· web viewyou can also consolidate the exchange of multiple emails discussing the same topic...

TRANSCRIPT

Documentation Guide

Middle Market & Small Commercial Underwriting

January 2013

Table of ContentsOverview...............................................................................................................................................................................3

General Information..............................................................................................................................................................3

Additional Documentation Guidance – Middle Market........................................................................................................6

Additional Documentation Guidance – Small Commercial....................................................................................................7

Documentation Guidelines by Category................................................................................................................................9

Operations………................................................................................................................................................................9

Financials…………….............................................................................................................................................................9

Loss History/Analysis…………............................................................................................................................................10

Coverage/LOB Analysis………............................................................................................................................................11

General Liability...........................................................................................................................................................12

Inland Marine..............................................................................................................................................................13

Crime...........................................................................................................................................................................14

Automobile..................................................................................................................................................................14

Workers’ Compensation..............................................................................................................................................15

Umbrella......................................................................................................................................................................16

International................................................................................................................................................................16

Loss Control…………..........................................................................................................................................................16

Pricing…………...................................................................................................................................................................17

Terms & Conditions…………..............................................................................................................................................18

1

Correspondence……………................................................................................................................................................18

Premium Audit……………...................................................................................................................................................19

Reinsurance…………….......................................................................................................................................................19

Agency Analysis…………….................................................................................................................................................19

Overall Account Evaluation……………………….....................................................................................................................19

Underwriter Referrals/Clearance………………….................................................................................................................20

Rater Attachments…………................................................................................................................................................20

Appendix.............................................................................................................................................................................21

ARF Conversion Document..............................................................................................................................................21

At-a-Glance Documentation Job Aid – Small Commercial & Middle Market...................................................................21

UWW Requirments for Rater Documentation.................................................................................................................21

Examples of good account documentation.....................................................................................................................21

2

Underwriting Workstation – Documentation Guide

OverviewIn 2013 the Underwriting Workstation will replace the Account Review Form (ARF) providing enhanced flexibility for documentation and attachments, including the ability to drag and drop many types of attachments into your underwriting file. Additionally, the Underwriting Workstation has more prefill capabilities, account flag opportunities, aggregation of account and policy information and direct access to underwriting tools, resources and guidelines.

We now have a one stop depository for all your small commercial and middle market new business, renewals, and mid-term items. Therefore documentation within Underwriting Workstation not only includes your issued accounts, but also quoted and declined accounts as well.

With great flexibility comes great responsibility. This documentation guide has been created to outline what is expected of your underwriting files within the Underwriting Workstation. This guide is not intended to replace underwriting direction outlined for a specific line of business, segment or niche found on iBank, MM Portal, email correspondence, etc. You will still refer to those resources as appropriate.

General InformationIn order to establish a more concise and appropriately documented file, the underwriter needs to tell the underwriting story first from an account level and then for the specific lines of business that we insure. Make the assumption that another underwriter or underwriting technician may need to handle the account in your absence.

You need to identify and evaluate the risk’s exposures, special & common hazards and controls in place; explain your thought process as to the positions that you take; mention why you think the risk is good for us to insure. Comments should address if the risk fits our appetite, adequacy of pricing relative to exposures, prior loss experience and potential for loss, and specifics relative to terms and conditions. Commentary on material changes in exposure bases (e.g. payroll, sales, and/or property values) and how that impacts the risk and the selected pricing should also be included as applicable.

3

You also need to consider what should not be included as you document your files. Some guidance is outlined below, but this list is not all inclusive so use your best judgment when documenting your file.

Do not copy and paste content from loss control reports or websites into the workstation, instead make reference to the information and explain how this information guided you to the decisions or helped form your opinions on the terms and conditions for the risk.

Email correspondence may be copied into Underwriting Workstation, but in most cases that cannot stand on its own as documentation.

o As you receive a response to an email or more information within the same email thread, be sure you replace the existing email in the Underwriting Workstation (the original email will be saved in the Workstation’s history). You can also consolidate the exchange of multiple emails discussing the same topic into a Word document that is added as an attachment to the Underwriting Workstation.

Do not attach a physical copy of any Hit Memo, position paper or internal presentations describing our market appetite or underwriting guidelines.

Documentation in the Underwriting Workstation should be viewed as a fluid process that starts on the first day of the underwriting process when the underwriter and underwriting technician start gathering information and analyzing the risk. It should not be handled as a post renewal/issuance/quote/declination chore. As a best practice, documentation must be done as the account is underwritten and completed prior to policy issuance.

4

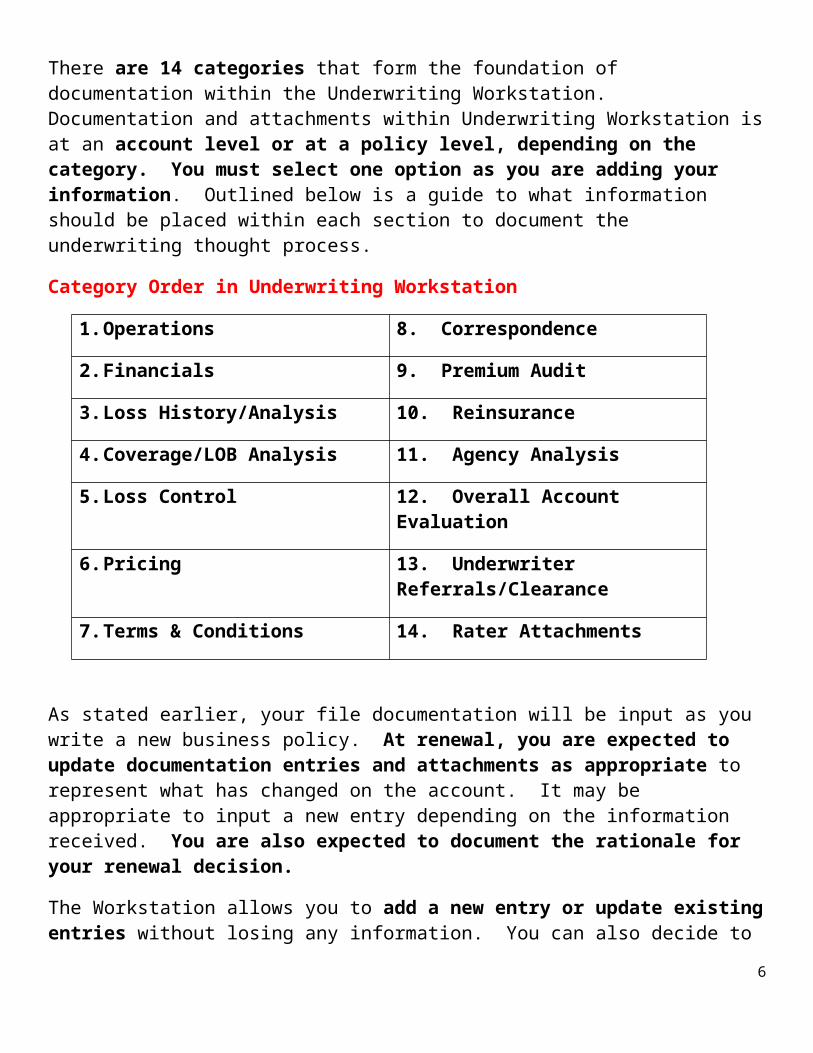

There are 14 categories that form the foundation of documentation within the Underwriting Workstation. Documentation and attachments within Underwriting Workstation is at an account level or at a policy level, depending on the category. You must select one option as you are adding your information. Outlined below is a guide to what information should be placed within each section to document the underwriting thought process.

Category Order in Underwriting Workstation

1. Operations 8. Correspondence

2. Financials 9. Premium Audit

3. Loss History/Analysis 10. Reinsurance

4. Coverage/LOB Analysis 11. Agency Analysis

5. Loss Control 12. Overall Account Evaluation

6. Pricing 13. Underwriter Referrals/Clearance

7. Terms & Conditions 14. Rater Attachments

As stated earlier, your file documentation will be input as you write a new business policy. At renewal, you are expected to update documentation entries and attachments as appropriate to represent what has changed on the account. It may be appropriate to input a new entry depending on the information received. You are also expected to document the rationale for your renewal decision.

The Workstation allows you to add a new entry or update existing entries without losing any information. You can also decide to hide entries that no longer apply and they are saved for you, but just not in the current view.

In the Appendix to this Documentation Guide, you will find best practices for naming your attachments. Following this guidance ensures that information will be easily retrieved with the search and filtering capabilities of the Workstation.

5

Additional Documentation Guidance – Middle MarketDocumentation should allow anyone reviewing a file to have a good understanding of the risk’s operations, the underwriter’s evaluation of management, financial condition, exposures and controls, and the underwriter’s rationale for accepting the risk.

Middle Market accounts should follow the guidelines within this document, with the exception of renewal accounts less than $50,000 premium. For those accounts, follow the bypass procedures documented in UT Best Practices: https://pci.allmerica.com/cl/workflows/ut/workflows_ut_chapters_02_renewal_prep.pdf

For every account, every category should contain documentation with the possible exceptions of Premium Audit, Reinsurance, Agency Analysis and Underwriter Referrals/Clearance where applicable. Depth will vary depending upon a number of factors including risk grade, exposures, special hazards and premium size. Documentation should be concise and clear to the reader.

6

Additional Documentation Guidance – Small CommercialDocumentation should allow anyone reviewing a file to have a good understanding of the risk’s operations and the underwriter’s evaluation of the account’s exposures and controls. As a best practice, documentation must be done as the account is underwritten and completed prior to policy issuance.

The less complex the account (e.g. lower risk grade & exposures), the less analysis and discussion needed; Accounts with higher risk grades, special hazards, loss issues and tougher products, exposures or operations deserve more in depth analysis and attention.

Types of Business Requiring Documentation:

New Business documentation in The Underwriting Workstation is required when one of the following conditions is met:

o Package, Auto and/or WC premium is $10,000 or greater;

o Account premium is $25,000+

o Risk Grade is 5 or higher

o Risk is over an Underwriter’s Authority

o An exception is made to an underwriting requirement (ie, private protection, waiving loss control recommendations, etc)

Note – When writing an Industry Segment meeting the above criteria, the segment risk profile tool and supplemental application (where available) must be completed and attached in the Operations Section of the Underwriting Workstation.

Most of our small commercial policies will have premiums less than the above thresholds. Ideally, the level of documentation for smaller premium policies should fit the complexity of the risk. Nevertheless, when an Underwriter handles a policy, The Underwriting Workstation must contain some level of thought process and analysis.

New Business referred to an Underwriter: documentation must include the reason for referral and thought process for acceptance. In addition, the underwriter must provide a brief overview in the Operations Section of the Underwriter Workstation of the insured’s operations, key exposures/controls, loss summary and website address (where available).

7

Renewal analysis should be done when a renewal is referred to an UW. The UW should evaluate whether the account has been profitable, exposures have changed and confirm that limits, terms, conditions and pricing are still adequate given exposures and controls. The appropriate renewal documentation is outlined in the New and Renewal Underwriting Best Practice Document (June 2011) located in iBank https://pci.allmerica.com/cl/ugdl/smcl/ugdl_smcl_new_renewal_uw_process_best_practice.doc

Midterm changes should be documented when there is a significant policy change such as a new location, change in operation, etc., in the appropriate section of the Underwriting Workstation.

8

Documentation Guidelines by Category

Operations Documentation level = Account

Describe the operations, management and ownership information for each named insured and match to a location on the policy. Be sure your analysis includes the following:

Years in business or prior management experience and form of ownership (such as corporation).

Evaluation of multiple Named Insureds with a match to a location and classification as applicable, including a discussion on whether any named insureds are nationally/internationally recognized companies/brands or discontinued operations as warranted.

Comment on exposure trends and insured’s customer base (payroll, sales, # of power units, property values) over the prior 3 years. If large increases or decreases exist, be sure to provide the rationale for the variances.

Management involvement and supervision of daily operations (versus absentee ownership).

Management’s actions to control exposures and promote safety.

Use of website and internet resources. Do the classifications on the policy match the descriptions on the website? Highlight discrepancies between multiple sources of internal and external information regarding exposures and controls described in the underwriting file.

Use of risk profile tools and supplemental applications. Remember to validate assigned NAICS and Group Code across all policies within the account.

Financials Documentation level = Account

The financial condition of a risk will impact the ability of a risk to invest in capital improvements, maintenance, and safety programs.

Credit Detail should be reviewed on all accounts. You will need to perform a deeper financial review if one or more of the following applies:

o Hanover Ranking is “Worse than Average” or “Much Worse than Average”;

o Paydex is below 70 and/or stress scores are 4/5;9

o Account premium is greater than $100,000;

o Any other information in the report that might suggest concerns with the insured’s financials (ie. liens, suits, judgments, history).

You can find more guidance to complete your financial review on iBank. https://pci.allmerica.com/cl/topic.asp?id=93&c=GUIDLN&v=CPP

Consider the following scenarios to determine if it is necessary to order a D&B report after reviewing the credit detail screen:

o There are multiple Named Insureds under one account or a DBA Name;

o There is no credit detail information available and you feel there should be a DBNI based on the Insured’s Operation and the length of time they have been in business, etc.;

o You need to perform a deeper financial review.

Attach any additional reports run within workstation and discuss your additional analysis.

Evaluate the direct bill payment history for evidence of legal notices or cancellation issues.

Loss History/Analysis Documentation level = Account

Both Frequency and Severity of loss should drive your loss analysis. While risks with prior losses are more likely to have losses in the future and claims may reveal uncontrolled exposures, even an account without claims has potential for loss.

Analyze premium and loss history (including paid, outstanding reserves, and defense expenses) for the last 5 years by account and line of business.

o Example of a frequency issue: You’re insuring a chain of retail auto parts store and the loss runs show a trend of high incident broken windshield and low impact rear end collisions. The agent states that the loss ratio is exceptional. This trend may indicate that the drivers are going too fast and that they eventually will be involved in a more serious accident if the behavior is ignored.

o Example of a severity loss: Your insured is a distributor of cooking appliances and three years ago they incurred a $1 million products claim due to a malfunction of a toaster oven resulting in fire damage to the customer’s property. The agent

10

indicates that the loss was not the insured’s fault since they were not the manufacturer. This may indicate that the insured is operating without proper risk transfer or engaging in direct importing. More analysis is required to understand the exposure and controls and additional loss history might be needed to fully evaluate the severity issues.

o Example of no losses: You’re quoting the GL coverage on a large real estate company that manages a group of 50 retail shopping malls in urban centers throughout the metropolitan area. Much to your surprise the loss runs show hardly any claims during the prior two years and the agent states that this is a great opportunity for you. After further investigation, you discover that the prior carrier’s insurance program included a $100,000 BI/PD deductible and the retained claims were not listed on the loss runs.

Discuss loss frequency trends indicating where they are occurring and what action was taken to reduce or prevent reoccurrence.

Discuss loss severity potential and what controls are in place to mitigate the exposure, even for those accounts with no past losses.

Explore large losses (e.g. $25,000 or higher) in order to find out details, cooperation of the insured, and if anything can be/has been done to improve the account.

On larger accounts, which are defined as $100,000 minimum account premium, evaluate whether you have enough loss frequency to consider trending and development of losses , and if performed, outline your analysis of the results.

Coverage/LOB Analysis Documentation level = MM Policy/LOB; SC Account

Property

Analyze and discuss the exposures to building, business personal property and business income.

COPE (Construction, Occupancy, Protection, Exposure) evaluation including a review of the year built for key structures and building updates, special (welding, cooking, flammables) hazards, common (housekeeping, electrical) hazards, and combustibility and susceptibility of personal property.

o ISO specific/tentative rates and Building Underwriting Reports (BUR) should be attached here.

11

Evaluating insurance-to-value (ITV) for buildings, business personal property and business income, which often require signed statements of value (SOV) and Business Income worksheets. MS Boeckh ITV calculation is required for every building greater than $1 million.

The Line Guide should be completed for every location with TIV greater than $1 million. Discussion here should include any locations where the amount subject exceeds the Final Maximum Retention provided by the Line Guide calculation and what you are recommending if still pursuing the risk.

Evaluation and documentation of what is considered one amount subject.

Identify and evaluate high value target commodities, including unique exposures and controls involving the perils of theft, employee dishonesty, inventory control and internal/external private protection.

Handling of catastrophe exposures (EQ, Flood, Wind, Hail, Wildfire & Terrorism), including identification and evaluation using Risk Meter, Google Earth, and various property tools to establish limits, retentions and to properly set policy construction.

Evaluate and comment on any unique coverage offerings.

General Liability

Analyze and discuss the exposures of the three major coverage sections of the GL form, (1) bodily injury and property damage, (2) personal and advertising injury, and (3) medical payments coverage as well as independent contractors and defense expenses. Depending on the coverage offered, the hazard level and terms & conditions of the exposures that you are evaluating, this section should include information on:

Premises/Operations Liability - evaluate exposures arising out of injury or damage due to the ownership, occupancy, or use of premises including off-site services performed by the insured.

Products/Completed Operations Liability - evaluate exposures arising out of injury or damage due to products sold or distributed by the insured including liability due to work completed by the insured including the end use of the product and direct importing exposures.

Personal & Advertising Injury - evaluate exposures arising out of slander, libel, use of another’s advertising idea and copyright infringement, and unlawful detention or

12

imprisonment. Are there any prior losses, and/or does an internet search show any past or recent litigation by or against the insured?

Professional Liability – evaluate exposures arising out of the failure of the insured to use the degree of skill expected of a person in their particular field and to perform those services in accordance with the appropriate standards of conduct. Comment on key responses to questions on supplemental applications.

Pollution Liability Coverage – whether covered or not, evaluate exposures arising out of any sites used by or for the insured for transportation, handling, storage, or treatment of waste, including above and/or below ground storage tanks. Document clearly what Pollution Exclusion you are using and why.

Independent Contractors/Subcontractors – evaluate the exposures arising out of the use of independent contractors/subcontractors by the insured, including what operations are subcontracted out, risk transfer measures in place and consistent use of the same subcontractors.

Describe the Risk Transfer in place, including Additional Insured status, Certificates of Insurance, Hold Harmless, and indemnification agreements. You can find more guidance to complete your review on iBank. https://pci.allmerica.com/cl/topic.asp?id=159&c=GUIDLN&v=GL

Discuss exposures and controls involving Miscellaneous Liability Coverage forms and endorsements, such as “Abuse & Molestation”, “Directors & Officers Liability”, “Liquor Liability”, “Employment Practices Liability”, “Owners-Contractors Professional”, Railroad Protective”, “Discontinued Products”, etc. This would include comments on responses to key questions on supplemental applications and also recognition of the need to be judicious with our inclusion of high limits and offering sub limits where required.

Inland Marine

The key information to document in this section includes the following:

Evaluate the largest value per item and also the total limit on scheduled or unscheduled floater forms;

Identify and evaluate high value target commodities, including unique exposures and controls involving the perils of theft, employee dishonesty, inventory control and internal/external private protection;

13

Evaluate COPE on inland marine coverage located at a fixed location;

Evaluate the Flood and Earthquake exposure, since most Inland Marine forms include flood and earthquake as covered perils;

Validate that the TIV of inland marine coverage is contemplated within the TIV of your standard property coverage forms and amount subject/line setting if at a fixed location.

Additionally, most Inland Marine forms are added manually to our policies. Since they are fill-in/variable forms, you must provide a completed form along with your issuance instructions to rating. You can find more guidance regarding Inland Marine forms and the Inland Marine Workbook on iBank. https://pci.allmerica.com/cl/topic.asp?id=815&c=GUIDLN&v=CPP

Crime

Analyze the major crime coverage forms: (1) employee dishonesty, (2) forgery or alteration, (3) money & securities, and (4) computer fraud. Your analysis should include:

What are the accounting controls to keep track of cash flows and to detect any improprieties or manipulation of a firm’s records and does the insured practice strong separation of duties;

Does the insured allow active access to target commodities, or do they limit access to a limited number of key employees;

Is there a diligent personnel screening processing to help prevent crime losses?

Automobile

Discuss exposures arising out of the ownership, maintenance, or use of covered autos including evaluating any concentration of values relative to the physical damage coverage. Identify how the vehicles are being used and who is driving all vehicles.

Evaluate the vehicles for use, radius, and size, including commodities transported. Make sure that the vehicles are properly classified based on the exposures identified.

Analyze the Hired and Non-owned auto exposures and controls for acceptability.

Consider the family use and personal use exposures and controls and acceptability relative to the established underwriting guidelines found on iBank https://pci.allmerica.com/cl/udoc/mvr/udoc_mvr_auto_2011.doc.

14

Include Policy Driver Multiplier (PDM) when using CAPE Auto, MVR summary, MVRs, existence of excluded or marginal drivers, and driver-to-vehicle ratios. Analyze the driver turnover and any exceptions to the MVR/Driver Underwriting Guidelines as outlined on iBank at https://pci.allmerica.com/cl/udoc/mvr/udoc_mvr_auto_2011.doc.

Existence of driver and fleet safety programs (when > 20 power units), driver training, accident investigation procedures, vehicle maintenance programs, driver selection process and driver monitoring process.

Indicate if there are state or federal filings (such as BMC-91X, MCS-90, Form E), explain why they are needed and review www.safersys.org (DOT website) for any concerns. More information on Auto filings can be found in iBank at https://pci.allmerica.com/cl/topic.asp?id=475&c=GUIDLN&v=AUTO.

Specify the handling of UM/UIM limits and signed rejection forms where applicable.

Inclusion of elective endorsements (if any) such as Drive Other Car, Garage Keeper’s Legal Liability, Designated Insured, etc.

Workers’ Compensation

The key information to document in this section includes:

The WC Risk Selection Tool for WC policies at the following thresholds:

o Middle Market: > $25,000

o Small Commercial: > $15,000 New Business only

Prompt reporting of claims, safety programs, accident investigation, medical management, return-to-work and drug screening programs.

Describe control of exposures including fall prevention, machine guarding, material handling, lock out tag out, height, and defensive driving.

Use of deductibles and/or dividend plans to include overall impact upon profitability.

Exposures covered by elective endorsements (if any) such as USL&H, Industrial Aircraft, and Voluntary Foreign Coverage endorsements.

Umbrella

Discuss potential catastrophe losses that the risk exposes us to.15

Comment on exclusionary and/or limiting endorsements that were included and our coverage intent. Validate that terms and conditions on the umbrella match the underlying policies.

Discuss other insurance carrier information if included in our underlying schedule, especially the auto line since the majority of umbrella losses involve auto liability claims.

International

Comment on your analysis of exposures and controls for any international exposures on both an admitted and nonadmitted basis, as appropriate. Follow the guidance above by line of business (ie. COPE, ITV, drivers, etc.) for documentation requirements depending on what international coverage you are placing and label it with the appropriate policy/lob as well. Begin any international specific documentation entry with the word “International” so it is easy to retrieve later.

Loss Control Documentation level = Account

Loss control surveys are used to validate risk quality, help insureds reduce likelihood of losses, and to demonstrate our value added service capabilities to both our agent and insured. The file documentation should include:

What locations were surveyed (and what locations were waived) and when. Utilize the current loss control ordering guidelines https://pci.allmerica.com/cl/ugdl/loss/ugdl_loss_control_ordering_guidelines_mm.xls;

Location grading, either “satisfactory,” “unsatisfactory until completed”, or “unsatisfactory” and if unsatisfactory or unsatisfactory until completed what is being done to address (and referrals where required);

o Red flags from vendor surveys and what is being done to address (and referrals where required);

Comment on which locations have unresolved essential recommendations and what actions are planned to secure compliance or bring to a satisfactory conclusion. If essential recommendations are waived, approval documentation from the CUO and LC Director must be included.

Pricing Documentation level = MM Policy/LOB; SC Account

The section should be used to discuss overall line of business and account pricing.

16

All Lines – Emphasize adequate rate-to-exposure using various underwriting tools and rating options. Generally, the pricing section should indicate how your recommended pricing will help us produce an underwriting profit. Include the following in this section (where applicable):

o IRPM/schedule modifications,

o Commission reduction,

o Company tier selection (where applicable),

Property/Liability/Package https://pci.allmerica.com/cl/udoc/standards/udoc_standards_ca_wa_ny_company_selection_criteria_tool.xls

Auto (CAPE only) https://pci.allmerica.com/cl/prc/auto/prc_avenues_tiers_101-105_uw_criteria.xls

Workers’ Comp https://pci.allmerica.com/cl/ugdl/wc/ugdl_wc_ca_company_selection_criteria_tool_eff_7-1-11.xls

o New Jersey De-Regulation https://pci.allmerica.com/src/cl/prc/rating_wksht/auto/prc_ratingwksht_auto_NJ_DeregulationTool_11766.xls

o New York Free Trade Zone https://pci.allmerica.com/cl/ugdl/process_procedures/ugdl_policies_procedures_ny_free_trade_zone.pdf

o The Renewal Comparison Worksheet (RCW) should be included in this section of the Underwriting Workstation.

Property – Average rate per $100 of exposure for your Building, Contents & BI/EE; Indicate rating methodology such as class, specific, tentative, or COP. Indicate, where applicable, guidance from minimum rate tool.

General Liability – For classes that are “A” rated, comment on use of “A” rate worksheet, and/or how the rate was established. Use of experience rating, other filed credits and/or rule 34 should be referenced in the file.

Inland Marine – Inland Marine pricing depends on whether you are using “filed” or “non-filed” forms:

17

o There are published loss costs for the filed forms with the same schedule rating plans that can be used with the property line.

o The non-filed forms follow judgment rating plans based on the individual characteristics of the insured risk. There are suggested pricing guidelines found in the AAIS manual.

Crime – The pricing should be based on your analysis of exposure and controls.

Automobile – For new business, if using the legacy companies instead of the Avenues Auto (CAPE) product, comment on the reason why. When using composite rating, indicate how the per unit rate compares to both the listed state average and test rating samples.

Workers’ Compensation – Indicate recommendation of WC Risk Selection Tool and adherence to the state specific pricing grid based on risk grade and state ranking.

International – Pricing calculations for the nonadmitted coverages should be included in this section and labeled with the appropriate policy/lob as well.

Terms & Conditions Documentation level = Account

Document all unique terms and conditions, endorsements, etc by line of business. In this section you should attach proposals, manuscript wording (indicating who granted approval), form lists, issuance instructions, and anything related thereto. If we are excluding a material exposure of the insured, document how the exposure is to be covered elsewhere, including obtaining a copy of any other coverage that is available.

Attachments should include an electronic version of admitted policies if coverage has been placed with a foreign insurer.

Correspondence Documentation level = Account

This is a freeform section to comment on and attach other written or electronic communications that do not have a more specific category that applies.

When this category is selected for an attachment, you are required to enter a description in the text box prior to saving. The naming of your attachment is also very important when this category is selected so you can retrieve it easily in the future.

18

Premium Audit Documentation level = MM Policy/LOB; SC Account

Comment on material changes in exposure bases between what is reported by premium audit and what appears on your most current renewal policy. Document any audit disputes and resolutions as well as premium audit advices (PATU) or Audit Worksheets regarding notification of changes in operations or discrepancies in classifications, exposure bases, or business operations.

Reinsurance Documentation level = MM Policy/LOB; SC Account

Comment by line of business and location(s) if facultative reinsurance was placed. Include reinsurer’s pricing and terms and conditions and the referral and signoff as applicable. The reinsurance spreader and certificate are attached here.

Agency Analysis Documentation level = Account

Comment on agency ranking and any other agency or business related facts including profitability, retention plans, etc. You can also include agency expertise managing the class of business as applicable and comment on the level of relationship the producer has with their client.

Overall Account Evaluation Documentation level = Account

Comment on your overall conclusion and summarize your decision without duplicating information already found in other sections of the Workstation:

Why the account as written belongs in our portfolio

Pricing – how is our pricing representative of the exposures and appropriate for this risk

Appetite – how well does this risk fall within our market appetite and industry guidelines based on our current strategy

Sales Strategy – any details that are pertinent to how you plan to win/retain the account

Follow Up – outline any items or conditions that need to be followed up on and the timeline for completion

19

Underwriter Referrals/Clearance Documentation level = Account

It is very important to document all your referral points in this section:

Outline your reason for referral and to whom. Attach approval documentation including what needs to be completed as part of the approval process.

Attach clearance instructions received from other offices as applicable.

Rater Attachments Documentation level = Policy/LOB

Attach rater attachments, such as ACT or POS quotes, policy construction tools and form listings, manual rating worksheets, etc. Refer to the Appendix for specific guidance by attachment type for more details.

20

Appendix

ARF Conversion Document

At-a-Glance Documentation Job Aid – Small Commercial & Middle Market

UWW Requirements for Rater Documentation

Examples of good account documentation

21