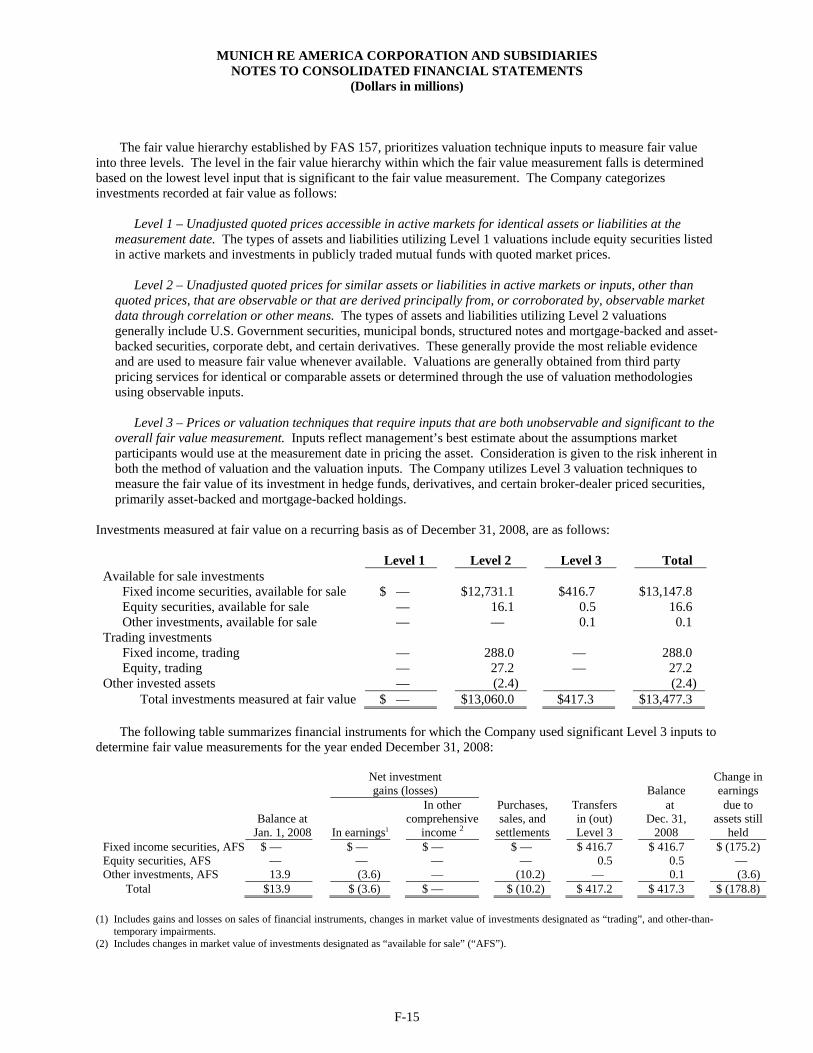

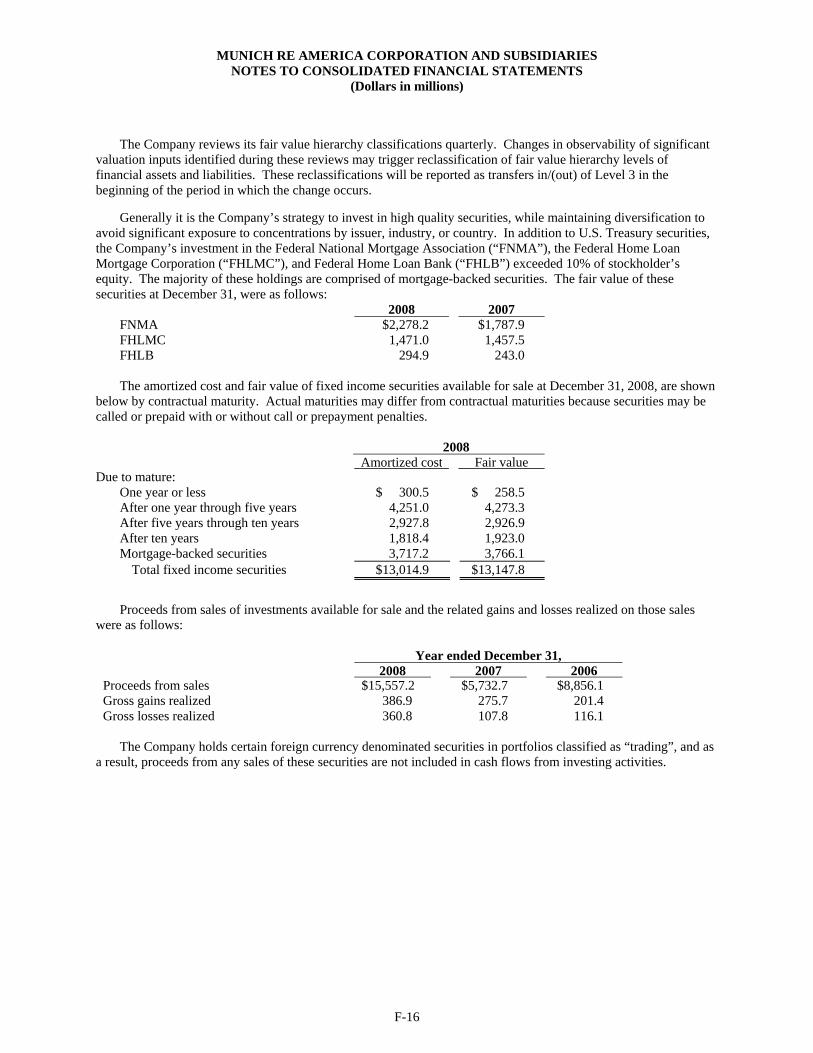

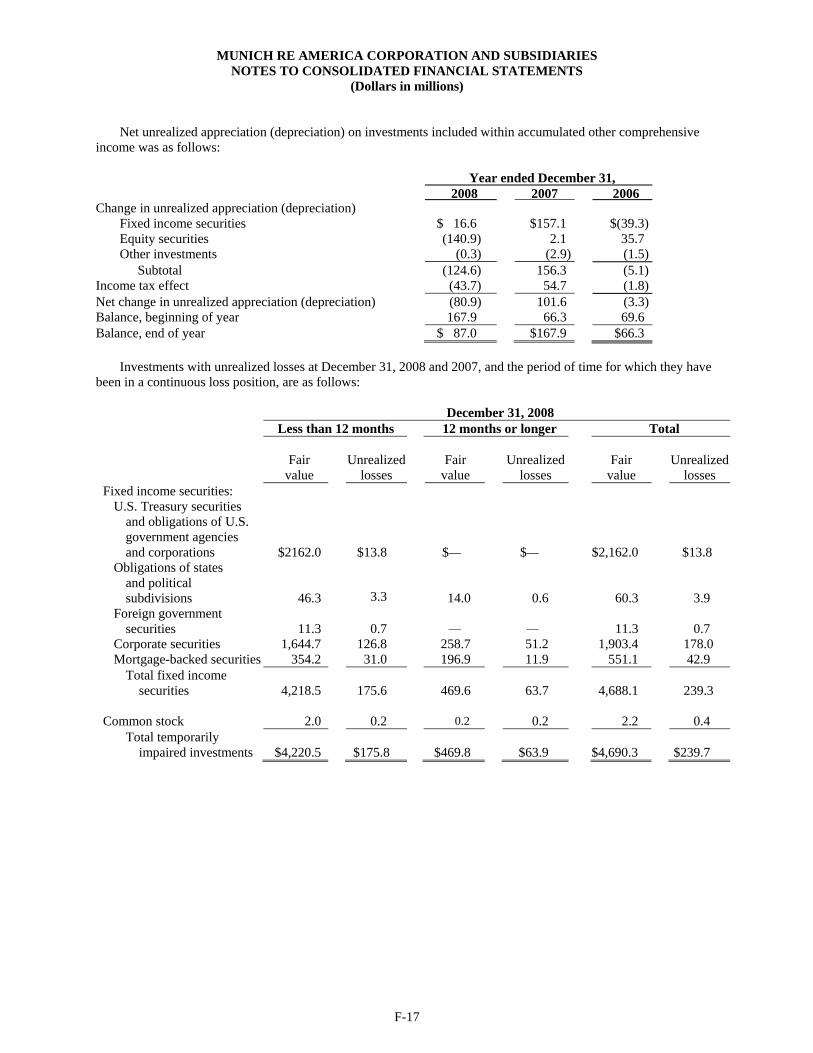

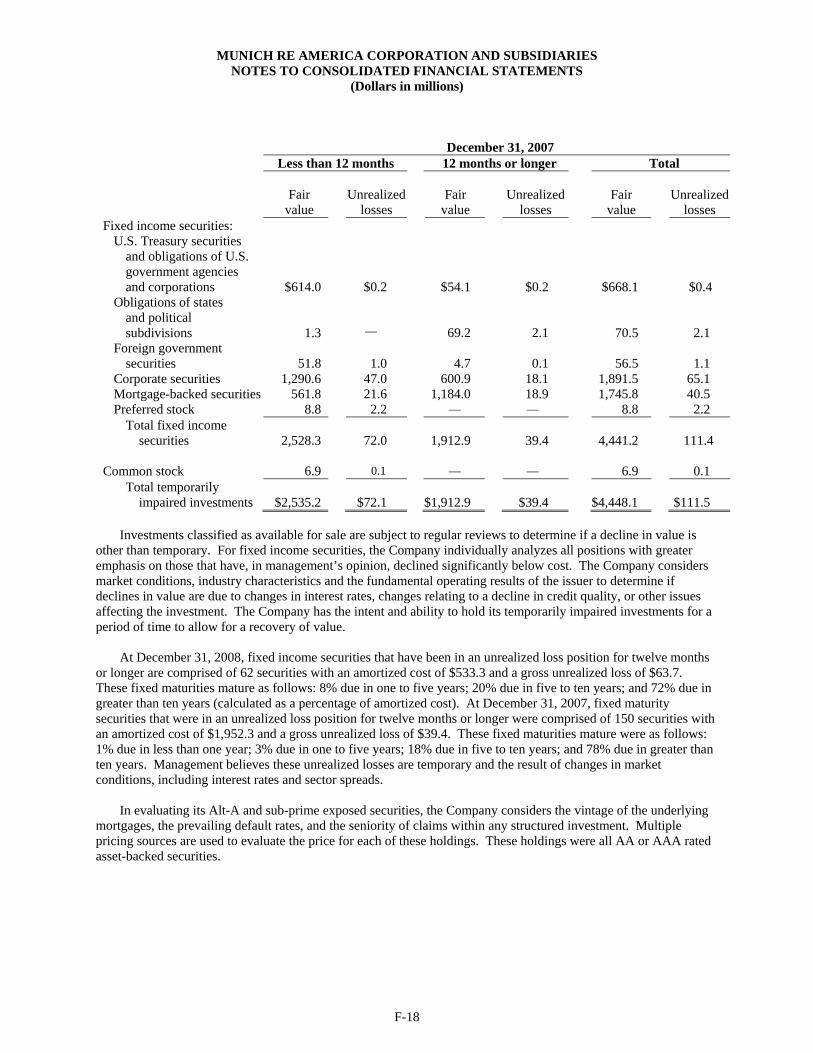

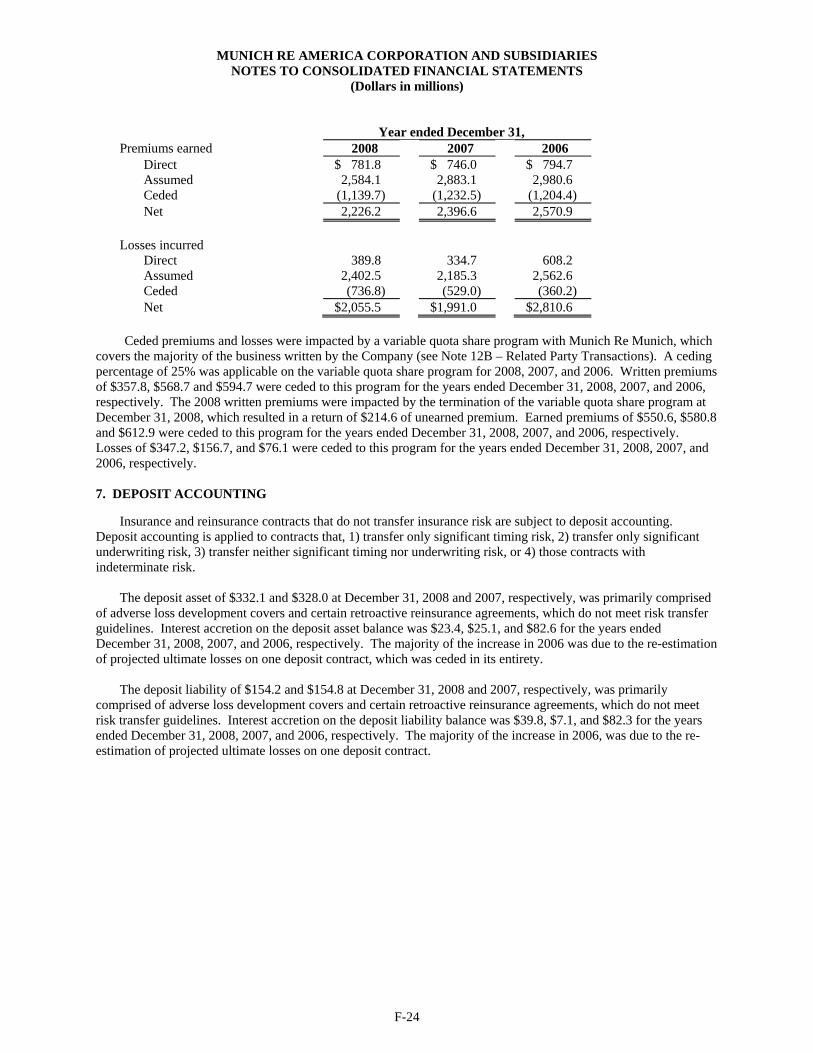

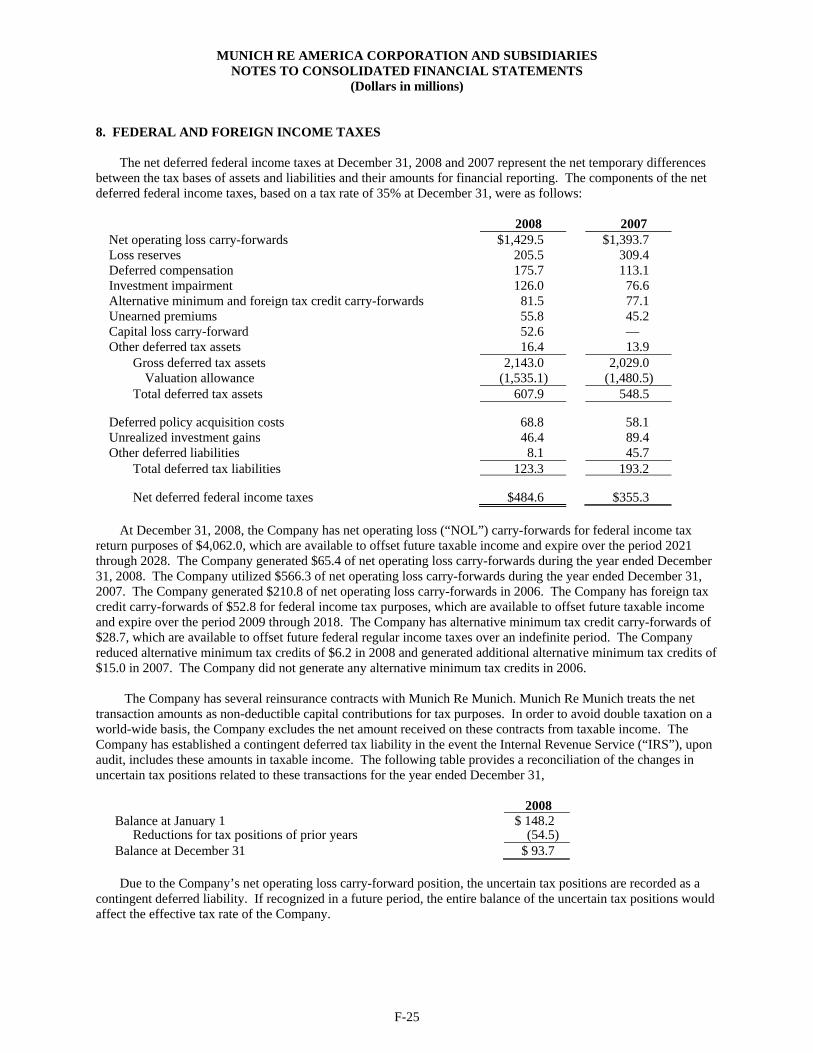

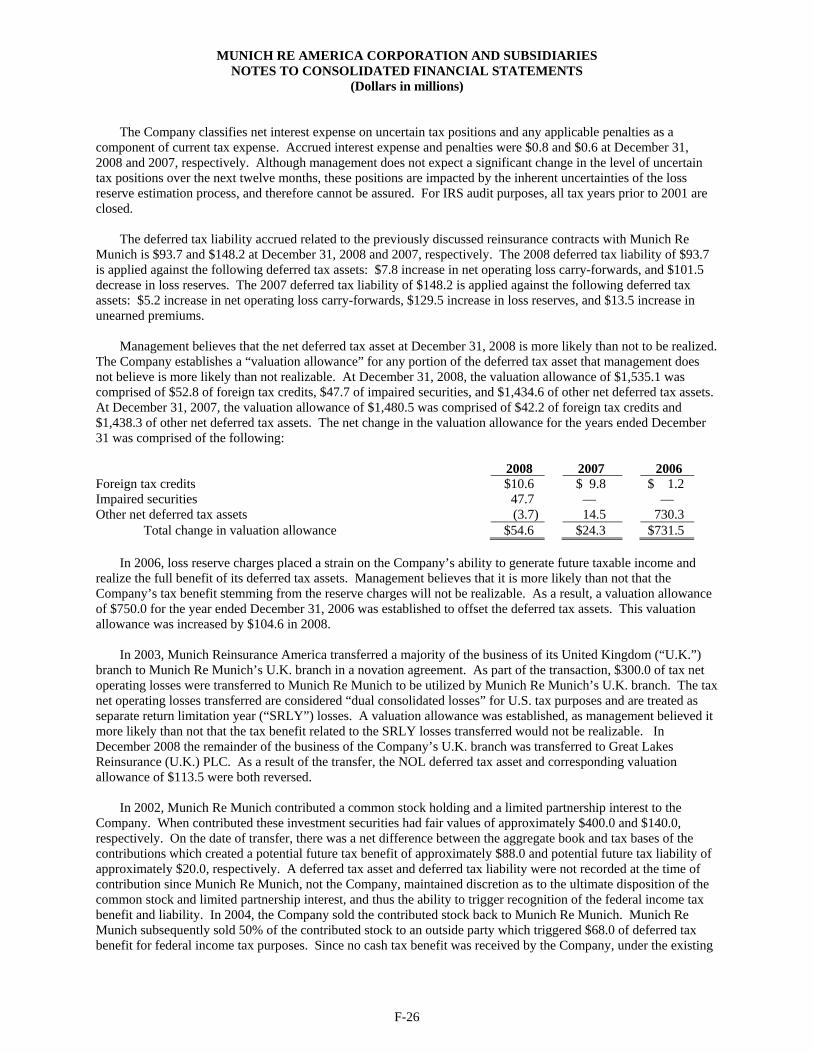

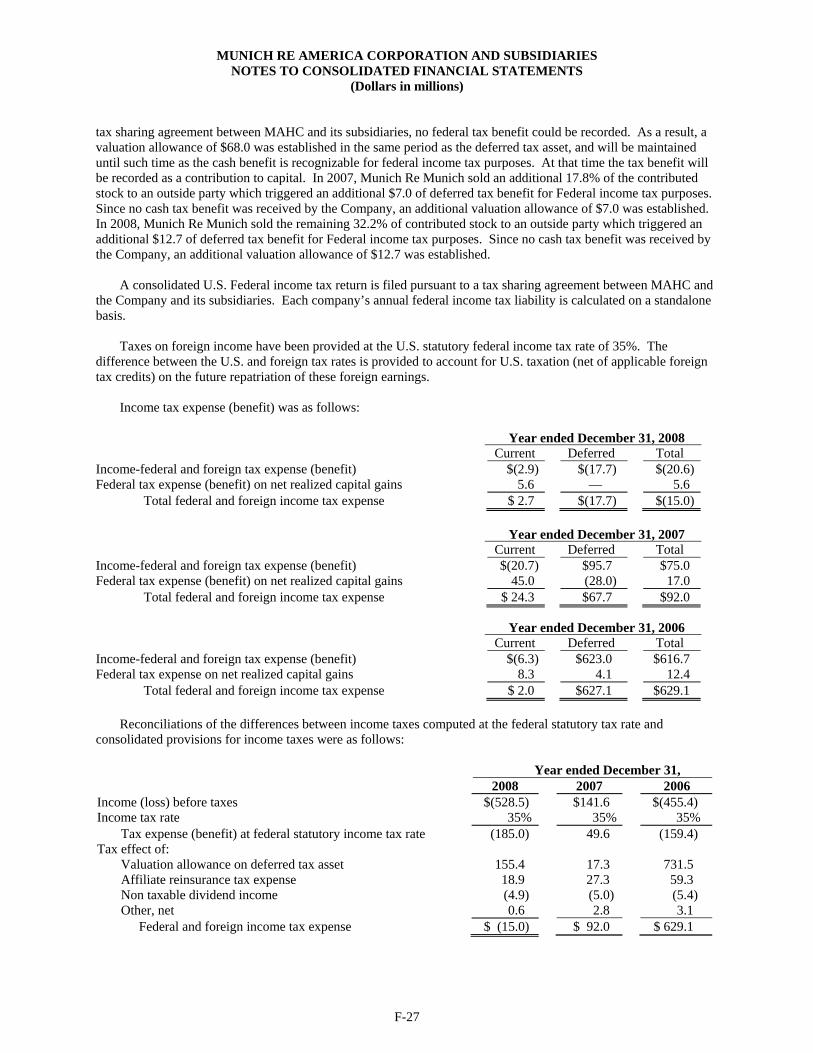

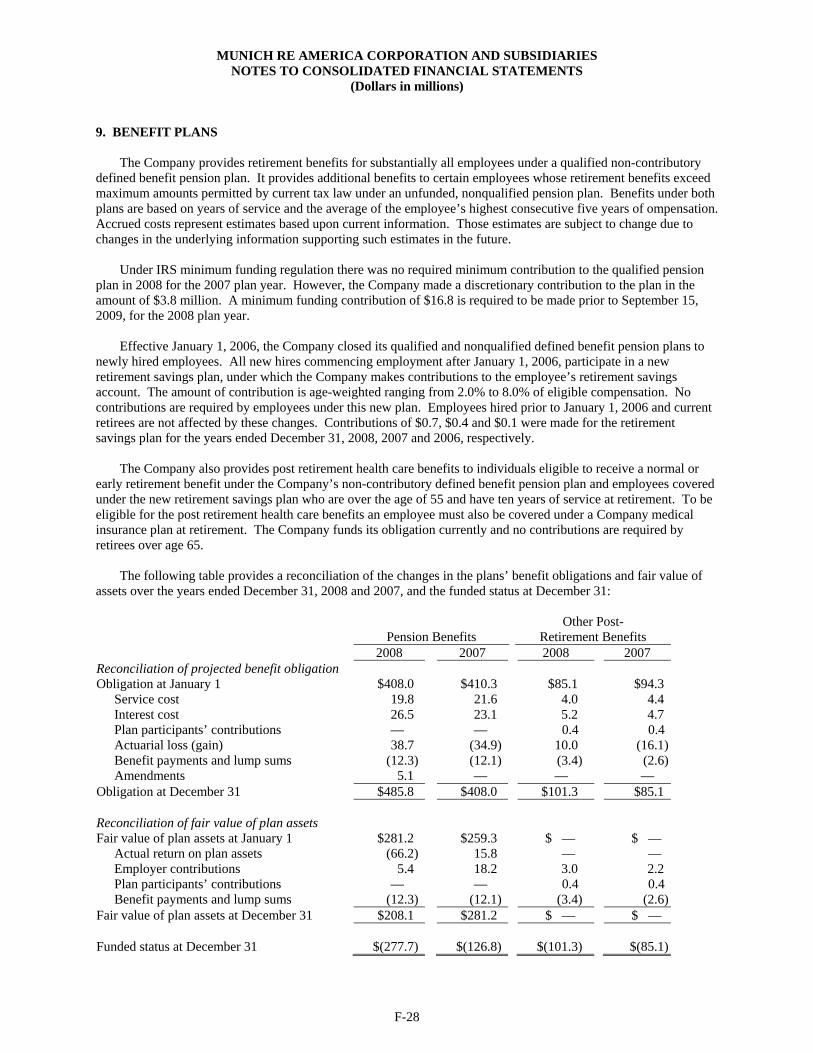

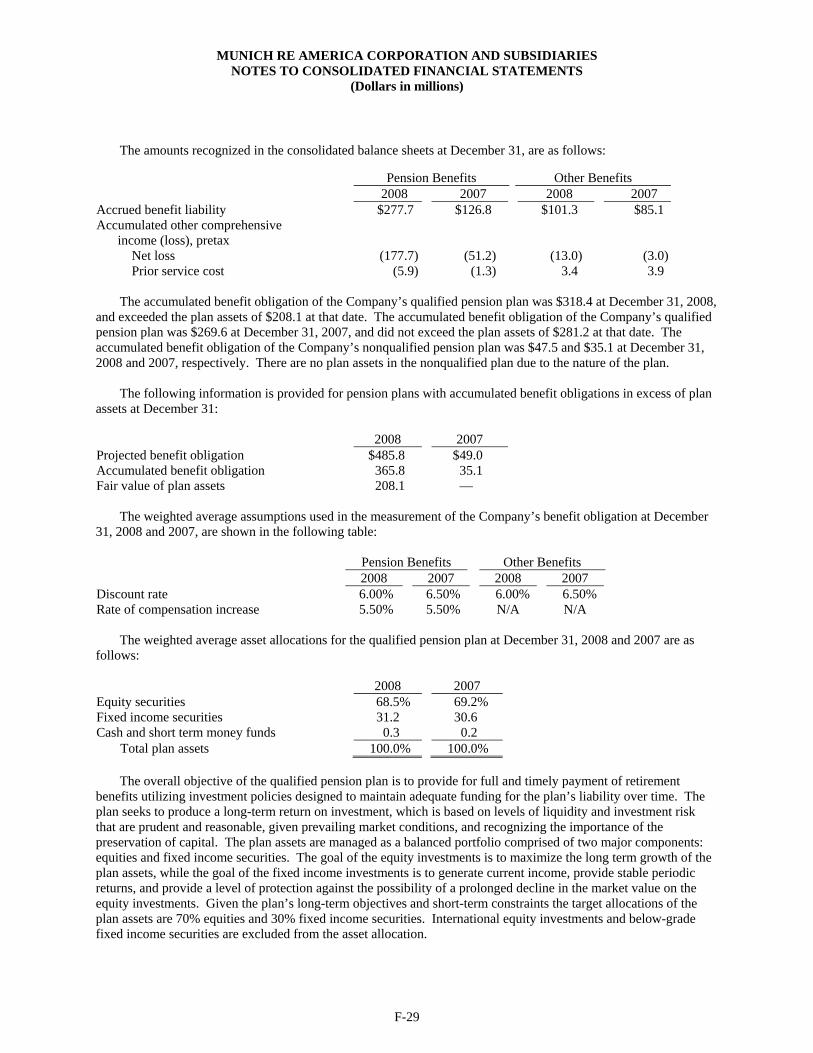

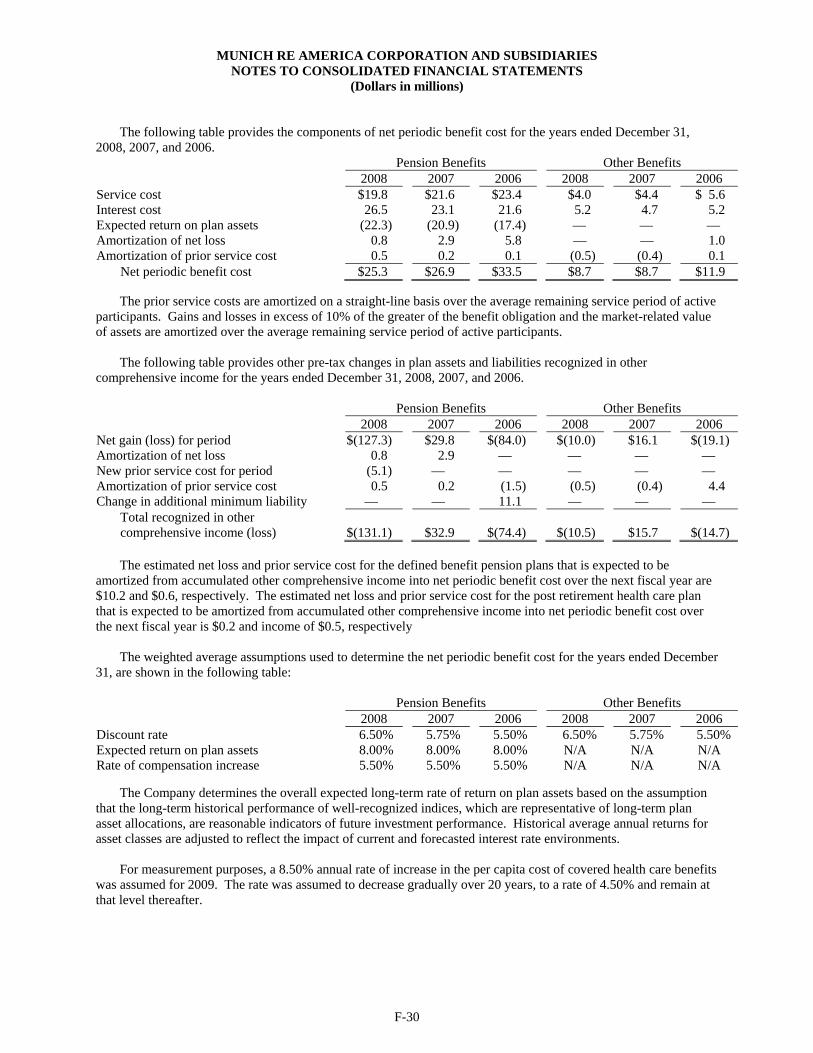

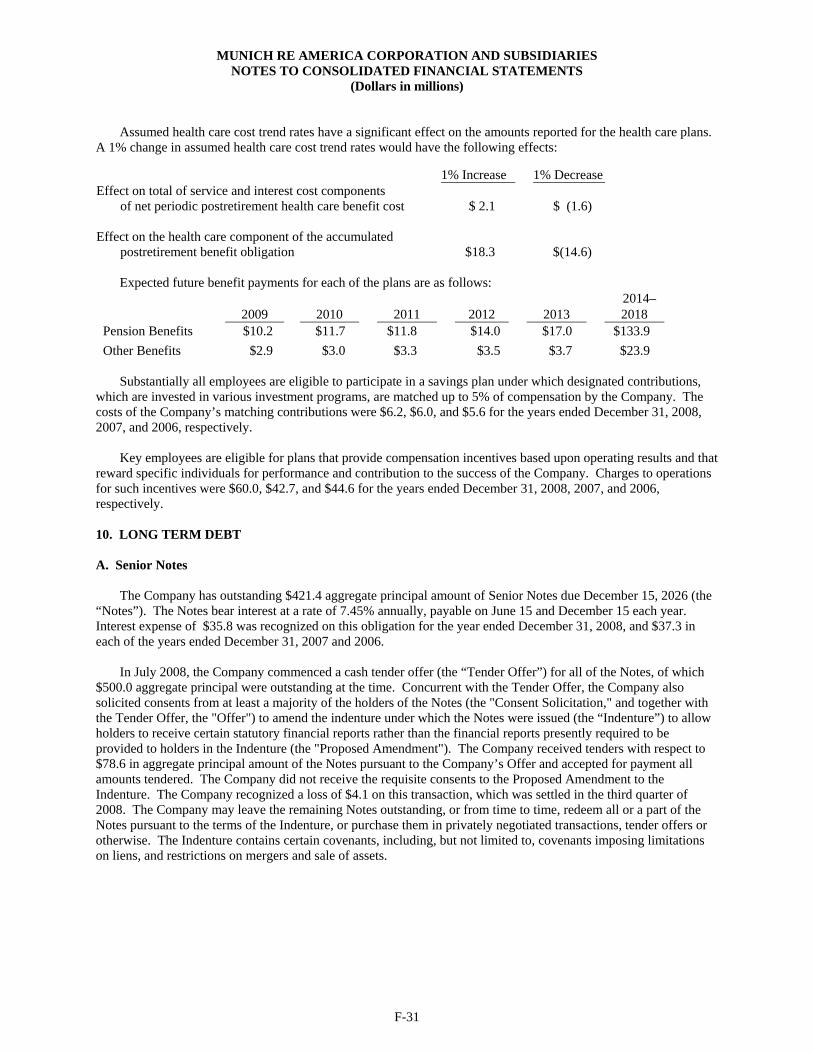

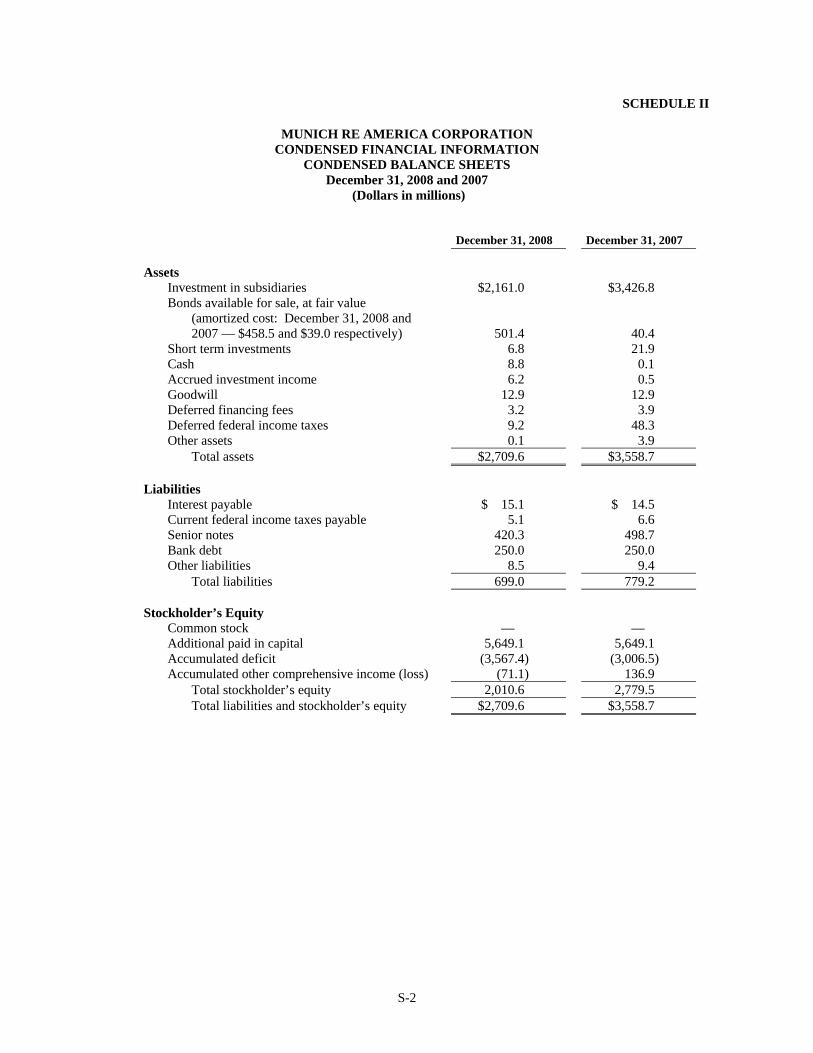

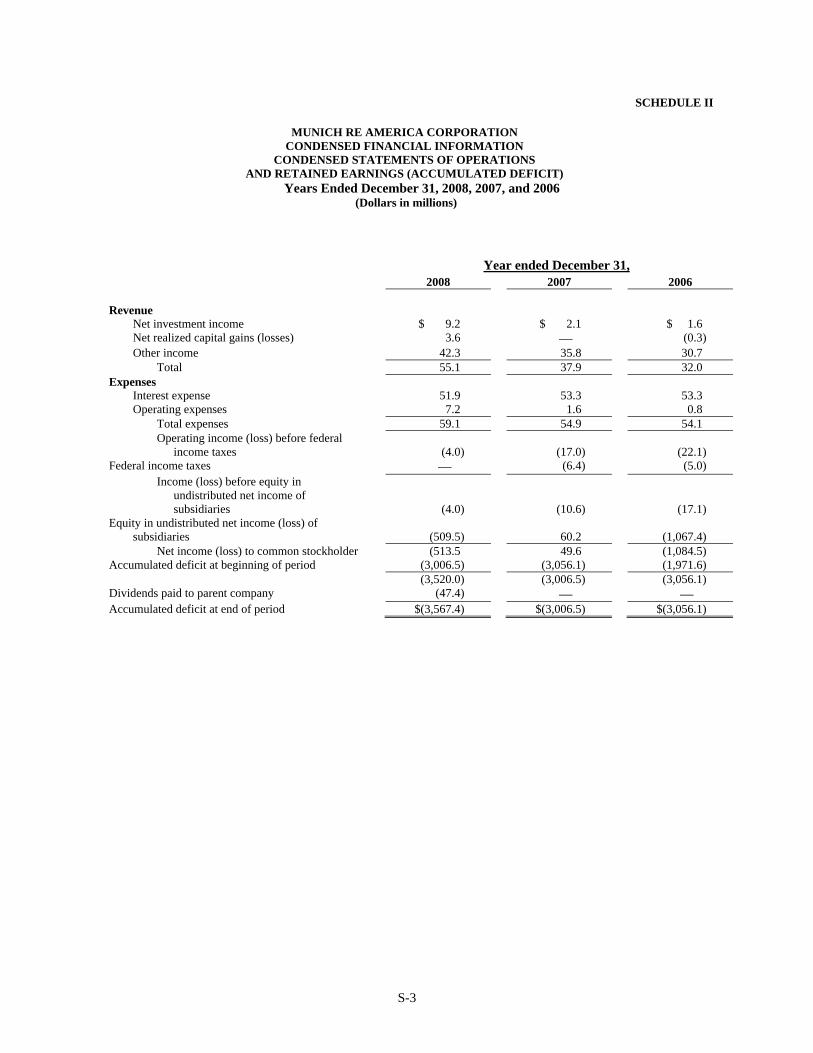

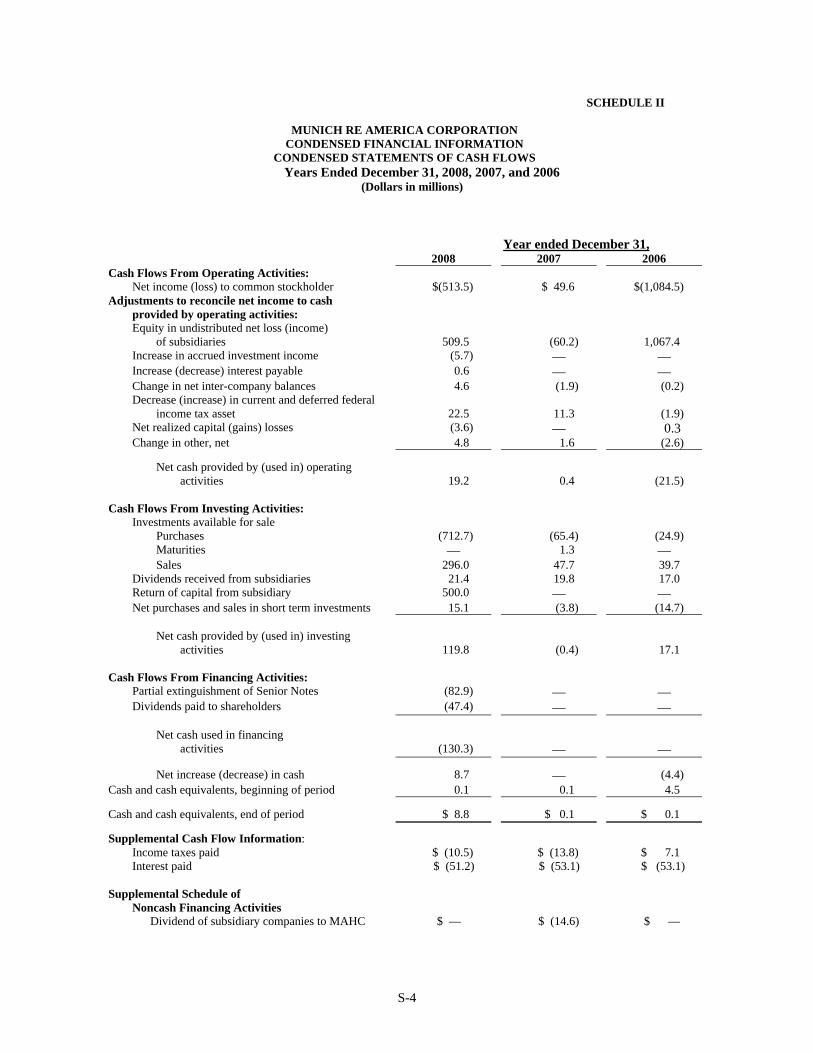

€¦ · munich re america corporation . annual report for the fiscal year ended december 31, 2008...

TRANSCRIPT

MUNICH RE AMERICA CORPORATION

Annual Report For The Fiscal Year Ended December 31, 2008 (Pursuant to Section 4.04 of the

Indenture between the Company and the holders of the Company’s 7.45% Senior Notes*)

555 College Road East PRINCETON, NEW JERSEY 08543

(609) 243-4200

*In March 2002 the Company deregistered the Notes in accordance with the rules and regulations of the Securities and Exchange Act of 1934. This Financial Report is not filed with the Securities and Exchange Commission.

March 30, 2009

MUNICH RE AMERICA CORPORATION

TABLE OF CONTENTS Page Business ...............................................................................................................................................1

Selected Financial Information of the Company .................................................................................8

Management’s Discussion and Analysis of the Company’s Results of Operations and

Financial Condition .............................................................................................................................8

Financial Statements and Supplementary Data ...................................................................................F-1

1

Unless indicated otherwise, all financial data presented herein are derived from or based on Munich Re America Corporation’s consolidated financial statements prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”). Statutory data, where specifically identified as such, are presented on a combined basis for Munich Reinsurance America Inc., American Alternative Insurance Corporation (“AAIC”), and The Princeton Excess and Surplus Lines Insurance Company (“Princeton E&S”). (These companies together are the “insurance subsidiaries”). The statutory data are derived from statutory financial statements. Such statutory financial statements are prepared in accordance with statutory accounting principles, which differ from GAAP. Business

The Company and Munich Reinsurance America Munich Re America Corporation (the “Company” or “Munich Re America”), is the holding company for various reinsurance and insurance entities which provide reinsurance, insurance and related services to insurance companies, commercial businesses, government agencies, and self-insurers in the United States. The Company’s principal subsidiary, Munich Reinsurance America Inc. (“Munich Reinsurance America”), a Delaware insurance company founded in 1917, primarily underwrites property and casualty reinsurance. The Company is one of the largest property and casualty reinsurers in the United States according to the Reinsurance Association of America, based on combined statutory gross premiums written by the insurance subsidiaries of $3,310.9 million in 2008. Other subsidiaries of the Company are American Alternative Insurance Corporation, which writes primary insurance business on an admitted basis (“AAIC”) and The Princeton Excess and Surplus Lines Insurance Company, which writes insurance coverage on a non-admitted basis (“Princeton E & S”). The Company had total assets of $27,900.9 million and stockholder’s equity of $2,010.6 million at December 31, 2008. The Company and its subsidiaries employed 1,256 persons as of December 31, 2008. Munich Re America is a wholly-owned subsidiary of Munich-American Holding Corporation, a Delaware holding company (“MAHC”), which in turn is wholly-owned by Münchener Rückversicherungs-Gesellschaft Aktiengesellschaft in München (“Munich Re Munich”), a company organized under the laws of Germany. Munich Re Munich is the world’s largest reinsurance company, based on 2007 net premiums written, according to Standard & Poor’s. The Munich Re Group, led by Munich Re Munich, includes primary insurance operations under the ERGO Insurance Group, reinsurance subsidiaries, branches, service companies and liaison offices in over 50 locations worldwide serving corporate clients in over 160 countries.

Munich Re America’s Strategy

Munich Re America’s strategy is to achieve the full potential of the U.S. property-casualty market through underwriting excellence and sustainable profitable growth over the course of the market cycle. The strategy seeks to increase its profitability through direct and broker reinsurance as well as primary insurance by:

• employing a client-centric approach to develop client strategies and reinsurance solutions that leverage the Munich Re Group’s expertise and risk appetite;

• developing closer broker relationships to support clients’ needs;

• building a dominant presence in niche primary insurance segments.

Munich Re America’s U.S. business model consists of four divisions aligned by client type. National Clients manages business placed by ceding companies through both direct production channels as well as through reinsurance intermediaries. Regional Clients manages business placed by regional insurance companies through a direct production channel. Specialty Markets focuses on alternative market clients including large commercial insurance buyers, captives, governmental entities and self insureds. Broker Market focuses its marketing efforts primarily on the top five reinsurance intermediaries (who control 90-95% of total domestic brokered reinsurance premium), but also markets to the smaller, more specialized and boutique brokers. Each U.S. property-casualty reinsurance client has a single client manager to ensure a consistent approach across business units and channels (direct and broker). The client manager serves a client’s needs throughout the reinsurance life cycle, including reinsurance placement structuring, underwriting, actuarial, claims and other services for that client. This allows the Company to develop client strategies and reinsurance solutions that leverage the Munich Re Group’s expertise and risk appetite.

2

The second part of the strategy is to develop closer broker relationships to support clients’ needs. Munich Re America’s strong partnerships with clients and brokers allows it to gain a deeper insight and understanding of the risks presented to it. In addition, the expert knowledge of risk that the Company provides its clients enhances their ability to manage their underlying risks, making these relationships more valuable to both the Company and its clients.

As part of the strategy to build a dominant presence in niche primary insurance segments, In April 2008,

MAHC completed the acquisition of The Midland Company, a highly focused provider of specialty insurance products and services through its American Modern Insurance Group, Inc (“American Modern”). American Modern controls eight property and casualty insurance companies, seven credit life insurance companies, three licensed insurance agencies and three service companies. American Modern is licensed, through its subsidiaries, to write insurance premiums in all 50 states and the District of Columbia.

Also, in December 2008, MAHC entered into an agreement to acquire the HSB Group, Inc. a Connecticut

corporation (“HSB”) from American International Group, Inc. HSB is the parent company of Hartford Steam Boiler Inspection and Insurance Company, a leading global provider of specialty insurances and inspections for commercial and industrial companies and institutions. The transaction is subject to regulatory approval and other customary closing conditions. The transaction is expected to be completed in early 2009, but no assurances can be made in this regard.

Munich Re America’s Products and Services in addition to Reinsurance

The Company offers a full range of property and casualty insurance coverage, including workers’ compensation, auto liability and physical damage, surety, marine, construction, errors and omissions, homeowners and commercial multi peril through its subsidiaries AAIC and Princeton E & S. In addition, Munich Re America HealthCare, which is closely aligned with Munich Re Munich’s global health business, provides risk management services and innovative health care solutions that use reinsurance and other risk related products and services in the health care marketplace. Munich Re America HealthCare has also established business relationships with a select group of health care management providers that offer catastrophic care and health care management services to Munich Reinsurance America’s clients.

Risks

In the course of conducting its business operations, the Company could be exposed to a variety of risks. Some of the significant risks that could affect the Company’s business, financial condition or results of operations are as follows:

Execution Risk. There are a number of risks and uncertainties that could cause actual results to differ materially from the Company’s plans with respect to its new profitable growth strategy. For example, Our future results of operations will depend in significant part on the extent to which we can implement our business strategies successfully, including our ability to realize the anticipated growth opportunities in niche markets and expanded market presence. The goals of the strategy may not be achieved as a result of (1) an inability or a delay in the integration of the company’s operations; (3) the strategy does not result in significantly improved synergies in serving the Company’s clients and brokers and (4) the Company may be adversely affected by other economic, business, and/or competitive factors.

Cyclical Market. As new capital has entered the market over the last several years during the hard market,

competition has increased, pressuring the Company’s margins and business volume. These factors have also created pressure to reduce rates in order to retain business. This is particularly difficult for facultative reinsurance, which generally benefits from companies having difficulty obtaining treaty reinsurance.

Adequacy of loss reserves. The Company regularly establishes reserves to cover its estimated liabilities for

losses and loss adjustment expenses for both reported and unreported claims. These reserves do not represent an exact calculation of liabilities. Rather, these reserves are management’s estimates of the cost to settle and administer claims. These expectations are based on facts and circumstances known at the time, predictions of future events, estimates of future trends in the severity and frequency of claims and judicial theories of liability and inflation. The establishment of appropriate reserves is an inherently uncertain process, and the Company cannot be sure that ultimate losses and related expenses will not materially exceed the Company’s reserves. To the extent that reserves prove to be inadequate in the future, the Company would have to increase its reserves and incur a charge to earnings

3

in the period such reserves are increased, which could have a material and adverse impact on our financial condition and results.

Market Volatility and Changes in Interest Rates. The Company’s investment portfolio primarily consists of fixed income securities (such as corporate debt securities and U.S. government securities). The fair value of securities in the investment portfolio may fluctuate depending on general economic and market conditions or events related to a particular issuer of securities. In addition, the Company’s fixed income investments are subject to risks of loss upon default and price volatility in reaction to changes in interest rates. Current market conditions and the instability in the global credit markets present additional risks and uncertainties for our business. In particular, continued deterioration in the credit markets could lead to additional investment losses. The severe downturn in the credit markets, reflecting uncertainties associated with the mortgage crisis, worsening economic conditions, widening of credit spreads, bankruptcies and government intervention in large financial institutions, has resulted in significant losses in our investment portfolio. Changes in the fair value of securities in the Company’s investment portfolio are reflected in the consolidated financial statements and, therefore, could affect the Company’s financial condition or results.

Collateralization Requirements. Ceding companies are increasing their demands on reinsurers to collateralize

their obligations. The Company’s policy against generally providing collateral to support its reinsurance transactions could detract from the Company’s ability to compete for some clients’ business.

Competition. Munich Reinsurance America competes in the United States reinsurance market. The property and casualty reinsurance business is highly competitive with no single competitor dominating any of the principal markets in which Munich Re America operates. Competition in the types of reinsurance in which Munich Reinsurance America is engaged is based on many factors, including the perceived overall financial strength of the reinsurer, premiums charged, contract terms and conditions, services offered, speed of claims payment and reputation and experience.

Munich Reinsurance America's competitors include independent reinsurance companies, subsidiaries or

affiliates of established worldwide insurance companies, some of which have greater financial resources than Munich Reinsurance America. Competitors write reinsurance on both a direct basis and through reinsurance brokers.

Regulation of Insurers and Reinsurers. U.S. domestic property and casualty insurers, including reinsurers, are

subject to regulation by their states of domicile and by those states in which they are licensed. Generally, state insurance departments closely regulate the rates and policy terms of primary insurance policies and agreements. Unlike many primary insurance policies, the terms and conditions of reinsurance agreements generally are not subject to regulation by any governmental authority with respect to rates or policy terms. As a practical matter, however, the rates charged by primary insurers do have an effect on the rates that can be charged by reinsurers. The regulation and supervision to which Munich Re America is subject relates primarily to licensing requirements, the standards of solvency that must be met and maintained, the nature of and limitations on investments, restrictions on the size of risks which may be insured, deposits of securities for the benefit of ceding companies, methods of accounting, periodic examinations of the financial condition and affairs of the insurance subsidiaries, and the form and content of financial statements required to be filed with state insurance regulators. In general, such regulation is for the protection of the ceding companies and, ultimately, their policyholders, rather than security holders. A primary insurer will ordinarily only enter into reinsurance agreements if the primary insurer can obtain credit for the reinsurance on its statutory financial statements. Credit is allowed when the reinsurer is licensed or accredited in a state where the primary insurer is domiciled. In addition, many states allow credit for reinsurance ceded to a reinsurer that is licensed in another state and which meets certain financial requirements, provided in some instances that the state has substantially similar reinsurance credit law requirements or the primary insurer is provided with collateral to secure the reinsurer's obligations. As writers of direct insurance, the Company’s insurance subsidiaries (AAIC and Princeton E&S) are also subject to substantial laws and regulations with respect to their coverages and operations. Management believes that Munich Reinsurance America, AAIC and Princeton E & S are in material compliance with all applicable laws and regulations pertaining to their business and operations. Munich Reinsurance America is domiciled in Delaware and licensed to transact insurance or reinsurance business in all fifty states and the District of Columbia. AAIC is also domiciled in Delaware and is licensed to transact insurance or reinsurance business in all fifty states and the District of Columbia. Princeton E&S is licensed as an admitted insurer in its state of domicile, Delaware, and is eligible to write insurance on a non-admitted basis in all other states.

4

Investment Limitations. The Delaware Code contains rules governing the types and amounts of investments that are permissible for a Delaware insurer, including the insurance subsidiaries. These rules are designed to ensure the safety and liquidity of the insurer's investment portfolio. Subject to these rules, the insurance subsidiaries may only invest in certain types of investments, including certain U.S., state and municipal government obligations, foreign securities, secured and unsecured debt instruments and preferred and common stocks of solvent U.S. and Canadian corporations, limited partnership interests, insured savings accounts, collateralized mortgage obligations, and real estate. In addition to specifically permitted types of investments, the insurance subsidiaries may make other loans or investments in an aggregate amount not exceeding 10% of its assets, provided that such loan or investment complies with the general restrictions described above, is not expressly prohibited under the Delaware Code and otherwise qualifies as a sound investment. Except for certain permitted investments in controlled insurance corporations and subsidiaries, Munich Reinsurance America is prohibited from investing in securities issued by any corporation or enterprise the controlling interest of which is, or after such investment will be, held directly or indirectly by Munich Reinsurance America or any combination of Munich Reinsurance America and its directors, officers, subsidiaries or controlling stockholder (other than the Company) and the spouses and children of the foregoing individuals. For purposes of the Delaware Code, any person directly or indirectly owning 10% or more of the voting securities of a company is presumed to have control of such company. Risk Based Capital. The Insurance Department of the State of Delaware (the “Insurance Department”) has a risk based capital (“RBC”) standard for property and casualty insurance (and reinsurance) companies which measures the amount of capital appropriate for a property and casualty insurance company to support its overall business operations in light of its size and risk profile. At December 31, 2008, Munich Reinsurance America’s RBC ratio was 447.4%, compared to 572.7% at December 31, 2007. An RBC ratio in excess of 200% generally requires no regulatory action. AAIC’s and Princeton E&S’s RBC ratios are also in excess of 200% at December 31, 2008 and 2007. Dividends. Because the operations of the Company are conducted primarily through its insurance subsidiaries, the Company is dependent upon management service agreements, dividends and tax allocation payments, primarily from Munich Reinsurance America, to meet its debt service obligations. The payment of dividends to the Company by the insurance subsidiaries is subject to limitations imposed by the Insurance Department. Under the Delaware Insurance Code, no Delaware insurer may pay any (i) dividend or distribution without 10 days' prior notice to the Insurance Department or (ii) "extraordinary" dividend or distribution until (a) 30 days after the Delaware Insurance Commissioner has received notice of the declaration thereof and has not within such period disapproved such payment or (b) the Delaware Insurance Commissioner has approved such payment within the 30-day period. Under the Delaware Insurance Code, an "extraordinary" dividend for a property and casualty insurer is a dividend, the amount of which, when taken together with all other dividends made in the preceding twelve months, exceeds the greater of (i) 10% of an insurer's statutory surplus as of the end of the prior calendar year or (ii) the insurer's statutory net income, not including realized capital gains, for the prior calendar year. Dividends must be paid from available unassigned funds, as set forth in the most recent annual statement of the insurer. Based on these restrictions, Munich Reinsurance America cannot pay dividends in 2009 without the prior approval of the Insurance Department. Statutory Financial Condition Examinations. As part of its general regulatory oversight process, the Insurance Department usually conducts financial condition examinations of domiciled insurers and reinsurers every three to five years, or at such other times as is deemed appropriate by the Insurance Commissioner. In 2009 the Insurance Department will begin a financial condition examination of the Company’s insurance subsidiaries for the triennial period 2006 through 2008. Insurance Regulatory Information System Ratios. The NAIC annually calculates thirteen financial ratios to assist state insurance departments in monitoring the financial condition of insurance companies. Results are compared against a “usual range” of results for each ratio, established by the NAIC. In 2008, Munich Reinsurance America had one ratio outside of the usual range: the gross change in policyholders’ surplus ratio was negative 18% compared to the usual range of negative 10% to positive 50%. The gross change in policyholders’ surplus ratio fell outside the usual range, primarily as a result of a $500.0 million return of capital from Munich Reinsurance America to the Company. Management believes the results of this ratio are not an indication of financial concern.

5

Legal Proceedings

The Company is involved in non-claim litigation incidental to its business principally related to insurance company insolvencies or liquidation proceedings in the ordinary course of business. Also, in the ordinary course of business, the Company is sometimes involved in adversarial proceedings incidental to its insurance and reinsurance business. The amounts at risk in these proceedings are taken into account in setting loss reserves.

The Company is cooperating with various federal and state governmental investigations as more fully described

below. Also, the Company is a defendant in a number of adversarial proceedings described below involving activities incidental to the investigations.

Based upon its familiarity with or review and analysis of such matters, the Company believes that none of the

pending litigation matters will have a material adverse effect on the consolidated financial statements of the Company. However, no assurance can be given as to the ultimate outcome of any such litigation matters.

Investigations with Respect to Broker Compensation and Certain Loss Mitigation Insurance Products. In October, 2004, the Attorney General of the State of New York filed a civil lawsuit against Marsh & McLennan Companies, Inc. and Marsh Inc. for alleged fraud and anti-competitive practices in the insurance industry. The lawsuit, an outgrowth of the Attorney General's investigation into broker compensation practices, specifically, agreements known as "placement service agreements" or "contingent commission arrangements", was settled in 2005. Munich Reinsurance America, including Specialty Markets, formerly known as Munich-American RiskPartners, a division of Munich Reinsurance America, was referenced in the Attorney General’s complaint and received subpoenas with respect to the Attorney General’s investigation. Subpoenas from other state Attorneys General and inquiries from several state insurance departments have also been received. Although settlement discussions have not been pursued by the various Attorneys General, management believes that settlement discussions may be continued at any time upon little or no notice with these regulators. On November 25, 2008 Munich Reinsurance America, Inc., (and its insurer affiliates American Alternative Insurance Corporation, and The Princeton Excess and Surplus Lines Insurance Company) entered into a settlement and cooperation agreement with the Attorney General of the State of Ohio and the Ohio Department of Insurance whereby the State of Ohio agreed to terminate its inquiries with respect to the Company and to fully release the Company from all claims, relating thereto, and Munich Reinsurance America, Inc and its insurer affiliates agreed to continue to cooperate in any ongoing investigations. No monetary payment was associated with this agreement with the Ohio authorities.

The U.S. Securities and Exchange Commission (“SEC”), the New York Attorney General, the Department of

Justice (U.S. Attorney’s Office for the Southern District of NY) and the States of Georgia and Delaware have made inquiries with respect to "certain loss mitigation insurance products". Munich Reinsurance America has responded to all such requests for information and will continue to cooperate fully with such inquiries.

Management has established a reserve of $5.0 million in connection with certain of the above referenced

proceedings. In view of the uncertainties discussed above, the Company could incur charges in excess of the currently established accrual and, to the extent available, any third party recoveries. In the opinion of management, any such future charges, individually or in the aggregate, would not have a material adverse effect on the consolidated financial statements of the Company.

Class Action Lawsuits. Munich Reinsurance America and certain of its affiliates have been named as defendants

in ten class actions brought in various state and U.S. federal courts, all of which have been transferred by the Judicial Panel on Multidistrict Litigation to the U.S. District Court for the District of New Jersey and consolidated in the action entitled In Re Insurance Brokerage Antitrust Litigation (“In Re Insurance Brokerage”).

All ten actions are essentially similar as each relies heavily on the information stated in the New York Attorney

General’s complaint against Marsh discussed above which has now been settled by Marsh. The complaints, in summary, allege that the broker defendants failed to adequately disclose contingent fee arrangements or placement services agreements and in so doing breached their fiduciary duty as brokers to the insureds. In addition, these complaints allege that the insurer defendants, including Munich Reinsurance America and certain of its affiliates, violated the Federal Racketeer Influenced and Corrupt Organization Act and that collectively, the defendants entered into a conspiracy and a pattern of “racketeering activity” by engaging in a common course of conduct to steer insurance business to certain carriers, to manipulate the bidding process for insurance placements, and thereby engaged in a “broker/insurer enterprise” with the resulting unlawful effect of manipulating the market for insurance. Other allegations include violations of the federal and state anti-trust laws, the duty of fiduciary care, breach of

6

contract, misrepresentation, and other states’ anti-trust and unfair and deceptive practices laws. The relief asked for includes certification of the respective class, treble damages, an accounting with respect to contingent fees by each defendant, and other relief, including costs and fees. An amended complaint in In Re Insurance Brokerage was filed on August 15, 2005. On April 5, 2007, the Court granted the defendants' motion to dismiss the complaint, ruling that plaintiffs did not meet their burden to sufficiently allege a “conspiracy” to violate the Sherman Antitrust act nor to sufficiently allege violations of the RICO statute and other laws.

The Court permitted the plaintiffs to amend their complaint within thirty days which plaintiffs did on May 22,

2007. The Defendants then made motions to dismiss the newly-amended complaint on June 21, 2007 and the Plaintiffs responded in July 2007. The Court granted the Defendant's motion to dismiss the Antitrust and RICO claims in August and September 2007. The Plaintiffs filed an appeal in October 2007. All further discovery has been stayed pending the appeal. Munich Reinsurance America will continue to aggressively defend these matters.

Operating Controls

Forecasting and Results Monitoring. To establish appropriate accident year loss ratios for future periods, the Company first quantifies the condition of the current portfolio. Then the Company considers the impact of market conditions to establish prudent loss ratios for the prospective period. The intent is to establish loss reserves for the accident year, which are sufficient in aggregate to fund future claim payments, and to avoid the need for future reserve increases after the end of the accident period.

Once the planning process is complete, the Company begins a rigorous results monitoring process to ensure that assumptions employed in building plan figures hold true. The key metrics that are monitored over the course of the year include: effective rate change on primary and reinsurance renewals; adherence to pricing guidelines; mix of business (including concentration levels in special risk areas); commission levels; and premium production. In addition, the Company reviews it’s largest client groups to ensure that the relationships are yielding results that are consistent with the Company’s strategy. The focus is on solid profitability.

To ensure that prior year reserves are adequate, the Company frequently monitors the emergence of actual reported and paid losses as compared to projected amounts. If actual paid and reported figures are higher than the amounts expected, then this information may be an indicator that loss reserves need to be increased. This information is used to supplement the formal reserve reviews conducted by the Company’s actuarial staff. The objective is to continuously have an adequate reserve position and integrity in the balance sheet at the close of each financial period.

The Company believes the planning and results monitoring process addresses many of the inherent risks associated with the casualty reinsurance product. Specifically, the reinsurance product is priced and sold using estimates of the ultimate costs to be incurred by the reinsurance company. The final costs are only known in hindsight. To ensure that financial statements are appropriately stated, the Company must continually re-examine the assumptions and data leading to the estimates of these ultimate costs. This estimation process is particularly difficult for casualty reinsurance providers given the complexity of many factors involved including: lengthy reporting and settlement lags associated with liability cases; and evolving judicial decisions, which can expand liability for reinsurers.

Aggregate Controls. Munich Re America closely manages and monitors its aggregations. Risk management

aggregation budgets have been established for natural catastrophe, terrorism, professional liability, political risk, worker's compensation losses resulting from natural perils and trade credit. Additional risk concentration exposures are continually being evaluated. The Company works closely with the Corporate Underwriting unit of Munich Re Munich to establish global aggregation budgets, and usage is monitored on a quarterly basis. The Company also uses group expertise in addition to a natural catastrophe-modeling tool to price and model the Company's natural peril exposures. Munich Re America uses a terrorism modeling tool in addition to the Company's own probable maximum loss estimation procedures to track terrorism exposure.

Strong Underwriting Audit Process. The Company has an extensive internal underwriting audit process and works closely with the Corporate Underwriting unit of Munich Re Munich in order to monitor adherence to underwriting guidelines and maintain best practices. Supplementing the on-site audit process is an individual account review of hand-selected programs as needed.

7

Integrated Risk Management (“IRM”). The IRM division’s role is to coordinate decentralized risk management processes into an enterprise risk governance process through the Risk Management Committee of Munich Reinsurance America. The functions of this Board Committee are closely aligned with the Munich Re Group Underwriting and Risk Committee. IRM is also responsible for risk modeling and support for the introduction of Munich Re Group risk management applications at the business unit level. In addition to the underwriting risk management activities listed above, Munich Reinsurance America closely manages and monitors its investment risks within tolerances and limits established at the Munich Re Group level.

8

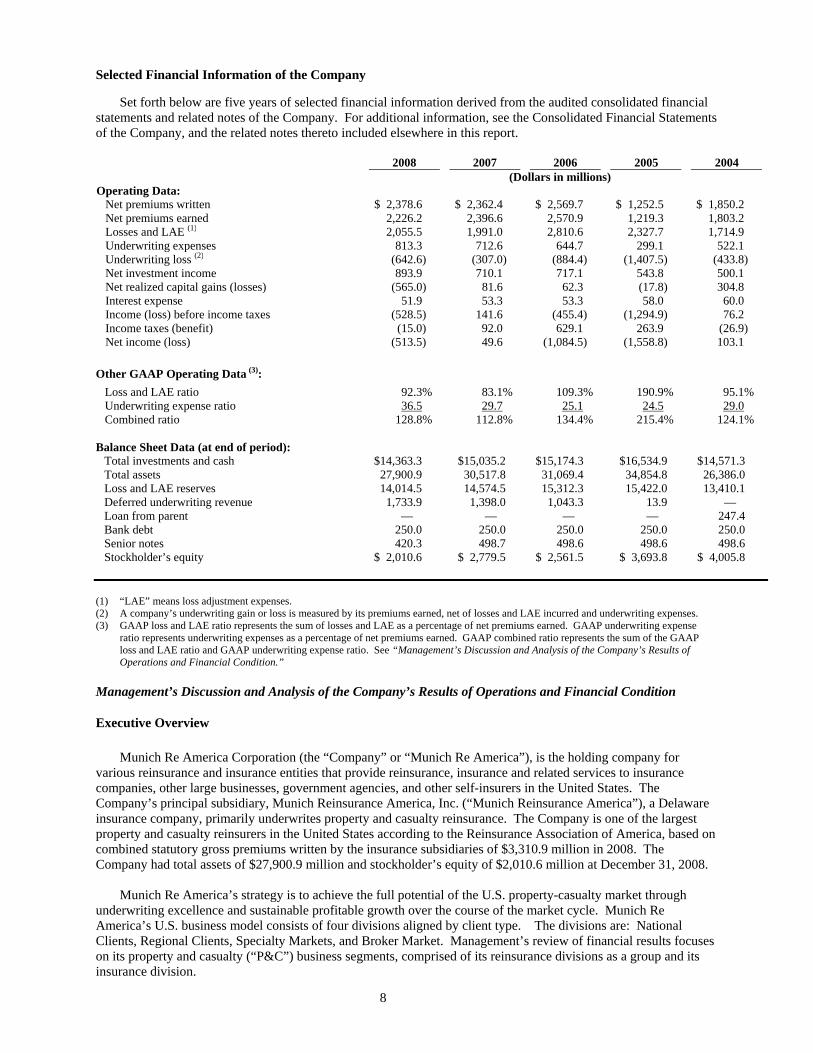

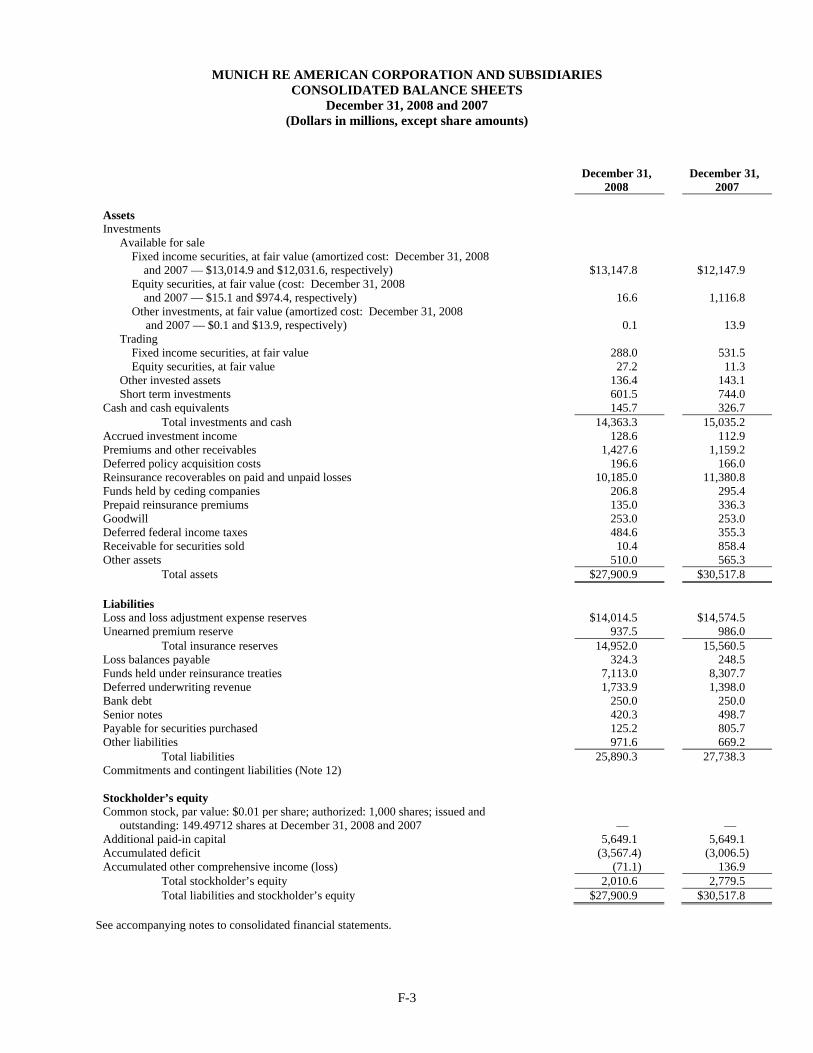

Selected Financial Information of the Company Set forth below are five years of selected financial information derived from the audited consolidated financial statements and related notes of the Company. For additional information, see the Consolidated Financial Statements of the Company, and the related notes thereto included elsewhere in this report.

2008 2007 2006 2005 2004 (Dollars in millions)

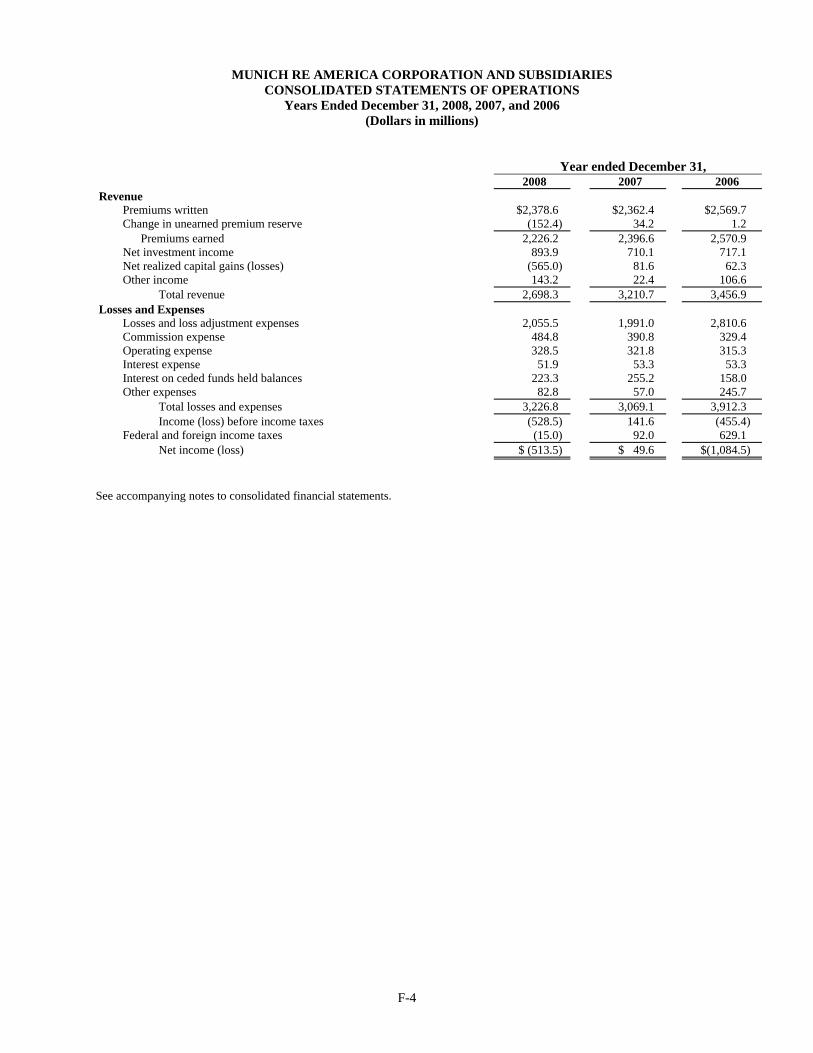

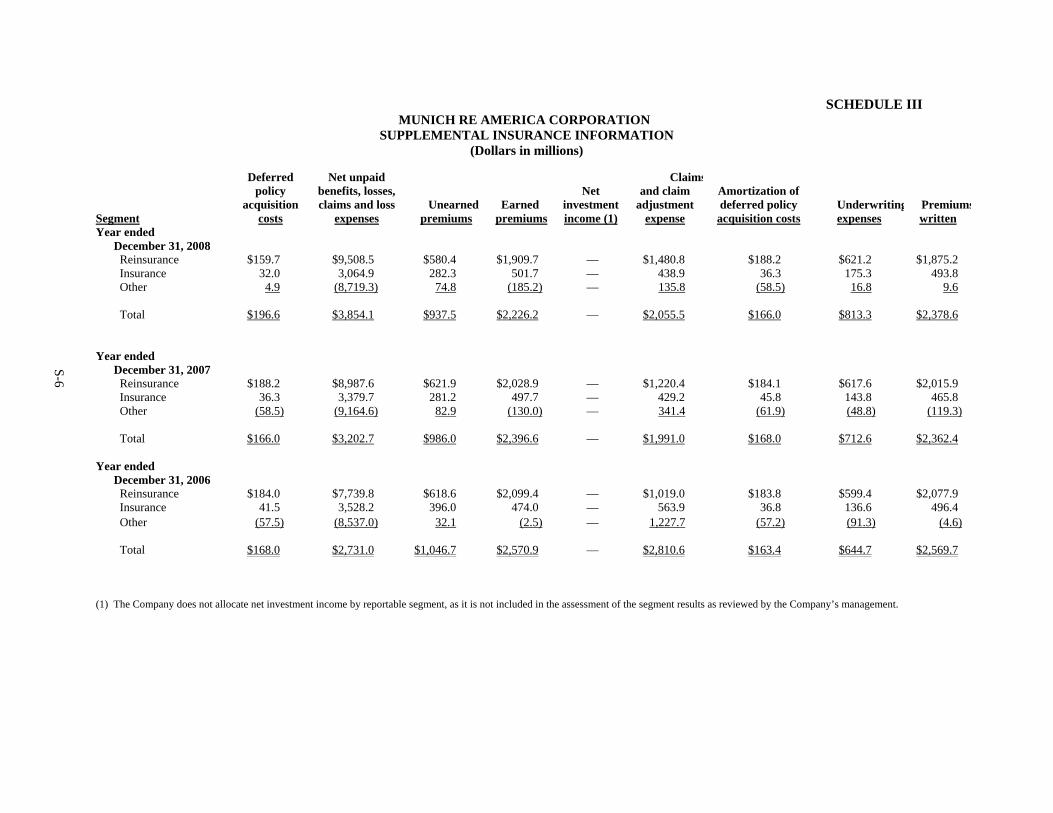

Operating Data: Net premiums written $ 2,378.6 $ 2,362.4 $ 2,569.7 $ 1,252.5 $ 1,850.2 Net premiums earned 2,226.2 2,396.6 2,570.9 1,219.3 1,803.2 Losses and LAE (1) 2,055.5 1,991.0 2,810.6 2,327.7 1,714.9 Underwriting expenses 813.3 712.6 644.7 299.1 522.1 Underwriting loss (2) (642.6) (307.0) (884.4) (1,407.5) (433.8) Net investment income 893.9 710.1 717.1 543.8 500.1 Net realized capital gains (losses) (565.0) 81.6 62.3 (17.8) 304.8 Interest expense 51.9 53.3 53.3 58.0 60.0 Income (loss) before income taxes (528.5) 141.6 (455.4) (1,294.9) 76.2 Income taxes (benefit) (15.0) 92.0 629.1 263.9 (26.9) Net income (loss) (513.5) 49.6 (1,084.5) (1,558.8) 103.1 Other GAAP Operating Data (3): Loss and LAE ratio 92.3% 83.1% 109.3% 190.9% 95.1% Underwriting expense ratio 36.5 29.7 25.1 24.5 29.0

Combined ratio 128.8% 112.8% 134.4% 215.4% 124.1% Balance Sheet Data (at end of period): Total investments and cash $14,363.3 $15,035.2 $15,174.3 $16,534.9 $14,571.3 Total assets 27,900.9 30,517.8 31,069.4 34,854.8 26,386.0 Loss and LAE reserves 14,014.5 14,574.5 15,312.3 15,422.0 13,410.1 Deferred underwriting revenue 1,733.9 1,398.0 1,043.3 13.9 — Loan from parent — — — — 247.4 Bank debt 250.0 250.0 250.0 250.0 250.0 Senior notes 420.3 498.7 498.6 498.6 498.6 Stockholder’s equity $ 2,010.6 $ 2,779.5 $ 2,561.5 $ 3,693.8 $ 4,005.8 (1) “LAE” means loss adjustment expenses. (2) A company’s underwriting gain or loss is measured by its premiums earned, net of losses and LAE incurred and underwriting expenses. (3) GAAP loss and LAE ratio represents the sum of losses and LAE as a percentage of net premiums earned. GAAP underwriting expense

ratio represents underwriting expenses as a percentage of net premiums earned. GAAP combined ratio represents the sum of the GAAP loss and LAE ratio and GAAP underwriting expense ratio. See “Management’s Discussion and Analysis of the Company’s Results of Operations and Financial Condition.”

Management’s Discussion and Analysis of the Company’s Results of Operations and Financial Condition

Executive Overview

Munich Re America Corporation (the “Company” or “Munich Re America”), is the holding company for various reinsurance and insurance entities that provide reinsurance, insurance and related services to insurance companies, other large businesses, government agencies, and other self-insurers in the United States. The Company’s principal subsidiary, Munich Reinsurance America, Inc. (“Munich Reinsurance America”), a Delaware insurance company, primarily underwrites property and casualty reinsurance. The Company is one of the largest property and casualty reinsurers in the United States according to the Reinsurance Association of America, based on combined statutory gross premiums written by the insurance subsidiaries of $3,310.9 million in 2008. The Company had total assets of $27,900.9 million and stockholder’s equity of $2,010.6 million at December 31, 2008. Munich Re America’s strategy is to achieve the full potential of the U.S. property-casualty market through underwriting excellence and sustainable profitable growth over the course of the market cycle. Munich Re America’s U.S. business model consists of four divisions aligned by client type. The divisions are: National Clients, Regional Clients, Specialty Markets, and Broker Market. Management’s review of financial results focuses on its property and casualty (“P&C”) business segments, comprised of its reinsurance divisions as a group and its insurance division.

9

Revenues Revenues are derived principally from the following:

• net premiums earned, which are gross premiums assumed from clients, earned during the accounting period, net of premiums ceded to retrocessionaires;

• net investment income earned on invested assets;

• realized capital gains on the sale of investments, and

• other income, which includes interest income on underwriting balances and margin income on underwriting

deposit balances. Expenses Expenses consist predominately of the following:

• losses and loss adjustment expenses, including estimates for losses and loss adjustment expenses incurred during the period and changes in estimates from prior periods, net of those insurance losses and loss adjustment expenses ceded to retrocessionnaires;

• commissions and other underwriting expenses, which consist of commissions paid to clients, in addition to

operating expenses related to the production and underwriting of reinsurance, less ceding commissions received under the Company’s retrocessional contracts;

• interest expense on debt obligations,

• interest on ceded funds held balances, predominantly on retrocessional programs with Munich Re Munich,

and

• other expenses, which include benefit plan costs, allowance for doubtful accounts, foreign exchange gains and losses on foreign-denominated assets and liabilities other than investments, and other expenses.

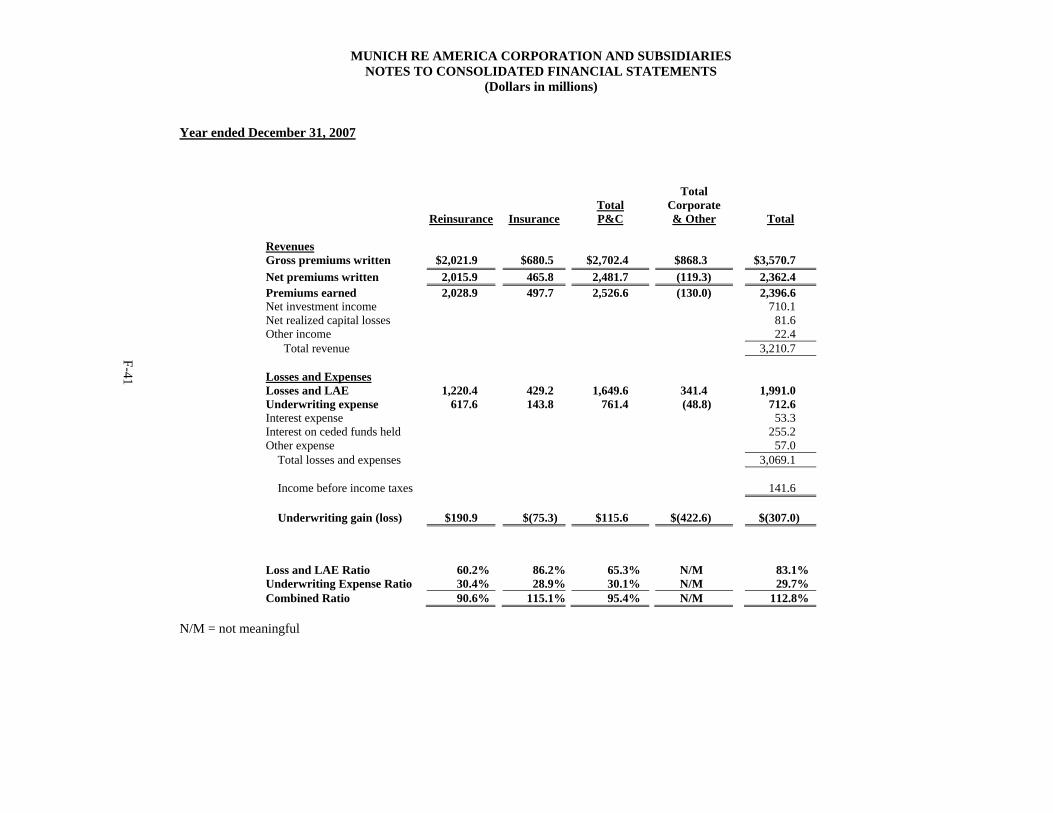

Results of Operations Year Ended December 31, 2008, Compared with Year Ended December 31, 2007 Underwriting Results and Combined Ratio A key measure of the financial success of a reinsurance company is a positive underwriting result, or an underwriting profit. A major goal of a successful reinsurance company is to produce an underwriting profit, exclusive of investment income. A company’s underwriting result is measured by its premiums earned, net of losses and LAE incurred and underwriting expenses. If underwriting is not profitable, investment income must be used to cover underwriting losses. Combined ratio is also an industry-wide measure of a reinsurance company’s profitability. Combined ratio is the sum of the loss ratio and the underwriting expense ratio. The combined ratio is calculated, on a GAAP basis, as the sum of the losses and loss adjustment expenses incurred and underwriting expenses, divided by net premiums earned. These ratios are relative measurements that describe the cost of losses and expenses for every $100 of net premiums earned. The combined ratio presents the total cost per $100 of premium production. A combined ratio below 100 demonstrates underwriting profit; a combined ratio above 100 demonstrates underwriting loss. In addition to reviewing the overall underwriting results and ratios of the Company at a corporate, or consolidated financial statement level, management focuses on “property and casualty underwriting results” in evaluating the underwriting performance of the Company. The property and casualty (“P&C”) underwriting results represent the aggregated results of the P&C business segments. The underwriting results of business segments in

10

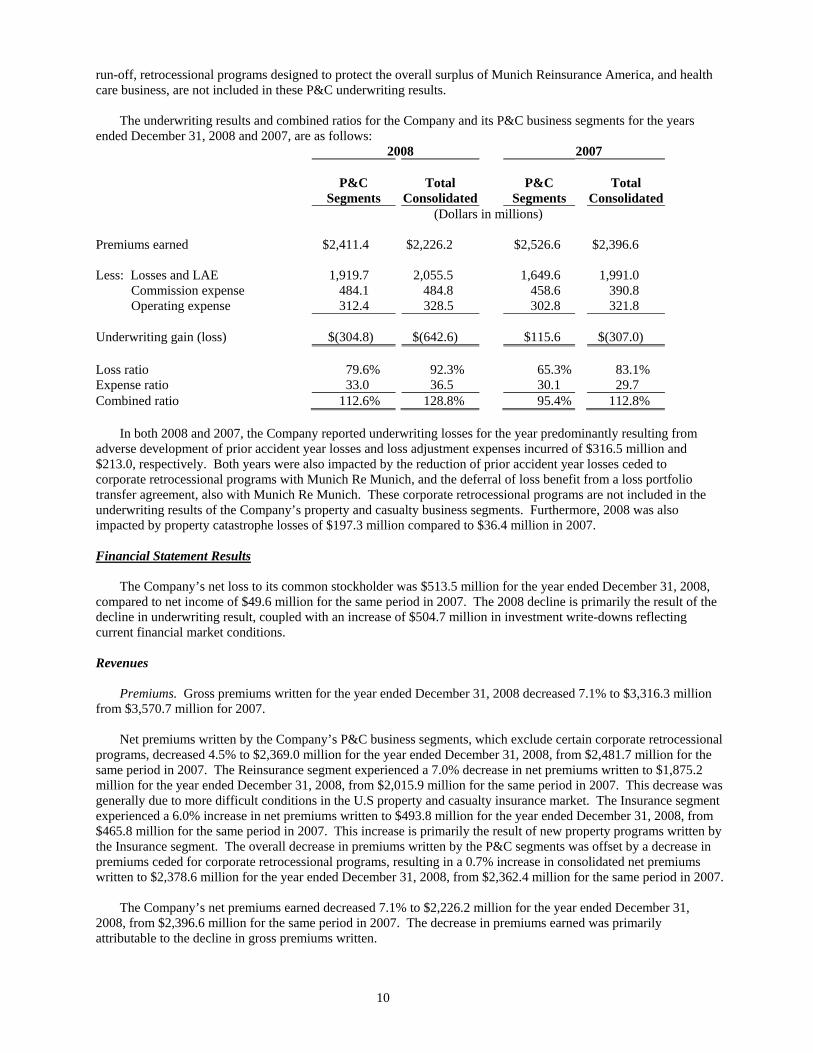

run-off, retrocessional programs designed to protect the overall surplus of Munich Reinsurance America, and health care business, are not included in these P&C underwriting results. The underwriting results and combined ratios for the Company and its P&C business segments for the years ended December 31, 2008 and 2007, are as follows:

2008 2007

P&C Segments

Total

Consolidated

P&C

Segments

Total

Consolidated (Dollars in millions)

Premiums earned $2,411.4 $2,226.2 $2,526.6 $2,396.6

Less: Losses and LAE 1,919.7 2,055.5 1,649.6 1,991.0 Commission expense 484.1 484.8 458.6 390.8 Operating expense 312.4 328.5 302.8 321.8 Underwriting gain (loss) $(304.8) $(642.6) $115.6 $(307.0) Loss ratio 79.6% 92.3% 65.3% 83.1% Expense ratio 33.0 36.5 30.1 29.7 Combined ratio 112.6% 128.8% 95.4% 112.8% In both 2008 and 2007, the Company reported underwriting losses for the year predominantly resulting from adverse development of prior accident year losses and loss adjustment expenses incurred of $316.5 million and $213.0, respectively. Both years were also impacted by the reduction of prior accident year losses ceded to corporate retrocessional programs with Munich Re Munich, and the deferral of loss benefit from a loss portfolio transfer agreement, also with Munich Re Munich. These corporate retrocessional programs are not included in the underwriting results of the Company’s property and casualty business segments. Furthermore, 2008 was also impacted by property catastrophe losses of $197.3 million compared to $36.4 million in 2007. Financial Statement Results The Company’s net loss to its common stockholder was $513.5 million for the year ended December 31, 2008, compared to net income of $49.6 million for the same period in 2007. The 2008 decline is primarily the result of the decline in underwriting result, coupled with an increase of $504.7 million in investment write-downs reflecting current financial market conditions. Revenues Premiums. Gross premiums written for the year ended December 31, 2008 decreased 7.1% to $3,316.3 million from $3,570.7 million for 2007. Net premiums written by the Company’s P&C business segments, which exclude certain corporate retrocessional programs, decreased 4.5% to $2,369.0 million for the year ended December 31, 2008, from $2,481.7 million for the same period in 2007. The Reinsurance segment experienced a 7.0% decrease in net premiums written to $1,875.2 million for the year ended December 31, 2008, from $2,015.9 million for the same period in 2007. This decrease was generally due to more difficult conditions in the U.S property and casualty insurance market. The Insurance segment experienced a 6.0% increase in net premiums written to $493.8 million for the year ended December 31, 2008, from $465.8 million for the same period in 2007. This increase is primarily the result of new property programs written by the Insurance segment. The overall decrease in premiums written by the P&C segments was offset by a decrease in premiums ceded for corporate retrocessional programs, resulting in a 0.7% increase in consolidated net premiums written to $2,378.6 million for the year ended December 31, 2008, from $2,362.4 million for the same period in 2007. The Company’s net premiums earned decreased 7.1% to $2,226.2 million for the year ended December 31, 2008, from $2,396.6 million for the same period in 2007. The decrease in premiums earned was primarily attributable to the decline in gross premiums written.

11

Investment Income. Net investment income increased 25.9% to $893.9 million for the year ended December 31, 2008, from $710.1 million for the same period in 2007. This increase is primarily due to increases in net income from fixed income and equity futures contracts and foreign exchange forward contracts, partially offset by lower book yields on the investment portfolio. The Company realized net capital losses of $565.0 million for the year ended December 31, 2008, compared to net capital gains of $81.6 million for the same period in 2007. The 2008 period included net capital gains of $26.1 million recognized on the sale of common equities, fixed income securities and other available-for-sale investments, offset by write-downs of $591.0 million of fixed income, common equities and other available-for-sale investments, as the decline in the fair value of these securities was considered to be “other than temporary.” These declines were due in part to changing spreads, yields, and the current illiquidity in the market. Management believed that it did not have the intent to hold these securities until such time as they recovered in value or until their scheduled maturity. The 2007 period included net capital gains of $167.9 million recognized on the sale of common equities, fixed income securities and other available-for-sale investments, offset by write-downs of $86.3 million of fixed income, common equities and other available-for-sale investments. Other Income. Other income increased to $143.2 million for the year ended December 31, 2008, from $22.4 million for the same period in 2007. This increase is primarily related to unrealized foreign exchange gains of $103.3 million on loss reserves and other foreign-denominated assets and liabilities other than investments, and income related to the Company’s ceded reinsurance contracts accounted for as deposits. Expenses Losses and Loss Adjustment Expenses. Losses and LAE incurred increased 3.2% to $2,055.5 million for the year ended December 31, 2008, from $1,991.0 million for the same period in 2007. This increase is primarily attributable to losses and LAE related to prior accident years of $316.5 million in 2008, compared to $213.0 million in 2007. The Company incurred net catastrophe losses of $197.3 million for the year ended December 31, 2008, compared to catastrophe losses of $36.4 million for the 2007 period. The 2008 losses were predominantly related to Hurricanes Ike and Gustav and Midwest Windstorms. Reflecting the indications of the Company’s ongoing monitoring of loss reserves and its in-depth annual reserve review, in 2008 the Company increased loss and LAE reserves by $155.2 million, excluding the impact of certain corporate retrocessional programs with Munich Re Munich. This overall reserve increase was attributable to an increase of $409.2 million for accident years 2001 and prior, primarily attributable to excess workers compensation and asbestos liability, partially offset by an aggregate decrease of $254.0 million for accident years 2002 and subsequent, primarily attributable to property and automobile liability lines. The decreased losses for accident years 2002 and subsequent were partially offset by reductions in losses ceded to various corporate retrocessional programs with Munich Re Munich. The increased losses for accident year 2001 and prior, were primarily ceded to a loss portfolio transfer agreement, also with Munich Re Munich; however, because this agreement is accounted for as retroactive reinsurance, the majority of these recoveries were deferred and will be recognized in income over the settlement period of the underlying claims. The reduced cessions, coupled with the deferral of the benefit from the LPT program, increased the impact of the prior accident year losses to $316.5 million on a net basis for the year ended December 31, 2008. Similar to 2008, the 2007 period was also impacted by increased loss and LAE reserves for accident years 2001 and prior, and decreased loss and LAE reserves for accident years 2002 and subsequent. (See Year Ended December 31, 2007, Compared with Year Ended December 31, 2006 – Losses and Loss Adjustment Expenses.) Underwriting Expense. Underwriting expense, consisting of commission expense plus operating expense, increased 14.1% to $813.3 million for the year ended December 31, 2008, from $712.6 million for the same period in 2007. This increase was due to a 24.1% increase in net commission expense to $484.8 million for the year ended December 31, 2008, from $390.8 million for the same period in 2007. The increase in commission expense is primarily attributable to a lower level of commission benefit from the corporate retrocessional programs and commission adjustments related to a retrocessional program in the 2008 period, compared to commission benefits in the Insurance segment in the 2007 period. Operating expenses increased 2.1% to $328.5 million for the year ended December 31, 2008 from $321.8 million for the year ended December 31, 2007. This increase was primarily due to increased compensation expenses for the 2008 period.

12

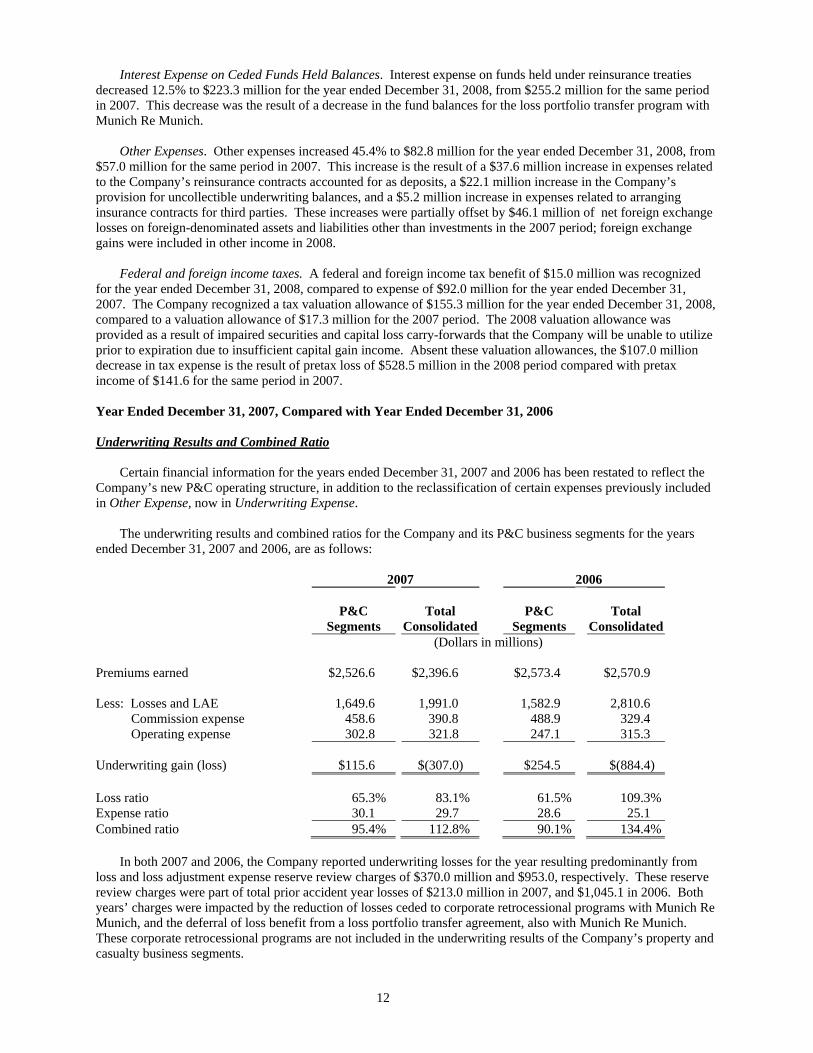

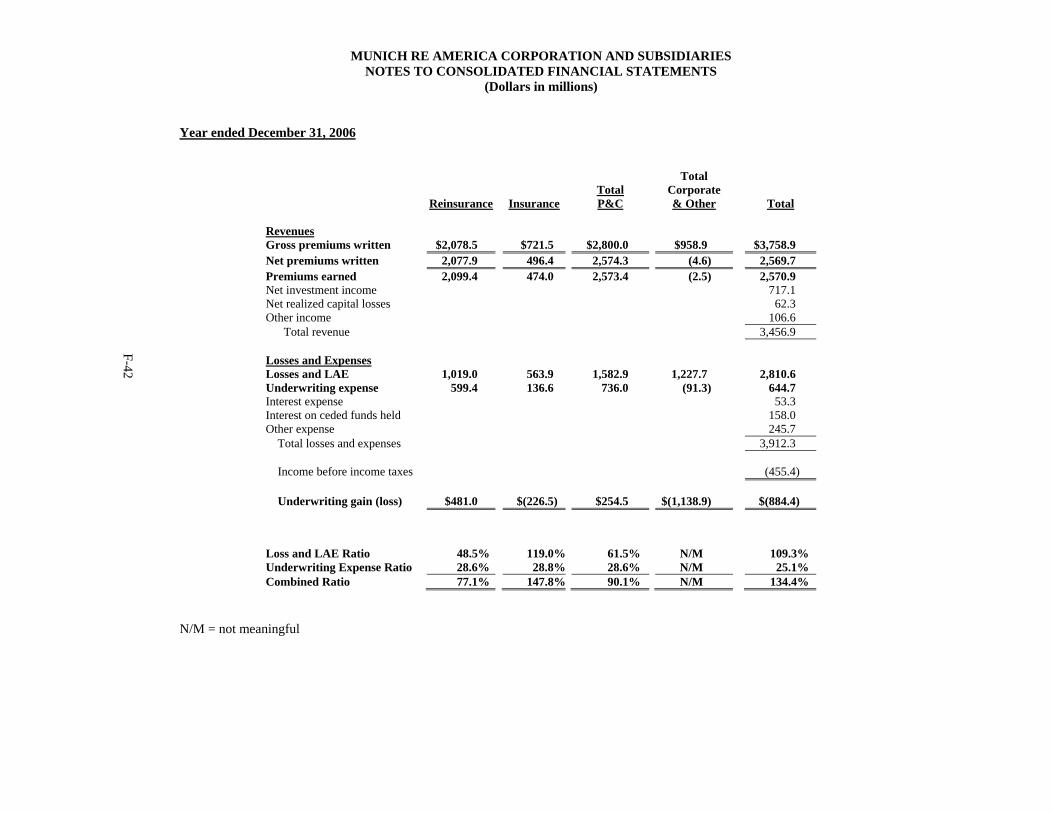

Interest Expense on Ceded Funds Held Balances. Interest expense on funds held under reinsurance treaties decreased 12.5% to $223.3 million for the year ended December 31, 2008, from $255.2 million for the same period in 2007. This decrease was the result of a decrease in the fund balances for the loss portfolio transfer program with Munich Re Munich. Other Expenses. Other expenses increased 45.4% to $82.8 million for the year ended December 31, 2008, from $57.0 million for the same period in 2007. This increase is the result of a $37.6 million increase in expenses related to the Company’s reinsurance contracts accounted for as deposits, a $22.1 million increase in the Company’s provision for uncollectible underwriting balances, and a $5.2 million increase in expenses related to arranging insurance contracts for third parties. These increases were partially offset by $46.1 million of net foreign exchange losses on foreign-denominated assets and liabilities other than investments in the 2007 period; foreign exchange gains were included in other income in 2008. Federal and foreign income taxes. A federal and foreign income tax benefit of $15.0 million was recognized for the year ended December 31, 2008, compared to expense of $92.0 million for the year ended December 31, 2007. The Company recognized a tax valuation allowance of $155.3 million for the year ended December 31, 2008, compared to a valuation allowance of $17.3 million for the 2007 period. The 2008 valuation allowance was provided as a result of impaired securities and capital loss carry-forwards that the Company will be unable to utilize prior to expiration due to insufficient capital gain income. Absent these valuation allowances, the $107.0 million decrease in tax expense is the result of pretax loss of $528.5 million in the 2008 period compared with pretax income of $141.6 for the same period in 2007. Year Ended December 31, 2007, Compared with Year Ended December 31, 2006 Underwriting Results and Combined Ratio Certain financial information for the years ended December 31, 2007 and 2006 has been restated to reflect the Company’s new P&C operating structure, in addition to the reclassification of certain expenses previously included in Other Expense, now in Underwriting Expense. The underwriting results and combined ratios for the Company and its P&C business segments for the years ended December 31, 2007 and 2006, are as follows:

2007 2006

P&C Segments

Total

Consolidated

P&C

Segments

Total

Consolidated (Dollars in millions)

Premiums earned $2,526.6 $2,396.6 $2,573.4 $2,570.9

Less: Losses and LAE 1,649.6 1,991.0 1,582.9 2,810.6 Commission expense 458.6 390.8 488.9 329.4 Operating expense 302.8 321.8 247.1 315.3 Underwriting gain (loss) $115.6 $(307.0) $254.5 $(884.4) Loss ratio 65.3% 83.1% 61.5% 109.3%Expense ratio 30.1 29.7 28.6 25.1 Combined ratio 95.4% 112.8% 90.1% 134.4% In both 2007 and 2006, the Company reported underwriting losses for the year resulting predominantly from loss and loss adjustment expense reserve review charges of $370.0 million and $953.0, respectively. These reserve review charges were part of total prior accident year losses of $213.0 million in 2007, and $1,045.1 in 2006. Both years’ charges were impacted by the reduction of losses ceded to corporate retrocessional programs with Munich Re Munich, and the deferral of loss benefit from a loss portfolio transfer agreement, also with Munich Re Munich. These corporate retrocessional programs are not included in the underwriting results of the Company’s property and casualty business segments.

13

Financial Statement Results The Company’s net income to its common stockholder was $49.6 million for the year ended December 31, 2007, compared to a net loss of $1,084.5 million for the same period in 2006. In 2006, the Company incurred a net charge of $953.0 million to losses and LAE (the “2006 reserve charge”) and a $750.0 million valuation adjustment for deferred federal income taxes, related to the recoverability of net deferred tax assets. Revenues Premiums. Gross premiums written for the year ended December 31, 2007 decreased 5.0% to $3,570.7 million from $3,758.9 million for 2006. Net premiums written by the Company’s P&C business segments, which exclude certain corporate retrocessional programs, decreased 3.6% to $2,481.7 million for the year ended December 31, 2007, from $2,574.3 million for the same period in 2006. The Reinsurance segment experienced a 3.0% decrease in net premiums written to $2,015.9 million for the year ended December 31, 2007, from $2,077.9 million for the same period in 2006. This decrease primarily reflects a continuing increase in clients’ risk retention levels and strict adherence to the Company’s pricing policies, in addition to the cancellation of a large workers’ compensation treaty in December 2006. The Insurance segment experienced a 6.2% decrease in net premiums written to $465.8 million for the year ended December 31, 2007, from $496.4 million for the same period in 2006, resulting in part from the cancellation of a large program in the 2007 period. The overall decrease in premiums written by the P&C business segments, coupled with a decrease in premiums written for health care business and increased premiums ceded for corporate retrocessional programs, resulted in a decrease in consolidated net premiums written to $2,362.4 million for the year ended December 31, 2007, from $2,569.7 million for the same period in 2006. The Company’s net premiums earned decreased 6.8% to $2,396.6 million for the year ended December 31, 2007, from $2,570.9 million for the same period in 2006. The decrease in premiums earned was consistent with the decrease in net premiums written. Investment Income. Net investment income decreased slightly to $710.1 million for the year ended December 31, 2007, from $717.1 million for the same period in 2006. This decrease is primarily due to foreign exchange losses of $38.9 million for the year ended December 31, 2007, compared to gains of $26.0 million for the same period in 2006. These foreign exchange losses were partially offset by increased book yields on the Company’s fixed income portfolio and income from equity futures. The Company realized net capital gains of $81.6 million for the year ended December 31, 2007, compared to net capital gains of $62.3 million for the same period in 2006. The 2007 period included net capital gains of $167.9 million recognized on the sale of common equities, fixed income securities and other available-for-sale investments, offset by write-downs of $86.3 million of fixed income, common equities and other available-for-sale investments, as the decline in the fair value of these securities was considered to be “other than temporary.” The 2006 period included net capital gains of $131.7 million recognized on the sale of common equities and other available-for-sale investments, offset by net capital losses of $46.4 million recognized on the sale of fixed income securities and the write-downs of $23.0 million of investments. Other Income. Other income decreased 79.0% to $22.4 million for the year ended December 31, 2007, from $106.6 million for the same period in 2006. This decrease is primarily the result of an $77.5 million decrease in income related to the Company’s ceded reinsurance contracts accounted for as deposit. Expenses Losses and Loss Adjustment Expenses. Losses and LAE incurred decreased 29.2% to $1,991.0 million for the year ended December 31, 2007, from $2,810.6 million for the same period in 2006. This decrease is predominantly attributable to losses and LAE related to prior accident years of $213.0 million in 2007, compared to $1,045.1 in 2006. While the adequacy of loss and LAE reserves is closely monitored throughout the year, the majority of prior accident year losses are recognized as a result of the Company’s annual reserve review process. In 2007, the Company recorded a net charge of $370.0 million resulting from its reserve review, compared to $953.0 million in 2006. In the fourth quarter of 2007, the Company completed its loss reserve review based upon data evaluated as of September 30, 2007. Reflecting the indications of the review, the Company decreased loss and LAE reserves by

14

$18.4 million, excluding the impact of certain corporate retrocessional programs with Munich Re Munich. This overall reserve decrease was comprised of a decrease of $511.1 million for accident years 2002 and subsequent accident years, the largest portion of which was derived from several lines of business; offset by an increase of $492.7 million for accident years 2001 and prior, primarily attributable to excess workers compensation and latent exposures other than asbestos and environmental. The decreased losses for accident years 2002 and subsequent were partially offset by reductions in losses ceded to the variable quota share and accident year stop loss programs with Munich Re Munich. The increased losses for accident year 2001 and prior, were primarily ceded to a loss portfolio transfer agreement, also with Munich Re Munich; however, because this agreement is accounted for as retroactive reinsurance, the majority of these recoveries were deferred and will be recognized in income over the settlement period of the underlying claims. The reduced cessions, coupled with the deferral of the benefit from the LPT program, resulted in a reserve review charge of $370.0 million on a net basis. Underwriting Expense. Underwriting expense, consisting of commission expense plus operating expense, increased 10.5% to $712.6 million for the year ended December 31, 2007, from $644.7 million for the same period in 2006. This increase was primarily due to an 18.6% increase in net commission expense to $390.8 million for the year ended December 31, 2007, from $329.4 million for the same period in 2006. The increase in commission expense is primarily the result of decreased commission income on the corporate retrocessional programs, primarily the variable quota share program. Operating expenses increased 2.1% to $321.8 million for the year ended December 31, 2007, from $315.3 million for the year ended December 31, 2006. This increase was primarily due to increased compensation expenses for the 2007 period. Interest Expense on Ceded Funds Held Balances. Interest expense on funds held under reinsurance treaties increased 61.5% to $255.2 million for the year ended December 31, 2007, from $158.0 million for the same period in 2006. This increase was primarily the result of the loss sensitive features of the variable quota share program with Munich Re Munich which decreased this expense in 2006. Other Expenses. Other expenses decreased 76.8% to $57.0 million for the year ended December 31, 2007, from $245.7 million for the same period in 2006. This decrease is primarily the result of an $88.5 million decrease in expense related to the Company’s reinsurance contracts accounted for as deposit, a $57.5 million decrease in the Company’s provision for uncollectible underwriting balances, and a $46.1 million decrease in net foreign exchange losses on foreign-denominated assets and liabilities other than investments. Federal and foreign income taxes. Federal and foreign income tax expense of $92.0 million was recognized for the year ended December 31, 2007, compared to $629.1 million for the year ended December 31, 2006. In 2006, a valuation allowance of $750.0 million, was provided as a result of the increased strain loss reserve charges had placed on the Company’s ability to generate sufficient future taxable income before the expiration of its net tax operating loss carry-forwards. Absent this valuation allowance the $212.9 million increase in tax expense is the result of higher pretax income in the 2007 period. Critical Accounting Policies and Estimates The accounting policies discussed in this section are those that management considers to be the most critical to understanding the Company’s financial statements. Certain accounting policies require management to make estimates that affect the amounts of assets and liabilities reported at the date of the financial statements and the amounts of revenues and expenses reported during the period. These estimates are necessarily based on numerous assumptions involving varying and potentially significant degrees of judgment and uncertainty. As such, actual results will likely differ from those estimates. Premiums and Unearned Premiums. Premiums are earned over the terms of the related insurance policies and reinsurance contracts. Unearned premiums reserves are computed for the remaining period of coverage using pro rata methods. Assumed reinsurance premiums are based on information provided by ceding companies. Written and earned premiums, and their related cost, which have not yet been reported to the Company are estimated and accrued. The information used in establishing these estimates is reviewed and subsequent adjustments are recorded in the period in which they are determined. On retrospectively rated contracts, estimated additional or return premiums are accrued.

15

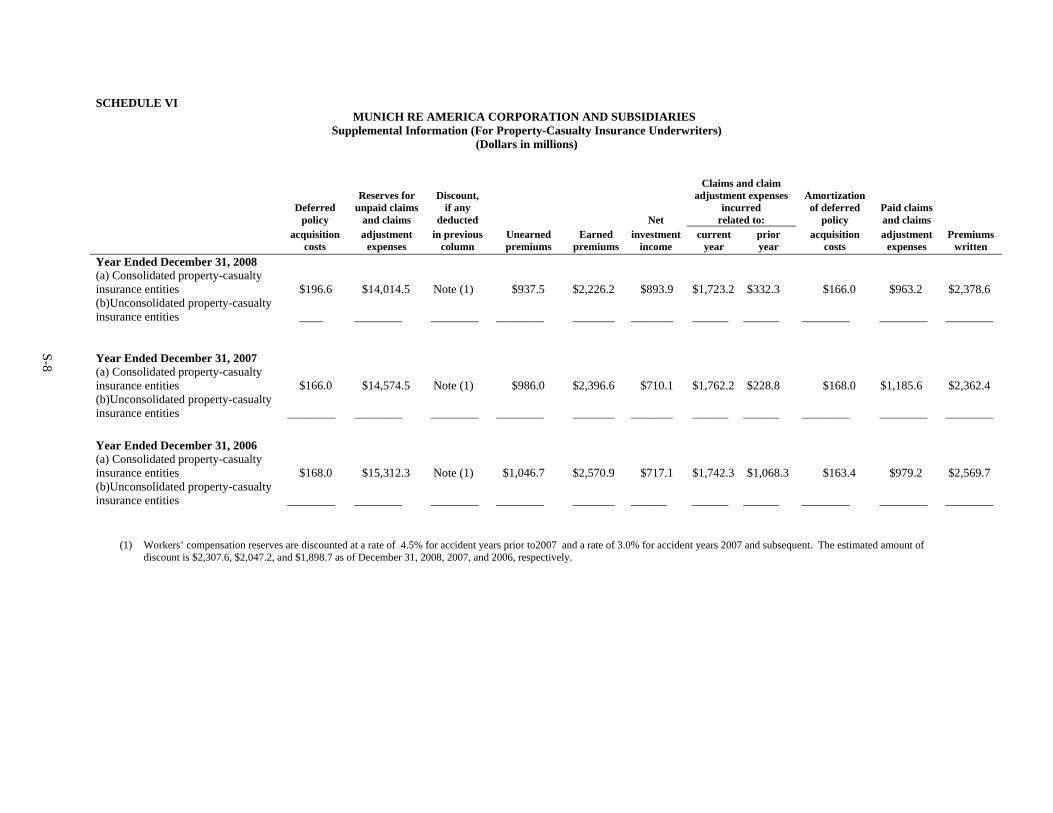

Assumed reinsurance and ceded retrocessional contracts that do not both transfer significant insurance risk and result in the reasonable possibility that the Company or its retrocessionnaires may realize a significant loss from the insurance risk assumed are required to be accounted for as deposits. These contract deposits are included in other assets and other liabilities in the Consolidated Balance Sheets and are accounted for as financing transactions with interest income or expense credited or charged to the contract deposits. Loss and Loss Adjustment Expense Reserves. The Company is required to maintain reserves to cover its estimated ultimate liability for losses and LAE with respect to reported and unreported claims incurred as of the end of each accounting period modified for current trends and estimates of expenses for investigating and settling claims (net of estimated related salvage and subrogation claims of Munich Re America). Generally, it is the Company’s policy to discount all workers’ compensation claims on reported and unreported losses at the rate permitted by the Commissioner of Insurance of the State of Delaware. Claims related to accident years prior to 2007 are discounted using an interest rate of 4.5%. Claims related to accident years 2007 and subsequent are discounted using an interest rate of 3.0%. The reserve for losses and LAE is based upon reports received from reinsureds supplemented with the Company’s own case reserve estimates provided by the Company’s Claims Division. These reserves are estimates involving actuarial and statistical projections at a given time of what management expects the ultimate settlement and administration of claims to cost based on facts and circumstances then known, predictions of future events, estimates of future trends in claims severity and other variable factors such as inflation and new concepts of liability. For certain types of claims, most significantly asbestos-related and environmental liability claims, the effects of evolving scientific, legal and social issues are potentially so significant that the Company’s reserve estimate is subject to significant revision as these issues are resolved over time. For example, asbestos, once regarded as a state-of-the-art construction material, was ultimately determined to be carcinogenic. Still more time passed before courts determined that various types of losses arising from the manufacture and use of asbestos (such as product liability, workers' compensation and the cost of removal) were covered by insurance companies, thereby requiring revisions in such estimates. For asbestos and environmental liabilities, considerable judgment has been exercised in formulating the Company’s estimates. However, these estimates will be revised as legal, judicial and factual information develops and/or is clarified. The amounts ultimately paid by the Company for these exposures likely will differ, perhaps significantly, from the Company’s currently recorded reserves. The inherent uncertainties of estimating loss reserves are exacerbated for reinsurers by the significant periods of time that often elapse between the occurrence of an insured loss, the reporting of the loss to the primary insurer and, ultimately, to the reinsurer, and the primary insurer's payment of that loss and subsequent indemnification by the reinsurer (the "tail"). As a consequence, actual losses and LAE paid may deviate, perhaps substantially, from estimates reflected in the Company’s reserves in its financial statements. Any adjustments of these estimates or differences between estimates and amounts subsequently paid or collected are reflected in income. Deferred Underwriting Revenue. The loss portfolio transfer agreement with Munich Re Munich is a retroactive reinsurance contract. As such, adverse loss development subsequent to the inception of the contract is generally deferred and recognized in income using the interest method over the settlement period of the underlying claims. Changes in the expected timing and estimated amounts of the underlying claims produce changes in the periodic income recognized. These changes in estimates are determined retrospectively and included in income in the period of the change and subsequent periods.

Reinsurance Recoverables on Unpaid Losses. Reinsurance recoverables are based upon the application of estimates of unpaid loss and LAE reserves in conjunction with terms specified under individual retrocessional contracts. The amounts ultimately collected may be more or less than such estimates. Any adjustments of these estimates or differences between estimates and amounts subsequently collected are reflected in income as they occur. Loss reserves ceded to unauthorized companies are collateralized by letters of credit, pledged trusts, or cash. The Company has provided for amounts deemed to be uncollectible. Management believes such provision is sufficient to reduce reinsurance recoverables to their collectible amounts. Investments. Debt and equity securities classified as available for sale are reported at fair value, with unrealized gains and losses excluded from earnings and reflected in stockholder’s equity as a component of accumulated other comprehensive income, net of related income taxes. Other investments classified as available for sale are comprised of the Company’s investment in equity-based and fixed income hedge funds for which the Company owns less than 3% of the fund’s total net assets. These funds are reported at fair value with unrealized gains and losses reflected in stockholder’s equity as a component of accumulated other comprehensive income.

16

Debt and equity investments classified as trading are reported at fair value, with gains and losses, both realized and unrealized, included in net investment income. Realized gains and losses on the sale of investments are determined on a first-in, first-out basis and are included in net income. Investment income is recognized as earned and includes the accretion of discounts and amortization of premiums related to fixed maturity securities. Purchases and sales are recorded on a trade date basis. Other invested assets includes the Company’s investment in foreign exchange forward contracts. These derivative instruments were purchased to reduce the foreign currency exchange risk associated with certain foreign currency denominated investments. Other invested assets also includes the Company’s investment in equity futures. These futures were purchased to minimize the down-side risk of the Company’s equity holdings. Derivative instruments are reported at fair value, with gains and losses, both realized and unrealized, included in net investment income. The value of these derivative instruments can change, sometimes significantly, based on varying factors such as changes in equity market values and foreign exchange rates. The Company continually monitors its investment portfolio, considering market conditions, industry characteristics and the fundamental operating results of an issuer, to determine if declines in value are due to changes relating to a decline in credit quality or market valuation, or other issues affecting the investment. Based on this analysis, if a decline in fair value of an invested asset is considered to be other than temporary, or if the asset is deemed to be permanently impaired due to credit considerations, or if management believes it does not have the intent and ability to hold a security until such time that it has recovered in value or its scheduled maturity, the investment is reduced to its fair value and the reduction is accounted for as a realized investment loss. Income Taxes. The Company uses the liability method of accounting for income taxes, whereby deferred tax assets and liabilities are determined based on differences between the financial reporting and tax bases of assets and liabilities and are measured using the enacted tax rates and laws. The Company establishes a “valuation allowance” for any portion of the deferred tax asset that management does not believe is more likely than not realizable. The Company recognizes the tax impact from an uncertain tax position taken, or expected to be taken, in income tax returns only if it is more likely than not that the tax position will be sustained upon examination by tax authorities, based on the technical merits of the position. Tax positions that meet the “more likely than not” threshold are then measured using a probability-weighted approach, whereby the largest amount of tax benefit that is greater than 50% likely of being realized upon ultimate settlement is recognized. The Company recognizes interest and penalties related to uncertain tax positions in income tax expense. Financial Condition The Company is a holding company, which includes its principal subsidiary, Munich Reinsurance America. Based on combined statutory gross premiums written by the insurance subsidiaries of $3,310.9 million in 2008, the Company is one of the largest property and casualty reinsurers in the U.S., according to Reinsurance Association of America statistics. Total consolidated assets decreased by 8.6% to $27,900.9 million at December 31, 2008, from $30,517.8 million at December 31, 2007. This decrease was primarily due to decreases of $1,195.8 million in reinsurance recoverables, mainly related to paid loss activity on retrocessional programs with Munich Re Munich and the decline in the market value of the Company’s investment portfolio. Total consolidated liabilities decreased by 6.7% to $25,890.3 million at December 31, 2008, from $27,738.3 million at December 31, 2007. The decrease was primarily due to decreases of $1,194.7 million on funds held under reinsurance treaties mainly related to paid loss activity on retrocessional programs with Munich Re Munich, and $560.0 million on loss and LAE reserves. Total assets and liabilities were also impacted by the 2008 settlement of December 31, 2007 open accounts payable and receivable balances on investment purchases and sales occurring near the end of the period. The Company did not have an equivalent level of unsettled investment transactions at the end of the 2008 period. In July 2008, the Company commenced a cash tender offer (the “Tender Offer”) for all of the Notes, of which $500.0 million aggregate principal were outstanding at the time. Concurrent with the Tender Offer, the Company also solicited consents from at least a majority of the holders of the Notes (the "Consent Solicitation," and together with the Tender Offer, the "Offer") to amend the indenture under which the Notes were issued (the “Indenture”) to allow holders to receive certain statutory financial reports rather than the financial reports presently required to be provided to holders in the Indenture (the "Proposed Amendment"). The Company received tenders with respect to $78.6 million in aggregate principal amount of the Notes pursuant to the Company’s Offer and accepted for payment all amounts tendered. The Company did not receive the requisite consents to the Proposed Amendment to the

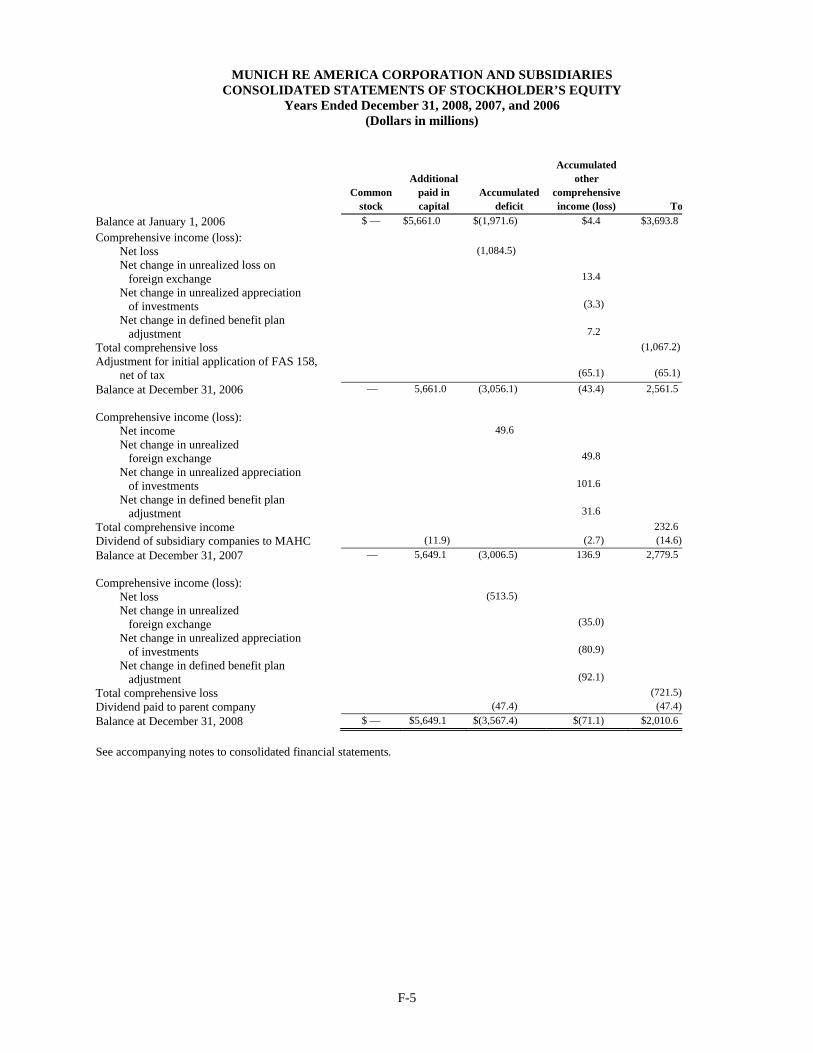

17

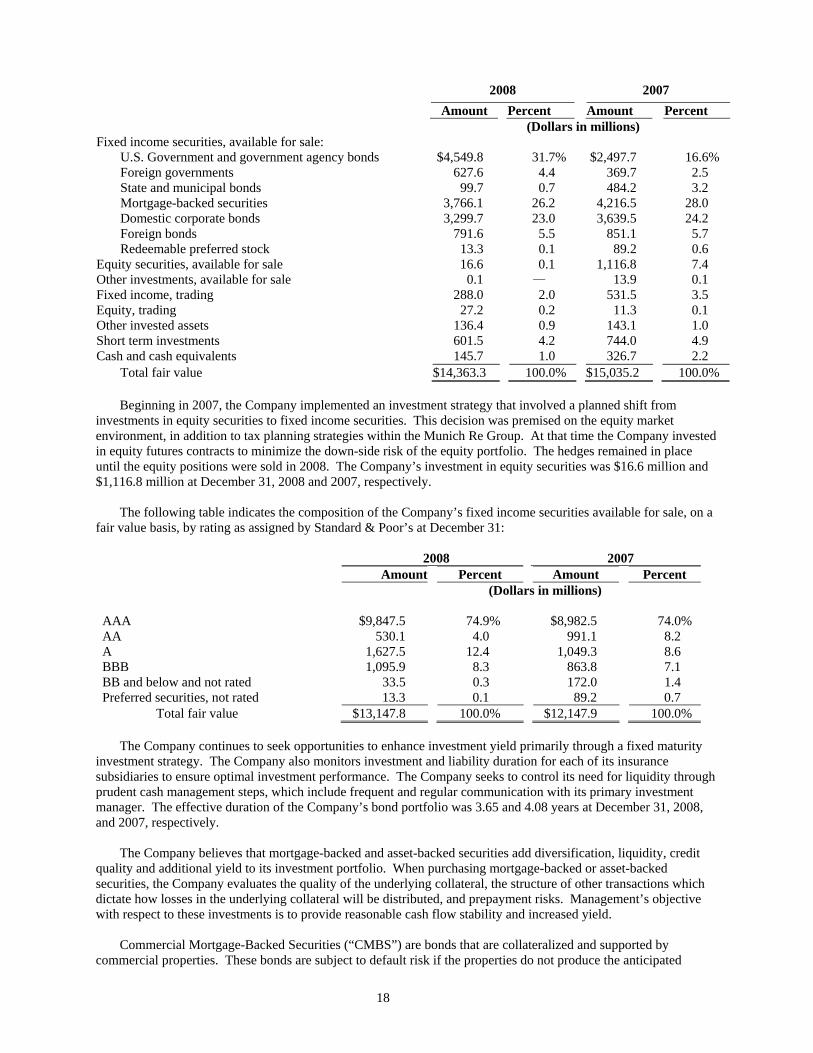

Indenture. The Company recognized a loss of $4.1 million on this transaction, which was settled in the third quarter of 2008. The Company may leave the remaining Notes outstanding, or from time to time, redeem all or a part of the Notes pursuant to the terms of the Indenture, or purchase them in privately negotiated transactions, tender offers or otherwise. The Indenture contains certain covenants, including, but not limited to, covenants imposing limitations on liens, and restrictions on mergers and sale of assets. In January 2009, the Company assigned to Munich Re Munich its outstanding $250.0 million loan with HSH Nordbank AG, formerly known as Landesbank Schleswig-Holstein Girozentrale, as lender and agent for a number of other banks (the “Loan”). The Loan had a term of three years remaining and bore interest at a fixed rate of 6.27%. The Loan was assigned for consideration of $243.3 million plus accrued interest. The assignment discharged the Company from all obligations under the Loan. Common stockholder’s equity decreased 27.7% to $2,010.6 million at December 31, 2008, from $2,779.5 million at December 31, 2007. This decrease was the result of the Company’s 2008 net loss of $513.5 million, $47.4 million of dividends paid to MAHC, and a decrease of $208.0 million in accumulated other comprehensive income, net of tax, primarily related to the decrease in unrealized appreciation of investments, and the change in the defined benefit adjustment, primarily resulting from the decline in the market value of the assets held in the pension trust. The Company’s insurance subsidiaries’ statutory surplus decreased to $3,648.9 million at December 31, 2008, from $4,415.7 million at December 31, 2007. The decrease was primarily a result of a $500.0 million return of capital from Munich Reinsurance America to the Company, $93.8 million of net unrealized investment losses, and an increase in non-admitted assets of $125.7 million for the year ended December 31, 2008. These decreases were slightly offset by combined statutory net income of $28.3 million for the year This statutory net income is different from the net loss reported in these financial statements, primarily due to differing accounting treatments for the LPT agreement with Munich Re Munich and investment write-downs. The Insurance Department of the State of Delaware (the “Insurance Department”) has a risk based capital (“RBC”) standard for property and casualty insurance (and reinsurance) companies which measures the amount of capital appropriate for a property and casualty insurance company to support its overall business operations in light of its size and risk profile. At December 31, 2008, Munich Reinsurance America’s RBC ratio is 447.4%, compared to 572.7% at December 31, 2007. An RBC ratio in excess of 200% generally requires no regulatory action. Investments The total financial statement value of investments and cash decreased 4.5% to $14,363.3 million at December 31, 2008, from $15,035.2 million at December 31, 2007, primarily resulting from net realized capital losses of $565.0 million, market valuation adjustments and unrealized foreign exchange adjustments of $204.3 million, the partial extinguishment of the Company’s senior notes of $82.9 million, and a dividend of $47.4 million paid to MAHC. These decreases were partially offset by positive net cash flow from operating activities as well as $167.5 million from the change in net security receivables and payables The financial statement value of the investment portfolio at December 31, 2008, included a net increase from amortized cost to fair value of $133.8 million for investments available for sale, compared to a net increase of $258.4 million at December 31, 2007. At December 31, 2008, the Company recognized a cumulative unrealized gain of $87.0 million due to the net adjustment to fair value on investments, after applicable income tax effects, which was reflected as a component of accumulated other comprehensive income. This represents a net decrease to stockholder’s equity of $80.9 million from the cumulative unrealized gain on investments of $167.9 million recognized at December 31, 2007. The Company holds foreign currency denominated securities in portfolios related to the Company’s international branch run-off operations. These portfolios are classified as “trading”, as it is the Company’s intent to actively trade these securities. These trading securities are reported at fair value with gains and losses, both realized and unrealized, included in net investment income. The Company follows an investment strategy that emphasizes maintaining a high-quality investment portfolio while maximizing total return. The composition of the Company’s investment portfolio, on a fair value basis, for the periods ending December 31, was as follows:

18

2008 2007

Amount Percent Amount Percent (Dollars in millions) Fixed income securities, available for sale: U.S. Government and government agency bonds $4,549.8 31.7% $2,497.7 16.6% Foreign governments 627.6 4.4 369.7 2.5 State and municipal bonds 99.7 0.7 484.2 3.2 Mortgage-backed securities 3,766.1 26.2 4,216.5 28.0 Domestic corporate bonds 3,299.7 23.0 3,639.5 24.2 Foreign bonds 791.6 5.5 851.1 5.7 Redeemable preferred stock 13.3 0.1 89.2 0.6 Equity securities, available for sale 16.6 0.1 1,116.8 7.4 Other investments, available for sale 0.1 — 13.9 0.1 Fixed income, trading 288.0 2.0 531.5 3.5 Equity, trading 27.2 0.2 11.3 0.1 Other invested assets 136.4 0.9 143.1 1.0 Short term investments 601.5 4.2 744.0 4.9 Cash and cash equivalents 145.7 1.0 326.7 2.2 Total fair value $14,363.3 100.0% $15,035.2 100.0%

Beginning in 2007, the Company implemented an investment strategy that involved a planned shift from investments in equity securities to fixed income securities. This decision was premised on the equity market environment, in addition to tax planning strategies within the Munich Re Group. At that time the Company invested in equity futures contracts to minimize the down-side risk of the equity portfolio. The hedges remained in place until the equity positions were sold in 2008. The Company’s investment in equity securities was $16.6 million and $1,116.8 million at December 31, 2008 and 2007, respectively. The following table indicates the composition of the Company’s fixed income securities available for sale, on a fair value basis, by rating as assigned by Standard & Poor’s at December 31:

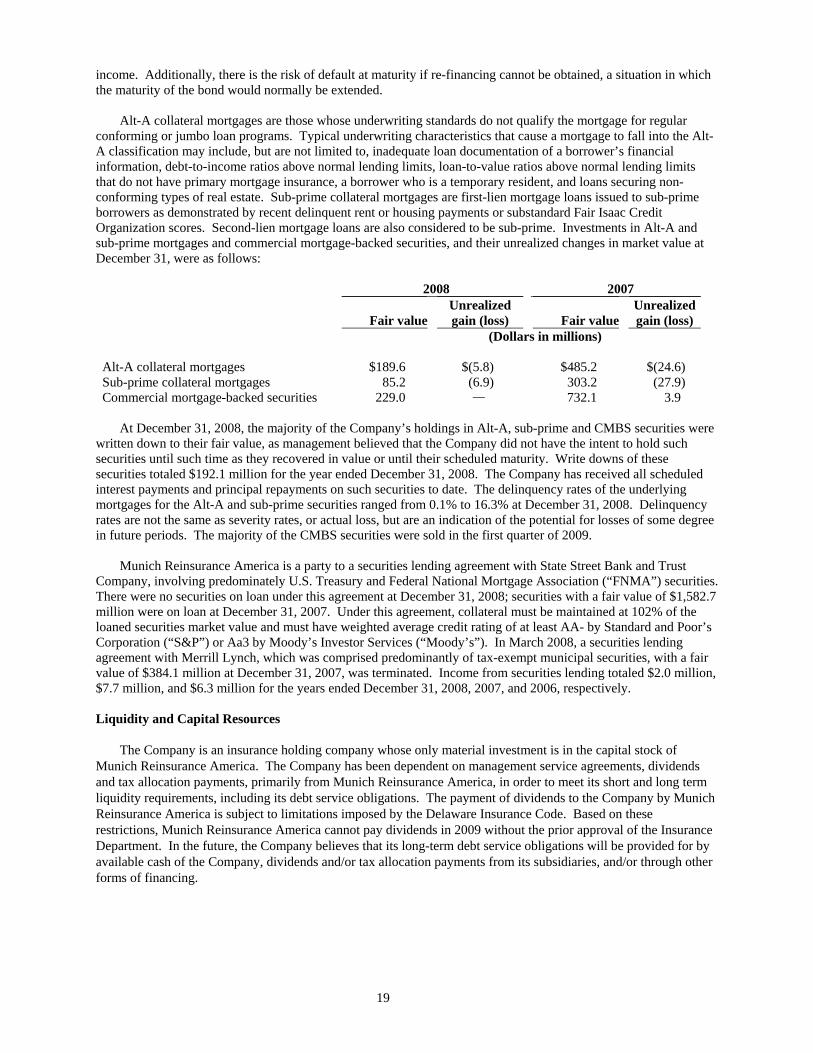

2008 2007 Amount Percent Amount Percent