· stifel -50%-25% 0% 25% 50% 75% 100% 125% 150% 175% 500 incremental annualized return of s&p...

TRANSCRIPT

Barry B. Bannister, CFA [email protected] (443) 224-1317

Jesse Cantor [email protected] (443) 224-1344

Stifel Equity Trading Desk (800) 424-8870

Market Commentary/Strategy

To QEternal or QExit, that is the Question: the Case Builds for Tapering Soon

We see a slow 12-month QE taper that starts as early as Dec-2013, consensus sees a Mar-2014 taper thatwinds QE down in ~6 months. Catalysts are: a counter-productive shrinkage of Treasury collateral,diminishing effectiveness of adding a constant $85B/month to base money, a need to holster QE before usingit again, and the historical tendency of post-WW II Fed Chairmen not to leave unfinished business. Stockmarket volatility typically jumps after Fed transitions, but despite more volatility we see the S&P 500 ending2014 flat as QE taper lowers the P/E by a percentage that equals the 2014 EPS growth we see, ergo a flatS&P 500. We take our risk with sectors, and since Materials, Energy, Industrials & Technology can do well inthe year before the first rate hike we see a window of opportunity as global GDP returns.

As we stated Oct-3, 2013 on Page 5-6, we see a modest QE taper as early as Dec-2013 that lasts a year, versus

consensus of a Mar-2014 taper that winds QE down more quickly. We show that adding a constant $85B monthly to the

monetary base has diminishing returns (Exhibit 1) and if credit creation is the goal there is little utility in removing 80% of

net Treasury debt issuance (i.e., high quality collateral) on a run-rate basis by 1Q14E (Exhibit 2). Even if the $40B/mo.

Treasury purchases are tapered, we doubt the Fed trims the $45B/mo. MBS QE until 2H14 since net MBS issuance is still

negative and past QE rounds did not end until net MBS issuance turned positive (Exhibit 3).

Another reason we see for commencing taper forthwith is a desire to save QE for later use. While the Fed frames its

communications in terms of objectives (ex., "until X% unemployment”) and time (ex., for a “prolonged period”) we use a

"builder" analogy and believe the Fed has three principal tools: (1) the "Hammer" of QE, (2) the "Bulldozer" of rate policy,

and (3) the "Scaffolding" of Fed-held assets (Exhibit 4-5). We believe the optimal use of the QE hammer - once it is

placed back in the Fed’s tool belt (tapered) - is to surprise the market to achieve maximal effect. This contrasts with rate

policy and stock of assets held, which we believe require more communication to achieve objectives.

In the year before leaving office the eight departing Fed Chairmen since 1948 have uniformly presided over rising policy

interest rates and periods of modest stock market volatility. In contrast, the first year of new Chairmen features a wide

divergence in rates (perhaps due to the human urge of a new Chairman to “do something”?) with spiking stock market

volatility, especially the first ~90 days (Exhibit 6). Though the FFR is currently resting on the zero bound, a higher Fed

Funds Rate (FFR) has already de facto occurred because QE was effectively a “negative” interest rate according to Fed

research that has traveled from minus 5% in late 2009 to about 0% currently (Exhibit 7). Given that FFR history may be

repeating itself, we believe it is reasonable for investors to expect heightened stock market volatility in 1H14.

Despite the bump in volatility we see 2014 as “full of sound and fury, signifying nothing.” Our view of a slow Fed taper that

starts in Dec-2013 and lasts all year to Dec-2014 serves to lower the S&P 500 P/E ratio (Trailing 12-month, Operating) by

~(9)% from 17x to 15.5x in 2014, in our view, given the correlation between QE and P/E (no such correlation exists

between EPS and QE). The Fed is a manipulator of the price of money - interest discount rates - and the P/E is a discount

rate (earnings yield). Multiplying our below Consensus 2014 EPS view of +7% y/y (Street view is +10.7% y/y) results in a

flat S&P 500 (Exhibit 8). The Materials, Energy, Industrials & Technology sectors typically do well in the year before a

rate hike, so we prefer them for a window of opportunity trade 4Q13/1Q14 as global growth returns (Exhibit 9).

November 6, 2013

Market Strategy*******

Stifel does and seeks to do business with companies covered in its research reports. As a result, investors shouldbe aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investorsshould consider this report as only a single factor in making their investment decision.

All relevant disclosures and certifications appear on pages 14 - 15 of this report.

STIFEL

Stifel Macro & Sector Views:

To QEternal or QExit, that is the Question:

the Case Builds for Tapering Soon

November 6, 2013

Barry B. Bannister, CFA

Managing Director, Equity Research – Chief Equity Strategist, Stifel [email protected] 443-224-1317

Stifel does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of

interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

All relevant disclosures and certifications appear on page 14 & 15 of this report.

STIFEL

CLICK HERE FOR VIDEO SUMMARY

Page 2

Market StrategyNovember 6, 2013

STIFEL

-50%

-25%

0%

25%

50%

75%

100%

125%

150%

175%

An

nu

ali

zed

Retu

rn o

f S

&P

500

Incremental annualized return of S&P 500 (price only) per $250B of marketable securities purchased by the Federal

Reserve, Nov-08 to present

-12,000

-10,000

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

An

nu

ali

ze

d G

row

th in

No

nfa

rm P

ayro

lls

(0

00

's)

Incremental nonfarm payroll growth (at annualized clip, thousands of jobs)* per

$250B of marketable securities purchased by the Federal Reserve, Nov-08 to present

* Interpolated to weekly figures

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Ja

n-1

0

Ap

r-1

0

Ju

l-1

0

Oc

t-1

0

Ja

n-1

1

Ap

r-11

Ju

l-11

Oc

t-11

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oc

t-1

2

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oc

t-1

3

Ja

n-1

4

Total Federal Reserve Assets YoY Change (Left) vs. Core PCE-Deflator 3-Month

Annualized Change (Right)

Source: U.S. Federal Reserve & Bloomberg data. Stifel format.

Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

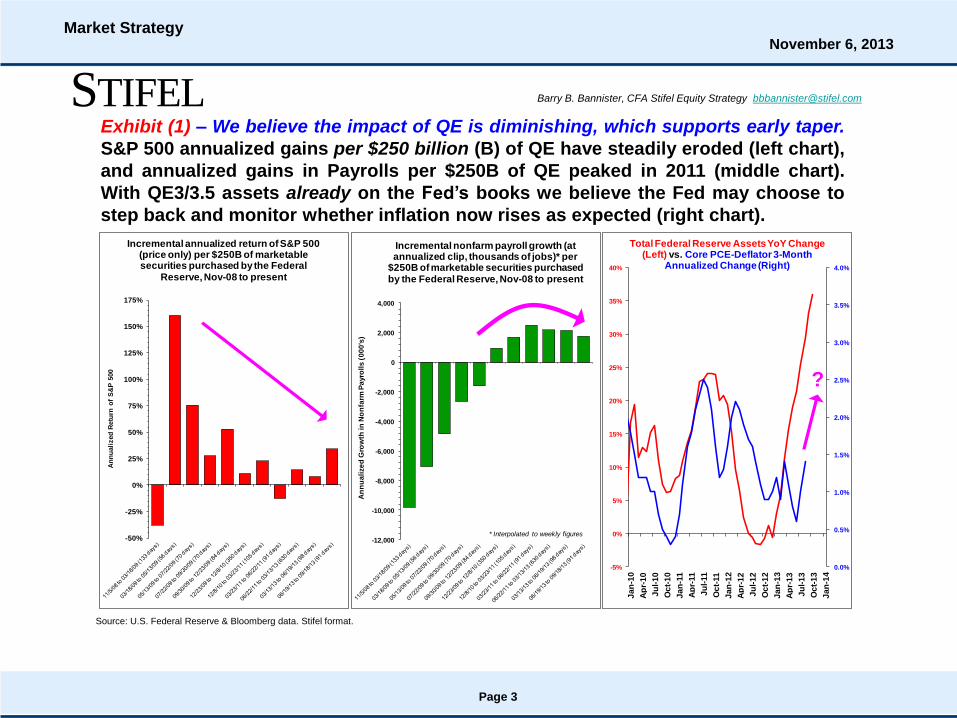

Exhibit (1) – We believe the impact of QE is diminishing, which supports early taper.

S&P 500 annualized gains per $250 billion (B) of QE have steadily eroded (left chart),

and annualized gains in Payrolls per $250B of QE peaked in 2011 (middle chart).

With QE3/3.5 assets already on the Fed’s books we believe the Fed may choose to

step back and monitor whether inflation now rises as expected (right chart).

?

Page 3

Market StrategyNovember 6, 2013

STIFEL

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

E

1Q

14

E

LTM % Net Treasury Issuance (New Supply of Treasuries) Purchased by the Federal Reserve

End of QE11Q2010

End of QE22Q2011

Estimates depict Fed purchases without taper

and Stifel est. of net treasury issuance

through 1Q14.

Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

Source: SIFMA, Dept. of Treasury, Bloomberg data. Stifel estimates.

Exhibit (2) – One catalyst for commencing a taper of the Treasury portion of

QE before Chairman Bernanke’s term ends 1/31/14 is collateral withdrawal. The

Fed’s purchases are removing quality collateral from the system, absorbing

80% of net trailing 12-month (TTM) Treasury issuance by 1Q14E. We believe

this supports an early start for tapering the $40B/mo. of Treasury purchases.

Page 4

Market StrategyNovember 6, 2013

STIFEL

-$0.4 Tr.

-$0.2 Tr.

$0.0 Tr.

$0.2 Tr.

$0.4 Tr.

$0.6 Tr.

$0.8 Tr.

$1.0 Tr.

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13E

1Q

14E

2Q

14E

3Q

14E

4Q

14E

LTM Net Mortgage-backed Security Issuance (New Supply of MBS) Purchased by the Federal Reserve

Net MBS Issued (i.e. negative = supply

shrinking)

Purchased by the FedEnd of QE1

1Q2010

End of QE22Q2011

Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

Source: SIFMA, Dept. of Treasury, Bloomberg data. Stifel estimates.

Exhibit (3) – We would expect tapering of the MBS portion of QE to wait until 2nd

half 2014. MBS purchases are $45B/month but net MBS issuance (black line) is

still negative. Since QE1 and QE2 only ended when net MBS issuance turned

positive (circles), the Fed may wait until 2H14 to withdraw MBS QE, in our view.

Page 5

Market StrategyNovember 6, 2013

STIFEL

Source: Stifel commentary.

(1) ZIRP is Zero Interest Rate Policy, IOER is Interest on Excess Reserves, RRR is Reserve Requirement Ratio.

Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

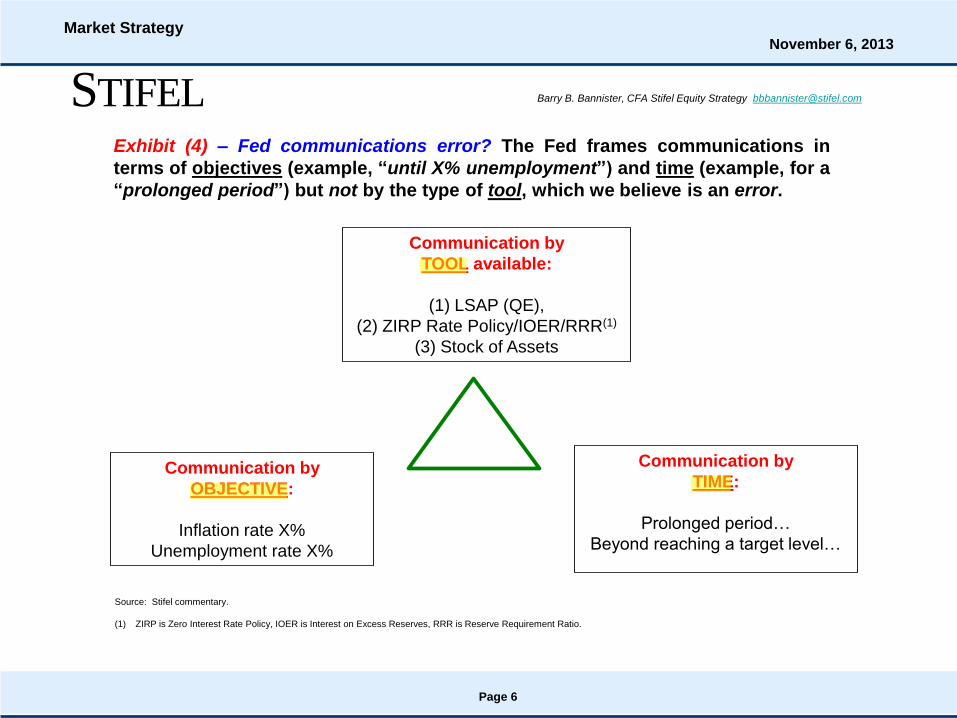

Communication by

TOOL available:

(1) LSAP (QE),

(2) ZIRP Rate Policy/IOER/RRR(1)

(3) Stock of Assets

Communication by

OBJECTIVE:

Inflation rate X%

Unemployment rate X%

Communication by

TIME:

Prolonged period…

Beyond reaching a target level…

Exhibit (4) – Fed communications error? The Fed frames communications in

terms of objectives (example, “until X% unemployment”) and time (example, for a

“prolonged period”) but not by the type of tool, which we believe is an error.

Page 6

Market StrategyNovember 6, 2013

STIFEL

Source: Wikimedia commons, Stifel commentary.

(1) ZIRP is Zero Interest Rate Policy, IOER is Interest on Excess Reserves. We could include Reserve Requirements in rates as well.

(2) Base Money is currency + bank reserves at the Federal Reserve.

Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

LSAP (QE) Asset purchases

(Hammer)

Target 0% rates & Interest on

Excess Reserves (IOER)

(Bulldozer)

Stock of assets held on Fed

balance sheet

(Scaffolding)

Optimal Communication Strategy:

Surprise

Objective of the Strategy:

To control rate volatility

Optimal Communication Strategy:

Moderate lead time

Objective of the Strategy:

To control rate levels

Optimal Communication Strategy:

Sustained with gradual change

Objective of the Strategy:

To flex base money(2)

Exhibit (5) - Our view is that QE is more effective without advance Fed

communication. The Fed has three “tools”, which are: (1) “Hammer” LSAP (QE),

(2) “Bulldozer” rate policy(1), and (3) “Scaffolding” Fed-held stock of assets. These

tools have different uses and optimal communications strategies, in our view. For

example, we have long contended that QE 3/3.5 was effective precisely because it

was open-ended and thus could not be discounted by the market.

Page 7

Market StrategyNovember 6, 2013

STIFEL

(A)(B)

(C)

(D)

(E)

(F)(G)

-400bps

-300bps

-200bps

-100bps

0bps

100bps

200bps

300bps

400bps

500bps

600bps

700bps

800bps

M-1

2M

-11

M-1

0M

-9M

-8M

-7M

-6M

-5M

-4M

-3M

-2M

-1M

+0

M+

1M

+2

M+

3M

+4

M+

5M

+6

M+

7M

+8

M+

9M

+10

M+

11

M+

12

Federal Funds Rate (FFR) Surrounding (12 Months Prior + 12 Months Following) Transitions of Federal Reserve

Chairmen, Indexed to Chairman Exit = 100, +/- in Bps

(A) Eccles (4/15/48)

(B) McCabe (3/31/51)

(C) Martin (1/31/70)

(D) Burns (1/31/78)

(E) Miller (8/6/79)

(F) Volcker (8/11/87)

(G) Greenspan (1/31/06)

Chairman (Departure)

Source: U.S. Federal Reserve, Dow Jones & Co. Stifel formats.

(1) NY Fed Discount Rate 1/48 to 6/54, Actual FFR 7/54 to 8/82, Target FFR 9/82 to 12/08, Actual FFR 1/09 to present. We acknowledge that the focus of past Federal Reserve

Boards was not always on rates (example: Fed research here). We use rates for simplicity as prima facie evidence of policy direction.

Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

15

25

35

45

55

65

75

Trailing 30-Day Volatility of Dow Jones Industrial Average, Composite of Days (+/- 250 Trading Days) Surrounding Transition of Fed Chairmen since 1948

Exhibit (6) - The year before the exit of past Fed Chairmen has featured higher policy

rates and modest stock market volatility, but the year after has greater

variance/volatility. Fed Chairmen since W.W. II (Appendix A) have exited with rising

rates(1), but new Chairmen have been more disparate (left chart), raising stock

market volatility the first ~90 days after the new Chairman takes office (right chart).

Fed uniformly tightens

before a Chairman

departs…

…but new Fed

Chairmen have a

disparate 1st year.

Stock market volatility

is modest before a

Chairman departs…

…but increases the

first quarter after a

new Chairman

takes office.

1st quarter of

new Chairman

Page 8

Market StrategyNovember 6, 2013

STIFEL Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

Exhibit (7) – In keeping with the history of past transitions, this Fed has already de

facto tightened rates. As the chart below from a Fed study(1) shows, once rates

reached 0% the LSAP (QE) and conditions created a “negative” FFR of -5% in 2009,

diminishing as economic & financial(2) variables have recovered, moving toward 0%.

Source: Cleveland Fed study.

(1) “Where Would the Federal Funds Rate Be, If It Could Be Negative?” Cleveland Fed, Oct-2012 here. Chart was updated by the Cleveland Fed upon request.

(2) The empirical model cited above used a Bayesian Vector Autoregressive (BVAR) model with 17 variables to determine an unrestricted forecast of the FFR. As

we would expect, financial variables contributed the most to the estimated FFR recovery from a -4% plateau post 4Q2010.

Pe

rce

nt

Page 9

Market StrategyNovember 6, 2013

STIFEL

13.0x

13.5x

14.0x

14.5x

15.0x

15.5x

16.0x

16.5x

17.0x

Ja

n-1

2

Ma

r-12

Ma

y-1

2

Ju

l-12

Se

p-1

2

No

v-1

2

Ja

n-1

3

Ma

r-13

Ma

y-1

3

Ju

l-13

Se

p-1

3

No

v-1

3

Ja

n-1

4

Ma

r-14

Ma

y-1

4

Ju

l-14

Se

p-1

4

No

v-1

4

Ja

n-1

5

S&P 500 Index P/E on Operating Earnings, Actual and Estimates through 4Q14,

Actual Projection$1,250

$1,300

$1,350

$1,400

$1,450

$1,500

$1,550

$1,600

$1,650

$1,700

$1,750

$1,800

De

c-11

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

De

c-1

2

Fe

b-1

3

Ap

r-13

Ju

n-1

3

Au

g-1

3

Oct-1

3

De

c-1

3

Fe

b-1

4

Ap

r-14

Ju

n-1

4

Au

g-1

4

Oct-1

4

De

c-1

4

S&P 500 Index Weekly Average PriceProjection based on Stifel Taper Assumptions

(Left Chart, Top) & Stifel Earnings Ests.

Actual Projection

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Ja

n-1

2

Ma

r-12

Ma

y-1

2

Ju

l-12

Se

p-1

2

No

v-1

2

Ja

n-1

3

Ma

r-13

Ma

y-1

3

Ju

l-13

Se

p-1

3

No

v-1

3

Ja

n-1

4

Ma

r-14

Ma

y-1

4

Ju

l-14

Se

p-1

4

No

v-1

4

Ja

n-1

5

BCA "Money Impulse": 2nd Derivative of U.S. Monetary Base, Advanced Six Weeks vs. S&P 500 LTM P/E Ratio (3-Mo. % Change),Actual Jan-12 to Latest, Stifel Estimates through 4Q14. 3-Month Smoothed

Fed taper 2nd deriv. leads S&P P/E change by ~6 weeks, implies S&P

P/E slightly down mid-2014E.

Actual Projection

Source: Standard & Poor’s, Bloomberg. Stifel format.

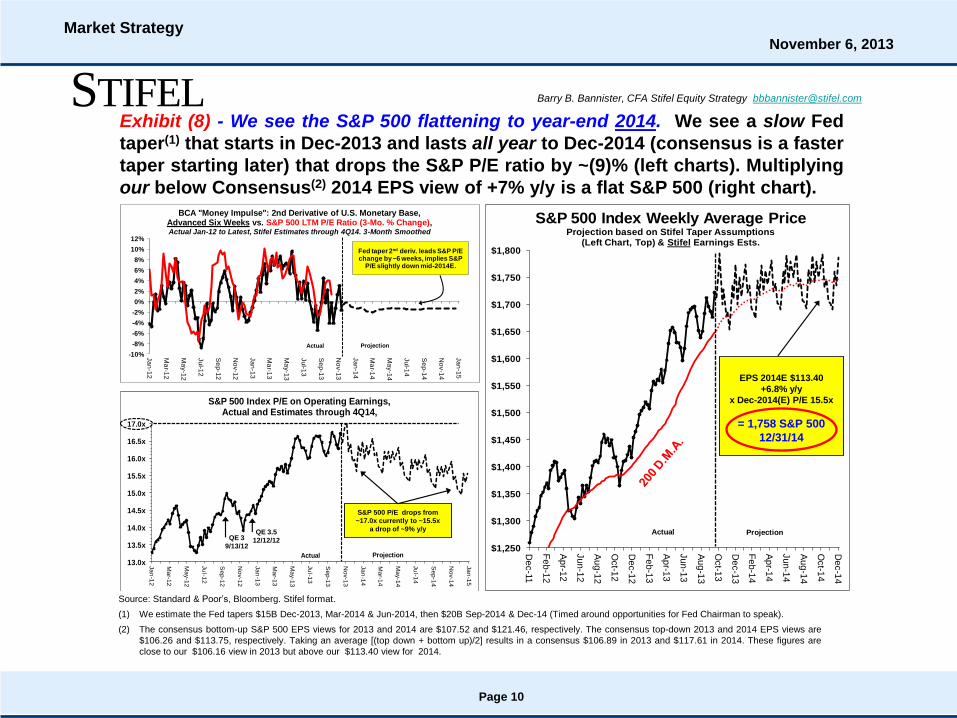

(1) We estimate the Fed tapers $15B Dec-2013, Mar-2014 & Jun-2014, then $20B Sep-2014 & Dec-14 (Timed around opportunities for Fed Chairman to speak).

(2) The consensus bottom-up S&P 500 EPS views for 2013 and 2014 are $107.52 and $121.46, respectively. The consensus top-down 2013 and 2014 EPS views are

$106.26 and $113.75, respectively. Taking an average [(top down + bottom up)/2] results in a consensus $106.89 in 2013 and $117.61 in 2014. These figures are

close to our $106.16 view in 2013 but above our $113.40 view for 2014.

EPS 2014E $113.40

+6.8% y/y

x Dec-2014(E) P/E 15.5x

= 1,758 S&P 500

12/31/14

S&P 500 P/E drops from

~17.0x currently to ~15.5x

a drop of ~9% y/y

QE 3

9/13/12

QE 3.5

12/12/12

Exhibit (8) - We see the S&P 500 flattening to year-end 2014. We see a slow Fed

taper(1) that starts in Dec-2013 and lasts all year to Dec-2014 (consensus is a faster

taper starting later) that drops the S&P P/E ratio by ~(9)% (left charts). Multiplying

our below Consensus(2) 2014 EPS view of +7% y/y is a flat S&P 500 (right chart).

Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

Page 10

Market StrategyNovember 6, 2013

STIFEL

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1.0%

Ja

n-1

1

Ap

r-11

Ju

l-11

Oc

t-11

Ja

n-1

2

Ap

r-12

Ju

l-12

Oc

t-12

Ja

n-1

3

Ap

r-13

Ju

l-13

Oc

t-13

Ja

n-1

4

Ap

r-14

Ju

l-14

Oc

t-14

Ja

n-1

5

Ap

r-15

Ju

l-15

Oc

t-15

Ja

n-1

6

Fed Funds Effective Rate FF Futures

Our take: Effective Fed Funds Rate with

Futures Curve Implications as of 9/30/13

Window of opportunity: 4Q13

to 1H14E

Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

Source: Ned Davis Research report (May 31, 2013) “Rising Interest Rates & Sector Themes”

Copyright 2013 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

For data vendor disclaimers refer to www.ndr.com/vendorinfo/.

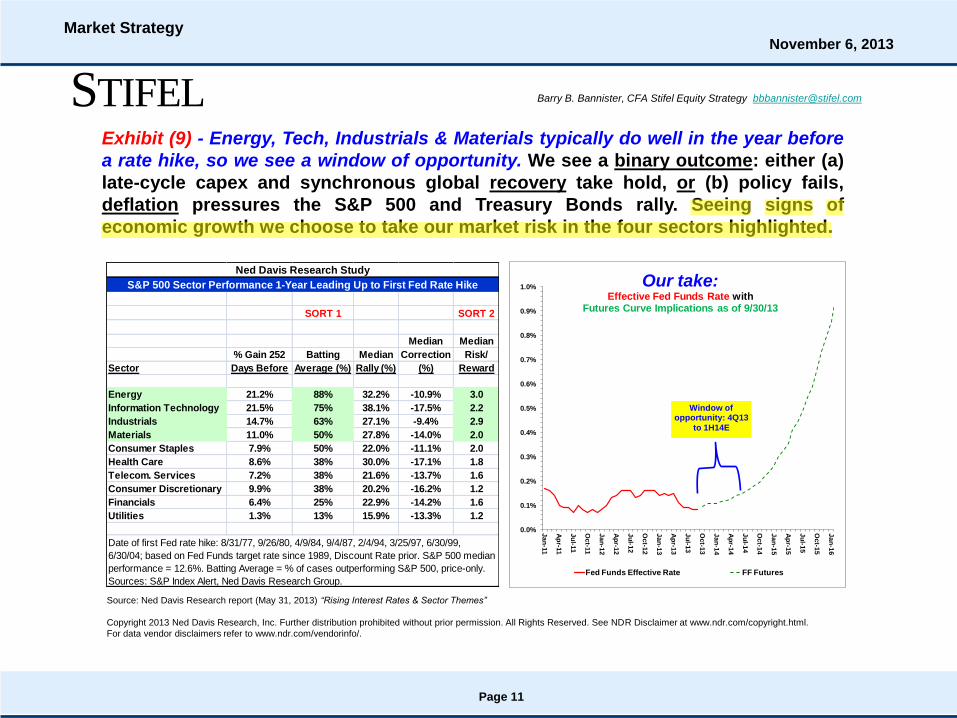

SORT 1 SORT 2

Median Median

% Gain 252 Batting Median Correction Risk/

Sector Days Before Average (%) Rally (%) (%) Reward

Energy 21.2% 88% 32.2% -10.9% 3.0

Information Technology 21.5% 75% 38.1% -17.5% 2.2

Industrials 14.7% 63% 27.1% -9.4% 2.9

Materials 11.0% 50% 27.8% -14.0% 2.0

Consumer Staples 7.9% 50% 22.0% -11.1% 2.0

Health Care 8.6% 38% 30.0% -17.1% 1.8

Telecom. Services 7.2% 38% 21.6% -13.7% 1.6

Consumer Discretionary 9.9% 38% 20.2% -16.2% 1.2

Financials 6.4% 25% 22.9% -14.2% 1.6

Utilities 1.3% 13% 15.9% -13.3% 1.2

Ned Davis Research Study

S&P 500 Sector Performance 1-Year Leading Up to First Fed Rate Hike

Date of first Fed rate hike: 8/31/77, 9/26/80, 4/9/84, 9/4/87, 2/4/94, 3/25/97, 6/30/99,

6/30/04; based on Fed Funds target rate since 1989, Discount Rate prior. S&P 500 median

performance = 12.6%. Batting Average = % of cases outperforming S&P 500, price-only.

Sources: S&P Index Alert, Ned Davis Research Group.

Exhibit (9) - Energy, Tech, Industrials & Materials typically do well in the year before

a rate hike, so we see a window of opportunity. We see a binary outcome: either (a)

late-cycle capex and synchronous global recovery take hold, or (b) policy fails,

deflation pressures the S&P 500 and Treasury Bonds rally. Seeing signs of

economic growth we choose to take our market risk in the four sectors highlighted.

Page 11

Market StrategyNovember 6, 2013

STIFEL

600

650

700

750

800

850

900

950

1000

4%

5%

6%

7%

8%

9%

10%

Ja

n-6

9

Fe

b-6

9

Ma

r-69

Ap

r-69

Ma

y-6

9

Ju

n-6

9

Ju

l-69

Au

g-6

9

Se

p-6

9

Oct-6

9

No

v-6

9

De

c-6

9

Ja

n-7

0

Fe

b-7

0

Ma

r-70

Ap

r-70

Ma

y-7

0

Ju

n-7

0

Ju

l-70

Au

g-7

0

Se

p-7

0

Oct-7

0

No

v-7

0

De

c-7

0

Ja

n-7

1

Do

w J

on

es I

nd

ustr

ials

Pri

ce

Fed

era

l F

un

ds R

ate

William McChesney Martin Jr.'s Exit (Jan-31, 1970)

700

750

800

850

900

950

1000

4%

5%

6%

7%

8%

9%

10%

11%

Ja

n-7

7

Fe

b-7

7

Ma

r-77

Ap

r-77

Ma

y-7

7

Ju

n-7

7

Ju

l-77

Au

g-7

7

Se

p-7

7

Oct-7

7

No

v-7

7

De

c-7

7

Ja

n-7

8

Fe

b-7

8

Ma

r-78

Ap

r-78

Ma

y-7

8

Ju

n-7

8

Ju

l-78

Au

g-7

8

Se

p-7

8

Oct-7

8

No

v-7

8

De

c-7

8

Ja

n-7

9

Do

w J

on

es I

nd

ustr

ials

Pri

ce

Fed

era

l F

un

ds R

ate

Arthur F. Burn's Exit (Jan-31, 1978)

190

200

210

220

230

240

250

260

270

280

1.45%

1.50%

1.55%

1.60%

1.65%

1.70%

1.75%

1.80%

Ma

r-50

Ap

r-50

Ma

y-5

0

Ju

n-5

0

Ju

l-50

Au

g-5

0

Se

p-5

0

Oct-5

0

No

v-5

0

De

c-5

0

Ja

n-5

1

Fe

b-5

1

Ma

r-51

Ap

r-51

Ma

y-5

1

Ju

n-5

1

Ju

l-51

Au

g-5

1

Se

p-5

1

Oct-5

1

No

v-5

1

De

c-5

1

Ja

n-5

2

Fe

b-5

2

Ma

r-52

Do

w J

on

es I

nd

ustr

ials

Pri

ce

NY

Fed

Dis

co

un

t R

ate

Thomas B. McCabe's Exit (Mar-31, 1951)

145

150

155

160

165

170

175

180

185

190

195

200

0.9%

1.0%

1.1%

1.2%

1.3%

1.4%

1.5%

1.6%

Ap

r-47

Ma

y-4

7

Ju

n-4

7

Ju

l-47

Au

g-4

7

Se

p-4

7

Oct-4

7

No

v-4

7

De

c-4

7

Ja

n-4

8

Fe

b-4

8

Ma

r-48

Ap

r-48

Ma

y-4

8

Ju

n-4

8

Ju

l-48

Au

g-4

8

Se

p-4

8

Oct-4

8

No

v-4

8

De

c-4

8

Ja

n-4

9

Fe

b-4

9

Ma

r-49

Ap

r-49

Do

w J

on

es I

nd

ustr

ials

Pri

ce

NY

Fed

Dis

co

un

t R

ate

Marriner S. Eccles' Exit (Apr-15, 1948)

Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

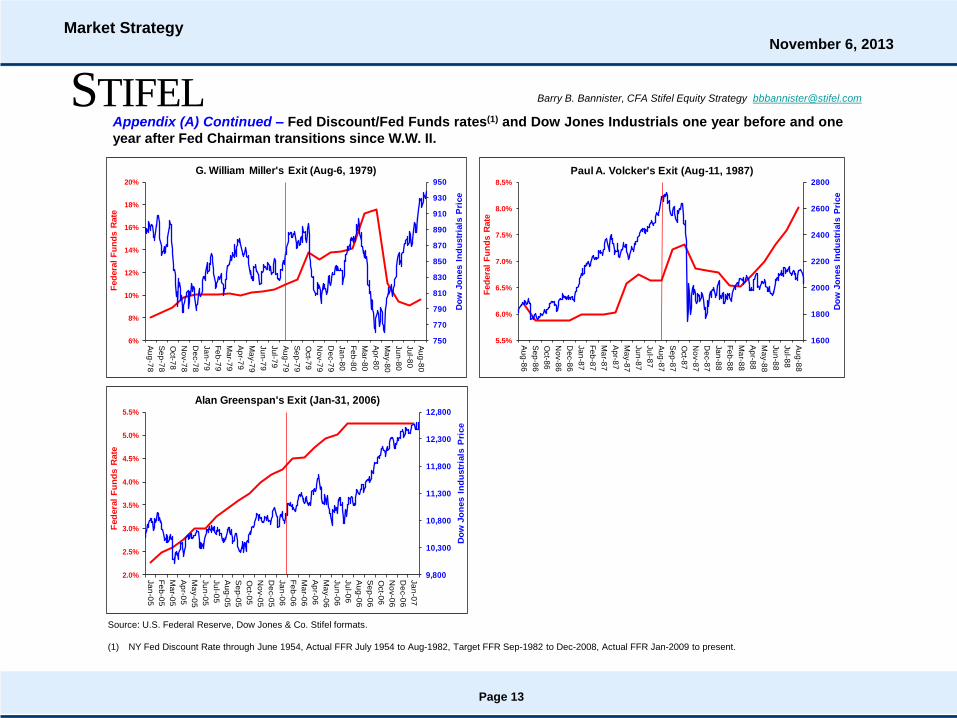

Appendix (A) – Fed Discount/Fed Funds rates(1) and Dow Jones Industrials one year before and one year after

Fed Chairman transitions since W.W. II.

Source: U.S. Federal Reserve, Dow Jones & Co. Stifel formats.

(1) NY Fed Discount Rate through June 1954, Actual FFR July 1954 to Aug-1982, Target FFR Sep-1982 to Dec-2008, Actual FFR Jan-2009 to present.

Page 12

Market StrategyNovember 6, 2013

STIFEL

750

770

790

810

830

850

870

890

910

930

950

6%

8%

10%

12%

14%

16%

18%

20%

Au

g-7

8

Se

p-7

8

Oct-7

8

No

v-7

8

De

c-7

8

Ja

n-7

9

Fe

b-7

9

Ma

r-79

Ap

r-79

Ma

y-7

9

Ju

n-7

9

Ju

l-79

Au

g-7

9

Se

p-7

9

Oct-7

9

No

v-7

9

De

c-7

9

Ja

n-8

0

Fe

b-8

0

Ma

r-80

Ap

r-80

Ma

y-8

0

Ju

n-8

0

Ju

l-80

Au

g-8

0

Do

w J

on

es I

nd

ustr

ials

Pri

ce

Fed

era

l F

un

ds R

ate

G. William Miller's Exit (Aug-6, 1979)

9,800

10,300

10,800

11,300

11,800

12,300

12,800

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

Ja

n-0

5

Fe

b-0

5

Ma

r-05

Ap

r-05

Ma

y-0

5

Ju

n-0

5

Ju

l-05

Au

g-0

5

Se

p-0

5

Oct-0

5

No

v-0

5

De

c-0

5

Ja

n-0

6

Fe

b-0

6

Ma

r-06

Ap

r-06

Ma

y-0

6

Ju

n-0

6

Ju

l-06

Au

g-0

6

Se

p-0

6

Oct-0

6

No

v-0

6

De

c-0

6

Ja

n-0

7

Do

w J

on

es I

nd

ustr

ials

Pri

ce

Fed

era

l F

un

ds R

ate

Alan Greenspan's Exit (Jan-31, 2006)

1600

1800

2000

2200

2400

2600

2800

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

Au

g-8

6

Se

p-8

6

Oct-8

6

No

v-8

6

De

c-8

6

Ja

n-8

7

Fe

b-8

7

Ma

r-87

Ap

r-87

Ma

y-8

7

Ju

n-8

7

Ju

l-87

Au

g-8

7

Se

p-8

7

Oct-8

7

No

v-8

7

De

c-8

7

Ja

n-8

8

Fe

b-8

8

Ma

r-88

Ap

r-88

Ma

y-8

8

Ju

n-8

8

Ju

l-88

Au

g-8

8

Do

w J

on

es I

nd

ustr

ials

Pri

ce

Fed

era

l F

un

ds R

ate

Paul A. Volcker's Exit (Aug-11, 1987)

Barry B. Bannister, CFA Stifel Equity Strategy [email protected]

Appendix (A) Continued – Fed Discount/Fed Funds rates(1) and Dow Jones Industrials one year before and one

year after Fed Chairman transitions since W.W. II.

Source: U.S. Federal Reserve, Dow Jones & Co. Stifel formats.

(1) NY Fed Discount Rate through June 1954, Actual FFR July 1954 to Aug-1982, Target FFR Sep-1982 to Dec-2008, Actual FFR Jan-2009 to present.

Page 13

Market StrategyNovember 6, 2013

Important Disclosures and Certifications

I, Barry B. Bannister, certify that the views expressed in this research report accurately reflect my personal viewsabout the subject securities or issuers; and I, Barry B. Bannister, certify that no part of my compensation was, is, orwill be directly or indirectly related to the specific recommendations or views contained in this research report. Forour European Conflicts Management Policy go to the research page at www.stifel.com.

Stifel research analysts receive compensation that is based upon (among other factors) Stifel's overall investment bankingrevenues.

Our investment rating system is three tiered, defined as follows:

BUY -For U.S. securities we expect the stock to outperform the S&P 500 by more than 10% over the next 12 months. ForCanadian securities we expect the stock to outperform the S&P/TSX Composite Index by more than 10% over the next 12months. For other non-U.S. securities we expect the stock to outperform the MSCI World Index by more than 10% over thenext 12 months. For yield-sensitive securities, we expect a total return in excess of 12% over the next 12 months for U.S.securities as compared to the S&P 500, for Canadian securities as compared to the S&P/TSX Composite Index, and for othernon-U.S. securities as compared to the MSCI World Index.

HOLD -For U.S. securities we expect the stock to perform within 10% (plus or minus) of the S&P 500 over the next 12months. For Canadian securities we expect the stock to perform within 10% (plus or minus) of the S&P/TSX CompositeIndex. For other non-U.S. securities we expect the stock to perform within 10% (plus or minus) of the MSCI World Index. AHold rating is also used for yield-sensitive securities where we are comfortable with the safety of the dividend, but believe thatupside in the share price is limited.

SELL -For U.S. securities we expect the stock to underperform the S&P 500 by more than 10% over the next 12 months andbelieve the stock could decline in value. For Canadian securities we expect the stock to underperform the S&P/TSXComposite Index by more than 10% over the next 12 months and believe the stock could decline in value. For other non-U.S.securities we expect the stock to underperform the MSCI World Index by more than 10% over the next 12 months andbelieve the stock could decline in value.

Of the securities we rate, 47% are rated Buy, 50% are rated Hold, and 3% are rated Sell.

Within the last 12 months, Stifel or an affiliate has provided investment banking services for 16%, 7% and 3% of thecompanies whose shares are rated Buy, Hold and Sell, respectively.

Additional Disclosures

Please visit the Research Page at www.stifel.com for the current research disclosures and respective target pricemethodology applicable to the companies mentioned in this publication that are within Stifel's coverage universe. For adiscussion of risks to target price please see our stand-alone company reports and notes for all Buy-rated stocks.

The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us and isnot a complete summary or statement of all available data, nor is it considered an offer to buy or sell any securities referred toherein. Opinions expressed are subject to change without notice and do not take into account the particular investmentobjectives, financial situation or needs of individual investors. Employees of Stifel or its affiliates may, at times, release writtenor oral commentary, technical analysis or trading strategies that differ from the opinions expressed within. Past performanceshould not and cannot be viewed as an indicator of future performance.

Stifel is a multi-disciplined financial services firm that regularly seeks investment banking assignments and compensationfrom issuers for services including, but not limited to, acting as an underwriter in an offering or financial advisor in a merger oracquisition, or serving as a placement agent in private transactions. Moreover, Stifel and its affiliates and their respectiveshareholders, directors, officers and/or employees, may from time to time have long or short positions in such securities or inoptions or other derivative instruments based thereon.

These materials have been approved by Stifel Europe Limited, authorized and regulated by the Financial Conduct Authority(FCA) in the UK, in connection with its distribution to professional clients and eligible counterparties in the EuropeanEconomic Area. (Stifel Europe Limited home office: London +44 20 7557 6030.) No investments or services mentioned areavailable in the European Economic Area to retail clients or to anyone in Canada other than a Designated Institution. Thisinvestment research report is classified as objective for the purposes of the FCA rules. Please contact a Stifel entity in yourjurisdiction if you require additional information.

Additional Information Available Upon Request

Page 14

Market StrategyNovember 6, 2013

© 2013 Stifel, Nicolaus & Company, Incorporated, One South Street, Baltimore, MD 21202.© 2013 Stifel Nicolaus Canada Inc. 79 Wellington Street West, 21st Floor Toronto, ON M5K 1B7.All rights reserved.

Page 15

Market StrategyNovember 6, 2013