msbfile03.usc.edu · web viewi. course objective this course covers the broad field of mergers,...

TRANSCRIPT

Course Title: FBE 460: MERGERS, ACQUISITIONS AND RESTRUCTURING

Syllabus for Spring 2016

Professor: Lloyd LevitinOffice: Acc. 301EOffice Phone: 310-740-6524E-mail: [email protected]: Erika Johnson (email: [email protected]

Lecture ClassTuesday and Thursday 2:00 – 3:50 P.M. Room: HOH2

Office HoursTuesday and Thursday 4:00 – 5:00 P.M.

I. COURSE OBJECTIVE This course covers the broad field of mergers, acquisitions, and divestitures. The primary objective of the course is for each student to gain a well-rounded understanding of the major strategic, economic, financial, and governance issues of mergers and acquisitions.

Takeovers and mergers are a daily fact of life and have evolved into a critical part of every CEO or manager’s strategic toolbox. Every person who enters the corporate world will most likely be affected by a merger or acquisition at some point in their career. Students will apply learned content to real mergers and acquisitions and have the opportunity to present to the class their findings and conclusions.

Specific academic course objectives include:

Examining the role that M&A plays in the contemporary corporate world, and its use as a strategic tool to provide growth, enhance competitive position, transform a company or industry, and create shareholder value.

To provide the student a framework for analyzing transactions including understanding strategic rationale, valuation methodologies, deal structures, bidding strategies, and the need for a value proposition.

Show how M&A can be used successfully as well as its pitfalls, dangers and risks. To identify ways to increase shareholder value through M&A and corporate restructuring.

The course will utilize a combination of lectures, readings, cases and student projects.

1

II. LEARNING OBJECTIVESThis course will help you to:

understand the role that M&A plays in the contemporary global market, and its use as a strategic tool to provide growth, enhance competitive position, transform a company or industry, and create shareholder value.

develop a framework that can be used for analyzing M&A transactions including understanding strategic rationale, valuation methodologies, deal structures, bidding strategies, and the need for a value proposition.

foster an understanding of the M&A process from target selection to doing the deal (including due diligence, integration planning, negotiating the agreement, announcing the deal), to closing and integration.

recognize the advantages and disadvantages of alternative deal structures. have an understanding of commonly used takeover tactics and defenses. choose a path for restructuring that will meet corporate goals and create shareholder value. understand the practical limitations of the various valuation approaches. minimize the risk that a merger or acquisition will not meet expectations. understand how value is created (or destroyed) as result of corporate mergers,

acquisitions, and restructuring transactions. understand the role played by corporate boards and third parties (consultants,

investment bankers, analysts, and institutional investors) in M&A deals

III. WHO SHOULD TAKE THIS COURSEThose who are seeking to become entrepreneurs, financial analysts, chief financial officers, operating managers, investment bankers, business brokers, portfolio managers, investors, corporate development managers, strategic planning managers, auditors, venture capitalists, business appraisers, consultants, or who simply have an interest in the subject.

IV. PREREQUISITE BUAD 215 or BUAD 306

V. REQUIRED MATERIALSRequired Text: Mergers, Acquisitions, and Other Restructuring Activities: An Integrated Approach to Process, Tools, Cases, and Solutions, 8th edition, Donald M. DePamphilis, Elsevier/Academic Press, San Diego, Ca., 2015 (ISBN: 9780128013908). For the textbook’s companion website, go to: http://booksite.elsevier.com/978 0123854872/section6.php Course packet containing cases is available at the HBS website. Use this link: https://cb.hbsp.harvard.edu/cbmp/access/43880679

Course Notes: Copies of lecture slides and other class information are available through your Blackboard account.

2

VI. TEACHING METHODS This course is taught through a combination of readings, cases, lectures and group projects. We begin each session with a discussion of current events. You are encouraged to read the Wall St. Journal and to visit dealbook.nytimes.com before each class to obtain a grasp of recent news.

VII. ABOUT THE INSTRUCTOR Lloyd Levitin is a Professor of Clinical Finance and Business Economics at Marshall. He was Executive Vice President and CFO of Pacific Enterprises from 1982-1995 (now Sempra Energy), and was actively involved in the firm’s diversification program which included numerous acquisitions. He testified as an expert on utility diversification to the Senate Finance Committee of the U.S. Congress and has been a consultant for JurEcon, Inc., a nationwide consulting and research firm for management and counsel. He has a MBA from Wharton and a JD from University of San Francisco. He practiced as a CPA after receiving his MBA, and as a tax attorney after receiving his JD.

VIII.GRADING SUMMARY:Points

Midterm 25Final Exam 30Team Project: Evaluation of a Recent Merger 25

Peer Evaluation 10

Class Participation 10

TOTAL 100

Final grades represent how you perform in the class relative to other students. Your grade will not be based on a mandated target, but on your performance. Three items are considered when assigning final grades:

1. Your average weighted score as a percentage of the available points for all assignments (the points you receive divided by the number of points possible).

2. The overall average percentage score within the class. 3. Your ranking among all students in the class.

Midterm and Final ExamThe midterm and final exam will be closed book, closed notes. The final exam is cumulative from the beginning of the course. Laptops or any hand-held device with email capabilities cannot be used. You should bring a calculator to perform calculations.

If you are unable to take a midterm, the following rules apply:

1. If you fail to inform me in writing before the midterm begins, you will receive a zero grade, even if you have a valid excuse. An exception will be made if you have a note from your doctor that you were unable to communicate your excuse.

2. If you inform me in writing before the midterm begins, and you have an acceptable excuse, then the final exam will count for 55% of your grade.

3

Team Project: Evaluation of a Recent Merger and Acquisition Deal

You are to evaluate a merger between two publicly-traded companies that took place between 2009-2013. This study should give you valuable perspectives on how deals are put together. Your group will prepare a paper on the acquisition selected and present your findings to the class.

This project is to be handed in to the instructor by April 12 and is worth 25 points (15 points for written report; 10 points for oral report to class).

An outline of the topics your paper should cover is stated on pages 9 and10:

Oral reports will be given during the period April 14-21. Your team will be notified of the date of your presentation by my TA by March 29.

The purpose of the oral presentation is to share with the class the highlights of your written report. Include the most important lessons you learned from this project. Use PowerPoint slides and plan to spend 20 minutes and then take questions for 5 minutes.

Groups for Team Project and Approval of Selected MergerStudents will divide themselves into “teams” of 4-8 students each by January 21 and select a team leader. Any student who cannot find a team should inform my TA by January 21 and the TA will assign you to a group. . The group team leader is to email the TA your first, second and third choice by February 4. The TA will inform you of your assigned acquisition by February 9.

Peer Evaluation on Group Projects (10% of your grade)Study groups provide a valuable learning experience – how to work effectively and efficiently in groups (a common practice in Corporate America), learning from others, and sharpening a student’s ability to communicate with others. However, human nature being what it is, some students are tempted to relax and let others carry their load. In order to provide an incentive for all students to make maximum contributions to the Pitch Book team project, students will be asked to grade each team member’s contributions on the Pitch Book project on a 1 to 10-point scale (10 representing the best performance).

This evaluation is to be submitted by email to the Instructor before the last day of classes. Any team member who does not email his (her) evaluation of team members will be deemed to have given a 10-point score to each member of the team.

Class Participation (10% of your grade). Attendance and participation are essential for success in this course.

You may earn up to 10 points for class participation. Each of you will be awarded these 10 points on the first day of class. Your objective will be to keep these 10 points throughout the semester. This requires attendance at classes and your participation in class discussion of the assigned cases.

Seven cases have been assigned, a copy of which is in the HBS course packet. These cases are listed on page 11.

4

Each student has an assignment to read the case and be prepared to discuss the case in class. These cases are not to be handed in. The issues and questions to be discussed in class for each case are itemized in the syllabus on pages 12 to 16.

To help me out, you should bring a name card and place it on the desk in front of you. After the enrollment in the course has stabilized, I will pass around a seating chart. At that point, I ask that you remain in that seat for the rest of the semester. This will help assure that class participation is accurately recorded and rewarded.

IX. ACADEMIC INTEGRITYUSC seeks to maintain an optimal learning environment. General principles of academic honesty include the concept of respect for the intellectual property of others, the expectation that individual work will be submitted unless otherwise allowed by an instructor, and the obligations both to protect one’s own academic work from misuse by others as well as to avoid using another’s work as one’s own. All students are expected to understand and abide by these principles. SCampus, the Student Guidebook, (www.usc.edu/scampus or http://scampus.usc.edu) contains the University Student Conduct Code (see University Governance, Section 11.00), while the recommended sanctions are located in Appendix A.

Students will be referred to the Office of Student Judicial Affairs and Community Standards for further review, should there be any suspicion of academic dishonesty. The Review process can be found at: http://www.usc.edu/student-affairs/SJACS/ . Failure to adhere to the academic conduct standards set forth by these guidelines and our programs will not be tolerated by the USC Marshall community and can lead to dismissal.

X. STUDENT DISABILITYAny student requesting academic accommodations based on a disability is required to register with Disability Services and Programs (DSP) each semester. A letter of verification for approved accommodations can be obtained from DSP. Please be sure the letter is delivered to be as early in the semester as possible. DSP is located in STU 301 and is open 8:30 AM to 5:00 PM, Monday through Friday. The phone number for DSP is (213) 740-0776. For more information visit www.usc.edu/disability.

XI. TECHNOLOGY POLICYLaptop and Internet usage is not permitted during academic or professional sessions unless otherwise stated by the professor. Use of other personal communication devices, such as cell phones, is considered unprofessional and is not permitted during academic or professional sessions. ANY e-devices (cell phones, PDAs, iPhones, Blackberries, other texting devices, laptops, iPods) must be completely turned off during class time. Videotaping faculty lectures is not permitted, due to copyright infringement regulations. Audiotaping may be permitted if approved by the professor. Use of any recorded material is reserved exclusively for USC students registered in this class.

XII. RETENTION OF GRADED COURSEWORKFinal exams and all other graded work which affected the course grade will be retained for one year after the end of the course if the graded work has not been returned to the student (i.e., if I returned a graded paper to you, it is your responsibility to file it, not mine).

5

XIII.CLASS NOTES POLICYNotes or recordings made by students based on a university class or lecture may only be made for purposes of individual or group study, or for other non-commercial purposes that reasonably arise from the student’s membership in the class or attendance at the university. This restriction also applies to any information distributed, disseminated or in any way displayed for use in relationship to the class, whether obtained in class, via email or otherwise on the Internet, or via any other medium. Actions in violation of this policy constitute a violation of the Student Conduct Code, and may subject an individual or entity to university discipline and/or legal proceedings.

XIV. EMERGENCY PREPAREDNESS/COURSE CONTINUITYIn case of a declared emergency if travel to campus is not feasible, USC executive leadership will announce an electronic way for instructors to teach students in their residence halls or homes using a combination of Blackboard, teleconferencing, and other technologies.

Please activate your course in Blackboard with access to the course syllabus. Whether or not you use Blackboard regularly, these preparations will be crucial in an emergency. USC's Blackboard learning management system and support information is available at blackboard.usc.edu.

XV. MARSHALL GUIDELINES

Learning Goals: In this class, emphasis will be placed on the USC Marshall School of Business learning goals as follows:

Goal DescriptionCourse Emphasis

1 Our graduates will understand types of markets and key business areas and their interaction to effectively manage different types of enterprises

Moderate

2 Our graduates will develop a global business perspective. They will understand how local, regional, and international markets, and economic, social and cultural issues impact business decisions so as to anticipate new opportunities in any marketplace

Moderate

3 Our graduates will demonstrate critical thinking skills so as to become future-oriented decision makers, problem solvers and innovators

High

4 Our graduates will develop people and leadership skills to promote their effectiveness as business managers and leaders.

Moderate

5 Our graduates will demonstrate ethical reasoning skills, understand social, civic, and professional responsibilities and aspire to add value to society

High

6 Our graduates will be effective communicators to facilitate information flow in organizational, social, and intercultural contexts.

Moderate

6

XVII. CLASS SCHEDULE AND ASSIGNMENTS: FBE 460SECTION DATE TOPIC ASSIGNMENTI. M&A Environment 1/12 Introduction

1/14 Regulatory Environment Text: Chapter 2 pgs, 52-69 and Case Study pg. 81

1/19 Corporate Takeover Market

Text: Chapter 3 and Case Study pg. 125

1/21 Case: C-1

II. M&A Process 1/26 Planning Text: Chapter 4 and Case Study pg. 166

1/28 Search Through Closing Text: Chapter 5 and Case Study pg. 201

2/2 Integration Text: Chapter 6 and Case Study pg. 232

2/4 Case: C-2

III. Valuation 2/9 Discounted Cash Flow Text: Chapter 7 and Case Study pg. 276

2/11 Market and Transaction Multiples

Text: Chapter 8 and Case Study pg. 312

2/16 Going PrivateTransactions and LBOs

Text: Chapter 10 and Case Study pg. 389

2/18 Text: Chapter 13 and Case Study pg. 501

2/23 MIDTERM

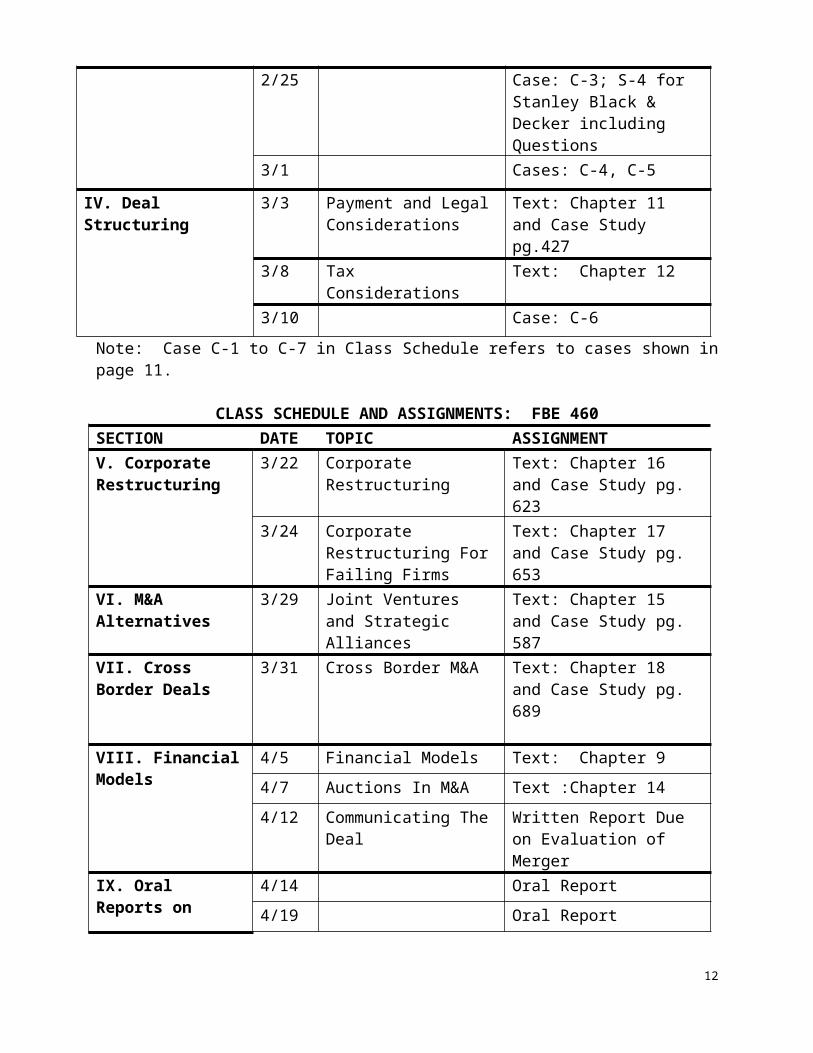

2/25 Case: C-3; S-4 for Stanley Black & Decker including Questions

3/1 Cases: C-4, C-5

IV. Deal Structuring 3/3 Payment and Legal Considerations

Text: Chapter 11 and Case Study pg.427

3/8 Tax Considerations Text: Chapter 12

3/10 Case: C-6

Note: Case C-1 to C-7 in Class Schedule refers to cases shown in page 11.

7

CLASS SCHEDULE AND ASSIGNMENTS: FBE 460SECTION DATE TOPIC ASSIGNMENTV. Corporate Restructuring

3/22 Corporate Restructuring Text: Chapter 16 and Case Study pg. 623

3/24 Corporate Restructuring For Failing Firms

Text: Chapter 17 and Case Study pg. 653

VI. M&A Alternatives

3/29 Joint Ventures and Strategic Alliances

Text: Chapter 15 and Case Study pg. 587

VII. Cross Border Deals

3/31 Cross Border M&A Text: Chapter 18 and Case Study pg. 689

VIII. Financial Models

4/5 Financial Models Text: Chapter 9

4/7 Auctions In M&A Text :Chapter 14

4/12 Communicating The Deal Written Report Due on Evaluation of Merger

IX. Oral Reports on Evaluating Merger

4/14 Oral Report

4/19 Oral Report

4/21 Oral Report

X. Review 4/26 Review Case C-7

4/28 Review - continued

Final Exam 5/5 2-4:00 PM

8

TOPICS TO BE COVERED IN WRITTEN REPORT ON EVALUATION OF A RECENT MERGER

A. ECONOMIC SETTING OF BUYER’S INDUSTRY

1. Important characteristics of the industry.2. Challenges faced by the industry at the time of the transaction.3. Industry trends, if applicable, prior to the transaction.4. Outlook for the industry over next 5-10 years as of time of transaction.

B. BUSINESS ECONOMIC REASONS FOR THE TRANSACTION

1. Reasons stated in SEC filings, annual report, and the deal announcement.2. Reasons stated in financial press.

C. STRATEGY

1. How did this particular transaction fit into the broad strategy of the acquiring firm? The selling firm?

2. Was the acquisition related or unrelated to buyer’s operations at time of deal?3. If related, explain how they are related.4. If unrelated, did this appear to occur because growth opportunities for the

buyer’s industry as a whole were not favorable or were opportunities lacking just for the individual firm studied?

D. TERMS OF THE TRANSACTION

1. How large was the premium paid to the target?2. How was the deal financed?

E. INITIAL REACTION TO DEAL

1. Stock market reaction for acquirer and target upon announcement of the deal 2. Security analyst reaction.3. Financial press (WSJ, Business Week, Forbes, etc.) reaction.

F. VALUE CREATION

1. How did buyer expect to create value?2. Describes sources of potential value creation.

G. DEAL HISTORY

1. What was the length of discussions between buyer and seller?2. Describe offers and counter-offers, changes in deal terms3. Describe other bidders (if any).

9Continued page 10

4. Describe defensive measures employed by seller either before or after the deal announcement.

5. Describe proxy fights, court battles, if any.6. Describe any deals made with regulatory authorities to gain approval of deal.

H. COMPARISON TO OTHER ACQUISITIONS OF BUYER

1. How did this acquisition compare to others, if any, made by buyer in previous 5 years with respect to size and premium paid?

2. Did this acquisition break the strategic pattern of usual transactions by the buyer?

I. IMPACT OF ACQUISITION ON BUYER

1. Initial impact of deal on buyer’s financial statements (e.g., changes in debt/capital ratio; EPS accretion or dilution).

2. Initial changes after the transaction due to acquisition (e.g., layoffs, divestitures, changes in seller’s management).

J. POST-MERGER PERFORMANCE (Up to 3 years after deal)

1. How did the economy and industry perform subsequent to the subject acquisition?

2. How did the firm perform at the merger measured by return to shareholders in subsequent years (capital gains plus dividend returns)

a. unadjusted?b. adjusted for a broad market index?c. adjusted for a market index for the industry?

3. How did the firm perform using accounting measures?

4. How do you think the firm would have performed absent the acquisition?

K. CONCLUSIONS

1. What was the outcome of this bad deal? Discuss in terms of:

a) Impact on market value (quantify)b) Financial stabilityc) Strategic positiond) Organization strengthe) Reputation

2. With the benefit of hindsight, did the acquiring firm make some mistakes in acquiring the target? Explain.

3. What were the most important lessons you learned from this project.

10

CASES IN COURSE PACKET

Case studies in Course Packet

C-1 Northrop versus TRW, HBS 9-903-115

C-2 Ben & Jerry’s Homemade, UV0273

C-3 Stanley Black & Decker, Inc; HBS 9-211-067

C-4 Acquisition of Consolidated Rail Corporation (A), 9-298-006

C-5 Acquisition of Consolidated Rail Corporation (B), 9-298-095

C-6 Proctor & Gamble’s Acquisition of Gillette – KEL183

C-7 American Cyanamid (A) and (B) Combined – HBS 9-898-120

SEC Filings Posted on Blackboard

S-4 Stanley Black & Decker Merger, 2010.

See pages 12-16 for questions to be prepared to discuss in class

11

Case C-1: Northrop versus TRW

1. As a member of TRW’s board, what action would you recommend?

Case C-2: Ben & Jerry’s Homemade

1. What decision does Morgan face?

2. How did Ben & Jerry’s become a takeover target?

3. What evidence is there that investors are dissatisfied?

4. What takeover defenses did Ben & Jerry’s have?

5. Should Morgan support a takeover offer?

Case C-3: Stanley Black & Decker, Inc.

1. What was the size of the acquisition premium?

2. If this were an all cash deal, what would be the NPV to Stanley’s shareholders?

3. In this case, with stock being used, what is the NPV to Stanley’s and B&D’s shareholders?

4. Why was this deal not done earlier?

5. Was Stanley really the acquirer?

6. Are the transaction incentives for the CEO’s fair to their shareholders?

7. What corporate governance and social issues are raised by this transaction?

12

QUESTIONS TO CONSIDER IN READING OF STANLEY BLACK & DECKER MERGER (2010)

1. What, specifically, are the shareholders being asked to vote upon?

2. What are the specific terms of the deal? In particular, who gets what? Pay attention to payments to shareholders, as well as side-payments to others (such as managers, financial advisors, etc.)

3. What is the argument in favor of this deal?

4. What are the “background risks” or uncertainties of the buyer or target?

5. What are the “transaction risks” of this deal? In other words, what could go wrong between now and the final consummation of this deal

6. On what questions will shareholders be asked to vote? Specifically, what does the ballot call for?

7. Who gets to vote on these questions? How many votes are needed to decide the questions?

8. When and where will the vote be held?

9. Who is soliciting my proxy? Management? Independent directors? Dissidents? What is their likely strategic purpose in seeking my support?

10. What is the selling shareholder’s tax exposure?

11. How will shareholders’ voting control of the firm be affected? Will some shareholder blocks dominate the voting in the new firm? How will the board of directors be composed?

12. Is there a “fairness opinion” about the terms of the deal? Who provided it? How was the fairness study conducted? What does the fairness opinion conclude?

13. What are the alternatives to this deal? Were other deals considered? If so, why were they rejected? If the majority of shareholders approves this deal and the minority does not want to accept the terms, do they have rights to seek an independent appraisal by a court?

14. What is the history of the deal? Is there evidence of objectivity, loyalty to shareholders, and care in the vetting of this deal?

15. What are the personal interests of directors and executives in this deal? What benefits will they receive if the merger is consummated?

16. What is the status of any litigation related to the deal? Could this litigation derail it? What is the legal form of this transaction? What does the choice imply about the tax exposure for the seller, and accounting dilution for the buyer?

13

17. Where will the target’s liabilities go? Will they be paid off? Will they go to the buyer? Or will they remain with the target (or outgoing) shareholders?

18. Upon what conditions is consummation of the deal dependent?

19. Under what circumstances can the deal be terminated without breaching the merger agreement? If the deal is terminated, are any special fees incurred? If terminated, who bears the expenses that have been incurred in the development of the deal?

20. Has this transaction been approved by the antitrust authorities?

21. Will critical licenses, patents, and leaseholds be conveyed to the new firm?

22. What have been the market prices for the target firm recently, and how does the bid compare to these prices?

23. Read the opinions of Stanley’s and Black & Decker’s Financial Advisors. Do these opinions satisfy you that the deal is fair to both parties? Or do they raise doubts in your mind?

24. What is the accounting treatment of the merger?

25. What effect will merger have upon dividend policy?

14

QUESTIONS ON CASES

Case C-4: Conrail (A) Case

1. Why does CSX want to buy Conrail?

2. How much should CSX be willing to pay for Conrail?

3. Why did CSX make a two-tiered offer?

4. What are the economic rationales for and takeover implications of the following provisions in the merger agreement:

a. No-talk clauseb. Lock-up optionsc. Break-up freed. Poison pill

5. As a Conrail shareholder would you tender your shares to CSX at $92.50 in the first stage offer?

Case C-5: Conrail (B) Case

1. Why did Norfolk Southern make a hostile bid for Conrail?

2. How much is Conrail worth to CSX? Norfolk Southern?

3. In a bidding war, who should be willing to pay more, Norfolk Southern or CSX?

15

QUESTIONS ON CASES

Case C-6: Proctor & Gamble’s Acquisition of Gillette (KEL183)

1. What were the potential synergies in P&G’s acquisition of Gillette?2. Discuss the positive and negative aspects of receiving shares or cash from the perspective

of P&G and Gillette shareholders.3. What are the possible reasons as to why P&G did not use a collar in the merger proposal?4. Compare the valuation analyses in Case Exhibits 6-9. Based on this analysis, determine

the bid range that you would recommend to P&G’s board of directors.5. Discuss the conflicts of interest for an investment bank in an M&A transaction.6. Discuss the possible impact politicians and regulators can have on an M&A deal.7. Evaluate the role played by Warren Buffet in the merger.

Case C-7: American Cyanamid (A) & (B) Combined (9-898-120)

1. Was AHP’s decision to bid for Cyanamid a good one for both firms’ shareholders? What evidence would you cite to support your case?

2. What are the potential sources for value creation, if any, in an AHP/Cyanamid merger?3. How did Cyanamid’s management respond to the AHP offer? Whose interests were they

taking into account? Whose interests should be taken into account when considering a takeover offer?

4. How can we explain the fact that American Cyanamid’s managers continue to express a preference for the SmithKline Beecham asset swap even after Perella’s analysis showed it to be a lower-valued alternative than the sale to AHP?

5. In your view, what per share value would the SmithKline asset swap have to generate to justify rebuffing the AHP offer? As a director, would you support management at a value of $85, which Ellberger suggests might have been sufficient to resist AHP?

6. Was MacAvoy’s assertion that he would go to the Wall Street Journal a reasonable response to his frustration with the boardroom processes? Why or why not, and from whose perspective? If you think it was a weak response, what would you suggest as an alternative?

7. What factors have contributed to boards of directors’ inability to govern publicly traded corporations effectively? Which, if any, of these materialize in the boardroom conflict at Cyanamid?

8. In a speech to MBA students at Northwestern, John Smale (former CEO of Proctor and Gamble and director of several Fortune 500 companies, including General Motors) stated: “Certainly the pursuit of optimum value for the shareholders is an important obligation of the corporation, but it should not be the primary obligation. The primary obligation of management and of a board of directors should be to the corporation and its successful continuation. Let me repeat that for emphasis. The primary obligation of management and of a board of directors should be the corporation and its successful continuation.”

Do you agree or disagree? Why? How is this statement relevant to the boardroom dynamics at Cyanamid?

16