paradox: two doctors heroes what a guy in a boat does counterfeiters workers who put together...

TRANSCRIPT

DIMENSION AND DEFINITION EXAMPLE QUESTIONS

Empathy

Access: Approachability and ease of contact.

How easy is it for me to talk to senior bank officials when I have a problem?

How easy is it for me to get through to a person who can handle my question over the phone?

Can I use social media to communicate with the bank?

DIMENSION AND DEFINITION EXAMPLE QUESTIONS

Empathy

Communication: Keeping customers informed in language they can understand and listening to them.

Can the loan officer clearly explain the various charges and fees associated with my card?

Are changes in fees clearly communicated?

Does the bank engage in two-way communication?

Does my bank solicit my feedback about its performance?

DIMENSION AND DEFINITION EXAMPLE QUESTIONS

Empathy

Understanding The

Customer: Making the effort to know customers and their needs.

Does the bank match the services they provide me with my needs?

Does the bank have personal financial management (PFM) tools to help me achieve my financial goals?

Does the bank ask about my needs, problems, and ideas for services?

Paradox:Two Doctors

HeroesWhat a guy in a boat does

Counterfeiters Workers who put together kitchen cabinets Bide Past tense of buy Bison What a father says when he drops his son off

at school

Wouldn’t Life Be Easier If Words Meant The Same Thing As The Way That They Are Pronounced

Parasites:

What you see from the top of the Eiffel Tower Subdued

Like, a guy, like who works on like one of those, like, submarines, man

Arbitrator:

A cook who leaves Arby’s to work at McDonalds

AvoidableWhat a bullfighter tries to do

Wouldn’t Life Be Easier If Words Meant The Same Thing As The Way That They Are Pronounced

`

Houma

Why Is Website Performance Important?

90% of customers form perceptions of company based on customer service experience…including WEBSITES

Source: Center for Customer Driven Quality, Purdue University.

Web Site Analytics

Analysis of Website Traffic: Visits, Bounce, Time of Site, Number of Pages Visited,

Conversion

Google Analytics Definitions

Visits = Sessions: period of interaction between a visitor's browser and a particular website, ending when the browser is closed or shut down, or when the user has been inactive on that site for a specified period of time.

Visitor: A visitor is a construct designed to come as close as possible to defining the number of actual, distinct people who visited a website. The most accurate visitor-tracking systems generally employ cookies to maintain tallies of distinct visitors.

Bounce Rate: Bounce rate is the percentage of single-page visits or visits in which the person left your site from the entrance (landing) page.

Pageview: A pageview is an instance of a page being loaded by a browser. Google Analytics logs a pageview each time the tracking code is executed.

Unique Views: Google Analytics records a visitor as NEW when any page on your site has been accessed for the first time by a web browser.

Google Analytics Definitions

Visits = Sessions: period of interaction between a visitor's browser and a particular website, ending when the browser is closed or shut down, or when the user has been inactive on that site for a specified period of time.

Visitor: A visitor is a construct designed to come as close as possible to defining the number of actual, distinct people who visited a website. The most accurate visitor-tracking systems generally employ cookies to maintain tallies of distinct visitors.

Bounce Rate: Bounce rate is the percentage of single-page visits or visits in which the person left your site from the entrance (landing) page.

Pageview: A pageview is an instance of a page being loaded by a browser. Google Analytics logs a pageview each time the tracking code is executed.

Unique Views: Google Analytics records a visitor as NEW when any page on your site has been accessed for the first time by a web browser.

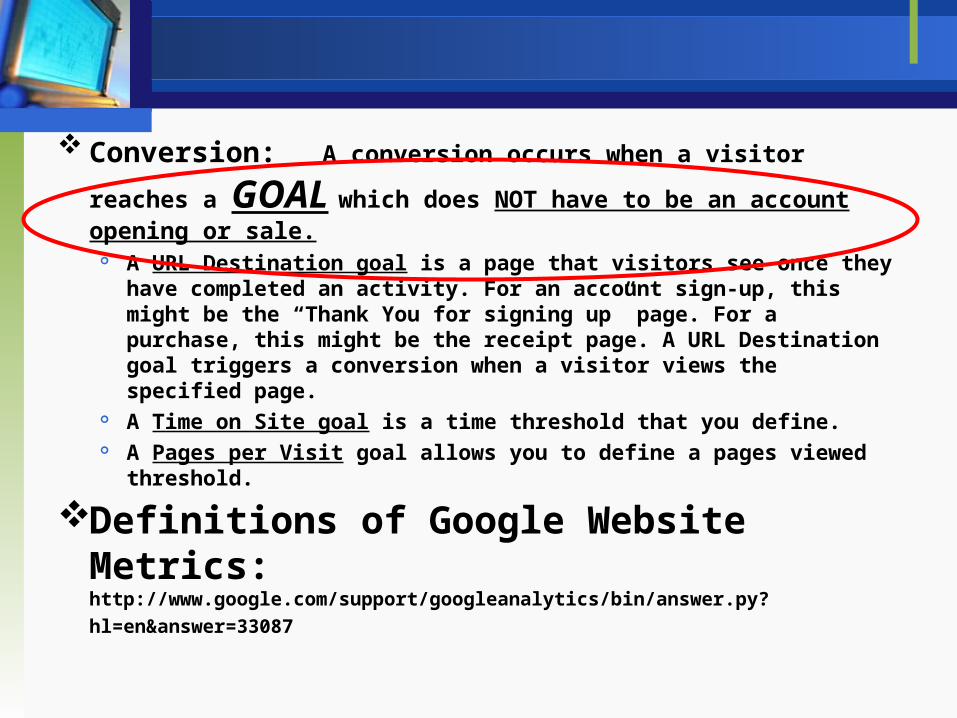

Conversion: A conversion occurs when a visitor reaches a

GOAL which does NOT have to be an account opening or sale.

A URL Destination goal is a page that visitors see once they have completed an activity. For an account sign-up, this might be the “Thank You for signing up” page. For a purchase, this might be the receipt page. A URL Destination goal triggers a conversion when a visitor views the specified page.

A Time on Site goal is a time threshold that you define. A Pages per Visit goal allows you to define a pages viewed

threshold.

Definitions of Google Website Metrics:

http://www.google.com/support/googleanalytics/bin/answer.py?

hl=en&answer=33087

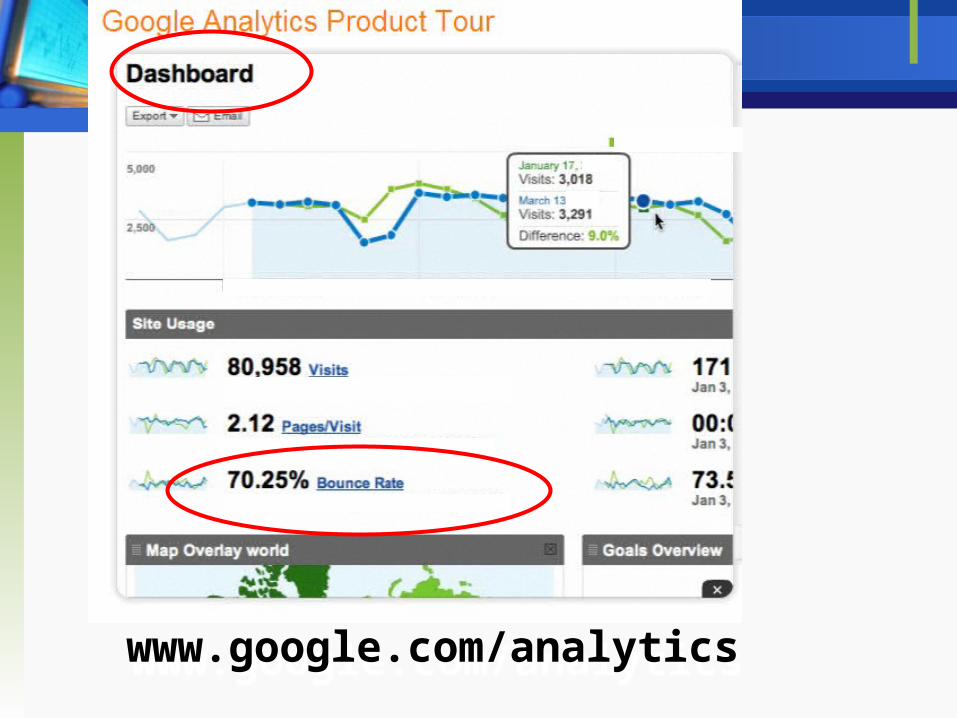

www.google.com/analyticswww.google.com/analytics

www.googlewebsiteoptimizer

Now called CONTENT EXPERIMENTS

http://www.youtube.com/watch?v=XJT9TCqzw4U

COST

Cost of Google Analytics and Google

Web Optimizer:

FREE

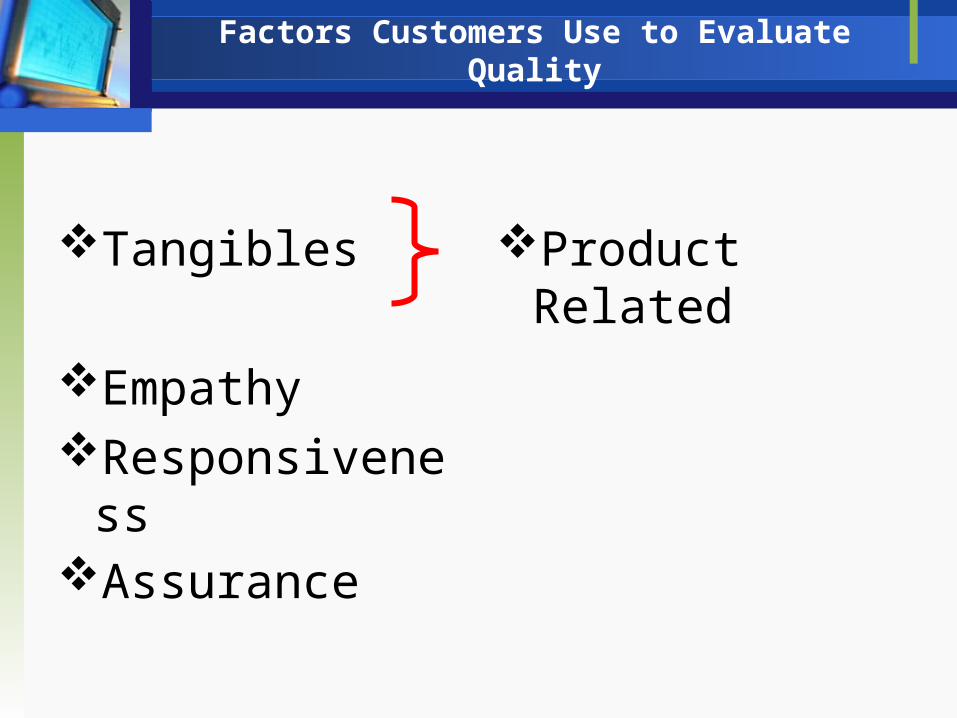

Factors Customers Use to Evaluate Quality

Tangibles

EmpathyResponsiveness

Product Related

Button Insurance?

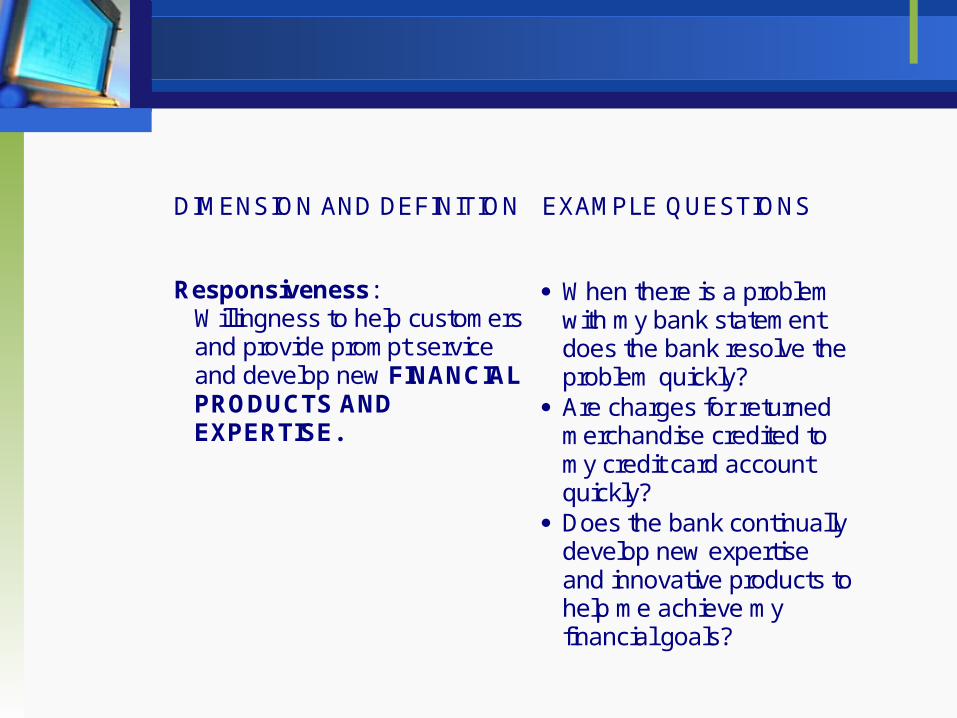

DIMENSION AND DEFINITION EXAMPLE QUESTIONS

Responsiveness: Willingness to help customers and provide prompt service and develop new FINANCIAL PRODUCTS AND EXPERTISE.

When there is a problem with my bank statement does the bank resolve the problem quickly?

Are charges for returned merchandise credited to my credit card account quickly?

Does the bank continually develop new expertise and innovative products to help me achieve my financial goals?

Factors Customers Use to Evaluate Quality

Tangibles

EmpathyResponsivenessAssurance

Product Related

DIMENSION AND DEFINITION EXAMPLE QUESTIONS

Assurance

Reliability: Ability to perform the promised service dependably and accurately.

When a customer service representative says she will call me back in 15 minutes, does she do so?

Is my bank statement free of errors?

Do the financial products work as promised?

DIMENSION AND DEFINITION

EXAMPLE QUESTIONS

Assurance

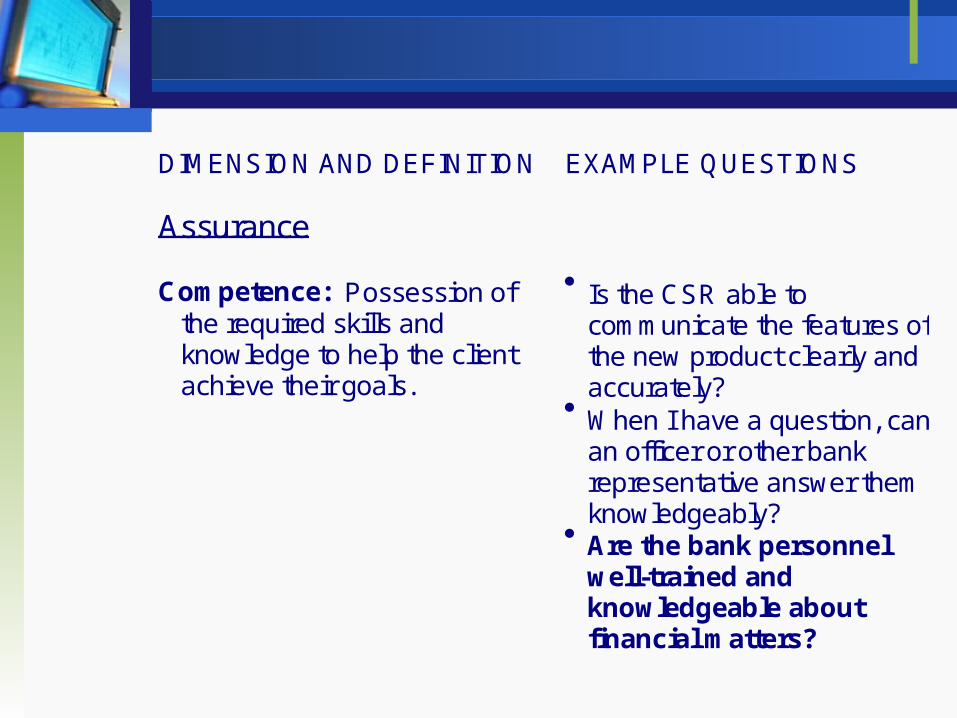

Competence: Possession of the required skills and knowledge to help the client achieve their goals.

Is the CSR able to communicate the features of the new product clearly and accurately?

When I have a question, can an officer or other bank representative answer them knowledgeably?

Are the bank personnel well-trained and knowledgeable about financial matters?

DIMENSION AND DEFINITION

EXAMPLE QUESTIONS

Assurance

Credibility: Trustworthiness, believability, honesty of the service provider.

Does the bank have a good reputation?

Are the interest rates/fees charges by my bank consistent with the services provided?

Does the bank deliver the quality it promises?

DIMENSION AND DEFINITION

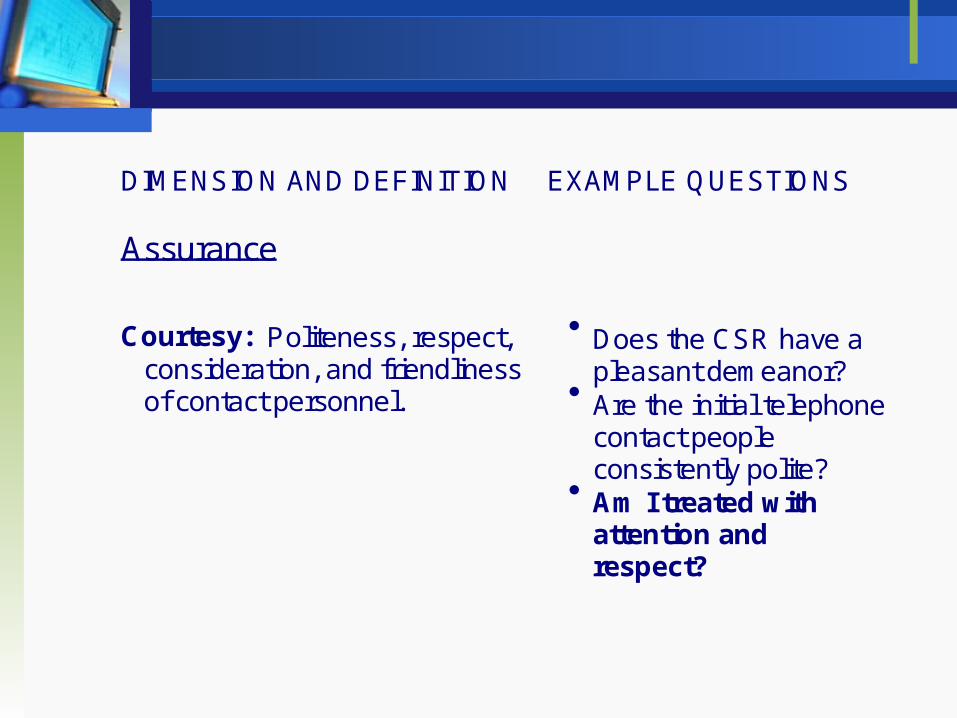

EXAMPLE QUESTIONS

Assurance

Courtesy: Politeness, respect, consideration, and friendliness of contact personnel.

Does the CSR have a pleasant demeanor?

Are the initial telephone contact people consistently polite?

Am I treated with attention and respect?

DIMENSION AND DEFINITION

EXAMPLE QUESTIONS

Assurance

Security: Freedom from danger, risk, or doubt.

Is my credit card safe from unauthorized use?

Are my assets and financial information safe with the bank and bank personnel?

Factors Customers Use to Evaluate Quality

Tangibles

EmpathyResponsivenessAssurance

Product Related

Service Related

Factors Customers Use to RATE The Quality of Bank Performance

R esponsiveness

A ssurance

T angibles

E mpathy

Competitive Structure Variables

Relative Perceived Quality

Profits

SMALL BUSINESS BANKING

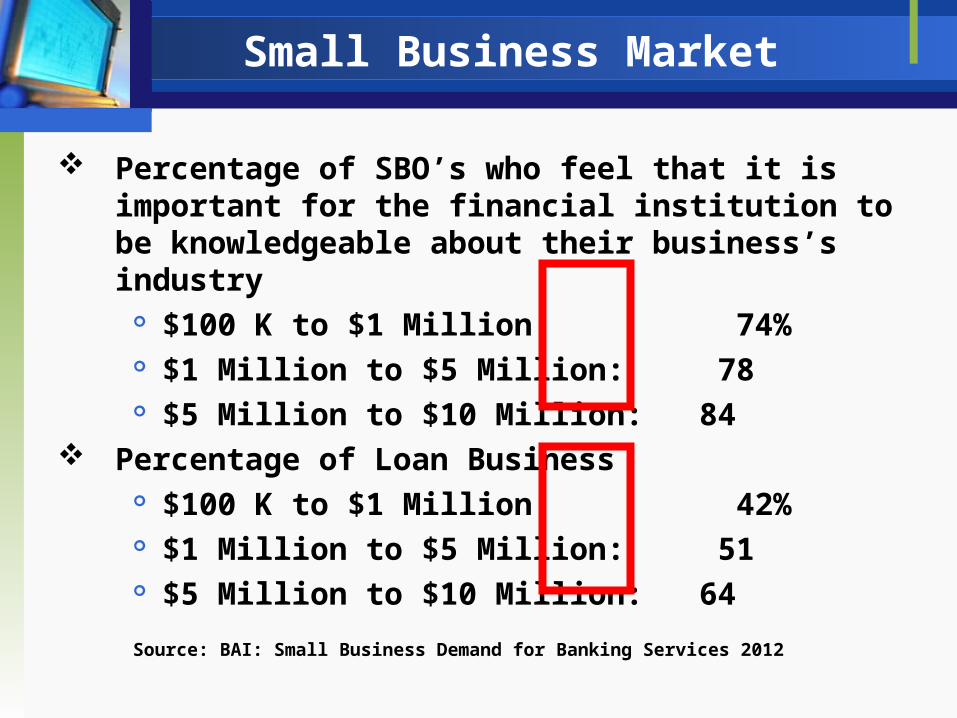

Small Business Market

Percentage of SBO’s who feel that it is important for the financial institution to be knowledgeable about their business’s industry

$100 K to $1 Million: 74% $1 Million to $5 Million: 78 $5 Million to $10 Million: 84

Percentage of Loan Business $100 K to $1 Million: 42% $1 Million to $5 Million: 51 $5 Million to $10 Million: 64

Source: BAI: Small Business Demand for Banking Services 2012

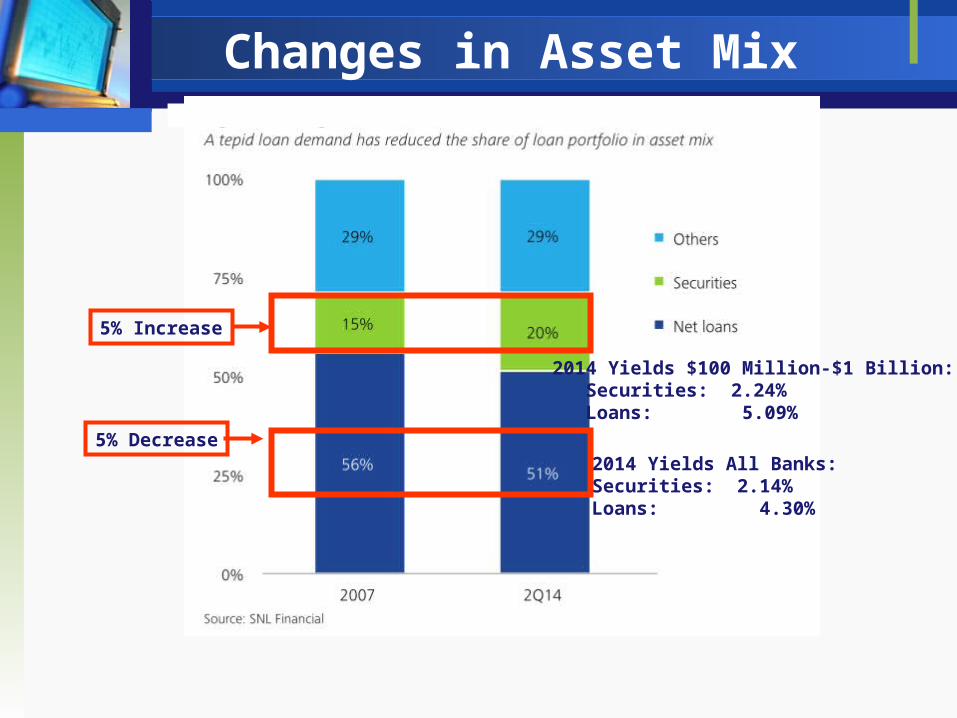

Changes in Asset Mix

2014 Yields $100 Million-$1 Billion: Securities: 2.24% Loans: 5.09%

2014 Yields All Banks:Securities: 2.14%Loans: 4.30%

5% Decrease

5% Increase

Small businesses are lower on their perceptions that banks offer loanproducts that meet their needs than are the banks themselves

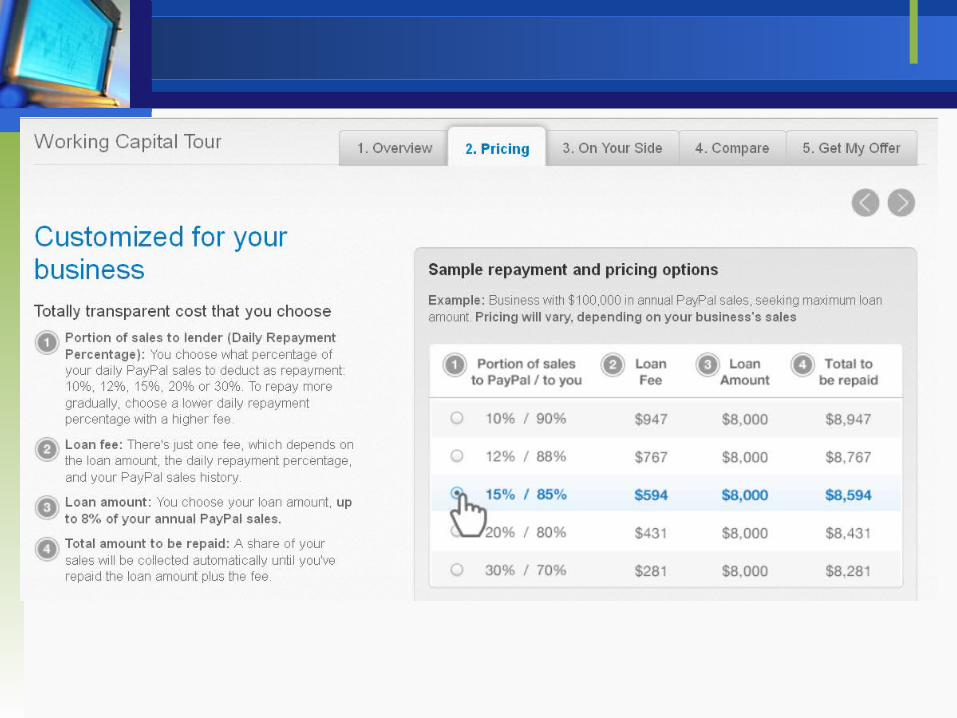

Source: PayPal Working Capital, March, 2014.

Hesitancy to Engage Business Owners in Financial Discussions

Average front line banker does not come from a business background

Don’t understand cash flow receivables inventory turn working capital other important small business management function

Thus, hesitant to engage in financial dialogue to identify financial issues and solutions for small business

PNC

Cash Flow Insightspnc.com/cashflowinsights

The Mobivore

TOOLS

To Help Your Bank Achieve Competitive Advantage

And Superior Performance

Competitive Structure Variables

Relative Perceived Quality

Profits

Factors Customers Use to Evaluate Quality

Tangibles

EmpathyResponsivenessAssurance

Product Related

Service Related

CSAT: Customer Satisfaction

RatingsVery Dissatisfied

Very Satisfied

1 2 3 4 5 6 7

CGAPBank

Competitive GAP Analysis

Empathy/Listening/Communications GAP

GAP 1 (EMPATHY GAP): Statements 1-14 Statements: 1-4 Marketing Research sub-GAP Statements: 5-8 Upward Communication sub-GAP Statement: 9 Levels of Management sub-GAP Statements: 10-13 Horizontal Communications sub-GAP Statement: 14 Overpromising-Underdelivering sub-GAP

Responsiveness GAP

GAP 2 (RESPONSIVENESS GAP): Statements 15-22 Statements 15-18 Management’s Commitment To Superior Performance sub-GAP Statement 19 Goal Setting sub-GAP Statement 20 Task Standardization sub-GAP Statements 21-22 Perception of Feasibility sub-GAP

Assurance GAP

GAP 3 (ASSURANCE GAP): Statements 26-37 Statements 23-24 Teamwork sub-GAP Statements 25-26 Employee-Job Fit sub-GAP Statement 27 Technology-Job Fit sub-GAP Statements 28 Perceived Control sub-GAP Statements 29-31 Supervisory Control Systems sub-GAP Statements 32-33 Role Conflict sub-GAP Statements 34-37 Role Ambiguity sub-GAP

General GAP Level Guidelines:

GAPS: 0-1.25 Probably not a significant competitive problem 1.25-1.75 Unclear…may or may not be a significant

problem…interpret as you would a financial analysis ratio. For example, if you had a potential borrower with a low current ratio (current assets divided by current liabilities), this might or might not be a problem for the company….you would look for the specific reasons. The same thought process applies to the GAP analysis. From 1.25 to 1.75, these might or might not be a problem. Analyze the GAP and then assess whether or not that particular GAP level inhibits your bank or area’s ability to retain or acquire customers from the chosen target market.

1.75 or Higher: Probably a competitive disadvantage. If you don’t

consider it a significant problem, comment as to why not.

Average GAP Rating Score

Performance Index: Percent of Perfect Score

0.0 100%

0.5 92

1.0 83

1.5 75

2.0 67

2.5 58

3.0 50

3.5 42

4.0 33

4.5 25

5.0 17

5.5 8

6.0 0

GAP 1: Management Does Not Understand or Effectively Manage Customer Expectations

Lack of Marketing Research Orientation

Including lack of website and social media analytics

Inadequate Upward Communication

Too Many Levels of Management

Lack of Horizontal Communication

Tendency to Overpromise and Underdeliver: External

Communication Problems

Empathy/Listening/ Communications GAP

More Than Managers 50 Percent Super- All Direct visors Employees Cust. Cont.

GAP 1: EMPATHY/LISTENING/ COMMUNICATIONS GAP

1. The bank regularly collects information about the needs and product/ service expectations of our customers.

3.41 3.39 3.43

2. The bank effectively uses digital techniques (including website analytics and social media) to better understand customers and to communicate with them more effectively.

4.11 3.33 4.89

3. The bank uses data mining and analytics to assess customer financial usage and to predict additional products to serve customers better.

4.78 5.01 4.55

4. The bank regularly uses market research and other information gathered from customer in decision making.

3.49 3.83 3.15

1a.Average for Marketing Research sub-GAP 3.95 3.89 4.01 (Add First 4 Questions and Divide by 4) 5. Managers in our bank frequently interact with customers. 1.50 1.75 1.25 6. The customer-contact personnel in our bank frequently 2.11 2.32 1.89 communicate with management. 7. Managers in our bank frequently seek suggestions about 2.55 3.32 1.78 serving customers from customer-contact personnel. 8. The primary means of communication in our bank between customer- 2.64 3.27 2.00 contact personnel and upper management is NOT memos, texts, or email. 1b. Average For Upward Communication sub-GAP 2.20 2.67 1.73 (Add Questions 5-8 and Divide by 4)

9. There are NOT too many levels of management between customer- 1.83 1.94 1.72 contact personnel and top management in the bank. 1c. Average For Too Many Levels of Management 1.83 1.94 1.72 sub-GAP

Empathy/Listening/Communications GAP

10. The people who develop our advertising and social media consult employees like me about the realism of promises made in our advertising.

4.95 5.22 4.68

11. I am almost always aware in advance of the promises made in our 2.72 2.74 2.70 bank's advertising and social media campaigns. 12. Employees like me interact with operations and IT people to discuss the 3.49 3.50 3.47 quality of products and service the bank can deliver to its customers. 13. Our bank's policies on serving customers are consistent among the 2.12 2.81 1.42 various departments and branches that interact with customers. 1d. Average For Horizontal Communication sub-GAP 3.32 3.57 3.07 (Add Questions 10-13 and Divide by 4)

14. Our bank does NOT make promises we cannot keep 3.84 3.77 3.90 in an effort to gain or keep customers. 1e. Average for Overpromising-Underdelivering sub-GAP 3.03 2.16 3.90 (Score for Question 14)

OVERALL MEASUREMENT OF GAP 1: EMPATHY GAP 2.84 3.17 2.89 (Add 1a + 1b + 1c + 1d + 1e and divide by 5)

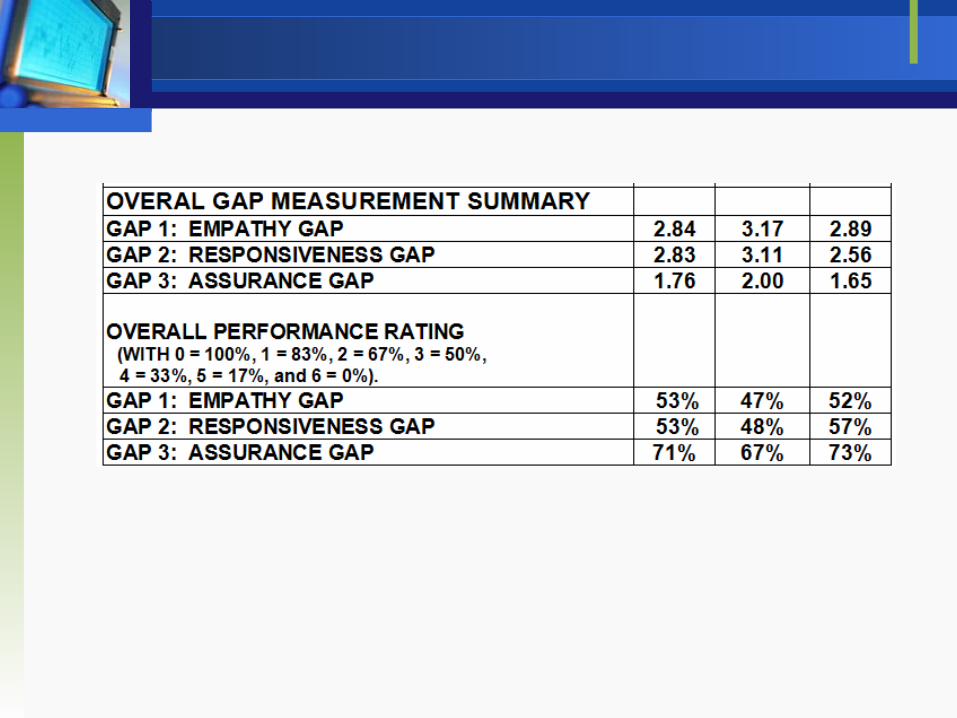

Overall Competitive GAP Summary

OVERAL GAP MEASUREMENT SUMMARY

GAP 1: EMPATHY GAP 2.84 3.17 2.89 GAP 2: RESPONSIVENESS GAP 2.83 3.11 2.56 GAP 3: ASSURANCE GAP 1.76 2.00 1.65 OVERALL PERFORMANCE RATING (WITH 0 = 100%, 1 = 83%, 2 = 67%, 3 = 50%, 4 = 33%, 5 = 17%, and 6 = 0%).

GAP 1: EMPATHY GAP 53% 47% 52% GAP 2: RESPONSIVENESS GAP 53% 48% 57% GAP 3: ASSURANCE GAP 71% 67% 73%

Percent ofAverage OptimalRating Performance Question

Q1 1.98 72%The bank regularly collects information about the needs and product/service quality expectations of our customers.

Q2 2.49 64The bank effectively uses digital techniques (including website analytics and social media) to better understand customers and to communicate with them more effectively.

Q3 2.59 62The bank uses data mining and analytics to assess customer financial usage and to predict additional products to serve customers better.

Q4 2.26 67The bank regularly uses marketing research and other information gathered from customers in decision-making.

2.33 66 AVERAGE FOR MARKETING RESEARCH GAPQ5 0.88 90 Managers in our bank frequently interact with customers.

Q6 1.36 82 The customer contact personnel in our bank communicate frequently with management.

Q7 1.91 73Managers in our bank frequently seek suggestions about serving customers from customer-contact personnel.

Q8 2.49 63The primary means of communication is our bank between customer contact personnel and upper management is NOT memos, texts, or email.

1.66 77 AVERAGE FOR UPWARD COMMUNICATION GAP

Q9 1.80 75There are NOT too many levels of management between customer contact personnel and top management in the bank.

1.80 75 AVERAGE FOR TOO MANY LEVELS OF MANAGEMENT GAP

Q10 3.01 55The people who develop our advertising and social media consult employees like me about the realism of the promises made in our advertising/social media.

Q11 2.58 62I am almost always aware in advance of the promises made in our bank's advertising and social media campaigns.

Q12 2.39 65Employees like me interact with operations and IT people to discuss the quality of products and service the bank can deliver to its customers.

Q13 1.54 79Our bank's policies on serving customers are consistent among the various departments and branches that interact with customers.

2.38 65 AVERAGE FOR HORIZONTAL COMMUNICATION GAPQ14 1.01 88 Our bank does NOT make promises we cannot keep in an effort to keep or gain customers.

1.01 88 AVERAGE FOR OVERPROMISING/UNDELIVERING GAP

2.0271

AVERAGE FOR EMPHATHY GAP (QUESTIONS 1-14)

Q15 1.62 78 Our bank does commit the necessary resources to provide high-quality products and service.Q16 1.92 73 Our bank has internal programs for improving the quality of products and service to customers.

Q17 2.07 70In our bank, managers who improve the quality of service for customers are more likely to be rewarded than other managers who do not attempt to improve quality of service.

Q18 1.79 75Our bank emphasizes serving existing customers as much or more than it emphasizes selling to acquire new customers.

1.85 74 AVERAGE FOR MANAGEMENT COMMITMENT GAPQ19 2.26 67 In our bank we set specific quality of product and quality of service goals.

2.26 67 AVERAGE FOR GOAL SETTING GAP

Q20 2.22 68Our bank effectively uses technology and automation to achieve consistency and excellence in serving customers

2.22 68 AVERAGE FOR TASK STANDARDIZATION GAP

Q21 1.96 72Our bank has the necessary human and technological capabilities to meet customers requirements for high quality service and products.

Q22 1.30 83Our bank believes that giving customers the high quality of products and service they really want will result in HIGHER PROFITS for the bank.

1.63 78 AVERAGE FOR FEASIBILITY GAP

1.89 73AVERAGE FOR RESPONSIVENESS GAP (QUESTIONS 15-22)

Q23 1.65 78 Everyone in my bank contributes to a team effort in serving customers.Q24 1.66 77 Employees in the bank feel a sense of responsibility to help fellow employees do their jobs well.

1.65 77 AVERAGE FOR TEAMWORK GAPQ25 1.09 87 I have the necessary capabilities, training, and resources to do my job well.Q26 1.57 79 My bank hires people who are qualified to do their jobs.

1.33 83 AVERAGE FOR EMPLOYEE/JOB FIT GAPQ27 1.31 83 My bank gives me the necessary tools, equipment, and technology I need to perform my job well.

1.31 83 AVERAGE FOR TECHNOLOGY/JOB FIT GAPQ28 1.27 84 I have the freedom in my job to truly satisfy my customers' needs.

1.27 84 AVERAGE FOR PERCEIVED CONTROL GAPQ29 1.64 78 My job performance appraisal includes how well I interact with and serve customers.

Q30 1.86 74In the bank, employees who do the best job of serving their customers are more likely to be rewarded (monetarily and non-monetarily) than other employees.

1.75 76 AVERAGE FOR SUPERVISORY CONTROL GAP

Q31 1.81 75The emphasis the bank places on selling to customers is NOT so great that it makes it difficult to serve existing customers properly.

Q32 2.11 70 What my customers want me to do and what management wants me to do are usually the SAME thing.Q33 1.44 81 Bank management and I have the same ideas about how to best perform my job.

1.79 75 AVERAGE FOR ROLE CONFLICT GAP

Q34 1.49 80I understand and have sufficient knowledge about all the products and services offered by the bank (including digital products and services) to serve customers' needs.

Q35 1.29 83 I am able to keep up with changes in the bank's products and service that affect how well I can do my job.

Q36 1.48 80I believe that I have been well-trained by the bank in how to effectively meet customers' needs and expectations.

Q37 1.19 85 I am sure which aspects of my job my supervisor will stress most in evaluating my performance.

1.36 82 AVERAGE FOR ROLE AMBIGUITY GAP

1.52 80 AVERAGE FOR ASSURANCE GAP(QUESTIONS 23-37)

Net Promoter Score (NPS)

How likely is it that you would recommend the ______ Bank to a friend or colleague?

0 1 2 3 4 5 6 7 8 9 100=Not at All 5 = Neutral 10 = Extremely

Likely Likely

Source: ‘The One Number You Need,’ Harvard Business Review, Frederick Reichheld, December 2003.

The ONE Critical Question for Profitability Growth

Net Promoter Score

Calculate the percentage of customers who respond with 9 or 10 (promoters) and the percentage who respond with 0 through 6 (detractors) and passively satisfied (7 and 8).

Subtract the detractor percentage from the promoters percentage.

Result: Net-Promoter Score

Net Promoter Score

Note: The median net-promoter score for more than 400 companies based on 130,000 customer survey responses was just 16 percent.

High profit and high growth firms need an NPS of

30 - 40 percent or greater.

`

Customer Experience (Effort) Score (CES)

How much effort did you personally have to put forth to handle your request?

Very Low Very High

Effort Effort

1 2 3 4 5

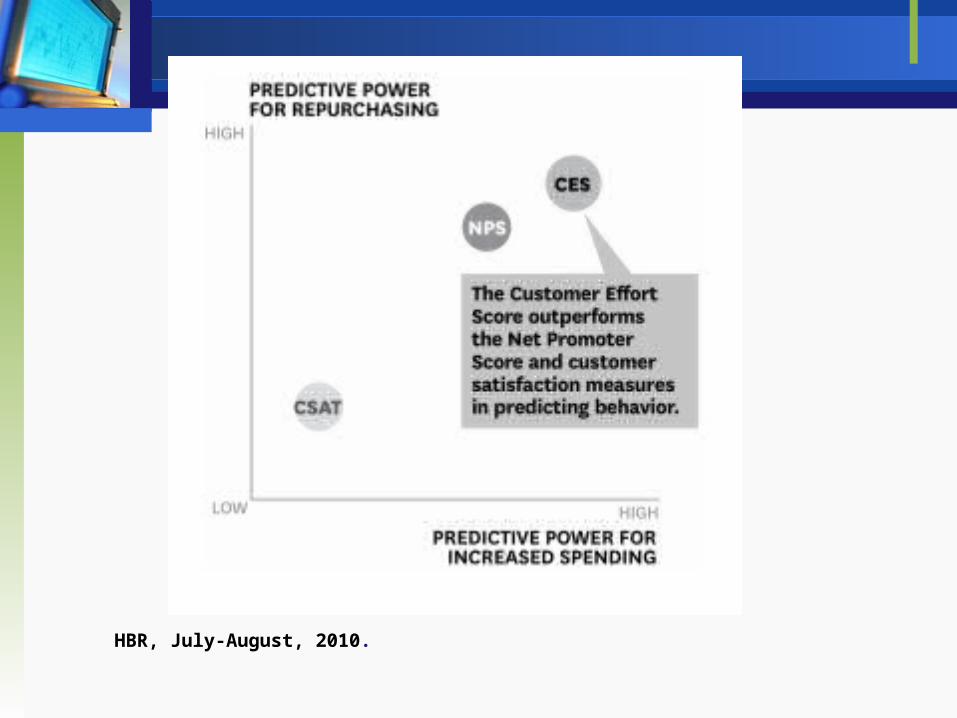

Harvard Business Review, ‘Stop Trying to Delight Your Customers,’ July-August, 2010.

HBR, July-August, 2010.

CEB: Corporate Executive Board www.executiveboard.com

HBR, July-August, 2010.

System Usability Scale (SUS)

Sources of Information

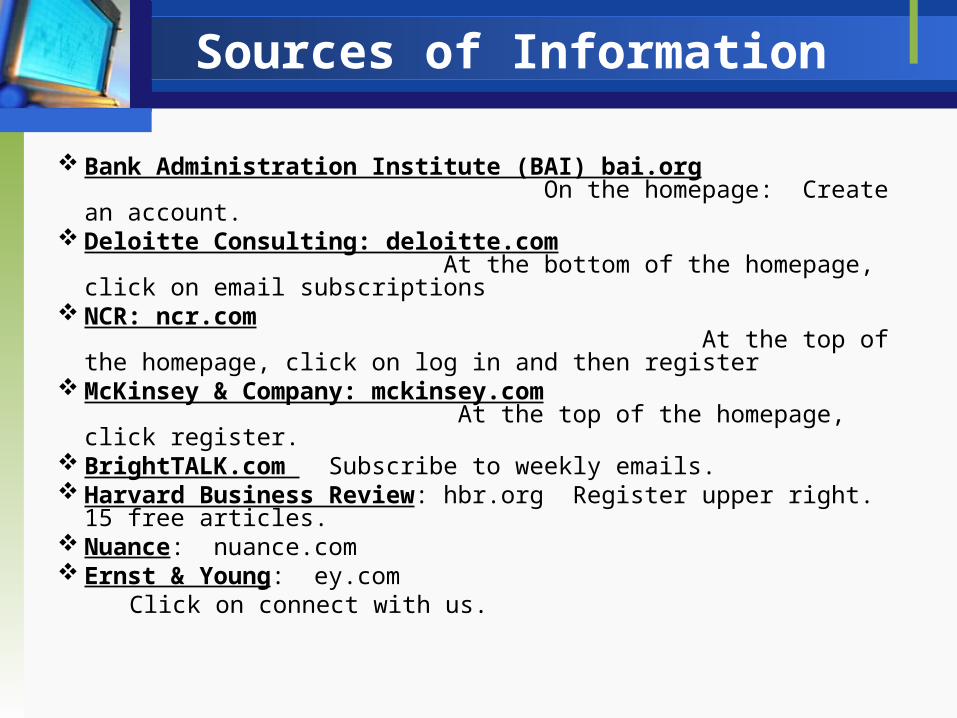

Bank Administration Institute (BAI) bai.org On the homepage: Create an account.

Deloitte Consulting: deloitte.com At the bottom of the homepage, click on email subscriptions

NCR: ncr.com At the top of the homepage, click on log in and then register

McKinsey & Company: mckinsey.com At the top of the homepage, click register.

BrightTALK.com Subscribe to weekly emails. Harvard Business Review: hbr.org Register upper right. 15

free articles. Nuance: nuance.com Ernst & Young: ey.com Click on connect with us.

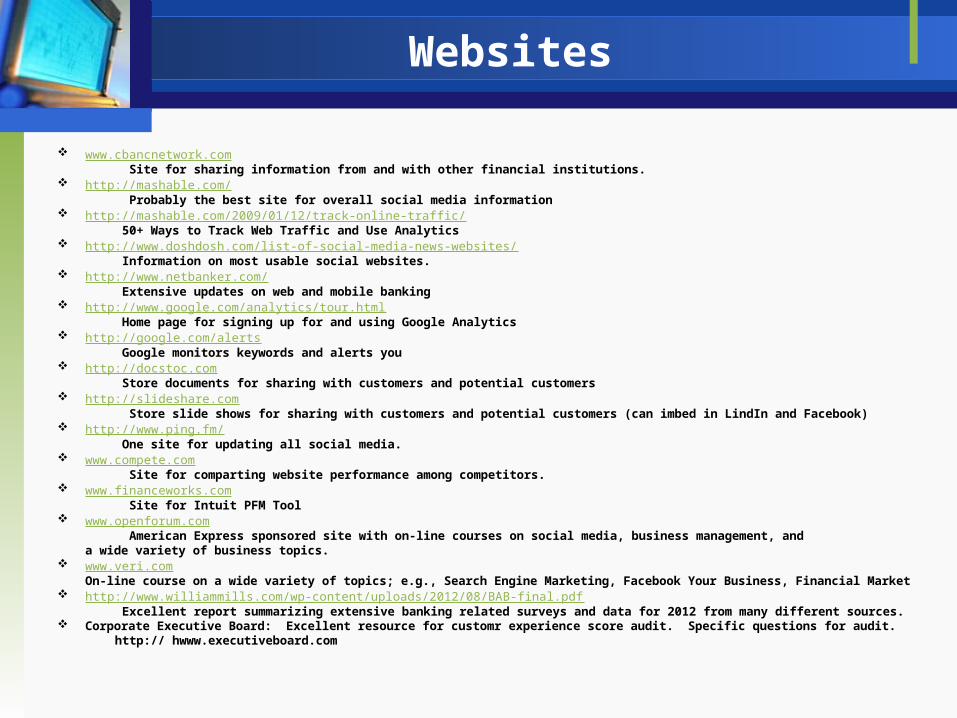

www.cbancnetwork.com Site for sharing information from and with other financial institutions. http://mashable.com/ Probably the best site for overall social media information http://mashable.com/2009/01/12/track-online-traffic/ 50+ Ways to Track Web Traffic and Use Analytics http://www.doshdosh.com/list-of-social-media-news-websites/ Information on most usable social websites. http://www.netbanker.com/ Extensive updates on web and mobile banking http://www.google.com/analytics/tour.html Home page for signing up for and using Google Analytics http://google.com/alerts Google monitors keywords and alerts you http://docstoc.com Store documents for sharing with customers and potential customers http://slideshare.com Store slide shows for sharing with customers and potential customers (can imbed in LindIn and Facebook) http://www.ping.fm/ One site for updating all social media. www.compete.com Site for comparting website performance among competitors. www.financeworks.com Site for Intuit PFM Tool www.openforum.com American Express sponsored site with on-line courses on social media, business management, and

a wide variety of business topics. www.veri.com

On-line course on a wide variety of topics; e.g., Search Engine Marketing, Facebook Your Business, Financial Market http://www.williammills.com/wp-content/uploads/2012/08/BAB-final.pdf Excellent report summarizing extensive banking related surveys and data for 2012 from many different sources. Corporate Executive Board: Excellent resource for customr experience score audit. Specific questions for audit. http:// hwww.executiveboard.com

Websites

Summary: 4 Key Questions

1. How do we FIND OUT what customers want – both outcome and process qualities?EMPATHY

2. How do we PROVIDE what the customers want?

RESPONSIVENESS AND ASSURANCE3. How do we MEASURE firm, group, and

individual performance on key ‘Customer Valued’ attributes?

4. How do we REWARD exceptional performance on ‘Customer Valued’ attributes?

Greatest Competitive Advantage in the World

Customers Go Where They Get Rewarded for Going

Customers Stay Where They Get Rewarded for Staying

“We do not act rightly because we have virtue or excellence, but we

rather have those because we have acted rightly. We are what

we repeatedly do.”

“Excellence, then, is not an act but a habit.”

-- Aristotle

Yoda

“I’ll Try!”

“Try Not.

Do or Do Not.There Is No TRY!”

Commit yourself and your bank to doing…to providing exceptional

customer satisfaction and performance

Then you will simply be THE BEST!

And the most PROFITABLE!

In Conclusion:

Success Is A Journey ...

Not A Destination

And I Wish You Well on Your Journey of

Success

Thank You

Appendix ABank Competitive GAP

Analysis

General GAP Level Guidelines:

GAPS: 0-1.25 Probably not a significant competitive problem 1.25-1.75 Unclear…may or may not be a significant problem…interpret as you

would a financial analysis ratio. For example, if you had a potential borrower with a low current ratio (current assets divided by current liabilities), this might or might not be a problem for the company….you would look for the specific reasons. The same thought process applies to the GAP analysis. From 1.25 to 1.75, these might or might not be a problem. Analyze the GAP and then assess whether or not that particular GAP level inhibits your bank or area’s ability to retain or acquire customers from the chosen target market.

1.75 Probably a significant competitive positioning problem. If you don’t or Higher consider it a significant problem, explain your reasoning.

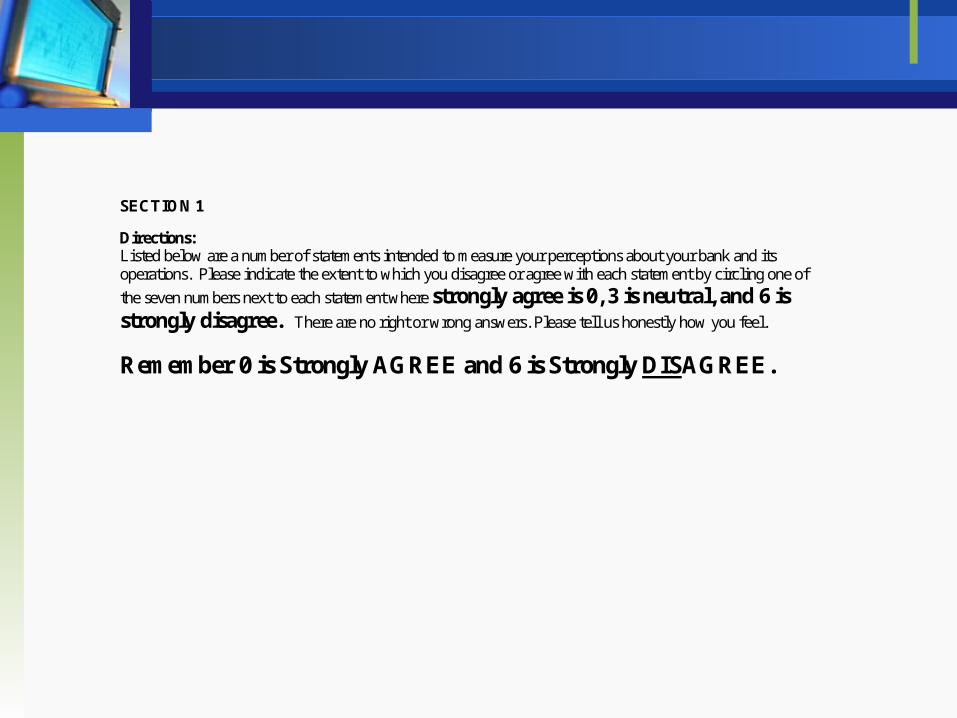

SECTION 1

Directions: Listed below are a number of statements intended to measure your perceptions about your bank and its operations. Please indicate the extent to which you disagree or agree with each statement by circling one of

the seven numbers next to each statement where strongly agree is 0, 3 is neutral, and 6 is strongly disagree. There are no right or wrong answers. Please tell us honestly how you feel.

Remember 0 is Strongly AGREE and 6 is Strongly DISAGREE.

Strongly Strongly Agree Disagree

1. The bank regularly collects information about the needs 0 1 2 3 4 5 6 and product/service expectations of our customers.

2. The bank effectively uses digital techniques (including 0 1 2 3 4 5 6 website analytics and social media) to better understand customers and to communicate with them more effectively. 3. The bank uses data mining and analytics to assess 0 1 2 3 4 5 6 customer financial usage and to predict additional . products to serve customers better. 4. The bank regularly uses marketing research and other 0 1 2 3 4 5 6 information gathered from customers in the bank’s decision-making. 5. Manager in our bank frequently interact with customers. 0 1 2 3 4 5 6 6. The customer-contact personnel in our bank 0 1 2 3 4 5 6 communicate frequently with management. 7. Managers in our bank frequently seek suggestions about 0 1 2 3 4 5 6 serving customers from customer-contact personnel. 7. The managers in our bank frequently have face-to-face 0 1 2 3 4 5 6 interactions with customer-contact personnel. 8. The primary means of communication in our bank 0 1 2 3 4 5 6 between contact-personnel and upper management is NOT memos, texts, or email. 9. There are NOT too many levels of management between 0 1 2 3 4 5 6 customer-contact personnel and top management in the bank.

Strongly Strongly Agree Disagree 10. The people who develop our advertising and social 0 1 2 3 4 5 6 media consult employees like me about the realism of the promises made in our advertising/social media. 11. I am almost always aware in advance of the promises 0 1 2 3 4 5 6

made in our bank’s advertising and social media campaigns. 12. Employees like me interact with operations and IT 0 1 2 3 4 5 6 people to discuss the quality of products and service the bank can deliver to its customers. 13. Our bank’s policies on serving customers are 0 1 2 3 4 5 6

consistent among the various departments and branches that interact with customers.

14. Our bank does NOT make promises we cannot keep 0 1 2 3 4 5 6 in an effort to gain or keep customers. 15. Our bank does commit the necessary resources 0 1 2 3 4 5 6 to provide high-quality products and service. 16. Our bank has internal programs for improving the 0 1 2 3 4 5 6 quality of products and service to customers. 17. In our bank, managers who improve quality of 0 1 2 3 4 5 6 quality of service are more likely to be rewarded than other managers who do not attempt to improve quality of service. 18. Our bank emphasizes serving existing customers 0 1 2 3 4 5 6 as much or more than it emphasizes selling to acquire new customers. 19. In our bank we set specific quality of product and 0 1 2 3 4 5 6 quality of service goals.. 20. Our bank effectively uses technology and automation 0 1 2 3 4 5 6 to achieve consistency and excellence in serving customers. 21. Our bank has the necessary human and technological 0 1 2 3 4 5 6 capabilities to meet customers' requirements for high quality service and products.

Strongly Strongly Agree Disagree 22. Our bank believes that giving customers the high level 0 1 2 3 4 5 6 of products and service they really want will result in HIGHER PROFITS for the bank. 23. Everyone in my bank contributes to a team effort 0 1 2 3 4 5 6 in servicing customers.

24. Employees in the bank feel a sense of responsibility 0 1 2 3 4 5 6 to help fellow employees do their jobs well.

25. I have the necessary capabilities, training, and resources 0 1 2 3 4 5 6 to do my job well. 26. My bank hires people who are qualified to do their jobs. 0 1 2 3 4 5 6 27. My bank gives me the necessary tools, equipment, and 0 1 2 3 4 5 6 technology I need to perform my job well. 28. I have the freedom in my job to truly satisfy my 0 1 2 3 4 5 6 customers' needs. 29. My job performance appraisal includes how well 0 1 2 3 4 5 6 I interact with and serve customers. 30. In the bank, employees who do the best job serving 0 1 2 3 4 5 6 their customers are more likely to be rewarded (monetarily and non-monetarily) than other employees. 31. The emphasis the bank places on selling to 0 1 2 3 4 5 6 customers is NOT so much that it makes it difficult to serve existing customers properly. 32. What my customers want me to do and what 0 1 2 3 4 5 6 management wants me to do are usually the SAME thing.

33. Bank management and I have the same ideas about 0 1 2 3 4 5 6 how to best perform my job.

34. I understand and have sufficient knowledge about all 0 1 2 3 4 5 6 the products and services offered by the bank (including digital products and services) to serve customers’ needs.

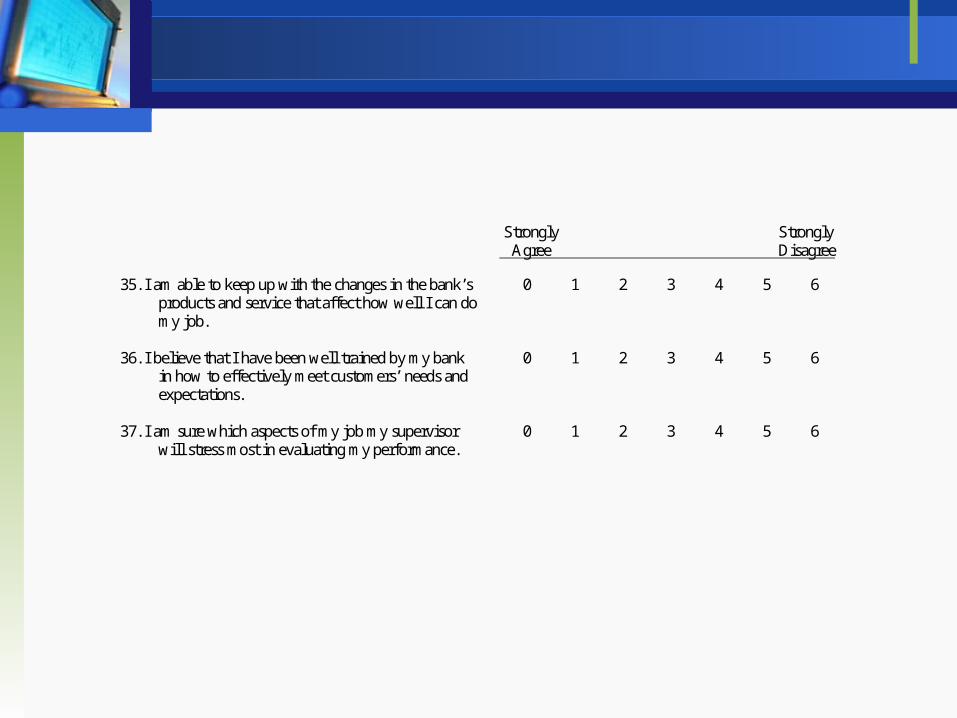

Strongly Strongly Agree Disagree

35. I am able to keep up with the changes in the bank’s 0 1 2 3 4 5 6 products and service that affect how well I can do my job. 36. I believe that I have been well trained by my bank 0 1 2 3 4 5 6 in how to effectively meet customers’ needs and expectations. 37. I am sure which aspects of my job my supervisor 0 1 2 3 4 5 6 will stress most in evaluating my performance.

SECTION 2 The questions in this section are strictly for classification and will be used only to compare how different groups within the bank feel about the issues in the questionnaire. ALL RESPONSES TO THIS QUESTIONNAIRE ARE STRICTLY ANONYMOUS. 1. How long have you been working for a bank or financial institution? ____ Less than six months ____ Six months but less than one year ____ 1-2 years ____ 3-5 years ____ 6-10 years ____ 10-20 years ____ Over 20 years

2. Do you supervise other people? ____ Yes If yes, please answer question 3. ____ No If no, skip to question 4.

3. How many people do you normally supervise? Full-Time Employees: ____ 1-2 ____ 3-5 ____ 6-10 ____ Over 10

Part-Time Employees: ____ None ____ 1-2 ____ 3-5 ____ 6-10 ____ Over 10 4. How much of your average work day is spent in direct contact with bank customers? ____ 0 percent ____ Less than 10 percent ____ 10-30 percent ____ 31-50 percent ____ 51-70 percent ____ 71-90 percent ____ Over 90 percent

THANK YOU FOR YOUR HELP AND COOPERATION

Questionnaires from: Rex Bennett, Ph.D., and The Customer Driven Company by Richard C. Whiteley of The Forum Corporation and Delivering Quality Service by Zeitham, Parasuraman, and Berry.

Appendix B

Customer Satisfaction and Dissatisfaction

Important Customer Characteristics

At any one time, one-fourth of a bank’s customers are upset enough to leave if they perceive there is a reasonable alternative

A bank hears from only about 3-30% of dissatisfied customers (depending on the severity of the problem)

Most go quietly awayMost never return

Dissatisfied customer tells 8-10 others They want REVENGE!

7 out of 10 will continue to do business with you if you resolve the problem

95% will if you resolve the problem on the spot and they are your MOST LOYAL CUSTOMERS!

Important Customer Characteristics

Very Dissatisfied

Very Satisfied

Customer Dissatisfaction vs. Customer Satisfaction

Are there different factors that produce these customer

reactions?

People in Their Work Environment

Satisfiers Dissatisfiers

Top Three Factors Influencing Job Satisfaction

3.

2.

1.

Linked to

Products…Outcomes… What

Very No

Dissatisfied Dissatisfaction

Customer Dissatisfaction

Customer Satisfaction

Linked to Service…Process…How

Customer Satisfaction

Linked to Service…Process…How

No Very

Satisfaction Satisfied

Customer Satisfaction

Linked to Service…Process…How Empathy Responsiveness Assurance

Appendix C

VITAREX BENNETT, Ph.D.

SUMMARYA combination of business, management, and academic experience provides a broad basis and integrated perspective for competitive strategy, bank financial

management strategy, customer satisfaction retention, and strategic planning consulting.

CONSULTING EXPERIENCECompetitive strategy, bank financial management, customer satisfaction, strategic planning, and marketing research consultant to a number of international

and national banks and other firms. Among the clients: International and National Banks and Organizations• American Bankers Association • First Data Resources • Medtronic, Inc.• Bank of America • First USA BankCard • Risk Management Resources, Inc.

• Bank Marketing Association • Kaiser-Permanente HMO • Target Department Stores• Capital One • Key Banks (KeyCorp) • US Treasury Department• Citicorp • KPMG Peat Marwick • US Agency for International Development

Regional and Local Banks and Organizations: Over 300 Clients

Banking and Executive Program Faculty Member Instructor and Lecturer on Competitive Strategy, Strategic Planning, Strategic Marketing, and Bank Financial Management.

• Barret School of Banking • Graduate School of Banking at Colorado • Southwestern GSB at SMU • Graduate School of Banking at LSU • Graduate School of Banking Madison, W I • School of Bank Marketing• Stonier Graduate School of Banking • Pacific Coast Banking School • US Treasury Department

SPEAKER AND PRESENTER Nationally and internationally recognized speaker at hundreds of businesses, organizations, associations, and executive and management development

seminars and courses. Speeches in the areas of achieving competitive advantage, becoming a customer-driven organization, customer satisfaction and retention, and strategic planning and thinking.

International ExperienceSpeaker and instructor for bank financial strategies, competitive strategies, and marketing strategies in Austria, Bulgaria, China, Czech Republic, Hong Kong, Indonesia, Poland, Romania, Slovakia, Thailand, and Ukraine.

Manager, International Financial Services, KPMG Peat Marwick, Prague, the Czech Republic. Responsible for developing and implementing bank training and curriculum for mid and upper management for the Czech banking industry. Topics included competitive advantage strategies, international banking, asset/liability management, credit, bank management, and strategic planning.

Expert Witness: Bank Profitability and New Bank FeasibilityComptroller of the CurrencySeveral State Banking Commissions and Boards

Academic Position: Professor Emeritus School of Business

University of San Francisco 2130 Fulton Street San Francisco, CA 94117-1080

Publications: Numerous articles in such publications as: The American Banker Journal of Retail BankingBankers MagazineBank Marketing

Contact: Rex Bennett, Ph.D. President, Achieving Unlimited 4 Excelso Trace Hot Springs Village, AK 71909

(415) 302-1182 Cell (501) 226-5555