philpapers.org · web viewi occasionally use the word . pet. to ... rethinking the legal...

TRANSCRIPT

2018 Apr 19

Companion Animal Intrinsic Value

Guardians of companion animals killed wrongfully in the U.S. historically receive compensatory judgments reflecting the animal’s economic value. As animals are property in torts law, an animal’s economic value is its fair market value (FMV), its value, as it were, to strangers. However, in light of the fact that guardians often value their companion animals at rates in excess of FMV, legislatures and courts have begun to recognize a second value, the animal’s value to its guardian, or its capital. Since guardians invest in their animals, when animals are killed guardians lose the opportunity to recoup their investments. In this paper, I argue for a third value, an animal’s intrinsic value, its value to itself, and I propose a method to determine it. The method assesses investments animals make in themselves expecting a return. The theory has legal implications for economic damages in wrongful companion animal death lawsuits and philosophical implications for proper assessment of the value of nonhuman animal life.

I. INTRODUCTIONII. COMPANION ANIMAL CAPITAL VALUEIII. COMPANION ANIMAL INTRINSIC VALUEIV. OBJECTIONS AND REBUTTALSV. CONCLUSION

1

I. INTRODUCTION

I propose and defend a novel legal concept, the intrinsic value of a companion animal’s life. Guardians of companion animals killed wrongfully in the U.S. currently may expect to receive compensatory judgments reflecting the animal’s economic value, the value of the animal life to humans. As the law classifies animals as property, an animal’s economic value is its fair market value (FMV), a value that may be null. However, two facts call into question the justice of this norm. First, guardians value their pets at rates exceeding FMV, as demonstrated by the amounts they spend on food, surgeries, training, and end-of-life veterinary care.1 Second, FMV assesses an animal’s value to strangers, thereby failing to capture the rich complexities of the guardian-pet relationship. Guardians sometimes sincerely claim to love their animals as much as their children; some claim to have suffered more from losing a dog than from losing a father.2 In light of these facts, many juries, state courts, and legislatures now also recognize an animal’s capital value.

A companion animal’s capital value is the amount its guardians have invested in their companion. When guardians of animals killed intentionally, maliciously, or recklessly demand compensation for lost opportunities to recoup their investments, awards increasingly exceed FMV. When Gabby, for example, died at a grooming business from being negligently exposed to extremely hot conditions, the New Jersey Superior Court acknowledged the dog had a “subjective value…to its owner” arising from “…their relationship and the length and strength of the owner’s attachment to the animal.”3 In another example, a Texas trial court awarded a woman $10,000 for the “loss of companionship” of her dog, Licorice.4

1 I occasionally use the word pet to refer to the companion animal recognizing that this term is controversial. However, I resist using owner to refer to the human guardian. I agree with an implication of a 2001 Rhode Island state legislative document that guardian is always the better word. R. Scott Nolen, After more than a decade, has pet guardianship changed anything?, JAVMA NEWS (2011), https://www.avma.org/News/JAVMANews/Pages/110401a.aspx (last visited Nov 27, 2017).2 Finlo Rohrer, How much can you mourn a pet?, BBC NEWS, 2010, http://news.bbc.co.uk/2/hi/uk_news/magazine/8454288.stm (last visited Oct 26, 2017).3 Harabes v. Barkery, Inc. No. 791 A.2d 1142, 1 (2001), https://www.animallaw.info/case/harabes-v-barkery-inc (last visited Aug 10, 2017).4 Petco Animal Supplies, Inc. v. Schuster, 144 S.W.3d 554, 1 (2004), https://scholar.google.com/scholar_case?case=3173788494839960216&q=Chavez+v.+Marten+Transport&hl=en&as_sdt=6,34&as_vis=1 (last visited Aug 10, 2017). The judgment was voided on appeal by a review panel that cited Heiligmann v. Rose 16 S.W. 931, 932, (1891), https://scholar.google.com/scholar_case?case=3173788494839960216&q=Chavez+v.+Marten+Transport&hl=en&as_sdt=6,34&as_vis=1 (last visited Aug 10, 2017), a nineteenth-century ruling in which the Texas Supreme Court said plaintiffs can only receive as compensation either the fair market value of the pet or a “special and pecuniary value to the owner” related to the animal’s services. Loss of companionship and affection were ruled not to be part of the animal’s special and pecuniary value because they were not services to the guardian.

2

In U.S. law, tort regimes are one of two applicable rules for determining monetary awards in wrongful death cases. The other set of rules originate in legislative bodies. For example, Tennessee law permits guardians of unlawfully killed pets to receive up to $5,000 in noneconomic damages to compensate guardians for the loss of “expected society, companionship, love and affection of the pet.”5 In Illinois law guardians may sue for damages for emotional distress and loss of companionship if a pet is intentionally or wantonly harmed. In a case testing that law, plaintiff was awarded $100,000 after their cat was killed in a veterinary clinic by an unattended visiting Rottweiler dog. The size of the award was revised downward on appeal, but the guardian’s claim that the cat’s true value was not captured by its FMV was allowed to stand.6

Juries and legislatures are justified in honoring a guardian’s lost investments in their pets, in part because guardians are deprived of hours of enjoyment and relaxation spent communing with their companions. But how is a jury to determine such awards? It is a difficult question. In Part I of this paper, I explain an economist’s answer.

The instrumental value of an animal—its value as a means to achieve human ends—however, does not exhaust the animal’s value. While many guardians keep animals to improve the guardian’s physical security, health, or emotional equilibrium, other guardians keep animals to improve the animals’ physical security, health, or emotional equilibrium. The latter are concerned about the well-being of the animal for the animal’s sake. These guardians desire that their nonhuman companions have good lives not primarily because a good dog life will bring salutary consequences for the guardian but, rather, because a good dog life will bring salutary consequences for the dog.

I’ll call this feature of an animal’s life its intrinsic value—the value of the animal’s life from its perspective.7 Now many will be skeptical about whether such a thing exists, and I will address this objection in Section II. For introductory purposes, notice the prima facie appeal of the idea. Intuitively, when one’s ten year-old Rottweiler has diabetes, major organ failure, and osteosarcoma, a painful bone tumor that is very difficult to treat, it is better for her to be put to sleep rather than to continue to suffer through additional months of pain. If that verdict seems right, as I think it should and as many pet guardians have affirmed when facing the circumstance, then it must be possible to take the animal’s perspective on the world. For that is what we must

5 Lauren M. Sirois, Recovering for the loss of a beloved pet: rethinking the legal classification of companion animals and the requirements for loss of companionship tort damages, 163 UNIVERSITY OF PENNSYLVANIA LAW REVIEW 1199 (2015).6 Marcella S. Roukas, Determining the Value of Companion Animals in Wrongful Harm or Death Claims: A Survey of U.S. Decisions and an Argument for the Authorization to Recover for Loss of Companionship in Such Cases, ANIMAL LEGAL & HISTORICAL CENTER (2007), https://www.animallaw.info/article/determining-value-companion-animals-wrongful-harm-or-death-claims-survey-us-decisions-and#_ftnref171.7 Intrinsic value is a complex and essentially contested concept. Cf. John O’Neill, The Varieties of Intrinsic Value, 75 THE MONIST 119–137 (1992); Michael J. Zimmerman, INTRINSIC VS. EXTRINSIC VALUE THE STANFORD ENCYCLOPEDIA OF PHILOSOPHY (Edward N. Zalta ed., Spring 2015 ed. 2015), https://plato.stanford.edu/archives/spr2015/entries/value-intrinsic-extrinsic/.

3

do to determine that euthanasia is better, all things considered, for the dog. Should a dog become incurably depressed, incontinent, in constant pain, and unable to drink or eat, its life may no longer be worth living for it. When the things that make an animal happy no longer interest her, when she is so sad and lethargic that every hour only seems to add to her burden, the question of euthanasia becomes urgent. Any minimally decent guardian will at least consider it. And a caring guardian will consider it—here is my point—from the animal’s perspective.

It seems clear enough that companion animals enjoy positive and suffer through negative experiences with their guardians. It does not take much imagination to see that they also have positive and negative experiences apart from their guardians, apart from any humans at all. They can enjoy solitary walks in the woods. Dogs in particular seem to enjoy the companionship of other dogs, preferring it even to the companionship of humans. If these animals have their own points of view, as they certainly seem to do, then wrongfully killing one of them involves harm even if the animal is being kept by a loutish guardian who does not care for the animal. Each animal is sentient, has a physical welfare, and is an emotional subject of a life. Each animal can be happy or sad, excited or bored; each can have its life go well or poorly.

So dogs have desires and aims that they pursue in common with their guardian, but they also have desires and aims that are independent of the guardian. This is the basis for the claim that animals make investments in themselves. They pay attention to challenges from which they can learn lessons. They concentrate their energies and focus their efforts on acquiring new skills and capacities. They set short-term goals for themselves and exercise self-control as they try to achieve them. As they do so, they are making investments in themselves. However, I recognize that this claim is controversial and, as I say, I will defend it below.

Let us assume for the moment that I am right, that wrongfully killed animals not only harm the guardian by denying the guardian the opportunity to recoup their investments in the animal. They also harm the animal by stealing from it the opportunity to recoup its investments in its mental and physical potentials. This is the pet’s intrinsic value. Some of this value is natural, and some of it is artificial. On the one hand, a dog’s natural intrinsic value reflects its innate self-investments, learned behaviors typical of its species. These behaviors the dog learns from and with conspecifics even if it has no guardian: self-grooming, foraging, playing with other conspecifics, having sex with them, parenting offspring, and so on. On the other hand, a dog’s artificial intrinsic value reflects self-investments it makes in cooperation with its human guardian: defending the apartment, hunting the ducks, guiding the blind, sniffing the contraband, catching the Frisbee, signaling the guardian’s imminent epileptic seizure, and so on.8

I will say more in Part II about the two components of intrinsic value and propose a method to determine monetary awards in wrongful death cases. However, as my procedure is built on top of an existing model of an animal’s capital value, I explain that model now.

II. COMPANION ANIMAL CAPITAL VALUE

8 Deborah J Dalziel et al., Seizure-alert dogs: a review and preliminary study, 12 EUROPEAN JOURNAL OF EPILEPSY 115–120 (2003).

4

Companion animal capital is Sebastien Gay’s phrase for the noneconomic value of an animal to its guardian, “the stock of competences, knowledge, personality attributes, and characteristics that comprises the companion animal’s ability to produce economic value for its owner.”9 This value usually increases after the animal and guardian have spent time together. “The owner invests emotionally and financially in her companion animal and, in return, the companion animal performs a special form of work for its owner…[offering] loyalty, enjoyment, company, and safety.”10

A court in Washington has acknowledged this value. In ANDERSON V. HAYLES, a jury awarded the plaintiff, Jim Anderson, $100,000 after his neighbor shot Chucky, Anderson’s 7 year-old English springer spaniel.11 Anderson, who adopted Chucky at 8 weeks, told the jury his dog had a vocabulary of 100 words, caught clay pigeons during target practice, and was an excellent swimmer. Anderson testified that he and the dog were inseparable, so close that Chucky suffered debilitating panic attacks were Anderson absent for long periods. The award primarily covered lawyer’s fees, but it included $10,500 for Chucky’s special skills as a hunting dog and retriever and $36,475 for Anderson’s emotional distress.12 “Chucky,” the court observed, “offered therapeutic, hedonic, and recreational value … made ‘coming home’ a more enriching experience … enhanced the value of Mr. Anderson’s relationships and built bonds to others.”13

Chucky’s case is precedent for a pet’s noneconomic value. However, the jury expressed a need for more objective guidance in determining the value of the award. To that matter I now turn.

Judicial bodies have a difficult time determining a wrongfully killed human’s non-economic value. If not completely arbitrary, awards are highly variable.14 The following factors are usually taken into account: “socioeconomic status, total assets, annual income, age, educational background, and so forth for both sides, the plaintiff’s level of pain and harm, the victim’s

9 Sebastien Gay, Companion Animal Capital, 17 ANIMAL LAW REVIEW (2011), http://papers.ssrn.com/abstract=2515864. Gay occasionally uses intrinsic value to refer to an animal’s capital value. I am at pains in this paper to resist this conflation. 10 Gay, supra note 9, p. 87.11 ANDERSON V. HAYLES, No. 14-2-51133-0, 1 (2016), https://www.courts.wa.gov/content/petitions/943893%20Amicus%20brief%20Animal%20Legal.pdf (last visited Feb 5, 2018).12 Erik Lacitis, Dog owner gets $100,000 settlement in shooting death of Chucky the spaniel, THE SEATTLE TIMES, August 13, 2016, http://www.seattletimes.com/life/pets/dog-owner-awarded-100000-settlement-in-shooting-death-of-spaniel/ (last visited Sep 5, 2017).13 ANDERSON V. HAYLES, supra note 11.14 Posner and Sunstein agree with David W. Leebron, Final Moments: Damages for Pain and Suffering Prior to Death, 64 N.Y.U. LAW REVIEW (1989) that awards for distress and loss of companionship in wrongful death cases “have a high degree of arbitrariness.” Eric A. Posner & Cass R. Sunstein, Dollars and Death, 72 THE UNIVERSITY OF CHICAGO LAW REVIEW 537–598 (2005). Mark Geistfeld, Placing a Price on Pain and Suffering: A Method for Helping Juries Determine Tort Damages for Nonmonetary Injuries, 83 CALIFORNIA LAW REVIEW (1995) also agrees.

5

negligence, the defendant’s repentance, and so on.” Nonetheless, “no formula exists for courts to determine the amount of pain and suffering damages” in wrongful death cases.15

Nor are instructions to juries helpful, because there are no judicial standards by which to measure mental pain and suffering. Instructions could hardly be helpful since, as the standard reference work on the issue, Jury Instructions on Damages in Tort Actions, puts it, “There are no objective guidelines by which you can measure the money equivalent of this element of injury; the only real measuring stick, if it can be so described, is your collective enlightened conscience.”16 Consequently, jurors are likely to be told only that the law permits them “… to award to plaintiff a sum that will reasonably compensate him for any past physical pain, as well as pain that is reasonably certain to be suffered in the future as a result of the defendant's wrongdoing.”17 As Chang observes, “Other than this, to date, there is no conventional wisdom or rules of thumb for quantifying pain and suffering. In practice, the plaintiff generally simply claims an amount and contends that it is just, with little supporting evidence.”18

It is a vexing problem, to determine the monetary sum of a dog’s capital value. But we find important direction from the methods used to value unjustly killed humans, in which cases we consider highly relevant the deceased persons’ investments in themselves. One way to estimate a deceased person’s self-investment is to predict their lost future income. The prediction will be based on the skills and achievements the deceased had made up until their demise. This is the reason for thinking survivors of victims who had made significant self-investments may be given larger awards than survivors of those with smaller self-investments. Self-investments vary. Some have devoted extensive time and energy to advanced education; others have taken considerable financial risks to embark on novel enterprises; others have foregone opportunities to make large sums of money in order to work for far lower compensation improving the lives of the dispossessed. When these lives are lost, we intuitively believe that their survivors are entitled to more money than survivors of others who may have mindlessly squandered their time or foolishly gambled away their resources. It is no surprise that juries find such considerations relevant to their decisions about compensatory awards to survivors.

How much is a human life worth? Survivors of victims of the 9/11 terrorist attacks on the Twin Towers were paid a minimum of $250,000, an average of $2.1 million, and a maximum of $7.1 million.19 Because of the finite nature of the pool of money available for awards and the project’s explicit avowal of a principle to try to lessen the gap between the awards due to the highest and

15 Yun-chien Chang et al., Pain and Suffering Damages in Wrongful Death Cases: An Empirical Study, 12 JOURNAL OF EMPIRICAL LEGAL STUDIES 128–160 (2015).16 GRAHAM DOUTHWAITE & RONALD W. EADES, JURY INSTRUCTIONS FOR PERSONAL INJURY AND TORT CASES: CURRENT SUPPLEMENTS (2nd ed. 1988) §6-17.17 Id.18 Chang et al., supra note 15.19 Posner and Sunstein, supra note 14. In the U.S., survivors of soldiers fallen in the line of duty are awarded a death gratuity payment of at least $100,000, but both the conditions of death and the final figure are highly variable and render it unsuitable for the kinds of evaluations I make here. Rod Powers, ACTIVE DUTY DEATH BENEFITS & ENTITLEMENTS - US MILITARY FAMILY MEMBERS, https://www.thebalance.com/active-duty-death-entitlements-3356940 (last visited Jan 8, 2018).

6

lowest earners, estimates of any victim’s annual future earnings were capped at $231,000 per year.20

Juries may consult work-life expectancy algorithms to determine the amount. These models take account of the fact that people enter and exit the workforce. Sometimes one goes months, or even years, without a job. And workers typically become more inactive as they age. Consequently, simply multiplying someone’s current salary by the number of years until their retirement while adjusting for raises generally overestimates their future earnings. For this reason, a more nuanced model using calculations made in 1985 (the time of the study) estimated that a man killed at 30 years of age earning $25,000 annually had a present value (in 1985) of expected total future earnings of $332,000.21

These methods are useful in determining the value of companion animals. As with humans, animals have a value likely to fluctuate over time. A trained, mature dog is likely to be more valuable than an untrained puppy. (The model to be explained may be used for any companion animal species, but I illustrate my points by referring to dogs for purposes of economy of expression.) Furthermore, an animal’s value is likely to taper off in its latter years as its physical infirmities render it incapable of providing the services it once provided even as they burden the guardian. To represent these changes in a dog’s capital over its lifetime, use t to represent the time at which the animal’s capital is assessed and it to represent the guardian’s annual investment in the animal at that time.

Prior to a guardian’s taking possession of a dog, a third party often has invested in the animal, including vaccines, food, and basic training lessons. Represent these as i0 . Recalling Chucky’s case, imagine that Anderson purchased the dog from an animal shelter. In that instance, Anderson might have incurred the following costs: an adoption fee of $310, $200 for neutering, $70 for a medical exam, $30 for a collar, $95 for a crate, $60 for a carrying crate, and $110 for a training course (estimates from the Humane Society22 and Weliver23). In this case, i0 = $875.24

Suppose Anderson faces $700 in recurring costs each year for (f) food, (m) medical care & license, (g) gifts, toys, treats, and (h) health status of the dog. Aggregate these costs under the following headings:

20 For an account of the principles used in deciding on 911 awards, see KENNETH R. FEINBERG, WHAT IS LIFE WORTH? THE UNPRECEDENTED EFFORT TO COMPENSATE THE VICTIMS OF 9/11 (1st ed ed. 2005). The future lost wages were subject to several adjustments, including reductions for the expenditures the deceased would have made.21 George C. Alter & William E. Becker, Estimating lost future earnings using the new worklife tables, MONTHLY LABOR REVIEW (1985).22 Adopt Your New Best Friend, THE HUMANE SOCIETY OF TACOMA AND PIERCE COUNTY (2013), http://www.thehumanesociety.org/adopt/ (last visited Sep 4, 2017).23 David Weliver, THE ANNUAL COST OF PET OWNERSHIP: CAN YOU AFFORD A PET? MONEY UNDER 30 (2016), https://www.moneyunder30.com/the-true-cost-of-pet-ownership (last visited Sep 4, 2017).24 These are probably conservative estimates. Costs would be twice as high were the guardian to pay a standard $1,500 fee for a purebred.

7

CF = the cost of foodCM = the cost of veterinary and medical care

Ct = the cost of all other investments (e.g., toys, bedding, grooming, etc.)

Using these notations, a guardian’s investment, it , on each day of the dog’s life will be determined as the sum of the guardian’s time spent training and tending to the animal’s health plus the actual costs of food and veterinary bills. Using a small-case t as the number of conscious hours a guardian spends with the dog in these activities, tM is the time a guardian invests in the dog’s medical care and tT is the time spent in training the dog.

Since dogs also provide services, a similar model may represent the current value of the dog’s “expected earnings.” Note, first, that hunting dogs, show dogs, guide dogs, and emotional support animals all provide their guardians with vital physical and psychological support as well as leisure and recreation. As demonstrated by loyal and agreeable dogs, animals can also serve as catalysts for community, conduits for guardians to get to know neighbors. Dogs can forge and strengthen social support networks.25 As acknowledged in ANDERSON V. HAYLES, Chucky “built bonds [for his guardian] to others.”

Furthermore, in the case of the wrongful death of children, some states also allow awards to compensate survivors for the lost “society” of the child and the corresponding “mental anguish” of the survivors. If Chucky played the role of a child to Anderson, Anderson might be entitled to compensation for harms called pecuniary losses. For example, the state of Ohio specifies that in the case of a lost child, the loss of their “society” includes

… loss of companionship, consortium, care, assistance, attention, protection, advice, guidance, counsel, …26

Dogs do not provide guardians with advice, guidance or counsel, but they often provide acceptance (companionship), commonality in pursuit of shared goals (consortium), solicitude (care), physical and psychological aid (assistance), concern (attention), and safety (protection).

How should the guardian of a wrongfully killed dog be compensated for these lost future services? Gay suggests we think of dogs as employees and of guardians as employers. In this thought experiment, guardians pay their dogs wages or, more accurately, “shadow-wages,” the marginal value of a unit of labor at the optimal point of a company’s production function. So the guardian might “pay” the dog for entertaining and protecting the guardian. And, since some dogs have more advanced skills than others, they may command, as it were, higher wages. For example, a woman might be willing to pay her purebred show dog more than she pays her yard 25 Phil Arkow, The Impact of Companion Animals on Social Capital and Community Violence: Setting Research, Policy and Program Agendas, 40 THE JOURNAL OF SOCIOLOGY & SOCIAL WELFARE (2013), http://scholarworks.wmich.edu/jssw/vol40/iss4/4; Lisa Wood et al., The Pet Factor - Companion Animals as a Conduit for Getting to Know People, Friendship Formation and Social Support, 10 PLOS ONE e0122085 (2015).26 THOMAS R. IRELAND & JOHN O. WARD, THE ESTATE OF A MINOR CHILD IN A CHILD DEATH CASE (2002), https://papers.ssrn.com/abstract=334560, citing Ohio Revised Code, n.d.)

8

dog. Along these same lines, she might not be willing to pay her lap dog as much as she pays her hunting dog if the latter provides her with a reliable, strenuous workout. To the extent that dogs have different valuations, as they do, our method should be sensitive to this fact.

Represent a dog’s shadow-wage as w t. Gay proposes the following formula to express the guardian’s recurring investments at t:

it = wt (tT + tM) + (CMt + CFt + C t)

We may illustrate the model by referring again to Chucky. Imagine that Anderson is willing to pay his dog up to $2 per day to entertain and comfort him plus another $5 per day for the dog’s role in persuading Anderson to walk twice a day. Under these assumptions, Chucky’s “wage” is $7/day. However, suppose Anderson thinks Chucky is not a sufficient guard dog (perhaps because he warms too readily to strangers), so Anderson must invest in a home security system at $10 per day. Now, had Anderson a larger, more menacing dog, he would not need the electronic security system. If he had, say, a German Shepherd, Anderson might “pay” the German Shepherd $2 for entertainment and $5 for exercise—the same amounts he pays Chucky--but he would save the money he now spends for security and could afford to pass along the savings to the bigger dog. Here the German Shepherd’s shadow-wage would be $17 ($2+$5+$10). However, we must now subtract the guardian’s relative costs for each dog, costs that also vary. Suppose a German Shepherd’s food and medical costs average $12/day whereas Chucky’s average $2/day. In this case, the cost-adjusted shadow-wage for each dog would be the same; $5 for the German Shepherd ($17-$12) and $5 for Chucky ($7-$2).

If we add the animal’s shadow wages and other recurring costs, it , to the initial fixed costs, i0 , we arrive at the guardian’s overall investment, or It :

I t=∑t=1

t

it +i0

For Chucky, since it= $700 and i0 = $875, then at the end of Chucky’s first year, I 1 = $1,575.

Typically, a companion animal’s value will rise over time. Let rt indicate the yearly interest rate to be used to compound the guardian’s investments from the time of the animal’s procurement until its death. The guardian need not have spent her money on the animal and, instead, could have earned money if she had invested the money spent on the animal in a risk-free bond. For example, were Anderson in Year 6 to decide that Chucky is no longer worth his investment, he could give Chucky away and put his funds instead into a risk-free bond returning, say, 3% annually. To represent a second interest rate, the rate used to compound lost opportunity costs, we use ρt .

To account for inflation, Gay provides the following calculation:

9

I t ≥∑t=0

a

( 11+rt )( 1

1+ρt )Ct

We must also take into account the guardians’ enjoyment of their dog. A guardian’s enjoyment will vary with the dog’s age, breed, and disposition. For example, guardians might spend 12 hours a day with puppies when they first come home and similarly with elderly dogs needing advanced care at the end of life. By contrast, they may spend but 2 hours a day with middle-aged dogs when the guardian is busy starting a career with a dog that needs only to be walked in the morning and evening. Similarly, the dog’s breed and disposition will affect the guardian’s enjoyment. If the dog is especially attentive and responsive, the guardian might derive more pleasure per hour spent with the dog than if the dog is inattentive and unresponsive. If the dog has made significant self-investments by learning, for example, to run obstacle courses or catch Frisbees at, say, a professional level, then the enjoyment of the guardian will correspondingly be higher.

Represent the guardian’s enjoyment of their companion as quality time spent with the animal (q). This variable will fluctuate relative to the guardian’s overall economic position. Wealthier guardians will, in principle, be able to spend more money on the activities they enjoy with their companion. To account for the effect of the guardian’s wealth on the value of the guardian’s time spent enjoying her relationship to her companion, let (Z) represent the guardian’s income.

Finally, we must take into account the characteristics of the animal that are beyond its control. These include the results of the genetic lottery (e.g. the individual animal’s markings, breed, conformation, and temperament) and the guardian’s disposition. Since pets are regarded by law as property, guardians have the option at any point to discontinue their relationship (e.g., giving the animal way or having it euthanized). Individual dogs will vary on this measurement, too. Gay defends this variable, Θ , as follows:

Owners generally choose the more costly option of continuing the relationship, unless there are extenuating circumstances such as the animal suffering extreme pain. Given that owners are rational, this phenomenon shows that there is a missing value in the owner’s cost-benefit analysis. The cost of keeping the animal alive is constantly in flux, based on the animal’s health, training, age, and appetite.

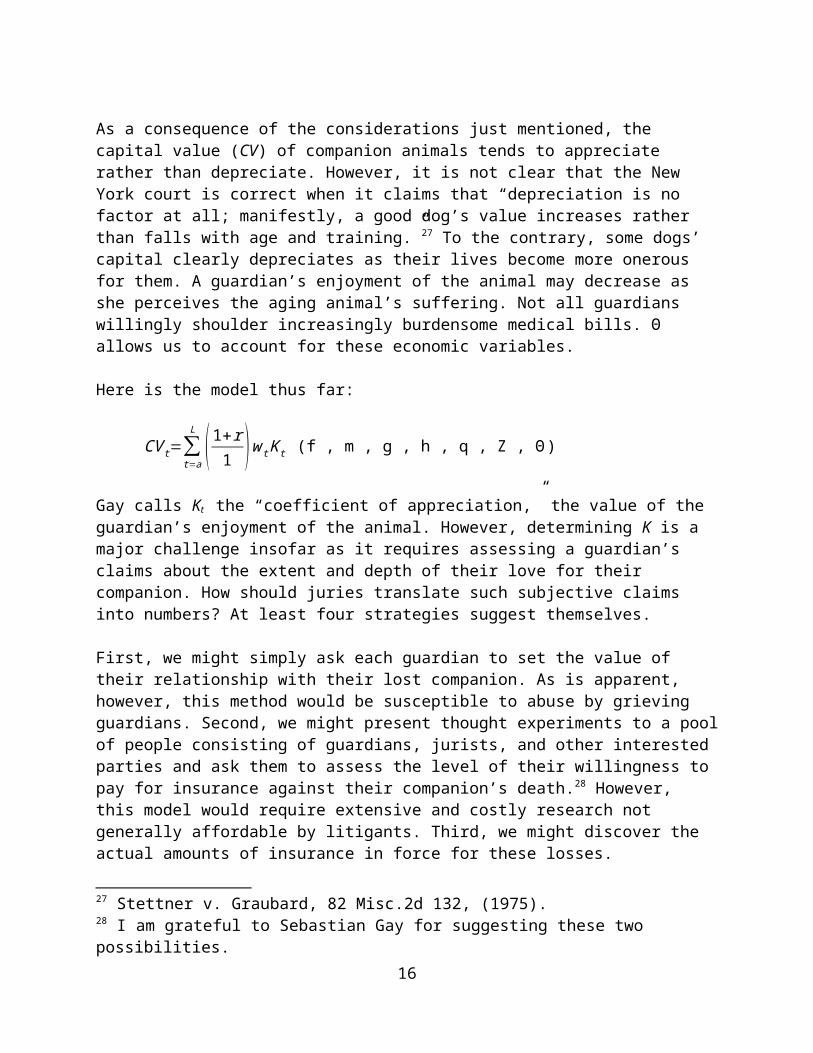

As a consequence of the considerations just mentioned, the capital value (CV) of companion animals tends to appreciate rather than depreciate. However, it is not clear that the New York court is correct when it claims that “depreciation is no factor at all; manifestly, a good dog’s value increases rather than falls

10

with age and training.”27 To the contrary, some dogs’ capital clearly depreciates as their lives become more onerous for them. A guardian’s enjoyment of the animal may decrease as she perceives the aging animal’s suffering. Not all guardians willingly shoulder increasingly burdensome medical bills. Θ allows us to account for these economic variables.

Here is the model thus far:

CV t=∑t=a

L

( 1+r1 )w t K t (f , m , g , h , q , Z , Θ )

Gay calls Kt the “coefficient of appreciation,” the value of the guardian’s enjoyment of the animal. However, determining K is a major challenge insofar as it requires assessing a guardian’s claims about the extent and depth of their love for their companion. How should juries translate such subjective claims into numbers? At least four strategies suggest themselves.

First, we might simply ask each guardian to set the value of their relationship with their lost companion. As is apparent, however, this method would be susceptible to abuse by grieving guardians. Second, we might present thought experiments to a pool of people consisting of guardians, jurists, and other interested parties and ask them to assess the level of their willingness to pay for insurance against their companion’s death.28 However, this model would require extensive and costly research not generally affordable by litigants. Third, we might discover the actual amounts of insurance in force for these losses. Unfortunately, to my knowledge this research has not been conducted and, therefore, results are not forthcoming.

A fourth method remains. Assume the coefficient of appreciation equals the amount of enjoyment the guardian has derived from the animal. This number, as noted, typically rises as the animal matures and falls as it approaches the end of life. Consequently, we should expect it to be at its highest when the animal’s powers are at their highest. But at its highest, K is unlikely to be more than an order of magnitude greater than it is at its beginning and end points. It is not unreasonable, then, to expect that the ratio of the guardian’s initial appreciation to the guardian’s highest appreciation will not exceed 10. Let us assume that this ratio will be in the 5 to 8 range.

Table 1 presents an estimate of Chucky’s projected capital value consistent with these assumptions. It shows that K is set at 1 in Year 1 and rises as high as 7 in Year 8, declining thereafter to 3 in Years 11-13.29 The value rises again in the dog’s last year as his natural death presumably occasions deep emotions for the guardian and a renewed appreciation of the animal.

27 Stettner v. Graubard, 82 Misc.2d 132, (1975).28 I am grateful to Sebastian Gay for suggesting these two possibilities. 29 Table 1 also appears to be consistent with Gay’s presumed values for K.

11

Year1 0 0 0 1 0 0 875 8752 1 150 10 2 1490 1810 875 26853 1 200 10 3 1505 2134.9 875 3009.94 8 100 10 3 1520 4159.9 875 5034.95 10 100 10 4 1535 5935.1 875 6810.16 12 150 10 5 1550 11150 875 120257 15 200 10 6 1566 20466 875 213418 15 200 10 7 1582 23632 875 245079 15 200 10 6 1597 20497 875 21372

10 15 150 10 5 1613 13613 875 1448811 15 100 10 3 1630 6579.6 875 7454.612 15 100 10 3 1646 6595.9 875 7470.913 10 100 10 3 1662 4962.3 875 5837.314 8 10 10 4 1679 2319 875 3194

wt tT tM Kt Ct it i0 It

1 2 3 4 5 6 7 8 9 10 11 12 13 140

5000

10000

15000

20000

25000

30000

Figure 1: Shape of Companion Animal Capital, Chucky

Table 1: Chucky’s Investment Value (It)

Given our assumptions, what conclusions should we reach about the amount due to Anderson? Two approaches seem reasonable. On the one hand, we could argue that the award should equal the dog’s It at the time it is killed. Since Chucky was killed at age 7, this answer sets the award at $21,341. Call this approach Flat Fee. On the other hand, the argument can be made that the award should compensate Anderson not simply for the amount Chucky was worth at year 7, but for all of Chucky’s lost future years as well. Since Anderson was deprived of Chucky’s presence from year 7 to year 14, this second method sets the award as the accumulated value of each of the years Chucky would have lived had he not been killed, or $105,665.30 Call this approach Cumulative. It determines Capital Value (CVt) as follows:

CV 7−14=∑7

14

I t

and includes all of the shaded area in Graph 1 to the right of year 7.

30 That is, 21341 + 24507 + . . . + 5837 + 3194 = 105,665.

12

1 2 3 4 5 6 7 8 9 10 11 12 13 140

5000

10000

15000

20000

25000

30000

Graph 1: Shape of Chucky’s Investment Value (It) in Dollars over Years

Which of these two answers is most defensible? Both seem reasonable. However, in light of two additional principles, the first is preferable.

Deterrence Awards must be high enough to deter future crimes.

Both methods satisfy this condition; awards in the lower range should be just as effective in deterring future crimes as awards in the higher range. The second principle is:

Order Awards must be low enough that they neither bankrupt the payer (thereby preventing payment of the penalty), make pet ownership excessively expensive (thereby making it impossible for average consumers to afford it), nor set the value of an animal’s life more than an order of magnitude less than a human’s life.

Only Flat Fee accords with Order. As the results found in Chucky’s case suggest, Flat Fee sets reasonable monetary awards in amounts not likely to overly inflate the costs of guardianship. As one study suggests (Green, 2004, p. 218), allowing emotional damages for a dog’s loss to run as high as $25,000 would increase a guardian’s annual veterinary costs by less than 13 cents and a veterinarian’s annual insurance premiums by less than $213, not unmanageable increases for either party. The second principle excludes Cumulative because $105,665 is of the same order of magnitude as $100,000, the US soldier death gratuity (see footnote 19). If we accept the two principles, as I think we should, Flat Fee is the best method to determine capital value.

To this point, I have followed Gay’s lead. However, the discussion omits a critical factor, to which I now turn.

13

III. COMPANION ANIMAL INTRINSIC VALUE

In this section I define intrinsic value; explain that it requires agency, self-investment, and prospection; defend the claim that dogs have these capacities; and explain a method to determine a companion animal’s intrinsic value.

Intrinsic value is often defined by contrasting it with what it is not. It is not instrumental value, the value of an object as the means to some end. To the contrary, intrinsic value is the value of something in itself, for itself, and to itself. Whereas some philosophers have ascribed intrinsic value to plants,31 most philosophers think only sentient animals can have intrinsic value because nonsentient living things, by definition, do not suffer. If something cannot feel pleasure or pain, it cannot feel its life going well or badly for it. If one cannot feel anything one cannot value anything. Whatever lacks the neural infrastructure necessary for sentience cannot value anything, much less itself.

Animals with sentience by definition have interests they want to fulfill; they want pleasure and do not want pain. These interests are the bases of their valuing their lives. To assess the intrinsic value of an animal’s experiences, we ask: What does the animal want—what does it desire, at what future state is it aiming? This question can be answered in the cases of cats and dogs, but not oak trees or ivy. For plants have things that are in their (biological) interests but not things in which they take a (psychological) interest.

Each human being has a unique set of interests consisting of their wants, desires, goals, and values. Each one of us, too, has a unique personal identity, an irreplaceable autobiographical consciousness consisting of our particular memories, capacities, skills, knowledge, and emotions. As we pursue our goals using our individual skills we produce value for ourselves. The literature of moral philosophy contains extensive debates about the intrinsic value of companion animals.32 However, to the best of my knowledge, there is no similarly robust discussion in the legal literature. The remainder of this paper is meant to begin remedying this deficiency.

Intrinsic value requires self-investment

31 NICHOLAS AGAR, LIFE’S INTRINSIC VALUE: SCIENCE, ETHICS, AND NATURE (2001). holds that all life has intrinsic value. GARY E VARNER, IN NATURE’S INTERESTS?: INTERESTS, ANIMAL RIGHTS, AND ENVIRONMENTAL ETHICS (1998) argued for a similar conclusion, but later gave it up.32 E.g. Brigid Brophy, The Rights of Animals, THE SUNDAY TIMES, October 10, 1965., Peter Singer PETER SINGER, ANIMAL LIBERATION (1975), R. G FREY, INTERESTS AND RIGHTS: THE CASE AGAINST ANIMALS (1980), TOM REGAN, THE CASE FOR ANIMAL RIGHTS (1983), Carl Cohen, The Case for the Use of Animals in Biomedical Research, 315 NEW ENGLAND JOURNAL OF MEDICINE 866–869 (1986); CARL COHEN & TOM REGAN, THE ANIMAL RIGHTS DEBATE (2001), and Christine M. Korsgaard, A Kantian Case for Animal Rights, in ANIMAL LAW – TIER UND RECHT. DEVELOPMENTS AND PERSPECTIVES IN THE 21ST CENTURY. ENTWICKLUNGEN UND PERSPEKTIVEN IM 21. JAHRHUNDERT 3–27 (Margot Michel, Daniela Kühne, & Julia Hänni eds., 2012), http://www.people.fas.harvard.edu/~korsgaar/CMK.Animal.Rights.pdf..

14

While philosophers disagree about the precise definition of intrinsic value, almost everyone agrees that it cannot exist apart, as I say, from a valuer. The life of a robotic dog may have value to a human, or a real dog, or some other valuer, but it does not have value for the robot. By contrast, a real dog’s life matters to it. The animal’s behavior implies that it is flourishing when its projects are succeeding, and it is languishing or becoming frustrated when they are failing. But can we be certain we are interpreting the behavioral clues correctly? How do we know that dogs value their lives?

This is a difficult question. We cannot get inside the dog’s head, as it were, and yet we do know, because we can see, that dogs have certain cognitive capacities. They remember. They taste. They see, they hear and, above all, they smell. They have personalities. They perceive things in their environments, react to them, form desires about what they want and hypotheses about how best to get it. If these claims are true, dogs are harmed when they are killed because their prospective desires are eliminated. They are deprived of the future they require to act on their beliefs and wants.

There are reasons to believe all of the claims are true. Begin, first, with perception and object permanence. Chucky could see things in the world and remember Anderson’s words for 100 objects. Chucky learned to retrieve specific items based on Anderson’s vocalizations. He saw, remembered, and responded appropriately to his guardian’s attempts to communicate with him.

Second, take desire. Chucky wanted to please his guardian, and believed he could achieve this goal by responding properly to commands to fetch this or that object. Third, take the formation of beliefs and hypotheses. Chucky’s personality was on the homebody side. He tended not to stray too far from his guardian. However, he loved to hunt and was occasionally torn between these two tendencies, wanting not to leave his guardian and wanting simultaneously to charge after a bird. So Chucky would formulate hypotheses. Not in English, or even in propositions, but in some way that made sense to him.

“I’ll hunt,” perhaps Chucky is thinking in his canine way, “but I won’t go too far from Mr. Anderson.” So he proposes to try to satisfy both desires. But then he sees a bird moving off rapidly while Mr. Anderson is moving in the opposite direction and he must quickly revisit his plan.

“Oh,” he thinks, “I’ll forego the hunting, then, and stay here for now.” How does he proceed if he then sees his guardian fall awkwardly into a ditch?

“Is he alright?” Chucky thinks in his Spaniel-ese. “I’ll meander over there and see if he needs help.”

We naturally, and appropriately, use the language of beliefs and desires to explain Chucky’s movements. There is no conclusive reason to think we are illegitimately anthropomorphizing when we do so.33 While we should not attribute to Chucky the grammatically correct English

33 Kristin Andrews, Beyond Anthropomorphism: Attributing Psychological Properties to Animals, in THE OXFORD HANDBOOK OF ANIMAL ETHICS 469–494 (Tom Beauchamp & R. G

15

sentences written above, neither should we hesitate to attribute to him something like the mental states represented by those sentences.

In fact, dogs act on hypotheses in pursuit of their desires all the time. For example, Chucky apparently learned the trajectory of clay pigeons and retrieved them quickly after Jim gave him the command. This is not an “innate” skill or something a dog has as an “instinct.” In Chucky’s case, his conscious interest in retrieving pigeons led to his death the day he was drawn onto a neighbor’s property as they were trap shooting. As Steven Wise observes, “the wrongful killing of one’s companion animal may threaten the way in which an owner constitutes herself: in losing her companion animal, she loses a vital part of herself.”34 When one’s animal is killed, the size of the loss to the human can be profound. However, the loss to the animal is complete. Deprived of its entire future, it no longer has desires and cannot strive to fulfill any of them. It cannot exercise its talents, develop new capacities or enjoy the pleasure of its human companions. Its intrinsic value is gone; the animal has lost all of itself.

Self-investment requires agency

To invest in oneself one needs a self. To have a self is to be an agent, to be in control of one’s choices. To be in control of one’s choices is to have the capacity to inhibit one’s short-term impulses so as to pursue one’s longer-term goals. We see a dog’s control—a dog’s agency—displayed in all sorts of ways and on all sorts of occasions, including but not limited to the implicit valuation dogs put on their lives when they fiercely resist attacks. However, behaviors in which dogs exhibit the value they place on their lives are not the only way they show their agency.

Dogs left in unfamiliar rooms with strangers will quickly move to their guardian’s side upon the guardian’s return, a fact that shows significant attachment to the guardian. However, the same dog will also move to the side of a complete stranger if the guardian does not soon return, a fact that shows that the dog’s values are dissociable from the guardian’s values. It also suggests that whereas a guardian may imagine their dog is exclusively bonded to them, the dog may not have the same opinion.35 Dogs have interests, desires, and attachments of their own.

Dogs have personalities that vary along many dimensions. They make choices based on their own set of preferences about matters such as whether to befriend or antagonize another conspecific, or an unfamiliar human. Dogs control themselves, learn to restrain their instincts to grab sandwiches off tables, learn to sit, to stay, to roll over, to come, to shake. In learning to cooperate with the guardian, the dog earns returns for the guardian on the guardian’s investments. However, it also earns returns on its own investments, its investments in itself. Much as kindergarteners earn returns on their investments when they develop similar,

Frey eds., 2011); Dale Jamieson, What do animals think?, in THE PHILOSOPHY OF ANIMAL MINDS 15–34 (Robert W Lurz ed., 2009).34 Steven M. Wise, Recovery of Common Law Damages for Emotional Distress, Loss of Society, and Loss of Companionship for the Wrongful Death of a Companion Animal, 4 Animal L. 33, 47 (1998)., 33 ANIMAL LAW (1998).35 Therese Rehn et al., I like my dog, does my dog like me?, 150 APPLIED ANIMAL BEHAVIOUR SCIENCE 65–73 (2014).

16

elementary-level, skills and capacities (“take turns and share, do what the teacher says, respect others’ personal space…”), dogs can be construed as investing in themselves without doing so intentionally. Dogs, like humans, exercise greater self-control when they are not stressed. Behavioral signs of stress include lip licking, yawning, circling, and increased levels of overall activity.36 Therapy and working dogs habitually face unpredictable situations that require that the animals “constantly adapt physiologically and behaviorally to maintain homeostasis.”37 Dogs, like humans, face similar impediments to self-control. The animals, like us, have greater success achieving their goals when they are not sucrose-depleted or worn out from prior exercises of self-restraint.38

Here are two kinds of evidence that suggest humans are agents. First, we have different personalities. Second, and corresponding in various ways to these different personalities, we have different levels of control of our impulses. If dogs are similarly agents, we would expect to find similar differences in personality and self-control. And we do. Dogs vary along at least three dimensions: their propensities to snap and attack, to threaten (stare, bark, bare the teeth, growl), or to cower (fearful behaviors such as fleeing, shrinking, tongue flicking, lifting front paw, squeaking).39 Dogs also vary in their ability to exercise executive control and inhibit their impulses. In reversal learning experiments, some dogs quickly learn new patterns while others seem bound by habit and perseverate with unsuccessful responses.

Agency requires prospection

Dogs have prospective agency even if they are not self-conscious. In the study of animal consciousness, Sphexishness is shorthand for unthinking scripted behavior.40 The word derives

36 Clara Palestrini et al., Stress level evaluation in a dog during animal-assisted therapy in pediatric surgery, 17 JOURNAL OF VETERINARY BEHAVIOR: CLINICAL APPLICATIONS AND RESEARCH 44–49 (2017).37 Ilia N. Karatsoreos & Bruce S. McEwen, Psychobiological allostasis: resistance, resilience and vulnerability, 15 TRENDS COGN. SCI. (REGUL. ED.) 576–584 (2011).38 William S. Robinson, CANINE SELF-CONTROL? YOUR BRAIN AND YOU (2010), http://yourbrainandyou.com/2010/11/07/canine-self-control/ (last visited Jun 21, 2015); Holly C. Miller et al., Self-Control Without a “Self”?, 21 PSYCHOLOGICAL SCIENCE 534–538 (2010); Suzanne C. Segerstrom & Lise Solberg Nes, Heart Rate Variability Reflects Self-Regulatory Strength, Effort, and Fatigue, 18 PSYCHOLOGICAL SCIENCE 275–281 (2007); Gary Comstock, La Mettrie’s Objection: Humans Act Like Animals, in THE MORAL RIGHTS OF ANIMALS 175–198 (Mylan Engel, Jr. & Gary Lynn Comstock eds., 2016); T W Belke, W D Pierce & R A Powell, Determinants of choice for pigeons and humans on concurrent-chains schedules of reinforcement., 52 J EXP ANAL BEHAV 97–109 (1989).39 L. van den Berg, M. B. H. Schilder & B. W. Knol, Behavior Genetics of Canine Aggression: Behavioral Phenotyping of Golden Retrievers by Means of an Aggression Test, 33 BEHAV GENET 469–483 (2003).40 Douglas R. Hofstadter, Can Creativity be Mechanized?, 247 SCIENTIFIC AMERICAN 18–34 (1982); DANIEL C. DENNETT, ELBOW ROOM: THE VARIETIES OF FREE WILL WORTH WANTING (First Edition ed. 1984).

17

from behavior of the Sphex, a wasp compelled to investigate the inside of its nest before dragging in its prey. The insect follows a series of algorithmic steps, beginning with a placement of its prey in a specific location outside its nest followed invariably by an investigation of the nest, a return to the prey, and then entry with the prey. If interrupted in these steps by, for example, an observer moving the position of the prey, the wasp goes back to the beginning of the procedure, replacing the prey in the spot and going back inside to investigate the nest. This happens no matter how many times the sphex has previously gone inside to look around.

Sphexishness holds a kind of fascination for interpreters seeking to explain animal behavior in terms of genetic determinism, automated responses to stimuli, or mere associative learning. However adequate these explanations may be for insects, however, they hide more than they reveal about the behavior of mammals, leaving all dog and cat behavior outside the realm of choice. Dogs are not sphexish robots with movements dictated by mechanical forces beyond their control. Rather, they are agents with the ability to learn new routines, form novel hypotheses to solve problems, and to initiate actions based on their decisions.

Prospection requires self-awareness, not self-consciousness

To be self-consciously prospective is to have the capacity to form propositional attitudes about one’s future goals, hypotheses, and successes. These propositional attitudes are available for recall and manipulation. For example, we are self-consciously prospective when we ask our partners whether we should buy an insurance policy. However, not all of our self-investments are conscious. Young children invest in themselves without knowing who they are or being able to say what their goals are. When a kindergartner persists in trying to tie her shoe she unconsciously invests in herself. When the first grader concentrates his mind on the novel word in front of him and tries to sound it out, he is investing in himself. To be prospectively self-aware is to exercise unconscious control over one’s bodily movements to achieve one’s ends.41 Nonconscious self-investments require that an agent have the capacity to perceive the world and learn from one’s mistakes. However, they do not require that these investments be accessible to or reportable by the subject.

It is unlikely that dogs form propositional attitudes about their interests and desires, have thoughts about revising their goals, or conceptualize themselves as temporally continuous subjects of a life. Nonetheless, these facts present no impediment to acknowledging the animal’s unconscious self-investments because dogs, like toddlers, invest in themselves whenever they act intentionally on a desire or want, whenever they try to achieve some end. In this way they are in the same position as a toddler. For example, 3 year-old Kylee is asked whether she needs to use the potty. Her inclination and practice is to respond unthinkingly “No!” so as to be able to keep playing with the puzzle. But she catches herself and tries to focus attention on her physiological state. She is still not interested in interrupting play, but she restrains the impulse to say “No,” wanting to obey mommy’s instructions. If she attempts to follow a rule she is strongly inclined to ignore, she unconsciously invests in herself. It is no strike against her if, afterwards, she is unable to report on the experience or articulate, even to herself in her toddler-ese, what she was

41 Christopher L. Suhler & Patricia S. Churchland, Control: conscious and otherwise, 13 TRENDS IN COGNITIVE SCIENCES 341–347 (2009).

18

attempting. For she was trying, at the time, to overcome her instincts and act on her longer-range plans.

A companion animal’s self-investments are, like a toddler’s, unconscious, implicit, and short-term. Nonetheless, they are occasions when the animal develops its basic capacities and skills, creating new possibilities for satisfying novel interests that, absent its self-investments, it would not possess. Simple nonconscious self-investments include meeting physiological needs such as eating, drinking, sleeping, mating, and finding a safe place to sleep. More complex companion animal interests, made possible by these simple self-investments, include meeting psychological needs such as recognizing and enjoying the individual personalities, affections, and talents of other conspecifics and humans. By working with their guardians to learn how to satisfy simple interests in the context of the norms of a specific household, dogs play an active role in creating opportunities for realizing returns on more advanced psychological self-investments in the confines, again, of their household’s norms.

Dogs are probably not self-conscious but they are self-aware

Dogs are not self-conscious, as far as we now know, but they are self-aware. They pay more attention to the scent of their own urine when a chemical has been added to it than they pay either to their unmodified urine or other dogs’ urine. This fact suggests that dogs know the by-products of their bodies and are able to connect the scent of their own urine with their own body.42

These claims are the basis for the idea, central to justifying the claim that dogs have intrinsic value, that nonhuman mammals can make investments in themselves. As Chucky acts on his desires and learns to overcome obstacles in the way of achieving them, he develops a distinctive personality. “Oh,” says Anderson, seeing his dog run to get his favorite toy before setting out on his walk, “that’s just Chucky’s way of doing things.” Unless this analysis is in error, aspects of Chucky’s identity and behavior are under Chucky’s control and at least some of his behaviors are achievements resulting from his labors.

Dogs have prospection

Every guardian who has trained a puppy to signal its need to go outside to defecate will be ready with examples of their animal’s self-investments. A Greyhound, for example, learns not to jump on its guardian’s lap when the guardian raises her eyebrow; it jumps into its guardian’s favored armchair when it wants to play; and it twists in delight in mid-air when catching a particularly well-thrown Frisbee or glances knowingly at its trainer after performing a difficult search and rescue mission. The dog is aware of its investments, too, as it shows when it develops its signature mid-air flip. The idiosyncracies of a dog’s personality endear it to its guardian and demonstrate the animal’s individuality and creativity, key components of self-investment.

42 Alexandra Horowitz, Smelling themselves: Dogs investigate their own odours longer when modified in an “olfactory mirror” test, 143 BEHAV. PROCESSES 17–24 (2017).

19

Dogs may change their behaviors in part to avoid punishment by others; human children also behave this way. But both individuals also learn to change their behaviors in pursuit of pleasures of their own.43 For example, Rufus, in training to become a Guide Dog for the blind, does not respond appropriately over time to his trainer’s instructions. Rufus sometimes demonstrates the required behavior, for example, moving in front of his companion when a stoplight turns red. However, Rufus acts quickly and seemingly impulsively, failing to display the gentle, calm spirit required of a seeing eye dog. Here, by failing to take an interest in performing the requested behaviors in the right way, that is, with the appropriate demeanor and attitude, Rufus fails to invest in himself. However, when his owner gives him a second chance as a sniffer-dog, Rufus succeeds, excelling at learning the nuanced skills and strategies required to find buried human corpses.44 Careful observation reveals that dogs take pleasure in learning new skills and respond, seemingly in pride, to handlers who praise them for performing novel maneuvers.

To deny Rufus credit for his skill acquisition would be unscientific as well as unfair. When a dog signals his guardian that the dog wants attention, the dog is exhibiting a unified mind focused on a particular objective. While the behaviors may be explicable in first-order terms, this possibility does not entail that the behaviors are not agential.45

Dogs are agents

These anecdotal observations have been confirmed experimentally by testing dogs with protocols called “Go-no-Go” and “A-not-B.” In Go-no-Go, dogs are first trained to nose a button when they hear a whistle (the “Go” sign). If they respond appropriately they receive a food reward. In the next phase of the trial they are presented with the following challenge. The experimenter raises their palm in a “stop” sign, a sign the dog has been trained to understand as a signal not to

43 We can be more precise about the claim that all self-investments are prospective. Tulving distinguishes “episodic” and “semantic” future thinking (ENDEL TULVING, ELEMENTS OF EPISODIC MEMORY, 1983). Episodic prospection is subjective thinking about the egoistic future and it contains events that are indexed to oneself (e.g., my trip to Portugal six days hence). On the other hand, semantic prospection is non-egoistic; it contains objective future events which involve no necessary reference to oneself (e.g., the Kenyan national election that, I read, will occur six days hence). Episodic future thinking involves behaviors indicating a desire to bring about some future state for myself. Bilateral activation of the hippocampus is involved in such thoughts, with the right side implicated in episodic prospection and the left side in semantic prospection Muireann Irish et al., Neural Substrates of Semantic Prospection – Evidence from the Dementias, 10 FRONT. BEHAV. NEUROSCI. (2016), https://www.frontiersin.org/articles/10.3389/fnbeh.2016.00096/full (last visited Jan 13, 2018). Cf. Richard D. Lane & Kateri McRae, Neural substrates of conscious emotional experience: A cognitive-neuroscientific perspective, in CONSCIOUSNESS, EMOTIONAL SELF-REGULATION, AND THE BRAIN (2004).44 CAT WARREN, WHAT THE DOG KNOWS : THE SCIENCE AND WONDER OF WORKING DOGS (First Touchstone hardcover edition. ed. 2013), https://catalog.lib.ncsu.edu/record/NCSU2812706.45 Gary Comstock & William A. Bauer, Getting It Together: Psychological Unity and Deflationary Accounts of Animal Metacognition, ACTA ANALYTICA (2018), https://www.readcube.com/articles/10.1007/s12136-018-0340-0 (last visited Jan 22, 2018).

20

move (“no Go”). After the signed “stop,” the “go” whistle sounds. Can the dog refrain from “acting on instinct” and refuse to act on its desire to touch the button? If so, it receives a food reward.

In A-not-B dogs see first a food reward hidden under one of three buckets, Bucket A, and they are permitted to nose the bucket and retrieve the treat. The food is left in Bucket A for three trials. In the next, so-called reversal, phase, they see the food hidden under bucket A but then immediately witness the experimenter remove the reward from A and place it in B. The animal’s challenge is to learn to inhibit its conditioned association of A with food and to choose instead the correct location, B. When 12 month-old human infants are presented with the reversal trial, they perseverate and look under the wrong bucket, Bucket A.46 However, by two years of age, typically developing infants have learned to inhibit that response and they look under bucket B. In the intervening year, infants display individual variances in their performances. Like 18 month-old babies, dogs display varying capacities to inhibit their responses in both Go-no-Go and A-not-B tests.47 Adult dogs generally succeed at Go-no-Go but often fail at A-not-B.48 Trying to explain these behaviors as “mere associations” or “learned instincts” need no more undermine the argument that dogs self-invest than a similar reductionist explanation of a human’s behavior need undermine the argument that we self-invest.49 What is sauce for the goose is sauce for the gander. Whatever reasons ground the belief that we should credit 18 month-old toddlers with achievements in developing themselves will also ground crediting dogs with achievements in developing themselves when the dogs exhibit behaviors similar to the toddlers’.

Dogs invest in themselves: neurobiology

We have ample behavioral evidence of dog self-investment, but is there any corroborating neuroanatomical evidence? Dogs are close models of human psychology and have emerged as one of the science community’s favored species for comparative research into cognitive control mechanisms. While a dog’s brain has marked dissimilarities from a human’s brain, including a less well-developed frontal lobe, other similarities are striking and some are extensive. A dog’s frontal cortices resemble human frontal cortices so closely that experimenters are mapping the dog’s neural control networks in the belief that these maps will assist efforts to map human neural control networks.

Brain scans of dogs successfully displaying inhibition show activation in the ventral frontal cortex, extending “rostrally and ventrally into proreal and orbital gyri.”50 Are these areas similar

46 József Topál et al., Infants’ perseverative search errors are induced by pragmatic misinterpretation, 321 SCIENCE 1831–1834 (2008).47 Peter F. Cook, Mark Spivak & Gregory Berns, Neurobehavioral evidence for individual differences in canine cognitive control: an awake fMRI study, 19 ANIM COGN 867–878 (2016).48 Zsófia Sümegi et al., Why do adult dogs (Canis familiaris) commit the A-not-B search error?, 128 J COMP PSYCHOL 21–30 (2014).49 Comstock, supra note 38.50 Cook, Spivak, and Berns, supra note 47.

21

to the human inferior frontal gyrus, the area active in us when we are successfully displaying inhibition?51 The jury is out, but there are reasons to think the answer may be affirmative.

We know that in dogs and humans the hippocampus is involved in episodic memory and episodic prospection. If similar neuroanatomical structures evolve in different species in response to similar environmental challenges, and if prospection brings fitness advantages to both humans and dogs, as it does, then the dog’s hippocampus is probably involved in their attempts to look ahead in time, too. In both species the frontocorticalstriatal circuits are active when one is trying to control an immediate impulse to act.52 In dogs, the proreal cortex is also implicated.53 The significance of this finding is that, as Cook et al. observe,54 the canine proreal cortex:

… includes granular layer IV55—a hallmark of primate prefrontal cortex56—and may be comparable to frontal regions supporting inhibition in humans and other primates, such as inferior frontal cortex.57 The ventrolateral pre-sylvian cortex has not been functionally defined in dogs, but tracing studies show it is connected with dorsal premotor regions,58 which, coupled with its proximity to frontal cortex, make it a likely candidate for an analog to human pre-supplementary motor area, also involved in inhibition.59

Similarities in function are also shown by ablation studies in which the structures in question have been damaged and the corresponding cognitive function is impaired. For example, when the orbital gyri in the lateral prefrontal cortex is extensively damaged in humans60 or dogs, 61 the individual loses the ability to inhibit responses. Furthermore, it is known that the same

51 Adam R. Aron, Trevor W. Robbins & Russell A. Poldrack, Inhibition and the right inferior frontal cortex: one decade on, 18 TRENDS IN COGNITIVE SCIENCES 177–185 (2014).52 Alicia Izquierdo & J. David Jentsch, Reversal learning as a measure of impulsive and compulsive behavior in addictions, 219 PSYCHOPHARMACOLOGY (BERL) 607–620 (2012).53 A. Kosmal, I. Stepniewska & G. Markow, Laminar organization of efferent connections of the prefrontal cortex in the dog, 43 ACTA NEUROBIOL EXP (WARS) 115–127 (1983).54 Cook, Spivak, and Berns, supra note 47.55 Duke Tanaka, Neostriatal projections from cytoarchitectonically defined gyri in the prefrontal cortex of the dog, 261 J. COMP. NEUROL. 48–73 (1987).56 Todd M. Preuss & Patricia S. Goldman-Rakic, Myelo- and cytoarchitecture of the granular frontal cortex and surrounding regions in the strepsirhine primate Galago and the anthropoid primate Macaca, 310 J. COMP. NEUROL. 429–474 (1991).57 Katya Rubia et al., Mapping Motor Inhibition: Conjunctive Brain Activations across Different Versions of Go/No-Go and Stop Tasks, 13 NEUROIMAGE 250–261 (2001); Adam R. Aron et al., Converging Evidence for a Fronto-Basal-Ganglia Network for Inhibitory Control of Action and Cognition, 27 J. NEUROSCI. 11860–11864 (2007); Aron, Robbins, and Poldrack, supra note 51.58 Kosmal, Stepniewska, and Markow, supra note 53.59 D. J. Sharp et al., Distinct frontal systems for response inhibition, attentional capture, and error processing, 107 PNAS 6106–6111 (2010).60 O. Godefroy, C. Lhullier & M. Rousseaux, Non-spatial attention disorders in patients with frontal or posterior brain damage, 119 ( Pt 1) BRAIN 191–202 (1996).61 J. Dabrowska & A. Szafrańska-Kosmal, Partial prefrontal lesions and go-no go symmetrically reinforced differentiation test in dogs, 32 ACTA NEUROBIOL EXP (WARS) 817–834 (1972).

22

neuropharmacological compounds, including but not limited to sugar and dopamine, play a role in self-control in both species and, in both species, disruptions in key metabolic functions cause difficulties in inhibiting aggression.62

We can be more specific about the human brain regions involved if we distinguish “episodic” and “semantic” thinking about the future.63 Episodic prospection is subjective thinking about the egoistic future and it contains events indexed to oneself indicating a desire to bring about some future state for myself (e.g., my trip to Portugal six days hence). On the other hand, semantic prospection is non-egoistic; it contains objective future events which involve no necessary reference to oneself (e.g., the Kenyan national election that, I read, will occur six days hence). The right side of the hippocampus is involved in human episodic prospection.64 We do not yet know whether the same is true for dogs.

Behavioral, neuroanatomical, and neurochemical evidence reveal critical similarities between dog and human executive control. Dogs can look ahead in time at least for a few seconds if not minutes.65 They are aware of their own bodies, capable of reversal learning, and able prospectively to inhibit their desires. They can control themselves, albeit un-selfconsciously, not only to get what they want but to change what they want in response to the changing affordances of their environment. They meet the conditions necessary to be able to invest in oneself.

Companion animal self-investment: definition

An investment is a prospective action, an intentional or unintentional act in which one entrusts something of personal value to another person or institution expecting a return. We invest in ourselves when we decide to go to college, or take out a loan to start a business, or buy a travel book to prepare for a trip abroad. These are conscious self-investments, and they require that one be able to learn from one’s mistakes. However, not all self-investments are conscious. Toddlers, I have argued, successfully invest in themselves when they inhibit their urges in conformity with norms.

Here, then, is a definition. Companion animal self-investment is a prospective act, conscious or unconscious, in which a companion animal aims at learning a novel skill in the expectation of a future return. The definition has the advantage of allowing us to make predictions about an animal’s intrinsic value. For example, we should predict that intrinsic value will vary according to each animal’s self-investments; that the self-investments will vary along with the animal’s age, species, and personality; and that animals with ambition and in the prime of their lives will have more intrinsic value than either puppies or elderly animals suffering dementia.

62 K Peremans et al., Estimates of regional cerebral blood flow and 5-HT2A receptor density in impulsive, aggressive dogs with 99mTc-ECD and 123I-5-I-R91150, 30 EUR J NUCL MED MOL I (2003).63 TULVING, supra note 43.64 Irish et al., supra note 43; Lane and McRae, supra note 43.65 Gary Comstock, Far-Persons, in ETHICAL AND POLITICAL APPROACHES TO NONHUMAN ANIMAL ISSUES 39–71 (Andrew Woodhall & Gabriel Garmendia da Trindade eds., 2017).

23

A model of companion animal intrinsic value

How can we determine the intrinsic value of a companion animal without adopting a method that is arbitrary or subjective? Here is a thought. Tie intrinsic value to capital value. In this way, we will avoid leaving the determination to the vague deliberations of unguided juries or the emotional appeals of legislative lobbyists. First, begin by establishing capital value using Gay’s method. Second, establish intrinsic value as a function of capital value. This procedure is transparent; recognizes that intrinsic and capital value are dissociable; and provides for the possibility that intrinsic value may be rising (if the dog is, say, spending pleasurable solitary hours hunting in the woods) as capital value is falling (if the guardian is, say, spending less time with him).

Two approaches are possible. The first approach uses a method akin to Gay’s shadow-wage schema. Define an animal’s self-investment at t as sit. This value will be determined as a function of the time the dog is engaged in guardian learning (glt ), educational and training activities with a human tutor, and in solitary learning (slt ), educational and training activities practiced by itself. Since the animal does not pay its own expenses for medical bills, food, and so on, we exclude CMt , CFt , and C t . Since investments made by others are not self-investments, we also exclude initial one-time fixed costs (i0). On this model, we imagine that the dog pays itself wages (wt ).

Call this approach Fine-grained. Its formula is:

sit = wt (glt + slt)

Whatever its merits, this approach is wrong-headed for two reasons.

First, it is nonsensical to think a dog could grasp the idea of paying itself for its own services. We can only estimate the dollar value humans put on their own time and work efforts because adult humans trade in the monetary ecosystem of exchanges. That is, we understand what money is and how it functions to replace the act of bartering goods for services. We grasp, some better than others, the possibility that a powerful person might use intimidation and obfuscation to corrupt negotiations and undermine the trust that is essential to exchange. By contrast, nonhuman animals do not—and presumably cannot—understand these concepts, much less engage in the prescribed practices. This is the first reason that Fine-grained is unworkable; it is not possible to make sense of the idea of a dog paying wages to anyone, much less itself.

Second, Fine-grained assumes we can make subtle judgments about animals’ mental states. How intently is the dog trying to learn a new trick? Is it worth $10 or $100 to the animal? Or $10 or $11? How would a dog even begin to make such judgments? It could not, and would not. Nor can we. This method requires us to set values in a way that is unjustifiable. As Aristotle noted, one should not aim at a level of scientific precision when one’s subject matter does not permit it. Fine-grained requires us to think we can apply the concept of a wage to situations in which a dog is negotiating with itself over how to spend its time. It also requires us to think the dog understands agreements, compensation, and power relations. Unfortunately, neither possibility is plausible; dogs have no access to fundamental economic ideas.

24

We must reject Fine-grained. It assumes what is plainly false, that nonhuman animals can deliberate about their value.

A second, more promising model, is available. This view, call it Coarse-grained, mimics a procedure followed in some human wrongful death cases and sets a flat rate for awards. Here, a dog’s intrinsic value is the median point between the lowest and highest capital values of all dogs similar in all relevant respects to the dog killed. This method is motivated by the need to recognize differences in dogs’ self-investments, by uncertainty about how to measure these differences, and by a commitment to fairness reflected in the desire to set a flat rate for all relevantly similar cases. Here is an illustration of how the method might work in practice.

Assume Chucky’s capital value at death is $21,341. Suppose there are 9 dogs in Chucky’s class, that is, dogs of Chucky’s age, breeding, training, personality, and disposition. Rank these individuals’ capital values in ascending order, from lowest (lct) to highest (hct). Assume further that four dogs have lower capital value than Chucky, and four higher. Since the number of animals in this set is odd, and the individuals {x1, x2, x3, … , xN} are rank ordered with N members, the intrinsic value (IV) of any given animal in the class at t will be:

IVt = xt(N+1)/2

In Coarse-grained, Chucky’s intrinsic value is the median value of the 9 dogs, that is, Chucky’s value, or $21,341. However, and this point is worth underscoring, the method sets the intrinsic value of the other 8 dogs—to include lct and hct –at $21,341 as well. But, given the differences among these dogs’ capital values, is this fair? One might think that the method underestimates hct, the dog with highest capital value, and overestimates the dog with lowest capital value. I resist this conclusion. When we try to estimate an animal’s intrinsic value, we should acknowledge that we are operating in murky territory. We should not try to be precise when we lack the information required to be precise. Coarse-grained honestly reflects the vagaries of our subject matter; to set one intrinsic value for the whole class of relevantly similar dogs is the best we can do. These are all points in favor of Coarse-grained. The method is open, its assumptions are clear, it reduces the subjectivity and uncertainty surrounding awards, and its results are available for debate and refinement. Choosing the median of the class rather than the mean also makes the method resistant to the skewing effects of outliers.

How do the results of Coarse-grained fair when compared to the results of methods used to make awards in human death cases? In its favor is the fact that it accords with the principle called Order above, that is, a presumption that the highest value of a companion animal should not be greater than an order of magnitude less than the lowest value of a person. The ratio between $250,000 (arguably the lowest value of human life in the US, as found in the settlements for 9/11 survivors) and $21,341—the Coarse-grained value of Chucky’s life—is roughly 10 : 1.66 This proportion is an argument in favor of Coarse-grained insofar as it preserves a

66 The highest valuations of human life approach $17 million Joseph Ax & Dan Whitcomb, O.J. Simpson Faces $58 Million Wrongful Death Damages After Release from Jail, INSURANCE JOURNAL (2017), http://www.insurancejournal.com/news/national/2017/07/21/458307.htm (last visited Oct 27, 2017).. The civil lawsuit finding OJ Simpson guilty of wrongful death of two people led to an award of more than $33.5 million, making each death worth about $17 million

25

difference between human and nonhuman valuations at not less than one order of magnitude. It guards against intrinsically valuing an animal more than a human.

Coarse-grained has two additional attractive features. First, it does not weaken a judgment’s deterrent effects by setting the award too low. Second, it minimizes the risk of making the defendant unable to pay restitution by setting the award too high. The model presents a reasonable, transparent, and enforceable method for determining companion animal intrinsic value.

IV. OBJECTIONS AND REBUTTALS

Before we take up specific objections to the approach, we must address two general worries.