01. introduction to economics

TRANSCRIPT

1

Introduction to Economics

ReferencesReferencesInternetInternetWikipediaWikipediaModern Economic Theory (K.K Dewett)Modern Economic Theory (K.K Dewett)

Resource Person: Furqan-ul-haq Siddiqui

Chapter # 1

2

Demand Supply Inflation Deflation Economic Crises Economic Condition Stock Exchange Super power ………………………

3

Why Economics……! Unlimited Wants Scarce Resources –

Land, Labour, Capital Resource Use Choices

4

Economics is about deciding Whether to buy a car or not?

Whether to have Biryani for dinner tonight, or something else?

Whether to marry your ______or some one else?

Which course to study/ where to take admission?

And many other decisions are related with economics

5

Economics The term economics comes from the The term economics comes from the Greek world world

οἰκονομία (oikonomia, "management of a οἰκονομία (oikonomia, "management of a household, administration") from οἶκος (oikos, household, administration") from οἶκος (oikos, "house") + νόμος (nomos, "custom" or "law"), "house") + νόμος (nomos, "custom" or "law"), hence "rules of the house(hold)“ or hence "rules of the house(hold)“ or ““one who one who manages a householdmanages a household.”.”

EconomicsEconomics is the study of how individuals/society manages its scarce resources.

Economics is about deciding

6

Economics The science which studies human behavior as a

relationship between ends and scarce means which have alternative uses.“

Scarcity means that available resources are insufficient to satisfy all wants and needs. Absent of scarcity and alternative uses of available resources there is no economic problem. The subject thus defined involves the study of choices as they are affected by incentives and resources.

7

Branches of Economicsa. Microeconomics (from Greek prefix micro- meaning

"small" + "economics") is a branch of economics that studies how the individual parts of the economy, the household and the firms, make decisions to allocate limited resources

b. Macroeconomics (from prefix "macr(o)-" meaning "large" + "economics") is a branch of economics that deals with the performance, structure, behavior and decision-making of the entire economy, be that a national, regional, or the global economy .

c. Econometrics: Applies the tools of statistics to economic problems.

8

Life is full of choices. People make many choices everyday. Choices, often called decisions, vary in their difficulty. Regardless of the level of difficulty, all choices carry costs and benefits. Young children make many choices/decisions. Research reveals that they should begin to learn decision-making skills at an early age. Learning basic economics concepts and principles fosters the development of good decision-making skills.

Economics is the study of choice under scarcity. Our resources are limited, and our wants are unlimited (scarcity). Scarcity is the inability to satisfy all of our wants at the same time. We must make choices about how to use our limited resources.

9

Opportunity Cost

is the next-best choice available to someone who has picked between several mutually exclusive choices. It is a key concept in economics.

A person who has $15 can either buy a CD or a shirt. If he buys the shirt the opportunity cost is the CD and if he buys the CD the opportunity cost is the shirt. If there are more choices than two, the opportunity cost is still only one item, never all of them.

10

Example

Benefit

(Salary)

Cost

(Transportation)

Net Benefit

Job A

Lahore15,000 1,000 ?

Job B

Gujranwala

20,000 7,000 ?

Rational Choice Job A is betterRational Choice Job A is better

11

Benefit

(Salary)

Cost

(Noise)

Net Benefit

Job A

Bank15,000 0 ?

Job B

Factory16,000 2,000 ?

Rational Choice Job A is better

Is it possible for a consumer to chooseJob B and still be rational ?

12

a. Wealth Definition/Classical Thoughts Classical economics is widely regarded as the first modern

school of economic thought. Its major developers include Adam Smith, Jean-Baptiste Say, David Ricardo, Thomas Malthus and John Stuart Mill.

Publication of Adam Smith's The Wealth of Nations in 1776, has been described as "the effective birth of economics as a separate discipline. "The book identified land, labor, and capital as the three factors of production and the major contributors to a nation's wealth.

Adam Smith (father of economics) defined economics as “ a science which enquires into the nature and cause of wealth of nation”. He emphasized the production and growth of wealth as the subject matter of economics.

13Publication date: 1776 Adam Smith (Father of Economics)

14

Characteristics:Takes into account only material goods.

Criticism of Wealth Oriented Definition :

Considered economics as a dismal or selfish science.

Defined wealth in a very narrow and restricted sense which considers only material and tangible goods.

Have given emphasis only to wealth and reduced man to secondary place in the study of economics.

15

b. Material Welfare Concept/Neoclassical economics According to A. Marshall “Economics is a study of mankind in

the ordinary business of life; it examines that part of individual and social action which is most closely connected with the attainment and with the use of material requisites of well being. Thus, it is on one side a study of wealth; and on other; and more important side, a part of the study of man.

Characteristics of Welfare Definition: Emphasize on material welfare as the primary concern of

economics i.e., that part of human welfare which is related to wealth.

Takes into account ordinary business of life – It is not concerned with social, religious and political aspects of man’s life.

Limited the scope to activities amenable to measurement in terms of money.

Economics is social science and not a study of isolated individuals

16

Other neo-classical economists

1. AC pigou: economics deals with the part of social welfare that can be brought directly or indirectly into relation with the measuring rod of money.

2. Edwin cannan: It is the study of causes of material welfare.

3. Beveridge: It is the study of general methods by which man cooperate to meet their material needs.

17

Alfred Marshall (1842 to 1924) was an English economist and one of the most influential economists of his time, being one of the founders of neoclassical economics. His book, Principles of Economics (1890), brings the ideas of i. supply and demand, of ii. marginal utility and of iii. the costs of production into a coherent whole. It became the dominant economic textbook in England for a long period.

i. Relationship between the quantity of a commodity that producers have available for sale and the quantity that consumers are willing and able to buy.

ii. the marginal utility of a good or service is the utility gained (or lost) from an increase (or decrease) in the amount available of that good or service.

iii. the cost-of-production theory of value is the theory that the price of an object or condition is determined by the sum of the cost of the resources that went into making it.

18

Criticisms of Welfare Oriented Definition :

Criticized for treating economics as a social science rather than a human science, Thus welfare definition restricts the scope of economics to the study of persons living in organized communities only.

It addresses only material welfare of man & neglects immaterial welfare.

Welfare definition was advertised as extensions and refinements of Classical Definition

Quantitative measurement of welfare

Lionel Robbins led a frontal attack on the Marshallian view.

19

c. Scarcity or Science of Choice Concept According to Lionel Robbins (1898 - 1984) “Economics is

the science which studies human behavior as a relationship between ends and scarce means which have alternate uses”

Characteristics of Scarcity Oriented Definition:

• Unlimited ends ( wants )- Unlimited and over overlapping.

• Scarce means-• Alternative use of means.• Choice – decision regarding which alternate would

be more effective.

20

Lionel Charles Robbins, Baron Robbins (November 22, 1898 - May 15, 1984) was a British economist, famous for his Essay on the Nature and Significance of Economic Science. his work was influential in the advancement of economics as a philosophy and science.

“True individual freedom cannot exist without economic security and independence. People who are hungry and out of a job are the stuff of which dictatorships are made.”

21

d.d. Growth/Development Concept Growth/Development Concept ::

According to Prof. Samuelson (May 15, 1915 – December 13, 2009) “Economics is the study of how men and society choose with or without the use of money, to employ the scarce productive resources which have alternative uses, to produce various commodities over time and distribute them for consumption now and in future among various people and groups of society.

Characteristics of Growth Oriented Definition: The definition is not merely concerned with the allocation of given

resources but also with the expansion of resources, tries to analyze how the expansion and growth of resources to be used to cope with increasing human wants.

More dynamic approach. According to him problem of resource allocation is a universal

problem whether it is a better economy or an exchange economy. Definition is comprehensive in nature as it is both growth oriented as

well as future oriented.

22

e. Need Oriented Definitions Even today economist don't agree on any one definition of

economics. Thus every time we face a dilemma therefore Prof. Viner defined “ Economics is what economists do”.

A social science concerned with the proper use and allocation of resources for achievement and maintenance of growth with stability.

A social science concerned chiefly with the way society chooses to employ its limited resources, which have alternative uses, to produce goods and services for present and future consumption.” It describes and analyses the nature and behavior of the economy.

23

Factors of Production/ Economic ResourcesFactors of Production/ Economic Resources

1. Natural resources: (economically referred to as land or raw materials) The things created by acts of nature such as land, water, mineral, oil and gas deposits, renewable and nonrenewable resources.

i. Renewable resources are ones that can be replenished or reproduced easily. like sunlight, air, wind, etc., are continuously available and their quantity is not affected by human consumption. Many renewable resources can be depleted by human use, but may also be replenished. Some of these, like agricultural crops, take a short time for renewal; others, like water, take a comparatively longer time, while still others, like forests, take even longer.

ii. Non-renewable resources are formed over very long geological periods. Minerals and fossil fuels are included in this category. Since their rate of formation is extremely slow, they cannot be replenished once they get depleted. Of these, the metallic minerals can be re-used by recycling them. But coal and petroleum cannot be recycled.

Factors of production are the resources that are used to Factors of production are the resources that are used to produce goods and services:produce goods and services:

24

2. Labor:The human effort, physical and mental, used by workers in the production of goods and services.

3. Physical Capital. (human-made tools and equipment)

All the machines, buildings, equipment, roads and other objects made by human beings to produce goods and services.Capital goods may be acquired with money or financial capital.

25

4. Human capital:

refers to the stock of competences, knowledge and personality attributes embodied in the ability to perform labor so as to produce economic value. It is the attributes gained by a worker through education and experience.

5. Entrepreneurship:The effort to coordinate the production and sale of goods and services. Entrepreneurs take risk and commit time and money to a business without any guarantee of profit. Entrepreneurs assemble resources including innovations, finance and business acumen in an effort to transform innovations into economic goods.

26

Economics as Positive and Normative StudyEconomics as Positive and Normative Studya. Positive Study (What is? What was? What will be?) – actual happenings.

Positive economics is the branch of economics that concerns the description and explanation of economic phenomena.- Lahore is an over-populated city.- Prices in Pakistani economy are constantly rising.

b. Normative Study (What ought to be? What ought to have been?) Normative economics is the branch of economics that incorporates value judgments about what the economy ought to be like or what particular policy actions ought to be recommended to achieve a desirable goal - Fundamental principle of economic development should be the development of rural areas of Balochistan.- Agricultural income should also be taxed.

27

Fundamental Problems Facing an Economy1. What to produce and of which quantity:

What should the economy produce efficiently in order to satisfy wants as best as possible using the limited resources available with alternate options. It also implies between allocation of resources between different type of goods: Consumer goods and capital goods (Consumer goods are finished products whereas capital goods are bought as an investment to help produce something else include factories, machinery, tools, & equipment etc. )

2. How to produce- Labor intensive vs. capital intensive3. For whom to produce- How the national product be distributed ?

who should get how much? Should the economy produce goods targeted towards those who have high incomes or those who have low incomes.

4. Problem of efficiency and growth- How to achieve efficiency of resource and how to ensure further growth and development in the economy.

5. Problem of full employment- fullest possible use of all resources including labor & other resources.

28

Economic Systems An economic system is the system of production,

distribution and consumption of goods and services of an economy. It is the set of principles and techniques by which problems of economics are addressed, such as the economic problem of scarcity through allocation of resources. 1. capitalism2. Socialism3. Mixed economy4. Islamic economic system

29

Capitalism Capitalism: It is the economic system

based on the principle of private ownership of factors of production which include natural resources and capital. Government control over the economic activities of the people is minimum. people have much freedom to make choices about consumption, production, and making contracts. Full capitalism is not found in any country. Capitalism is also called Market economy, free economy or price system.

30

Socialism

A theory or system of social organization that advocates the vesting of the ownership and control of the means of production and distribution, of capital, land, etc., in the community as a whole. The government in a planned way, decides what is to be produced in the country. Means of production such as farms, factories, shops etc are owned by government. It is also called marxism.

31

Mixed economy

Features of both capitalism and socialism are found side by side. A part of industry, trade, energy, transport and communication, is controlled by the government while private sector is also quite strong.

32

Islamic economic system Islamic economics is

accordance with Islamic law. People have freedom to produce and consume goods but within the limits prescribed by the Holy Quran and Hadith. E.g. following Islamic law in regards to spending, saving, investing, giving, etc

33

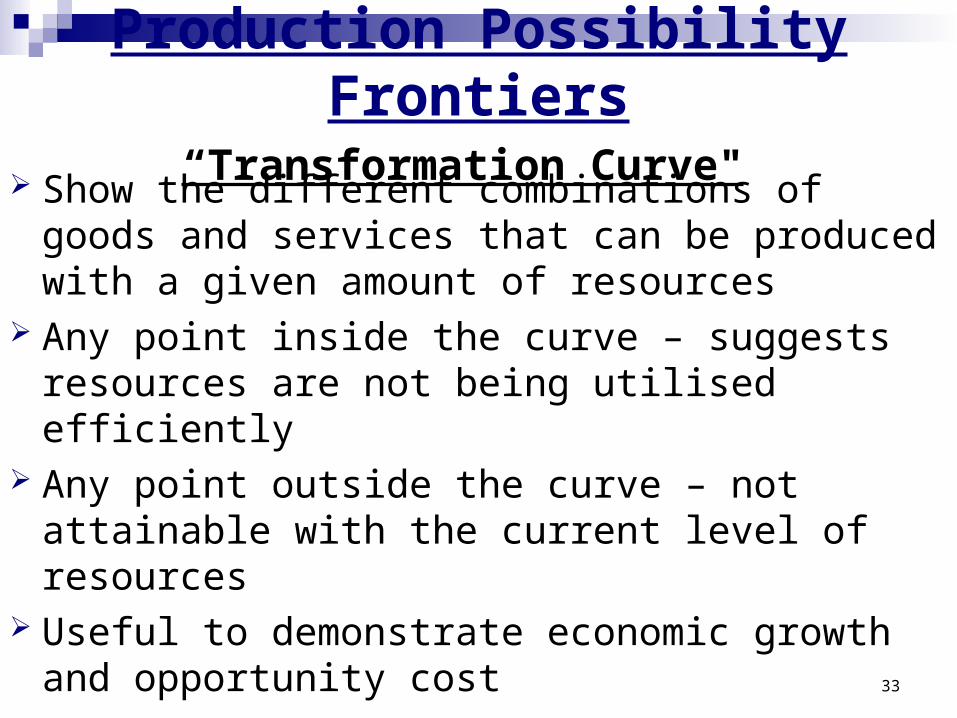

Production Possibility Frontiers“Transformation Curve"

Show the different combinations of goods and services that can be produced with a given amount of resources

Any point inside the curve – suggests resources are not being utilised efficiently

Any point outside the curve – not attainable with the current level of resources

Useful to demonstrate economic growth and opportunity cost

34

When the economy is at point i, resources are not fully employed and/or they are not used efficiently.

Point g is desirable because it yields more of both goods, but not attainable given the amount of resources available.

35

Point d is one of the possible combinations of goods produced when resources are fully and efficiently employed.

• To increase the amount of farm goods by 10 tons, we must sacrifice 100 tons of factory goods.

36

The PPF curve is bowed out because resources are not perfectly adaptable to the production of the two goods.

As we increase the production of one good, we sacrifice progressively more of the other.

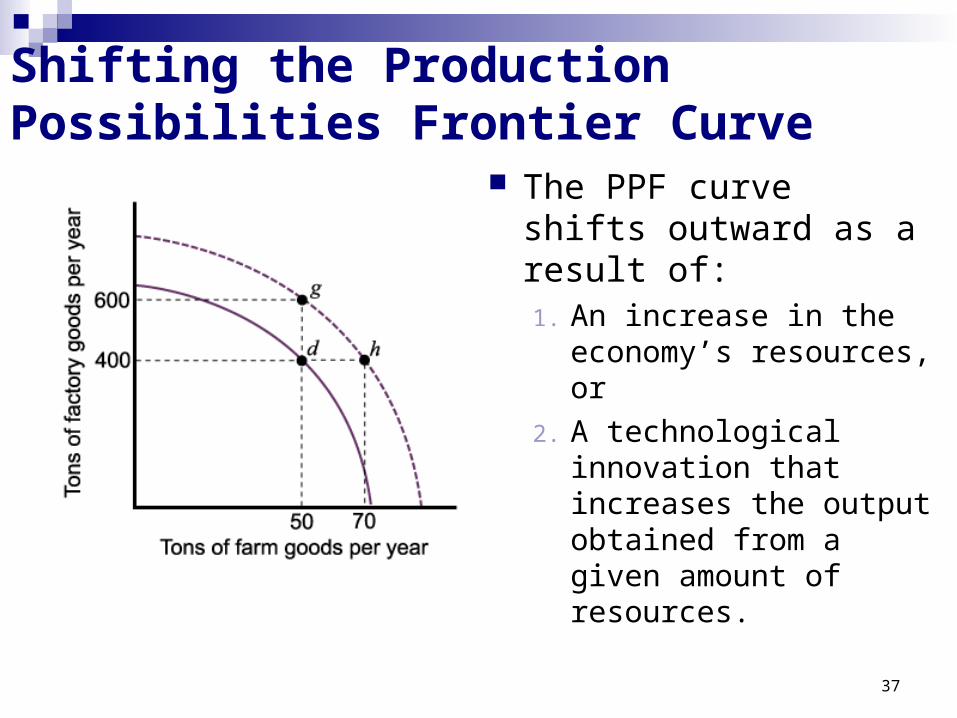

To increase the production of one good without decreasing the production of the other, the PPF curve must shift outward.

37

Shifting the Production Possibilities Frontier Curve

The PPF curve shifts outward as a result of:1. An increase in the

economy’s resources, or

2. A technological innovation that increases the output obtained from a given amount of resources.

38

• From point d, an additional 200 tons of factory goods or 20 tons of farm goods are now possible (or any combination in between).

39

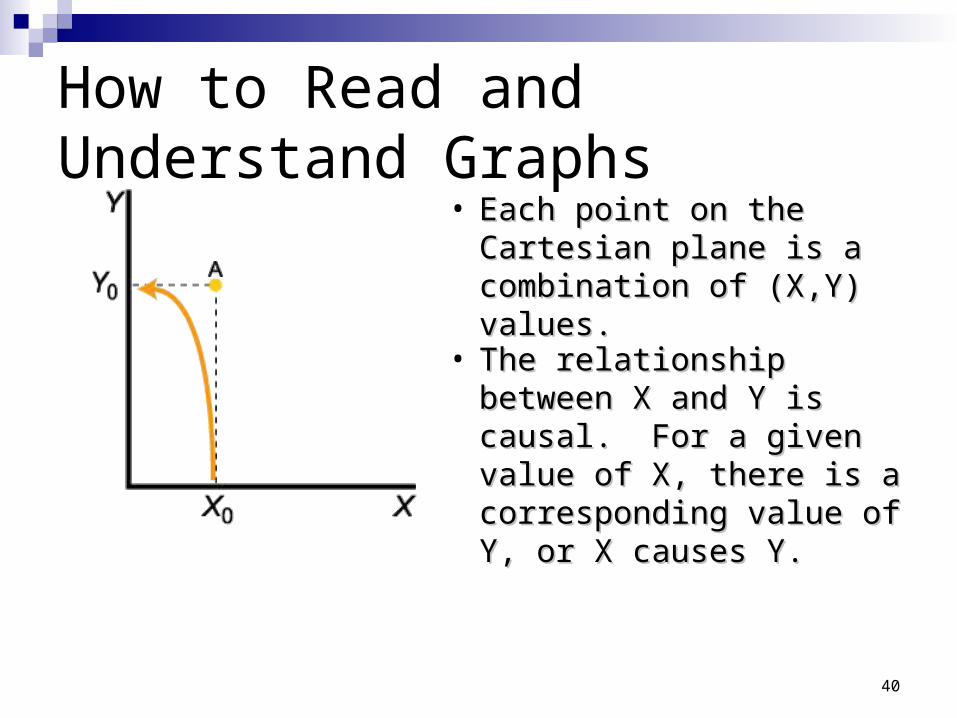

The Cartesian plane consists of two directed lines that perpendicularly intersect their

respective zero points.

40

How to Read and Understand Graphs

• Each point on the Cartesian Each point on the Cartesian plane is a combination of plane is a combination of (X,Y) values.(X,Y) values.

• The relationship between X The relationship between X and Y is causal. For a given and Y is causal. For a given value of X, there is a value of X, there is a corresponding value of Y, or corresponding value of Y, or X causes Y.X causes Y.

41

Reading Between the Lines• A A lineline is a continuous string is a continuous string

of points, or sets of (X,Y) of points, or sets of (X,Y) values on the Cartesian values on the Cartesian plane.plane.

• The relationship between X The relationship between X and Y on this graph is and Y on this graph is negative. An increase in the negative. An increase in the value of X leads to a value of X leads to a decreasedecrease in the value of Y, in the value of Y, and vice versa.and vice versa.

42

Positive and Negative Relationships

A A downward-slopingdownward-sloping line describes a line describes a negative relationship negative relationship between X and Y.between X and Y.

An An upward-slopingupward-sloping line line describes a positive describes a positive relationship between X relationship between X andand Y.Y.

43

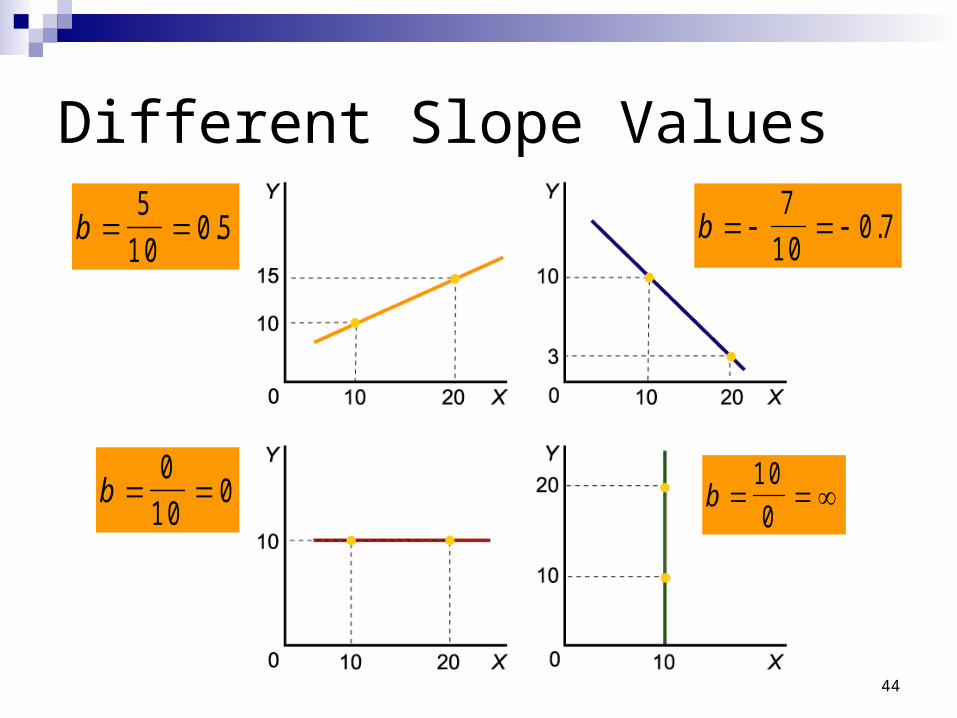

The Components of a Line• The algebraic expression of The algebraic expression of

this line is as follows:this line is as follows:

Y = a + bXwhere:where:Y = dependent variabledependent variableX = independent variableindependent variablea = Y-interceptY-intercept, or value of, or value of YY when when XX = 0. = 0.

b = slopeslope of the line, or the of the line, or the rate of change in rate of change in YY given a change in given a change in XX..

+ = positive relationshippositive relationship between between XX and and YY

b =

Y

X

Y Y

X X

1 0

1 0

44

Different Slope Values

b 5

1 00 5. b

7

1 00 7.

b 0

1 00 b

1 0

0

45

Strength of the Relationship BetweenX and Y • This line is This line is relatively flatrelatively flat. .

Changes in the value of X have Changes in the value of X have only a small influence on the only a small influence on the value of Y.value of Y.

• This line is This line is relatively steeprelatively steep. . Changes in the value of X have a Changes in the value of X have a greater influence on the value of greater influence on the value of Y.Y.

46

The Difference Between a Line and a Curve

Equal increments in Equal increments in XX lead to diminished lead to diminished increases in increases in YY..

Equal increments in Equal increments in XX lead to constant lead to constant increases in increases in YY..

47

Interpreting the Slope of a Curve

• Graph A hasGraph A hasa positive and a positive and decreasing decreasing slope. slope.

• Graph B hasGraph B hasa negative a negative slope, then a slope, then a positive slope. positive slope.

• Graph C shows Graph C shows a negative and a negative and increasing increasing relationship relationship between between XX and and YY. .

• Graph D Graph D shows a shows a negative and negative and decreasing decreasing slope. slope.