- kuwait enterprise risk management …kuwaiterm.com/ppt/18-tony_milsom.pdf · ·...

TRANSCRIPT

www.kuwai term.com

TONY MILSOM Specialist – Risk

Engineering

KPC

Quantitative Risk Management

Methods, Techniques and Tools

w w w. k u w a i t e r m . c o m

KPC ERM Objectives:

SOURCE: Team analysis

Three key objectives of KPC’s risk journey

Achieve high certainty that the oil sector will meet

the expectations of the State

Enable the oil sector to make a more fact-based and

quantitative assessment of risk vs. return trade-offs

in its activities and projects

Ensure the availability of adequate funding to

support oil sector capital expenditure

6

Risk modeled and

have effect

KCo1 KCo2 KCo3 KCo4 KCo5 KCo6 KCo7 KCo8 KCo9

7b HR and HSSE – Labor disruptions

6d Retail margin volatility

5d Charter rates

9 New technologies

7a HR and HSSE - Manpower

8b Operational - Sabotage

10 Unexpected drop in reserves

1 Domestic political influence

2 Regional instability

3 Project execution

4 Hydrocarbon market disruption

5a Crude price volatility

5b Gas price volatility

5c Interest rate volatility

6a FX volatility

6b Refining margin volatility

6c Petrochemical price volatility

6e Counter-party credit risk

8a Operational - Production

Risk

SOURCE: Team Analysis

The top ten risks for KPC were identified and

mapped to each of the K-Cos

KPC

1400 risks from risk

registers

were considered

9

KPMs help measure success of these directives…. KPC’s strategic directives (not exhaustive)…

Upstream

▪ Increase crude production to

4.0 mmbpd by 2020

▪ Increase non-assoc. gas prod.

capacities to 2.1 BSCF/d by

2020

▪ …

Downstream

▪ Grow domestic refining capacity

to 1.4 mmbpd (new built) and

subsequent 1,6 mmbpd

(enhancement of facilities)

▪ Increase refining complexity

▪ …

Midstream

and others

▪ Human Capital attraction and

retention

▪ …

Production/

capacity

▪ Free gas production

▪ Proven reserves

▪ …

Costs

▪ Cost of risk

▪ R&T spend vs. plan

▪ …

HSEE

▪ Fatal cases

▪ Environmental incidents

▪ …

Kuwaitization

and stake-

holders

▪ Percentage of Kuwaitis in KPC ▪ Share of Capex spent locally ▪ …

Profitability

▪ Profit margin

▪ ROACE

▪ …

▪ Strategic project risk

▪ Political/regulatory

▪ Operational/technical

▪ Portfolio/business risk

▪ Financial risks (counterparty,

liquidity, market)

Ability to attain targets on KPMs are influenced by multiple risks

Risk modeling aims to increase transparency and

improve decision making

12

13

Cash flow at risk model

Model top risk effects via quantitative risk model

Price Technical

Political

▪ Capex

▪ Production disruption

▪ Tax changes

▪ Nationalization

Company-by-

company profiles

▪ Production

▪ Capex

▪ Opex

LOX-ZZV233-20061123-MHDC

13

Working D

raft -Last M

odified 11/24/2006 4:22:00 AM

Industry has a limited set of project growth options. We characterised

these with 28 projects covering 75% of industry growth potential

Russia non-PSC

Norway oil

GoM DW

Canada oil sand

NOC bonusbuyback

Mid East GTL

Angola DW

U.K. oil

Nigeria DW

Oman oil

Mid East LNG

Malaysia DW

U.K. gas

US onshore gas

NA Arctic gas

Mexico DWCentral

Africa OilNOC

redevelopment

OECD Frontier

Exploration

Non-OECD

Frontier

Exploration

NA Steam flood

Estimated 75% of future

hydrocarbon resource

types modelled

Source: USGS; McKinsey

$35

04080

120

$55 Forward Curve

Growth projects/Strategic initiatives

Company portfolio

Risk assessment

Quantitative risk model

SOURCE: McKinsey Risk Practice

Project valuation model

Risk return portfolio

model

13

Refining

capacity

Risk measures

▪ Annual crude capacity

Financial

risk

measures ▪ Annual cash flow to both Kuwaiti government and KPC (remaining cash flow share)

Gas

production

▪ Annual associated and non-associated gas production

Crude

capacity

▪ Annual refining capacity

Probability distribution variable

Stakeholder

and KPC cash

flow

Cash flow

for KPC and

Subsidiaries

▪ Annual cash flow for next year(s) (operating cash flow)

Non-

financial

risk

measures

Risk measures chosen on

the basis of KPC and K-

Companies KPMs

▪ For financial KPMs (e.g.,

ROACE), cash flow

identified as main driver

of uncertainty

▪ For non-financial KPMs,

production and capacity

levels identified as most

impactful factors

The impact of risks is assessed by five key measures in

line with the business KPM’s

14

Risk Modeling

15

Each K Company has it’s own risk model; output measures

risks modelled both in deterministic and stochastic cases

SOURCE: Team analysis; expert interviews; k-company working teams

War/political scenario

Project delays

Oil price

Relevant risk factors

▪ All relevant risks modelled for all

K Companies

▪ Focused risks modelled in detail

for K Companies

▪ Deviation from base case due to

each of these risks modelled

separately

Financial models

▪ All 9 K companies deterministic

financial cash flows is modelled

▪ For each of these deterministic, the

impact of all relevant risks modelled

separately for output

…

KPI

KNPC

KOC

Model output

Financial Non-financial

▪ Cash flow

distribution (by

each risk type

for each K

Company)1

▪ Varies by K

company

▪ For KGOC and

KOC

– Oil capacity

– Gas

production

▪ For KNPC

– Refining

capacity

1 While we calculate cumulative cash flows, we will use discount rate as follows – 0% for next 5 years, 10% for remaining 15 years/there after

17

Model provides cash flow from operation over time and

as a cumulative distribution

SOURCE: K-Company CFAR model – illustrative example. Team analysis

20YY +3 +2 +1 20XX

Mean Baseline 95th

5th

Mn KD

Yearly cash flow from operations

(20XX-20YY)

5th 95th Mean

Cumulative operating five year cash

flow (20XX-20YY)

Model can also calculate

deviation from baseline for

production volumes

Pro

bab

ilit

y

Cash flow

Cash

flo

w

x y z

Illustrative

Baseline

18

Rank risks based on contribution to total cash flow at

risk, and quantifies diversification effect

Cash Flow @ Risk =

Baseline – 5th Percentile Risks

Total

Diversification

HSSE and HR risks

Operational risks

Refining/petrochemical prices

New technologies risks

Large project execution risks

External influence on

key decisions

Global crude/gas price volatility Remarks

▪ Baseline refers to

currently projected

cash flows from the 5

Year plan

▪ Diversification results

from low or negative

correlation of various

individual risks leading

to total risk lower than

sum of individual risks

SOURCE: K-Company CFAR model – illustrative example. Team analysis

5 year cash flows (20XX-YY) Illustrative

19

Risk Modeling Strategic Projects

20

Current project appraisal approach with a

probabilistic risk view

From deterministic … … to probabilistic

3 2 1

Future value

Frequency of occurrence in simulation

3

2 1 High

case Base

Case

Low

case

▪ Discrete scenarios with no associated

understanding of probability of

occurrence

▪ Scenarios based on “intuitive”

assessment – bias likely in selection

▪ Fat tail risks often ignored

▪ Fact based assessment of full range of

outcomes with associated probabilities

▪ Removes bias towards “most likely

scenario”

▪ Quantify potential downsides and

upsides at appropriate probability

21

The risk-return quantification methodology adds probabilistic

metrics on top of the current appraisal and strategic metrics

SOURCE: Team analysis

▪ Stress-test expected economic performance of the project

▪ Prioritize and assess magnitude of key risks to focus mitigation actions

▪ Estimate likelihood of project success and the underlying value to the organization

Return

metrics

Time metrics

Sensitivity/

Scenarios

Value metrics

Additional risk-adjusted metrics

introduced by the methodology

Metrics currently used for

program appraisal1

▪ Expected IRR

▪ RAROC (Risk adjusted return on capital)

▪ IRR

▪ Profitability index

▪ Expected payback period ▪ Payback period

▪ NPV at risk (NPVaR)

▪ Probabilities

– To breakeven

– To meet baseline

▪ Sensitivity of NPV to

– CAPEX overrun

– Oil price

– Project delay

▪ Scenarios

▪ Expected NPV ▪ NPV

1 Using base case assumptions

23

Ranking N

… and informs decision making at portfolio level ILLUSTRATIVE

Technology

22

8

12

17

17

22

20

54

13

2

9

8

6

5

3

4

1

7

158

75

85

53

30

55

50

145

35

!

!

Expected NPV

KD million

I

A

B

C

D

E

F

G

H

Site

New Prioritization

NPV/(Inv+NPVatRisk) (%)

5

9

8

2

6

3

4

1

7

Old Prioritization

NPV/investment (%)

31

15

19

48

23

37

33

97

19

SOURCE: McKinsey Risk Practice 26

Overview of risk-based economics for project

Key metrics

▪ IRR, % 13 10%

▪ Payback period, year 10 tbd

▪ NPVaR, KD B1-P5

▪ Prob. to breakeven, % 70% tbd

▪ NPV/I, % >0

24% ▪ Prob. to meet baseline, % tbd

▪ Profitability index 1.88 >1

E1 ▪ NPV, KD

Min

Required

Expected

metrics

NPV distribution, KD

Key risks

Key risks

NPVaR,

KD

Contribution,

Percent

0

NPVaR = B1-P5

Expected

NPV Baseline

Observations

▪ Difference between baseline NPV and expected NPV, mainly driven

by crude price, results in a lower probability to meet the baseline

▪ Probability to breakeven implying that the project is likely to be

profitable

▪ Large NPVaR brings down expected return on capital after risk

adjustment

E1 B1 (P5)

24%

5th

percentile

10

9

1.8

B1

Baseline

metrics

▪ RAROC, % 10% >0

80% Return on

capital

BIGGER ▪ Capex , KD BIG

85%

Breakeven

point

SOURCE: Economic model, team analysis

70%

NPV,

KD

20BB ▪ Commissioning date 20AA

.CCCX ▪ Peak production, tpa CCC2

69

4

20

R4

Execution delay

Feedstock availability

Crude price

Refining margins

Capex overrun

R1

R2

R3

-R5

59

Probability to

meet baseline

Probability to

breakeven

-1

Illustrative Numbers

28

Risk Modeling Strategic Options

30

▪ KPC strategy identifies a set

of strategic initiatives to guide

future investments

Risk based capital allocation

▪ Assess project economics for

each strategic initiative

▪ Integrate risks in the economic

appraisal and generate risk

based metrics

▪ Rank projects based on

RAROC

▪ Prioritize and select projects

given budget constraint

Risk based project appraisal Project selection

Budget

limit

Capex KD mm

RAROC %

2 Project 1 5 3 4

Risk could be integrated in both capital allocation and project

appraisal processes in a consistent way

SOURCE: team analysis

Pre-

requisites

Process

▪ Assess strategic initiatives

on a stand-alone basis

▪ Assess impact of

combinations of strategic

initiatives on KPC portfolio

▪ Pipeline of projects by strategic

initiative, with project economic

model and parameters

▪ Understanding of project risks

▪ Pipeline of projects for a

strategic initiative, with risk

based economic assessment

▪ Budget allocated to initiative

Outcome

▪ Risk based project economic

metrics including RAROC

▪ Suggested list of projects for

approval within a strategic

initiative

▪ Allocated budget for each

strategic initiative and/or K-

company

1

2

31

Taking the Stakeholder perspective can significantly

change the risk-return profile of strategic options

SOURCE: Strategic Planning model, team analysis

Stakeholder view

RAROC Less risky strategy

More risky strategy

Alternative option preferable

Preferred option depends

on risk appetite

Preferred option depends on

risk appetite

Current FYP preferable

10.0 9.5 9.0 8.5 8.0 7.5 7.0 6.5 6.0 5.5 5.0 4.5 4.0 3.5 3.0

Value (NPV), KD

Risk (NPVaR), KDmm

Option 6

Option 5

Option 4

Option 3 Option 2

Option 1a

Option 1

(Current plan)

Alternative option

preferable

Preferred option

depends on risk appetite

Preferred option depends on risk

appetite

Current FYP preferable

Value creation of strategic options on portfolio

RAROC Less risky strategy

More risky strategy

KPC view

10 9

Risk (NPVaR), KDmm

Option 6

Option 5 Option 4

Option 3

Option 2

Option 1a Option 1

(Current plan)

Value (NPV), KD

Illustrative

33

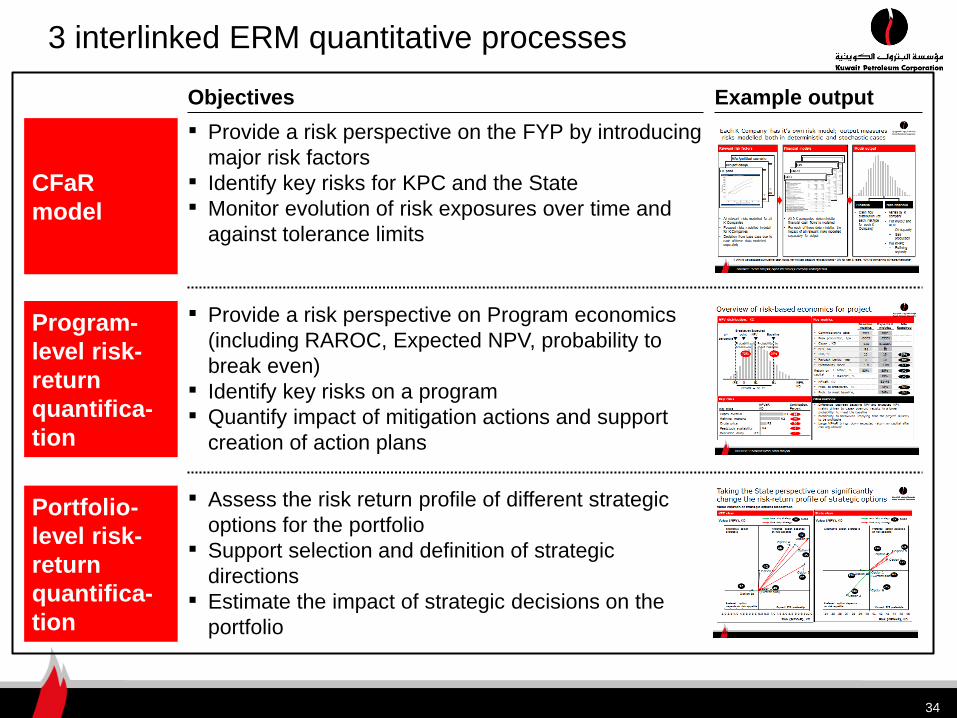

3 interlinked ERM quantitative processes

Objectives Example output

CFaR

model

▪ Provide a risk perspective on the FYP by introducing

major risk factors

▪ Identify key risks for KPC and the State

▪ Monitor evolution of risk exposures over time and

against tolerance limits

▪ Provide a risk perspective on Program economics

(including RAROC, Expected NPV, probability to

break even)

▪ Identify key risks on a program

▪ Quantify impact of mitigation actions and support

creation of action plans

Program-

level risk-

return

quantifica-

tion

▪ Assess the risk return profile of different strategic

options for the portfolio

▪ Support selection and definition of strategic

directions

▪ Estimate the impact of strategic decisions on the

portfolio

Portfolio-

level risk-

return

quantifica-

tion

34

By the end of the ERM journey KPC will be a much

more effective organisation

A much deeper understanding of major risks and how they affect the

businesses and Oil sector's ability to implement the 2030 strategy

Concrete materials with quantification of the risks improving ability to

engage the stakeholders in an informed manner

Attention drawn towards the extreme tail risks facing the oil sector

Suitable leading risk indicators and a good understanding how to

quantify and assess the impact of range of mitigation options

Ability to evaluate the investment portfolio from a risk adjusted point of

view to create increased organizational value both at a KPC level and

individual K-co level

Effective management tools to support better decision making

35