-market and industry trends - adpi · -market and industry trends chicago ... in 2008 the global...

TRANSCRIPT

3A Business Consulting3A Business Consulting97

Dairy and whey ingredients- market and industry trends

Chicago - April 27, 2010

Tage Affertsholt, 3A Business Consulting

3A Business Consulting3A Business Consulting98

Introduction

Dairy and whey ingredients –market overview

Dairy and whey ingredients –production/trade trends

Dairy and whey ingredients –industry trends & outlook

1

2

3

4

Agenda

3A Business Consulting3A Business Consulting99

3A Business model

Strategy and businessdevelopment for all elements of the food value chain

Key competenceswithin functional foods, health& wellness and ingredients

Core structure - global network

3A Business Consulting3A Business Consulting100

Dairy and whey ingredient-related reports

3A Business Consulting3A Business Consulting101

Dairy ingredient overview

Milk as raw

material

Whey as raw material

SMPWMPCaseinCaseinates

Micellar casein

WPDWPWPC35 Lactose Permeate

MPCMPI

WPC80WPI

Minerals Lactose-pharma

MPHPeptidesProtein fractions

WPH

PeptidesProtein fractionsPhospho-lipids Lactose derivatives

Added value level

Milk ingredients

Whey ingredients

Note: Cheese and butterfat as an ingredient is not included in respective 3A reports, although an important market

Applications

Pharma

Nutrition

Health care

Personal care

Food

Feed

CheeseCasein

3A Business Consulting3A Business Consulting102

Introduction

Dairy and whey ingredients –market overview

Dairy and whey ingredients –production/trade trends

Dairy and whey ingredients –industry trends & outlook

1

2

3

4

Agenda

3A Business Consulting3A Business Consulting103

Milk production vs. exports and imports 2008

86.3

44.1

35.9

25.8

16.7 14.511.6 11.6 11.1

8.4 7.3 6.1 5.93.1

0.2

13.0

0.2

0.9

0.0

0.1 4.

0

0.0 1.6

0.2

0.7

0.6

1.2

0.0 2.3

1.6

0.1

0.7

0.1

0.1 2.6

0.5

1.6

0.0

0.2

0.4

147.6

0.1

0.13.7

10.3

0

20

40

60

80

100

120

140

EUU

nite

d Sta

tes

Indi

a

Chi

na

Rus

siaN

ew Z

eala

nd

Brazi

l

Ukr

aine

Pakis

tan

Mex

ico

Austra

lia

Japa

nArg

entin

a

Can

ada

Switz

erla

nd

Qu

an

tity

in

Mil

lio

ns t

on

nes

Milk Production

Exports in Milk equivalent

Imports in Milk equivalent

Source: EU Commission

3A Business Consulting3A Business Consulting104

Imports of dairy products 2008

(in million tonnes of milk equivalent)

India

9

Mexico

2 578

China

2 317

Russia

1 623

Japan

1 576

United States

1 245Brazil

732Australia

546

Pakistan

91Ukraine

150

Canada

236

Switzerland

368

EU

566

Argentina

22

New Zealand

90

Source: EU Commission

3A Business Consulting3A Business Consulting105

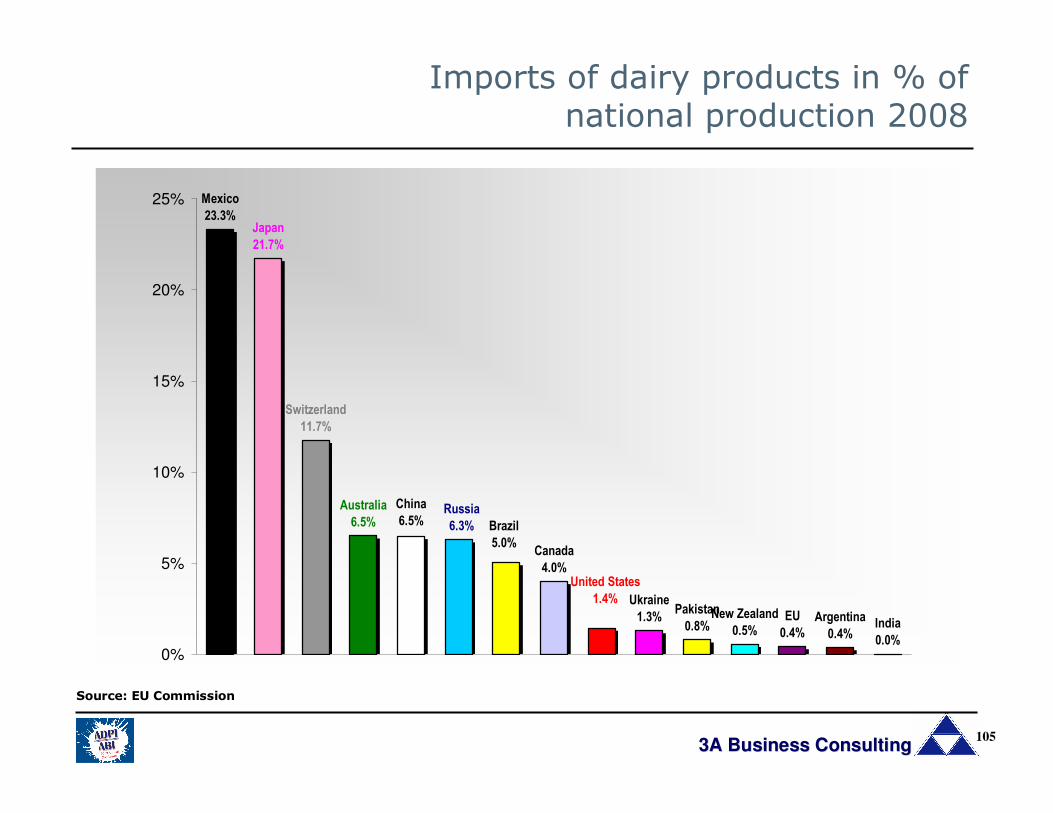

Imports of dairy products in % of national production 2008

EU

0.4%

Argentina

0.4%India

0.0%

Mexico

23.3%Japan

21.7%

Switzerland

11.7%

Australia

6.5%

China

6.5%Russia

6.3%

Canada

4.0%

New Zealand

0.5%

Pakistan

0.8%

Ukraine

1.3%

United States

1.4%

Brazil

5.0%

0%

5%

10%

15%

20%

25%

Source: EU Commission

3A Business Consulting3A Business Consulting106

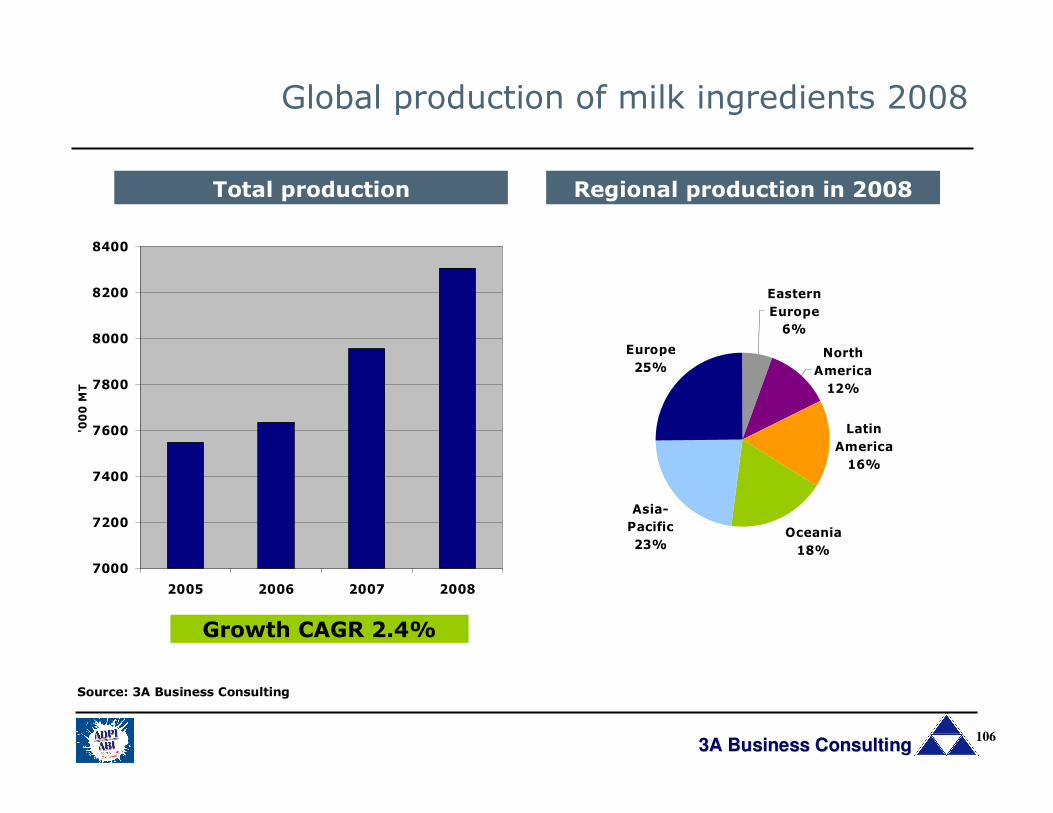

Global production of milk ingredients 2008

7000

7200

7400

7600

7800

8000

8200

8400

2005 2006 2007 2008

'000 MT

Europe

25%

Asia-

Pacific

23%Oceania

18%

Latin

America

16%

North

America

12%

Eastern

Europe

6%

Total production Regional production in 2008

Source: 3A Business Consulting

Growth CAGR 2.4%

3A Business Consulting3A Business Consulting107

Global production of milk ingredients 2008 - per main category

SMP

WMP

HighLow

Low

High

Growth

Volume Size of blue circles indicates market size

Casein/caseinate MPC/MPI

Other milk ingredients can be found, however volumes are

comparatively small

Total production volume approx.

8,300,000 MT

In 2008 the global milk ingredient market was worth roughly USD 19 bio

Between ’05-’08, market volume up 2-3% p.a. and market value up by 27%

Source: 3A Business Consulting

3A Business Consulting3A Business Consulting108

Global whey ingredients market 2008

Growth

Volume

HighLow

Low

High

Whey powder

WPC80

WPH

WPI

DWP

WPC35

Other protein ingredients can be found, however

volumes comparatively small

Size of blue circles indicates market size

The global whey protein market was worth roughly USD 3.8 bio in 2008

Between ’05-’08, market volume up 3% and market value up by 24%

Market volume of approx. Market volume of approx. Market volume of approx. Market volume of approx. 3,200,000 MT3,200,000 MT3,200,000 MT3,200,000 MT

3A Business Consulting3A Business Consulting109

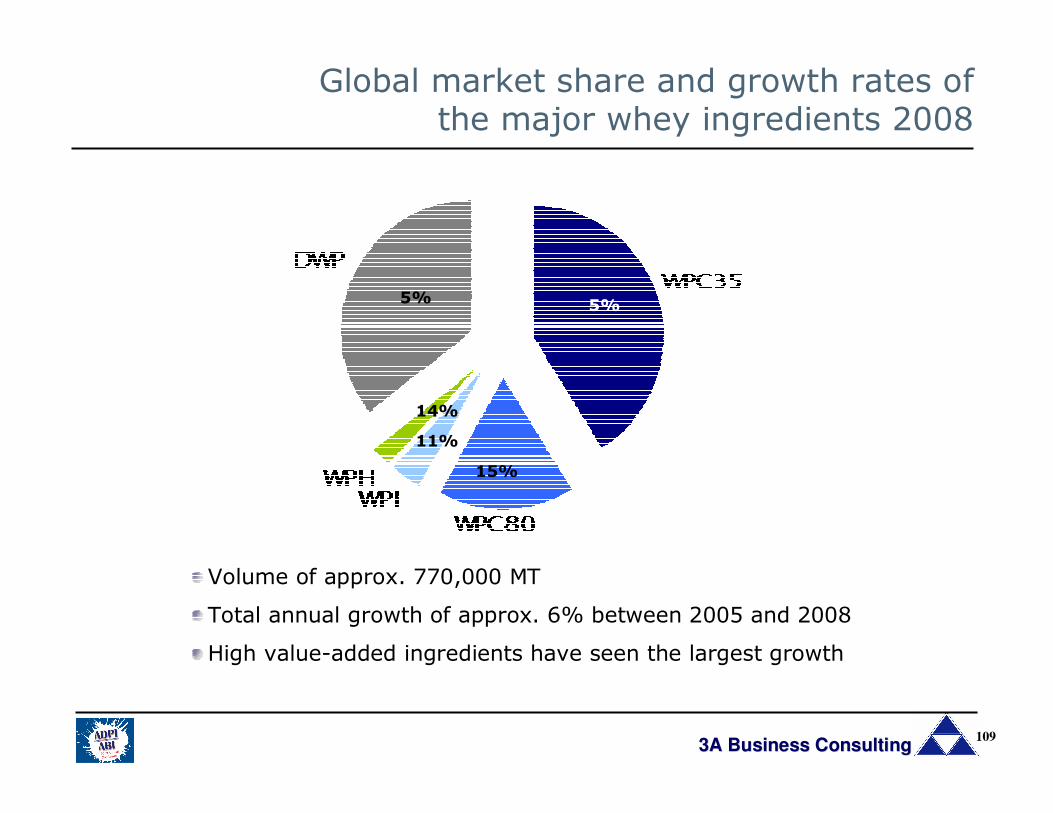

Global market share and growth rates of the major whey ingredients 2008

5%

11%

14%

15%

5%

Volume of approx. 770,000 MT

Total annual growth of approx. 6% between 2005 and 2008

High value-added ingredients have seen the largest growth

3A Business Consulting3A Business Consulting110

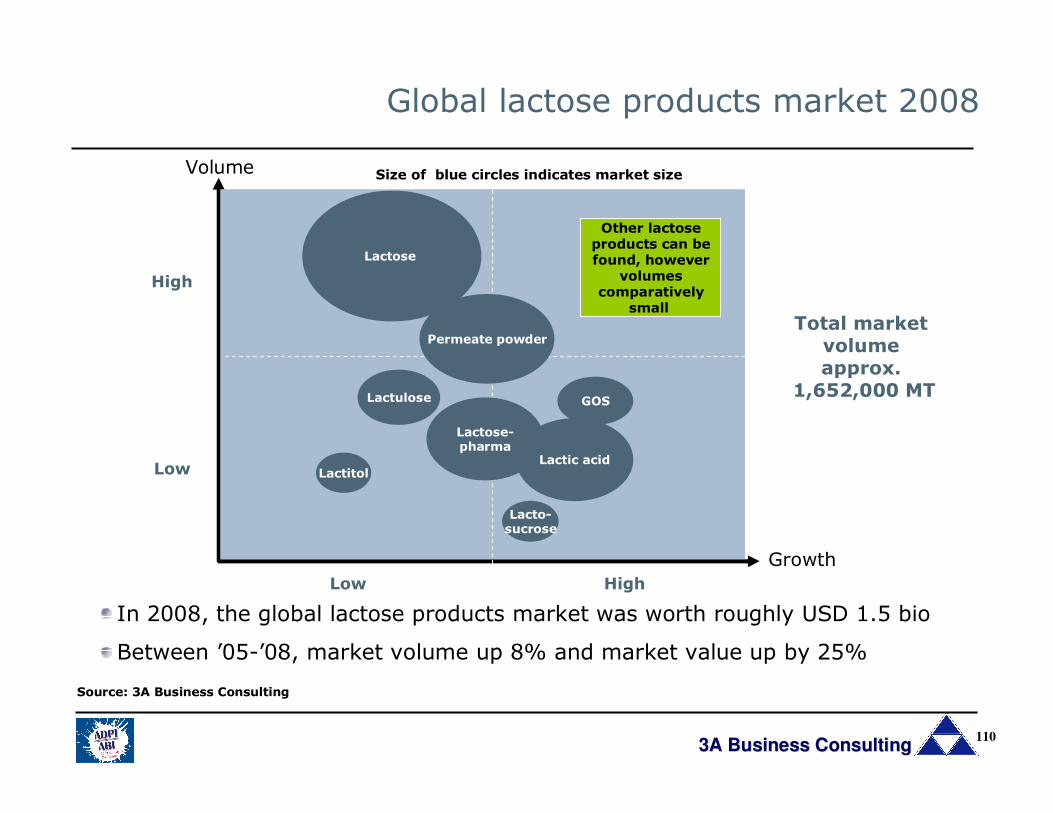

Global lactose products market 2008

Growth

HighLow

Volume

Low

High

Size of blue circles indicates market size

Lactose

Lactose-pharma

Permeate powder

Lactulose

Lactitol

GOS

Lacto-sucrose

Lactic acid

Other lactose products can be found, however

volumes comparatively

small

Total market volume approx.

1,652,000 MT

In 2008, the global lactose products market was worth roughly USD 1.5 bio

Between ’05-’08, market volume up 8% and market value up by 25%

Source: 3A Business Consulting

3A Business Consulting3A Business Consulting111

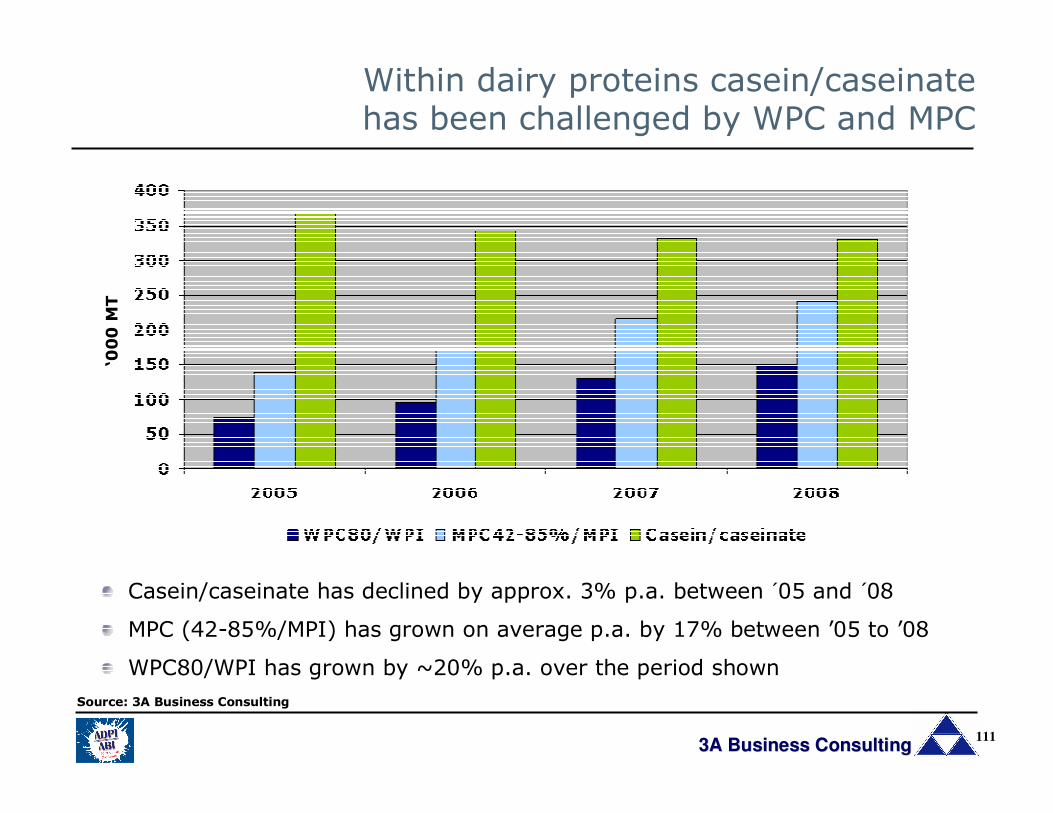

Within dairy proteins casein/caseinate has been challenged by WPC and MPC

Casein/caseinate has declined by approx. 3% p.a. between ´05 and ´08

MPC (42-85%/MPI) has grown on average p.a. by 17% between ’05 to ’08

WPC80/WPI has grown by ~20% p.a. over the period shown

Source: 3A Business Consulting

‘000 MT

3A Business Consulting3A Business Consulting112

Bioactives are an emerging dairy ingredient category

The global market for dairy bioactive ingredients is minor, even when compared to other high-end dairy ingredient volumes

Market volume is estimated to be approx. 33,000 MT and to be worth approximately USD 700 million in 2009

MPC80, MPI & casein/caseinates

Dairyprotein fractions

Dairy peptides

400,000 MT

WPC80& WPI

MPH& WPH

Est. growth rate 10-20% p.a.

3A Business Consulting3A Business Consulting113

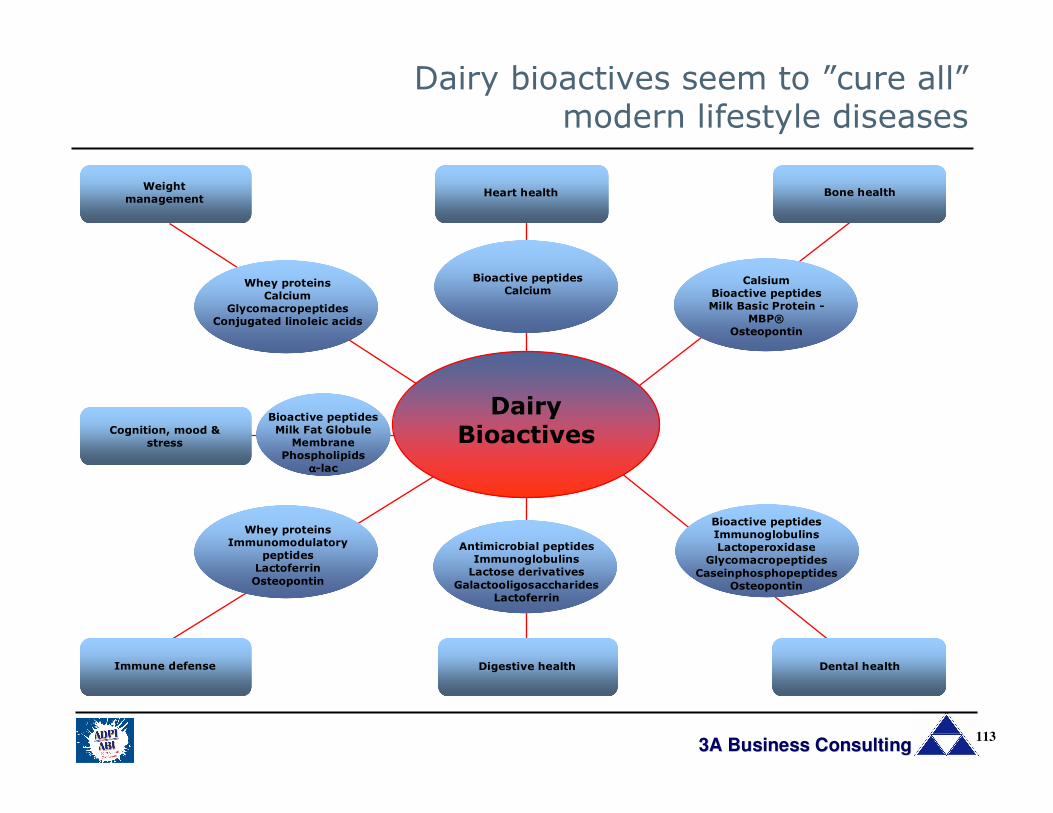

Dairy bioactives seem to ”cure all” modern lifestyle diseases

Dental healthDigestive healthImmune defense

Cognition, mood & stress

Bone healthHeart healthWeight

management

Whey proteins Immunomodulatory

peptidesLactoferrin

Osteopontin

Antimicrobial peptidesImmunoglobulins Lactose derivatives

Galactooligosaccharides Lactoferrin

Bioactive peptidesMilk Fat Globule

MembranePhospholipids

αααα-lac

Whey proteins Calcium

Glycomacropeptides Conjugated linoleic acids

Bioactive peptidesCalcium

Bioactive peptidesImmunoglobulins Lactoperoxidase

Glycomacropeptides

Caseinphosphopeptides Osteopontin

CalsiumBioactive peptidesMilk Basic Protein -

MBP®Osteopontin

DairyBioactives

3A Business Consulting3A Business Consulting114

Introduction

Dairy and whey ingredients –market overview

Dairy and whey ingredients –production/trade trends

Dairy and whey ingredients –industry trends & outlook

1

2

3

4

Agenda

3A Business Consulting3A Business Consulting115

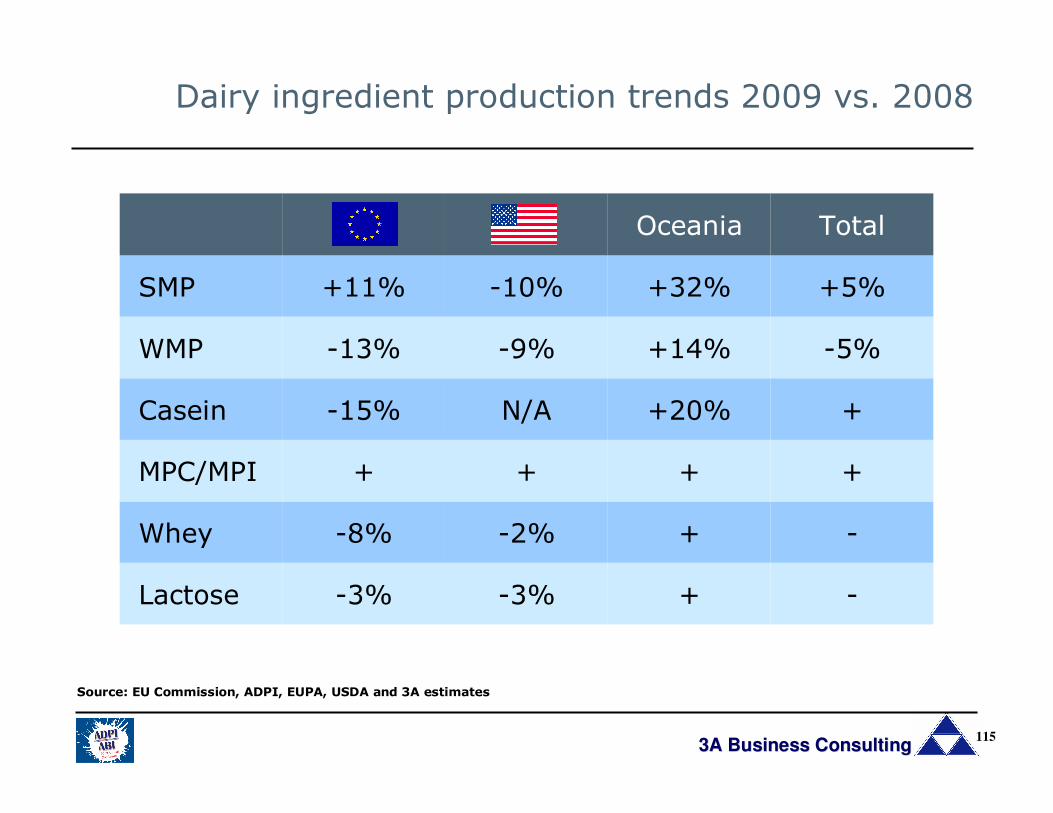

Dairy ingredient production trends 2009 vs. 2008

-+-3%-3%Lactose

-+-2%-8%Whey

++++MPC/MPI

++20%N/A-15%Casein

-5%+14%-9%-13%WMP

+5%+32%-10%+11%SMP

TotalOceaniaUSEU

Source: EU Commission, ADPI, EUPA, USDA and 3A estimates

3A Business Consulting3A Business Consulting116

-15%

-10%

-5%

0%

5%

10%

15%

EU US

EU total sales in 2009 were down 2% and stocks end 2009 down 28% vs. 2008

US total sales in 2009 were ±0 and stocks end 2009 down 29% vs. 2008

EU production trends in 2010: >+10% vs. 2009 end Feb

US production trends in 2010: +8% vs. 2009 end Feb

Whey ingredients production trends 2009 vs. 2008

WP WPC<50%

WPC80/WPI

LactoseAll wheyproducts

3A Business Consulting3A Business Consulting117

Dairy ingredients – export trends 2009

++14%+18%+27%Lactose

+++3%+19%Whey

+±0%N/A+MPC/MPI

++13%N/A+4%Casein

+6%+28%N/A-7%WMP

+12%+55%-36%+28%SMP

TotalOceaniaUSEU

Note: Oceania casein and lactose figures refer to NZSource: EU Commission, USDA and 3A estimates

3A Business Consulting3A Business Consulting118

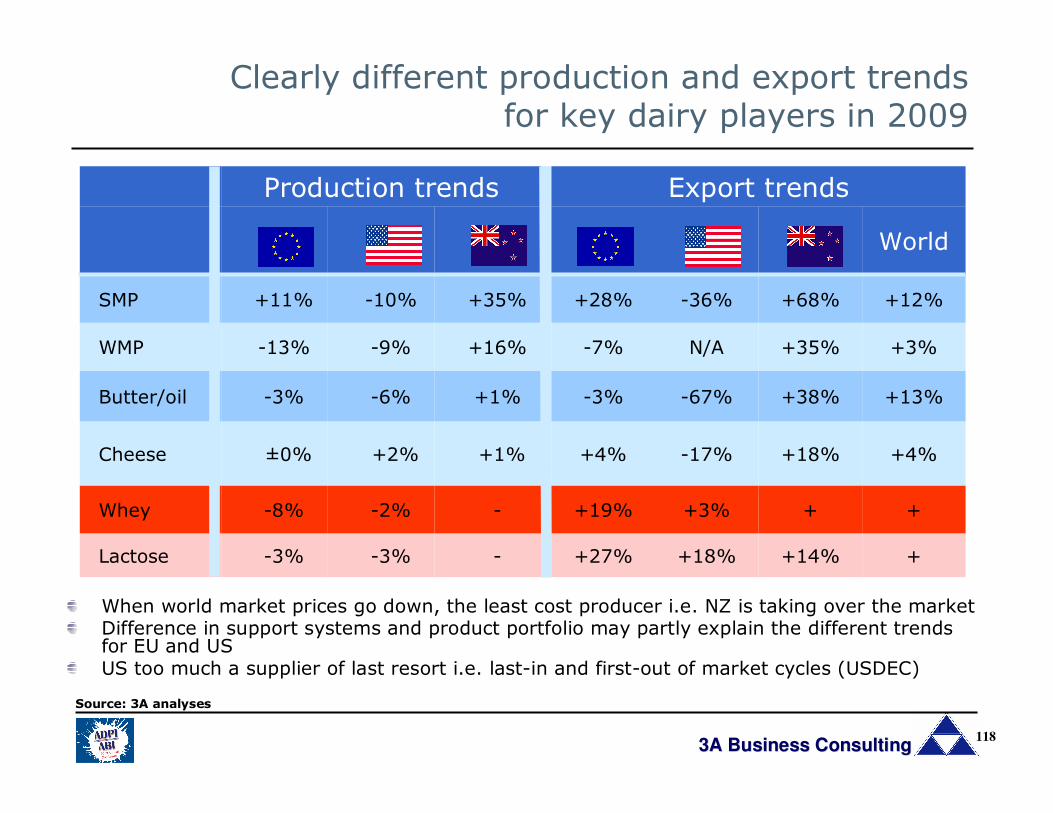

Clearly different production and export trends for key dairy players in 2009

When world market prices go down, the least cost producer i.e. NZ is taking over the marketDifference in support systems and product portfolio may partly explain the different trends for EU and USUS too much a supplier of last resort i.e. last-in and first-out of market cycles (USDEC)

+

+

+4%

+13%

+3%

+12%

World

-

-

+1%

+1%

+16%

+35%

NZ

-3%

-2%

+2%

-6%

-9%

-10%

US

-3%

-8%

±0%

-3%

-13%

+11%

EU

Production trends

Lactose

Whey

Cheese

Butter/oil

WMP

SMP

Export trends

+14%+18%+27%

++3%+19%

+18%-17%+4%

+38%-67%-3%

+35%N/A-7%

+68%-36%+28%

NZUSEU

Source: 3A analyses

3A Business Consulting3A Business Consulting119

Introduction

Dairy and whey ingredients –market overview

Dairy and whey ingredients –production/trade trends

Dairy and whey ingredients –industry trends & outlook

1

2

3

4

Agenda

3A Business Consulting3A Business Consulting120

Dairy and whey ingredient prices still fairly volatile

Note: Based on average US prices Source: Wisconsin University & 3A Business Consulting

The dramatic fluctuations between 2007 and 2009 resulted from supply/demand imbalances and boosted by economic recession

0

1 .000

2 .000

3 .000

4 .000

5 .000

6 .000

jan-

04

jul-04

jan-0

5

jul-05

jan-0

6

jul-06

jan-0

7

jul-07

jan-0

8

jul-08

jan-0

9

jul-09

jan-1

0

USD per MT

Lac tose SMP WP WPC 3 5

Price development 2004-10 – dairy and whey ingredients

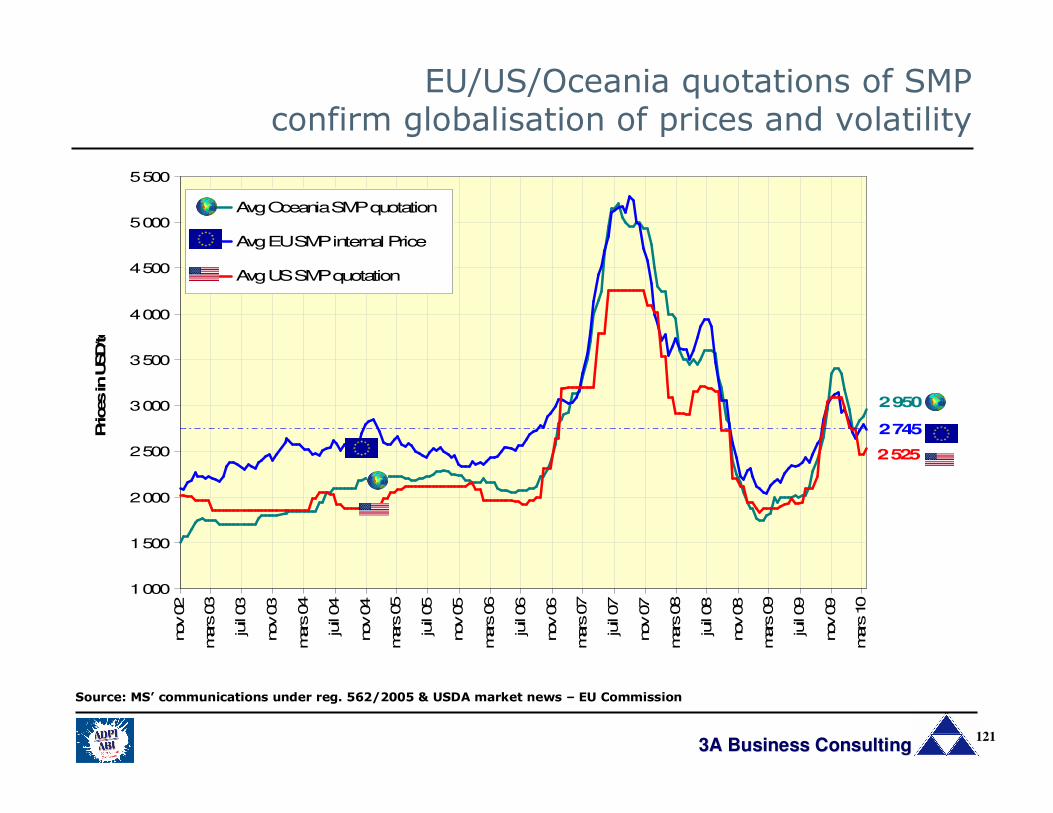

3A Business Consulting3A Business Consulting121

2 950

2 745

2 525

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

5 500nov 02

mars

03

juil 03

nov 03

mars

04

juil 04

nov 04

mars

05

juil 05

nov 05

mars

06

juil 06

nov 06

mars

07

juil 07

nov 07

mars

08

juil 08

nov 08

mars

09

juil 09

nov 09

mars

10

Prices in U

SD/tonne

Avg Oceania SMP quotation

Avg EU SMP internal Price

Avg US SMP quotation

Source: MS’ communications under reg. 562/2005 & USDA market news – EU Commission

EU/US/Oceania quotations of SMP confirm globalisation of prices and volatility

3A Business Consulting3A Business Consulting122

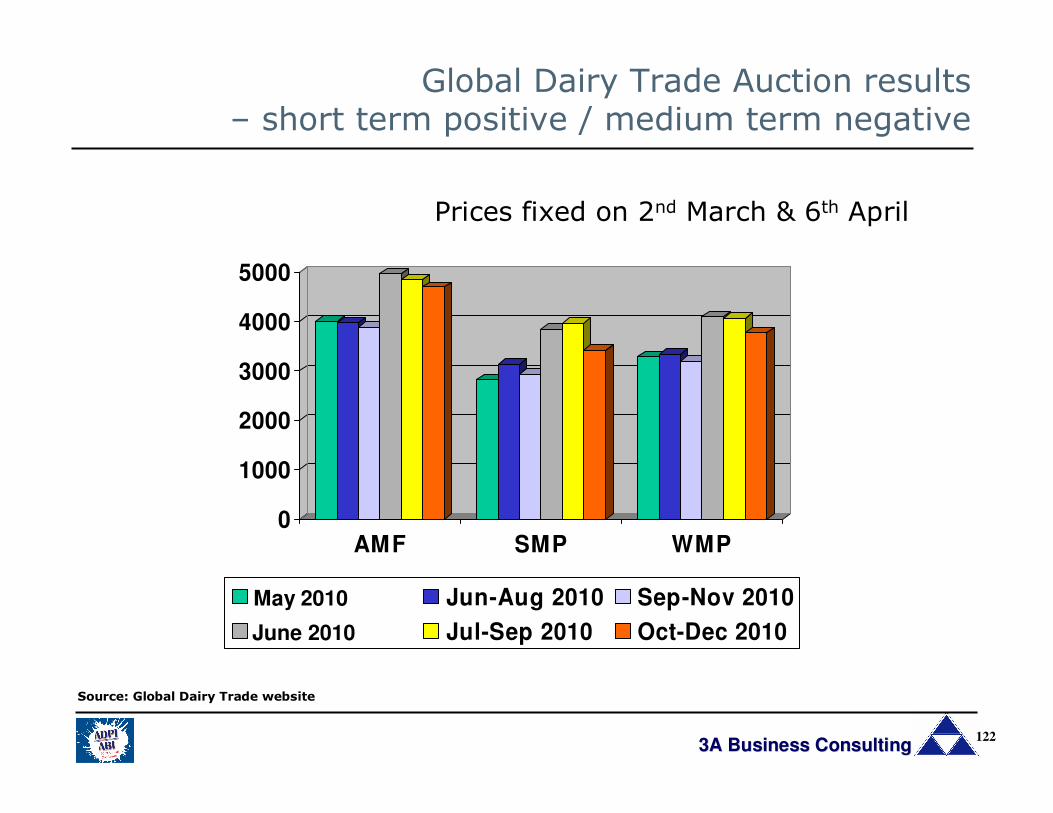

Prices fixed on 2nd March & 6th April

0

1000

2000

3000

4000

5000

AMF SMP WMP

maj-10 Jun-Aug 2010 Sep-Nov 2010

jun-10 Jul-Sep 2010 Oct-Dec 2010

Global Dairy Trade Auction results – short term positive / medium term negative

Source: Global Dairy Trade website

May 2010

June 2010

3A Business Consulting3A Business Consulting123

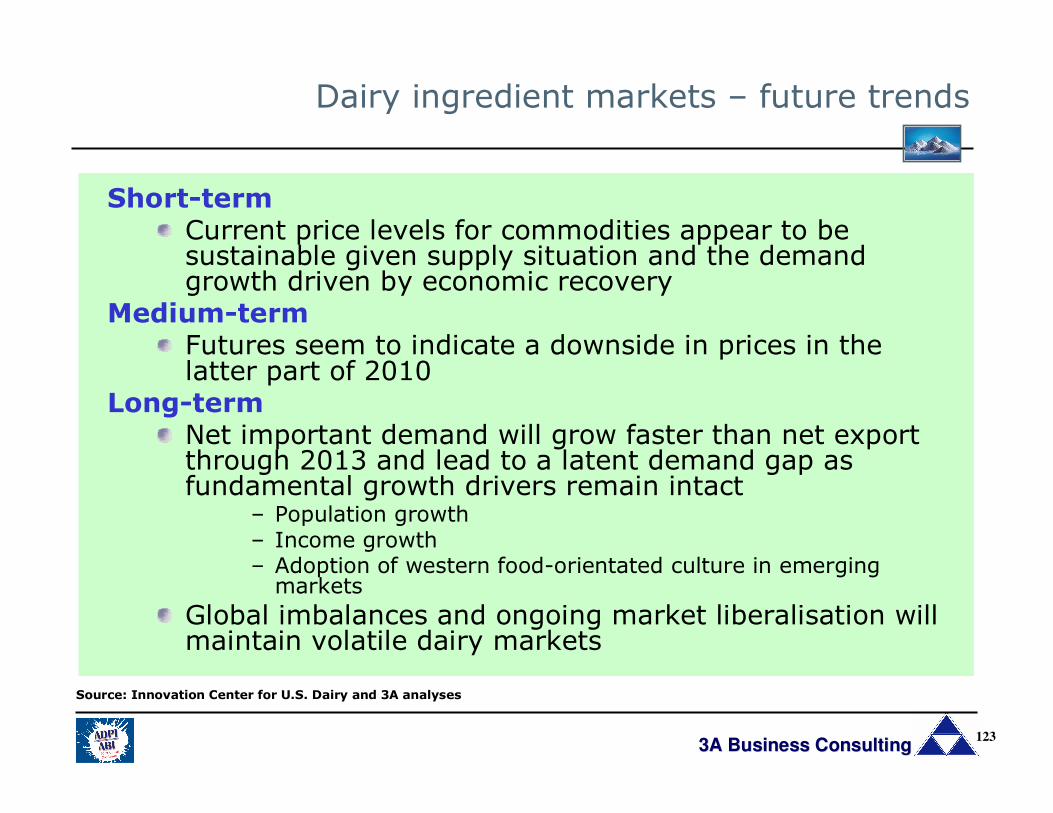

Dairy ingredient markets – future trends

Short-termCurrent price levels for commodities appear to besustainable given supply situation and the demandgrowth driven by economic recovery

Medium-termFutures seem to indicate a downside in prices in the latter part of 2010

Long-termNet important demand will grow faster than net exportthrough 2013 and lead to a latent demand gap as fundamental growth drivers remain intact

– Population growth– Income growth– Adoption of western food-orientated culture in emergingmarkets

Global imbalances and ongoing market liberalisation willmaintain volatile dairy markets

Source: Innovation Center for U.S. Dairy and 3A analyses

3A Business Consulting3A Business Consulting124

Asia-Pacific: No 1 market for dairy ingredients and willremain strongly import dependent

Latin America: Has potential to become a major supplier to the world market (particularly Brazil and Argentina)

Oceania: Production and export set to increase medium term

Eastern Europe: Russia to remain an important import market despite government incentives to increase production. Ukraine has the potential to play a bigger role on worldmarkets

US: Holds the potential for both a bigger production and a more significant role on the world market

EU: Still the world’s largest producer of dairy ingredients, however its relative importance in global markets to decrease– mostly for butter, SMP, WMP and less for cheese and whey

Dairy ingredient markets – future long-term trends

3A Business Consulting3A Business Consulting125

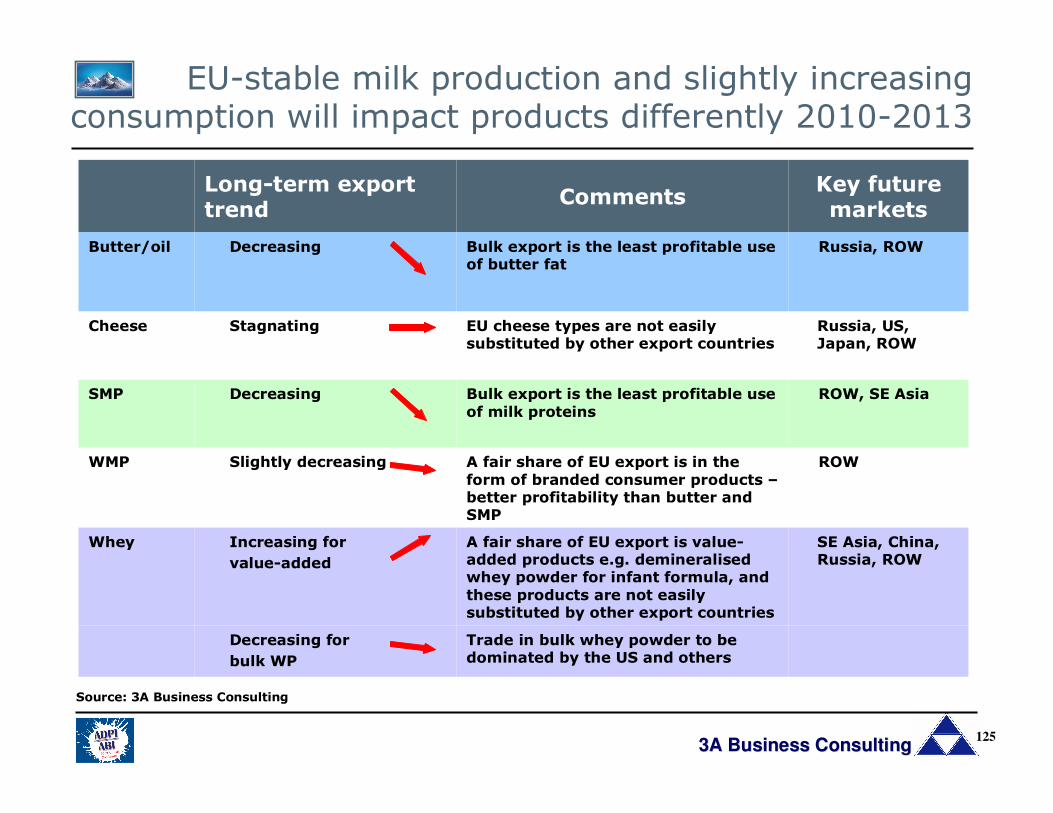

EU-stable milk production and slightly increasing consumption will impact products differently 2010-2013

Whey

WMP

SMP

Cheese

Butter/oil

Trade in bulk whey powder to bedominated by the US and others

A fair share of EU export is value-added products e.g. demineralisedwhey powder for infant formula, and

these products are not easilysubstituted by other export countries

A fair share of EU export is in the

form of branded consumer products –better profitability than butter and SMP

Bulk export is the least profitable use

of milk proteins

EU cheese types are not easilysubstituted by other export countries

Bulk export is the least profitable useof butter fat

Comments

SE Asia, China, Russia, ROW

Increasing for

value-added

Decreasing for

bulk WP

ROWSlightly decreasing

ROW, SE AsiaDecreasing

Russia, US, Japan, ROW

Stagnating

Russia, ROWDecreasing

Key future markets

Long-term exporttrend

Source: 3A Business Consulting

3A Business Consulting3A Business Consulting126

Future key challenges for dairy ingredient companies

Competence

Different skill sets required for commodities and high value-added products –not necessarily easy to integrate simultaneously into the same organisation

Cost concern

The price premium of dairy in relation to other competing ingredientsconstrains its use. The price hike in 2007-2008 taught the food processingindustry how to replace dairy in many applications

Solution marketing approach

Mass-market sectors such as dairy, ice cream, confectionery, bakery, meat etc. require specific application functionalityNutrition and health sectors including infant formula, functional foods, dietarysupplements require additional expertise in nutritional and regulatory issues

Food safety

Safety assurances and traceability issues increasingly important