© the mcgraw-hill companies, inc., 2000 5-1 operating cycle decision-making you are here! special...

TRANSCRIPT

© The McGraw-Hill Companies, Inc., 2000

5-1

Operating cycle decision-making

YOU ARE HERE!

Special order decisions

Discontinue product line decisions

Make or buy decisions

Chapter 5

Short-Tem

Operating

Decisions

Indifference point decisions

Sell or process further decisions

© The McGraw-Hill Companies, Inc., 2000

5-2

PART TWO:PLANNING

Chapter 5 - Short-Term Operating Decisions

© The McGraw-Hill Companies, Inc., 2000

5-3

CHAPTER 5 LEARNING OBJECTIVES

L.O.1: Describe a relevant variable analysis for making short-term operating decisions.

L.O.2: Use a relevant variable analysis to analyze a special order accept-or-reject decisions.

L.O.3: Employ a relevant variable analysis to assess a make-or-buy decision.

L.O.4: Apply a relevant variable analysis to solve sell-now-or-process-further and sell-later decisions.

© The McGraw-Hill Companies, Inc., 2000

5-4

CHAPTER 5 LEARNING OBJECTIVES

L.O.5: Use a relevant variable analysis to analyze decisions to discontinue a product line.

L.O.6: Apply the indifference point concept to assess short-term operating decisions.

L.O.7: (Appendix) Determine product mix in a scarce resource environment.

© The McGraw-Hill Companies, Inc., 2000

5-5

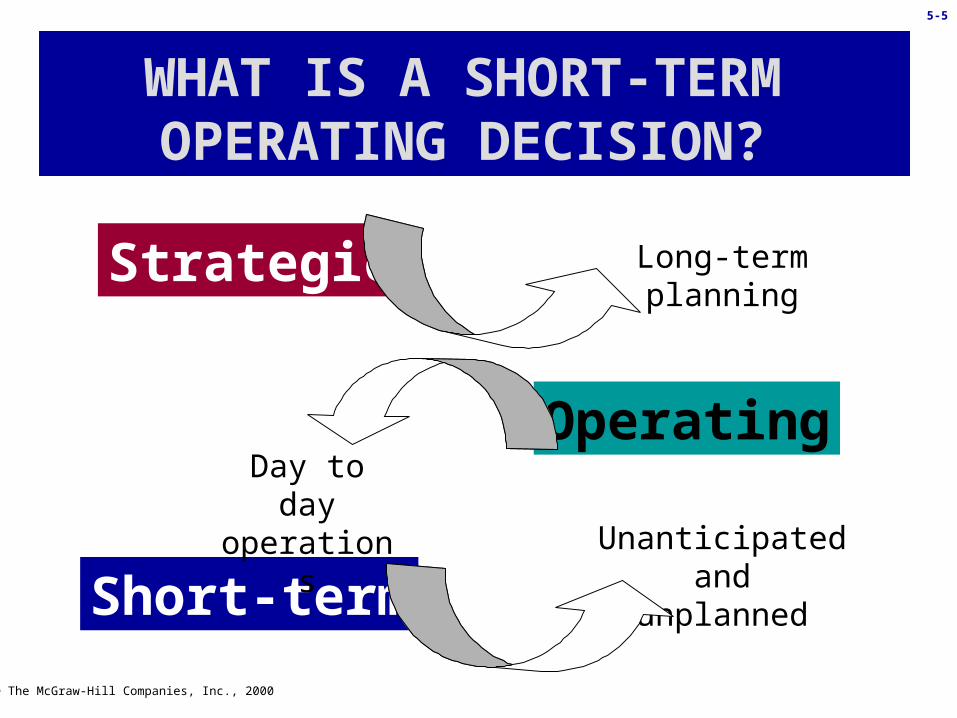

Operating

Strategic

Short-term

WHAT IS A SHORT-TERM OPERATING DECISION?

Long-termplanning

Day to dayoperations

Unanticipated andunplanned

© The McGraw-Hill Companies, Inc., 2000

5-6

Assumes current capacity is fixed since, in the short-term, a company cannot increase its physical capacity.

Decisions not planned as part of the management cycle; ad hoc opportunities or issues that must be addressed in a timely manner.

Unique decisions - each decision must be analyzed as a distinct opportunity.

SHORT-TERM OPERATING DECISION vs. OTHER

OPERATING DECISIONS

© The McGraw-Hill Companies, Inc., 2000

5-7

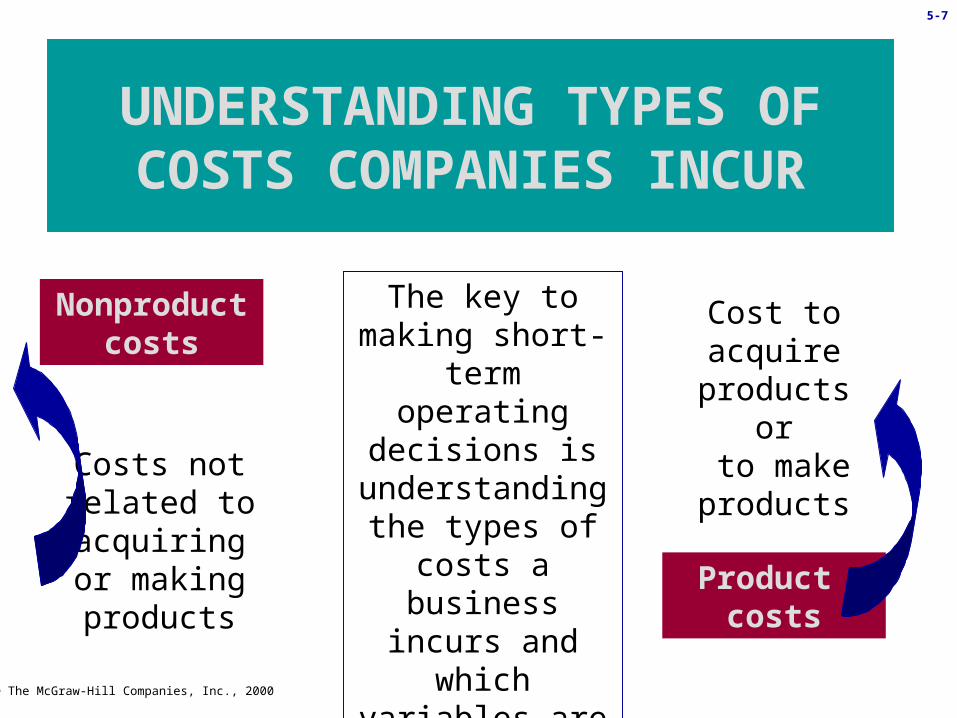

UNDERSTANDING TYPES OF COSTS COMPANIES INCUR

The key to making short-term

operating decisions is

understanding the types of costs a business incurs

and which variables are

relevant.

Nonproduct costs

Product costs

Cost to acquire

products or to make productsCosts not

related to acquiring or

making products

© The McGraw-Hill Companies, Inc., 2000

5-8

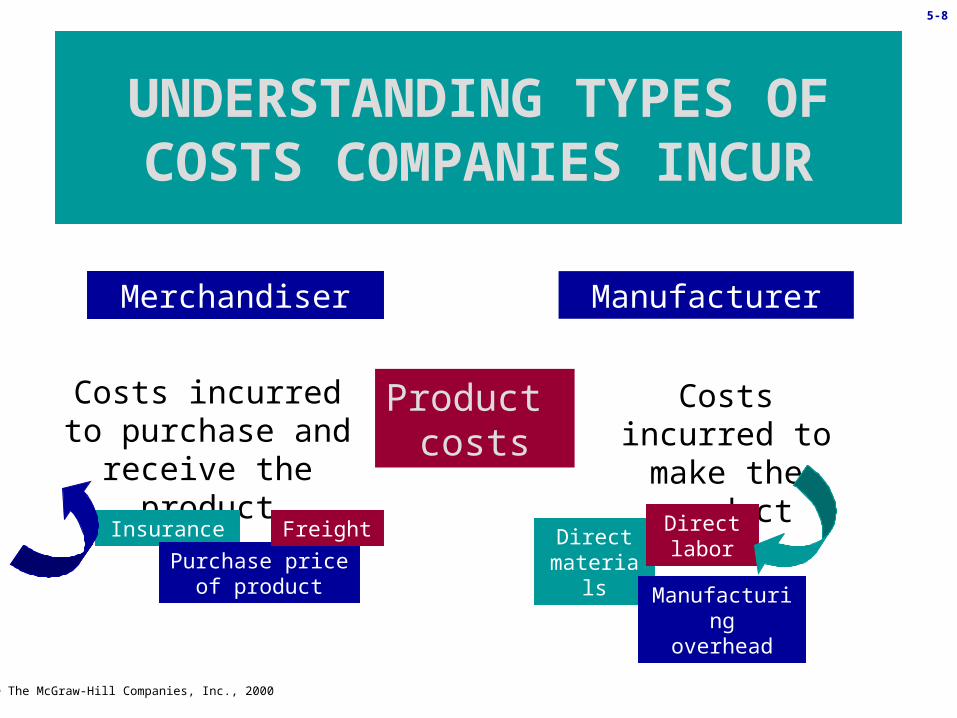

UNDERSTANDING TYPES OF COSTS COMPANIES INCUR

Product costs

Merchandiser Manufacturer

Costs incurred to purchase and

receive the product

Costs incurred to make the

product

Directmaterials

Directlabor

Manufacturingoverhead

Insurance

Purchase price of product

Freight

© The McGraw-Hill Companies, Inc., 2000

5-9

UNDERSTANDING TYPES OF COSTS COMPANIES INCUR

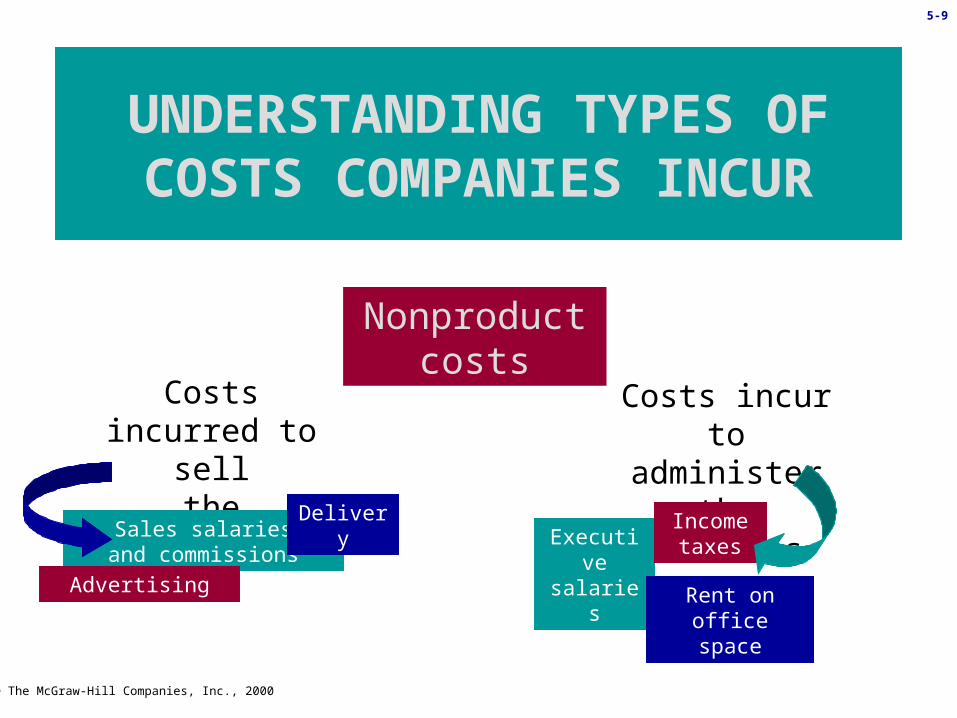

Nonproductcosts

Costs incurred to sell

the products

Costs incur to administer the

business

Executive salaries

Income taxes

Rent on office space

Sales salariesand commissions

Advertising

Delivery

© The McGraw-Hill Companies, Inc., 2000

5-10

PAUSE AND REFLECT

If Procter & Gamble rents warehouse space for its finished products, is this rent a nonproduct or product cost? Why?

Typically, we would call rent

for finished products a nonproduct cost. However,

since storing inventory is part of the conversion cycle, we

could define it as a product cost.

Typically, we would call rent

for finished products a nonproduct cost. However,

since storing inventory is part of the conversion cycle, we

could define it as a product cost.

© The McGraw-Hill Companies, Inc., 2000

5-11

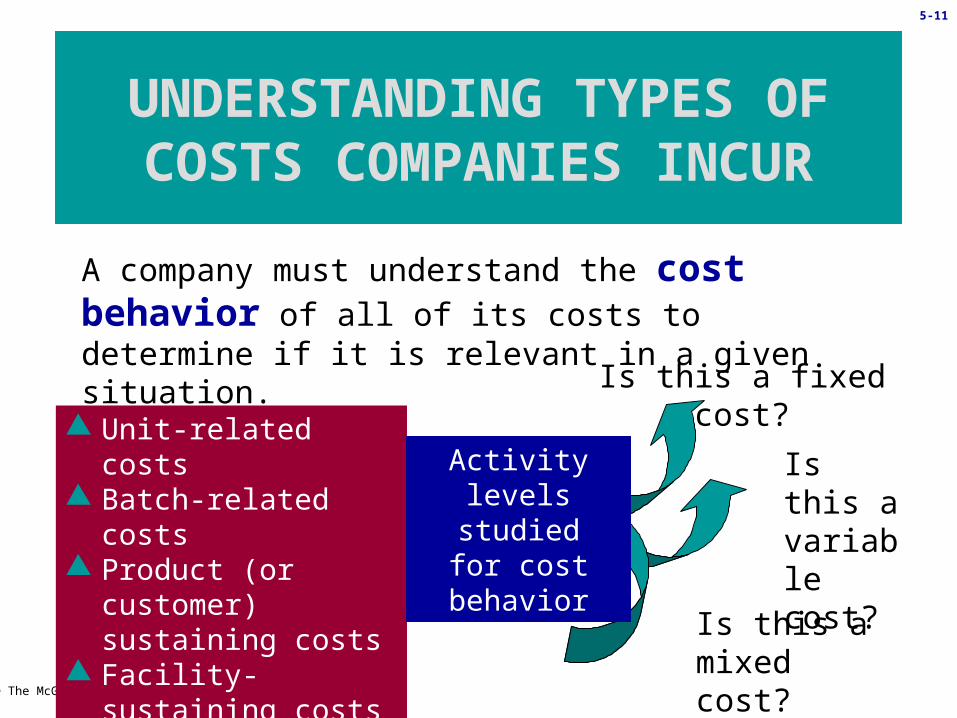

UNDERSTANDING TYPES OF COSTS COMPANIES INCUR

A company must understand the cost behavior of all of its costs to determine if it is relevant in a given situation.

Unit-related costs Batch-related costs Product (or customer)

sustaining costs Facility-sustaining

costs

Is this a fixed cost?

Is this a variable cost?

Is this a mixed cost?

Activity levels studiedfor cost

behavior

© The McGraw-Hill Companies, Inc., 2000

5-12

PAUSE AND REFLECT

Identify each of the following costs as unit-related, batch-related, product (customer) -sustaining, or facility-sustaining:

Freight paid per unit ordered

Freight paid per order

Cost incurred to service Customer A

Costs incurred to hire a new CEO

Freight paid per unit is a unit-

related cost; freight paid per order is a batch-related cost; cost incurred to service customers is a

product (customer)-sustainingcost; and costs incurred to

hire a new CEO are facility sustaining

costs.

Freight paid per unit is a unit-

related cost; freight paid per order is a batch-related cost; cost incurred to service customers is a

product (customer)-sustainingcost; and costs incurred to

hire a new CEO are facility sustaining

costs.

© The McGraw-Hill Companies, Inc., 2000

5-13

A cost or revenue that will occur in the

future and that differs among alternatives

considered.

WHAT IS A RELEVANT VARIABLE?

Focus for short-term decision

making

© The McGraw-Hill Companies, Inc., 2000

5-14

• Past cost• Irrelevant

SUNK COSTS

© The McGraw-Hill Companies, Inc., 2000

5-15

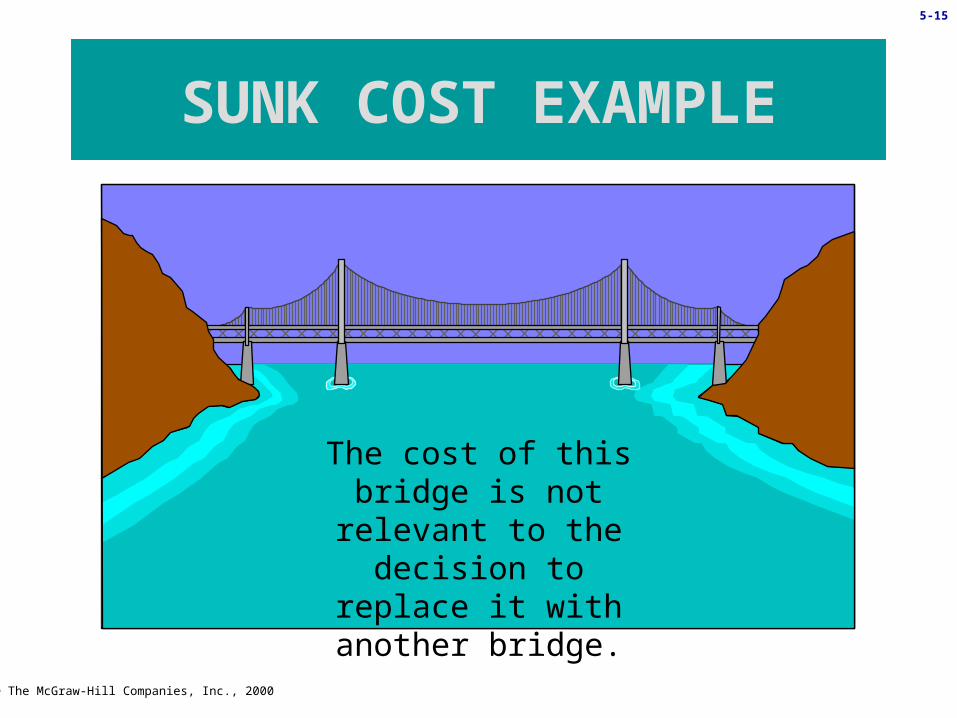

The cost of thisbridge is not relevant to the decision to replace it

with another bridge.

SUNK COST EXAMPLE

© The McGraw-Hill Companies, Inc., 2000

5-16

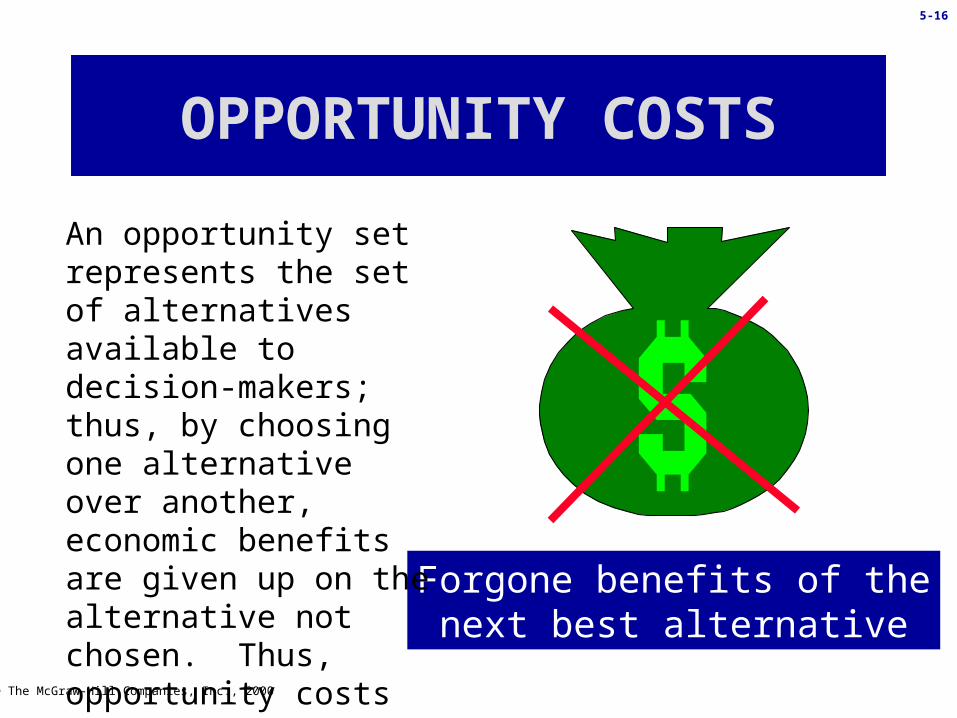

Forgone benefits of thenext best alternative

OPPORTUNITY COSTS

An opportunity set represents the set of alternatives available to decision-makers; thus, by choosing one alternative over another, economic benefits are given up on the alternative not chosen. Thus, opportunity costs are always relevant costs.

© The McGraw-Hill Companies, Inc., 2000

5-17

ECONOMIC FRAMEWORK: SHORT-TERM DECISION

MAKING

B? A?A o

r B

? D?C ?

C or D?B?

A?

C ?

I give up! Which alternative

increases operatingincome the most?

© The McGraw-Hill Companies, Inc., 2000

5-18

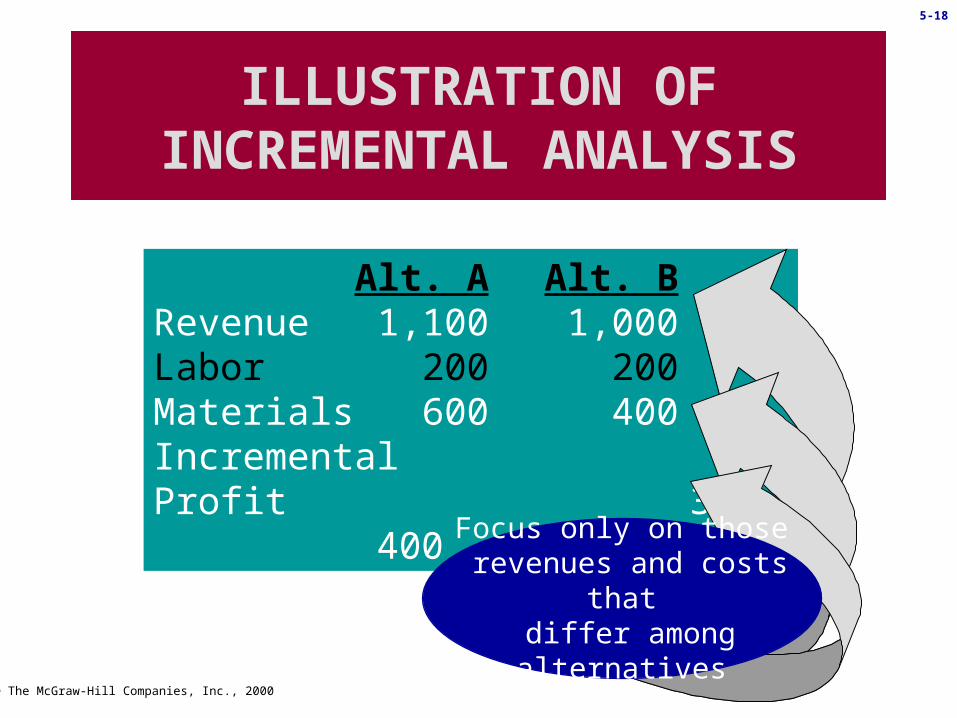

Alt. A Alt. BRevenue 1,100 1,000Labor 200 200Materials 600 400IncrementalProfit 300 400

ILLUSTRATION OF INCREMENTAL ANALYSIS

Focus only on those revenues and costs that differ among alternatives

© The McGraw-Hill Companies, Inc., 2000

5-19

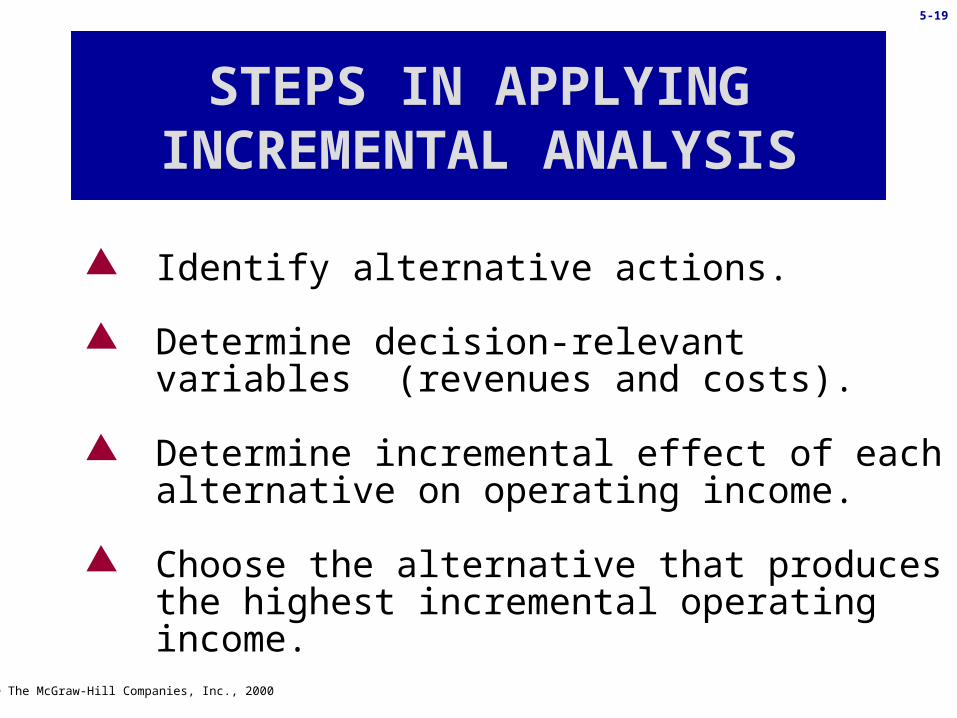

Identify alternative actions.

Determine decision-relevant variables (revenues and costs).

Determine incremental effect of each alternative on operating income.

Choose the alternative that produces the highest incremental operating income.

STEPS IN APPLYING INCREMENTAL ANALYSIS

© The McGraw-Hill Companies, Inc., 2000

5-20

Special order decisions

Make-or-buy decisions

Add or delete a product line decisions

EXAMPLES OF SHORT-TERM DECISIONS

© The McGraw-Hill Companies, Inc., 2000

5-21

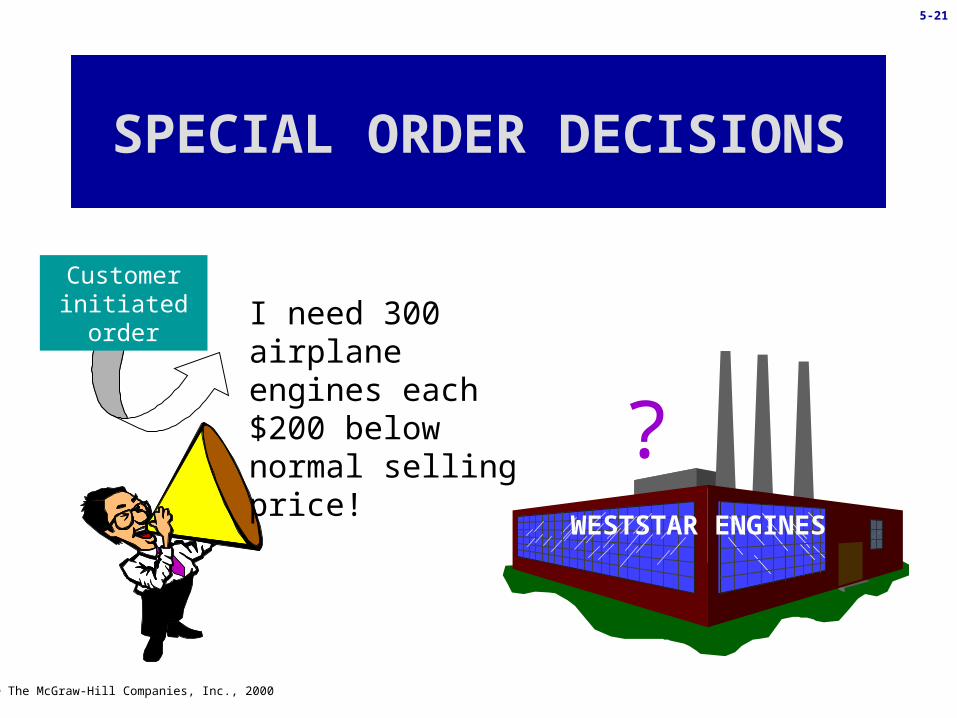

I need 300 airplane engines each $200 below normal selling price! ?

SPECIAL ORDER DECISIONS

WESTSTAR ENGINES

Customer initiated order

© The McGraw-Hill Companies, Inc., 2000

5-22

Accept special order if the relevant profit is positive.

Reject special order if the relevant profit is negative.

OPERATING DECISION RULE: SPECIAL ORDERS

© The McGraw-Hill Companies, Inc., 2000

5-23

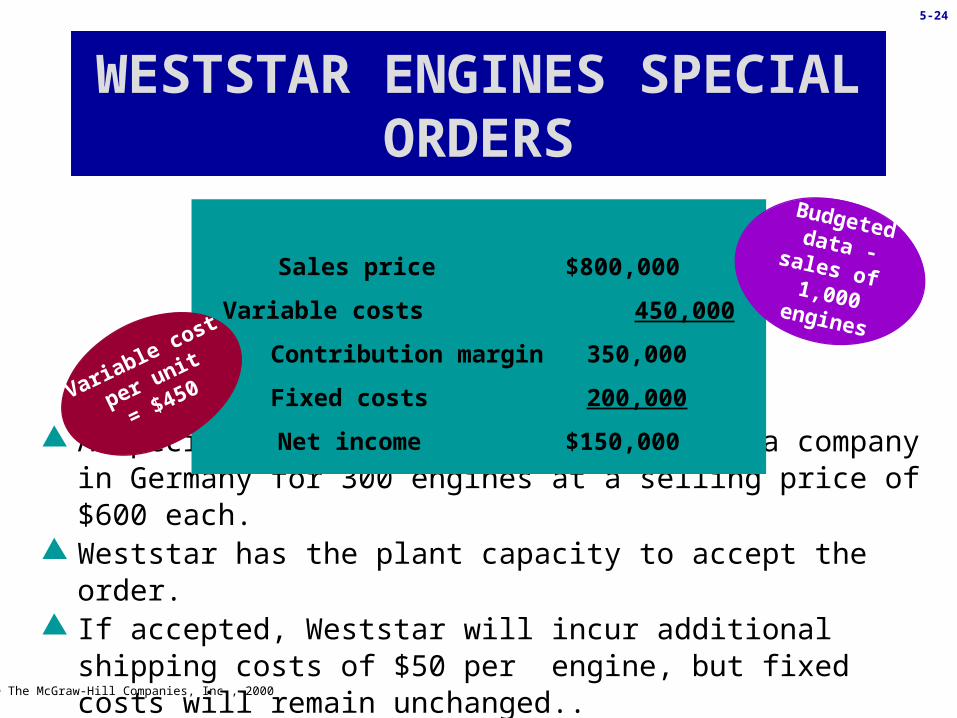

The Weststar company manufacturers and sells short-blockengines. Budgeted sales and cost data for the year are as follow:

Sales price $800,000

Variable costs 450,000

Contribution margin 350,000

Fixed costs 200,000

Net income $150,000

WESTSTAR ENGINES SPECIAL ORDERS

© The McGraw-Hill Companies, Inc., 2000

5-24

A special order has been received from a company in Germany for 300 engines at a selling price of $600 each.

Weststar has the plant capacity to accept the order. If accepted, Weststar will incur additional shipping costs of $50

per engine, but fixed costs will remain unchanged..

Sales price $800,000

Variable costs 450,000

Contribution margin 350,000

Fixed costs 200,000

Net income $150,000

Budgeted data - sales of 1,000 engines

Variable cost

per unit =

$450

WESTSTAR ENGINES SPECIAL ORDERS

Variable cost

per unit

= $450

© The McGraw-Hill Companies, Inc., 2000

5-25

WESTSTAR ENGINES SPECIAL ORDERS

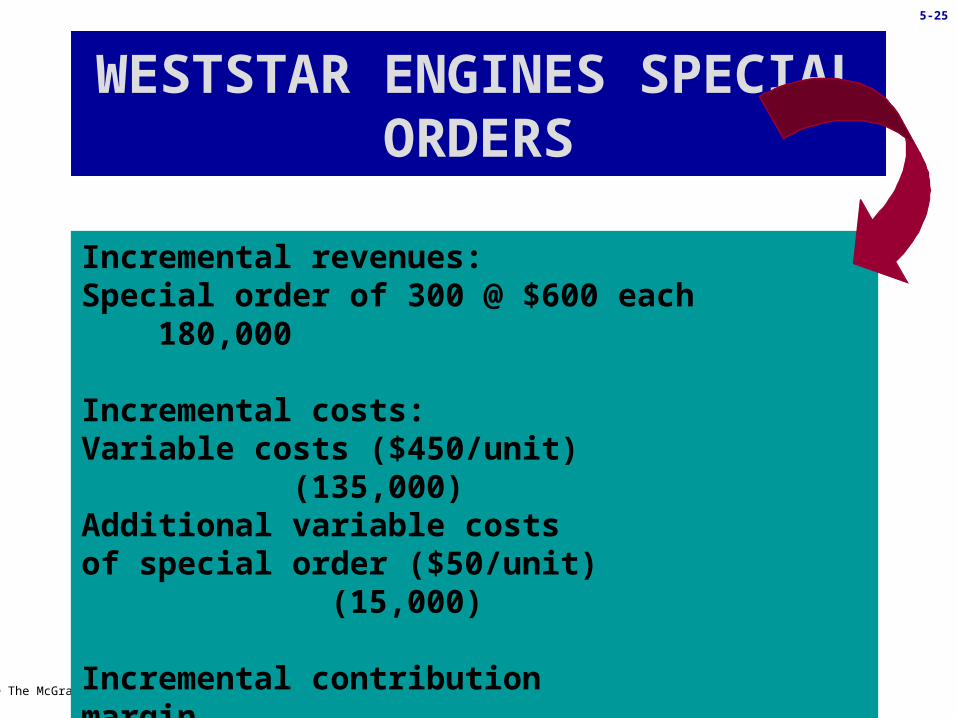

Incremental revenues:Special order of 300 @ $600 each 180,000

Incremental costs:Variable costs ($450/unit) (135,000)Additional variable costs of special order ($50/unit) (15,000)

Incremental contributionmargin 30,000

© The McGraw-Hill Companies, Inc., 2000

5-26

PAUSE AND REFLECT

If Wal-Mart approaches Procter & Gamble with a large order and requests a bid, what quantitative and qualitative factors should Procter & Gamble consider?

If P&G has the capacity, it should

consider the incremental costs to fill the order and the profit needed. P&G should also consider whether giving Wal-Mart a special price will affect the prices offered to others,

and how this short-term offer will affect long-term

pricing.

If P&G has the capacity, it should

consider the incremental costs to fill the order and the profit needed. P&G should also consider whether giving Wal-Mart a special price will affect the prices offered to others,

and how this short-term offer will affect long-term

pricing.

© The McGraw-Hill Companies, Inc., 2000

5-27

?

OR

MAKE OR BUY DECISION

HD Motorcycle Corporation

MAKEMOTORCYCLES

BUY MOTORCYLES

Outsourcing decisions

© The McGraw-Hill Companies, Inc., 2000

5-28

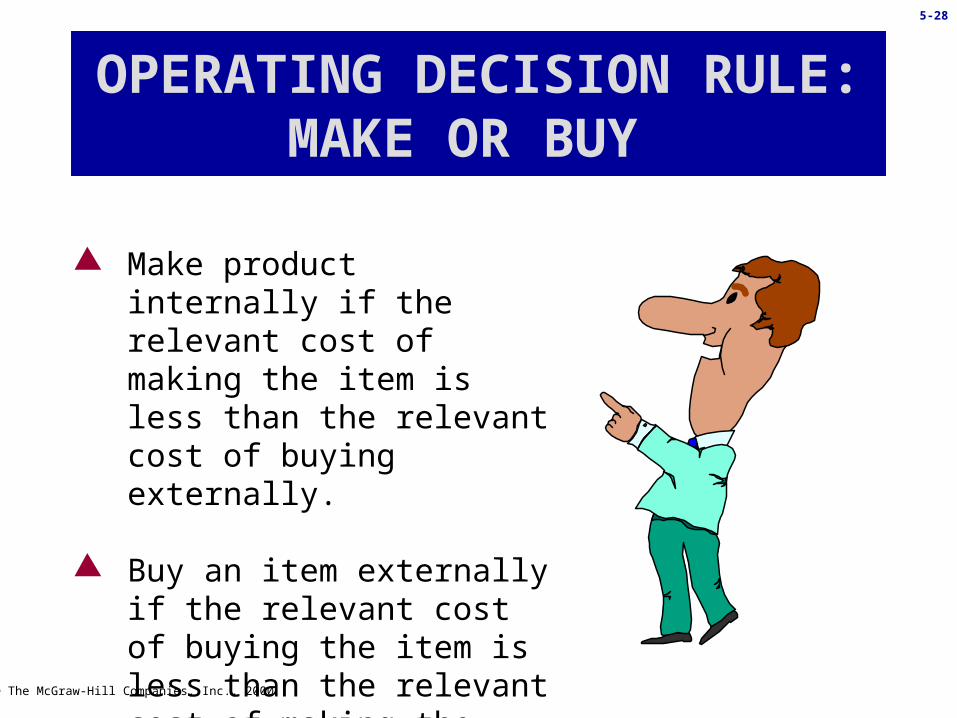

OPERATING DECISION RULE: MAKE OR BUY

Make product internally if the relevant cost of making the item is less than the relevant cost of buying externally.

Buy an item externally if the relevant cost of buying the item is less than the relevant cost of making the item.

© The McGraw-Hill Companies, Inc., 2000

5-29

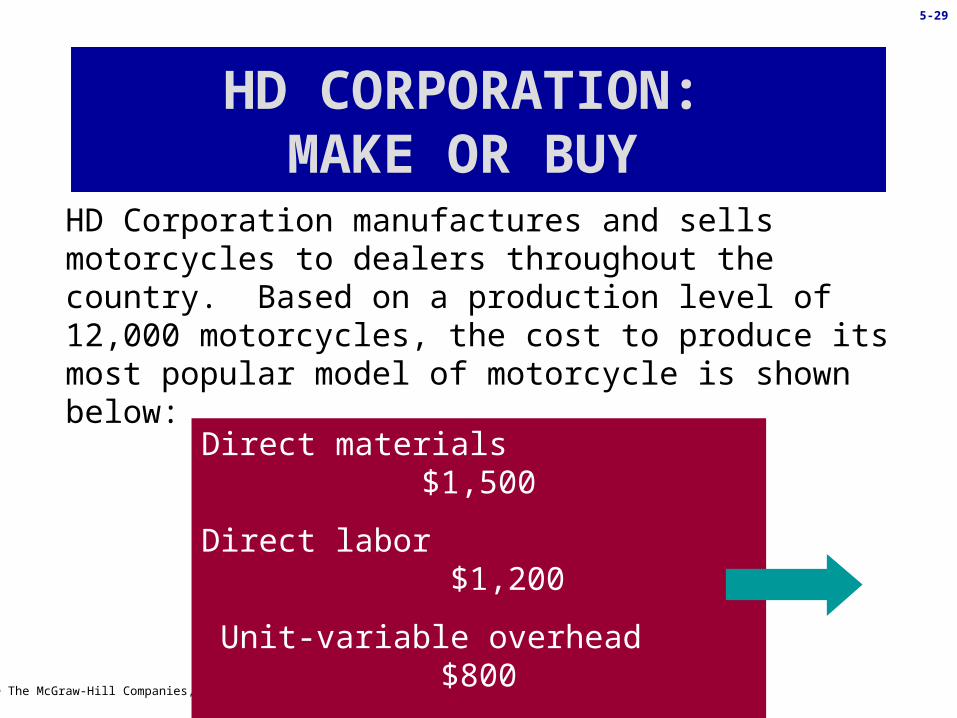

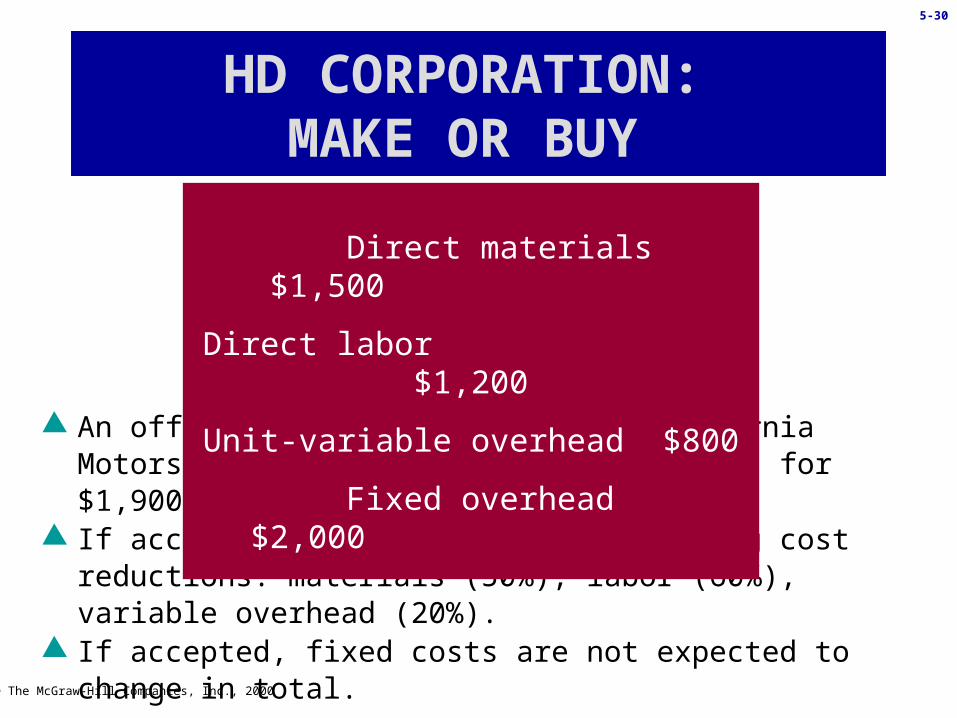

HD Corporation manufactures and sells motorcycles to dealers throughout the country. Based on a production level of 12,000 motorcycles, the cost to produce its most popular model of motorcycle is shown below:

Direct materials $1,500

Direct labor $1,200

Unit-variable overhead $800

Fixed overhead $2,000

HD CORPORATION: MAKE OR BUY

© The McGraw-Hill Companies, Inc., 2000

5-30

An offer has been received from California Motors to supply the motorcycle engines for $1,900 per engine.

If accepted, HD estimates the following cost reductions: materials (50%), labor (60%), variable overhead (20%).

If accepted, fixed costs are not expected to change in total.

Direct materials $1,500

Direct labor $1,200

Unit-variable overhead $800

Fixed overhead $2,000

HD CORPORATION: MAKE OR BUY

© The McGraw-Hill Companies, Inc., 2000

5-31

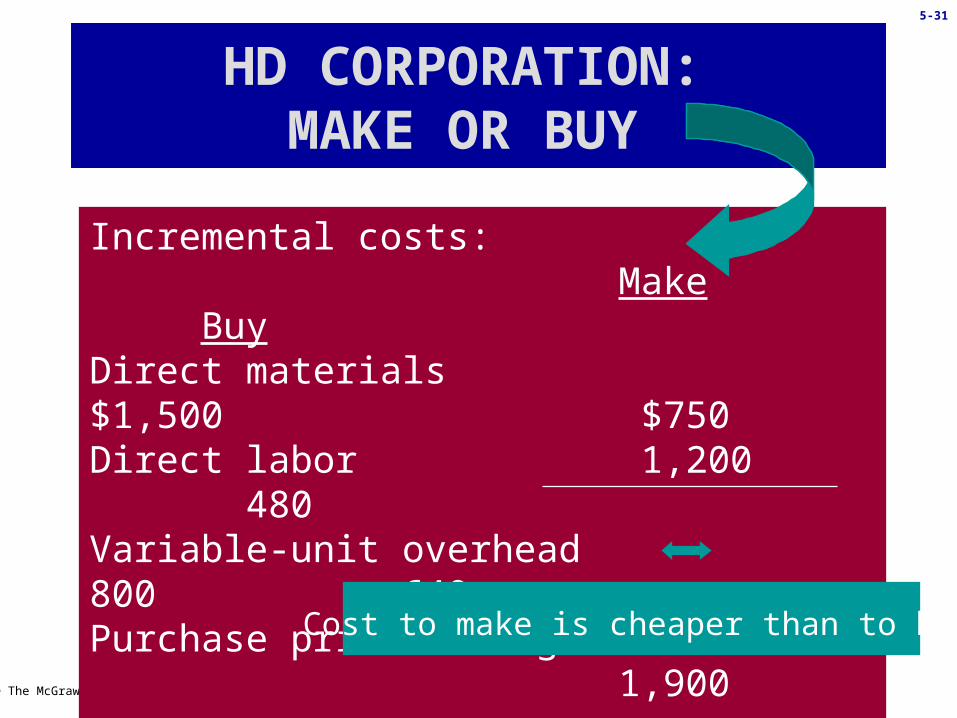

Incremental costs: Make Buy

Direct materials $1,500 $750Direct labor 1,200 480 Variable-unit overhead 800 640Purchase price of engines 1,900

Incremental cost $3,500 $3,770

HD CORPORATION: MAKE OR BUY

Cost to make is cheaper than to buy

© The McGraw-Hill Companies, Inc., 2000

5-32

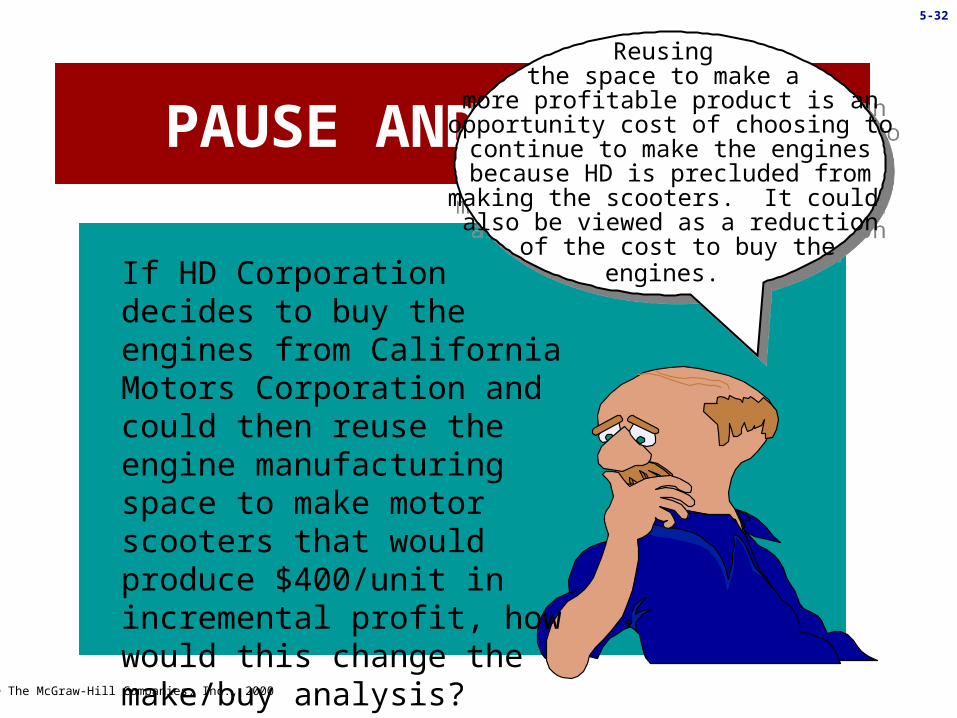

PAUSE AND REFLECT

If HD Corporation decides to buy the engines from California Motors Corporation and could then reuse the engine manufacturing space to make motor scooters that would produce $400/unit in incremental profit, how would this change the make/buy analysis?

Reusing the space to make a

more profitable product is anopportunity cost of choosing tocontinue to make the enginesbecause HD is precluded frommaking the scooters. It could also be viewed as a reduction

of the cost to buy theengines.

Reusing the space to make a

more profitable product is anopportunity cost of choosing tocontinue to make the enginesbecause HD is precluded frommaking the scooters. It could also be viewed as a reduction

of the cost to buy theengines.

© The McGraw-Hill Companies, Inc., 2000

5-33

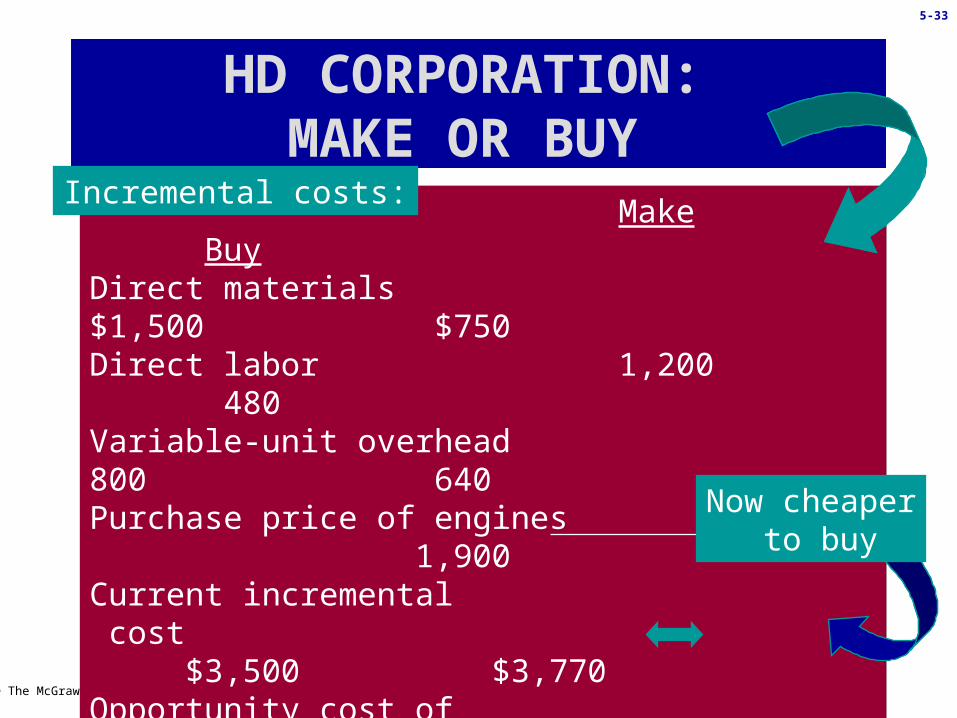

Make BuyDirect materials $1,500 $750Direct labor 1,200 480 Variable-unit overhead 800 640Purchase price of engines 1,900Current incremental cost $3,500 $3,770Opportunity cost ofmaking scooter 400

Revised incremental cost $3,900 $3,770

Make BuyDirect materials $1,500 $750Direct labor 1,200 480 Variable-unit overhead 800 640Purchase price of engines 1,900Current incremental cost $3,500 $3,770Opportunity cost ofmaking scooter 400

Revised incremental cost $3,900 $3,770

HD CORPORATION: MAKE OR BUY

Incremental costs:

Now cheaper to buy

© The McGraw-Hill Companies, Inc., 2000

5-34

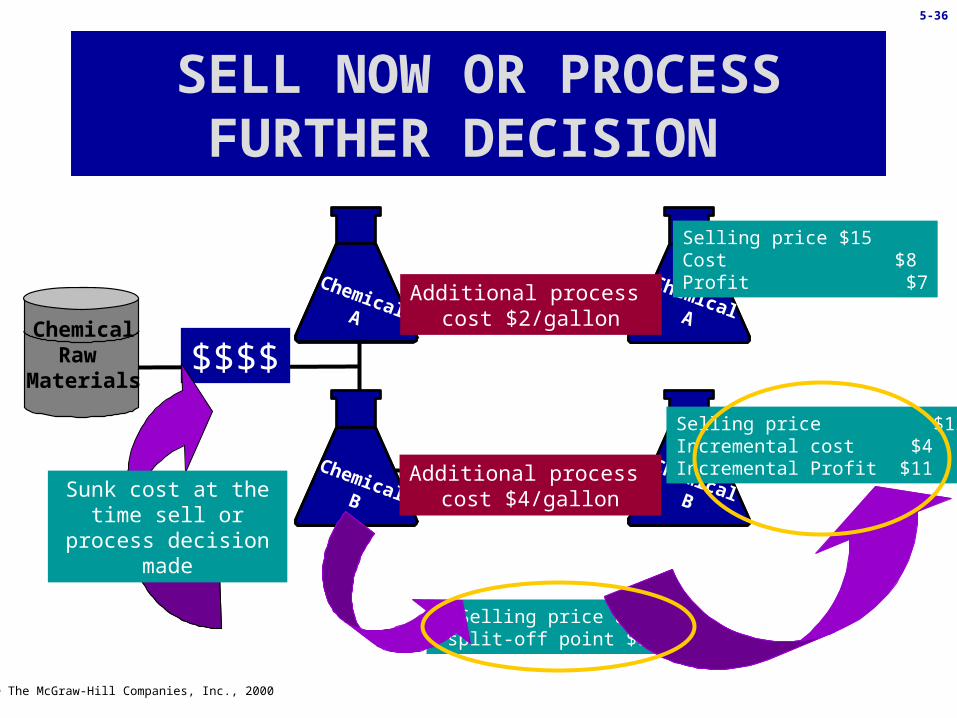

Joint costs ofprocessing tosplit-off point

$$$$

Split-offpoint

Jointproducts

Raw Materials

SELL NOW OR PROCESS FURTHER DECISION

© The McGraw-Hill Companies, Inc., 2000

5-35

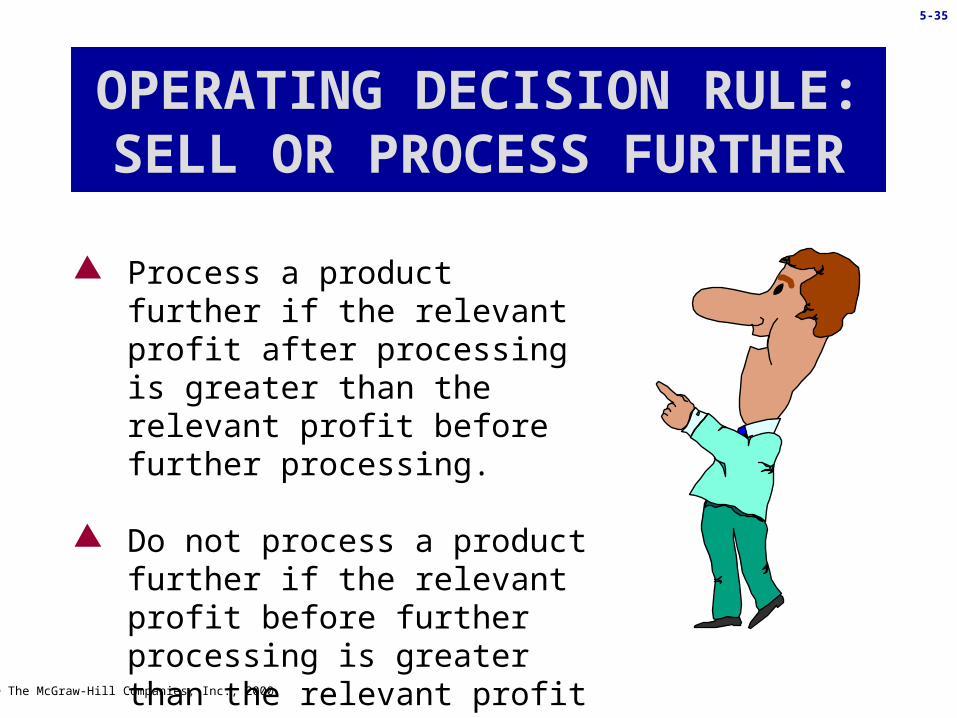

OPERATING DECISION RULE: SELL OR PROCESS FURTHER

Process a product further if the relevant profit after processing is greater than the relevant profit before further processing.

Do not process a product further if the relevant profit before further processing is greater than the relevant profit after further processing.

© The McGraw-Hill Companies, Inc., 2000

5-36

SELL NOW OR PROCESS FURTHER DECISION

$$$$Chemical

Raw Materials

ChemicalA

ChemicalBSunk cost at the time sell or process decision made

ChemicalAAdditional process

cost $2/gallon

ChemicalBAdditional process

cost $4/gallon

Selling price $15Cost $8Profit $7

Selling price $15Incremental cost $4Incremental Profit $11

Selling price at split-off point $10

© The McGraw-Hill Companies, Inc., 2000

5-37

DISCONTINUING A PRODUCT LINE

Jason Enterprises

SpecialRoast

RegularRoast

PremiumRoast

Should the unprofitable special roast

coffee be discontinued?

© The McGraw-Hill Companies, Inc., 2000

5-38

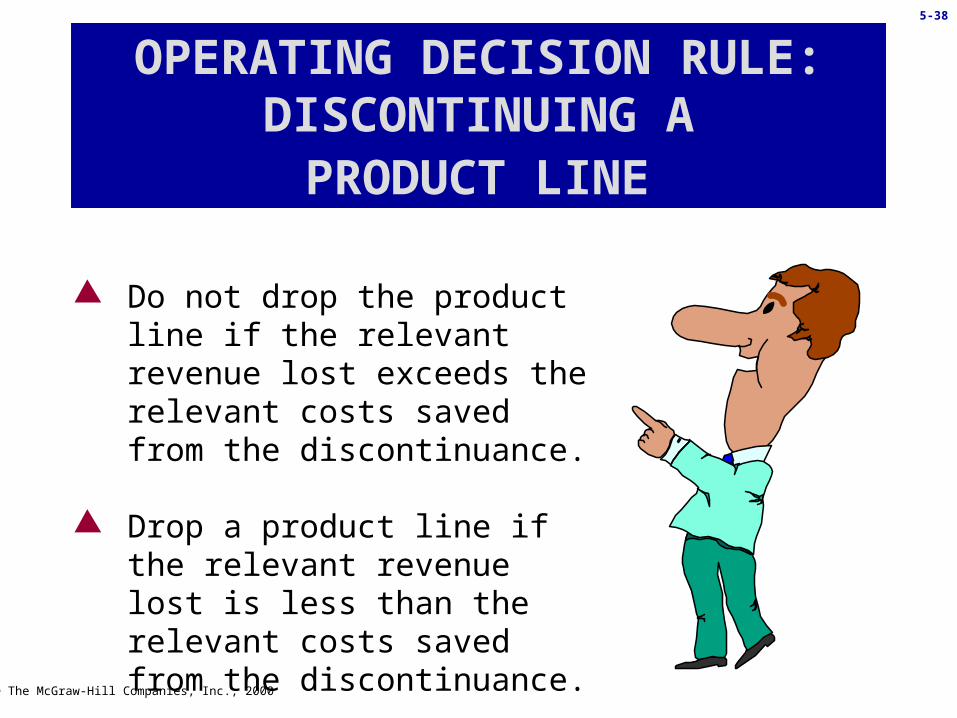

OPERATING DECISION RULE: DISCONTINUING A PRODUCT LINE

Do not drop the product line if the relevant revenue lost exceeds the relevant costs saved from the discontinuance.

Drop a product line if the relevant revenue lost is less than the relevant costs saved from the discontinuance.

© The McGraw-Hill Companies, Inc., 2000

5-39

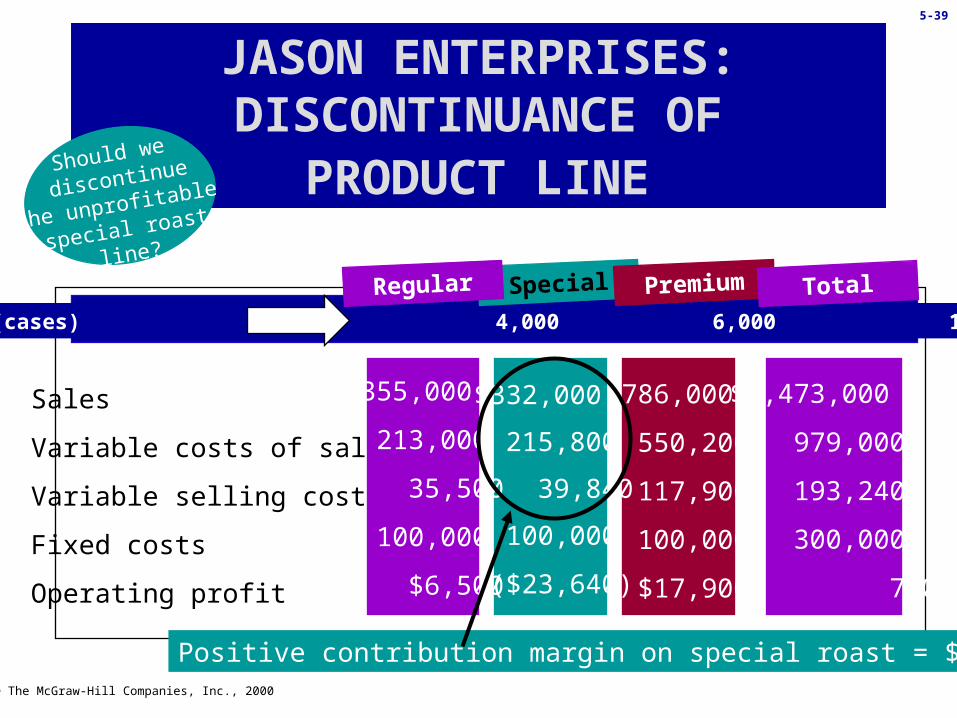

Sales (cases) 5,000 4,000 6,000 15,000

Sales

Variable costs of sales

Variable selling costs

Fixed costs

Operating profit

$355,000

213,000

35,500

100,000

$6,500

$332,000

215,800

39,840

100,000

($23,640)

$786,000

550,200

117,900

100,000

$17,900

$1,473,000

979,000

193,240

300,000

760

Special Premium TotalRegular

Positive contribution margin on special roast = $76,360

JASON ENTERPRISES: DISCONTINUANCE OF

PRODUCT LINE Should we

discontinue

the unprofitable

special roast

line?

© The McGraw-Hill Companies, Inc., 2000

5-40

Sales (cases) 5,000 6,000 11,000

Sales

Variable costs of sales

Variable selling costs

Fixed costs

Operating profit

$355,000

213,000

35,500

150,000

($43,500)

$786,000

550,200

117,900

150,000

($32,100)

$1,141,000

763,200

153,400

300,000

($75,600)

Premium TotalRegular

JASON ENTERPRISES: DISCONTINUANCE OF

PRODUCT LINE

Fixed costs do not go away; there is $76,360 less contribution margin to cover them

© The McGraw-Hill Companies, Inc., 2000

5-41

PAUSE AND REFLECT

In 1997, Procter & Gamble discontinued its Duncan Hines line. What quantitative and qualitative factors do you think led Procter & Gamble to this decision?

P&G determined that it could make a higher profitby focusing on its main product lines. In addition, it probably

considered its marketing strategy and how it would be affected

by having fewer, more closelyrelated products.

P&G determined that it could make a higher profitby focusing on its main product lines. In addition, it probably

considered its marketing strategy and how it would be affected

by having fewer, more closelyrelated products.

© The McGraw-Hill Companies, Inc., 2000

5-42

INDIFFERENCE POINT ANALYSIS

Some short-term decisions must be decided on volume. Indifference point analysiscompares the cost equations of two alternatives to derive an indifferent point - the volume point where choosing either alternative costs the same.

Who cares?I’m

indifferent!

© The McGraw-Hill Companies, Inc., 2000

5-43

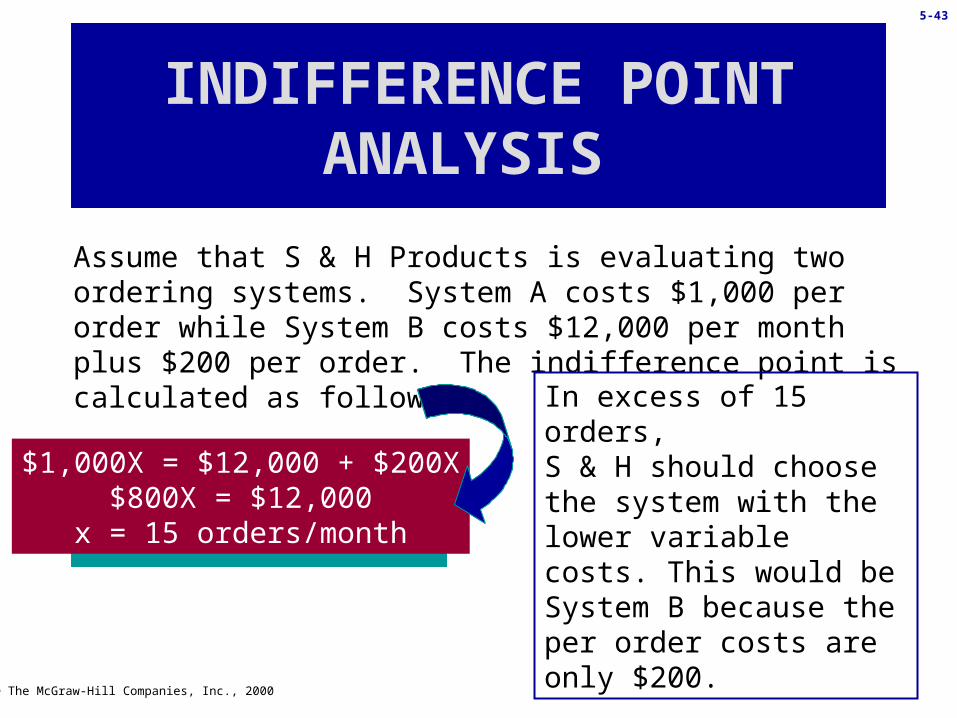

INDIFFERENCE POINT ANALYSIS

Assume that S & H Products is evaluating two ordering systems. System A costs $1,000 per order while System B costs $12,000 per month plus $200 per order. The indifference point is calculated as follows:

$1,000X = $12,000 + $200X$800X = $12,000

x = 15 orders/month

In excess of 15 orders,S & H should choose the system with the lower variable costs. This would be System B because the per order costs are only $200.