© healthpass 20111 how health insurance exchanges will affect employers and health plans shawn...

TRANSCRIPT

© HealthPass 2011 1

How Health Insurance Exchanges Will Affect Employers and Health PlansShawn Nowicki, MPHDirector, Health PolicyHealthPass | New York Business Group on Health

A Presentation for the National Congress on Health Insurance Reform Pre-Conference on Health Insurance Exchanges

Ritz-Carlton Hotel, Washington, DCJanuary 19, 2011

© HealthPass 2011 2

1. About HealthPass

2. How Exchanges Affect Employers

3. How Exchanges Affect Health Plans

4. Questions

Today’s Agenda

© HealthPass 2011 3

About HealthPass New York

© HealthPass 2011 4

• Commercial health insurance exchange started in 1999

• Joint collaboration between:– Northeast Business Group on Health– Mayor’s Office of the City of New York– Health insurance industry

• Missions:– Grant small businesses greater access to healthcare– Help stem the tide of the working uninsured

A Commercial Health Insurance Exchange for NY Small Businesses

© HealthPass 2011 5

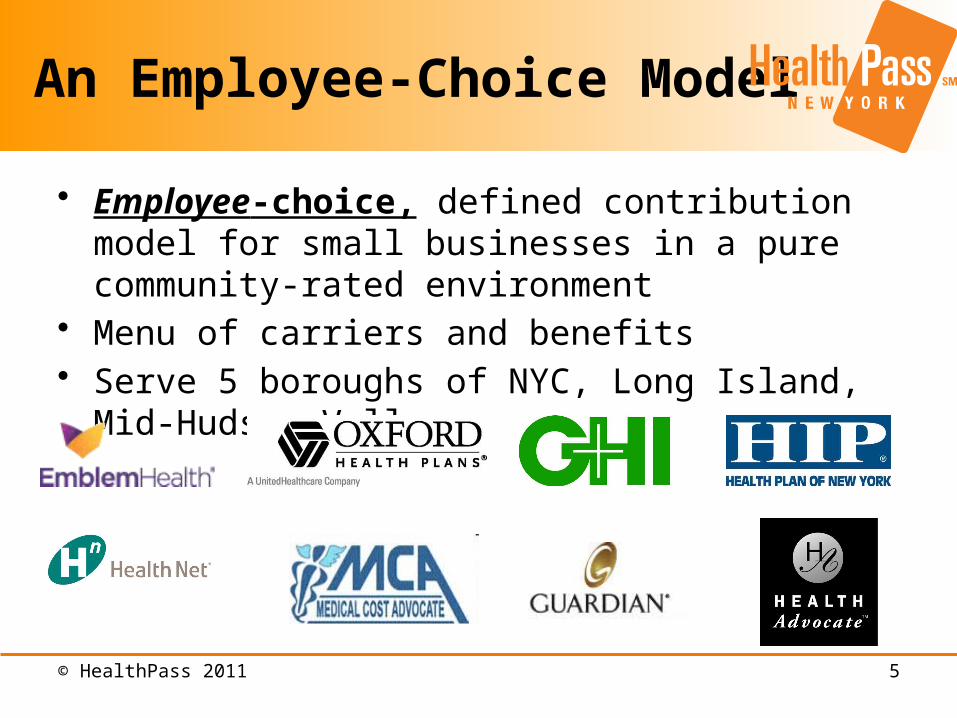

An Employee-Choice Model

• Employee-choice, defined contribution model for small businesses in a pure community-rated environment

• Menu of carriers and benefits• Serve 5 boroughs of NYC, Long Island, Mid-Hudson Valley

© HealthPass 2011 6

How Exchanges Affect Employers

© HealthPass 2011 7

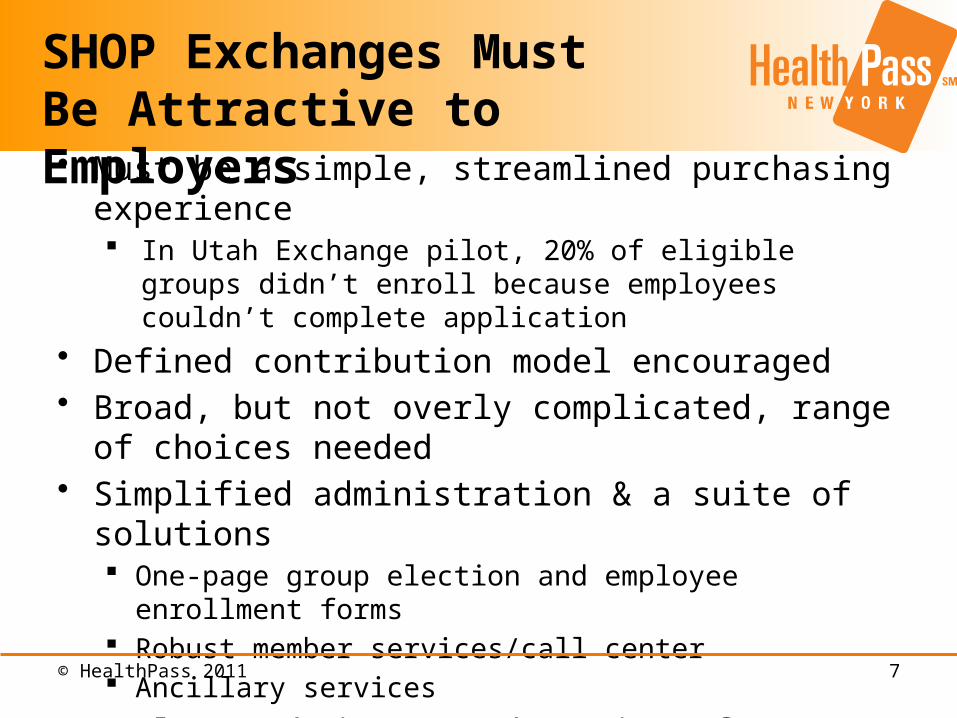

• Must be a simple, streamlined purchasing experience In Utah Exchange pilot, 20% of eligible groups didn’t enroll

because employees couldn’t complete application • Defined contribution model encouraged• Broad, but not overly complicated, range of choices needed• Simplified administration & a suite of solutions

One-page group election and employee enrollment forms Robust member services/call center Ancillary services

• Employee choice (at the point of enrollment) Relieves employer from choosing coverage plan that may or may

not fit employees’ needs and budget

SHOP Exchanges Must Be Attractive to Employers

© HealthPass 2011 8

Exchange Must Streamline Health Benefits Services

ROBUST ADMINISTRATIVE SERVICES

In-House Member Services

COBRA & State Continuation

Admin.

Premium Aggregation & Monthly

Consolidated “List” Billing

Section 125 for Pre-Tax Premium

Contributions

Eligibility Determination

Enrollment &

Subsequent Employer

and Employee Education

S i z e o f s m a l l b u s i n e s s c o r r e l a t e d w i t h H R c a p a b i l i t y

© HealthPass 2011 9

Choice at What Level?

• Mirrors individual exchange options• Small ERs offer cost-sharing options outside of

Exchange (e.g., HDHP/HSA vs. traditional plan)

FULL/BROAD EMPLOYEE CHOICE

ACROSS TIERS

• Explicit option in Affordable Care Act• Enjoys some support because of adverse risk selection

concerns

WITHIN EMPLOYER-DESIGNATED PRECIOUS

METAL TIER

• Traditional method of employer-sponsored coverage• However, system needs to move to individual,

employee choiceEMPLOYER CHOICE

Defined fixed-dollar employer contribution recommended across all options

DE

SIR

AB

ILIT

Y

© HealthPass 2011 10

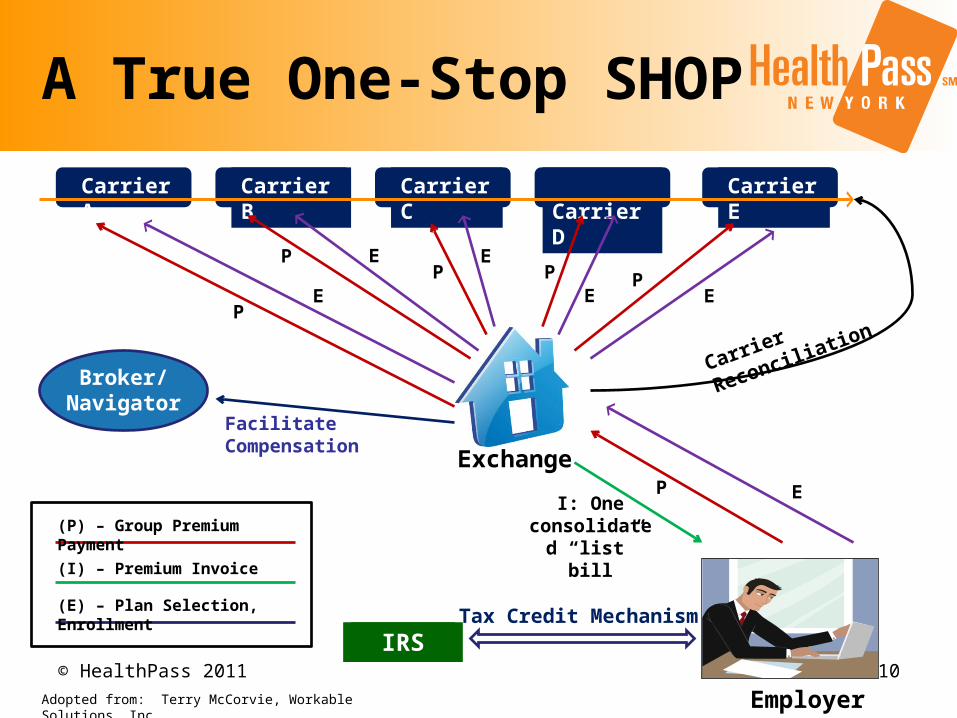

A True One-Stop SHOP

Exchange

Employer

Carrier A Carrier B Carrier C Carrier D Carrier E

Broker/ Navigator

IRSTax Credit Mechanism

(P) – Group Premium Payment

(E) – Plan Selection, Enrollment

(I) – Premium Invoice

I: One consolidated

“list” bill

P E

Facilitate Compensation

P

PP P P

EE

EE

E

Carrier Reconciliation

Adopted from: Terry McCorvie, Workable Solutions, Inc.

© HealthPass 2011 11

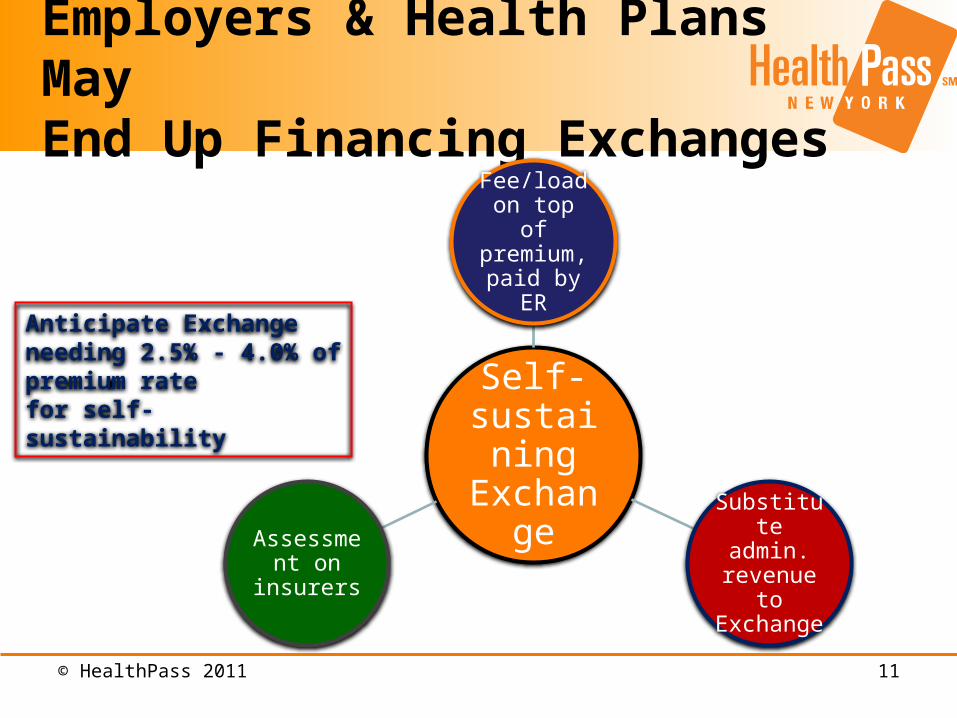

Employers & Health Plans May End Up Financing Exchanges

Self-sustaining Exchange

Fee/load on top of

premium, paid by ER

Substitute admin.

revenue to Exchange

Assessment on insurers

Anticipate Exchange needing 2.5% - 4.0% of premium rate for self-sustainability

© HealthPass 2011 12

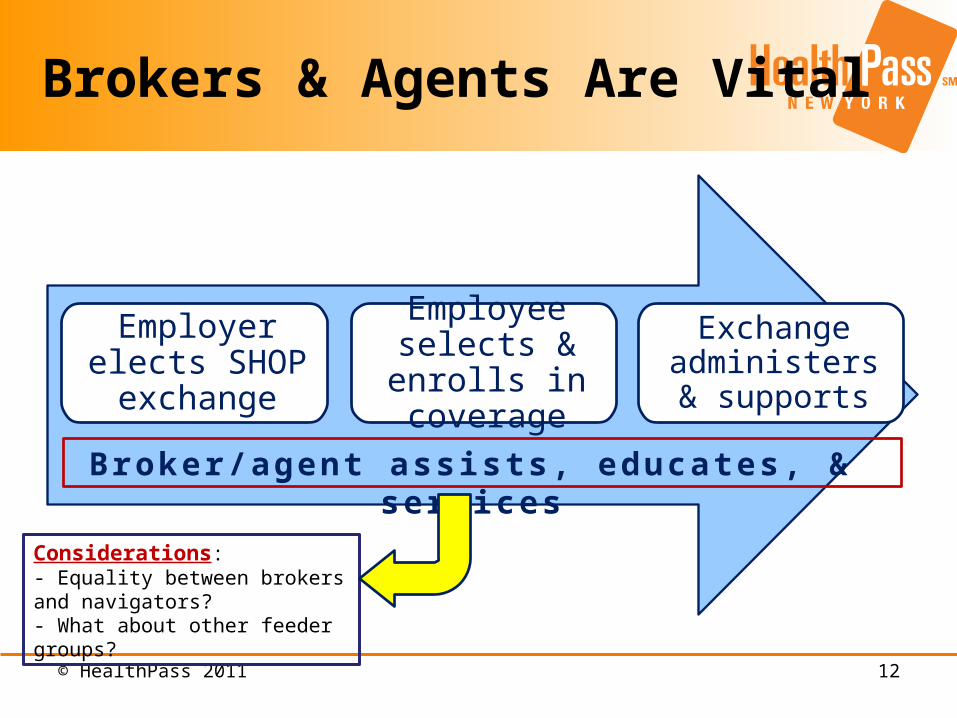

Brokers & Agents Are Vital

Employer elects SHOP exchange

Employee selects & enrolls in

coverage

Exchange administers &

supports

Considerations: - Equality between brokers and navigators? - What about other feeder groups?

B r o ke r /a g e n t a s s i s t s , e d u c a t e s , & s e r v i c e s

© HealthPass 2011 13

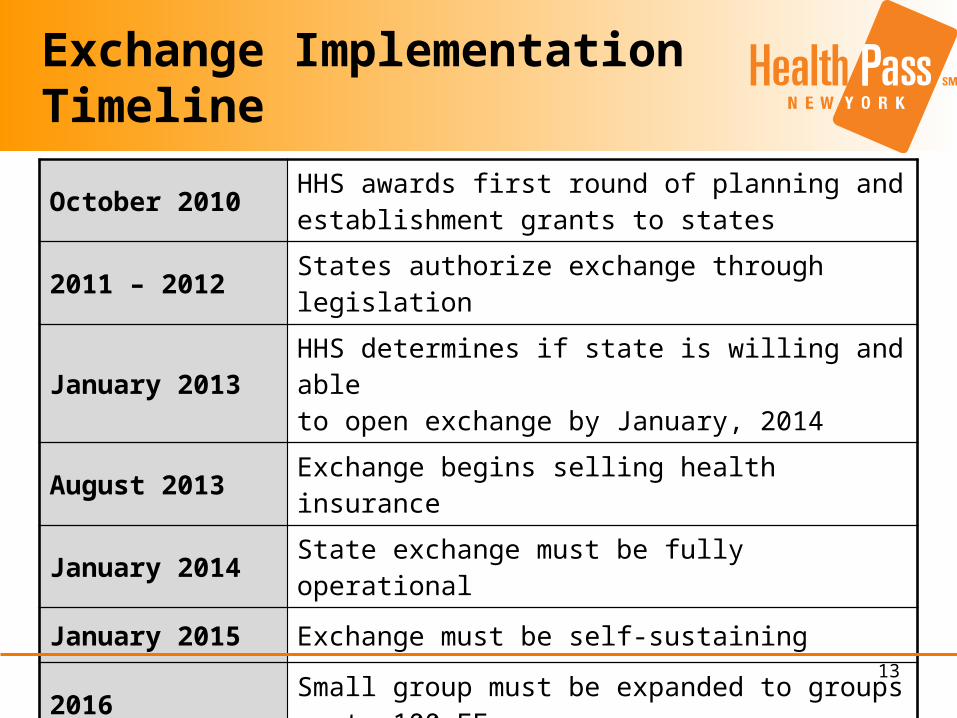

Exchange Implementation Timeline

October 2010 HHS awards first round of planning and establishment grants to states

2011 – 2012 States authorize exchange through legislation

January 2013 HHS determines if state is willing and able to open exchange by January, 2014

August 2013 Exchange begins selling health insurance

January 2014 State exchange must be fully operational

January 2015 Exchange must be self-sustaining

2016 Small group must be expanded to groups up to 100 EEs

2017 State may open exchange to large groups (>100 EEs)

© HealthPass 2011 14

Employer & Employee Benefits

Employer Benefits

• No need to pick one plan for different employees• Curbs wasted healthcare spending• Helps to attract and retain key employees• Empowers employees to participate in making informed healthcare decisions• Defined contribution sets a benefits budget• Simplified administration• Robust client support • Home billing of COBRA and COBRA administration• No need to shop for insurance every year

Employee Benefits• A voice in a personal decision – healthcare • Choice of plan types (e.g., HMO, EPO, POS, PPO, HSA)• Choice of insurer• Annual choice to meet individual healthcare and budget requirements• Pre-Tax contributions (thru Section 125) minimize out of pocket costs• Robust member and advocacy services

© HealthPass 2011 15

How Exchanges Affect Health Plans

© HealthPass 2011 16

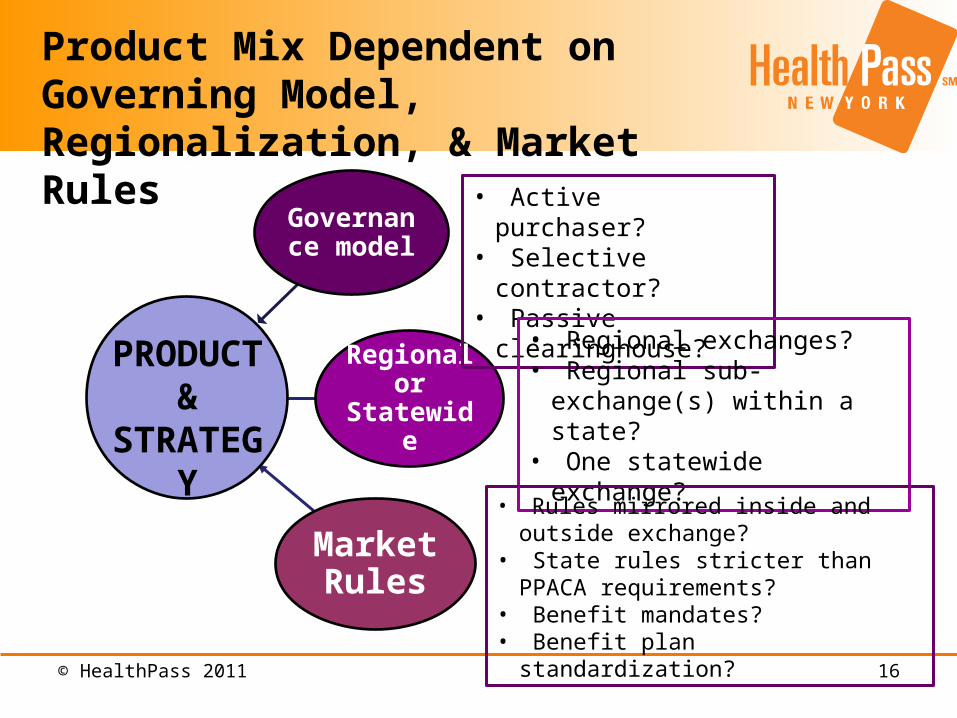

Product Mix Dependent on Governing Model, Regionalization, & Market Rules

Governance model

Regional or Statewide

Market Rules

PRODUCT &

STRATEGY

• Active purchaser?• Selective contractor?• Passive clearinghouse?

• Regional exchanges?• Regional sub-exchange(s) within

a state?• One statewide exchange?

• Rules mirrored inside and outside exchange?

• State rules stricter than PPACA requirements?

• Benefit mandates?• Benefit plan standardization?

© HealthPass 2011 17

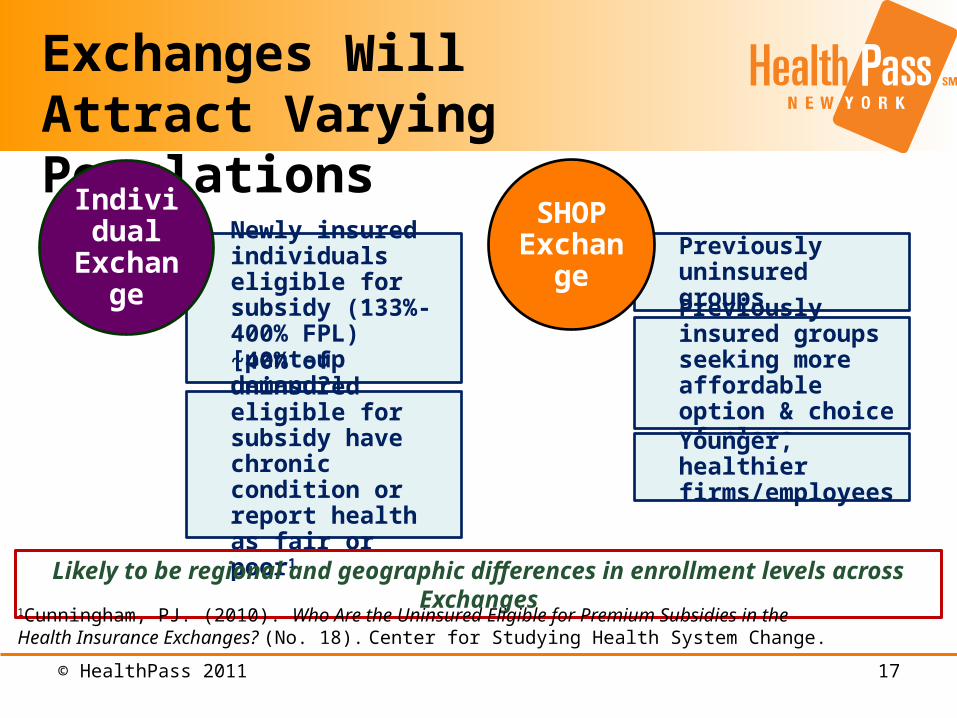

Exchanges Will Attract Varying Populations

Newly insured individuals eligible for subsidy (133%-400% FPL) [pent-up demand?]

~40% of uninsured eligible for subsidy have chronic condition or report health as fair or poor1

Individual Exchange Previously uninsured

groups

Previously insured groups seeking more affordable option & choice of plans

Younger, healthier firms/employees

SHOP Exchange

Likely to be regional and geographic differences in enrollment levels across Exchanges

1Cunningham, PJ. (2010). Who Are the Uninsured Eligible for Premium Subsidies in the Health Insurance Exchanges? (No. 18). Center for Studying Health System Change.

© HealthPass 2011 18

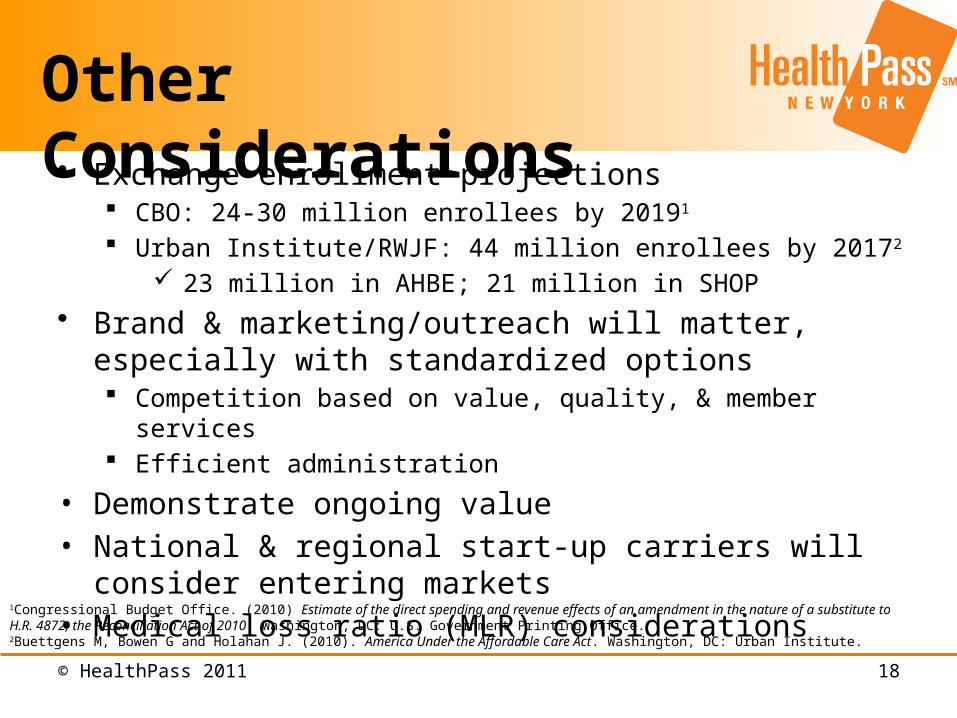

• Exchange enrollment projections CBO: 24-30 million enrollees by 20191

Urban Institute/RWJF: 44 million enrollees by 20172

23 million in AHBE; 21 million in SHOP• Brand & marketing/outreach will matter, especially with

standardized options Competition based on value, quality, & member services Efficient administration

• Demonstrate ongoing value• National & regional start-up carriers will consider entering markets• Medical loss ratio (MLR) considerations

Other Considerations

1Congressional Budget Office. (2010) Estimate of the direct spending and revenue effects of an amendment in the nature of a substitute to H.R. 4872, the Reconciliation Act of 2010. Washington, DC: U.S. Government Printing Office.2Buettgens M, Bowen G and Holahan J. (2010). America Under the Affordable Care Act. Washington, DC: Urban Institute.

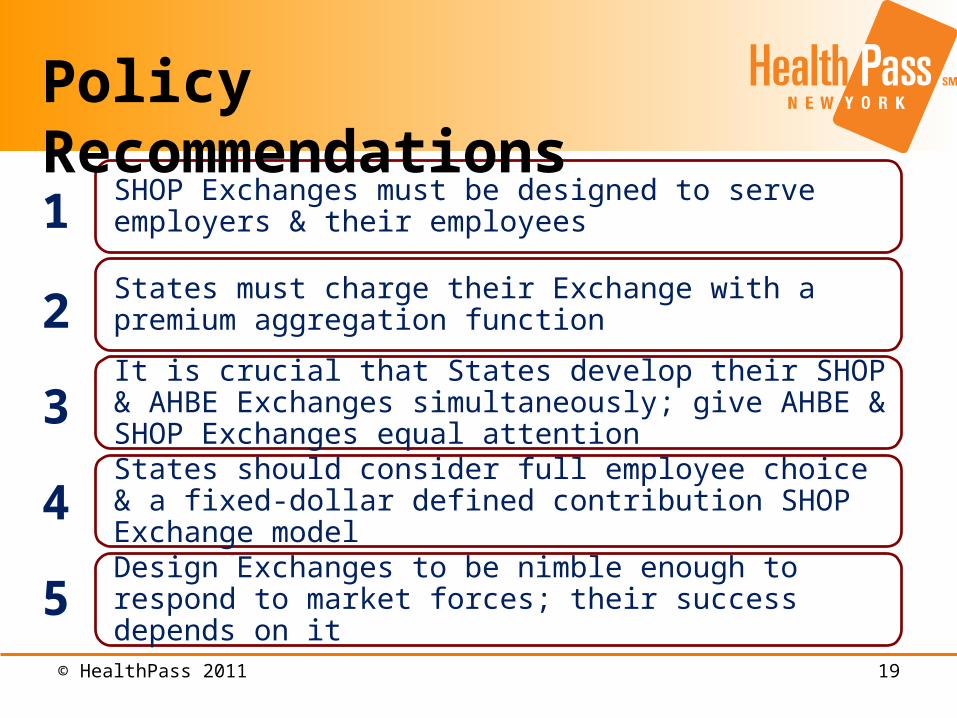

© HealthPass 2011 19

SHOP Exchanges must be designed to serve employers & their employees

States must charge their Exchange with a premium aggregation function

It is crucial that States develop their SHOP & AHBE Exchanges simultaneously; give AHBE & SHOP Exchanges equal attention

States should consider full employee choice & a fixed-dollar defined contribution SHOP Exchange model

Design Exchanges to be nimble enough to respond to market forces; their success depends on it

Policy Recommendations

1

2

3

4

5

© HealthPass 2011 20

Questions

Q & A

© HealthPass 2011 21

Contact Information

Shawn Nowicki, MPHDirector, Health Policy

61 BroadwaySuite 2705(212) 252-8010 [email protected]