© 2013 pam wilde interim presentation: developing the b2b offering 1 1. introduction & agenda...

TRANSCRIPT

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering1

1. Introduction & Agenda

• Situational analysis Competitor analysis Products Pricing and revenue analysis Distribution including customer acquisition and international Process Market sector analysis Customer needs analysis

Headline recommendations Areas to explore

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering2

2. Definition

• What is “B2B”?“Generating revenue and building reputation from activities in areas other than the

direct education of students”

• Collateral benefits Supports strategic priorities – research engaged, business focussed Greater industry & business relevance of University offering and research Enhanced student / faculty opportunities and experience Community and stakeholder benefits Enhanced reputation with students, academics and businesses/organisations

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering3

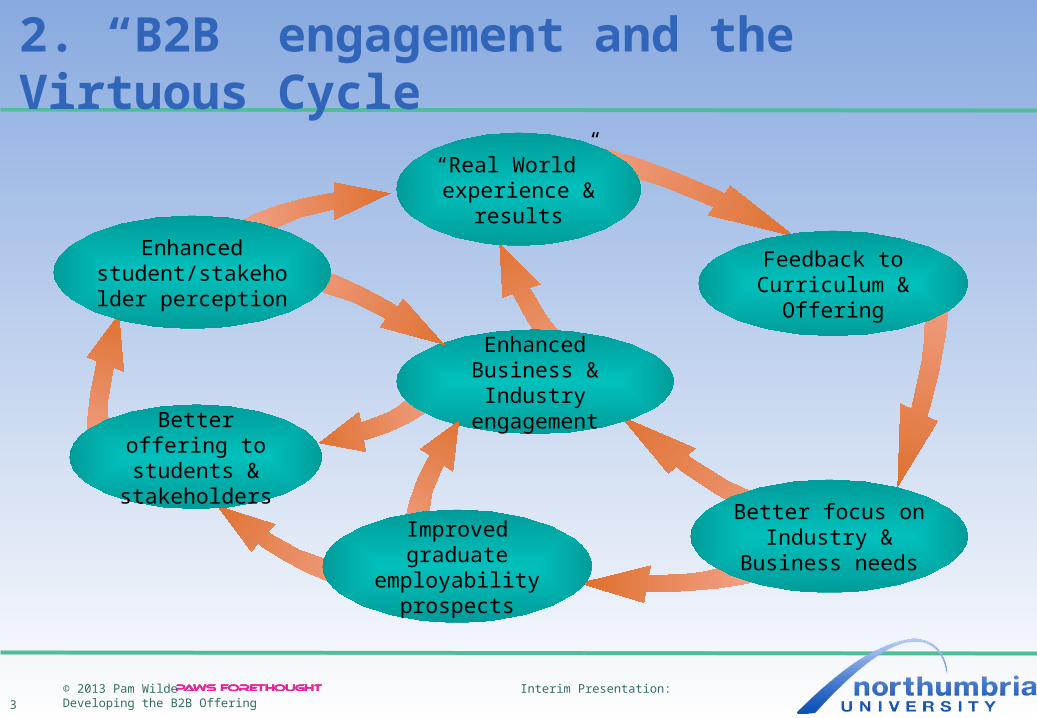

2. “B2B” engagement and the Virtuous Cycle

Enhanced Business & Industry engagement

Feedback to Curriculum & Offering

Better focus on Industry & Business

needsImproved graduate

employability prospects

Enhanced student/stakeholder

perception

Better offering to students &

stakeholders

“Real World” experience &

results

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering4

3. Situational Analysis: Competitive Set

Blue-chipcredibility

SMEcredibilty

Public & 3rd SectorCredibility

InternationalCredibility

Effective InterfaceAccess & Navigation

Awareness / Saliency

Value

Track-record& Reputation

Partnership /CollaborationCapacity

Proactive

Nimble

PracticalImplementation

Objectivethinking

Innovative/Bleeding edge

Multi-Disciplinary

People experience & expertise

High-endConsultancy

In-houseR&D

Industry SpecialistGroups

NorthumbriaUniversity

• Perceptions of Strengths & Weaknesses

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering5

3. Situational Analysis: Competitive Set• Perceptions of Strengths & Weaknesses

Blue-chipcredibility

SMEcredibilty

Public & 3rd SectorCredibility

InternationalCredibility

Effective InterfaceAccess & Navigation

Awareness / Saliency

Value

Track-record& Reputation

Partnership /CollaborationCapacity

Proactive

Nimble

PracticalImplementation

Objectivethinking

Innovative/Bleeding edge

Multi-Disciplinary

People experience & expertise

High-endConsultancy

NorthumbriaUniversity

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering6

3. Situational Analysis: Competitive Set• Perceptions of Strengths & Weaknesses

Blue-chipcredibility

SMEcredibilty

Public & 3rd SectorCredibility

InternationalCredibility

Effective InterfaceAccess &

Navigation

Awareness / Saliency

Value

Track-record& Reputation

Partnership /Collaboration

Capacity

Proactive

Nimble

PracticalImplementation

Objectivethinking

Innovative/Bleeding edge

Multi-Disciplinary

People experience & expertise

In-houseR&D

NorthumbriaUniversity

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering7

3. Situational Analysis: Competitive Set• Perceptions of Strengths & Weaknesses

CambridgeOxford

Imperial College London

LSE

Durham

University College LondonWarwick

Bath

BristolYork

Southampton

Exeter

King's College LondonNotti ngham

SOASLoughborough

Glasgow

Birmingham

Leicester

Newcastle

Aston

East Anglia

Surrey

Manchester

Liverpool Queen's, Belfast

Royal Holloway

Kent

Reading

Queen MaryCardiff

Essex

Heriot-WattStrathclyde

City

Dundee

KeeleStirling

Aberdeen

Oxford Brookes

Hertfordshire

Aberystwyth

Brunel

Robert Gordon

Ulster

Plymouth

Swansea

Chichester

Goldsmiths College

Huddersfield

University of the Arts, London

West of England, Bristol

Bournemouth

Hull

Sheffield Hallam

Central Lancashire

Birmingham City

Lincoln

Brighton

Winchester Middlesex

Coventry

Bradford

Roehampton

Gloucestershire

Glasgow Caledonian

Westminster

Bangor

University for the Creative Arts

Chester

De Montfort

Portsmouth

Glamorgan

Edinburgh Napier

Bath Spa

Cumbria

Queen Margaret

Kingston

University of Wales, Newport

Teesside

Sunderland

Trinity Saint David

Manchester Metropolitan

West London

Abertay Dundee

Leeds Metropolitan

Salford

Edge Hill

Staffordshire

Canterbury Christ Church

Liverpool John Moores

York St John

Bedfordshire

GlyndwrNorthampton

Worcester

Buckinghamshire New

Derby

Greenwich

Anglia Ruskin

Southampton Solent

West of Scotland

East London

Bolton

London Metropolitan

London South Bank

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

2.80

3.00

40 45 50 55 60 65 70 75 80 85 90

Rese

arch

Ass

essm

ent

(CU

G 2

013)

Graduate Prospects (CUG 2013)

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering8

History, History of Art

Art & Design

Comm & Media Studies

Dance, Drama, Cinematics

English

“Modern Languages”

Linguistics

Politics

Social Policy

Sociology

Accounting & Finance

Business Studies

Economics

Hospitality, Tourism etc

Law

Planning, Land, Property etc

Architecture

Building

Computer Science

Engineering Subjects

Geography & Environment

Information Management

Mathematics

Social Policy

Biological & Food Sciences

Chemistry

Education

Nursing & Allied Medical

Psychology

Social Work

Sports Science

1Q

2Q

3Q

4Q

CUG Overall, Research and Graduate Prospects Rank 2013Art, Design & Social

SciencesBusiness & Law Engineering &

EnvironmentHeath &

Life Sciences

3. Situational Analysis: Competitive Set

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering9

3. Situational Analysis: Products• Product set broadly in-line with HE offerings

Selected opportunities for product development• Strengths & track-record in selected disciplines

Reliance on these few specialisations = future risk• Historically faculty driven

Need integrated & multidisciplinary product approach • Core competencies restricted to specific disciplines

e.g. Student Law Clinic model – expand into other areas Not used capabilities to expand/build reputation in new sectors/disciplines

• CPD and employee training highly rated, research strength variable• Variable customer experience – dependent on individuals• Course delivery options could be more flexible• No obvious prioritisation – capacity and focus issues

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering10

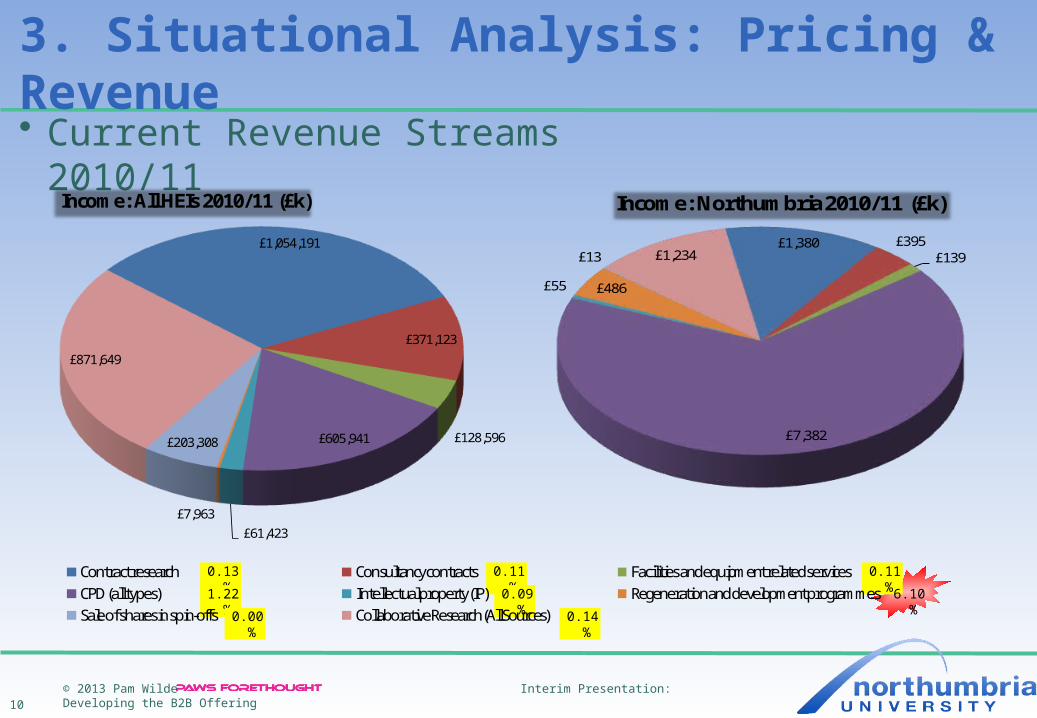

£1,380 £395 £139

£7,382

£55 £486

£13 £1,234

Income: Northumbria 2010/11 (£k)

3. Situational Analysis: Pricing & Revenue• Current Revenue Streams 2010/11

£1,054,191

£371,123

£128,596 £605,941

£61,423 £7,963

£203,308

£871,649

Income: All HEIs 2010/11 (£k)

Contract research Consultancy contracts Facilities and equipment related servicesCPD (all types) Intellectual property (IP) Regeneration and development programmesSale of shares in spin-offs Collaborative Research (All Sources)

0.13% 0.11% 0.11%

1.22% 0.09% 6.10%

0.00% 0.14%

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering11

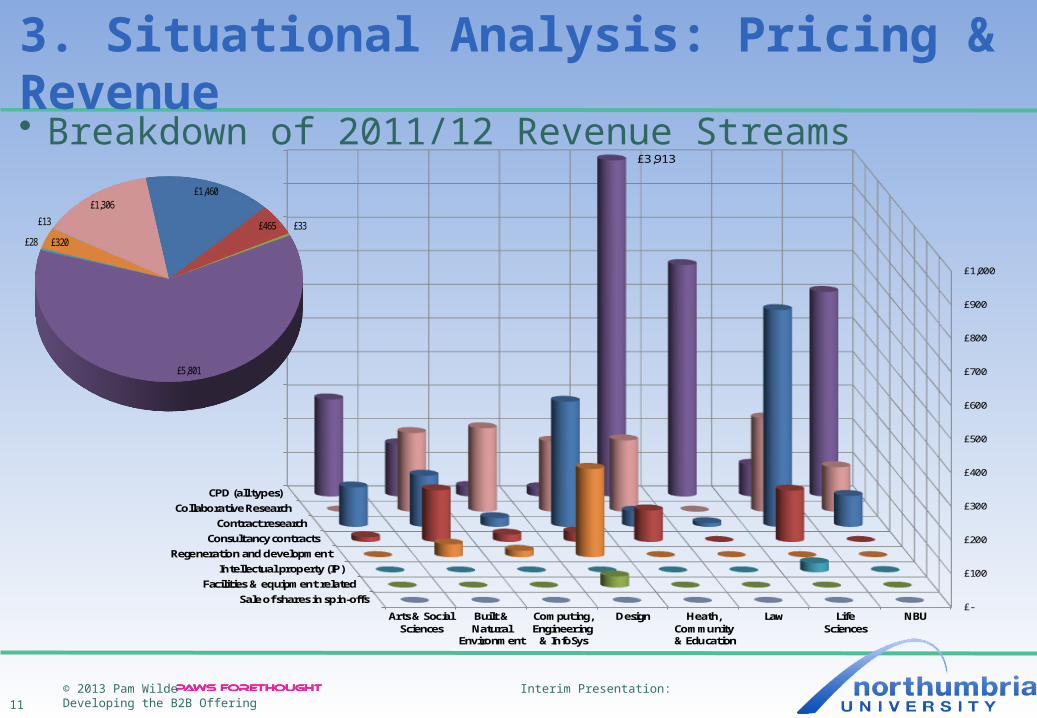

3. Situational Analysis: Pricing & Revenue• Breakdown of 2011/12 Revenue Streams

Sale of shares in spin-offsFacilities & equipment related

Intellectual property (IP)Regeneration and development

Consultancy contractsContract research

Collaborative ResearchCPD (all types)

£-

£100

£200

£300

£400

£500

£600

£700

£800

£900

£1,000

Arts & SocialSciences

Built &Natural

Environment

Computing,Engineering & InfoSys

Design Heath,Community

& Education

Law LifeSciences

NBU

£3,913

£1,460

£465 £33

£5,801

£28 £320

£13

£1,306

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering12

3. Situational Analysis: Pricing & Revenues• Pricing internally focussed and faculty based

cost plus, lack of transparency/consistency Lack of clarity around margins – overall and by discipline/market

• Strengths & track-record in selected disciplines But ... insensitive to market trends and opportunities

• Limited understanding around different revenue stream profitability e.g. research margin % and value versus consultancy

• Disproportionate income from CPD Not a bad thing per se, but a source of risk

• Benchmarking data not readily/easily available Barrier to understanding and creating external/competitor focus

• Use to inform where resources best deployed

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering13

3. Situational Analysis: Revenues• Surprisingly low contribution from SMEs• Consultancy largest revenue generator for SMEs (£56m). Contract research contributes

£40m, as does equipment/facilities. • SME income increasing – indicates increasing appetite and engagement to innovate SME

products and services.Figure 1 Total income by partner 2003-04 to 2010-11 (real terms)

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering14

3. Situational Analysis: Revenues• Contract research represents largest opportunity, with largest demand from public and

third sector• Consultancy services offer similar market opportunity to CPD• As pressure mounts on public sector spending, large business spending next attractive

opportunityFigure 2 Selected HE-BCI income streams 2003-04 to 2010-11 (real terms) Figure 3 Income by activity and partner 2010-11

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering15

3. Situational Analysis: Revenues• Consultancy & Contract Research income

Collaborative research presents potential opportunity due to nebulous nature – plays to partnership strengths and project specific expertise.

But ... often multi-disciplinary Non-commercial and SMEs increasing spending on contract research

Figure 6 Contract research income 2003-04 to 2010-11 (real terms)Figure 7 Consultancy income 2003-04 to 2010-11 (real terms)

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering16

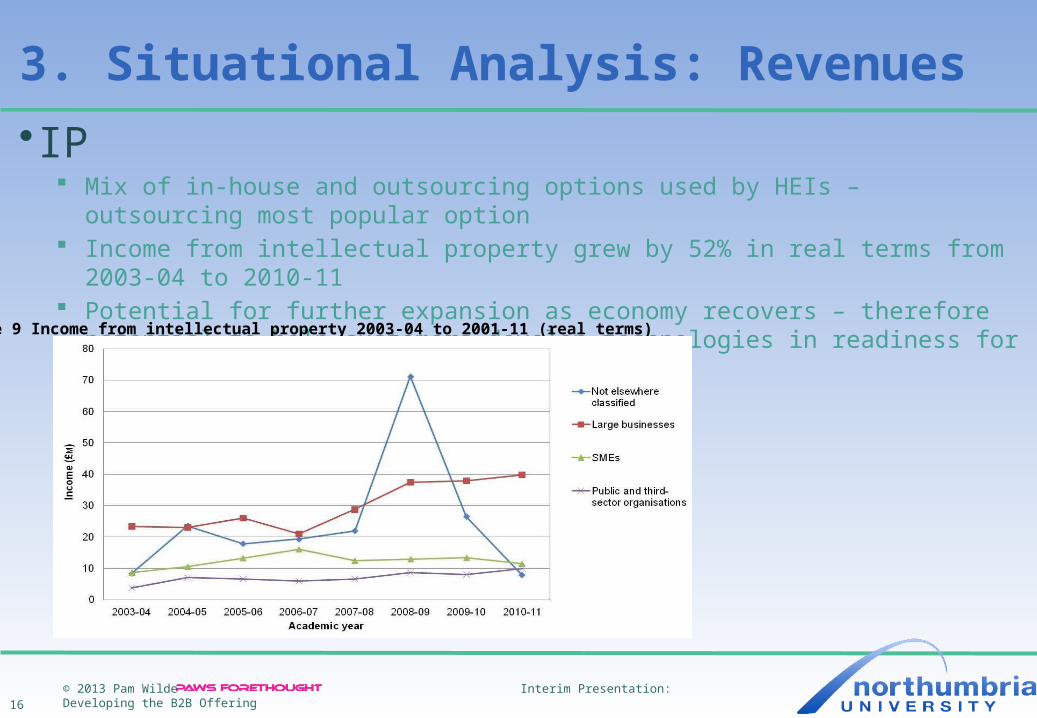

3. Situational Analysis: Revenues• IP

Mix of in-house and outsourcing options used by HEIs – outsourcing most popular option Income from intellectual property grew by 52% in real terms from 2003-04 to 2010-11 Potential for further expansion as economy recovers – therefore potential to help customers

develop technologies in readiness for upturn

Figure 9 Income from intellectual property 2003-04 to 2001-11 (real terms)

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering17

3. Situational Analysis: Revenues• CPD

Figure 14 CPD and continuing education 2010-11 High proportion of CPD from

public sector plays to Northumbria University's strengths

But...potential risk through over-reliance

Opportunity to take CPD/training/personal skills training competencies into new disciplines and areas

Need to articulate clearly the generic capabilities and target audience benefits

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering18

3. Situational Analysis: Revenues• Facilities & EquipmentFigure 8 Facilities and equipment 2003-04 to 2010-11 (real terms)

• Northumbria University's facilities stand up well against other HE offerings

• Large businesses increased their spending • Opportunity to leverage to build business

relationships as well as generate income – focussing on combination of facilities with leading edge expertise – not each in isolation

• Need to understand if any facilities are unique in what they offer

• Opportunity to invite businesses to experience and also offer virtual tours to potential students

• Market focus more on technology e.g. digital media suites, wind tunnels

• Vocational facilities e.g. sports centres could be used to support wider offering e.g. sports psychology

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering19

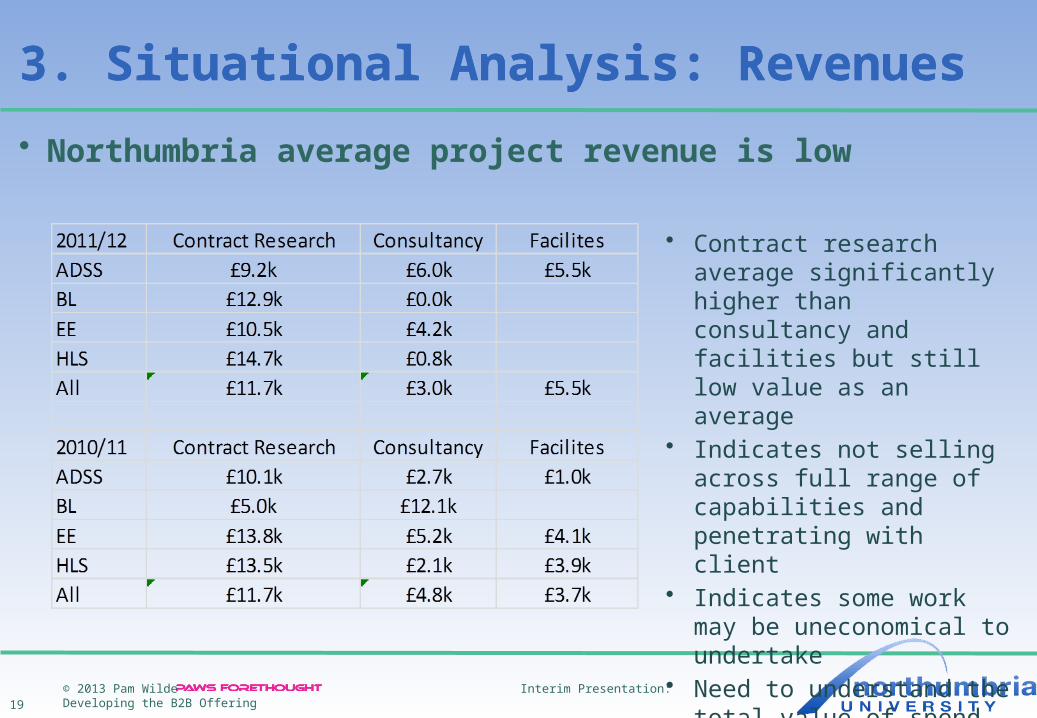

3. Situational Analysis: Revenues

• Northumbria average project revenue is low

3. Situational Analysis: Revenues

• Contract research average significantly higher than consultancy and facilities but still low value as an average

• Indicates not selling across full range of capabilities and penetrating with client

• Indicates some work may be uneconomical to undertake

• Need to understand the total value of spend over a period to see if small pieces of work are successfully converted into larger projects

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering20

3. Situational Analysis: Process• Customer Acquisition

Unclear Process – does not support full capabilities Competing priorities and issues with capacity to deliver Not easy to navigate around the University and find the right person Industry feedback indicates identifying and engaging with academics is

a major barrier for external clients (in particular SMEs) Demonstrated ability to focus on the process of design & methodology Not maximised this capability or communicated competency CRM system & process being introduced – crucial to successful

acquisition strategy – behavioural change required Must provide information to support proactive BDM lead generation

• e.g. finding target companies/companies similar to university successes,• e.g. holding information on existing customers including contact details & routes to access• e.g. won/lost reporting and analysis of opportunities• Performance metrics support behaviours and focus

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering21

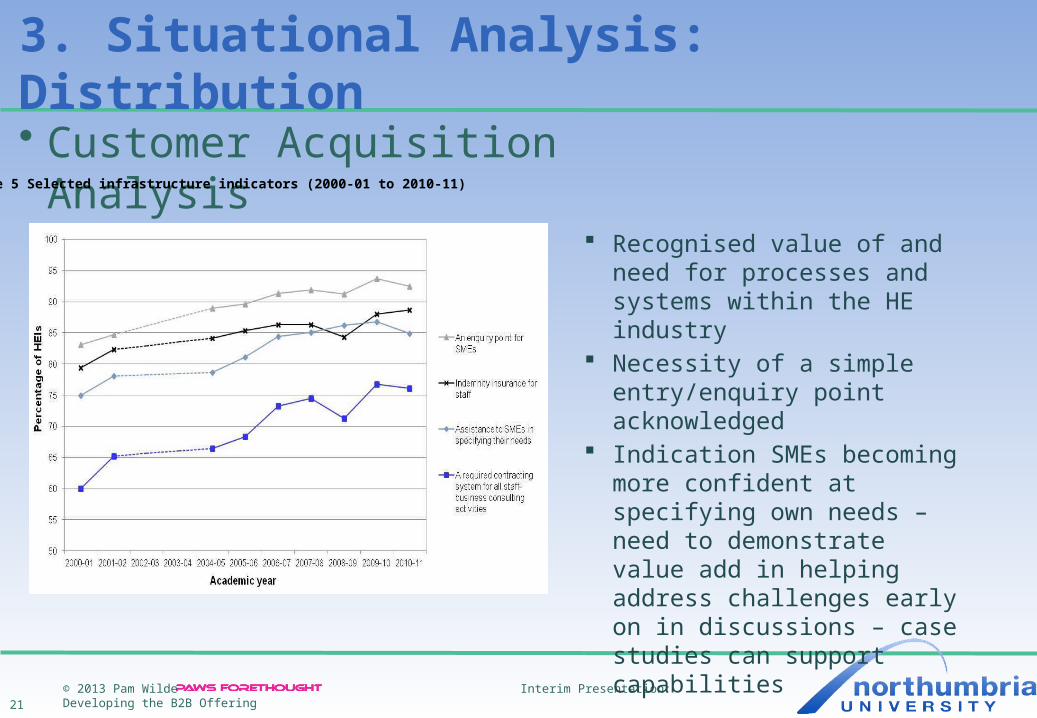

3. Situational Analysis: Distribution• Customer Acquisition Analysis

Figure 5 Selected infrastructure indicators (2000-01 to 2010-11)

Recognised value of and need for processes and systems within the HE industry

Necessity of a simple entry/enquiry point acknowledged

Indication SMEs becoming more confident at specifying own needs – need to demonstrate value add in helping address challenges early on in discussions – case studies can support capabilities

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering22

3. Situational Analysis: Distribution• Customer Acquisition Analysis

Figure 4 Incentives for staff to engage with business and the community 2000-01 to 2010-11

In response to the question ‘How would you rate the level of incentives for staff at your HEI to engage with Business and the Community?’

HE staff recognise the importance of engaging with businesses – the challenge is to provide the processes and develop the capability to optimise the opportunity

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering23

3. Situational Analysis: Distribution

• International development - 1 Handled through international office independently of BDMs International office focus is on student recruitment Most of business is from Middle East – have the money to invest

• Risk of over-reliance on this Region• Monitor and seek out opportunities globally

International sales model: individual reps covering specific countries talk to sponsors to communicate Uni benefits

• need resources and capabilities to offer full range and demonstrate wide range of experience• Indications not promoting/focussing on all opportunities/disciplines e.g. not strong in oil and

gas – growing market opportunity and synergies with Middle East

Success measures not clearly defined or co-ordinated with BDMs

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering24

3. Situational Analysis: Distribution• International – 2

Businesses think in terms of product and capability Reputation important for overseas – based on what delivered and

longevity/heritage Basic Marketing support not supplied: for example

• brand messages e.g. quality, environment• specific sector/discipline competency examples• digital and soft copy communications• translated versions

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering25

3. Situational Analysis: Best Practice

• NDC – Design Centre Good reputation. Innovative. Good at problem identification and issue

definition. Cross-disciplinary – bring together and lead cross-functional teams.

Focuses on the process of design and methodology rather than individual products

Demonstrated ability to work successfully with large companies e.g. Unilever, Mars; as well as SMEs

Designers good at e.g. blogs – use to promote university and engage with wider business community

Opportunity to use core competencies of NDC and also share best practices

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering26

3. Situational Analysis: Best Practice Examples

• Coventry University Business engagement focus

• Newcastle University• MIT – ILP (Industry Liaison Programme)

membership model

• Cranfield communication of industry/student benefits

• Lancaster multi-disciplinary branded “Imagination”

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering27

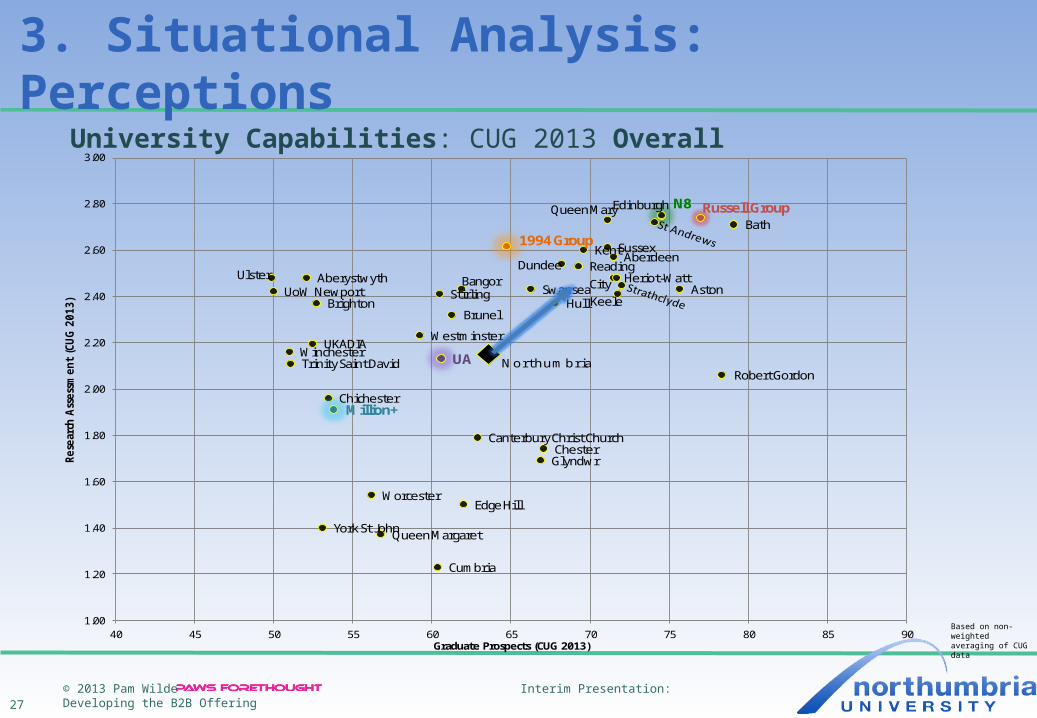

3. Situational Analysis: Perceptions

Edinburgh N8 Russell GroupQueen MaryBath

1994 Group SussexKent AberdeenDundee Reading

Ulster Aberystwyth Heriot-WattCityBangorSwansea AstonUoW Newport Stirling

KeeleBrighton HullBrunel

WestminsterUKADIA

WinchesterNorthumbriaUATrinity Saint David

Robert Gordon

ChichesterMillion+

Canterbury Christ ChurchChesterGlyndwr

WorcesterEdge Hill

York St JohnQueen Margaret

Cumbria

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

2.80

3.00

40 45 50 55 60 65 70 75 80 85 90

Rese

arch

Ass

essm

en

t (C

UG

201

3)

Graduate Prospects (CUG 2013)

University Capabilities: CUG 2013 Overall

Based on non-weighted averaging of CUG data

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering28

3. Situational Analysis: Perceptions

CambridgeOxford

Imperial College London

LSE

Durham

University College LondonWarwick

Bath

BristolYork

Southampton

Exeter

King's College LondonNotti ngham

SOASLoughborough

Glasgow

Birmingham

Leicester

Newcastle

Aston

East Anglia

Surrey

Manchester

Liverpool Queen's, Belfast

Royal Holloway

Kent

Reading

Queen MaryCardiff

Essex

Heriot-WattStrathclyde

City

Dundee

KeeleStirling

Aberdeen

Oxford Brookes

Hertfordshire

Aberystwyth

Brunel

Robert Gordon

Ulster

Plymouth

Swansea

Chichester

Goldsmiths College

Huddersfield

University of the Arts, London

West of England, Bristol

Bournemouth

Hull

Sheffield Hallam

Central Lancashire

Birmingham City

Lincoln

Brighton

Winchester Middlesex

Coventry

Bradford

Roehampton

Gloucestershire

Glasgow Caledonian

Westminster

Bangor

University for the Creative Arts

Chester

De Montfort

Portsmouth

Glamorgan

Edinburgh Napier

Bath Spa

Cumbria

Queen Margaret

Kingston

University of Wales, Newport

Teesside

Sunderland

Trinity Saint David

Manchester Metropolitan

West London

Abertay Dundee

Leeds Metropolitan

Salford

Edge Hill

Staffordshire

Canterbury Christ Church

Liverpool John Moores

York St John

Bedfordshire

GlyndwrNorthampton

Worcester

Buckinghamshire New

Derby

Greenwich

Anglia Ruskin

Southampton Solent

West of Scotland

East London

Bolton

London Metropolitan

London South Bank

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

2.80

3.00

40 45 50 55 60 65 70 75 80 85 90

Re

sear

ch A

sse

ssm

en

t (

CU

G 2

01

3)

Graduate Prospects (CUG 2013)

University Capabilities: CUG 2013 Overall

Based on non-weighted averaging of CUG data

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering29

3. Situational Analysis: PerceptionsUniversity Capabilities – Art, Design & Social Sciences Subjects: CUG 2012

Based on non-weighted averaging of CUG data

Aberdeen

Aberystwyth

Arts University College at Bournemouth

Aston

Bangor

BathBrighton

Brunel

Canterbury Christ Church

CS of Speech and Drama

Chester

Chichester

City

Courtauld Institute

Cumbria

Dundee

Edge Hill

Edinburgh

Falmouth

Glyndwr

Heriot-Watt

Hull

Kent

Leeds TrinityMillion+

N8

Newman

Norwich UCotA

Queen Margaret

Queen Mary

Reading

Robert Gordon

Russell Group

St Andrews

St Mary's

Strathclyde

Sussex

Swansea

Trinity Saint David

UA UKADIA

Ulster UoW NewportWestminster

Winchester

WorcesterYork St John

Northumbria

Average of Averages

1.00

1.50

2.00

2.50

3.00

3.50

30 35 40 45 50 55 60 65 70 75 80

Rese

arch

Ass

essm

ent

(CU

G 2

012)

Graduate Prospects (2012)ADSS

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering30

3. Situational Analysis: Perceptions

1994 Group

Aberdeen

Aberystwyth

Aston

Bangor

Bath

Brighton

Brunel

Canterbury Christ Church

ChesterChichester

City

Dundee Heriot-Watt

Hull

Keele

Million+

N8

Queen Margaret

Queen Mary

Reading

Robert Gordon

St Andrews

St Mary's

Stirling

Sussex

Swansea

UA

Ulster

Westminster

Northumbria

Average of Averages

1.00

1.50

2.00

2.50

3.00

3.50

30 40 50 60 70 80

Re

sear

ch A

sse

ssm

en

t (C

UG

20

12

)

Graduate Prospects (CUG 2012)B&L

University Capabilities – Business & Law Subjects: CUG 2012

Based on non-weighted averaging of CUG data

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering31

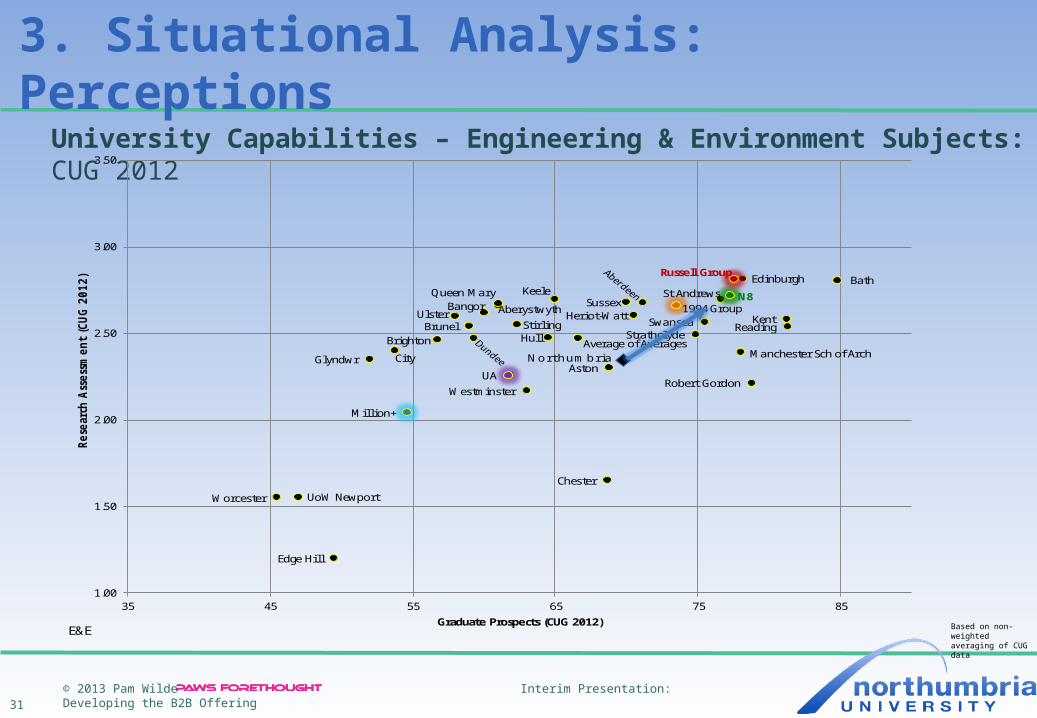

3. Situational Analysis: Perceptions

1994 GroupAberystwyth

Aston

Bangor

Bath

BrightonBrunel

Chester

City

Edge Hill

Edinburgh

Glyndwr

Heriot-Watt

Hull

Keele

Kent

Manchester Sch of Arch

Million+

N8Queen Mary

Reading

Robert Gordon

Russell Group

St Andrews

StirlingStrathclyde

Sussex

Swansea

UA

Ulster

UoW Newport

Westminster

Worcester

NorthumbriaAverage of Averages

1.00

1.50

2.00

2.50

3.00

3.50

35 45 55 65 75 85

Re

sear

ch A

sse

ssm

en

t (C

UG

20

12

)

Graduate Prospects (CUG 2012)E&E

University Capabilities – Engineering & Environment Subjects: CUG 2012

Based on non-weighted averaging of CUG data

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering

32

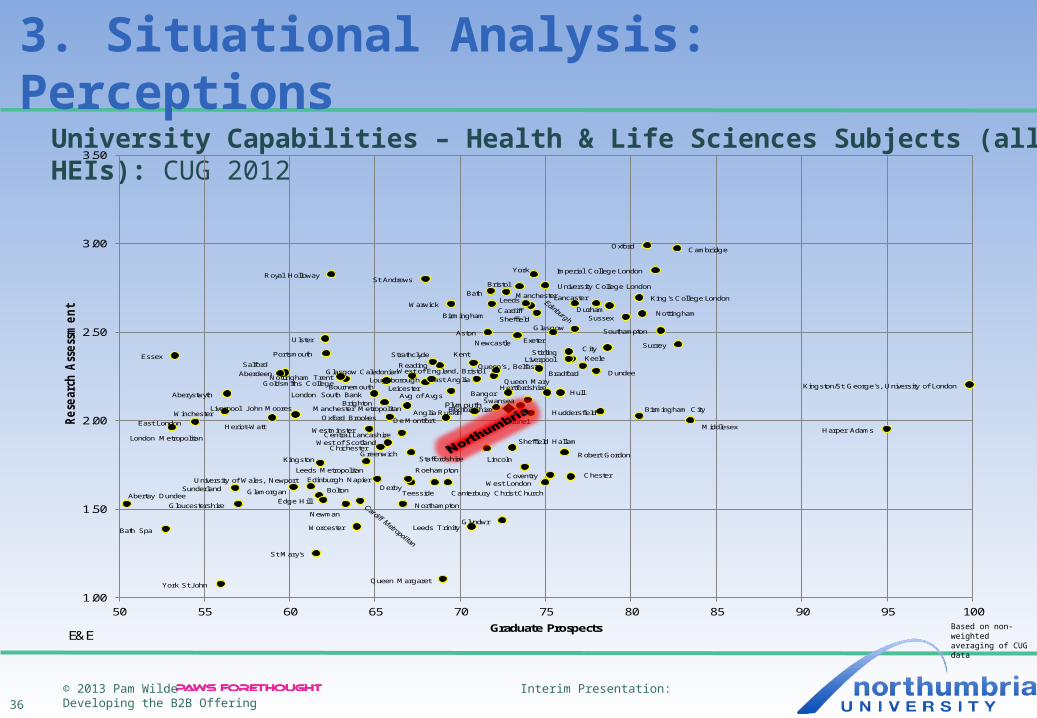

3. Situational Analysis: PerceptionsUniversity Capabilities – Health & Life Sciences Subjects: CUG 2012

Aberdeen

Aberystwyth

Aston

Bangor

Bath

Brighton

Brunel

Canterbury Christ ChurchChester

Chichester

CityDundee

Edge Hil l

Edinburgh

Glyndwr

Harper AdamsHeriot-Watt

Hull

KeeleKent

Kingston/St George's, UoL

Leeds Trinity

Million+

N8

Newman

Queen Margaret

Queen MaryReading

Robert Gordon

Russell Group

St Andrews

St Mary's

Stirling

Strathclyde

Sussex

Swansea

UA

Ulster

UoW Newport

Westminster

Winchester

Worcester

York St John

NorthumbriaAverage of Averages

1.00

1.50

2.00

2.50

3.00

3.50

55 60 65 70 75 80 85 90 95 100

Graduate ProspectsH&LS

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering33

3. Situational Analysis: PerceptionsUniversity Capabilities - Art, Design & Social Science Subjects (all HEIs): CUG 2012

Based on non-weighted averaging of CUG data

Aberdeen

AberystwythAnglia Ruskin

Arts University College at Bournemouth

Aston

Bangor

Bath

Bath Spa

Bedfordshire

Birmingham

Birmingham City

Bolton

Bournemouth

Bradford

BrightonBristol

Brunel

Cambridge

Canterbury Christ Church

Cardiff

Cardiff Metropolitan

Central Lancashire

Central School of Speech and Drama

Chester

Chichester

City

Courtauld Institute

Coventry

Cumbria

De Montfort

Derby

Dundee

Durham

East Anglia

East London

Edge Hill

Edinburgh

Edinburgh Napier

Essex

Exeter

Falmouth

Glamorgan

Glasgow

Glasgow Caledonian

Gloucestershire

Glyndwr

Goldsmiths College

Greenwich

Heriot-Watt

Hertfordshire

Huddersfield

Hull

KeeleKent

King's College London

Kingston

Lancaster

Leeds

Leeds Metropolitan

Leeds Trinity

Leicester

Lincoln

Liverpool

Liverpool John Moores

London Metropolitan

London School of Economics

London South Bank

Loughborough

Manchester

Manchester Metropolitan

Middlesex

Newcastle

NewmanNorthampton

Northumbria

Norwich UCA

Nottingham

Nottingham Trent

Oxford

Oxford Brookes

Plymouth

Plymouth St Mark and St John

Portsmouth

Queen Margaret

Queen Mary

Queen's, BelfastReading

Robert Gordon

Roehampton

Royal Holloway

Salford

Sheffield

Sheffield Hallam

SOAS

Southampton

Southampton Solent

St Andrews

St Mary'sStaffordshire

Stirling

StrathclydeSunderland

Surrey

Sussex

Swansea

Teesside

Trinity Saint David

Ulster

University College London

University for the Creative Arts

University of the Arts, London

UoW, Newport

Warwick

West London

West of England, Bristol

West of Scotland

Westminster

Winchester

York

York St John

1.00

1.50

2.00

2.50

3.00

3.50

30 35 40 45 50 55 60 65 70 75 80 85

Re

sear

ch A

sse

ssm

en

t

Graduate ProspectsAD&SS

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering34

3. Situational Analysis: PerceptionsUniversity Capabilities – Business & Law Subjects (all HEIs): CUG 2012

Based on non-weighted averaging of CUG data

Aberdeen

Abertay Dundee

Aberystwyth

Aston

Bangor

Bath

Bedfordshire

Birmingham

Bolton

Bournemouth

Bradford

Brighton

Bristol

Brunel

Canterbury Christ Church

Cardiff

Cardiff Metropolitan

Chester

Chichester

City

Coventry

De Montfort

Dundee

Durham

East Anglia

East London

Edinburgh

Edinburgh Napier

Essex

Exeter

Glamorgan

Glasgow

Glasgow Caledonian

Gloucestershire

Goldsmiths College

Greenwich

Heriot-Watt

Hertfordshire

Huddersfield

Hull

Keele

KentKing's College London

Kingston

LancasterLeeds

Leeds Metropolitan

Leicester

Lincoln

Liverpool

Liverpool John MooresLondon Metropolitan

London South Bank

Loughborough

Manchester

Middlesex

Newcastle

Northampton

Northumbria

Nottingham

Nottingham Trent

Oxford Brookes Plymouth

Portsmouth

Queen Margaret

Queen Mary

Queen's, Belfast

Reading

Robert Gordon

Roehampton

Royal Holloway

Salford

Sheffield

Sheffield Hallam

SOAS

Southampton

St Andrews

St Mary's

Staffordshire

Stirling

Strathclyde

Sunderland

Surrey Sussex

Swansea

Teesside

Ulster

University College London

Warwick

West of England, Bristol

West of Scotland

Westminster

York

Grand Total

1.00

1.50

2.00

2.50

3.00

3.50

30 35 40 45 50 55 60 65 70 75 80 85

Re

sear

ch A

sse

ssm

en

t

Graduate ProspectsB&L

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering35

3. Situational Analysis: PerceptionsUniversity Capabilities – Engineering & Environment (all HEIs): CUG 2012

Based on non-weighted averaging of CUG data

AberdeenAberystwyth

Aston

Bangor

Bath

Bath Spa

Bedfordshire

Birmingham

Birmingham City

Bolton

Bournemouth

Bradford

Brighton

Bristol

Brunel

Cambridge

Cardiff

Chester

City

Coventry

De Montfort

Dundee

Durham

East Anglia

East London

Edge Hill

Edinburgh

Glamorgan

Glasgow Caledonian

Gloucestershire

Glyndwr

Goldsmiths College

Greenwich

Heriot-Watt

Hertfordshire

Huddersfield

Hull

Imperial College London

Keele

Kent

Kingston

Leeds Metropolitan

Leicester

Lincoln

Liverpool

Liverpool John Moores

London Metropolitan

London School of Economics

London South Bank

Manchester Metropolitan

Manchester School of Architecture

Middlesex

Newcastle

Northumbria

Nottingham

Nottingham Trent

Oxford

Oxford Brookes

Plymouth

Portsmouth

Queen Mary

Queen's, Belfast Reading

Robert Gordon

Royal Holloway

Salford

Sheffield

Sheffield Hallam

Southampton

Southampton Solent

Staffordshire

Stirling

Strathclyde

Sunderland

Surrey

Sussex

Teesside

Ulster

University College London

University of Wales, Newport

Warwick

West London

West of England, Bristol

West of Scotland

Worcester

Average of Averages

1.00

1.50

2.00

2.50

3.00

3.50

35 40 45 50 55 60 65 70 75 80 85 90

Re

sea

rch

Ass

ess

me

nt

Graduate ProspectsE&E

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering36

3. Situational Analysis: PerceptionsUniversity Capabilities – Health & Life Sciences Subjects (all HEIs): CUG 2012

Based on non-weighted averaging of CUG data

Aberdeen

Abertay Dundee

Aberystwyth

Anglia Ruskin

Aston

Bangor

Bath

Bath Spa

Bedfordshire

Birmingham

Birmingham City

Bolton

Bournemouth

Bradford

Brighton

Bristol

Brunel

Cambridge

Canterbury Christ Church

Cardiff

Central Lancashire

Chester

Chichester

City

Coventry

De Montfort

Derby

Dundee

Durham

East Anglia

East London

Edge Hill

Edinburgh Napier

Essex

Exeter

Glamorgan

Glasgow

Glasgow Caledonian

Gloucestershire

Glyndwr

Goldsmiths College

Greenwich

Harper AdamsHeriot-Watt

Hertfordshire

Huddersfield

Hull

Imperial College London

KeeleKent

King's College London

Kingston

Kingston/St George's, University of London

LancasterLeeds

Leeds Metropolitan

Leeds Trinity

Leicester

Lincoln

Liverpool

Liverpool John Moores

London Metropolitan

London South Bank

Loughborough

Manchester

Manchester Metropolitan

Middlesex

Newcastle

NewmanNorthampton

Nottingham

Nottingham Trent

Oxford

Oxford Brookes

Plymouth

Portsmouth

Queen Margaret

Queen Mary

Queen's, BelfastReading

Robert Gordon

Roehampton

Royal Holloway

Salford

Sheffield

Sheffield Hallam

Southampton

St Andrews

St Mary's

Staffordshire

StirlingStrathclyde

Sunderland

Surrey

Sussex

Swansea

Teesside

Ulster

University College London

University of Wales, Newport

Warwick

West London

West of England, Bristol

West of Scotland

Westminster

Winchester

Worcester

York

York St John

Avg of Avgs

1.00

1.50

2.00

2.50

3.00

3.50

50 55 60 65 70 75 80 85 90 95 100

Re

sear

ch A

sse

ssm

en

t

Graduate ProspectsE&E

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering37

4. Market Analysis

• Sectors & Trends Economic recession and challenges – impact on spending, investment, innovation and

skills development Identify and develop plans to maximise opportunities in emerging markets and

growing sectors Reduction in Public Sector spending increases need to diversify Winding down of Regional Development Agencies means new relationships may need

to be established Impact arising from e.g. changes in e.g. HE Innovation Funding need to be assessed

and quantified Possible opportunities arising out of legislative and political changes e.g. freeing up

legal market, CRE disbanding

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering38

5. Customer Needs Analysis

• Businesses think in terms of product and (multi-disciplinary) capability• Business Needs from Graduates

Graduate leadership, management & communication skills Graduate ‘real-world’ &/or workplace experience Basic & fundamental skills Common sense, commercial perspective Independent thought and & problem solving capabilities Self motivation, passionate, positive attitude

• Articulate these outcomes in collateral – in business language• Demonstrate how they are integrated into courses and adopted by

graduates• Student needs driven by business needs re employability

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering39

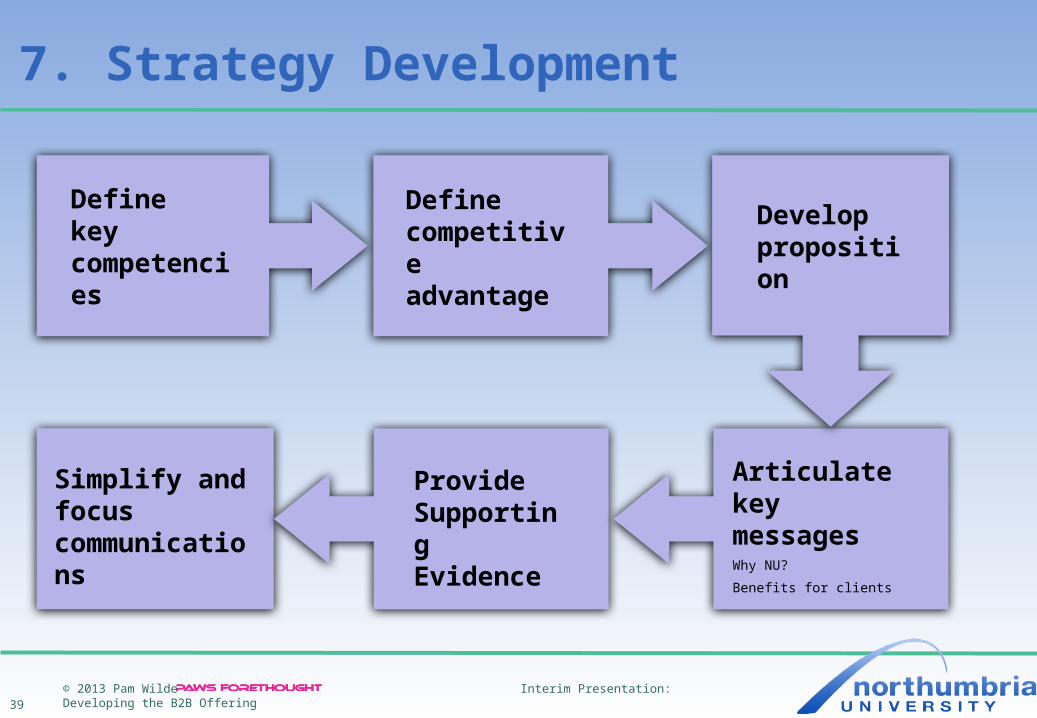

7. Strategy Development

Define keycompetencies

Define competitive advantage

Provide Supporting Evidence

Simplify and focus communications

Articulate key messagesWhy NU?

Benefits for clients

Develop proposition

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering40

8. Headline findings – early indications• Recommended areas to explore

Develop a clear proposition for engaging business community

Internally focussed – need to focus on external market & customer needs

Prioritise resources and activities based on market needs

Develop brand positioning based on market needs and competitive advantages

Develop multi-disciplinary capability and positioning

Communications – key messages, simply articulated and presented

Process improvements: e.g. easier access and interface with University

Develop sales strategy that supports delivery of University objectives

Embed business thinking and terminology in the University

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering41

8. Headline findings – early indications• (Marketing) organisational recommendations

Remits more externally focussed: international, market, customer, competitor

Increased market intelligence and competitor monitoring focus Dedicated B2B resource –

• “go to” person in Marketing who “lives” B2B Specific communications, brand and digital B2B responsibilities

incorporated into Marketing roles Specific Brand and Communications Strategy Manager role

covering B2B as part of remit B2B Product Manager

• focus on developing multi-disciplinary portfolio

© 2013 Pam Wilde Interim Presentation: Developing the B2B Offering42

8. Headline findings – early indications• Cultural recommendations

Investigate option of Commercial Manager – with B2B accountabilities – responsibilities to include pricing and analysis of BDM activity/wins/losses• Supports move to university being more commercially focussed

Emphasis on centralisation in the short to medium term until disciplines embedded• Enables control, consistency• Dedicated resource to focus on agreed priorities and demonstrate importance• Supports focus on market-led multi-disciplinary rather than individual faculty focus• Facilitates cultural change and sharing of learning/best practice• Need to ensure supports move to being more proactive and nimble

Hold e.g. market insight and best practice sessions