© lakshmikumaran & sridharan, 2011 1 1 ‘ scope of taxation and issues’ -n. mathivanan

TRANSCRIPT

© Lakshmikumaran & Sridharan, 2011

1 1

‘ SCOPE OF TAXATION AND ISSUES’

-N. MATHIVANAN

© Lakshmikumaran & Sridharan, 2011

2

BUSINESS SUPPORT SERVICES

1

2

2

COVERAGE

BUSINESS AUXILARY SERVICES

© Lakshmikumaran & Sridharan, 2011

3

BUSINESS AUXILARY SERVICES

© Lakshmikumaran & Sridharan, 2011

4

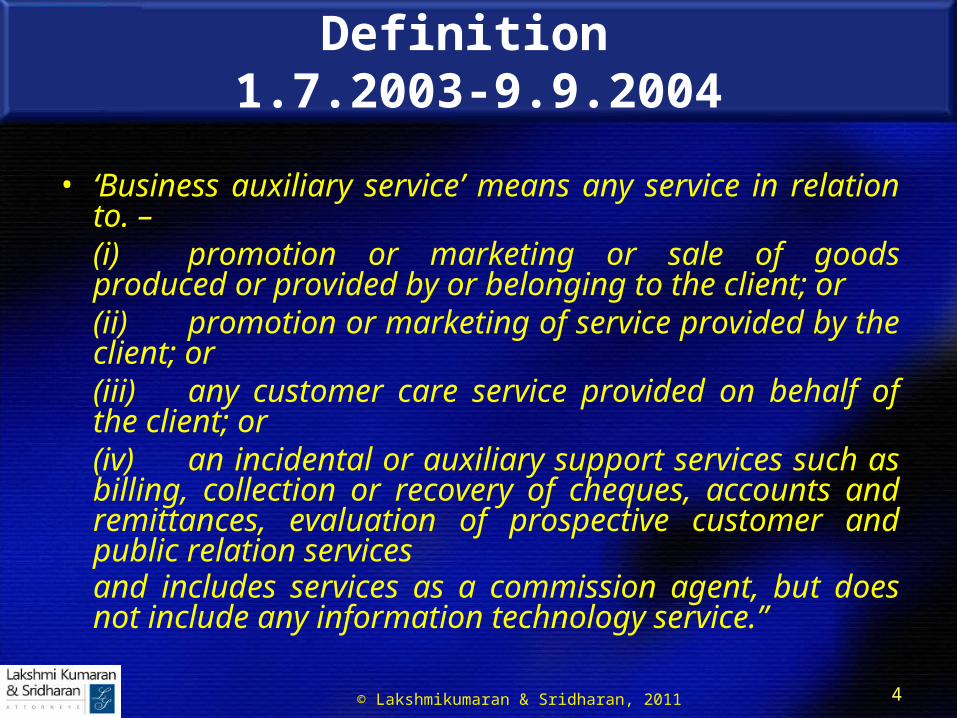

Definition 1.7.2003-9.9.2004

• ‘Business auxiliary service’ means any service in relation to. –(i) promotion or marketing or sale of goods produced or provided by or belonging to the client; or(ii) promotion or marketing of service provided by the client; or(iii) any customer care service provided on behalf of the client; or(iv) an incidental or auxiliary support services such as billing, collection or recovery of cheques, accounts and remittances, evaluation of prospective customer and public relation servicesand includes services as a commission agent, but does not include any information technology service.”

© Lakshmikumaran & Sridharan, 2011

5

Definition 10.9.2004 -15.6.2005

• “65(19)“business auxiliary service” means any service in relation to, —(i) promotion or marketing or sale of goods produced or provided by or belonging to the client; or(ii) promotion or marketing of service provided by the client; or (iii) any customer care service provided on behalf of the client; or (iv) procurement of goods or services, which are inputs for the client; or (v) production of goods on behalf of the client; or(vi) provision of service on behalf of the client; or(vii) a service incidental or auxiliary to any activity specified in sub-clauses (i) to (vi), such as billing, issue or collection or recovery of cheques, payments, maintenance of accounts and remittance, inventory management, evaluation or development of prospective customer or vendor, public relation services, management or supervision,and includes services as a commission agent, but does not include any information technology service and any activity that amounts to “manufacture” within the meaning of clause (f) of section 2 of the Central Excise Act, 1944 (1 of 1944).

© Lakshmikumaran & Sridharan, 2011

6

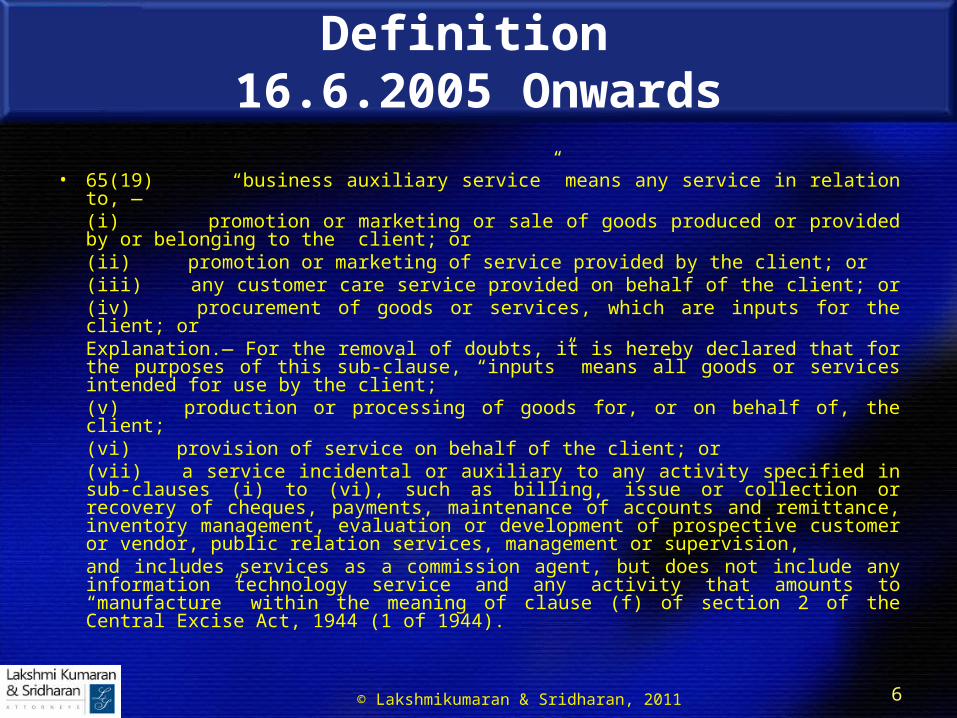

Definition 16.6.2005 Onwards

• 65(19) “business auxiliary service” means any service in relation to, —(i) promotion or marketing or sale of goods produced or provided by or belonging to the client; or(ii) promotion or marketing of service provided by the client; or (iii) any customer care service provided on behalf of the client; or (iv) procurement of goods or services, which are inputs for the client; orExplanation.— For the removal of doubts, it is hereby declared that for the purposes of this sub-clause, “inputs” means all goods or services intended for use by the client;(v) production or processing of goods for, or on behalf of, the client;(vi) provision of service on behalf of the client; or(vii) a service incidental or auxiliary to any activity specified in sub-clauses (i) to (vi), such as billing, issue or collection or recovery of cheques, payments, maintenance of accounts and remittance, inventory management, evaluation or development of prospective customer or vendor, public relation services, management or supervision,and includes services as a commission agent, but does not include any information technology service and any activity that amounts to “manufacture” within the meaning of clause (f) of section 2 of the Central Excise Act, 1944 (1 of 1944).

© Lakshmikumaran & Sridharan, 2011

7

Definition 16.6.2009 Onwards

• 65(19) “business auxiliary service” means any service in relation to, —(i) promotion or marketing or sale of goods produced or provided by or belonging to the client; or(ii) promotion or marketing of service provided by the client; or (iii) any customer care service provided on behalf of the client; or (iv) procurement of goods or services, which are inputs for the client; orExplanation.— For the removal of doubts, it is hereby declared that for the purposes of this sub-clause, “inputs” means all goods or services intended for use by the client;(v) production or processing of goods for, or on behalf of, the client;(vi) provision of service on behalf of the client; or(vii) a service incidental or auxiliary to any activity specified in sub-clauses (i) to (vi), such as billing, issue or collection or recovery of cheques, payments, maintenance of accounts and remittance, inventory management, evaluation or development of prospective customer or vendor, public relation services, management or supervision,and includes services as a commission agent, but does not include any information technology service and any activity that amount to “manufacture” of excisable goods.

© Lakshmikumaran & Sridharan, 2011

8

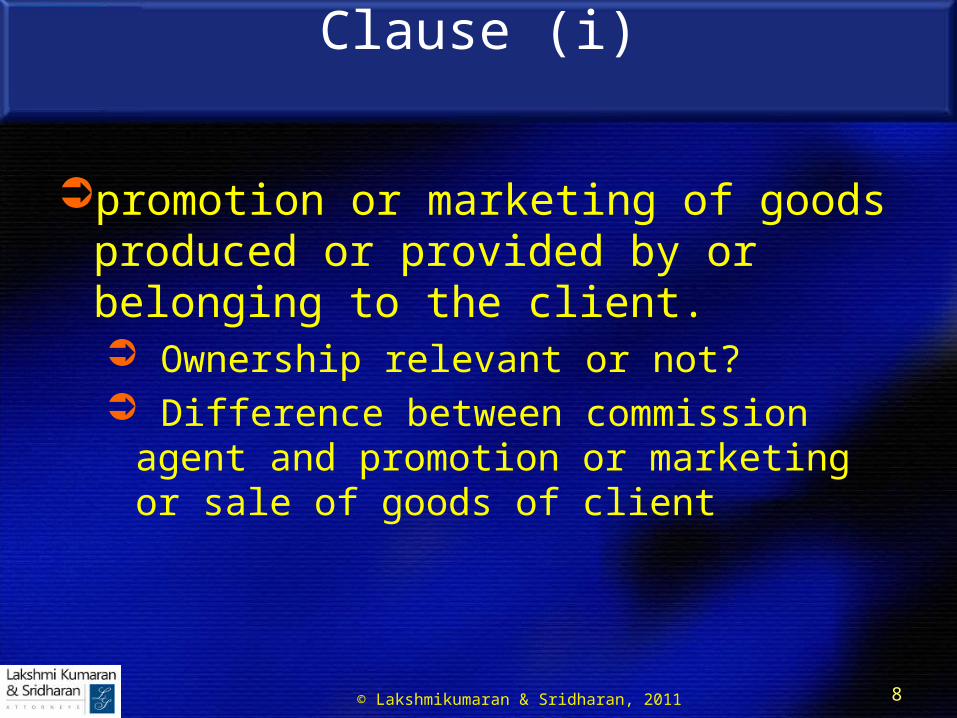

Clause (i)

promotion or marketing of goods produced or provided by or belonging to the client. Ownership relevant or not? Difference between commission agent and

promotion or marketing or sale of goods of client

© Lakshmikumaran & Sridharan, 2011

9

Clause (ii)

Promotion or marketing of services provided by the client. Illustrations:

Jet Lite Sample collection centres {Dr. Lal Path Labs}

© Lakshmikumaran & Sridharan, 2011

10

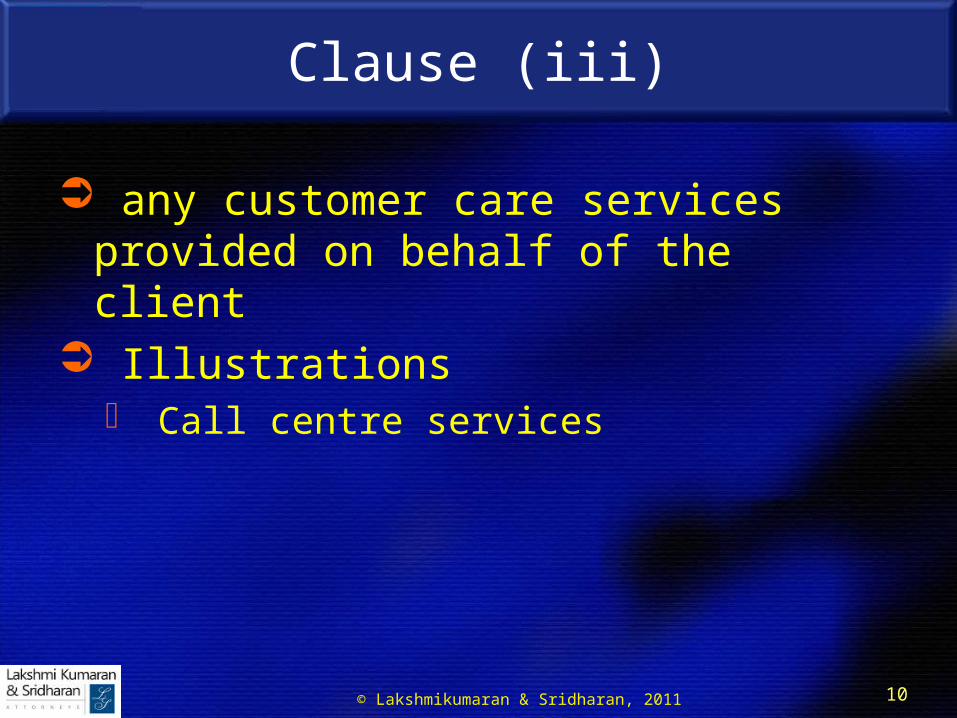

Clause (iii)

any customer care services provided on behalf of the client

Illustrations Call centre services

© Lakshmikumaran & Sridharan, 2011

11

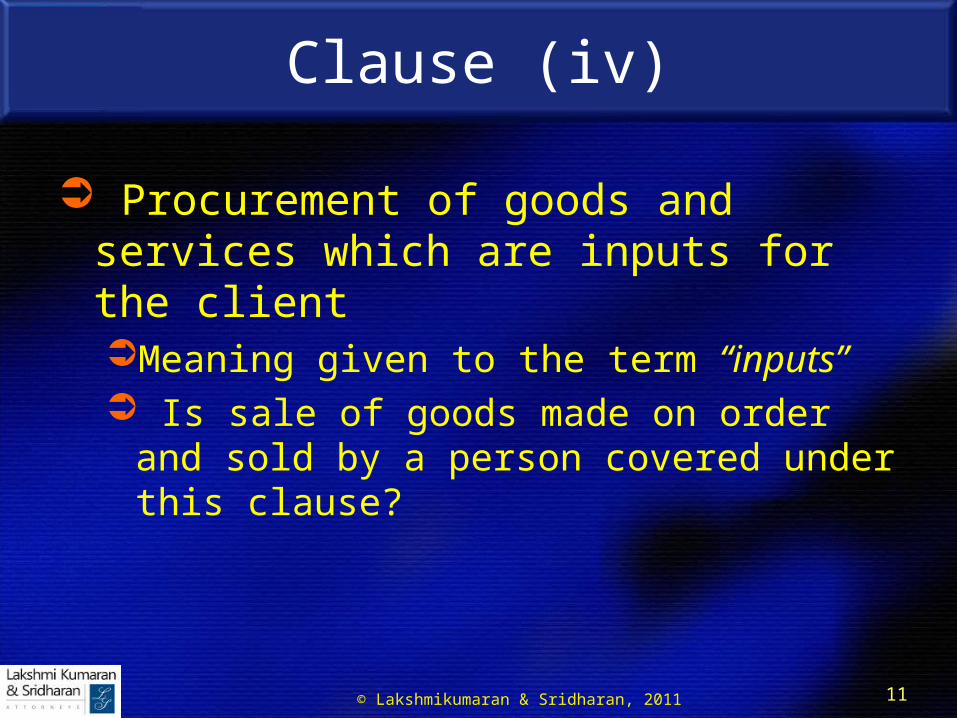

Clause (iv)

Procurement of goods and services which are inputs for the clientMeaning given to the term “inputs” Is sale of goods made on order and sold by a

person covered under this clause?

© Lakshmikumaran & Sridharan, 2011

12

Clause (v)

From 10.9.2004 to 16.6.2005Production of goods on behalf of the client

• Auto coats• Sonic watch

From 16.6.2005Production or processing of goods for, or on

behalf of, the client

© Lakshmikumaran & Sridharan, 2011

13

NOTIFICATION 8/2005-ST

Production or processing of goods for, or on behalf of, the client [clause (v)]

Using raw material/semi finished goods supplied by the client

Goods produced or processed are returned to the clients For use in or in relation to dutiable goods Exempted from the whole of service tax

© Lakshmikumaran & Sridharan, 2011

14

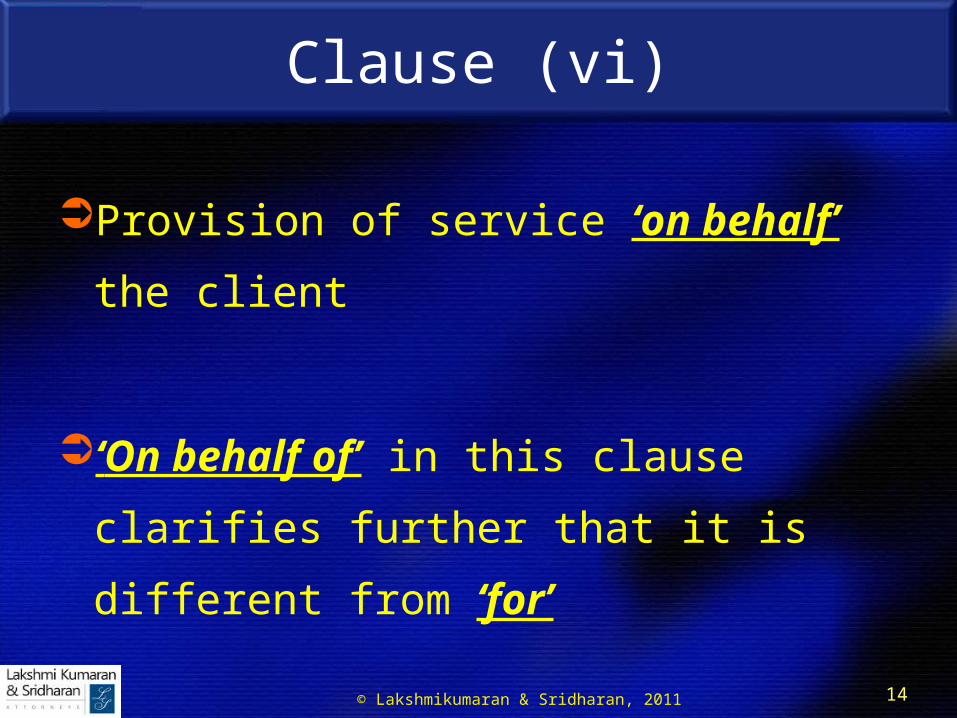

Clause (vi)

Provision of service ‘on behalf’ the client

‘On behalf of’ in this clause clarifies

further that it is different from ‘for’

© Lakshmikumaran & Sridharan, 2011

15

Notification 14/2004[amended vide Notification 19/2005 & 19/2006]

the taxable service provided to a client by any person in relation to the business auxiliary service, has been exempted from the whole of the service tax leviable thereon

under section 66 of the Act in so far as it relates to:

procurement of goods or services, which are inputs for the client; production or processing of goods for, or on behalf of, the client; provision of service on behalf of the client; or a service incidental or auxiliary to the above specified services

and provided in relation to agriculture, printing, textile processing or education.

© Lakshmikumaran & Sridharan, 2011

16

Amendment vide Finance Act 2009

But does not include any activity that amounts to

‘manufacture’ within the meaning of clause (f) of section

2 of the Central Excise Act, 1944.

But does not include manufacture of any ‘excisable

goods’

© Lakshmikumaran & Sridharan, 2011

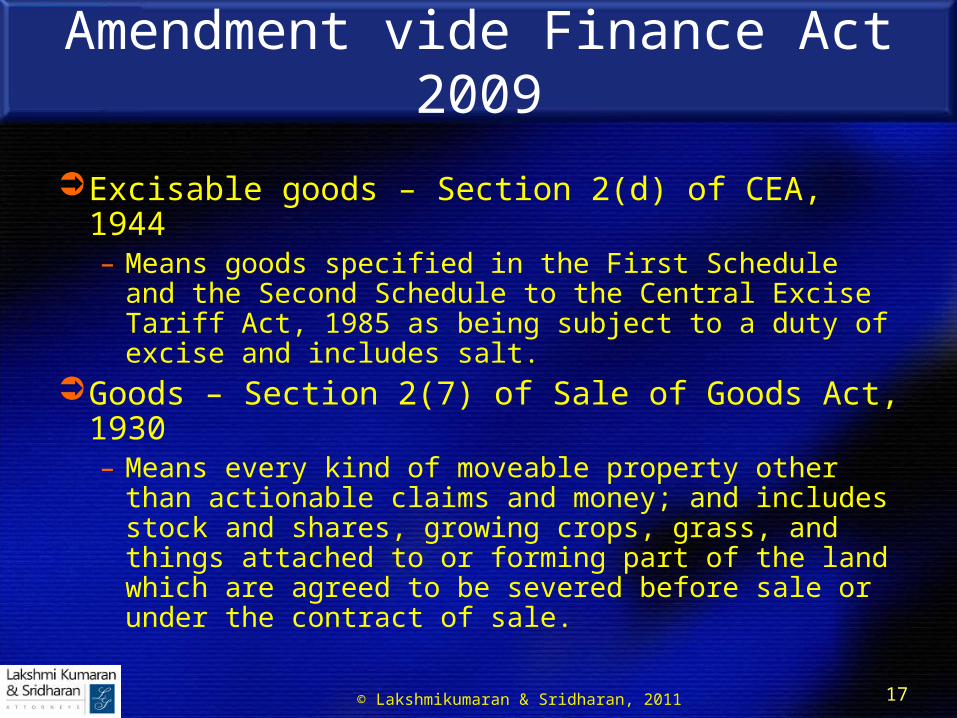

17

Amendment vide Finance Act 2009

Excisable goods – Section 2(d) of CEA, 1944– Means goods specified in the First Schedule and the

Second Schedule to the Central Excise Tariff Act, 1985 as being subject to a duty of excise and includes salt.

Goods – Section 2(7) of Sale of Goods Act, 1930– Means every kind of moveable property other than

actionable claims and money; and includes stock and shares, growing crops, grass, and things attached to or forming part of the land which are agreed to be severed before sale or under the contract of sale.

© Lakshmikumaran & Sridharan, 2011

18

Amendment vide Finance Act 2009

Manufacture – Section 2(f) of CEA, 1944Includes any process, -

(i) incidental or ancillary to the completion of a manufactured product;

(ii) which is specified in relation to any goods in the Section or Chapter notes of the First Schedule to the Central Excise Tariff Act, 1985 as amounting to manufacture; or

© Lakshmikumaran & Sridharan, 2011

19

Amendment vide Finance Act 2009

Includes any process …

(iii) which in relation to the goods specified in the Third Schedule, involves packing or repacking of such goods in a unit container or labelling or re-labelling of containers including the declaration or alteration of retail sale price on it or adoption of any other treatment on the goods to render the product marketable to the consumer,

And the word ‘manufacturer’ shall be construed accordingly and shall include not only a person who employs hired labour in the production or manufacture of excisable goods, but also any person who engages in their production or manufacture on his own account.

© Lakshmikumaran & Sridharan, 2011

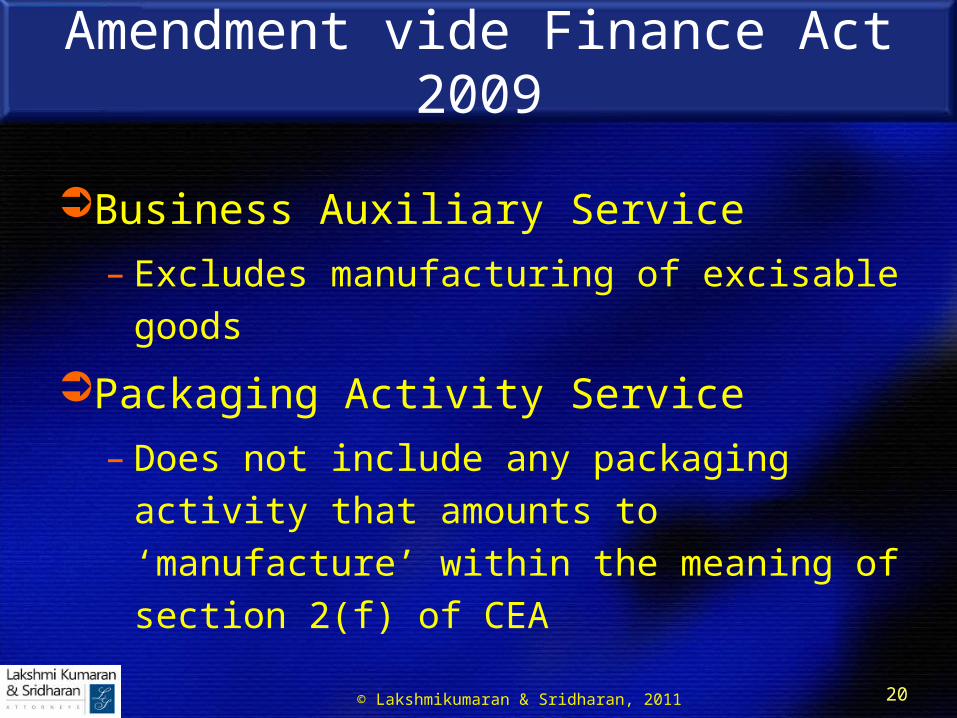

20

Amendment vide Finance Act 2009

Business Auxiliary Service

– Excludes manufacturing of excisable goods

Packaging Activity Service

– Does not include any packaging activity that

amounts to ‘manufacture’ within the meaning

of section 2(f) of CEA

© Lakshmikumaran & Sridharan, 2011

21

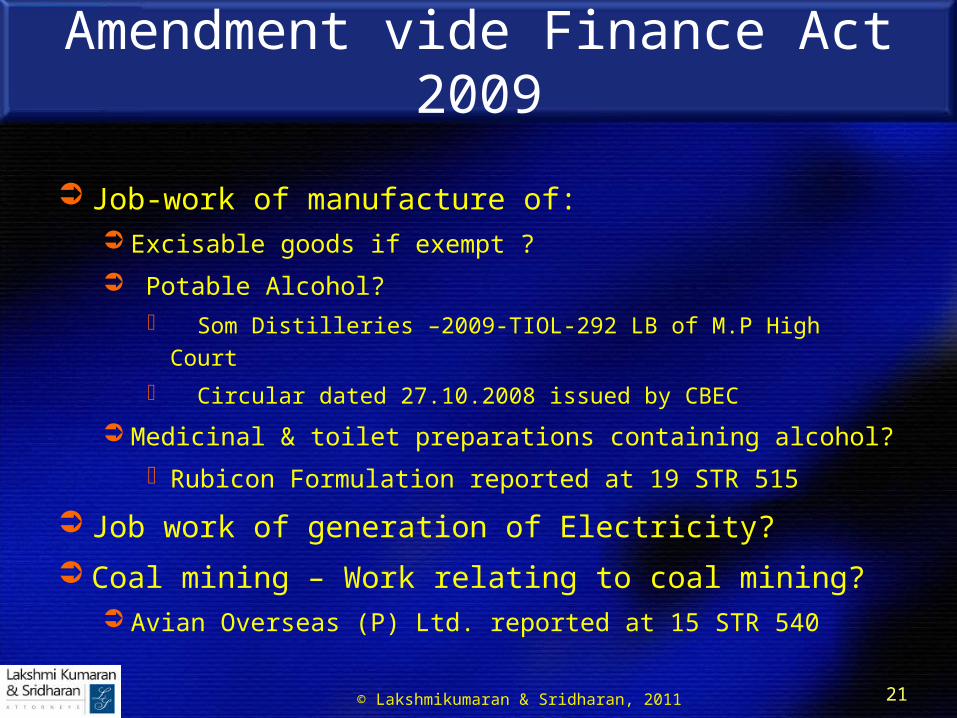

Amendment vide Finance Act 2009

Job-work of manufacture of: Excisable goods if exempt ?

Potable Alcohol? Som Distilleries –2009-TIOL-292 LB of M.P High Court

Circular dated 27.10.2008 issued by CBEC

Medicinal & toilet preparations containing alcohol?

Rubicon Formulation reported at 19 STR 515

Job work of generation of Electricity?

Coal mining – Work relating to coal mining? Avian Overseas (P) Ltd. reported at 15 STR 540

© Lakshmikumaran & Sridharan, 2011

22

Notification No. 13/2003-ST

Commission agent’s services exempted

Notification amended with effect from

9.7.2004

Now only the activities in relation to sale or

purchase of agricultural produce exempted

© Lakshmikumaran & Sridharan, 2011

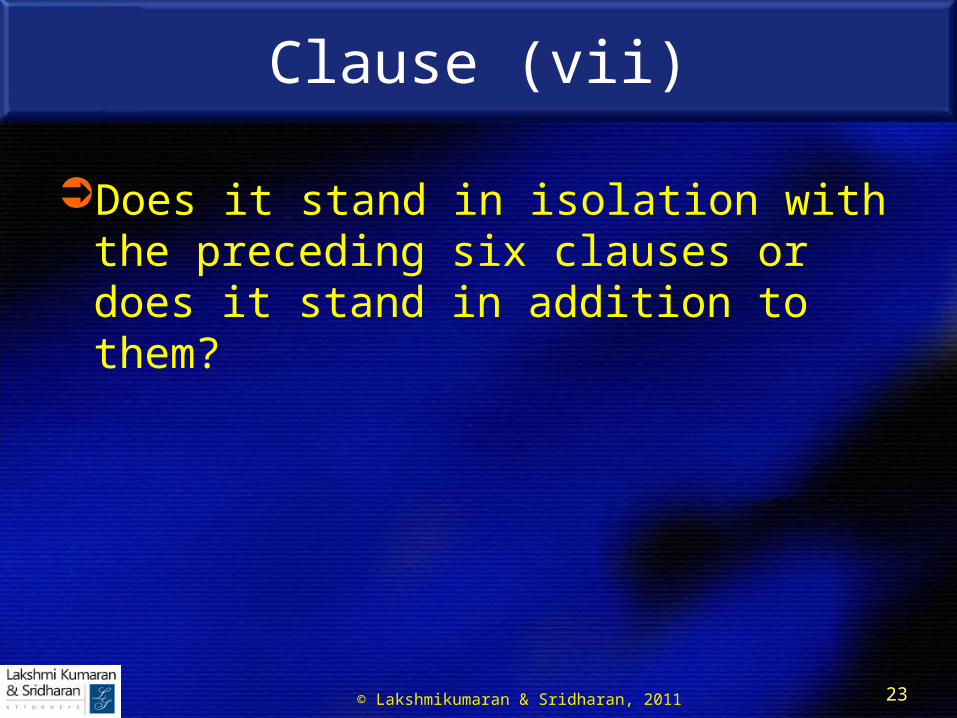

23

Clause (vii)

Does it stand in isolation with the preceding six clauses or does it stand in addition to them?

© Lakshmikumaran & Sridharan, 2011

24

BUSINESS SUPPORT SERVICES

© Lakshmikumaran & Sridharan, 2011

25

Ministry’s Letter

D.O.F. No. 334/4/2006-TRU dated 28.2.2006

Business entities outsource a number of services for use in business or commerce. These services include transaction processing, routine administration or accountancy, customer relationship management and tele-marketing. There are also business entities which provide infrastructural support such as providing instant offices along with secretarial assistance known as “Business Centre Services”. It is proposed to tax all such outsourced services. If these services are provided on behalf of a person, they are already taxed under Business Auxiliary Service. Definition of support services of business or commerce gives indicative list of outsourced services.

© Lakshmikumaran & Sridharan, 2011

26

Business Support Services

Section 65(105)zzzq Provided to any person By any other person In relation to support services of business or

commerce, in any manner

© Lakshmikumaran & Sridharan, 2011

27

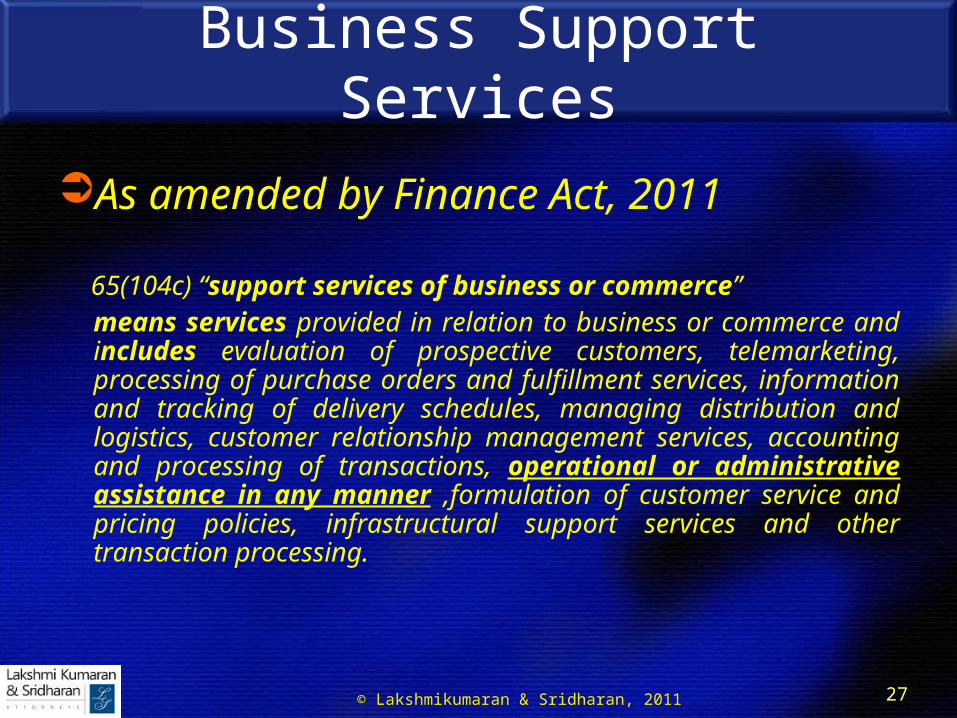

Business Support Services

As amended by Finance Act, 2011

65(104c) “support services of business or commerce”means services provided in relation to business or commerce and includes evaluation of prospective customers, telemarketing, processing of purchase orders and fulfillment services, information and tracking of delivery schedules, managing distribution and logistics, customer relationship management services, accounting and processing of transactions, operational or administrative assistance in any manner ,formulation of customer service and pricing policies, infrastructural support services and other transaction processing.

© Lakshmikumaran & Sridharan, 2011

28

Business Support Services

Explanation.—For the purposes of this clause, the expression “infrastructural support services” includes providing office along with office utilities, lounge, reception with competent personnel to handle messages, secretarial services, internet and telecom facilities, pantry and security;

© Lakshmikumaran & Sridharan, 2011

29

Business Support Services

DOF No.334/3/2011-TRU Dated 28.02.2011

The scope of the service is being expanded to include operational or administrative assistance of any kind. The scope will cover all support activities for others on a contract or fee, that are ongoing business support business functions that businesses and organizations commonly do for themselves but sometimes find I economical or otherwise worthwhile to outsource.

The word ‘operational and administrative assistance’ have wide connotation and can include certain services already taxed under any other head of more specific description. The correct classification will continue to be governed by Section 65A.

© Lakshmikumaran & Sridharan, 2011

30

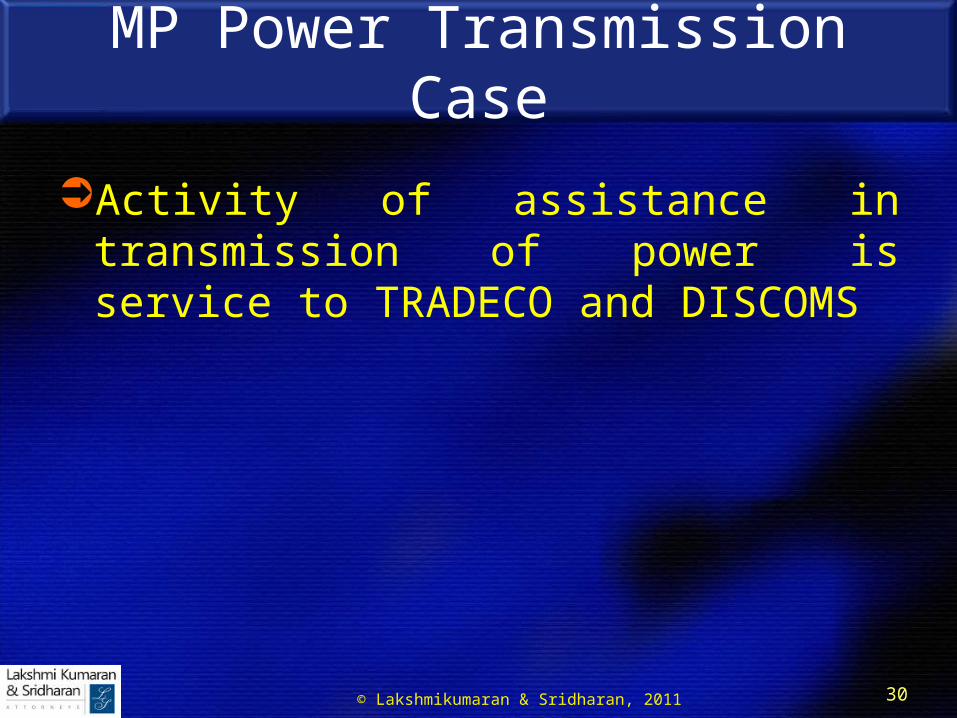

MP Power Transmission Case

Activity of assistance in transmission of power is service to TRADECO and DISCOMS

© Lakshmikumaran & Sridharan, 2011

31

Business Support Services

How to define “outsourced service”?

How does it differ from business auxiliary service?Promotion of services of banks by agent is business

support services and not business auxiliary Wings Group reported at 12 STR 287 “

Is it residuary entry for services to business or commerce?

© Lakshmikumaran & Sridharan, 2011

32

DISCUSSION

© Lakshmikumaran & Sridharan, 2011

33

New DelhiB-6/10, Safdarjung EnclaveNew Delhi – 110 029, IndiaPh: +91-11-26192243, 5129 9800Fax: +91-11-26197578, 5129 9899E-mail: [email protected]

Mumbai401-404, Kakad Chambers,132, Dr. Annie Besant RoadWorli, Mumbai – 400 018Ph: +91-22-24914382 /84/86Fax: +91-22-24914388E-mail: [email protected]

Bangalore505-508, 5th Floor, Brigade Plaza (North Block) No.71/1, Subedar Chatram Road, Anand Rao Circle, Banglaore-560009E-mail: [email protected] Thank You

Our contacts

HyderabadBlock No 301, 3rd FloorHermitage office complexHill Fort Road, HyderabadTel: +91-40-2323 4924/25Fax: +91-40-2323 4826E-mail: [email protected]

Chennai2, Wallace Garden, 2nd StreetChennai -600 006Tel: +91-44-2833 4700/701Fax: +91-44-2833 4702E-mail: [email protected]

AhmedabadB-334 (3rd Floor), Sakar-VII, Nehru Bridge Corner, Ashram Road, Ahmedabad-380009Tel: +91-79-4001 4500Fax: +91-79-4001 4599E-mail: [email protected]