© 2011 mcnees wallace & nurick llc key compliance issues for school districts march 17, 2011...

TRANSCRIPT

© 2011 McNees Wallace & Nurick LLC

Key Compliance Issues for School Districts

March 17, 2011

YEAR #2 OF HEALTHCARE REFORM:

Eric N. Athey Jennifer E. Will

Co-Chair, Labor & Employment Member

717.581.3708 717.237.5418

© 2011 McNees Wallace & Nurick LLC

PPACA AT A GLANCE

Patient Protection and Affordable Care Act Passed 3/23/10

Some Near-Term Highlights:• Unpaid breaks for nursing mothers (2010)• Dependent care extended to age 26 (2010-11)• Pre-existing condition exclusions phased out (2010-

14)• Lifetime & Annual Maximum Benefit Limits phased

out (2010-14)• FSA/HRA/HSAs: OTC reimbursements nixed (2011)• Extension of nondiscrimination rules to fully insured

plans (unknown)

2

© 2011 McNees Wallace & Nurick LLC

PPACA AT A GLANCE

PPACA Long-Term Requirements (2014)• Free Rider Penalty: Up to $2085 annual penalty

for families who don't have coverage• No Coverage Penalty for Employers: $2000/yr per

employee• Unaffordable Coverage Penalty for Employers:

$3000 per subsidized employee• Free Choice Vouchers• Cadillac Tax (2018)

Issue: How much of PPACA will survive the 2012 elections?

3

© 2011 McNees Wallace & Nurick LLC 4

PPACA COMPLIANCE AND YOUR CBA:WHERE TO BEGIN?

Determine whether your plan is grandfathered ("GF")

Determine cost/benefits of maintaining GF status

Determine timing & costs of PPACA mandates

© 2011 McNees Wallace & Nurick LLC 5

PPACA COMPLIANCE AND YOUR CBA:WHERE TO BEGIN?

Develop a bargaining strategy that ensures compliance without breaking the bank

(i.e. what does district get in exchange for new benefits)

Develop a bargaining strategy that complies with bargaining obligations

© 2011 McNees Wallace & Nurick LLC 6

GRANDFATHERING AND COLLECTIVE BARGAINING AGREEMENTS (CBAS)

General Rule: ALL collectively bargained plans must comply with PPACA requirements when they become effective BUT fully-insured CBA plans may retain grandfathered status longer than non-CBA plans

Fully Insured collectively bargained plans in effect before 3/23/10 remain grandfathered until expiration of CBA

Issue: Scope of "binding contract" exception?

© 2011 McNees Wallace & Nurick LLC 7

GRANDFATHERING AND COLLECTIVE BARGAINING AGREEMENTS (CBAS)

Once CBA expires, any post-3/23/10 changes to fully-insured collectively bargained plans will be analyzed under general GF rules

Change of carriers or of TPA during current term does not eliminate grandfathered status

Grandfathered status determined on a benefit package level rather than plan-wide

© 2011 McNees Wallace & Nurick LLC 8

APPLYING THE GRANDFATHERING RULES TO CBAS

Hypothetical 1: CBA (July 1, 2009-June 30, 2012) Employee Health Contributions Per

Month: 2009-10: $100

2010-11: $110

2011-12: $120 Still Grandfathered?

© 2011 McNees Wallace & Nurick LLC 9

APPLYING THE GRANDFATHERING RULES TO CBAS

Hypothetical 2: CBA (July 1, 2008-June 30, 2012) Employee Health Contributions Per

Month:2008-09: 7%

2009-10: 8%

2010-11: 9%

2011-12: 10% Still Grandfathered?

© 2011 McNees Wallace & Nurick LLC 10

APPLYING THE GRANDFATHERING RULES TO CBAS

Hypothetical 3: CBA (July 1, 2008-June 30, 2011) Employee Health Contributions Per

Month:2008-09: $100

2009-10: $100

2010-11: The % equivalent of $100 Still Grandfathered?

© 2011 McNees Wallace & Nurick LLC 11

APPLYING THE GRANDFATHERING RULES TO CBAS

Hypothetical 4: CBA (July 1, 2008-June 30, 2012) No changes in cost-sharing – but

indemnity plan option is eliminated in 2010-11

Still Grandfathered?

© 2011 McNees Wallace & Nurick LLC 12

APPLYING THE GRANDFATHERING RULES TO CBAS

Hypothetical 5: CBA (July 1, 2008-June 30, 2012) No changes in cost-sharing or

benefits – but plan moves from self-insured to fully insured in 2010-11

Still Grandfathered?

© 2011 McNees Wallace & Nurick LLC 13

APPLYING THE GRANDFATHERING RULES TO CBAS

Hypothetical 6: CBA (July 1, 2008-June 30, 2013) The following cost-sharing changes are

implemented during the CBA – which ones defeat GF status:

• 7/1/08: Exclude benefits for treatment of morbid obesity

• 7/1/09: Reduce "supplemental insurance" pool from $300 to $200 per year

© 2011 McNees Wallace & Nurick LLC 14

APPLYING THE GRANDFATHERING RULES TO CBAS

Hypothetical 6 (cont'd):• 7/1/10: Annual Deductible increased from

$200 to $400• 7/1/11: Office visit co-pay increase from $10 to

$20• 7/1/12: District decreases its contribution to

indemnity plan premium from 90% to 75%

© 2011 McNees Wallace & Nurick LLC 15

BARGAINING CONSIDERATIONS FOR PRE-2014 REQUIREMENTS

How important is GF status to your District?

Should you renegotiate (or delay) concessions to maintain GF status?

What is the cost of losing GF status relative to desired cost-sharing concessions?

© 2011 McNees Wallace & Nurick LLC 16

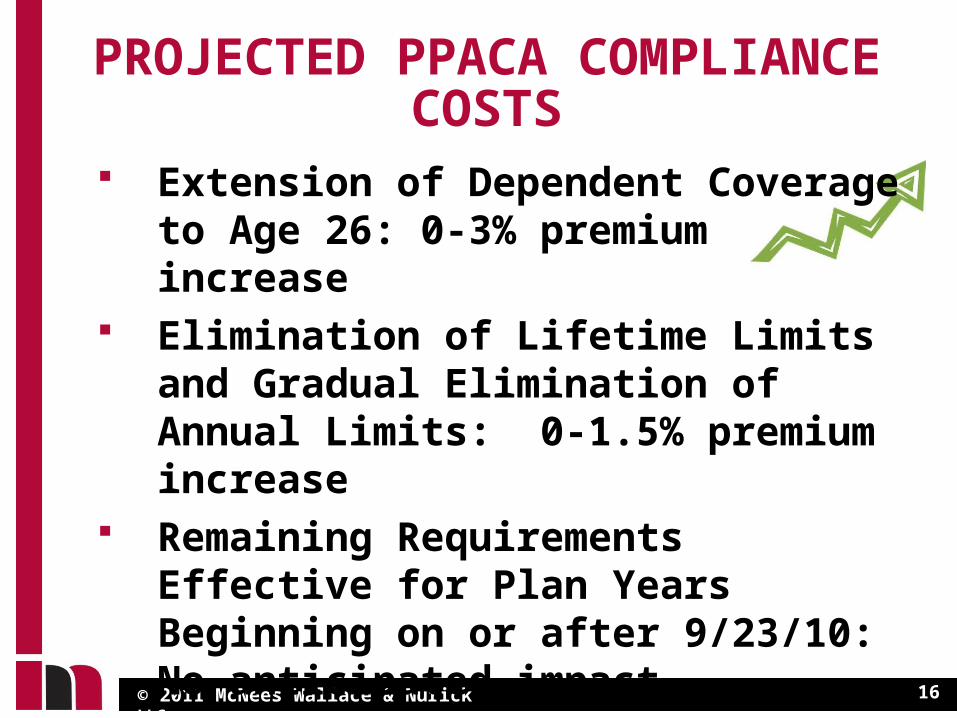

PROJECTED PPACA COMPLIANCE COSTS

Extension of Dependent Coverage to Age 26: 0-3% premium increase

Elimination of Lifetime Limits and Gradual Elimination of Annual Limits: 0-1.5% premium increase

Remaining Requirements Effective for Plan Years Beginning on or after 9/23/10: No anticipated impact

*Source: Aetna, "Impact of Health Care Reform in 2010

© 2011 McNees Wallace & Nurick LLC 17

NEGOTIATING THE RIGHT LANGUAGE

Minimize changes to CBA; Address Amendments in Plan Document/SPDs

Annual/Lifetime Limits – OK in CBA with proper context language

Can you charge more for older dependents – No.

© 2011 McNees Wallace & Nurick LLC 18

NEGOTIATING THE RIGHT LANGUAGE

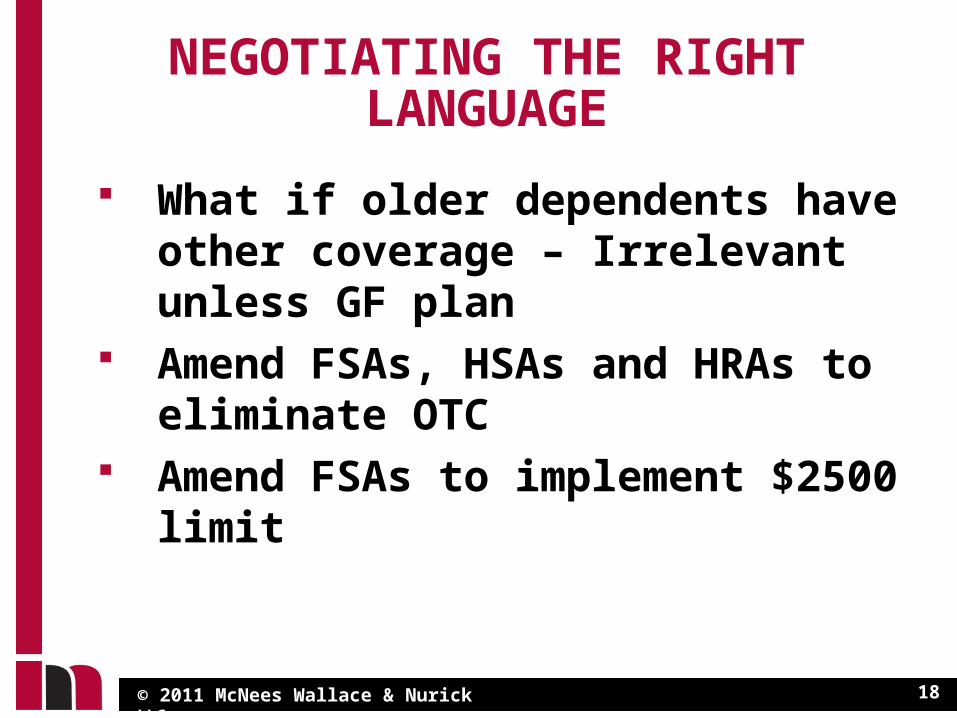

What if older dependents have other coverage – Irrelevant unless GF plan

Amend FSAs, HSAs and HRAs to eliminate OTC

Amend FSAs to implement $2500 limit

© 2011 McNees Wallace & Nurick LLC 19

NEGOTIATING THE RIGHT LANGUAGE

Preventive Health Services – Avoid listing in CBA

Appeals Procedure – Avoid listing in CBA

Reopener language as needed for compliance

© 2011 McNees Wallace & Nurick LLC 20

BARGAINING CONSIDERATIONS FOR 2014/2018 REQUIREMENTS

What are the 2014/2018 requirements?

Will the 2014/2018 requirements be repealed?

How will they impact school districts?

What are the key bargaining considerations?

© 2011 McNees Wallace & Nurick LLC 21

WHAT ARE THE 2014/2018 REQUIREMENTS?

Free rider penalty for employees No coverage penalty: $2,000 x [# of

FTEs – 30] Unaffordable coverage penalty:

$3,000 x # of subsidized FTEs [if employee cost of coverage exceeds 9.8% of gross household income]

© 2011 McNees Wallace & Nurick LLC 22

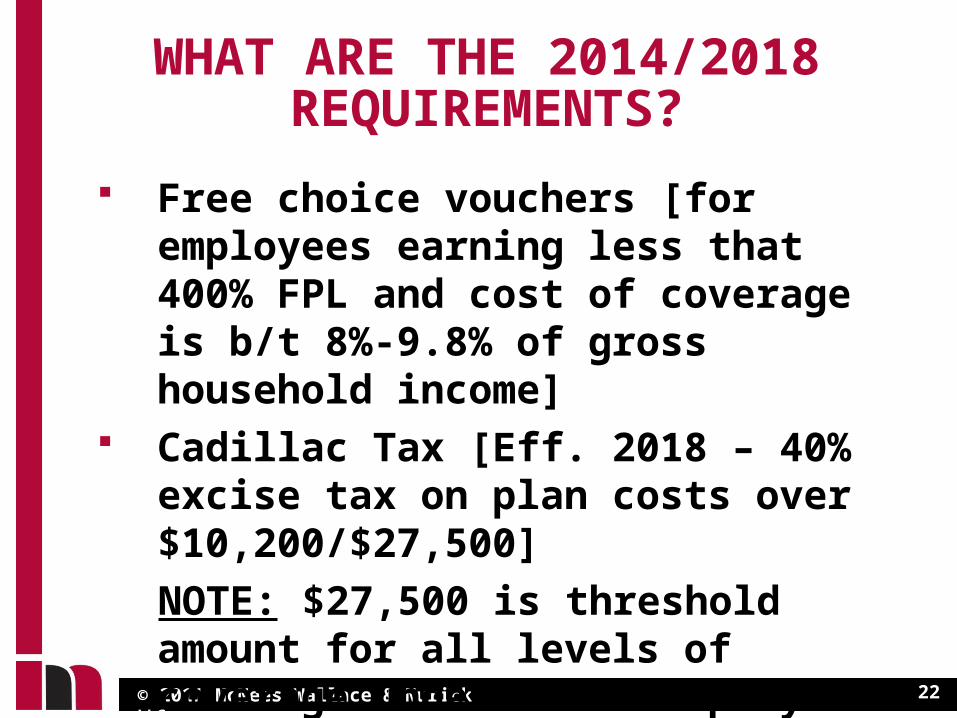

WHAT ARE THE 2014/2018 REQUIREMENTS?

Free choice vouchers [for employees earning less that 400% FPL and cost of coverage is b/t 8%-9.8% of gross household income]

Cadillac Tax [Eff. 2018 – 40% excise tax on plan costs over $10,200/$27,500]

NOTE: $27,500 is threshold amount for all levels of coverage under multi-employer plan

© 2011 McNees Wallace & Nurick LLC 23

WILL THE 2014/2018 REQUIREMENTS BE REPEALED?

20 State Attorney Generals sue to block 2014 Provisions

6 States pass laws purporting to reject 2014 Provisions

Republicans now control House Who will act first, Congress or the

Supreme Court? In the meantime, we must address the

2011 requirements

© 2011 McNees Wallace & Nurick LLC 24

GENERAL BARGAINING STRATEGIES FOR THE UNKNOWN

Short-term CBAs expiring pre-2014 Long-term CBAs with salary/benefit

reopeners pre-2014 "Me too" provisions to match

administrative or support staff (with a floor)

Negotiate waiver of duty to bargain as necessary to comply and/or avoid penalties

© 2011 McNees Wallace & Nurick LLC 25

SPECIFIC 2014/2018 STRATEGIES

Free Rider Penalties Strategy: Negotiate provision

prohibiting waiver of coverage or allowing waiver only with proof of other coverage

No Coverage Penalty Strategy: Compare current coverage to

plans on Exchange Consider sharing of savings if

elimination of coverage is feasible

© 2011 McNees Wallace & Nurick LLC 26

SPECIFIC 2014/2018 STRATEGIES

Unaffordable Coverage Penalty Strategy: Knowing gross household

income (GHI) will be key to avoidance

Implement GHI reporting requirement Mutually explore benefit of

eliminating coverage Tighten up opt-out payments

© 2011 McNees Wallace & Nurick LLC 27

SPECIFIC 2014/2018 STRATEGIES

Free Choice Vouchers Strategy: Control cost-sharing to stay

below 8% of GHI Monitor cost/benefits of exchange

plans Consider negotiating elimination of

coverage Trigger elimination of coverage on

threshold number of employees seeking vouchers?

© 2011 McNees Wallace & Nurick LLC 28

SPECIFIC 2014/2018 STRATEGIES

Cadillac Tax (eff. 2018) Reopener provision to avoid imposition of

tax Elimination of benefits triggered by

imposition of tax Unilateral reduction of benefits provision

to avoid imposition of tax Greater employee contributions triggered

by imposition of tax Union/Employee indemnification if tax

imposed

© 2011 McNees Wallace & Nurick LLC 29

WILL THE CADILLAC TAX BE DRIVING YOUR DISTRICT IN 2018?

2010 Avg. District Pseudo Rate*: • Employee Only: $6996/yr or 68.5 of

$10,200• Family: $16,344/yr or 60% of $27,500• Avg. % Premium Increase for Districts

since 2006: 10.65% Where will the avg. pseudo rate be in

2018?*Source: Lancaster County School District Data

© 2011 McNees Wallace & Nurick LLC 30

ANTICIPATED AVERAGE PSEUDO-RATE FOR 2018:

Assuming 10.65% increase per year• Employee Only: $15,719

Excess of $5,519/yr subject to 40% tax (or $2,207 tax per employee per year)

• Family: $36,726Excess of $9,226/yr subject to 40% tax (or $3,690 tax per employee per year)

© 2011 McNees Wallace & Nurick LLC

QUESTIONS

Visit our blog at:

http://www.palaborandemploymentblog.com/

31