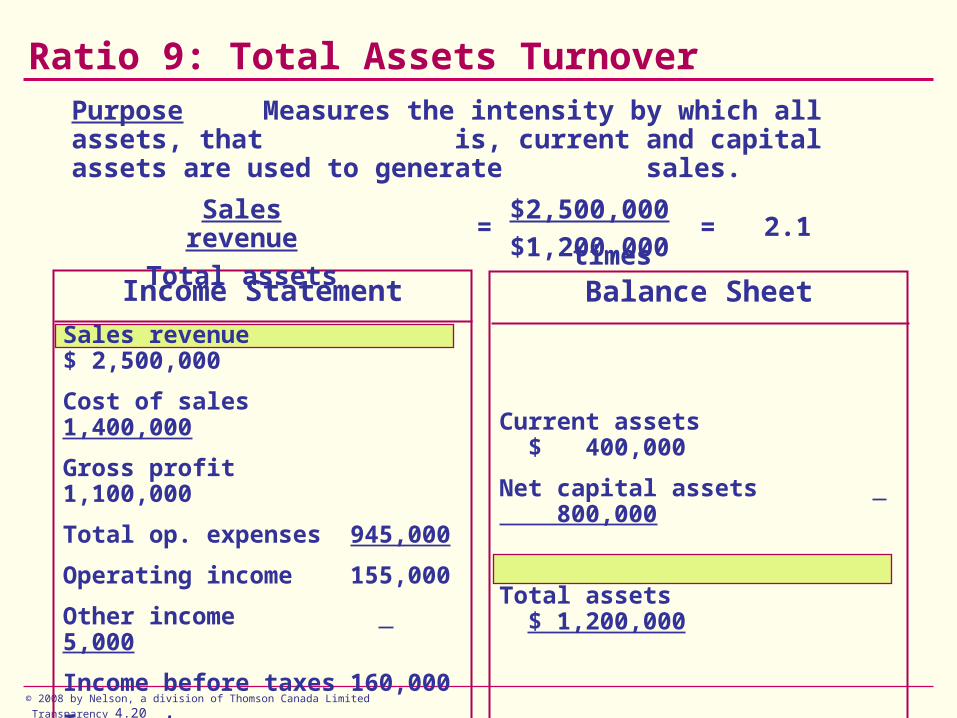

Ratio 9: Total Assets TurnoverPurpose Measures the intensity by which all assets, that

is, current and capital assets are used to generate sales.

Balance Sheet

Current assets $ 400,000

Net capital assets 800,000

Total assets $ 1,200,000

Income Statement

Sales revenue $ 2,500,000

Cost of sales 1,400,000

Gross profit 1,100,000

Total op. expenses 945,000

Operating income 155,000

Other income 5,000

Income before taxes 160,000

Income taxes 80,000

Net income $ 80,000

Sales revenue

Total assets

$2,500,000

$1,200,000 = = 2.1 times

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.21

Ratio 10: Profit Margin on Sales

Purpose Shows the efficiency of the business.

Sales revenue $ 2,500,000

Cost of sales 1,400,000

Gross profit 1,100,000

Operating expenses

Total selling expenses $355,000

Total admin. expenses 590,000 945,000

Operating income 155,000

Add: interest income 80,000

Less: interest charges 75,000 5,000

Income before taxes 160,000

Income taxes 80,000

Net income $ 80,000

Operating income

Sales revenue

$155,000

$2,500,000 = = 6.2 percent

Vertical analysis

100.0

44.0

6.2

3.2

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.22

Ratio 11: Return on Total Assets

Purpose Measures the return on funds invested in the business by both the owners and the lenders.

Balance Sheet

Current assets $ 400,000

Net capital assets 800,000

Total assets $ 1,200,000

Income Statement

Sales revenue $2,500,000

Cost of sales 1,400,000

Gross profit 1,100,000

Total op. expenses 945,000

Operating income 155,000

Other income 5,000

Income before taxes 160,000

Income taxes 80,000

Net income $ 80,000

Net income

Total assets

$ 80,000

$ 1,200,000 = = 6.7 percent

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.23

Ratio 12: Return on Equity

Purpose Shows how profitable a business is to its owners.

Balance Sheet

Current liabilities $ 200,000

Total long-term debts 600,000

Total debts 800,000

Equity 400,000

Total liabilities & equity $1,200,000

Income Statement

Sales revenue $2,500,000

Cost of sales 1,400,000

Gross profit 1,100,000

Total op. expenses 945,000

Operating income 155,000

Other income 5,000

Income before taxes 160,000

Income taxes 80,000

Net income $80,000

Net income

Owners’ equity

$80,000

$400,000 = = 20.0 percent

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.24

Supplementary Financial and Market Ratios

LIQUIDITY RATIOS

DEBT/COVERAGE RATIOS

ASSET/MANAGEMENT RATIOS

PROFITABILITY RATIOS

1. Cash ratio (times)

2. Working capital ratio (times)

3. Debt-to-equity (times)

4. Accounts receivable turnover (times)

5. Day’s sales to inventory (days)

6. Income after taxes to sales (percent)

7. Gross margin on sales (percent)

8. Return on invested capital (percent)

MARKET RATIOS

9. Earnings per share (dollars)

10. Cash flow per share (dollars)

11. Return per share (percent)

12. Price/earnings ratio (times)

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.25

4. External Financial Ratios

LIQUIDITY RATIOS

DEBT/ COVERAGE

RATIOS

ASSET/ MANAGEMENT

RATIOS

PROFITABILITY RATIOS

1. Current ratio (times)

2. Quick or acid test ratio (times)

3. Debt to total assets (percent)

4. Times-interest-earned (times)

5. Fixed-charges coverage (times)

6. Average Collection period (days)

7. Inventory turnover (times)

8. Capital Assets turnover (times)

9. Total Assets turnover (times)

10. Profit Margin on sales (percent)

11. Return on total assets (percent)

12. Return on equity (percent)

2.00

1.25

.67

3.10

2.70

27.70

9.30

3.10

2.10

6.20

6.70

20.00

Modern Industries Ltd.

1.50

1.00

.55

5.00

5.00

35.00

8.00

4.50

3.50

5.50

5.50

15.00

External ratios

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.26

5. Du Pont Financial System

Cash+

Accountsreceivable

+Prepaid

expenses +

Inventory

Cost of sales

+Amortization

+ Selling

expenses+

Administrativeexpenses

Currentassets

+Capitalassets

Sales-

Total cost of operation

Total assetsturnover

X

Return on total

assets

Sales÷

Total assets

÷

Sales

Operating margin

Operatingmargin

© 2008 by Nelson, a division of Thomson Canada Limited Transparency 4.27

6. Limitations of Financial Ratios

To make ratios meaningful, you should …

1. Look at trends

2. Compare your financial performance with other businesses or industry

The caveats of financial ratios

• They only give signals – they do not answer questions relating

to why, what, or how.

• When comparing ratios with other businesses, make sure that

the closing dates of the financial statements are the same.

• Make sure that the numbers used are similar.

• The size of the business may make a difference.

• The nature of the operations may also be different (new plant versus

worn-out plant).