01146 voice 60 english - microinsurance network · from microinsurance initiative 17 housing...

TRANSCRIPT

OPINIONWith stakeholder support, the mutual/cooperative model

can improve the impact of microinsurance

FEATURE ARTICLEColombia’s insurance industry promotes financial education

MUTUALS AND MICROINSURANCEPiloting index- based weather insurance in IndiaProsper

SOWING THE SEEDS OF MUTUAL PROTECTION

the ICMIF develoPMent MagazIne: www.microinsurance.coop issue 10/june 2012

14

Prosperissue 10/june 2012

eDiTORiAL & pRODucTiOnsenior editor sabbir patel

deputy editor marine guais

desiGn gareth kendrick

cOnTRibuTing AuThORsandrew bibby, arup chatterjee, kumar shailabh;

imran nafeer; mortuza ali; daysi rosales; ludy

medina; barbara chesire; cherif benhabiles;

arlene sabaris; javier escobar; laurent bernard;

josée st hilaire; didyme pambou-dimina; silvina

cra vazon; karat gopinath, perez fernando;

rizick rosario; deepak dhakal; erwin embuscado;

basant maharjan; flora hermet; donna swiderek;

alejandra diaz; fiona melinda; sarah bel;

mackenzie vanderhyden; gabriele ramm; karina

avakyan; paula jimenez; matthew genazzini

submissiOns+44 161 929 5090 [email protected]

subscRipTiOns+44 161 929 5090 [email protected]

cOveR sTORysowing the seeds of mutual protection

(read the full article page 8)

photo provided by cherif benhabiles,

insurance manager, cnma (caisse nationale

de la mutualite agricole, algeria)

exchAnge RATes As AT 08/05/121 USD = 83 KES

1 USD = 53 INR

1 USD = 128 LKR

1 USD = 82 BDT

1 USD = 42 PHP

copyright © 2012 icmif. all rights reserved. reproduction

without permission is prohibited. the views and opinions

expressed in prosper are the author’s own and are

not meant to reflect the official position of icmif,

its entire membership, or their respective employers

(unless otherwise specified). information is provided

for informational purposes only and provided with

no warranty. while prosper provides web links, icmif

exercises no authority over third-party sites, each

of which maintains its own independent policies and

procedures. prosper is published by the international

cooperative and mutual insurance federation (icmif),

altrincham, cheshire, wa14 4qe, uk.

www.icmif.org/prosper

In this issueOPINION02 with stakeholder support, the mutual/cooperative

model can improve the impact of microinsurance

MUTUALS AND MICROINSURANCE04 overcoming challenges of microtakaful in sri lanka05 members of bangladeshi groups offered

microtakaful product05 seguros futuro launches a new and innovative

surgery insurance in el salvador06 card on hand to help typhoon-hit members07 kenya’s cic insurance takes microinsurance by storm08 sowing the seeds of mutual protection in algeria09 microinsurance take-up doubles for coop-

seguros in the dominican republic10 strategic alliances enable ecuador’s coopseguros

to benefit members with health protection11 canadian cooperative desjardins contributes

to microinsurance development12 protection offered to sugarcane producers in cameroon13 csr is at the heart of our operations, says rio uruguay14 piloting index- based weather insurance in india16 microenterprises in argentina benefit

from microinsurance initiative17 housing cooperative residents in puerto

rico get access to microinsurance18 protecting credit union members in nepal19 helping out in times of need19 women’s cooperative in nepal offers

access to health protection20 the role of mutual societies in the extension

of health protection in africa

ICMIF NEwS22 growing video library is a valuable resource24 participants get to grips with the microinsurance business

FEATURE ARTICLE26 colombia’s insurance industry promotes financial education

FROM THE SECTOR29 providing risk protection to low-income groups in indonesia30 how technology can support efficiency and client

value: the case of livestock insurance in india32 using microinsurance to protect vulnerable

communities from financial impacts of climate change: the res-risk project in india

34 reaching out to individual microinsurance clients37 exploring the potential of micro-pensions as a

response to the issues of global ageing

Mutuals, cooperatives and coMMunity-

Based orGanisations (Mccos) play an important

role in the economy and society, providing social

protection and other types of insurance to a

significant proportion of the world’s population. This

role is deeply embedded, historically, economically

and culturally in a large number of countries,

both developing and developed (although with

differentiations between each specific national

context).

Development requires among other things risk

reduction and the protection of assets and lives.

With a long history of greater access to vital

insurance services, far beyond the reach of formal

insurers, mccOs remain an important element in the work of reducing the vulnerability of the poor during crises by enabling them to accrue savings, build

assets, smooth out consumption, and invest in income

generating activities. MCCOs operate according to the

principles of solidarity between members who pool

funds against social and property risks, and can be

seen as predecessors to the modern form of voluntary

insurance.

Depending on the activities they perform and the

legal context within which they operate, it is not

always easy to determine whether and how insurance

laws are applicable to MCCOs. Given the large (and,

in many countries, growing) numbers of such

providers that already serve poor households in many

countries, formalisation of informal providers within

a proportionate regulatory framework is important

for effective financial consumer protection. The

framework should take into account the nature, size

and complexity of the business being conducted.

At the same time, formalisation can run counter to

the overall objective of financial inclusion to improve

the well-being of poor households, and there is

strong justification in some specific circumstances

for allowing certain small institutions to operate

informally in case their members have no access to

safer options. This is a delicate balance that should be

addressed prudently.

Mutuals and cooperatives should be better recognised

as a distinct and important form of organisation for

insurance provision. Needless to reiterate, the idea

of mutuality can be safeguarded in the future only

when mutuals themselves improve their products and

convince future members that this is indeed a cost

effective and sustainable alternative to commercial

insurance.

Developing and maintaining sustainable and

affordable social protection systems through MCCOs

can be ensured under the umbrella of an enabling

and policy environment where there is a proper

understanding of the opportunities and the risks.

This in turn will offer the right climate to scale up and

expand access, by strengthening their network as well

as capacity and performance.

In the International Year of Cooperatives 2012,

declared by the United Nations General Assembly, this

edition of Prosper is one means of raising awareness

of the cooperative and mutual enterprise model, and

its potential contribution to poverty reduction, among

policy makers, regulators and donors, and of seeking

their involvement and support.

arup chatterjee

Senior Financial Sector Specialist

Asian Development Bank

FOREwORD by ARUP CHATTERJEE

icmif prosper issue 10 | june 2012 1

wITH STAkEHOLDER SUPPORT, THE MUTUAL/COOPERATIvE MODEL CAN IMPROvE THE IMPACT OF MICROINSURANCE

it has Been less than a decade that microinsurance has emerged

on the development and poverty front but already there are impact

evaluations and researches being carried out worldwide as whether

these small ticket size transactions are making sense to providers

(including donors) as well as buyers.

Though there is a visible interest among donors and commercial

insurance providers alike to support microinsurance given the

untapped market size across Asia , Africa, Latin America and

elsewhere, there is a palpable anxiety that maybe we are still too far

from providing lasting solutions.

Complicated, frequent transactions involving risk products like

health (very high in demand) often make insurance providers think

twice before offering them in the microinsurance space. Credit

life and to an extent life are the most spread out microinsurance

products. The ones that offer health are largely limited to countries

like India where huge government subsidies on health insurance

premiums are the reason behind large uptakes,-without them

(subsidies) it would be impossible to have those million numbers.

To club such state financed social protection programmes under

microinsurance, somewhere also sounds misleading. Elsewhere,

in Africa specially, microinsurance is riding as add-ons to popular

brands and services that people use and trust, pointing to a deficit of

trust and understanding on the insurance product by the buyers.

In a largely, supplier led ecosystem, is then microinsurance

delivering the goods that it is intended for? This is a tough

question that current and future practitioners and supporters of

microinsurance have to face.

The fact that the eco system of microinsurance is largely

supplier driven often limits rather than focuses the challenges of

microinsurance to the issue of distribution. In fact success stories in

microinsurance are mostly measured in numbers rather in millions.

Success stories from markets like India are about these million

numbers mostly from the state financed social protection schemes

on health and life.

There is no debating that whether distribution is an issue or not,

it definitely is of a critical nature and one that needs innovative

answers since the ticket size is so low and the risk of moral hazard

and adverse selection too high. State run social protection schemes

in India, and add-ons strategy and others followed in Africa, point

to viable options in distribution, but is this all? That is the pertinent

question.

When a study conducted by the Indian Insurance Regulator

admitted that 60% of insurance clients were not clear as to what cover and benefits they have bought, it points to a rather alarming situation, this against a

background of bleeding portfolios in motor and health insurance in

Kumar Shailabh

2

India. If people were not aware then the insurance providers should

have been making money, this is not the case either!

It’s now increasingly being accepted that client awareness is of

critical importance in the success of microinsurance, but won’t it

mean that it would push the claims graph of the providers as well?

There are other challenges in the delivery of microinsurance but

a closer look at all these challenges reveal that these are partly

symptomatic, the root to these challenges perhaps lie in the fact that

the buyers/clients are not the epicentre of this delivery . That clients

of micro insurance come at the end of the supply chain (mostly

as beneficiaries/consumers) and that they have no role in risk

management (and is supposed to be the prime role of the providers).

The client as a consumer of finished product is still very strong in

the microinsurance space.

This is where the cooperative/ mutual model can become a game

changer and there are strong ground evidences now emerging that

variants of cooperative and mutual models are doing better than the

pure risk transfer models in microinsurance with special reference

to value for money. These emerging models in microinsurance are

taking insurance to its roots where the emphasis is to share the risk

rather than transfer it. Even when the clients or consumers are not

sharing the risks completely there is a very clear role of the clients

in the management and decision making of such programmes.

What makes these microinsurance programmes work is

the ownership of the programme by the members and an

understanding that they are sharing the risk and hence the need

to be more responsible. Distribution in these models is often group

based and product process known to members, and the members

or their representatives being central to the risk management

process. These models spend quality time in educating their

members and being on the ground when they need information

or help. In these models, the consumers are also the producers

and these PROSUMERS ensure that these models sustain and

grow. The asymmetry of information which has become the bane

of commercial insurance is structurally missing in these models

thereby making them better for democratic dispensation.

Trust among members in mutual microinsurance model is a

critical factor of success that has to be combined with systems.

These models are therefore not easy to setup as they are client and

context focussed and take up 5-8 years of gestation period even

before they can be partly sustainable. In the race of having numbers

in microinsurance and space dominated mostly by commercial

providers, these models stand appreciated but alone. The mutuality

or cooperative components and benefits of these models are often

overshadowed by financial benchmarks.

Of late, though, there is emerging evidence that these models are

working better (client value, value for money), but the support

for them has been very limited or in some cases non-existent.

These models face multiple problems that range from not having

adequate resources and technical know-how to not having efficient

Management Information Systems (MIS) and many cannot grow

because of unfavourable regulatory environments.

These micro mutual insurance models have been out there for

some time and they have grown despite several odds. Odds that

ensure their growth is slower and will take long to mature. There

is also a danger that without a favourable eco system they might

not withstand the competition from large commercial providers

and may have to be disrupted for want of conducive regulatory

environment.

These micro mutual insurance models are the potential giant

mutual insurers of tomorrow as has been the case with existing

mutual and cooperative insurers who are leading the insurance

space for quite some time now. However a look at the support

offered for mutual microinsurance by stakeholders i.e. donors, policy

makers and even established mutual-cooperative insurer’s reveals,

that the support is almost negligible.

mutual/cooperative models in microinsurance require patience and persistence and without support from donors/policymakers, it will be difficult for them to survive and grow. This

absence of support will slow down or rather hinder new initiatives

making them a difficult proposition to envisage.

While the lack of support and understanding from donors and

policymakers exist, the lack of support from larger and established

Mutual and Cooperative insurers works as a double disadvantage.

Firstly, the ability of such micro mutual models to gain business

respect in their respective countries, as there is no existing example

of scale and sustainability or for that matter regulation. Secondly,

regulators, donors, policymakers believe what they see and they see

these micro mutual models alone, growing very slowly and many a

times as a one-time experiment project thanks to donor subsidies.

The arguments for supporting micro mutuals is only one, delivering

demonstrable, qualitatively effective risk protection mechanisms

to the poor where they have say in it. These micro mutuals are the

roots of mutuals of tomorrow. They are one of the best promises

the poor are left with when it comes to risk protection in emerging

economies and though the ticket size is small they are the future

mass markets.

KuMar shailaBh

The writer works with Uplift Mutuals in India.

icmif prosper issue 10 | june 2012 3

OvercOming challenges Of micrOtakaful in sri lankaicMiF MeMBer aMana taKaFul is working

with Muslim Aid Sri Lanka in implementing Islamic

microinsurance programmes in Sri Lanka. Insurance

provision is being coupled with credit services that

are offered by Muslim Aid to the people in villages.

Borrowers are put into small groups consisting of

three members, each of whom is a mutual guarantor

for the other members’ loans. The same practice

is followed in insurance service as well. Members

themselves are able to form their own groups.

The members of the group sign for each other’s loans

and insurance policies which are explained to the

individuals in front of other members. Ten groups of

three people are in turn linked together into a larger

group called a ‘Centre’, which meets monthly for loan

repayment purposes on a set day of the month.

Although both loans and insurance are provided

to individuals, the products are aimed at the family

unit. Involvement of each family member, including

both husbands and wives, is seen as a very important

factor in any financial service provision for the poor.

Because of low understanding of the concept of

insurance and a lack of trust in insurance service

providers by those on low incomes, it has proved a

challenging task to convince the people about the

value of having insurance cover. According to muslim Aid, many people initially perceived insurance as a savings option. Muslim Aid tried initially to conduct a

few sessions about insurance with members, but this

approach proved unsuccessful in getting the message

out to family members. To overcome this challenge,

a Financial Literacy Training programme has been

introduced for members. One of the main components

of the training programme has focused on the

importance of insurance. The training is conducted

in an interactive way coupled with pictures and other

visual material.

There have been other challenges relating to claims

handling, a new experience for Muslim Aid. Payment

of claims is a key factor to make people comfortable

about insurance but two identified bottlenecks were

delaying the process. The first was in receiving claims

documents from the client, the second in getting the

approval from the insurance service provider for the

claims. Process improvements in both aspects were

facilitated and a couple of training programmes were

conducted for Muslim Aid staff members about claims

handling, especially the importance of identifying

claim documents for hospital treatment at a field level.

Improved operational capacity of the field officers has

allowed claims to be paid within a day.

To make the insurance services more tangible

and provide a physical record for the members,

an Insurance Card is given to them with details of

the insurances that they have taken out and the

premiums they have paid. A further innovation has

been to use 5-10 minutes of the monthly Centre

meetings to discuss insurance. Members who

have received claims are given time to share their

experience with fellow members.

According to Muslim Aid, this is the strongest

marketing tool available. The organisation adds that

support of the village leaders is very important to

spread the message across the community effectively

and efficiently.

Muslim Aid seeks random client feedback, and

is aware that there would be a demand for more

customised insurance products. However so far the

insurance has been offered as a standardised product

to each member. One of the most important factors

is to keep the operation cost as low as possible

while providing a quality service to clients and

Muslim Aid is aware that more complex products

might complicate key issues such as the payment of

premiums and claims handling.

delegates at the last takaful network

meeting in Colombo observing Microtakaful

premium collection

4

members Of bangladeshi grOups Offered micrOtakaful prOduct the BanGladeshi taKaFul operator and ICMIF

member Prime Islami Life Insurance Limited has

recently launched a new group microtakaful product,

Karmajibi Kalyan Bima, to complement the other

takaful products it makes available.

Karmajibi Kalyan Bima is a completely new group

term insurance product in the Bangladesh market.

While other group insurance products in the market

provide an assured sum at death this product

provides several additional benefits. For example,

double the sum assured is paid in the event of

accidental death, the full sum assured is paid for total

and permanent disability, whilst a funeral payment

is also made, based on 20% of the sum assured.

Furthermore a monthly stipend for a nominated

person is also paid after the death of assured. These

benefits are included without any extra premiums

being required.

The product’s target group are factory workers and

employees, office staff, members of trade unions and

associations, and members of co-operative societies.

The product is also available for Bangladeshi workers

who are engaged in hazardous & non- hazardous

occupations abroad.

The premium rates for Karmajibi Kalyan Bima range

from USD 6.8 to USD 14.5 for a term of one year and

from USD 17.3 to USD 40.8 for a term of three years

for BDT 100,000 (USD 1,221) sum assured.

The minimum sum assured (the equivalent of USD

610) has been set low, to enable people of all walks of

life to get the benefit of life insurance. The minimum

number of people in each insured group is fifty, again

kept low to enable members of as many organisations

as possible to sign up.

segurOs futurO launches a new and innOvative surgery insurance in el salvadOrthere was a big turnout for the launch on 22

March this year of an innovative new surgery

insurance product from Seguros Futuro, El Salvador’s

only insurance cooperative. Among those present at

the event were delegates from cooperatives, micro-

finance companies, medical and insurance brokers,

the cooperative training institute el Instituto de

Fomento Cooperativo and the Development Bank

Banco Interamericano de Desarrollo.

The costs of surgery in private hospitals in El Salvador

are very high, whilst public hospitals have very long

waiting lists. Seguros Futuro’s new product aims

to provide better protection for the families of the

members of the country’s cooperatives as well as

the general public, by covering medical and hospital

costs arising exclusively from surgery. More than two

hundred different surgical operations are covered.

Costs incurred in pre-surgery consultations and

examinations can also be claimed, up to USD 130.

The insurance cover can be taken out just for the

insured person, for them and their spouse, for a

family unit, or for the insured person and their

children. Children are covered up to their 25th

birthday. The cost of the premium depends on the age

of the policyholder and the plan selected, starting at

USD 40 per annum.

Seguros Futuro says that the product has been

designed to be easy to obtain at an affordable price.

Policyholders can go to any hospital, and claims are

paid within five working days. There is no limits on

the numbers of operations which can be carried out

under the policy.

icmif prosper issue 10 | june 2012 5

card On hand tO help typhOOn-hit members

typhoon sendonG (or washi as it was

More coMMonly Known internationally)

caused catastrophic damage in the Philippines on

the night of December 16 and the early morning of

December 17, 2011. It devastated a large part of the

city of Cagayan de Oro and significantly damaged

parts of Iligan City, Agusan and Surigao del Sur, with

one month’s equivalent of rainfall leading to flash

flooding. Unfortunately hundreds of fatalities were

reported while some people are still missing. Most of

the casualties were women and children according to

the Philippine National Red Cross.

icmiF member cARD mutual benefit Association, inc. had nearly 23,000 members in the areas affected by the typhoon, very many of whom lost their

homes and valuables. Some also lost family members

in the flood, whilst others are still hoping that their

loved ones are alive and in one of the many packed

evacuation centres.

CARD had offices in Cagayan de Oro and these offices

were also affected. However, after re-organizing and

cleaning up of the flooded offices, CARD staff were

able to recover from the nightmare and quickly

started visiting the clients in their respective areas

and in the evacuation centres. A day after the typhoon,

the Managing Director of CARD MRI Dr. Aris Alip also

visited the affected provinces to determine what help

CARD could offer its members and staff. Staff from

CARD offices are affected by the flood helped out and

started packing relief goods for affected clients in the

evacuation centres.

CARD’s policy is to provide benefits to members and

their families immediately in times when it is needed,

but because of the flood many did not have the

required documents with them. CARD management

consulted the Insurance Commission and were given

permission to give out the benefits with minimum

paperwork requirements.

For policyholders who were missing, CARD paid 50%

of the death benefits due, on the basis that this would

be returned if the person was later found alive. The

remaining 50% will be paid if the person remains

missing after a year. Many CARD members expressed

their gratitude for this immediate help, which assisted

them in recovering from both the physical and

emotional pain brought about by the disaster.

In total CARD MBA paid out 94 claims related to

death (including those missing), with claims totalling

USD 18,341. 75 claims were met under the Package

Assistance in case of Disaster (PAID) Plan policies,

totalling USD 11,969. Over USD 50,000 was met in

claims under the CARD Disaster Relief Assistance

Program.

Typhoon Sendong has been a painful experience,

but it has provided an opportunity for CARD to think

further about new products and services that can

help CARD clients on occasions like this. Among two

ideas are insurance for clients’ businesses and loan

protection insurance.

Cdo unit office after the flood brought about by the typhoon Sendong

Relief operation team meets with dr. alip, CaRd MRI Managing director (second from right)

6

kenya’s cic insurance takes micrOinsurance by stOrm

a CIC activation tent in donholm, nairobi

2012 has so far been an exciting year at CIC on the

microinsurance front, and the new buzz word at CIC

is M-Bima (Swahili for Mobile Insurance). M-Bima is

a first in the Kenyan insurance landscape, allowing

clients to sign up, pay for their premiums and review

their statements from a touch of a mobile phone

button or on the internet at www.m-bima.co.ke.

The platform was developed by CIC in response to

information from clients that they would like to be

able to pay their premiums in a mode that fits their

lifestyle. Most of the low income market in Kenya

work in the informal sector where they earn a wage

on a daily basis.

To stimulate the market, CIC has been going to

particular neighbourhoods, setting up a tent and

inviting local people to talk to CIC sales people. The

insurer attracts attention by playing popular music

and by offering entertainment.

The M-Bima initiative has received global attention

and in particular from the ILO Microinsurance

Innovation Facility in Geneva. With backing from the

ILO, various market research activities are taking

place, including focus group discussions with sample

groups of M-BIMA clients. This feedback is helping

CIC develop its future marketing plan which includes

branding, communication and distribution.

A recent survey entitled Kenya Microinsurance

Landscape and conducted by Cenfri identified

the main areas of key interest as being health

protection, as well as life cover (and in particular

cover for funeral costs) and the risks associated with

agricultural production. Generally, the cost of health

in Kenya is relatively high, and delivering health

insurance to the low income market poses unique

challenges. With difficulty of claims management

and high administration expenses, it has become

increasingly difficult to design an appropriate health

microinsurance cover.

Despite this, cic is currently piloting a new and improved health microinsurance cover called Afya imara (swahili for good health). The product, still in its piloting stage, offers both

inpatient and outpatient covers as a family package

at an affordable rate. The main challenge in health

insurance is normally the outpatient cover as it has

high levels of uptake and can potentially lead to a

very high claims ratio. In the product design stage, CIC

approached mission and low-cost hospitals around

the country and negotiated with the hospitals to

offer services to Afya Imara clients at a subsidized

rate. Based on this, CIC has been able to price a

highly discounted health insurance cover. To reduce

on administration expense, CIC has approached

cooperative societies and microfinance institutions to

extend this cover to their members. The institutions

are also offering insurance premium financing to ease

the burden of payment.

a client uses his mobile phone to sign up for M-Bima jijenge Savings Plan

an M-Bima Focus group of existing clients

icmif prosper issue 10 | june 2012 7

sOwing the seeds Of mutual prOtectiOn in algeriala caisse nationale de MutualitÉ aGricole

(cnMa) has a long and distinguished history in

supporting the agricultural sector in Algeria and

in developing effective democratic and cooperative

way of working. It is now working on a five year plan

to modernise both its operation and the products it

offers its members, with the aim of better meeting its

members’ needs and building a successful ‘modern

mutual’.

Among the developments are an extension of crop

insurance. CNMA is among other things widening

the coverage of insurance against hail, offering full

insurance on cereal cultivation covering the risk

of drought, and introducing multi-risk insurance

against climatic hazards for crops such as vines, olives

and tomatoes that are dedicated to the low income

population. New insurance that will cover irrigated

crops such as potatoes and dates will be on the

market in 2013.

CNMA is also preparing new microinsurance products

for the rural population to protect their belongings

and health, including Takaful products. Another

aspect of CNMA’s strategy is dynamic management of

reinsurance.

cnmA stresses its mutual values, those of spirit of service, the sense of development and responsibility, solidarity and proximity. It sees its role

as extending into wider areas of rural development,

including the creation of social services and

professional institutions in the rural world, to

help farming populations to improve their living

conditions and earn additional income.

8

micrOinsurance take-up dOubles fOr cOOp-segurOs in the dOminican republiccoop-seGuros in the doMinican repuBlic reports a very

rapid growth in take up of its microinsurance products in 2011,

compared with the previous year. The number of members with

loan protection cover grew from about 77,000 to 133,000, whilst

members taking out savings protection grew even faster, from 5,000

to 46,000. In total, the numbers covered by microinsurance products

(which on average cost USD 10 or less a year, or under a dollar a

month) climbed from 91,000 to 191,000.

The growth follows Coop-seguros’s strategy of providing the

cooperative population in its country with greater protection. In

2011 it started a growth plan strategically oriented to the growth

of personal insurance, in particular group life assurance savings,

with special features covering death and invalidity, and with sums

insured in line with the needs of each grassroots cooperative and

its members. Coop-seguros anticipates that 2012 will also be a year

of major growth. It expects to add a further 50,000 members to the

micro life assurance plans, in particular strengthening the savings

policies and adding a new personal accident plan designed for

schoolchildren with the aim of protecting pupils and teachers. The

idea is to create a permanent system of protection for members’

children, which will promote not only security for the school, but

also cooperativism and an awareness of insurance in the families of

the children insured. For this plan, Coop-seguros is hoping to obtain

national or international support.

coop-seguros is also continuing its work of educating members and their families about insurance. In 2010 it identified some key points of insurance

education that members needed, and on this basis prepared a

Working Plan. This has already achieved tangible results and

continues to be a point of reference for the company.

The plan was broken down into several stages. Firstly, Coop-seguros

has concentrated on its own employees so that they in turn could

train others. For this purpose it created an “Insurance Diploma” for

its technical managers, divided into several modules lasting ten

weeks. In 2011, a total of 21 employees took part in the programme,

and this year a further 20 have joined, taking the total to total of 41

people or 73% of the staff.

The second stage was initiated in 2011, and has involved training

distributor agents. As they are the first line of contact for the

grassroots cooperative members, they have to know the needs met

by insurance and its importance, so that they can pass this on to

their members. Nine workshops were held in 2011, spread across all

the main regions of the country, and a total of 393 people took part.

A further five workshops have already been held in 2012, reaching

more than 200 people.

A third stage, also initiated last year, focuses on the managers of

Coop-seguros’s member cooperatives, and aims to train them in

principles of insurance and reinsurance. This project, where Coop-

seguros is also seeking international support for vocational training

with an academic institution, has a target of reaching 200 managers

this year, and in the first quarter of 2012, 35 have already taken part.

Coop-seguros’s programme of prevention through education

also includes the distribution of educational materials on fire,

hurricane, flood and earthquake in members’ insurance renewal

packs. Its forthcoming meeting in June this year will be dedicated

to disaster prevention, and the lecture will be given by the Director

of Civil Defence. On this occasion, in addition to talking about the

importance of safety in construction and the steps to be taken in

the event of a disaster, the insurer is giving away books containing

advice on good driving practice. This means that Coop-seguros will

be covering prevention in the main branches of insurance it sells

(vehicle, fire, and life).

icmif prosper issue 10 | june 2012 9

strategic alliances enable ecuadOr’s cOOpsegurOs tO benefit members with health prOtectiOnFewer than 10% of the population of Ecuador have

access to health services, whether private or provided

by the State. But members of Ecuador’s network

of savings and credit cooperatives can now obtain

health protection through an innovative product from

cooperative insurer Coopseguros. Currently 100,000

members already have this cover.

Coopseguros’s product offers general medical and

dental treatment, including two visits a month, and

access to generic medicines according to diagnosis.

The policy also includes life cover (USD 1,000, doubled

in the event of accidental death), cover for permanent

incapacity (USD 1,000) and help to families for funeral

expenses (USD 100).

Any member of a savings and credit cooperative whose account is active is entitled to sign up to the cover, in exchange for a monthly insurance premium payment of usD 1.25. To

receive medical attention, policyholders simply have

to go to any of the 25 or so medical centres around

the country and show their identity cards. Services

offered are provided in top level surgeries with

capable medical professionals and with friendly,

supportive medical personnel. Coopseguros monitors

the quality of service, contacting clients after

the event to find out about the suitability of their

treatment and they way they were looked after.

The medical centres see an average of 15 patients a

day in each surgery, and are open from Monday to

Saturday. This means that approximately 300 people

are attended to every month per clinic, or in total

between 8,000 and 10,000 members a month.

The success of this product for Coopseguros comes

through its partnership with the cooperatives who

share its vision of support for, and solidarity with,

the population in the medium/low economic bracket

who are vulnerable in health matters. Cooperatives

provide Coopseguros with a monthly report showing

new members for inclusion in the service and inactive

members for exclusion. New cooperative members are

covered from the day they join.

Due to the success of the current service, Coopseguros

is discussing with partner cooperatives extending the

cover to include medical treatment of the family of the

insured. Family cover of this kind will cost no more

than USD 4 per family per month, covering the main

member, his or her spouse, and three children under

the age of 23. Both Coopseguros and the savings and

credit cooperatives see this as helping create stronger

identity by all family members with the cooperative,

as well as generating future enrolment in the

cooperatives s as the children who access the service

become adults.

don gonzalo and his wife, self-employed adults who benefit from medical cover. no public system offers them cover. With the lIFe and health product, they obtain service without having to queue or get up early to get into line.

Mrs. Miriam del Pilar tamayo and her husband and daughter, waiting to be attended to in one of the cooperatives committed to providing comprehensive care for members and their families.

10

canadian cOOperative desjardins cOntributes tO micrOinsurance develOpmentinterventions By dÉveloppeMent international

desjardins (did), a component of Desjardins Group (the leading

cooperative financial group in Canada), are helping to increase the

reach of microinsurance in many parts of the world.

Among other things, DID’s support has permitted the development

and establishment of a crop insurance scheme in Sri Lanka, based

on a rainfall index. This insurance, currently on offer in twelve

regions and due to be expanded to 27 regions shortly, has been

issued to nearly 4,400 farmers. The objective is to increase this

to 10,000 farmers. DID’s engagement has also helped increase

local understanding of the development, sound management and

distribution of such products and the diversification of risks on a

global and international scale.

DID has contributed to the improvement of the efficiency and

profitability of a scheme offering life insurance on loans which has

been introduced in West Africa by six cooperative financial networks

reaching over 2 million households. This form of credit insurance

encourages people to engage in business and borrow safely. In

addition, it facilitates borrowing terms since the loan is insured

against different types of risk. DID’s work has included offering

technical support on underwriting calculations. Further, it has

enabled the development of new tools for better analysis and more

appropriate follow-through of the results.

DID has also coordinated several activities that have improved

operational efficiency of la Mutuelle-Sociale, part of the PAMÉCAS

network in Senegal, relating to health insurance. The partner has

noticed a significant improvement in the distribution, marketing

and administrative processes of the existing product. The health

insurance product now insures about 15,000 persons and this

number is expected to grow rapidly over time as the product is

available through the network in different regions.

For Kenya, support was offered by DID to the cooperative insurance

company CIC in order to review its policies and strategies following

the integration of a new business line for the poor. More specifically,

the support covered the areas of marketing and distribution of

microinsurance products, manager and employee training, the

development of system management information, and awareness-

raising on the attitudes of low-income populations to protection and

insurance concepts.

With finance from the World Bank, DiD has been able to undertake analysis on the viability of microinsurance in several countries in West Africa. The aim has been to initiate the development of expertise

in microinsurance among partners and to make recommendations

on possible products. Similarly, support for capacity building of

microfinance associations has been achieved through encouraging

production of action plans and through facilitating budgets for the

implementation of these initiatives.

An analysis of supply and demand of insurance and microinsurance

products was conducted in a representative sample of countries,

in order to identify drivers and barriers to market development.

Based on this analysis, recommendations have been made to

improve access to microinsurance in Benin, Burkina Faso, Cameroon,

Central African Republic, Congo, Ivory Coast, Gabon, Guinea Bissau,

Equatorial Guinea, Mali, Niger, Senegal, Chad and Togo.

icmif prosper issue 10 | june 2012 11

prOtectiOn Offered tO sugarcane prOducers in camerOOntsala ZoMBo has been working in the crops

industry for the last 10 years. He is married and has

8 children. In addition to his mother and mother-in-

law who are over 65 years old, he is looking after his

three nephews. He earns XAF 80,000 per month (USD

161).

Mr Zombo is one of a growing number of people in

Cameroon to take out the microinsurance product

FAS Association (Fund for Aid and Solidarity) being

offered by ICMIF member Garantie Mutuelle des

Cadres (GMC) since February this year.

The FAS product is available to employees of the

Cameroon Sugar Company (SOSUCAM) which

employs 7,000 workers in the communities of

Nkoteng and Mbandjock about 150 km from the

capital city of Yaoundé. The product offers two main guarantees. These are assistance in case of hospitalisation (the gmc takes responsibility for 80% of the costs up to a chosen limit), and assistance in the case of a death in the family, where the gmc contributes to funeral costs.

Heads of households in Cameroon have enormous

responsibilities towards their families that extends

beyond the immediate family and includes cousins,

uncles, aunts, and even some friends. Due to the

state of poverty, the few people who have a source of

income must assume all of the family expenses. In

this context, a case of illness or death is the worse

economic disaster: the head of the family is often

forced to borrow money from others or from the

company that employs him. In this context, the FAS

product of the GMC is an opportunity for people to

reduce stress. The employer also benefits, with fewer

requests for salary advances from staff.

GMC has deployed a staff team in the localities where

SOSUCAM operates, to build the maximum number

of policyholders in a short time. There are 3 different

types of premium depending on the chosen option;

the lowest costs XAF 1,500 per month (USD 3), a

second is available at XFA 3,000 per month (USD 6),

and there is also an option of paying XFA 6,000 a

month (USD 12).

To facilitate the management of the policies,

cooperation agreements have been signed by GMC

with health facilities in the region.

12

csr is at the heart Of Our OperatiOns, says riO uruguayFroM its Birth, the Argentinean insurer Rio Uruguay Seguros has

always sought to promote a strong message of social concern and

cooperation. This is reflected in the company’s approach to corporate

social responsibility (CSR), which is directly overseen by the Board

of Directors and forms part of Rio Uruguay’s corporate vision and

mission.

Rio Uruguay is the first company to obtain ISO 9001 certification

in integrated management in general insurance, a quality scheme

which includes certification of all CSR management processes. The

company also addresses the key subjects covered in ISO 26000

(governance, human rights, labour practices, environment, ethics,

consumer issues and active participation and development of

the community). Rio Uruguay has been a signatory to the United

Nations Global Compact since 2004.

In its CSR work, the company operates both internally and

externally. Internally employees are engaged in a range of training

and learning opportunities, in issues including road safety, health

prevention, the environment, and retirement preparation. On the

external front, Rio Uruguay undertakes a range of educational work,

often organised jointly with universities and schools. Road safety

education programmes are arranged for both children and for adult

drivers. The company also works with civil society organisations

seeking to strengthen them institutionally and to support them in

sustainable projects.

Rio Uruguay’s approach is also reflected in the products it has

developed aimed at low-income communities. The company has

insurance products available for people who depend on public

assistance, for instance. One example is the “Seguro Médico Básico”

(Basic Medical Insurance) product, that covers a range of medical

interventions, assistance in case of hospitalisation and death

benefits.

Other products are aimed at people who do not have public

assistance but who are looking to provide protection for their

families. “Salud Familiar Plus” (Family Health Plus) insurance offers

cover for a range of health needs, including operations, prosthetics,

treatment of substance abuse, stroke, multiple trauma, major burns

and cancer.

A report of Rio Uruguay’s CSR work in 2011 can be

found at http://www.riouruguay.com.ar/comunicandonos/rse/index.php?option=com_content&task=view&id=364.

Rio uruguay team CSR 2011

icmif prosper issue 10 | june 2012 13

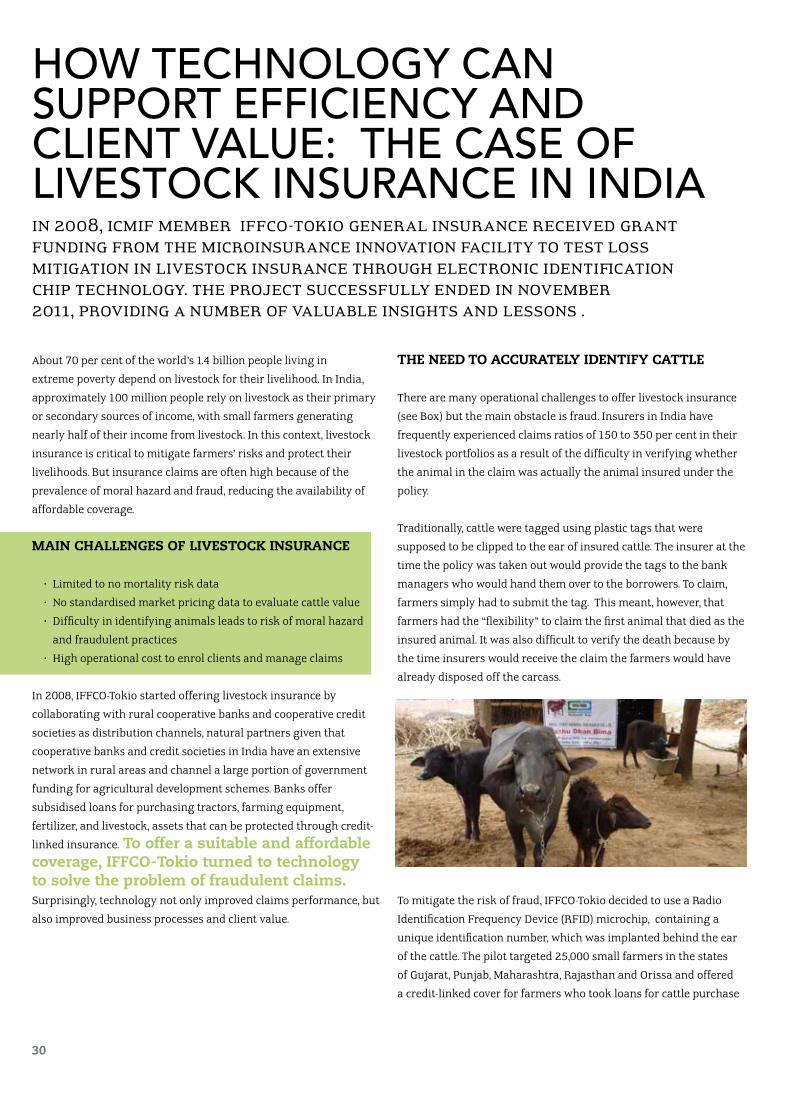

pilOting index- based weather insurance in india indian insurer iFFco toKio honoured its

commitment to its policyholders when 2,905 farmers

received cheques on 1st February this year for claims

they had made for damage to their crops during the

2011 monsoon season. They were policyholders with

IFFCO TOKIO’s Weather-based Crop Insurance Scheme

(WBCIS), the innovative index-based insurance which

covers rainfall and temperature. The cheques (totaling

8.21m rupees, or USD 150,000) were handed across at

a public ceremony in Fatehabad district in Haryana

state attended by the Agriculture minister of Haryana

Mr. Paramvir Singh, Director of IFFCO Mr. Prahlad

Singh and Mr. N.K. Kedia, Director (Marketing) IFFCO

TOKIO.

IFFCO TOKIO General Insurance is a joint venture

between the Indian Farmers Fertilizer Cooperative

Ltd (IFFCO), formed by more than 40,000 farmers

cooperatives, and Tokio Marine and Nichido Fire

Insurance Inc., of Japan. The Index-based weather

Insurance product was first introduced in 2004, and

sold to the members of IFFCO societies in the states

of Maharashtra, Gujarat and Karnataka. In 2007, the

Indian government gave a huge impetus to WBCIS

by extending subsidy, Ranging from 50% to 80%

depending on the type of crops. However for all the

government-supported schemes, there is an upper

cap for the premium to be charged. IFFCO TOKIO is

currently marketing its weather insurance products

in ten states covering thirty two districts.

Agriculture is the mainstay of the indian economy, sustaining close to 70% of the population and contributing nearly one fifth of the country’s gDp. Farm holdings are typically

very small, with the average size merely 0.4 hectares.

The climate of India revolves around the south west

monsoon (June to September) that contributes nearly

three-quarters of the annual rainfall received by the

country. Therefore an excess or shortfall of monsoon

rains result either in floods or droughts. Consequently

uncertainty of crop yield due to vagaries of weather is

one of the fundamental risks, the farmers face.

Mr n.K. Kedia director (Marketing) IFFCo toKIo (left)

14

Index based weather insurance policies are based

on weather data provided by automatic weather

stations, which means that the claims settlement

process is fast and transparent. During Kharif season

(the monsoon season), the policy covers weather

indicators such as excess rainfall, deficit rainfall,

consecutive dry days and consecutive wet days whilst

during Rabi (the winter season), the policy covers

unseasonal rainfall, low and high temperature,

relative humidity and wind speed.

The Index based weather insurance throws up its own

set of challenges. According to IFFCO TOKIO, these

include design of the product term sheets, which

can realistically measure the crop losses and which

are simple to understand. Though historical rainfall

data is easily available in India, other data such as

temperature, humidity and wind speed are not easily

available. Lack of an adequate number of weather

stations has been an issue, and those stations which

do exist need regular maintenance and calibration.

IFFCO TOKIO is currently designing its term sheets

on inputs from agronomists and government

experts. An actuarial based pricing tool is also being

developed jointly with Asia Risk Centre of Singapore,

a subsidiary of RMS, USA. To make the historical data

more reliable, various statistical methods are used

to fill in data gaps and to correct absurd readings. To

reduce basis risk, the density of automatic weather

stations is being increased to one station for every ten

kilometres.

IFFCO TOKIO leverages the strengths of its promoter

IFFCO to market these policies. In retail sales, a

capacity building workshop is held in primary

agriculture societies and the product is explained

in simple terms. In case of government sponsored

WBCIS, products are distributed through cooperatives,

scheduled commercial and regional rural banks and

linked with credit. The company has covered more

than one million people under this scheme and more

than four hundred thousand people have benefited.

The growing popularity of the scheme is reflected

in the large number of insured in such a short

span of time. Already newer and more improved

products, coupling index-linking with yield, have

been piloted. Satellite based yield estimations are also

being experimented with. The index based weather

insurance thus has the potential to transform the lives

of poor farmers and to a large extent addresses the

production risks associated with erratic weather.

Weather station

icmif prosper issue 10 | june 2012 15

micrOenterprises in argentina benefit frOm micrOinsurance initiativesancor seGuros (arGentina) is just beginning

the second year of operation of a pioneering

microinsurance programme which aims to help

reduce the vulnerability and the risks that people

running microentreprises are exposed to.

The initiative is a three-way partnership with the

Social Capital Fund (Foncap), an organisation with

long experience of working for social inclusion

throughout Argentina, and with the international

non-governmental organisation Planet Finance,

which has worked in the field of microfinance in

many countries and which provides management and

know-how. Sancor Seguros for its part contributes its

strong brand reputation and well-developed insurance

operation throughout Argentina.

As elsewhere in the world, microinsurance in

Argentina requires a commitment to meeting the

needs of low income people who do not have access

to traditional insurance. There is also the necessity

to create awareness about the role of insurance.

Sancor points out that this cultural process requires

economic resources and needs to be seen as a long-

term vision. Sancor stresses the social, as well as the

business, aspects of the insurance industry.

sancor’s microenterprise insurance aims to meet the requirements of all microinsurance schemes to be simple, accessible and low cost. The

product is flexible, and can be tailored to particular

needs. It includes a loan protection element, which

pays off any sums outstanding on loans in the event

of death or total and permanent disability, and a

family protection insurance which includes funeral

expenses. There are no medical exclusions and the

management process in the event of an accident is

kept very simple.

Sancor Seguros sees insurance as an increasingly

important tool to help economic predictability

and security for the community, particularly for

vulnerable people. The assessment after the first

year of the microinsurance initiative is that it has

successfully helped microentrepreneurs achieve

greater economic security and has improved the

quality of life for their families. Road safety practice area

16

Road safety practice area

since its incorporation in 1963, Cooperativa de Seguros

Múltiples has been recognised for its commitment to strengthening

the Puerto Rican cooperative movement and for its continuous

contribution to the country’s social development. Its success is due

in part to developing products which meet the needs of the market,

and it is now extending its work into the area of microinsurance.

One of its most recent initiatives is a microinsurance product aimed

at members of Puerto Rico housing cooperatives, who now have the

opportunity to obtain insurance policies in line with their needs

at affordable prices. The cover includes protection for personal

property including personal belongings such as clothing, furniture

and electronic equipment. Public liability against third party claims

for injury or death, damage to the property of others, and personal

injury is included, as is home and roadside breakdown assistance

services.

This microinsurance initiative, which builds on the established

alliance between Seguros Múltiples and the housing cooperatives,

has been warmly welcomed by the residents. Seguros Múltiples

says that it is strengthening its relationship with the cooperative

movement and contributing to the development of a solidarity

economy in the country.

Microinsurance housing ProgrammeMr. Roberto Castro hiraldo,

President, Coop Seguros Múltiples (left) signs the contract with

Mr. josé lópez and Mrs. Rosalina león, executive director housing Cooperative

jardines de San Francisco

hOusing cOOperative residents in puertO ricO get access tO micrOinsurance

icmif prosper issue 10 | june 2012 17

prOtecting credit uniOn members in nepalthe nepal Federation oF savinGs and credit cooperative unions ltd. (neFscun) is

offering microinsurance for SACCOS members through its NEFSCUN Mutual Aid Programme (N-MAP).

This operates under cooperative principles and values to help those who are excluded from formal social

protection mechanisms.

The N-MAP service started in 2005, initially offering a death risk policy, with pay-outs doubled in the event

of accidental death. In 2008, the cooperative security policy (CSP) a ten year term combined saving and

death risk policy, was launched. Currently, 1,700 CSPs are in force, for members of 66 SACCOS.

NEFSCUN is continuing to discuss with its member credit unions ways in which it can develop its

microinsurance offerings, most recently at a training event for SACCOS staff and members held in January

this year. Nefscun’s aim is to encourage more SACCOs to provide this additional service package to their

members, which they say helps increase individual members’ sense of security. The insurance can be

obtained via flexible premium payments, with claim handling undertaken by the SACCOS themselves.

Among challenges identified by NEFSCUN are the lack of awareness of insurance among members, the

lack of a culture of risk mitigation, the lack of reliable data and the conflict which Nepal has experienced

in recent years.

18

helping Out in times Of needthe asKi Mutual benefit association in the Philippines has

drawn attention to the individual human stories behind the

provision of microinsurance, in reporting the experience of one

of its policyholders Shirley Viernes, 39, who lives in the town of

Pantabangan. Shirley was an ASKI client of four years’ standing

when in 2010 her husband was diagnosed with cancer.

Like any loving wife, Shirley did everything she could to finance

her husband’s medical treatment. She borrowed money wherever

she could and got deeper into debt. Sadly, despite these efforts, her

husband succumbed to cancer and died in late 2010.

Whilst lenders demanded their money from Shirley immediately

after the funeral, ASKI by contrast gave money to her. A beneficiary

of her husband’s insurance plan, ASKI MBA provided Shirley with

USD 473 in insurance benefit. This helped her settle some of her

loans and gave her peace of mind.

ASKI reports that Shirley and her family are on their way to

recovery. Her daughter, a third year college student, helps provide

income to the family by selling beauty products and electronic

phone services to her school mates. For her part, Shirley works full

time on a vegetable growing and charcoal trading business.

Manuel Gola, ASKI MBA president, says that his company now pays

claims within twenty-four hours of claims being made following

death.

wOmen’s cOOperative in nepal Offers access tO health prOtectiOnKirtipur Mahila eKata sahaKari sanstha (Kirtipur

woMen united Multi purpose cooperative society,

KwuMpcs) was established in 2007 under the cooperative law

of Nepal by a group of women who were aiming to improve local

women’s economic and social development. Kirtipur, one of the

historic places in Nepal, has a population of about 50,000.

KWUMPCS’s activities are targeted at women in low income

households working primarily in the informal sector. Members in

the cooperative include housewives, carpet workers, street vendors

and farmers as well as some local teachers and microentrepreneurs.

KWUMPCS pools the small amounts of money saved by local women

and utilises them in small scale, productive works that directly

involve women. In other words, KWUMPCS is serving as micro

saving and credit institution for those who have practical difficulties

in getting access to existing banks and large finance companies

in the locality, but who have enough capability and self confidence

to do something productive. At present, there are around 2,000

members in the cooperative, all women.

KWUMPCS is anxious to promote its members’ health, and has been

doing in this in various ways, including health awareness activities

and health camps focusing on children and on reproductive health.

it has also launched a micro health insurance scheme for members and their families. This

involves a partnership with the not-for-profit NGO Public Health

Concern trust (Phect-NEPAL), which runs the Kathmandu Model

Hospital, a 125-bed general hospital with specialized services in

the Capital City of Nepal as well as the Kirtipur Hospital, a 15-bed

hospital with maternity services in the locality.

Kathmandu Model Hospital, established in 1993, has a high

reputation for the quality of its care and treatment in Nepal. Phect-

NEPAL’s Community Health Insurance System is designed for

ensuring a quality and accessible health care services to low income

people. The scheme operates only through community based micro

cooperative institutions, such as KWUMPCS.

icmif prosper issue 10 | june 2012 19

the rOle Of mutual sOcieties in the extensiOn Of health prOtectiOn in africaMutual BeneFit societies in Africa can play

in providing health protection to their members.

This was the strong message which came out of a

conference in Abidjan, Cote d’Ivoire, in February this

year, organised by the International Association of

Mutuality and the Union of African Mutuality. The

conference provided an opportunity for African

mutuals to reassert their common values.

In countries where the majority of the population is

not covered by compulsory health insurance, people

face very high health expenses. Mutual benefit

societies can help in many ways. Firstly, mutuals’

membership subscriptions spread the financial

risk and avoid the huge expenses which come at

the time when medical treatment is needed. Unlike

commercial insurers, mutuals are not-for-profit and

their objective consists of meeting the needs of their

members instead of looking for financial returns.

For this reason, they are likely to provide insurance

coverage to the sectors of the population which are

not profitable from an economical point of view.

This principle of solidarity implies that the

populations considered ‘at risk’ because of their age

or their health will not be excluded from the mutual

system but will receive the same services for a similar

price as others. Finally, mutuals are often linked to

preexisting communities of interest, and as such

promote social cohesion and give a high sense of

responsibility to members. Policyholders have a right

to vote and acquire a better understanding of their

rights.

The practical benefits of participation in a health

mutual have been borne out in a new report from the

University of Montreal. The report, which focuses on

Benin, found that members used health care more

often than non-members and that medical costs

were lower. Typically, the cost of a birth was 30% lower for mutual members, at around FcFA 9,000 (us$ 18), compared with FcFA 12,500 (us$ 25) for non-members. Hospitalisation cost on

average 40% less for members.

There were other benefits. One significant change

is that members were better informed about their

rights, which enabled them to reject and denounce

abuses (such as requests for bribes) from health

workers and thus improve the quality of the service

they received.

Participants at the February conference heard

detailed presentations of the spread of mutual benefit

societies in several African countries. In Rwanda, for

example, 91% of the population are now covered by

thirty locally based health mutual benefit societies, a

massive increase from 2003 when the percentage was

only 7%. The change follows a 2007 law which obliges

Rwandans to subscribe to a health insurance service.

Subscriptions, set by the government at USD 1.90 per

year, are co-financed by members of the mutual and

20

the State. A little over a quarter of the population,

those who are the poorest, have their subscription

paid for the international financing institution the

Global Fund.

In Mali, where only a little part of the population

(mainly public servants and wage earners) are

covered by a compulsory health system, health

mutuals provide help for about 330,000 people.

There are 703 locally based town mutuals, sixty

mutual unions, nine regional federations as well

as the umbrella national federation. As in Rwanda,

subscriptions to health mutuals are co-financed, with

half paid for by members and half by the state

Nevertheless, despite the advantages, the mutual

insurance system faces three main challenges: the

poverty of the population, their lack of information

and the poor quality of care services. The financial

contribution, even reduced, remains the principal

barrier to their membership. A 2005 report for the

International Labour Organization found for example

that in Ghana, despite a 75% subsidy towards

premium costs, many people could not even carry the

costs associated with the photograph needed for the

insurance card.

The penetration of mutuals also remains low, because

many people are not familiar with the mutual system.

In Tanzania, as part of the Community Health Fund,

districts are supposed to pay the premiums of the

rural households in poor areas. However, a 2007

survey showed that the poor population did not know

about their tax-exempt contribution.

We can conclude, therefore, that people who are members of mutuals benefit from significant advantages in terms of access to care services, cost savings, greater understanding of the health system, and social links. Thanks to the principles of solidarity and

non-profit orientation, mutuals can cover the poor,

the elderly and those who are ill who would never be

covered by commercial insurers.

Despite all these benefits, important work on public

awareness needs to be done to expand the mutual

system and make it better known. Governments need

to make a political and financial commitment, as in

Rwanda, to support these developments..

Information about the abidjan conference can be found at:

http://www.MuGeF-ci.coM/jour-present.php. with videos available at:

http://www.MuGeF-ci.coM/jour-plus-video.php. the university oF Montreal report Mentioned aBove can Be downloaded FroM http://www.vesa-tc.uMontreal.ca/pdF/2011/noveMBre/Mutuelles_Benin_weB.pdF.

opening ceremony of the conference in

abidjan with Mr jean Philippe huchet (left)

icmif prosper issue 10 | june 2012 21

twenty and counting: the library of videos available on icmif’s new microinsurance website (www.microinsurance.coop) is growing rapidly in number and already proving a valuable source of key business information. they include interviews primarily with chief executives of icmif member firms in latin america, africa and asia, and offer an insight into the key issues facing these firms.

GROwING vIDEO LIbRARy IS A vALUAbLE RESOURCE

22

“There is a real benefit in hearing senior executives talk openly

about the challenges they are encountering and the strategies they

are adopting,” says Marine Guais, ICMIF’s Research Assistant who

has undertaken many of the interviews. “Video is rapidly proving

a vital resource for internet users, and we’re proud that ICMIF’s use

of this new technology is already so popular.” She adds that the

bank of video interviews provide a quick introduction to the work

of member firms. The interviews with Latin American executives are

conducted in Spanish, with English subtitles available. Conversely,

Spanish subtitles are available for several of the English language

videos. Users can switch subtitles on and off using the ‘CC’ button

on the video tool bar.

The interviews cover a range of topics. aMilcar ivan córdoBa

oF seGuros Fedpa (panaMa), (pictured above left) discusses

the development of the Latin American Reinsurance Group

(LARG) in a joint interview with LARG’s coordinator Martha

julia de Marroquín, (pictured above right) , for example.

They discuss how cooperatives and mutuals from several Latin

American countries have successfully banded together to meet

their reinsurance needs. Amilcar Córdoba stresses that LARG

works because it is based on shared interests: “It’s easier to work

on the basis of things we have in common than on the basis of our

differences. All cooperative companies have a lot in common, and

this is what we must look for,” he says.

Another joint interview features daniel spessot (la seGunda,

arGentina) and carMen BarBoZa, General ManaGer

at tajy (paraGuay), two ICMIF members who are engaging in

an innovative transborder partnership to develop agricultural

insurance. Daniel Spessot emphasizes that the effectiveness of the

collaboration depends very much on the two organisations having

shared cooperative values.

Several of those interviewed discuss their experiences of

introducing new products. Francisco Morales (coopseGuros,

ecuador), for example, discusses how his firm has begun to

offer medical and dental health cover. “There are clinics in the

country which can cost you from around twenty to sixty dollars,

and people don’t have the money for this. This is why they’ve gone

for self-healing, or to pharmacies and simply administered drugs

themselves, and all this has done has been to make their problems

worse,” he explains. Coopseguros has been able to introduce

insurance cover which enables policyholders to access medical and

dental help when they need it. “People pay a very, very small sum

each month in order to have free access to these clinics,” he adds.

The challenge of bringing insurance products to those on low

incomes including those who are working in the informal economy

is discussed in many of the interviews. For example arlene

saBaris, General ManaGer at coop seGuros (doMinican

repuBlic), (above) says that the development of microinsurance is

now an important part of her firm’s current five year strategy. “It’s

going to be a very big step. We have more than 700,000 members

within our cooperatives base, so we will be able to reach many

people through this. In our five-year plan we aim to reach this

population, with a growth of at least 30%,” she explains.

cleMente jaiMes puentes, executive president at

la equidad (coloMBia), discusses the challenge of finding

appropriate distribution channels for microinsurance. “We

developed a project back in 2004, mainly supported by US Aid,

that helped us identify the needs of the lowest-paid sectors of the

population and to design products to deliver to these sectors. The

critical point was to determine what distribution channel to use.

In fact, this has been a major challenge: to discover a channel with

the least possible cost, to be able to offer low premiums,” he says.

Among other distribution networks, La Equidad makes use of the

reach of the state-owned Agricultural Bank of Columbia.

For Sabbir Patel, ICMIF Senior Vice-President, the video interviews

are an important additional feature of ICMIF’s work. “One of icmiF’s key roles is to help in the exchange of business information and ideas between member firms, and we believe these videos will be another way to help bring this about,” he says. “There is also a direct opportunity for members to use

the video interviews as part of a benchmarking exercise, to compare

their performance and strategies against those of other member

firms.”

The interviews can be accessed directly at:

hTTp://WWW.yOuTube.cOm/useR/icmiFmicROinsuRAnce or

hTTp://WWW.micROinsuRAnce.cOOp.

icmif prosper issue 10 | june 2012 23

PartICIPants get to grIPs WIth the mICroInsuranCe busIness

three years were magically squeezed into two

busy but productive days for the participants taking

part in a microinsurance simulation exercise held

immediately before the main ICMIF conference in

Manchester.

ICMIF’s bespoke AGILE simulation tool, already used

widely by ICMIF members as a training tool in the

challenges of running an insurance business, has

now been specially reprogrammed to simulate the

challenges of operating in the microinsurance field.

The Manchester event, well attended with participants

from Asia, Africa, Europe and the Americas, was the

first time that the new version of AGILE had been

tried out for real, and ICMIF’s Mike Ashurst admits

that he had a certain nervousness in advance of

the workshop. “Yes, we were concerned that people

wouldn’t get into the simulation, but in fact the

participants got to grips with it very quickly. I was

very pleased with the way it went,” he says.

The workshop was structured to allow time not

only for AGILE, which simulated the first three

years of a microinsurance operation, but also for

informal presentations and round-table discussions

on aspects of microinsurance. The mix generally

seemed to be appreciated by the delegates, some of

whom were from ICMIF members already engaged

in microinsurance and some from organisations

interested in developing this area of work.

“I came with an open mind because I’d never worked

in microinsurance, so I wanted to acquire as much denis garand, facilitating the event

24

knowledge as possible, and this simulation was

absolutely fantastic for me. Then, people coming

from different parts of the world, working in

microinsurance, sharing their information and their

ideas was very enriching and very enlightening at

the same time,” said Asif Khan of IFFCO TOKIO (India),

one of the participants.

His comments were echoed by Aashiq Aminuddin

from ICMIF Sri Lanka member Amana Takaful. “The simulation brought us together and we had opportunity to share our learning from home, and also to be able to apply it in a scenario on the computer and see where we were going wrong, and what was going right. It challenged us to look at all aspects of

the company, not only the product and the pricing,

the market and the coverage, but also the finances,

liquidity and solvency and so many other variables of

running the business,” he said.

Greg Grothe from US based mutual Thrivent also paid

tribute to the facilitators. “They had a tremendous

amount of wealth of knowledge and experience,” he

said.

“As a facilitator, one of the most exciting aspects

of the workshop was seeing participants with

different backgrounds working together to make

organizational decisions. How often do we see a

representative from each department (marketing,

actuary, CEO and various managers) interacting to