glevenscc.files.wordpress.com€¦ · web view*promissory note with interest is known as an...

TRANSCRIPT

Business Math Chapter 5 Notes

Section 5 – 1: Promissory Note

Definitions

Promissory Note – written promise, or IOU, that you will repay the money to the lender on a certain date.

Interest – money paid for the privilege of using someone else’s money. *Promissory Note with Interest is known as an interest bearing note.

Collateral – pledging property as security for a loan. Ex: Car or stocks. *Home equity loans - Property is seized if a loan is not repaid.

Principal – the amount of money borrowed. The “face” of the note.

Rate of interest – interest shown as a percent.

Exact interest method – interest based on exact time and a 365 day year.

Ordinary interest method – interest based on a 360 day year with 30 days in each month. “bankers year”

Interest = P*R*T (Time is years for this example.)

Ex 1

Borrowed $2,500 with a 6 month promissory note at 11% interest.

A. Amount of Interest

I = (2500)*(.11)*(.5)

I = $137.50

B. Total Amount Due (maturity value)

2500 + 137.50 = $2,637.50

Exact Interest Method

Ex 2

Borrows $5,000 for 75 days at 8% exact interest.

A. How much interest?

I = 5000 * .08 * 75/365

I = 82.19

B. How much is due at maturity?

5000 + 82.19 = $5,082.19

Ordinary Interest

Ex 3

$4,000 borrowed at 9% ordinary interest for four months.

A. Interest

I = 4000 * .09 * 120/360

I = $120

B. Amount Due

$4,120

Rate of Interest R =I/P

Ex 4

Paid $320 interest on $8,000 that was borrowed for four months.

A Find rate of interest

12/4 = 3 periods

320 * 3 = 960 which is the interest for a year

R = 960/8000

R = 12%

Pg 175, 7 - 26

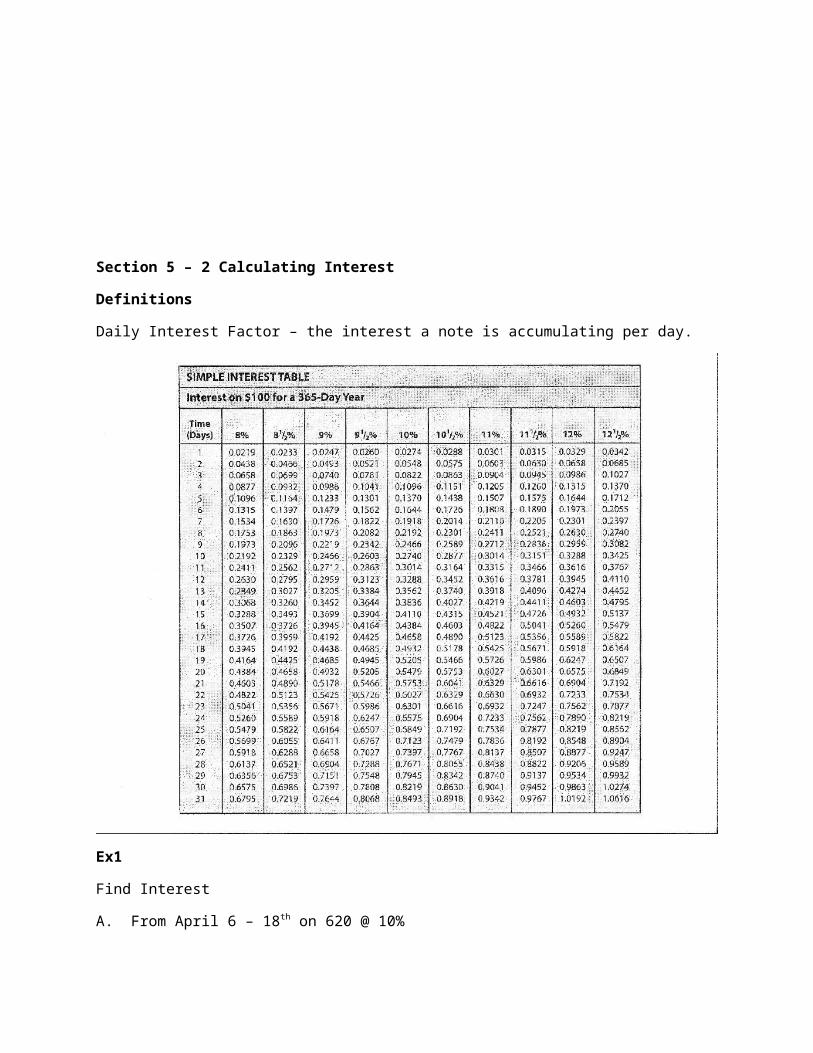

Section 5 – 2 Calculating Interest

Definitions

Daily Interest Factor – the interest a note is accumulating per day.

Ex1

Find Interest

A. From April 6 – 18th on 620 @ 10%

Days 18 – 6 = 12 days

620/1000 = 6.2 which is the number of $100 in principal

From table = 12 days, 10% * .3288

.3288 * 6.2 = $2.04

B. From Dec 7 to Dec 21 on $550 at 9%.

Days 21 – 7 = 14 days

550/100 = 5.5

Chart 14 days 9.5% = .3644

.3644 * 5.5 = $2.00

C. From May 8 – June 4 on $1,320 at 10%

Days: May 8 – May 31 = 23 days

June 1 – 4 = 4 days (Note: Count June 1st)

Total 27 days

1320/100 = 13.2

Table: 27 days, 10% = .7397

13.2 * .7397 = $32.76

Daily Interest Factor

Daily interest factor = Principal * rate/number of days in a year

Ex 2

Find daily interest factor for $600 at 18% exact interest

600 * .18/365 = $.2959

Ex 3

Find the ordinary interest for $750 at 9% ordinary interest from November 8 to November 22.

(Days = 14)

750 * .09/360 = $.1875

$.1875 * 14 = $2.63

Pg. 182, 11 – 34

Section 5 - 3 Installment Loan

Definitions

Down Payment – the part of a price that is paid at the time of buying on the installment plan.

Finance Charge – sum of interest and any other charge on an installment loan.

Installment Loan – a loan in which you repay the principal in installments.

Ex 1

Buy watch $125 cash OR Pay $25 down and balance in 12 monthly payments of $9?

A. What is the installment price?

25 + 12(9) = $133

B. What percent would installment price be higher?

133-125 = $8

8/125 = 6.4%

Ex 2

Westsuit costs $175 on installment plan. Must make down payment of $25. Payments are for 15 months.

A. Find monthly payment

175 – 25 = $150

150/15 = $10 per month

Installment Loans

Ex 3

Borrowed $1,000 on one year simple interest installment loan. 15% interest. Monthly payments = $90.26

A. Amount of interest paid first month

15/12 = 1.25%

I = 1000 * .0125 * 1 = $12.50

B. Amount applied to principal

90.26 – 12.50 = $77.76

C. New balance after month one

1000 – 77.76 = $922.24

Ex 4

$2,500 six month simple interest installment loan

18% interest

Monthly payments 438.81

A. First month interest

18/12 = 1.5%

2500 (.015)(1) = $37.50

B. First month amount applied to principal

438.81 – 37.50 = $401.31

C. Balance after month 1

2500 – 401.31 = $2,098.69

D. Second month interest

(2098.69)(.015)(1) = $31.48

E. Second month applied to principal

438.81 – 31.48 = $407.33

F. Balance after month 2

2098.69 – 407.33 = $1,691.36

Pg. 188 11 – 19, 21 - 28

Section 5 - 4 Early Loan Repayment

Definitions

Prepayment penalty – fee charged if you pay a loan off early. *Must be disclosed in original terms of loan.

*When paying a loan off early, you must pay the unpaid balance plus the current months interest (possibly a prepayment penalty.)

Ex 1

12 month, $2,000 simple interest loan. 9% interest. Repaid in full after 6 th payment when balance was $1,188.40.

A. Final payment

.09/12 = .0075

I = 1188.40 * .0075 = 8.91

1188.40 + 8.91 = $1,197.31

Ex 2

9 month, $3,000 installment loan. 15% interest. Repaid after 6 months with balance $1,374.82.

A. Final payment

.15/2 = .0125

I = .0125 *1374.82 = 17.19

1374.832 + 17.19 = $1,392.01

Ex 3

$5,000 loan at 6% interest. 24 months. Monthly payment = $221.60

A. If you make all of the monthly payments, how much is paid back.

221.60 * 24 = $5,318.40

B. After 12 months balance is $2,574.79 pay off with next payment.

Final payment

.06/12 = .005

I = 2574.79 * .005 – 12.87

2574.79 + 12.87 = $2,587.66

C. How much paid when paid off after the 12th month.

221.60 * 12 = 2659.20

2659.20 + 2587.66 = $5,246.86

D. How much saved

5318.40 – 5246.86 = $71.54

Pg. 194 7 – 14, 20

Section 5 - 5

Definitions

Annual percentage rate – cost of credit for one year. *Used to evaluate and compare loans.

Finance charge per $100 financed = Finance charge *100 Amount financed

Ex 1

Borrowed $800. Finance charge $78.

A. Find finance charge per $100 financed.

78/800 * 100 = $9.75

B. Find annual percentage rate if you were making 15 payments.

14 ¼%

Ex 2

Borrowed $250 with a 12 month loan period. The finance charge is $20.

A. Finance charge per $100

20/250 * 100 = $8

B. Find the annual percentage rate

14.5%

Ex 3

Borrow 1,600 with a 12 month loan. Monthly payment $145.

A. Finance charge

12(145) = 1740

Finance charge = 1740 – 1600 = $140

B. Finance charge per $100

140/1600 * 100 = $8.75

C. Annual percentage rate

15 ¾%

Pg. 198 11 – 26, 45