0.440 160 january 3, 2016 statistics jumbo group ltd

TRANSCRIPT

January 3, 2016

Consu

mer

Sta

ple

s Sin

gapore

SEE PAGE 43 FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS Co. Reg No: 198700034E MICA (P) : 099/03/2012

Gregory Yap [email protected] (65) 6231 5848

Jumbo Group Ltd (JUMBO SP)

Give Me More Of This Crab

Initiating coverage: BUY to SGD0.58 TP

Jumbo’s highly-profitable seafood restaurants and signature crab dishes

are much loved in Singapore and now, being successfully exported to

China where it has three outlets. With its far bigger market potential and

high ROI, there is room to add one new outlet in China a year as new

outlets fully recoup investments in just 1-3 years. Jumbo deserves a

premium to peers for its uniquely-Singapore brand and product and first-

mover advantage in China. We initiate coverage with a BUY and DCF-P/E

blended TP of SGD0.58.

Bringing a uniquely Singapore dish to China

Jumbo’s expansion in China is just beginning. The mainland Chinese have

taken to chilli crabs in droves, and we think this expansion will provide

years of double-digit growth to come. We project accelerating earnings

growth of 9%/11%/20% in FY16E-18E, driving China from a 10% market

now to 32% of revenue by FY18E. By our estimates, its China outlets are

capable of generating ROI of 32-86% with a relatively short payback

period of 1-3 years which reduces risk.

More than just crabs that can travel

Jumbo has demonstrated that it can successfully replicate its seafood-

restaurant business in China. But it has other dining concepts (eg hotpot,

Teochew cuisine, bak kut teh) that can be exported overseas as well, not

just in China but the rest of South-east Asia. Gross margins for all its

brands run in the 40-60% range, and with scale, we see room for upside.

Deserving of a tasty premium

We value Jumbo at SGD0.58 for c.40% potential upside. We use blended

P/E and DCF valuations to capture the full value of its mid-term

expansion potential. This values Jumbo at 25x FY16E, 22x FY17E and 19x

FY18E EPS, a slight premium to its regional peers. Our DCF valuation of

SGD0.65 is conservative, assuming a higher-than-usual 10% market return

and 1.2x beta for possibly higher risks from its China expansion.

Good growth, high margins, strong cashflow: What more can you ask for?

Share Price SGD 0.43

12m Price Target SGD 0.58 (+36%)

BUY

Company description

Statistics

52w high/low (SGD)

3m avg turnover (USDm)

Free float (%)

Issued shares (m)

Market capitalisation

Major shareholders:

57.9%

6.6%

6.2%

641

3.8

F&B retailer in Singapore and China, most famous for

its chilli crabs and JUMBO Seafood brand JPOT

Hotpot. Has five other brands in its stable.

JBO Holdings

Mr Tan Gee Jian

Orchid 1 Investments

na/na

24.3

SGD272.6M

USD193M

Price Performance

90

100

110

120

130

140

150

160

0.300

0.320

0.340

0.360

0.380

0.400

0.420

0.440

Nov-15 Nov-15 Nov-15 Nov-15 Dec-15 Dec-15 Dec-15 Dec-15

Jumbo Group Ltd - (LHS, SGD) Jumbo Group Ltd / Straits Times Index - (RHS, %)

-1M -3M -12M

Absolute (%) 8 na na

Relative to index (%) 6 na na

Source: FactSet

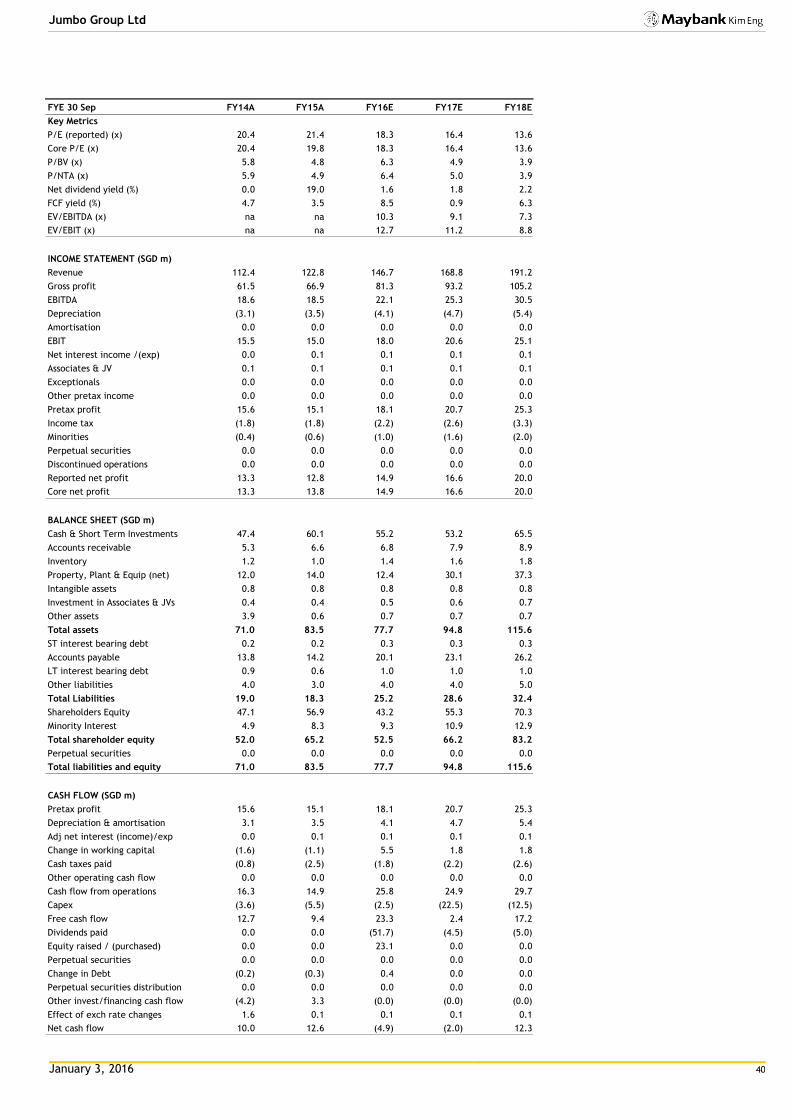

FYE Sep (SGD m) FY14A FY15A FY16E FY17E FY18E

Revenue 112 123 147 169 191

EBITDA 19 18 22 25 31

Core net profit 13 14 15 17 20

Core EPS (cts) 2.1 2.1 2.3 2.6 3.1

Core EPS growth (%) 39.8 3.0 8.6 11.1 20.5

Net DPS (cts) 0.0 8.1 0.7 0.8 0.9

Core P/E (x) 20.4 19.8 18.3 16.4 13.6

P/BV (x) 5.8 4.8 6.3 4.9 3.9

Net dividend yield (%) 0.0 19.0 1.6 1.8 2.2

ROAE (%) 31.8 26.4 29.8 33.7 31.8

ROAA (%) 20.8 17.8 18.5 19.2 19.0

EV/EBITDA (x) na na 10.3 9.1 7.3

Net debt/equity (%) net cash net cash net cash net cash net cash

Consensus net profit - - na na na

MKE vs. Consensus (%) - - na na na

0%

10%

20%

30%

40%

50%

60%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

FY15 FY16E FY17E FY18E

(SGD'000)

Net cash Free cashflow

Core NP growth (RHS) Gross margin (RHS)

January 3, 2016 2

Jumbo Group Ltd

Company Proposition

A restaurant operator whose greatest value proposition is

ability to generate high demand for its business with

reasonable prices and consistent taste.

Iconic dishes, footprint of outlets in ideal locations, strong

brands and effective front- and back-end operations

provide high defensible margins.

Branding and identity that hinge on signature seafood such

as chilli crab, a national dish. Helps it stand out in

crowded markets especially when expanding overseas.

Low-cost cash business financed by suppliers’ credit. High

FCF generation supports aggressive expansion plans yet

provides future dividend support for shareholders.

How Jumbo stacks up on profitability & returns

Source: FactSet estimates, Maybank Kim Eng

Price Drivers

Revenue breakdown

Source: Company data, Maybank Kim Eng estimates

Listed just in Nov 2015, trading history is too short to

identify inflexion points. We believe market will focus on its

opening of new outlets in China and/or introduction of new

dining concepts.

1. Second China JUMBO SEAFOOD outlet opened in Raffles

City Shanghai in Aug 2015.

2. Third China outlet opening in IFC Mall in Jan 2016.

3. Fourth China outlet assumed to open in Oct 2016.

4. Fifth China outlet assumed to open in Oct 2017, fourth

JPOT outlet in Singapore assumed to open in mid-FY17

Financial Metrics

Revenue growth. Given two new JUMBO outlets in China,

would expect to see increasingly stronger topline growth

in next 3-4 quarters, unless other brands underperform.

EBIT & net margins. Gross margin (excluding direct costs

such as food & rental) is controllable. There may be

quarters of higher start-up costs where margins fall below

trend, but generally expect good indirect cost

management and efficient tax planning.

Watch for deteriorating asset & liability turns. Strong FCF

generation comes from AP days far exceeding AR and stock

days. Don’t be alarmed if FCF is dragged down by capex.

Strong revenue growth with stable margins expected

Source: Company data, Maybank Kim Eng estimates

Swing Factors

Upside

Better-than-expected Singapore and China sales,

especially from new outlets.

Lower-than-expected food and staff costs that could lead

to better-than-expected margins.

Expectations of higher dividends or articulation of a

dividend policy.

Downside

Any changes in China’s food safety laws that could affect

China’s import of mud crabs.

Shortage of critical ingredients for its signature dishes:

crabs, other seafood.

Epidemics or health scares that can damage its

reputation or cuisine eg mass food poisoning, salmonella.

(6.0)

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

(70.0) (60.0) (50.0) (40.0) (30.0) (20.0) (10.0) 0.0 10.0 20.0 30.0 40.0

Avg 3Y ROE

Avg 3Y Net Margin

JumboJapan Foods

ABR Holdings

Soup Restaurant

BreadTalkSakae Holdings

Auric Pacific

Tung Lok

Flagship brands:Jumbo - JUMBO SEAFOODJapan Foods - Ajisen RamenABR - Swensen's, Gloria Jean's CoffeesSoup Restaurant - SOUPBreadTalk - Din Tai Fung, Carl's JrSakae Holdings - Sakae SushiAuric Pacific - Delifrance, Food JunctionTung Lok - TungLok, Lao Beijing

12.2% 12.3% 12.2% 13.2%10.4% 10.2% 9.8% 10.4%

9%

19%

15%

13%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

FY15 FY16E FY17E FY18E

EBIT margin Net margin Revenue growth

1

1 2 3 4

January 3, 2016 3

Jumbo Group Ltd

Fig 1: SWOT Analysis

Strengths

Strong branding in Singapore, widely known by locals.

Outlets well-located in key tourist hotspots.

14 restaurants in Singapore, two in China with five brands.

Front-end optimises diner-capture and outlet utilisation.

Back-end centralises cooking and food preparation.

Consistent taste of dishes through standardised

preparation of ingredients lowers staffing cost.

Weaknesses

Limited differentiation of menu, especially signature

seafood dishes.

Supply of seafood, especially crabs, may be affected by

disease or closure of source markets.

Rental costs may escalate, especially as expansion is

taking it into REIT-controlled malls.

Opportunities

Strong reception in China. Room to grow number of

outlets in Shanghai.

Capitalise on rising food-safety awareness in China as a

well-regarded Singapore brand.

Other brands can also be exported to China or South-east

Asia.

Expansion into higher-margin catering business.

Threats

New outlets or brands fail to take off.

Fluctuation of food cost (80% of COGS), especially seafood

which account for 70-80% of revenue.

Adverse food-safety developments could hurt revenue and

brand value.

Change in consumer tastes and preferences or sharp drop

in tourist arrivals could affect demand.

Source: Company data, Maybank Kim Eng

Fig 2: Porter’s Five Forces Model Analysis

Source: Company data, Maybank Kim Eng

Bargaining power of suppliers:

Low Top three seafood suppliers account

for less than 20% of COGS. Other fresh

ingredients are freely available on

the market.

Industry competition: High

Seafood restaurant business is fragmented. Jumbo’s biggest value proposition is in fair transparent prices and consistent taste that keeps customers coming back.

Bargaining power of

customers: Medium

Buyers can vote with their feet and wallets. However, Jumbo’s 48,000-member loyalty program acts to

dilute buyer power.

Threat of substitutes: Low

No substitute for signature chilli crab

which is a national dish of Singapore.

Threat of new entrants: Low-to-Medium

Anyone can start a seafood restaurant, but not many have as large a footprint as Jumbo or its

strong branding.

January 3, 2016 4

Jumbo Group Ltd

Table of Contents 1. Investment thesis 5

1.1 Deserving of a tasty premium 5

1.2 Catalyst #1: China expansion the main growth driver 5

1.3 Catalyst #2: More than just crabs that can be exported 5

1.4 Catalyst #3: May pay more dividends to get fatter ROEs 5

2. Company Background 6

2.1 The seafood specialist 6

2.2 Among the top 10 players locally 7

2.3 Taking the chilli crab to the hairy crab kingdom 7

2.4 Other hot & spicy brands that can also be exported 8

3. Industry Potential 10

3.1 Singapore on the global foodie’s trail… 10

3.2 …with crab at the top of the menu 11

3.3 China bursting with potential 11

4. Growth Drivers 13

4.1 Expand further in China 13

4.2 Attractive locations secured in China 14

4.3 Part of the solution for China’s retail challenges 16

4.4 Export other brands to the region 17

4.5 Acquisitions, JVs or strategic alliances 17

5. Barriers to Entry 18

5.1 Competitive with a clear path to growth 18

5.2 Food quality & safety a key mantra 18

5.3 Expand central kitchen & IT to enhance scalability 19

6. Forecasts & Assumptions 21

6.1 Sales to grow by 16% CAGR, NP 13% in FY16E-18E 21

6.2 China to be the main growth driver 21

6.3 Optimistic on China expansion 22

6.4 Singapore a sturdy mainstay 23

6.5 Why do we believe future expansion will favour JUMBO and JPOT? 23

6.6 Overall revenue assumptions 24

6.7 Margin trends should be stable 25

6.8 Well-financed, capex not a concern given ample FCF 26

6.9 Can afford to pay more dividends 27

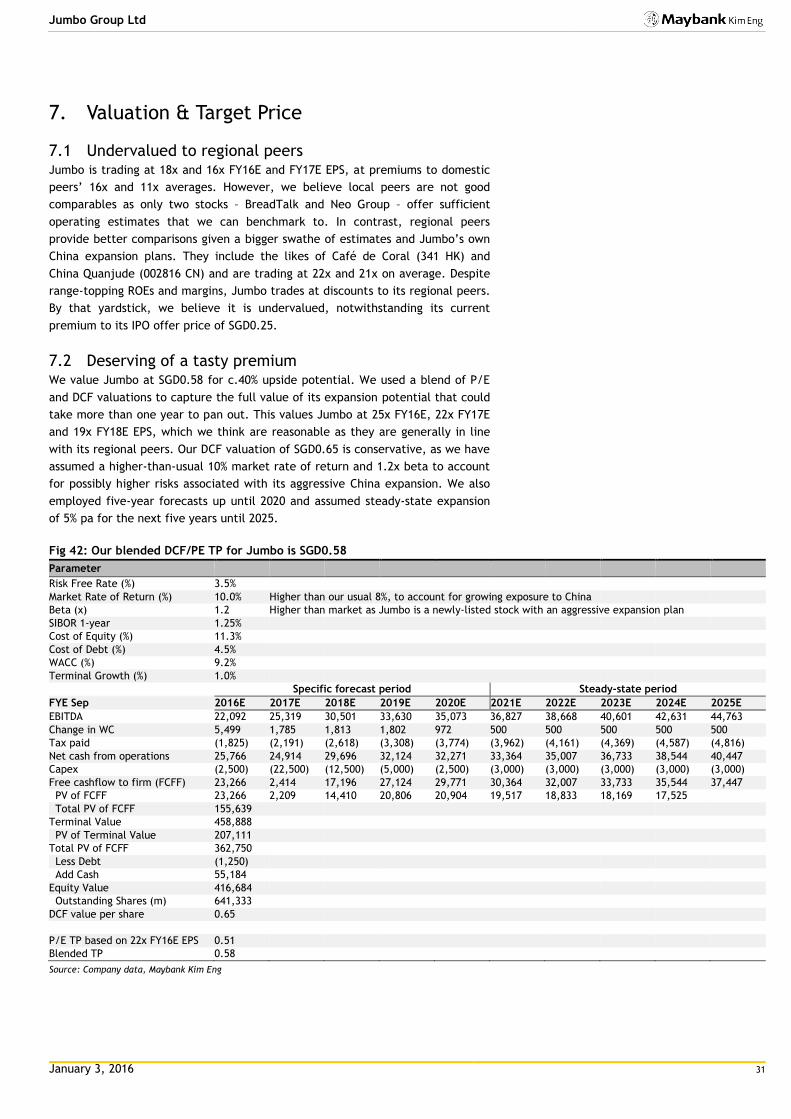

7. Valuation & Target Price 31

7.1 Undervalued to regional peers 31

7.2 Deserving of a tasty premium 31

8. Risks & Concerns 34

8.1 Singapore tourism down but not a dealbreaker 34

8.2 Must keep reputation intact at all costs 34

8.3 Crab shortages 35

8.4 Possible earnings volatility until new outlets mature 35

Annex I: Listing Details 36

Annex II: Board of Directors/Senior Management 36

Annex III: Shareholding Details 39

January 3, 2016 5

Jumbo Group Ltd

1. Investment thesis

Restauranteur Jumbo Group is the leading brand in Singapore’s seafood

dining industry which accounts for 80% of its revenue. Its signature dishes

– chilli crab and black pepper crab – are widely available in Singapore,

varying only with the creativity of the chef. Singapore lays claim to chilli

crab as a “uniquely Singapore” dish, prompting other Southeast Asian

countries such as Malaysia to also lay claim to it as their own. For

investors, however, it is not so much the formulation or origin of this dish

but Jumbo’s brands, execution, well-tested systems and growth strategy

that merit investment. We forecast accelerating earnings growth of

9%/11%/20% in FY16E-18E, underpinned by expansion in China, and

initiate coverage with a BUY and blended DCF-P/E TP of SGD0.58.

1.1 Deserving of a tasty premium We value Jumbo at SGD0.58 for c.40% upside potential. We use blended

P/E and DCF valuations to capture the full value of its expansion prospects

that should take more than a year to pan out. This values Jumbo at 25x

FY16E, 22x FY17E and 19x FY18E EPS, a slight premium to its regional

peers. We think this is reasonable. Our DCF valuation is conservative, as

we have assumed a higher-than-usual 10% market rate of return and 1.2x

beta to account for possibly higher risks associated with its aggressive

China expansion. We employed five-year forecasts up until 2020 and

assumed steady-state expansion of 5% pa until 2025.

1.2 Catalyst #1: China expansion the main growth driver China is expected to generate the biggest revenue and earnings growth for

Jumbo, justifying the addition of four outlets in FY15-FY18E, of which two

have been confirmed for FY15-FY16E. The early results have been

overwhelmingly positive for Jumbo. China accounted for 6% of group

revenue in the year that its first outlet opened in FY14. This number

climbed to 9% by the second year in FY15, all from just one outlet in

Shanghai. Profitability was achieved by the end of the first year. The

additional outlets we have forecasted are expected to lift China’s revenue

contributions to 32% by FY18E, with the biggest jump in FY16E from two

new outlets in Aug 2015 and Jan 2016 respectively.

1.3 Catalyst #2: More than just crabs that can be exported While Jumbo’s seafood business can be easily replicated in different

markets, it has four other brands in Singapore that we think can be

profitably exported overseas as well. Gross margins for all its brands run

in the 40-60% range and with scale, we see room for upside. Financing

expansion capex is not a problem at all. Jumbo generates solid cash flows

as it’s mostly a cash business with almost no credit terms. Nothing is kept

in stock for long, and what’s more, suppliers are financing its business, by

giving Jumbo c.30 days of credit.

1.4 Catalyst #3: May pay more dividends to get fatter ROEs Jumbo intends to pay out at least 30% of its annual earnings as dividends

in FY16-17. On our part, we think it can afford to pay more as by our

estimates, its ROE could be dragged down if it does not do so, given the

ample amount of FCF that it generates. We currently forecast ROE

declining from 30% in FY17E to 28.4% in FY18E assuming a 30% payout

ratio. However, if it pays out 50%, ROEs should remain stable at 31-32% in

FY17E-18E. If so, dividend yield should rise from <2% to 3% in FY16E and

closer to 4% by FY18E.

In this report, Jumbo refers to Jumbo Group the listed company, while JUMBO or JUMBO SEAFOOD refers to its seafood restaurant brand only.

January 3, 2016 6

Jumbo Group Ltd

2. Company Background

2.1 The seafood specialist Jumbo is one of Singapore’s leading multi-concept dining establishments.

Arguably, it has done more than its fair share to put Singapore on the world

culinary map, with its signature chilli and black pepper crabs. JUMBO SEAFOOD

outlets are popular with both locals and tourists. A quick search on

tripadvisor.com.sg for Singapore chilli crab throws up three of JUMBO SEAFOOD’s

five restaurants among the top 10. While there are no estimates from the

company, our eyeball estimates suggest a 50/50 local/tourist customer

composition for Jumbo. Anecdotally, it is usually the first stop on the dining trail

of tourists. We observe that its outlets remain crowded in fair and foul weather,

including the annual haze in Singapore.

Fig 3: Tripadvisor search rankings for Singapore chilli crab

Ranking Restaurant

1. Jumbo Seafood, East Coast Seafood Centre

2. Jumbo Seafood, Riverside Point

3. No Signboard Seafood, Geylang

4. Long Beach, East Coast Parkway

5. No Signboard Seafood, Esplanade

6. Jumbo Seafood, Dempsey

7. Long Beach, Dempsey

8. Mellben Seafood, Ang Mo Kio

9. Red House Seafood, Robertson Quay

10. Palm Beach Seafood, Fullerton

11. Chinatown Seafood, Trengganu Street

12. Eng Seng Restaurant, Joo Chiat

13. Forum Seafood, Boat Quay

14. Newton Hawker Centre

15. The Halia, Raffles Hotel

Source: www.tripadvisor.com.sg, accessed 23 Nov 2015

Fig 4: Jumbo’s award-winning chilli crab

Source: Company

The first JUMBO SEAFOOD outlet was opened in 1987 at the East Coast Seafood

Centre. This is still its largest, with a 1,250-pax capacity. It is also its most

profitable, by our reckoning, given its location. Jumbo opened four more outlets

in Singapore in 2002, 2004, 2006 and 2008. Its five restaurants in Singapore today

prepare more than 1.5m tonnes of crabs each day for hordes of hungry diners.

Average pax spending, according to a local foodie website, Hungrygowhere, is

SGD79. This is the highest in the group’s stable of five dining concepts.

Fig 5: JUMBO SEAFOOD restaurants in Singapore and China

No. of diners GFA (sf) Opened in

Singapore

- East Coast Seafood Centre 1,250 20,484 1987

- Riverside Point 280-300 5,447 2002

- The Riverwalk 280-300 5,965 2004

- NSRCC SAFRA @ Changi 280-300 7,309 2006

- Dempsey Hill 280-300 6,129 2008

China

- IAPM, Shanghai 250 12,239 2013

- Raffles City, Shanghai (new outlet) 200 7,368 Aug 2015

- IFC Mall, Shanghai (new outlet) 150 6,997 Jan 2016

Source: Company data, Maybank Kim Eng

January 3, 2016 7

Jumbo Group Ltd

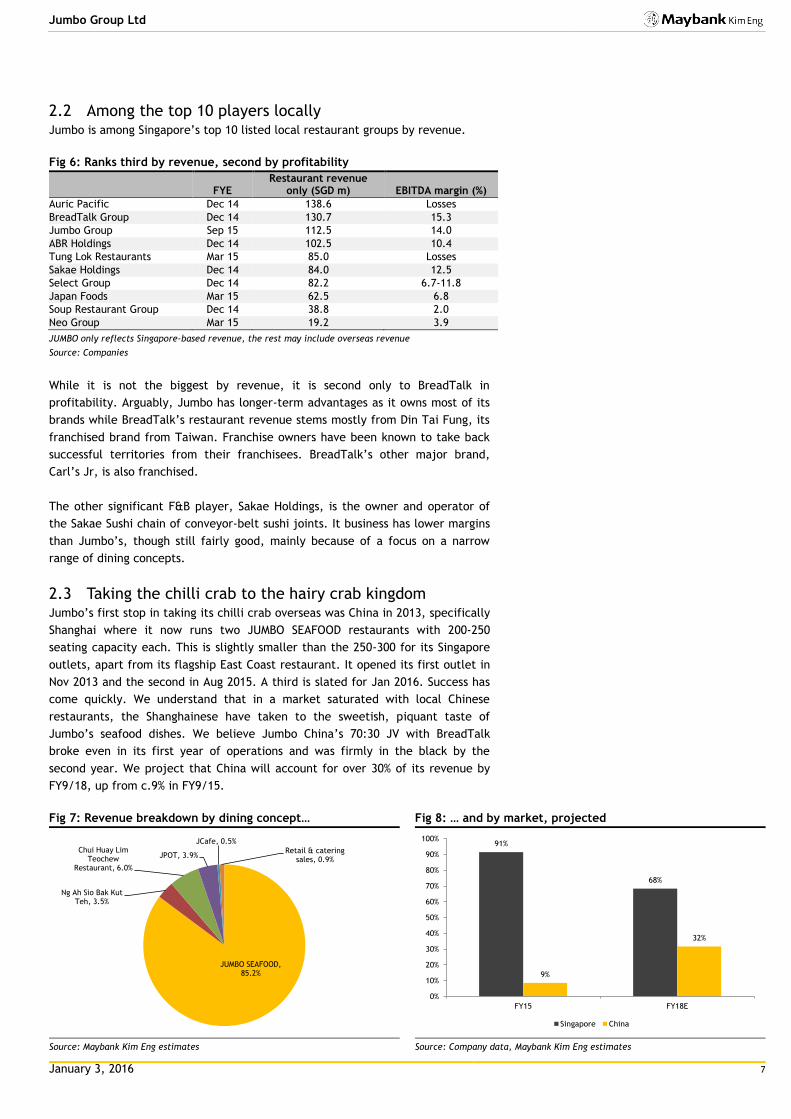

2.2 Among the top 10 players locally Jumbo is among Singapore’s top 10 listed local restaurant groups by revenue.

Fig 6: Ranks third by revenue, second by profitability

FYE Restaurant revenue

only (SGD m)

EBITDA margin (%)

Auric Pacific Dec 14 138.6 Losses

BreadTalk Group Dec 14 130.7 15.3

Jumbo Group Sep 15 112.5 14.0

ABR Holdings Dec 14 102.5 10.4

Tung Lok Restaurants Mar 15 85.0 Losses

Sakae Holdings Dec 14 84.0 12.5

Select Group Dec 14 82.2 6.7-11.8

Japan Foods Mar 15 62.5 6.8

Soup Restaurant Group Dec 14 38.8 2.0

Neo Group Mar 15 19.2 3.9

JUMBO only reflects Singapore-based revenue, the rest may include overseas revenue

Source: Companies

While it is not the biggest by revenue, it is second only to BreadTalk in

profitability. Arguably, Jumbo has longer-term advantages as it owns most of its

brands while BreadTalk’s restaurant revenue stems mostly from Din Tai Fung, its

franchised brand from Taiwan. Franchise owners have been known to take back

successful territories from their franchisees. BreadTalk’s other major brand,

Carl’s Jr, is also franchised.

The other significant F&B player, Sakae Holdings, is the owner and operator of

the Sakae Sushi chain of conveyor-belt sushi joints. It business has lower margins

than Jumbo’s, though still fairly good, mainly because of a focus on a narrow

range of dining concepts.

2.3 Taking the chilli crab to the hairy crab kingdom Jumbo’s first stop in taking its chilli crab overseas was China in 2013, specifically

Shanghai where it now runs two JUMBO SEAFOOD restaurants with 200-250

seating capacity each. This is slightly smaller than the 250-300 for its Singapore

outlets, apart from its flagship East Coast restaurant. It opened its first outlet in

Nov 2013 and the second in Aug 2015. A third is slated for Jan 2016. Success has

come quickly. We understand that in a market saturated with local Chinese

restaurants, the Shanghainese have taken to the sweetish, piquant taste of

Jumbo’s seafood dishes. We believe Jumbo China’s 70:30 JV with BreadTalk

broke even in its first year of operations and was firmly in the black by the

second year. We project that China will account for over 30% of its revenue by

FY9/18, up from c.9% in FY9/15.

Fig 7: Revenue breakdown by dining concept…

Source: Maybank Kim Eng estimates

Fig 8: … and by market, projected

Source: Company data, Maybank Kim Eng estimates

JUMBO SEAFOOD, 85.2%

Ng Ah Sio Bak Kut Teh, 3.5%

Chui Huay Lim Teochew

Restaurant, 6.0%

JPOT, 3.9%

JCafe, 0.5%

Retail & catering sales, 0.9%

91%

68%

9%

32%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY15 FY18E

Singapore China

January 3, 2016 8

Jumbo Group Ltd

2.4 Other hot & spicy brands that can also be exported Besides JUMBO SEAFOOD, which we estimate makes up c.85% of its revenue,

Jumbo has acquired or built a host of other dining concepts. We believe they can

also be exported to other countries, especially JPOT to China and Ng Ah Sio Bak

Kut Teh or Chui Huay Lim to countries with similar food and receptive

populations such as Malaysia or Thailand.

Ng Ah Sio Bak Kut Teh. Established in 1955, Jumbo acquired 51% of Ng Ah

Sio Investments in 2010, which operates an established bak kut teh

restaurant on Rangoon Road. This restaurant specialises in a Singapore

Teochew dish known as “white pepper” bak kut teh, a savoury pork-rib soup

prepared with toasted white pepper and garlic. Jumbo has proven to be a

supportive shareholder. Ng Ah Sio now has four outlets, up from just one

before its entry. After Jumbo came onboard in 2010, it added an Ng Ah Sio

food stall at the Rasapura Masters food court in Marina Bay Sands the same

year. This was followed by more outlets at a shophouse in Tanjong Katong

and on the premises of the Chui Huay Lim Club - a private Chinese clan

association - in 2012. Prices average SGD13-14 per pax, according to

Hungrygowhere.

JPOT hotpot restaurants. This is a fresh take on traditional hotpot dining

with a range of Singapore-style soup bases such as laksa (coconut-based

curry soup), silky porridge, tom yum (Thai spicy soup) and bak kut teh

(savoury pork broth). Jumbo owns and operates three JPOT outlets in

Singapore, with capacity for 160-210 diners each. Jumbo started this dining

concept in 2009 and added two more outlets in 2012 and 2014. Situated in

Vivocity, Tampines 1 and Parkway Parade, close to major population centres

and tourist attraction Sentosa, JPOT enjoys a locational advantage. Despite

higher rentals in these malls which are owned by REITs, our channel checks

suggest quick table turns and lean operations. For example, the outlet in

Vivocity can seat more than 200 but is staffed by only a service crew of 10.

Diners order through iPads and food is delivered within minutes. We

estimate at least three turns per table per night. The outlet is crowded even

on weekday nights. Prices average SGD35 per pax, according to

Hungrygowhere.

Fig 10: JPOT’s outlets

No. of diners Opened in Mall owner

Singapore

- Vivocity 160-210 2009 Mapletree Commercial Trust

- Tampines 1 160-210 2012 Asia Retail Mall Fund

- Parkway Parade 160-210 2014 Parkway Parade Partnership Ltd - 46%-owned by NTUC Income, 33% by PGGM Real Estate Fund

Source: Company, Maybank Kim Eng

Chui Huay Lim Teochew Cuisine. Serving authentic Teochew cuisine, this

restaurant is located at the Chui Huay Lim club, a private clan association

for Teochew businessmen. It serves an extensive menu of classic Teochew

dishes and offers Teochew porridge with more than 20 side dishes during

lunch. Seating capacity is 1,000 with nine private dining rooms and two

banquet halls. Average pax spending is SGD50, according to Hungrygowhere.

J Café. The latest dining concept launched in 2014, essentially on the

golfers’ terrace of the National Service Resort & Country Club, J Cafe serves

Singapore hawker classics. As it is this should have been a package deal with

the JUMBO SEAFOOD restaurant on the same premises, its rentals may be

lower.

Fig 9: Average spend per pax

SGD

JUMBO SEAFOOD 79

Singapore Seafood Republic 65

Chui Huay Lim Teochew Cuisine 50

JPOT 35

Yoshimaru Ramen Bar 16

Ng Ah Sio Bak Kut Teh 13-14

J Café n/a

Source: www.hungrygowhere.com

January 3, 2016 9

Jumbo Group Ltd

Finally, Jumbo manages and invests in two other dining concepts: the Singapore

Seafood Republic (SSR) chain of Singapore-style seafood cuisine in Singapore and

Japan, and Yoshimaru Ramen Bar in Holland Village. It operates these through

two JVs: SRPL for the SSR outlets in Japan plus Yoshimaru in Singapore; and SSR

Singapore for the SSR outlet in Singapore. At the moment, their profit

contributions are booked under associates and are not significant.

January 3, 2016 10

Jumbo Group Ltd

3. Industry Potential

3.1 Singapore on the global foodie’s trail… According to the Singapore Tourism Board (STB), shopping and F&B spending

makes up the bulk of domestic tourism revenue, at 21% and 10% respectively.

Singapore is widely regarded as a top eating capital in the Asia Pacific, with

ample food haunts and trails. In recent years, its restaurant scene has

blossomed, with the number of restaurants up from 2,041 in 2008 to 2,480 in

2013, according to SingStat.

There were 6,751 F&B establishments in Singapore in 2013 with restaurants

accounting for about a third. While restaurants have not grown as quickly as

other segments such as catering, they account for the largest chunk of revenue

and are growing the fastest, especially chain restaurants that can exploit size

advantages when negotiating for rental space in Singapore’s REIT-controlled

shopping malls.

The gastronomy bar has also been raised with the entry of renowned chefs like

Joël Robuchon (L’Atelier and Joël Robuchon Restaurant at Resorts World

Sentosa), Tetsuya Wakuda (Waku Ghin at MBS), Jamie Oliver (Jamie’s Italian at

Forum and Vivocity) and Gordon Ramsay (Bread Street Kitchen).1

Fig 11: Restaurants comprise 37% of F&B establishments…

Source: SingStat

Fig 12: …and 40% of operating receipts

Source: SingStat

Fig 13: They have been growing the fastest of all the F&B operations

Source: SingStat

1 source: www.stb.gov.sg/industries/dining-and-retail

January 3, 2016 11

Jumbo Group Ltd

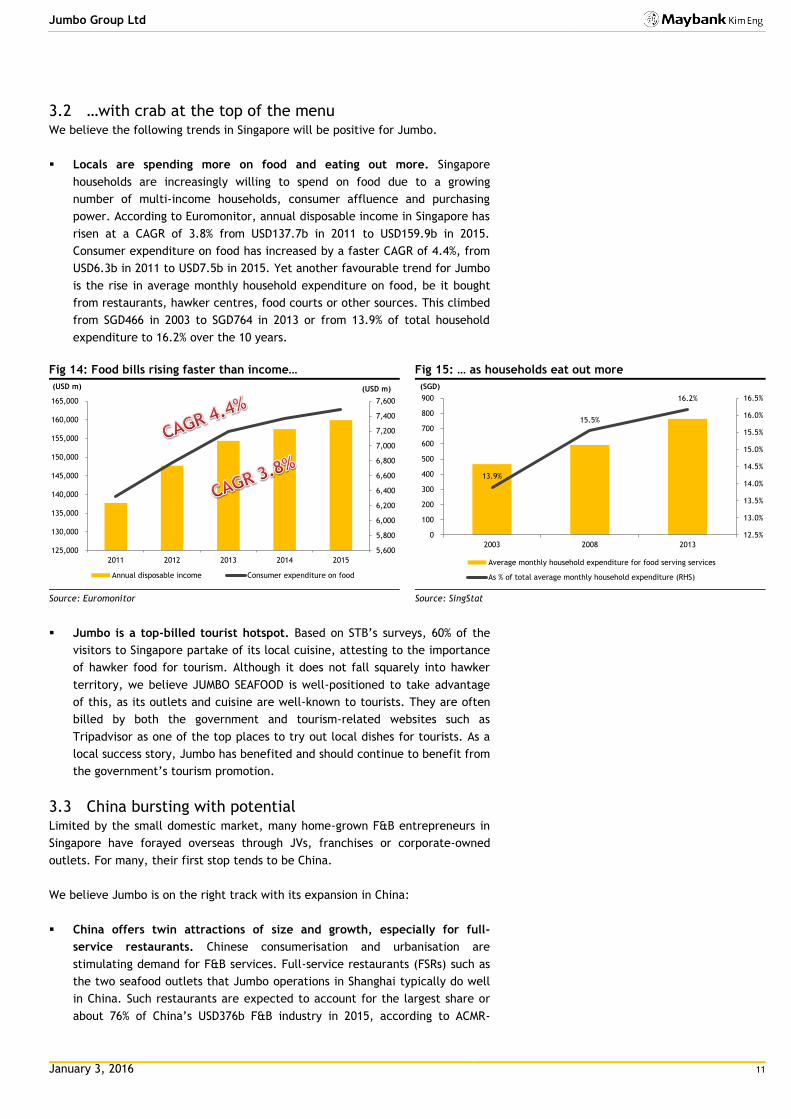

3.2 …with crab at the top of the menu We believe the following trends in Singapore will be positive for Jumbo.

Locals are spending more on food and eating out more. Singapore

households are increasingly willing to spend on food due to a growing

number of multi-income households, consumer affluence and purchasing

power. According to Euromonitor, annual disposable income in Singapore has

risen at a CAGR of 3.8% from USD137.7b in 2011 to USD159.9b in 2015.

Consumer expenditure on food has increased by a faster CAGR of 4.4%, from

USD6.3b in 2011 to USD7.5b in 2015. Yet another favourable trend for Jumbo

is the rise in average monthly household expenditure on food, be it bought

from restaurants, hawker centres, food courts or other sources. This climbed

from SGD466 in 2003 to SGD764 in 2013 or from 13.9% of total household

expenditure to 16.2% over the 10 years.

Fig 14: Food bills rising faster than income…

Source: Euromonitor

Fig 15: … as households eat out more

Source: SingStat

Jumbo is a top-billed tourist hotspot. Based on STB’s surveys, 60% of the

visitors to Singapore partake of its local cuisine, attesting to the importance

of hawker food for tourism. Although it does not fall squarely into hawker

territory, we believe JUMBO SEAFOOD is well-positioned to take advantage

of this, as its outlets and cuisine are well-known to tourists. They are often

billed by both the government and tourism-related websites such as

Tripadvisor as one of the top places to try out local dishes for tourists. As a

local success story, Jumbo has benefited and should continue to benefit from

the government’s tourism promotion.

3.3 China bursting with potential Limited by the small domestic market, many home-grown F&B entrepreneurs in

Singapore have forayed overseas through JVs, franchises or corporate-owned

outlets. For many, their first stop tends to be China.

We believe Jumbo is on the right track with its expansion in China:

China offers twin attractions of size and growth, especially for full-

service restaurants. Chinese consumerisation and urbanisation are

stimulating demand for F&B services. Full-service restaurants (FSRs) such as

the two seafood outlets that Jumbo operations in Shanghai typically do well

in China. Such restaurants are expected to account for the largest share or

about 76% of China’s USD376b F&B industry in 2015, according to ACMR-

5,600

5,800

6,000

6,200

6,400

6,600

6,800

7,000

7,200

7,400

7,600

125,000

130,000

135,000

140,000

145,000

150,000

155,000

160,000

165,000

2011 2012 2013 2014 2015

(USD m)(USD m)

Annual disposable income Consumer expenditure on food

13.9%

15.5%

16.2%

12.5%

13.0%

13.5%

14.0%

14.5%

15.0%

15.5%

16.0%

16.5%

0

100

200

300

400

500

600

700

800

900

2003 2008 2013

(SGD)

Average monthly household expenditure for food serving services

As % of total average monthly household expenditure (RHS)

January 3, 2016 12

Jumbo Group Ltd

IBISWorld. The market has grown by an 11% CAGR since 2010.2 FSRs are

particularly relevant for big cities such as Shanghai, which now offer a

dizzying variety of international cuisines to expats and an increasingly

wealthy local middle class. Shanghai alone has more than 58,000 restaurants

touting 10 regional and 11 international cuisines, according to EURObiz, the

European Union Chamber of Commerce in China.3

Singapore-style cuisine works in China. According to Jumbo, Singapore’s

cuisine has been warmly embraced by the Shanghainese, as its sweetish,

lightly-spicy taste contrasts well with local flavours that are heavily spiced

eg Sichuan or Beijing cuisine. Moreover, Shanghainese are used to eating

crabs, since they have their own hairy-crab dishes. Unlike the hairy crab

which comes into season only in Oct-Dec, Jumbo’s chilli crab is available all

year round. Still, as management is cautious about whether its crab-based

seafood would work outside Shanghai, we believe further expansion for

JUMBO SEAFOOD will be limited to Shanghai for now. Outside Shanghai,

Jumbo is likely to try out its other dining concepts.

Positive hotpot precedent for Jumbo. One dining concept that has found

favour in China is hotpots. We believe its successful expansion in the past

reflects well on Jumbo. The Mongolian hotpot chain, Little Sheep Group

acquired by YUM! Brands, is China’s second-largest FSR chain after Pizza

Hut. YUM!’s 2011 acquisition underscored China’s multi-tiered nature of

demand in China. While demand for high-end, Western-style dining options

from global chains is still significant and growing, Euromonitor believes there

remains untapped demand for more familiar and affordable offerings from

chains such as Little Sheep, which combine more familiar dishes with a

clean, consistent chain experience that is highly appealing. Jumbo’s chain of

hotpot restaurants in Singapore under its JPOT brand with Singapore-

flavoured soups could be brought into play in China at some point, in our

view. Given its high margins, we would not be surprised if Jumbo rolls out

JPOT as its second exportable brand in China sometime in the future.

2 http://www.ibisworld.com/industry/china/full-service-restaurants.html 3 http://www.eurobiz.com.cn/food-thought-investing-chinas-fb-industry/

January 3, 2016 13

Jumbo Group Ltd

4. Growth Drivers

4.1 Expand further in China In China, Jumbo will operate three JUMBO SEAFOOD outlets by FY9/16E.

JUMBO@IAPM Mall was opened in Nov 2013, JUMBO@ Raffles City in Aug 2015,

and JUMBO@IFC Mall will be opened in Jan 2016. The IAPM and Raffles City

outlets have received good reviews on www.dianping.com, China’s equivalent of

www.hungrygowhere.com, a popular restaurant review website in Singapore.

Although it was opened just a few months ago, JUMBO@Raffles City has already

notched up almost 1,000 reviews vs >3,400 for JUMBO@IAPM. Both have been

rated a maximum of five stars by reviewers and ranked above 9/10 for taste,

ambience and service.

Fig 16: JUMBO IAPM - 5 stars/3,666 reviews

Source: www.dianping.com/shop/13784702, as at 30 Dec 2015

Fig 17: JUMBO@Raffles City – 5 stars/1,117 reviews

Source: www.dianping.com/shop/24996989, as at 30 Dec 2015

With just one outlet in operation, China accounted for c.6% of revenue in FY14

and c.9% of revenue in FY15. We think it could contribute 32% by FY18E, after

the opening of two more outlets in China for a total of five.

Fig 18: Jumbo Seafood restaurants in China so far

No. of diners GFA (sf) Opened in

- IAPM Mall, Shanghai 250 12,239 2013

- Raffles City, Shanghai 200 7,368 Aug 2015

- IFC Mall, Shanghai (opening in Jan 2016) 150 6,997 Jan 2016

Source: Company data

Jumbo intends to fully capitalise on its brand strength to expand further. It hopes

to open at least four more restaurants in Singapore and China in the next 24

months. It may offer new or existing dining concepts ranging from high-end fine

to casual dining. It intends to use SGD12m or 30% of its IPO proceeds for this.

January 3, 2016 14

Jumbo Group Ltd

4.2 Attractive locations secured in China Jumbo appears to have formed a strong working relationship with Sun Hung Kai

Properties (SHK), which owns both the IAPM Mall and IFC Mall. IAPM Mall houses

its first outlet opened in Nov 2013 while IFC Mall will soon host its third in Jan

2016. SHK (16 HK) is one of the largest property companies in Hong Kong, owned

by the Kwok brothers. It has a strong presence in China as an owner and

developer of residential, office and hotel properties.

IAPM Mall: Opened in Aug 2013, IAPM Mall is an upscale mall with a late-night

shopping concept. It is part of the integrated Shanghai ICC development, which

sits on Huaihai Middle Road in the busy commercial district of Puxi. The whole

development comprises two office towers, a shopping mall and deluxe

residences. With 1.3m sf of shopping GFA, the mall is fully leased out. In its

latest results presentation, SHK continued to report strong traffic growth and

tenant sales. This location is promising as it sits at the interchange of three

major metro lines.

Fig 19: IAPM Mall is at the interchange of Shanghai metro lines 1, 10 and 12, accessible by Shanxi Nan Lu station

Source: Shanghai ICC

IFC Mall: Mostly completed in 2010 but continuing to be upgraded, IFC Mall is

part of the Shanghai IFC integrated development located in the Pudong Lujiazui

Finance and Trade Zone. Jumbo’s third outlet will open here in Jan 2016. We are

equally optimistic on this high-end location on the famous Lujiazui roundabout,

near tourist attractions such as the Oriental Pearl Tower and Super Brand Mall.

The two towers are also home to the five-star Ritz Carlton Shanghai and the

Shanghai HQ of HSBC in China. It can be accessed via Lujiazui station on Metro

Line 2 and is just across the road from the bustling Super Brand Mall.

January 3, 2016 15

Jumbo Group Ltd

Fig 20: Shanghai IFC at the Lujiazui roundabout, near famous landmarks such as the Oriental Pearl Tower

Source: Shanghai IFC

Figure 21: Shanghai ICC in Puxi, site of IAPM Mall

Source: Sun Hung Kai Properties, FY14/15 annual results presentation

Figure 22: Shanghai IFC in Pudong, site of IFC Mall

Source: Sun Hung Kai Properties, FY14/15 annual results presentation

Raffles City: Jumbo’s second outlet was opened in Raffles City Shanghai in Aug

2015. Owned by Capitaland Mall Asia, this is a bustling mid-to-high-end mall

located at Xizang Middle Road in Shanghai’s downtown. The mall is close to

tourist haunts such as People’s Square, Nanjing Road Pedestrian Street, Shanghai

Museum and Shanghai Municipal Building with connectivity to People’s Square

subway station.

January 3, 2016 16

Jumbo Group Ltd

4.3 Part of the solution for China’s retail challenges Malls in China have had to evolve or devolve to deal with the country’s economic

slowdown. Retail sales, though still growing, have slowed, especially at the high-

end where big lux brands such as Prada, Chanel and LV have closed stores in the

past two years. Online shopping is having an adverse impact on bricks and mortar

retail, as is the import taxes that result in higher prices within China, leading

many to shop overseas or take advantage of daigou agents to provide overseas

buying services. The anti-corruption campaign by the government has also led to

a sharp halt in “gifting” luxury items in business deals.

In evolving to the changing landscape, the retail experience in China in becoming

less about shopping and buying products, but for leisure, entertainment, eating &

drinking and other social fulfilment concepts that bring differentiation to a highly

competitive retail environment. These include areas for children, unique food &

beverage options, live entertainment such as music or fashion shows, cinemas,

ice skating rinks, bowling alleys, etc. Malls have become destinations in

themselves, drawing in people to enjoy a day out and fill their leisure time with

activities that distract them from the daily grind.

Strong mall operators such as Sun Hung Kai Properties and Capitaland Mall Asia

are able to do this because they own the entire property and are able to provide

a unique shopping experience with a planned tenant mix. A key part of iAPM

Mall’s success is offering longer hours. The mall is open until 11pm for shops and

midnight for dinner and drinks. It has a wide range of entertainment, including a

6-screen IMAX cinema complex that accommodates more than 1,000 viewers.

Also, it has a successful social media loyalty program called VIC with over 1.7m

Weibo followers.

Where it applies to Jumbo, mall operators are setting aside 30-40% of the gross

floor area for food & beverage, up from 10-15% before 2007, according to real

estate consultancy CBRE. More F&B and entertainment space makes sense,

especially since Chinese malls are often integrated with residential projects. As

such, operators are also looking out for unique F&B options, such as what Jumbo

can offer. In terms of the broad numbers, this strategy appears to be working. A

report by the China Hotel Association said that F&B revenue in China rebounded

9.7% in 2014 after three years of slowdown.4

The trend to having more food-related activities as part of the high-end shopping

experience is in-line with what luxury brand companies are doing globally as

well. Food is a resilient business because restaurant meals are relatively

inexpensive pleasures compared to luxury shopping. According to Asia Retail

Partners, a HK retail consultancy, the next big wave in China is food as mainland

Chinese are eager to discover a new lifestyle. As a result, more and more lux

brands have entered the high-end food sector through acquisitions and restaurant

or café openings.

In 2014, LVMH acquired Milanese coffee house Pasticceria Confetteria Cova

Srl and took it to Beijing in 2015, with plans for Taiwan in 2016.5

In 2014, L Capital, LVMH’s private equity arm, bought Singapore’s Crystal

Jade, a chain of over 100 Chinese restaurants across Asia.6

In 2015, Gucci opened the world’s first Gucci Café in iAPM Mall in Shanghai.7

4 www.ibtimes.com/chinas-food-beverage-industry-rebounding-amid-anti-corruption-drive-1924543 5 http://www.straitstimes.com/lifestyle/food/the-pastry-war 6 http://www.lcapitalasia.com/portfolio_detail/crystal-jade 7 jingdaily.com/luxury-brands-break-into-food-business-to-reach-chinas-shoppers/#.VnC_10p97tQ

Fig 23: China retail sales growth slowing

Source: National Bureau of Statistics

January 3, 2016 17

Jumbo Group Ltd

4.4 Export other brands to the region Besides JUMBO and JPOT, we also believe that Jumbo can also export its other

food brands to other countries, especially Ng Ah Sio Bak Kut Teh or Chui Huay

Lim to countries with similar food and receptive populations such as Malaysia or

Thailand. While management has not made any mention of this in its growth

strategy yet, we believe it makes sense and could form the second phase of its

expansion plans in the region after China.

4.5 Acquisitions, JVs or strategic alliances Finally, Jumbo may expand its business in Singapore or overseas through

acquisitions, JVs or alliances with parties which can strengthen its market

position, add value to its business or help it expand. Examples are its partners in

the SSR JVs such as Tung Lok in Singapore or Maruha Restaurant Systems in Japan,

as well as Breadtalk which owns 30% of China’s JUMBO SEAFOOD outlets. Given

January 3, 2016 18

Jumbo Group Ltd

5. Barriers to Entry

5.1 Competitive with a clear path to growth Unlike Ngiam Tong Boon, a bartender widely credited to be the creator of the

Singapore Sling in the early 1900s, Jumbo is not the inventor of the chilli crab.

That honour goes to Mdm Cher Yam Tian of Roland Restaurant. In fact, its

signature dishes – chilli crab and black pepper crab – are widely available in

Singapore, varying only with the creativity of the chef.

Jumbo prices its signature crab dishes at a market-topping SGD78/kg.

Anecdotally, the market range is SGD45-80/kg. The lower-end prices can be

found in eating places such as non-air-conditioned coffee shops or industrial food

centres. Higher-end establishments such as JUMBO can charge more as they are

located in popular dining enclaves such as the East Coast Seafood Centre, Clarke

Quay or Dempsey Hill that also serve tourists. Despite similar dishes at lower

prices, we do not view the lower-end places as direct competitors of JUMBO.

For investors, however, the formulation, origin or price points of this dish are not

determinants for their investment, in our view. What matters should be the

following:

Great branding and marketing – Lower-end seafood places do not have the

branding, marketing reach or scale of Jumbo. Locals may claim that

Mellben’s or Roland’s crabs taste better, but they may equally choose to eat

at JUMBO whenever they want to be assured of consistency in taste and

ambience. For tourists, JUMBO is usually their dining destination of choice.

Arguably, locals also introduce their foreign friends to JUMBO for their first

“typical” taste of seafood in Singapore, on the reasonable assumption that

JUMBO is likely to leave a good impression with the tourists, not bad.

Growing footprint of outlets and brands – Now up to five brands, of which

only one is seafood-related, and 16 outlets in Singapore and China. The

growing footprint will serve Jumbo well in dealing with future competitive

pressures, in our view.

Well-tested systems and execution – This footprint is backed by a 10,000 sf

central kitchen and processes that allow it to reduce costs, maximise

revenue per staff, achieve consistency in food quality and tastes, and try out

more dining concepts with lower risk.

Clear expansion strategy – Jumbo intends to open four new outlets in the

next two years in Singapore and China. For its overseas story, it plans to

focus on China first, specifically Shanghai and JUMBO. Its first outlet in

China, opened in 2013, has been so successful that it will have three outlets

there by 2016.

5.2 Food quality & safety a key mantra Jumbo’s reputation and branding should work in its favour in China. As a

Singapore company, we believe Chinese consumers can be confident that the

quality of its ingredients, food preparation and food service are second to none.

This should appeal to the average Chinese consumer who is by now extremely

wary and demanding when it comes to food safety.

Jumbo only buys its ingredients from a list of approved suppliers and kitchen

staff must adhere to strict procedures in preparing and handling dishes.

According to management, even the crabs sold in its Shanghai outlets are

imported live from Singapore to ensure freshness and quality.

January 3, 2016 19

Jumbo Group Ltd

To further ensure high food-safety standards, Jumbo applies the HACCP safety

management system to all its operations. HACCP stands for Hazard Analysis and

Critical Control Point. While it is also used in non-food industries such as

chemicals and pharmaceuticals, its seven principles8 are just as applicable to the

food industry, namely:

(1) Identify hazards in each step, from purchasing, delivery and storage to

preparation, cooking and chilling

(2) Determine critical control points (CCPs) that ensure the control of the

hazards eg cooking raw meat thoroughly to kill pathogens

(3) Establish critical limits to facilitate the identification of a CCP when it is out

of control eg when cooking beef burgers, the centre of the burger must

reach a certain temperature to ensure the destruction of pathogens

(4) Establish a system to monitor control of the CCP

(5) Take corrective measures when monitoring indicates that a particular CCP is

not under control

(6) Establish procedures for confirmation that the HACCP system is working

effectively

(7) Establish documentation for all procedures

5.3 Expand central kitchen & IT to enhance scalability Jumbo’s central kitchens in Singapore and China prepare sauces and marinades,

process certain food ingredients and roll out semi-finished food products such as

marinated meats for its outlets. This way, quality and taste are controlled and

standardised. According to management, it does not need to station a master

chef at each outlet as the central kitchen is able to standardise the critical

ingredients and food preparations.

Jumbo’s 10,000 sf central kitchen in Singapore supplies to its local and China

outlets. Although located within the same building, it is separate from its

corporate offices and other kitchens. Jumbo intends to utilise SGD11.5m or 29%

of its IPO proceeds to bring together its operations under one roof in either

acquired or leased premises. It also wants to acquire new equipment and

machinery. In China, Jumbo has a small facility for marinating ingredients,

although its all-important pastes and spices are imported from Singapore to

protect its recipes. It also imports live crabs and certain critical herbs such as

lemongrass from Singapore. At some point, it may expand this operation.

Central kitchens are crucial to Jumbo’s operations as they can support scalability

as it expands its network. Their advantages are:

Ensuring food consistency. Before Jumbo opened its central kitchen in

2008, even its signature crab differs in taste from outlet to outlet. This is no

longer an issue as its central kitchen standardises the pastes and spices.

Jumbo has also found a way to reproduce its signature dishes easily, such

that even junior chefs can prepare the dish. This does away with the need to

employ expensive onsite master chefs.

Space and time savings. Laborious work such as washing and chopping are

done by kitchen helpers at its central kitchen. This leaves its chefs fresh to

work the whole night, to focus on food consistency. Furthermore, food

8 https://www.fsai.ie/food_businesses/haccp/principles_of_haccp.html

January 3, 2016 20

Jumbo Group Ltd

preparation starts at 2pm at its central kitchens instead of 5pm at each site,

saving on space and allowing for faster table turns.

Greater automation. Jumbo’s central kitchens use automation which

requires just 1-2 workers to produce sauces and spices for all its outlets.

Finally, Jumbo is big on using IT to improve efficiency and productivity. It was

among the first F&B establishments in Singapore to use integrated front-end

point-of-sale systems, whereby iPads and mobile POS terminals are used to take

orders that go straight to the kitchen. This leaves servers with more time to

attend to customers. Jumbo works with chope.com for online reservations for all

its outlets except Ng Ah Sio and J Café, which do not take reservations. Queuing

is also automated. Upon entering their mobile numbers, customers waiting for

their tables can leave and an SMS will alert them when their tables are ready.

A capable back-end IT system gives management timely information. We

understand that the implementation of an ERP system by early 2016 will give

management access to sales and cost data that are updated every five minutes.

This upgrade should allow management to respond faster to dining conditions.

For example, management will be aware of slow nights at a particular restaurant

in real time or slow-selling dishes. It can immediately instruct servers to respond

with special offers to diners.

January 3, 2016 21

Jumbo Group Ltd

6. Forecasts & Assumptions

6.1 Sales to grow by 16% CAGR, NP 13% in FY16E-18E We forecast sales to rise by 19%/15%/13% and core net profit to grow by

9%/11%/20% in FY16E/17E/18E. The revenue spike in FY16E is due mainly to the

addition of two JUMBO outlets in China. However, we expect FY16E NP growth to

be lower at 9% as we assumed that these two outlets will need a year to break

even. Thereafter however, NP growth should accelerate to 11% in FY17E and 20%

in FY18E as they start to positively contribute in the second year. While we

expect Jumbo to continue to open new outlets each year (eg one outlet per year

in China assumed with an additional outlet in Singapore assumed for FY17E), the

pace should be less frenetic and will allow the existing outlets to better cover

start-up costs of new outlets.

Fig 24: Revenue/net profit CAGRs of 16%/13% in FY15-18E…

Source: Company data, Maybank Kim Eng

Fig 25: … mainly from one new outlet per year in China

Source: Company data, Maybank Kim Eng

6.2 China to be the main growth driver China is expected to generate the biggest revenue and earnings growth for

Jumbo, justifying the addition of four outlets in FY15-FY18E, of which two have

been confirmed for FY15-FY16E. The early results have been overwhelmingly

positive for Jumbo. China accounted for 6% of group revenue in the year that its

first outlet opened in FY14. This number climbed to 9% by the second year in

FY15, all from just the one outlet in IAPM Mall. Profitability was achieved by the

end of the first year. The additional outlets we have forecasted are expected to

lift China’s revenue contributions to 32% by FY18E, with the biggest jump in

FY16E from two new outlets opened in Aug 2015 and Jan 2016 respectively.

Fig 26: China is expected to account for 32% of group revenue by FY18E…

Source: Company data, Maybank Kim Eng

Fig 27: …far outperforming Singapore’s single-digit growth

Source: Company data, Maybank Kim Eng

3%

9%

11%

20%

9%

19%

15%

13%

0%

5%

10%

15%

20%

25%

0

50,000

100,000

150,000

200,000

250,000

FY15 FY16E FY17E FY18E

(SGD'000)

Revenue Core NP

Core NP growth (RHS) Revenue growth (RHS)

5 5 5 5

6 6

1

2

3

4

5

0

1

2

3

4

5

6

7

FY13 FY14 FY15 FY16E FY17E FY18E

Singapore JUMBO China JUMBO

100%94% 91%

79%73% 68%

6% 9%

21%27% 32%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15 FY16E FY17E FY18E

Singapore China

6% 4% 5% 7%

60%

189%

53%

31%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

FY15 FY16E FY17E FY18E

(SGD'000)

Singapore China

Singapore growth (RHS) China growth (RHS)

January 3, 2016 22

Jumbo Group Ltd

6.3 Optimistic on China expansion Based on our estimates, Jumbo’s first China seafood outlet at IAPM Mall should

have been profitable by the end of the first year. We believe its ROI is very high

as spending per pax in China tends to exceed Singapore’s with lower operating

costs. Its China prices are higher as crabs and sauces are imported from

Singapore but margins are better as other ingredients such as meat and

vegetables are sourced locally and sold at Singapore prices. Rental and labour

costs are also estimated to be lower than in Singapore due to preferential rental

rates from landlords and the employment of students/interns who are known to

be willing to trade lower wages for work experience.

At full operation, the investment payback time for an outlet could be as good as

three years with an ROI of 32%, assuming one table turn per night. Furthermore,

assuming Jumbo is able to capitalise on the positive impact it has made on the

local market so far by driving up table turns to an average of two per night, its

outlet payback could be as short as 1-2 years with an ROI of 86%, by our

estimates. Arguably, returns could be even better as we did not control for staff

and utility costs which are semi-variable for an F&B business. Just because

revenue doubles, staff and utility costs may not double along with it. Hence, we

believe our analysis is still conservative.

Fig 28: China ROI - our analysis of JUMBO IAPM’s performance

FY14 % of revenue 1 turn/night 2 turns/night YoY chg

Months of operation, opened in Nov 2013 10 12 12

Revenue (SGD'000) 6,529

12,000 24,000

Revenue (CNY'000), @ 4.50 CNY/SGD 29,381

54,000 108,000 100%

Revenue/table/month (CNY) 9,794

18,000 36,000

Revenue/table/night (CNY) 326

600 1,200

Table turns/night 1

1 2

Revenue/pax (CNY), based on 2 pax/table, 1 turn/night & dianping.com average spend/pax

163.2 300.0 300.0

Depreciation (assume 10 years) (1,125) 4% (1,125) (1,125)

Food costs (8,814) 30% (16,200) (32,400)

Rental costs (2,350) 8% (4,320) (4,320)

Gross profit (CNY'000) 17,091

32,355 70,155 117%

Gross margin 58%

60% 65% Staff costs (4,407) 15% (8,100) (16,200) EBIT 12,684

24,255 53,955 122%

EBIT margin 43%

45% 50% Utilities cost (2,938) 10% (5,400) (10,800) Other opex (5,876) 20% (10,800) (21,600) Pretax profit (CNY'000) 3,870

8,055 21,555 168%

Taxation, assume 25% statutory rate (967)

(2,014) (5,389) Minorities (30% owned by Breadtalk) (1,161)

(2,417) (6,467)

Net profit (CNY'000) 1,741

3,625 9,700 168%

Net margin 6%

7% 9%

Return on investment 15%

32% 86%

Payback period (years) 6.5

3.1 1.2

Estimated capex (CNY'000) 11,250

No. of tables 250

Source: Maybank Kim Eng estimates

January 3, 2016 23

Jumbo Group Ltd

6.4 Singapore a sturdy mainstay Against the backdrop of a surging China, Singapore’s growth is expected to be

mid-to-high single digits, stoked largely by the performance of existing JUMBO

restaurants as well as the expansion of the JUMBO and JPOT network.

Singapore’s growth should mainly centre on diner growth and higher table spend,

especially at JUMBO outlets:

Improving diner volume. We are confident that Jumbo can continue to draw

customers to its flagship brands such as JUMBO SEAFOOD, JPOT or Ng Ah Sio

as they are established names serving popular cuisine. The trick is to

improve table turns. Jumbo has slick front-end service which includes online

reservations, an SMS-based queuing system and electronic order-taking.

When its new ERP system comes online, management can moreover access

sales and cost data that are updated every five minutes. This upgrade should

allow for a faster response to dining conditions.

Raising the price of crabs. According to Maybank Kim Eng’s in-house

foodies, Jumbo raised its crab prices twice last year from SGD68/kg to

SGD72/kg and further to SGD78/kg early this year. These hikes did not seem

to have been necessitated by costlier crabs as crab costs rose only a tame 6%

vs its FY15 revenue growth of 9%. Rather, prices were raised apparently to

offset higher rental costs and allow Jumbo to maintain its gross margins.

With full-year effects, we expect gross margins to improve in FY16.

For the organic growth of the existing outlets, we have predicated Singapore

growth on the following:

3% growth in average table spend for JUMBO (vs a more robust 5% for JUMBO

in China to account for the newness of the dining concept and brand)

1% growth in average table spend for Ng Ah Sio, Chui Huay Lim, JPOT and J

Café

To account for expansion of new outlets, our forecasts assumed the following:

The addition of one new 285-table JUMBO outlet, its sixth, in FY17E.

The addition of one new 50-table JPOT outlet, its fourth, in FY17E.

Obviously, this assumes that Jumbo is able to find suitable locations, especially

for JUMBO outlets which are usually found in tourist hotspots near rivers, the sea

or in foodie haunts such as Dempsey Hill. We do not preclude the possibility that

Jumbo could launch new dining concepts and the new outlets could involve new

brands instead of existing brands.

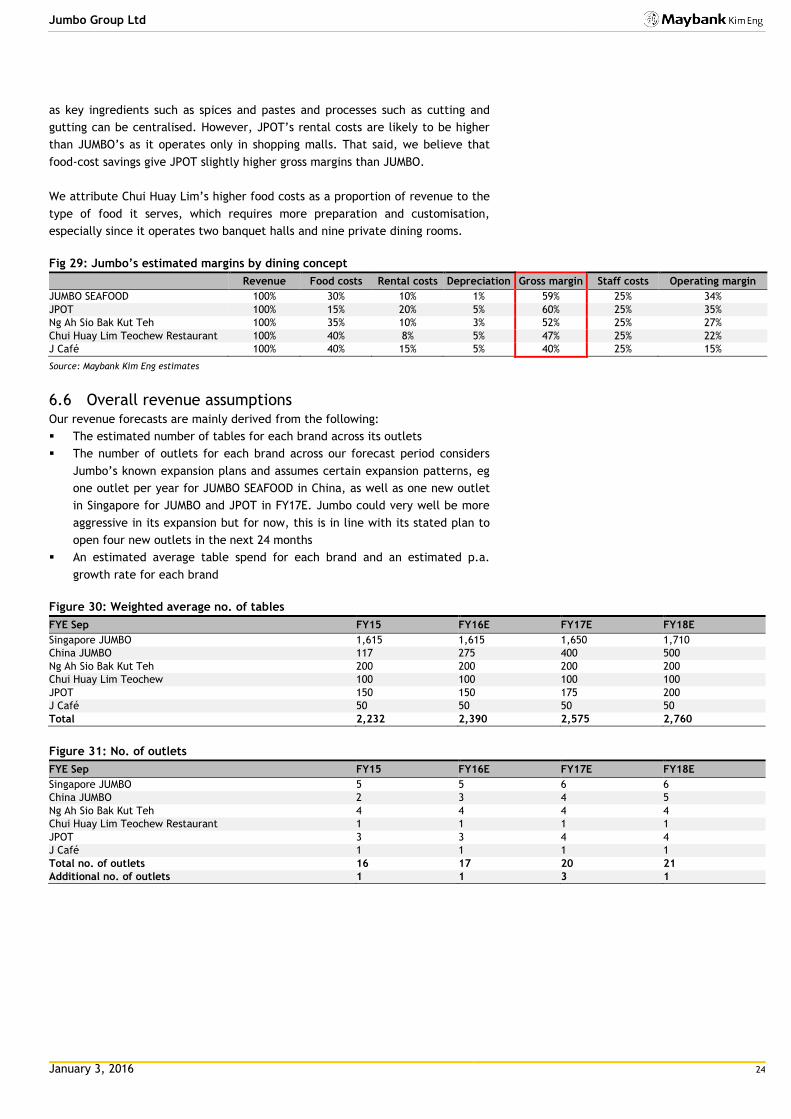

6.5 Why do we believe future expansion will favour JUMBO

and JPOT? Subject to finding the right locations at the right costs, we believe that

management is more likely to expand JPOT and JUMBO than its other dining

concepts. By our estimates, JUMBO SEAFOOD and JPOT command the best

margins, both gross and operating. These are followed by Ng Ah Sio Bak Kut Teh,

Chui Huay Lim Teochew Restaurant and J Café, in that order. Nevertheless, we

estimate that all its dining concepts are able to command gross margins of at

least 40% up to 60% for its flagship brands.

We believe food costs for JUMBO SEAFOOD and JPOT are among the lowest in the

group, given their central-kitchen modus operandi. JPOT’s ingredients are mainly

raw, with little to no preparation except for cutting and marinating. These can

be centralised. We also believe JUMBO’s food costs are below the group average

January 3, 2016 24

Jumbo Group Ltd

as key ingredients such as spices and pastes and processes such as cutting and

gutting can be centralised. However, JPOT’s rental costs are likely to be higher

than JUMBO’s as it operates only in shopping malls. That said, we believe that

food-cost savings give JPOT slightly higher gross margins than JUMBO.

We attribute Chui Huay Lim’s higher food costs as a proportion of revenue to the

type of food it serves, which requires more preparation and customisation,

especially since it operates two banquet halls and nine private dining rooms.

Fig 29: Jumbo’s estimated margins by dining concept

Revenue Food costs Rental costs Depreciation Gross margin Staff costs Operating margin

JUMBO SEAFOOD 100% 30% 10% 1% 59% 25% 34%

JPOT 100% 15% 20% 5% 60% 25% 35%

Ng Ah Sio Bak Kut Teh 100% 35% 10% 3% 52% 25% 27%

Chui Huay Lim Teochew Restaurant 100% 40% 8% 5% 47% 25% 22%

J Café 100% 40% 15% 5% 40% 25% 15%

Source: Maybank Kim Eng estimates

6.6 Overall revenue assumptions Our revenue forecasts are mainly derived from the following:

The estimated number of tables for each brand across its outlets

The number of outlets for each brand across our forecast period considers

Jumbo’s known expansion plans and assumes certain expansion patterns, eg

one outlet per year for JUMBO SEAFOOD in China, as well as one new outlet

in Singapore for JUMBO and JPOT in FY17E. Jumbo could very well be more

aggressive in its expansion but for now, this is in line with its stated plan to

open four new outlets in the next 24 months

An estimated average table spend for each brand and an estimated p.a.

growth rate for each brand

Figure 30: Weighted average no. of tables

FYE Sep FY15 FY16E FY17E FY18E

Singapore JUMBO 1,615 1,615 1,650 1,710

China JUMBO 117 275 400 500

Ng Ah Sio Bak Kut Teh 200 200 200 200

Chui Huay Lim Teochew 100 100 100 100

JPOT 150 150 175 200

J Café 50 50 50 50

Total 2,232 2,390 2,575 2,760

Figure 31: No. of outlets

FYE Sep FY15 FY16E FY17E FY18E

Singapore JUMBO 5 5 6 6

China JUMBO 2 3 4 5

Ng Ah Sio Bak Kut Teh 4 4 4 4

Chui Huay Lim Teochew Restaurant 1 1 1 1

JPOT 3 3 4 4

J Café 1 1 1 1

Total no. of outlets 16 17 20 21

Additional no. of outlets 1 1 3 1

January 3, 2016 25

Jumbo Group Ltd

6.7 Margin trends should be stable We expect stable margin trends for Jumbo. Not all companies break out their

costs but for those that do, Jumbo compares quite favourably, particularly on

raw materials and staff costs.

Figure 32: Operating margins

Source: Company data, Maybank Kim Eng

Fig 33: Operating cost trends

Raw materials

Staff costs

Rental costs

As % of revenue FY13 FY14 FY15 FY13 FY14 FY15 FY13 FY14 FY15

Jumbo Group 38.9 38.0 36.9 27.7 27.1 28.3 8.1 7.9 8.4

Breadtalk Group - - - 26.6 26.9 27.3 - - -

Neo Group 31.0 29.6 38.3 30.1 32.4 30.2 6.2 6.8 5.7

Select Group - - - - - 34.8 9.7 7.9 6.7

Soup Restaurant Group 23.3 23.3 23.1 34.7 36.2 37.2 36.6 35.4 35.7

Tung Lok Restaurants - - - 33.7 31.5 33.6 16.2 15.1 15.9

Source: Companies

The key costs are:

Raw materials and consumables (36-37% of revenue) form the biggest

chunk of Jumbo’s costs, presumably because seafood is behind more than

70% of its revenue. Such costs have been declining in the last few years,

from 39% in FY13 to below 37% in FY15. As Jumbo becomes an ever bigger

buyer of seafood, it should be able to attract better pricing from its

suppliers. It mentioned in its IPO prospectus that it was able to obtain more

competitive pricing for seafood from another supplier between FY12 and

1H15. An expanded central kitchen should also help it optimise raw-material

usage.

Staff costs (27-28% of revenue) are the second biggest chunk. Jumbo has

consistently paid less than the industry for staff except BreadTalk. We

attribute this to its lean staffing and savvy use of IT at the front of the house

to maximise table turns. Stable staff turnover is another positive, keeping

staff costs in check. About 100 of its 700+ employees have been with Jumbo

for more than 10 years. We believe an ERP system early next year will be

another step in optimising staff costs, through real-time decisions on the

deployment of temporary workers, in response to nightly takings. We have

assumed staff costs will be higher in future now that it is a listed company.

Rentals (8% of revenue) should be more or less stable, though they may

creep slightly higher. Jumbo generally signs three-year leases which seem to

be evenly spaced out as its rental expenses have been increasing every year.

52%

52%

53%

53%

54%

54%

55%

55%

56%

56%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

FY13 FY14 FY15 FY16E FY17E FY18E

Gross margin (RHS) EBITDA margin

PBT margin Net margin

January 3, 2016 26

Jumbo Group Ltd

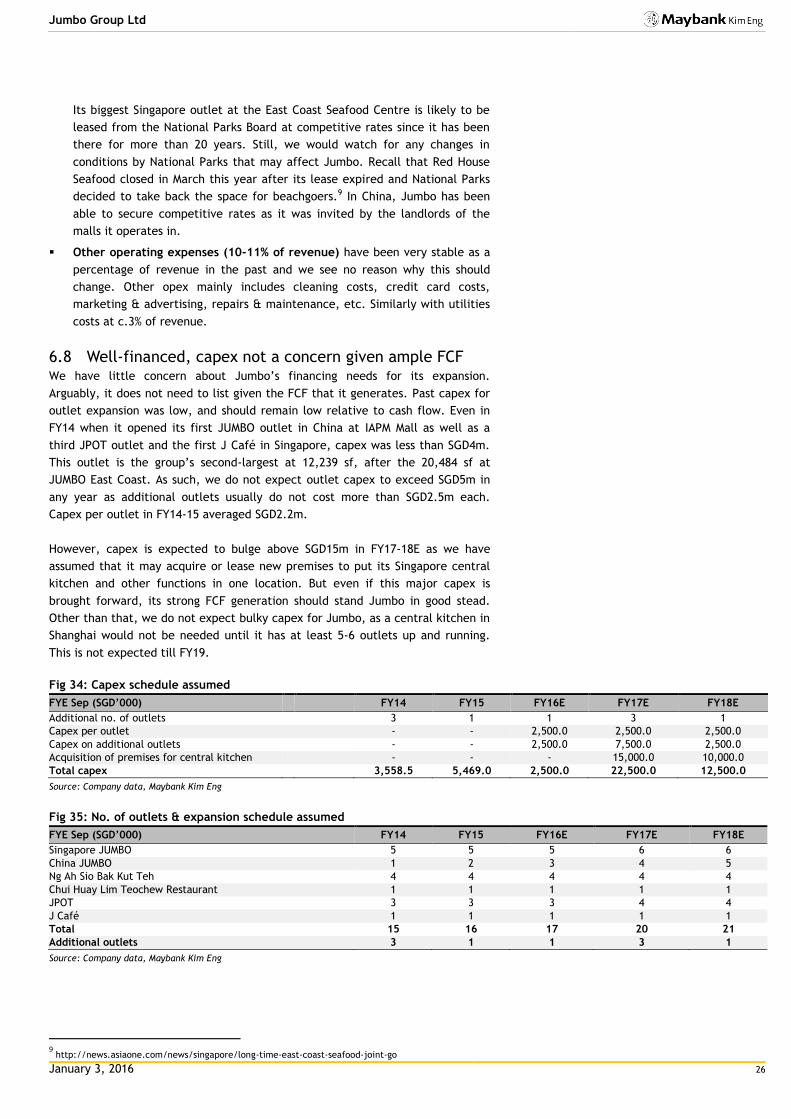

Its biggest Singapore outlet at the East Coast Seafood Centre is likely to be

leased from the National Parks Board at competitive rates since it has been

there for more than 20 years. Still, we would watch for any changes in

conditions by National Parks that may affect Jumbo. Recall that Red House

Seafood closed in March this year after its lease expired and National Parks

decided to take back the space for beachgoers.9 In China, Jumbo has been

able to secure competitive rates as it was invited by the landlords of the

malls it operates in.

Other operating expenses (10-11% of revenue) have been very stable as a

percentage of revenue in the past and we see no reason why this should

change. Other opex mainly includes cleaning costs, credit card costs,

marketing & advertising, repairs & maintenance, etc. Similarly with utilities

costs at c.3% of revenue.

6.8 Well-financed, capex not a concern given ample FCF We have little concern about Jumbo’s financing needs for its expansion.

Arguably, it does not need to list given the FCF that it generates. Past capex for

outlet expansion was low, and should remain low relative to cash flow. Even in

FY14 when it opened its first JUMBO outlet in China at IAPM Mall as well as a

third JPOT outlet and the first J Café in Singapore, capex was less than SGD4m.

This outlet is the group’s second-largest at 12,239 sf, after the 20,484 sf at

JUMBO East Coast. As such, we do not expect outlet capex to exceed SGD5m in

any year as additional outlets usually do not cost more than SGD2.5m each.

Capex per outlet in FY14-15 averaged SGD2.2m.

However, capex is expected to bulge above SGD15m in FY17-18E as we have

assumed that it may acquire or lease new premises to put its Singapore central

kitchen and other functions in one location. But even if this major capex is

brought forward, its strong FCF generation should stand Jumbo in good stead.

Other than that, we do not expect bulky capex for Jumbo, as a central kitchen in

Shanghai would not be needed until it has at least 5-6 outlets up and running.

This is not expected till FY19.

Fig 34: Capex schedule assumed

FYE Sep (SGD’000)

FY14 FY15 FY16E FY17E FY18E

Additional no. of outlets

3 1 1 3 1

Capex per outlet

- - 2,500.0 2,500.0 2,500.0

Capex on additional outlets

- - 2,500.0 7,500.0 2,500.0

Acquisition of premises for central kitchen

- - - 15,000.0 10,000.0

Total capex

3,558.5 5,469.0 2,500.0 22,500.0 12,500.0

Source: Company data, Maybank Kim Eng

Fig 35: No. of outlets & expansion schedule assumed

FYE Sep (SGD’000) FY14 FY15 FY16E FY17E FY18E

Singapore JUMBO 5 5 5 6 6

China JUMBO 1 2 3 4 5

Ng Ah Sio Bak Kut Teh 4 4 4 4 4

Chui Huay Lim Teochew Restaurant 1 1 1 1 1

JPOT 3 3 3 4 4

J Café 1 1 1 1 1

Total 15 16 17 20 21

Additional outlets 3 1 1 3 1

Source: Company data, Maybank Kim Eng

9 http://news.asiaone.com/news/singapore/long-time-east-coast-seafood-joint-go

January 3, 2016 27

Jumbo Group Ltd

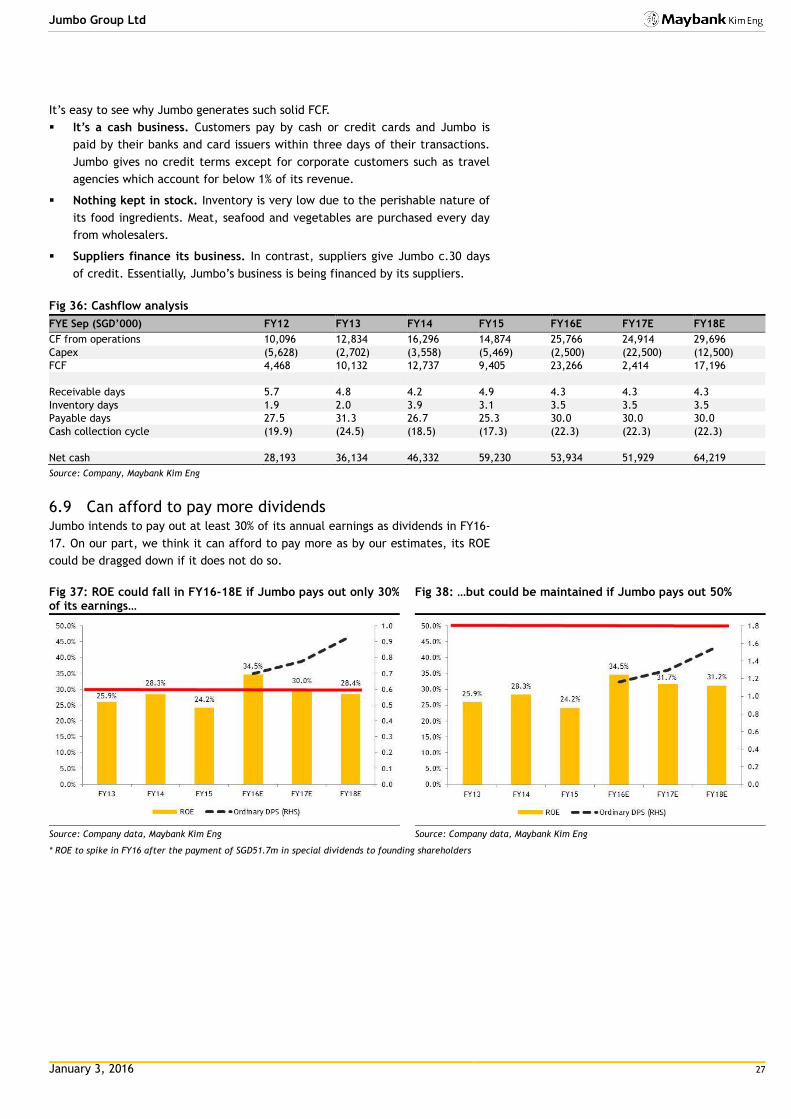

It’s easy to see why Jumbo generates such solid FCF.

It’s a cash business. Customers pay by cash or credit cards and Jumbo is

paid by their banks and card issuers within three days of their transactions.

Jumbo gives no credit terms except for corporate customers such as travel

agencies which account for below 1% of its revenue.

Nothing kept in stock. Inventory is very low due to the perishable nature of

its food ingredients. Meat, seafood and vegetables are purchased every day

from wholesalers.

Suppliers finance its business. In contrast, suppliers give Jumbo c.30 days

of credit. Essentially, Jumbo’s business is being financed by its suppliers.

Fig 36: Cashflow analysis

FYE Sep (SGD’000) FY12 FY13 FY14 FY15 FY16E FY17E FY18E

CF from operations 10,096 12,834 16,296 14,874 25,766 24,914 29,696

Capex (5,628) (2,702) (3,558) (5,469) (2,500) (22,500) (12,500)

FCF 4,468 10,132 12,737 9,405 23,266 2,414 17,196

Receivable days 5.7 4.8 4.2 4.9 4.3 4.3 4.3

Inventory days 1.9 2.0 3.9 3.1 3.5 3.5 3.5

Payable days 27.5 31.3 26.7 25.3 30.0 30.0 30.0

Cash collection cycle (19.9) (24.5) (18.5) (17.3) (22.3) (22.3) (22.3)

Net cash 28,193 36,134 46,332 59,230 53,934 51,929 64,219

Source: Company, Maybank Kim Eng

6.9 Can afford to pay more dividends Jumbo intends to pay out at least 30% of its annual earnings as dividends in FY16-

17. On our part, we think it can afford to pay more as by our estimates, its ROE

could be dragged down if it does not do so.

Fig 37: ROE could fall in FY16-18E if Jumbo pays out only 30% of its earnings…

Source: Company data, Maybank Kim Eng

Fig 38: …but could be maintained if Jumbo pays out 50%

Source: Company data, Maybank Kim Eng

* ROE to spike in FY16 after the payment of SGD51.7m in special dividends to founding shareholders

January 3, 2016 28

Jumbo Group Ltd

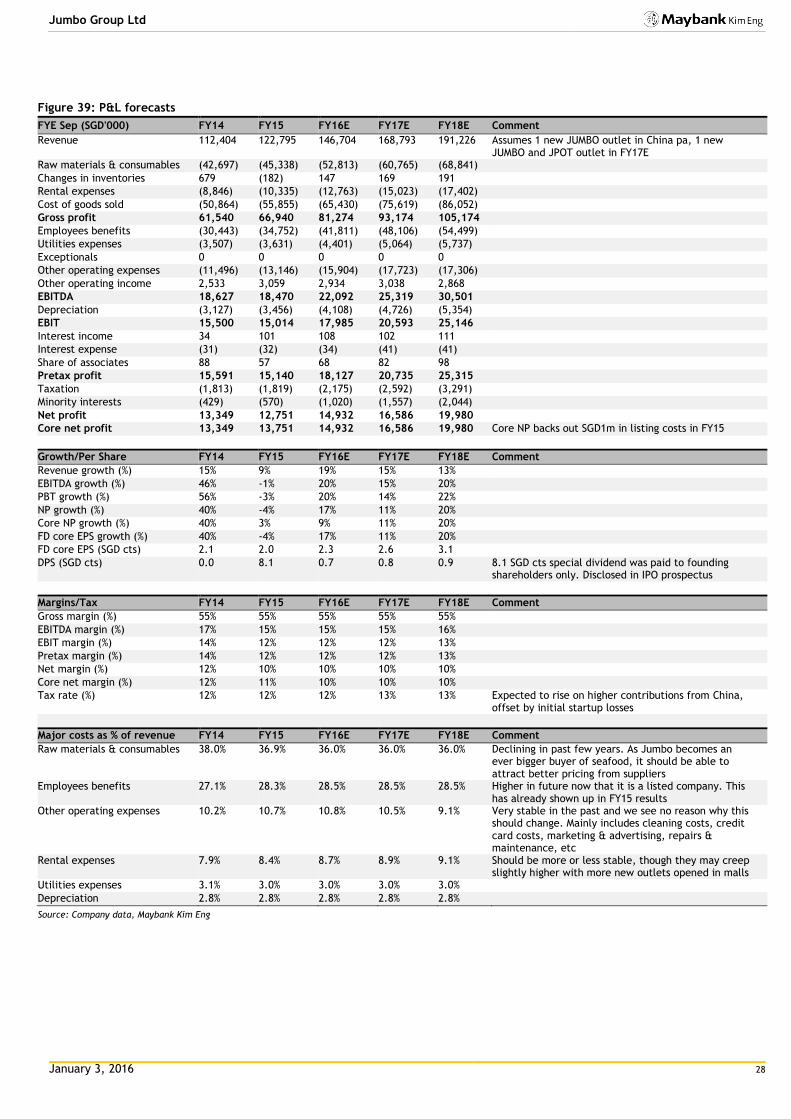

Figure 39: P&L forecasts

FYE Sep (SGD'000) FY14 FY15 FY16E FY17E FY18E Comment

Revenue 112,404 122,795 146,704 168,793 191,226 Assumes 1 new JUMBO outlet in China pa, 1 new JUMBO and JPOT outlet in FY17E

Raw materials & consumables (42,697) (45,338) (52,813) (60,765) (68,841)

Changes in inventories 679 (182) 147 169 191

Rental expenses (8,846) (10,335) (12,763) (15,023) (17,402)

Cost of goods sold (50,864) (55,855) (65,430) (75,619) (86,052)

Gross profit 61,540 66,940 81,274 93,174 105,174

Employees benefits (30,443) (34,752) (41,811) (48,106) (54,499)

Utilities expenses (3,507) (3,631) (4,401) (5,064) (5,737)

Exceptionals 0 0 0 0 0

Other operating expenses (11,496) (13,146) (15,904) (17,723) (17,306)

Other operating income 2,533 3,059 2,934 3,038 2,868

EBITDA 18,627 18,470 22,092 25,319 30,501

Depreciation (3,127) (3,456) (4,108) (4,726) (5,354)

EBIT 15,500 15,014 17,985 20,593 25,146

Interest income 34 101 108 102 111

Interest expense (31) (32) (34) (41) (41)

Share of associates 88 57 68 82 98

Pretax profit 15,591 15,140 18,127 20,735 25,315

Taxation (1,813) (1,819) (2,175) (2,592) (3,291)

Minority interests (429) (570) (1,020) (1,557) (2,044)

Net profit 13,349 12,751 14,932 16,586 19,980

Core net profit 13,349 13,751 14,932 16,586 19,980 Core NP backs out SGD1m in listing costs in FY15

Growth/Per Share FY14 FY15 FY16E FY17E FY18E Comment

Revenue growth (%) 15% 9% 19% 15% 13%

EBITDA growth (%) 46% -1% 20% 15% 20%

PBT growth (%) 56% -3% 20% 14% 22%

NP growth (%) 40% -4% 17% 11% 20%

Core NP growth (%) 40% 3% 9% 11% 20%

FD core EPS growth (%) 40% -4% 17% 11% 20%

FD core EPS (SGD cts) 2.1 2.0 2.3 2.6 3.1

DPS (SGD cts) 0.0 8.1 0.7 0.8 0.9 8.1 SGD cts special dividend was paid to founding shareholders only. Disclosed in IPO prospectus

Margins/Tax FY14 FY15 FY16E FY17E FY18E Comment

Gross margin (%) 55% 55% 55% 55% 55%

EBITDA margin (%) 17% 15% 15% 15% 16%

EBIT margin (%) 14% 12% 12% 12% 13%

Pretax margin (%) 14% 12% 12% 12% 13%

Net margin (%) 12% 10% 10% 10% 10%

Core net margin (%) 12% 11% 10% 10% 10%

Tax rate (%) 12% 12% 12% 13% 13% Expected to rise on higher contributions from China, offset by initial startup losses

Major costs as % of revenue FY14 FY15 FY16E FY17E FY18E Comment

Raw materials & consumables 38.0% 36.9% 36.0% 36.0% 36.0% Declining in past few years. As Jumbo becomes an ever bigger buyer of seafood, it should be able to attract better pricing from suppliers

Employees benefits 27.1% 28.3% 28.5% 28.5% 28.5% Higher in future now that it is a listed company. This has already shown up in FY15 results

Other operating expenses 10.2% 10.7% 10.8% 10.5% 9.1% Very stable in the past and we see no reason why this should change. Mainly includes cleaning costs, credit card costs, marketing & advertising, repairs & maintenance, etc

Rental expenses 7.9% 8.4% 8.7% 8.9% 9.1% Should be more or less stable, though they may creep slightly higher with more new outlets opened in malls

Utilities expenses 3.1% 3.0% 3.0% 3.0% 3.0%

Depreciation 2.8% 2.8% 2.8% 2.8% 2.8%

Source: Company data, Maybank Kim Eng

January 3, 2016 29

Jumbo Group Ltd

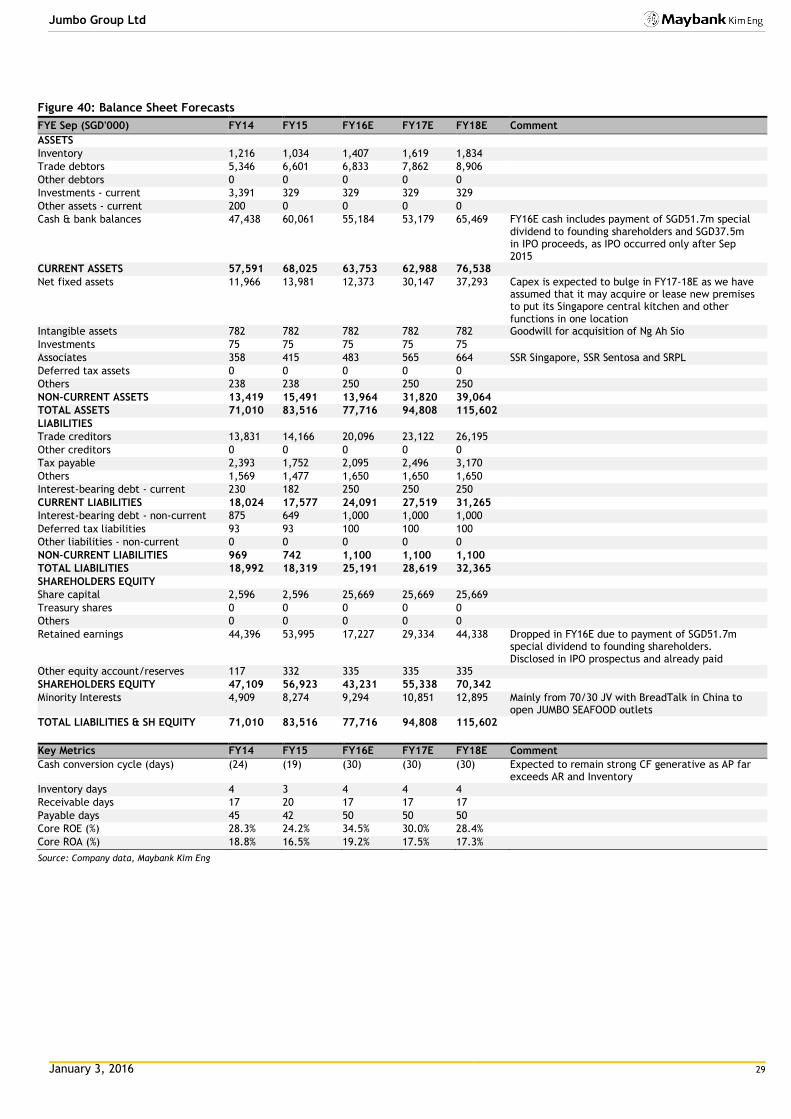

Figure 40: Balance Sheet Forecasts

FYE Sep (SGD'000) FY14 FY15 FY16E FY17E FY18E Comment

ASSETS

Inventory 1,216 1,034 1,407 1,619 1,834

Trade debtors 5,346 6,601 6,833 7,862 8,906

Other debtors 0 0 0 0 0

Investments - current 3,391 329 329 329 329

Other assets - current 200 0 0 0 0

Cash & bank balances 47,438 60,061 55,184 53,179 65,469 FY16E cash includes payment of SGD51.7m special dividend to founding shareholders and SGD37.5m in IPO proceeds, as IPO occurred only after Sep 2015

CURRENT ASSETS 57,591 68,025 63,753 62,988 76,538

Net fixed assets 11,966 13,981 12,373 30,147 37,293 Capex is expected to bulge in FY17-18E as we have assumed that it may acquire or lease new premises to put its Singapore central kitchen and other functions in one location

Intangible assets 782 782 782 782 782 Goodwill for acquisition of Ng Ah Sio

Investments 75 75 75 75 75

Associates 358 415 483 565 664 SSR Singapore, SSR Sentosa and SRPL

Deferred tax assets 0 0 0 0 0

Others 238 238 250 250 250

NON-CURRENT ASSETS 13,419 15,491 13,964 31,820 39,064

TOTAL ASSETS 71,010 83,516 77,716 94,808 115,602

LIABILITIES

Trade creditors 13,831 14,166 20,096 23,122 26,195

Other creditors 0 0 0 0 0

Tax payable 2,393 1,752 2,095 2,496 3,170

Others 1,569 1,477 1,650 1,650 1,650

Interest-bearing debt - current 230 182 250 250 250

CURRENT LIABILITIES 18,024 17,577 24,091 27,519 31,265

Interest-bearing debt - non-current 875 649 1,000 1,000 1,000

Deferred tax liabilities 93 93 100 100 100

Other liabilities - non-current 0 0 0 0 0

NON-CURRENT LIABILITIES 969 742 1,100 1,100 1,100

TOTAL LIABILITIES 18,992 18,319 25,191 28,619 32,365

SHAREHOLDERS EQUITY

Share capital 2,596 2,596 25,669 25,669 25,669

Treasury shares 0 0 0 0 0

Others 0 0 0 0 0

Retained earnings 44,396 53,995 17,227 29,334 44,338 Dropped in FY16E due to payment of SGD51.7m special dividend to founding shareholders. Disclosed in IPO prospectus and already paid

Other equity account/reserves 117 332 335 335 335

SHAREHOLDERS EQUITY 47,109 56,923 43,231 55,338 70,342

Minority Interests 4,909 8,274 9,294 10,851 12,895 Mainly from 70/30 JV with BreadTalk in China to open JUMBO SEAFOOD outlets

TOTAL LIABILITIES & SH EQUITY 71,010 83,516 77,716 94,808 115,602