06-06-2013_4784812000 nam ve song elliot va dieu gi se xay ra trong the ky 21 - copy.pdf

TRANSCRIPT

12,000 YEARS OF ELLIOTT WAVES

AND

WHAT THIS MEANS FOR THE 21ST CENTURY

BY Joseph M. Miller

Daan Joubert

Marion Butler

[email protected] Comments, corrections or questions can be sent to any or all of the authors at the email addresses listed above.

© COPYRIGHT 1999 BY THE AUTHORS

ALL RIGHTS RESERVED

INTRODUCTION

The information in the article that you are preparing to read is breaking new ground in

the long-term analysis of human development. This project is an ambitious effort

designed to show that the upward direction of human development over many

millennia has taken place in a series of structured up and down cycles (or waves, in

Elliott terminology).

The Elliott Principle says that Elliott Waves of varying degree can be observed in

organized markets such as the DJIA or the S&P 500. These waves can cover hours,

days, weeks, months or years. Prior to Elliott's death, he talked and wrote about a

large wave that he called a Grand Super Cycle Wave (GSC), which lasted up to 300

years and was the largest wave discussed by him. During the research for this article,

the authors found evidence that larger waves were evident when longer and longer

periods of human history were examined.

An earlier work concerning this topic covered a shorter period from approximately

1600 AD to 2000 AD. In researching the shorter time period the concept of an X-

wave that consists of 5 full GSC waves was introduced. It became apparent the

analysis raised important questions which could only be answered by broadening the

time span even further to include a great deal of earlier history.

The authors learned when they examined human development from the end of the last

Ice Age in about 10,000BC through to 2000AD, that there was evidence of several

large Elliott Waves. These larger waves have been designated as follows: an X Wave

that lasts 800 to 1,000 years and is composed of five complete Grand Super Cycle

Waves; a Y Wave that lasts from 2,500 to 3,000 years and is composed of five

complete X Waves; and a Z Wave that lasts from 8,000 to10,000 years and is

composed of five complete Y Waves.

The reason for taking the longer-term view is to adequately interpret just where we are

in the wave structure at the end of the Twentieth Century. More importantly, without

this additional information, it was impossible to develop a picture of where we are

headed as we enter the 21st Century. It is really the search for an answer to this latter

question that guided the work presented here.

Most research concerning the Elliott Principle has pertained to the last 150 years, and

has been based on the value of equities as presented in stock market averages. The

reasons for this include the fact that such averages have only been available in a

reliable form for that period of time. Further, for typical investment decisions it was

not necessary to go any farther back in time to gain additional perspective of where

stock values had been and where they might be heading.

In our much more ambitious project, stretching further back in time, we were faced

with the problem of how to evaluate the position and timing of past cycles (waves)

when there was no viable stock market average to guide us. The only choice we

uncovered as usable was a combination of history and archeological evidence. The

authors encountered some problems in using this type of data to analyze past cycles

(waves) prior to about 1850. A critical reader, especially readers who have a working

knowledge of the Elliott Principle, need to take especial note of the problems the

authors faced and the limitations these placed on our analysis.

It was not until circa 3000 BC that writing came into existence. Prior to that time

archeological records are our only source of information, and of consequence are

imprecise to say the least. After circa 3000BC written accounts of events are available

and over time became more accurate. Even so, many important periods such as the

Roman period still pose factual problems because many of the histories of Rome were

not written until as late as 300 to 200 BC and covered all of Roman history from the

establishment of Rome in circa 750 BC. Much detail was lost and many dates and

important historical events were only approximately pinned down due to the time

lapse between the historical events and their written record.

One obvious problem this posed to the authors was in ascertaining the starting and

ending dates for cycles (waves) with any degree of precision. In the absence of market

related data the authors assumed that the rise and fall of empires and civilizations are

good approximations for the peaks and troughs in the economic cycle of the region

under review, which initially consisted largely of the Middle East and Europe. Also,

this meant that time became a more important characteristic for deciding on cycles

than the actual level of economic activity or of market prices, which are prominent in

the analysis of more recent market action.

At this point a direct quote from Nature's Law is appropriate. "(Elliott) Waves of

different degrees occur whether or not recording machinery is present". The recording

machinery Elliott was talking about was a viable stock market average. In spite of the

fact that adequate recording machinery was not available prior to circa 1850, it is the

opinion of the authors that the data as available and presented in this article displays

remarkable adherence to the Elliott Principle and its rules over a span of 12,000 years.

Our conclusion is that there are relatively few instances where it appears the Elliott

Principle has been found wanting, and these do not warrant dismissing the other

evidence that confirms the working of the Elliott Principle over the last 12,000 years.

The foregoing is especially true when the difficulty of obtaining precise dates is taken

into consideration.

An obvious question a reader may have is, "This is ancient history. Is any of this

important?" As our analysis progressed, it became more and more clear that this study

is in fact very important.

The reason is that Elliott Theorists have observed that we are ending a Grand Super

Cycle Impulse Wave in the period from 1998 to 2000. During the research by the

authors of this work a question arose. Is the GSC Wave now nearing its end the first,

second or third impulse GSC Wave in the next higher degree wave, the X Wave? The

answer to this question will determine the depth and duration of the coming

correction.

Much additional data had to be accumulated and digested to learn the answer. This

search took us back to the end of the last Ice Age and uncovered the waves described

above. This research has convinced the authors that in this period of time just prior to

the 21st Century, the GSC Wave being completed is the third complete GSC Impulse

Wave of an X Wave which started in about 1000AD.

When a wave of any degree ends, the Elliott Principle says we can expect a correction

of that wave commensurate with the degree of the wave ending. It makes a great deal

of difference to a market observer in 1999 to know that we are not just ending a GSC

Wave, but also an X Wave.

This is important because our study of history shows that a reasonable correction for a

GSC Wave lasts about 40 to 60 years. However, for an X Wave the duration of the

correction appears to be 100 years or more. Obviously, even the shorter correction

will boggle the minds of current market participants who have been taught by market

action over the last few decades to expect bear markets of only a few days, weeks or

months.

The data and history used in this discussion will concentrate on Western Civilization,

starting in the Middle East and progressing through Greek, Roman, European, English

and finally United States history. Readers who are unfamiliar with the Elliott Wave

Principle will perhaps have difficulty following the wave sequences described in the

text. To overcome this difficulty, an elementary discussion of the Principle has been

included in Appendix A. We recommend to those who are unfamiliar with the Elliott

Principle to not dwell on the intricacies of the wave sequences, but to focus on the

conclusions drawn by the authors based on their study of the Principle. If this

monograph stimulates your interest in the subject, there are several good books you

can read for a more complete understanding of the Principle.

Many readers will perhaps have a tendency to dismiss the findings and conclusions

drawn by the authors in this article. The reasons for this are several. The most obvious

will be that the Principle itself is too esoteric. Another reason is many people distrust

technical analysis in any form, and this Principle relies heavily on technical analysis.

Still other market participants are just too optimistic, have too much faith in

technology and the future of humankind to listen to any long term bearish arguments.

It is the opinion of the authors, after much research and thoughtful consideration, to

say to the reader that they ignore the message the Elliott Wave Principle and this

article are sending to them at their peril.

A study of history clearly indicates that humankind has progressed over time in a

series of up and down periods (waves). The story of human development is certainly

not an unbroken upward movement. There have been many regressive periods that

have interrupted the upward path. There is every reason to believe that future events

will repeat and confirm this type of up and down movement in human development.

Various studies have shown the Elliott Wave Principle to have been operative over

many decades. The results of the study you are about to read indicate that the Elliott

Wave Principle is apparent in the entire 12,000-year span of human history that is the

theme of this study. Using this knowledge allows the authors to reach some very

interesting conclusions about the future of human activity and the Western stock

markets and economies as we go into the Twenty First Century. These will be

discussed in subsequent parts of the article.

(C) 1999 By The Authors

All rights reserved

SETTING THE STAGE

Why should we care about the long-term outlook for the stock market?

First let's discuss what we mean by "Long Term". Most people consider long term to

be a few years at the most. Most businessmen seem to be preoccupied with the next

quarter and at the outside, next year. Long term as used by us in this article will be

much longer. Twelve thousand years long, which makes this effort a very ambitious

undertaking.

Now let's go back to why we should be interested in these long-term periods of

history. "History repeats itself," is a common saying. A study of the Elliott Wave

Principle lends validity to this statement, as we will endeavor to demonstrate here. As

the reader will appreciate, obtaining reliable data for stock market series going back

over many years is difficult. Fortunately, there is reasonably reliable data available,

which can be used going back several hundred years. There is also a large body of

human history going back to the beginning of civilization, which we can draw upon.

Readers who understand the Elliott Principle know that when we look at the larger

degree waves and see the simple and elegant eight-wave structure, we must realize

this is less true when we try to analyze the smaller degree waves. We find in the

smaller degree waves a great deal of diversity which is often difficult to fit into the

wave pattern. We also find that there is a great deal of variation in corrective waves,

which Elliott and his followers tried to codify.

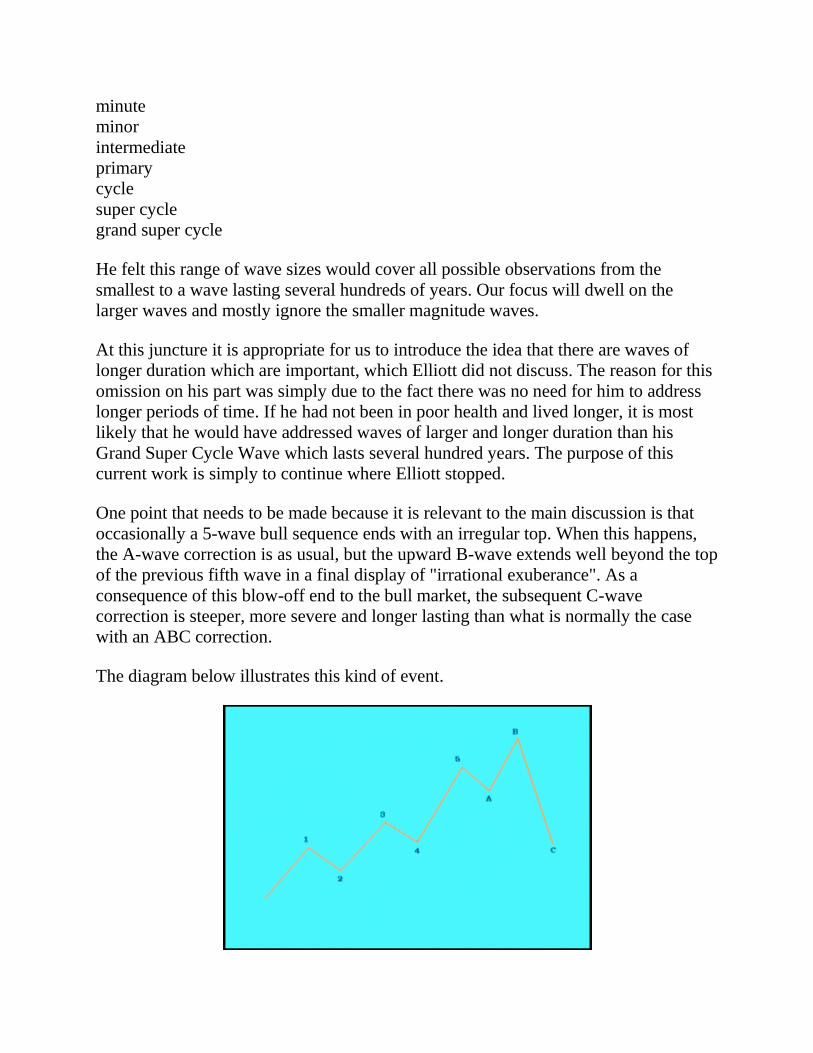

In addition, fifth waves can become extension waves of a bull trend. When this occurs

it usually surprises and confuses Elliott analysts. This makes accurate wave analysis a

risky business from a forecasting point of view. This problem has tripped up most

practitioners of the Principle at one time or another, with embarrassing results. This

very thing happened in 1995 when a fifth wave became an extension wave.

Extension waves are typical of major blow-off in the markets, at times becoming a

complete market bubble with all the signs typical of such developments. Our first

discussion therefore hinges on more recent history to illustrate that we are

experiencing extension waves and, therefore, that we are in the process of a market

blow-off. This leads to the conclusion that global markets, which have been largely

sustained and driven by Wall Street and American imports, are due to enter a major

correction, again lead by events on Wall Street.

The question of how large this correction might be is evaluated later.

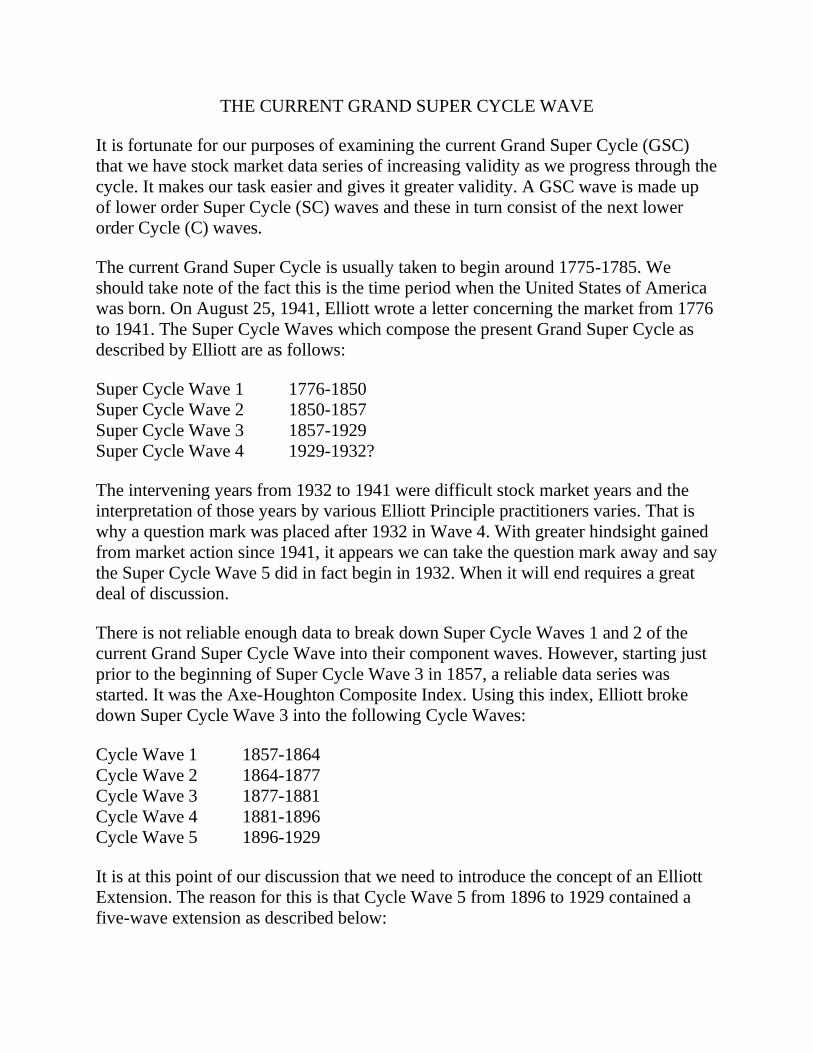

THE CURRENT GRAND SUPER CYCLE WAVE

It is fortunate for our purposes of examining the current Grand Super Cycle (GSC)

that we have stock market data series of increasing validity as we progress through the

cycle. It makes our task easier and gives it greater validity. A GSC wave is made up

of lower order Super Cycle (SC) waves and these in turn consist of the next lower

order Cycle (C) waves.

The current Grand Super Cycle is usually taken to begin around 1775-1785. We

should take note of the fact this is the time period when the United States of America

was born. On August 25, 1941, Elliott wrote a letter concerning the market from 1776

to 1941. The Super Cycle Waves which compose the present Grand Super Cycle as

described by Elliott are as follows:

Super Cycle Wave 1 1776-1850

Super Cycle Wave 2 1850-1857

Super Cycle Wave 3 1857-1929

Super Cycle Wave 4 1929-1932?

The intervening years from 1932 to 1941 were difficult stock market years and the

interpretation of those years by various Elliott Principle practitioners varies. That is

why a question mark was placed after 1932 in Wave 4. With greater hindsight gained

from market action since 1941, it appears we can take the question mark away and say

the Super Cycle Wave 5 did in fact begin in 1932. When it will end requires a great

deal of discussion.

There is not reliable enough data to break down Super Cycle Waves 1 and 2 of the

current Grand Super Cycle Wave into their component waves. However, starting just

prior to the beginning of Super Cycle Wave 3 in 1857, a reliable data series was

started. It was the Axe-Houghton Composite Index. Using this index, Elliott broke

down Super Cycle Wave 3 into the following Cycle Waves:

Cycle Wave 1 1857-1864

Cycle Wave 2 1864-1877

Cycle Wave 3 1877-1881

Cycle Wave 4 1881-1896

Cycle Wave 5 1896-1929

It is at this point of our discussion that we need to introduce the concept of an Elliott

Extension. The reason for this is that Cycle Wave 5 from 1896 to 1929 contained a

five-wave extension as described below:

Cycle Wave 5 (Extension Wave 1) 1896-1899

Cycle Wave 5 (Extension Wave 2) 1899-1907

Cycle Wave 5 (Extension Wave 3) 1907-1909

Cycle Wave 5 (Extension Wave 4) 1909-1921

Cycle Wave 5 (Extension Wave 5) 1921-1929

Elliott describes in a letter dated May 3, 1944, how Extension Wave 5 of Cycle Wave

5 (1921-1929) also became an extended wave of five waves, which ended in a

colossal blow off in the fifth wave of this sequence between 1927 and 1929. Figure 1

shown below gives us a picture of Super Cycle Wave 3, with its component waves.

FIGURE 1

Super Cycle wave 3 consists of 5 Cycle waves (I) to (V). Cycle wave (V)

in turn is made up of 5 extension waves, I to V. The fifth extension wave,

V, also consists of 5 extension waves, 1 to 5.

Super Cycle Wave 4, which was the corrective wave for the entire bull market from

1857 to 1929, turned out to be fast, violent, traumatic, and ushered in a very bad

period for America. We will not dwell on that point since there are many sources of

information on that period of American History.

We are now ready to attack Super Cycle Wave 5 (1932-????). Figure 2 below displays

the yearly price range for the Dow Jones Industrial Average from 1900 to the top

made in early 1999. Please note the y-axis is logarithmic scale.

FIGURE 2

Bar chart of Dow Jones Industrial Index, 1900-1999

From Figure 2, we can clearly see the cycle waves making up Super Cycle Wave 5

break down as follows:

Cycle Wave 1 1932-1937

Cycle Wave 2 1937-1942

Cycle Wave 3 1942-1966

Cycle Wave 4 1966-1974

Cycle Wave 5 1974 – 1999/2000?

Cycle Wave 5 (1974 –1999/2000?), brings us closer to a period of stock market

history familiar to many current stock traders. Cycle waves consist of what Elliott

termed Primary Waves and the five Primary Waves that make up Cycle Wave 5 are as

follows:

Primary Wave 1 1974-1976

Primary Wave 2 1976-1982

Primary Wave 3 1982-1986

Primary Wave 4 1986-1987

Primary Wave 5 1987-1999/2000?

Figure 3 below gives us a schematic picture of Super Cycle Wave 5 (1932-1999?).

Readers should note at this point in our discussion that the same basic schematic was

used for both Super Cycle Waves 3 and 5 (Figures 1 and 3). The Elliott Wave

Principle does indeed seem to have form and structure.

FIGURE 3

Super Cycle wave 5 of the current Grand Super cycle breaks down into

Cycle waves (I) to (V). The extensions take place as described in Figure

1.

We can further see from Figure 3 that Primary Wave 5 (1987-1999?), of Cycle Wave

5 (1974-1999?), of Super Cycle Wave 5 (1932-1999?), started from the low made in

1987. This point is emphasized because of its great significance – we are approaching

the end of the fifth waves of three orders of waves. It is also very important to

recognize that we are therefore in the process of ending a Grand Super Cycle Wave

(GSC – the largest wave Elliott recognized). This implies a sizable correction is ahead

of us – greater than the one that followed the 1929 Crash. More on that important

topic is to come later.

The wave action from 1994 to 1998 is complex and may find differing counts by

various Elliott analysts. For example, many analysts treat the July 1998 top in the

Dow as the end of wave 5 of the Cycle and Super Cycle. The correction that started

with the virtual collapse of the Russian financial system then becomes a major A

wave correction. This is followed by a rising B wave that exceeded the high of the

previous fifth wave. This constitutes an irregular top, which is also, a sign of a market

blow off. Alternative counts try to fit the end of wave 5 to the highs reached in 1999.

Using any of these wave designations does not in any way change the fact that all of

the evidence points to the end of a Grand Super Cycle in the 1998-2000 time frame,

and therefore to a major correction just ahead.

Table 1 shown below, lists the important waves from 1780 to the present time in 1999

in terms of Grand Super Cycle, Super Cycle and Cycle waves.

TABLE 1

This table shows the elements of the most recent Grand Super Cycle

wave which is indicated as GSC?, where '?' can be 1, 3 or 5. Each wave

with its components in a column to the right is shown with start and end

dates and duration in years. More recent waves are shown in greater

detail. In the next part of this monograph we will determine whether this

is the 1st, 3rd or 5th grand super cycle wave of the present X-wave.

Even though the Table does not show this clearly, it is of great importance to

remember that the bull trend concluded with Extension Waves. In the Elliott

Principle, an Extension Cycle is evidence of a highly speculative market.

As was mentioned earlier, there are also striking similarities (in Elliott terms as well

as other criteria) in stock market behavior between the period of 1921-1929 and 1987-

1998(9).

IMPLICATIONS

Indications suggest there is a very high probability that over the period 1998-2000 we

have come to the end of a Grand Super Cycle Elliott Wave, the largest size wave

Elliott listed in his wave descriptions. The bull phase of this cycle started about 1776

and has lasted over two hundred years. When the bull phase of any cycle ends, the

logical conclusion is that we are going to start the bear (correction) phase associated

with this cycle. Each correction phase of any cycle degree is commensurate with the

preceding bull phase it is correcting.

We are ending a Grand Super Cycle Bull Market, so we can expect at the very least a

Grand Super Cycle Bear Market Correction.

The question now to be discussed is whether this is a GSC1, GSC3 or GSC5 wave of

the larger X-wave. If the current GSC wave is a GSC1 or GSC3, the correction will be

shorter and of less intensity than the correction which would occur at the end of the

GSC5 wave. We must realize any GSC correction is bound to be worse than the one at

the end of the previous Super Cycle in 1929.

If we are dealing with a GSC5 wave, the correction would be more extensive as it

would also come at the end of the next higher order X-wave.

(C) 1999 By The Authors

All rights reserved

12,000 YEARS OF ELLIOTT WAVES

Part 3: The current X-wave.

A SECOND STARTING POINT

We are going to use as our second starting point a historical period that most

historians can agree upon, both in timing and in its impact on human endeavor - the

Renaissance. From this vantage point we are going to work backward in time and then

go forward in our effort to place ourselves at the proper spot in the current Elliott

Wave sequence.

The term Renaissance, which describes the period of European history from about

1400AD to 1720AD, is derived from the French word for rebirth, and originally

referred to the revival of the values and artistic styles of classical antiquity. Voltaire in

the 18th century classified the Renaissance in Italy as one of the great ages of human

cultural achievement. In the 19th century, Jules Michelet and Jakob Burckhardt

popularized the idea of the Renaissance as a distinct historical period heralding the

modern age, characterized by the rise of the individual, the birth of scientific inquiry,

geographical exploration, and the growth of secular values.

This historical evidence allows us to theorize that the estimated 320-year period of the

Renaissance can be categorized as a Grand Super Cycle in the Elliott Wave scheme of

things. Historical facts of the following type bolster this belief. The Black Death

(bubonic and pneumonic plague), which devastated Europe in the mid-14th century

and reduced its population by as much as one-third, created chaotic economic

conditions. Labor became scarce, industries contracted, and the economy stagnated. It

is logical to theorize that this downward adjustment in economic progress with a

duration of about 50 years can be designated as a Grand Super Cycle Wave correction

– either a wave 2 or a wave 4.

To find out which it is, we have to go further back in history. The long period of

human expansion from the end of the Dark Ages in about 1000AD until it was ended

by the plague in about 1350AD, also has a duration of about 350 years. It is thus

logical to believe that this period can be designated as another Grand Super Cycle

impulse wave.

By comparison with what appears to be a normal Grand Super Cycle Wave correction

of about 50-60 years, the extended period of 663 years of the Dark Ages appears far

too long to be a mere Grand Super Cycle correction. Therefore, we can conclude it is

a correction of at least the next higher degree, which we have termed the X-wave. We

therefore concluded that the period of expansion following the Dark Ages has to be

Grand Super Cycle Wave 1 of a new X-wave at least, with the decline in economic

activity as a result of the plague as Grand Super Cycle Wave 2 – the first corrective

wave of the current X-wave.

This analysis then allows us to logically designate the Renaissance as Grand Super

Cycle Wave 3 in the forgoing sequence. Additional evidence that the Renaissance was

Grand Super Cycle Wave 3 is the way it ended in about 1720, when a speculative

blow off of gigantic proportions occurred, events that are typical of either a wave 3 or

wave 5.

The end of the final bull phase of the Renaissance Grand Super Cycle 3 is so

important for us to understand, and of such important historical significance, we are

going to discuss it in detail. The story involves a man named John Law. He was born

in April 1671, and died Mar. 21, 1729. He was a Scottish financier whose brilliant but

overly speculative banking and stock market projects in France during LOUIS XV's

minority created a spectacular but short-lived economic boom.

Law persuaded the near-bankrupt French government to test his theory that state

credit schemes based on public confidence could greatly increase national wealth. In

1716 his government-chartered General Bank began to issue paper currency and

provide low-interest loans to businesses. At the same time Law's Company of the

West, organized in 1717, sold 100 million livres of stock based on the potential wealth

of its monopoly over France's Louisiana Territory (the MISSISSIPPI SCHEME,

which later became the INFAMOUS MISSISSIPPI BUBBLE).

By 1720, Law was controller general of finance in France. In that year he merged his

bank and company into a vast financial organization that assumed control of state

debts, coinage, and taxation. During the final stages of the speculative bubble that

developed from his policies and actions, prices rose in a spectacular fashion. It all

ended in panic public selling later in the year of 1720, which destroyed the entire

scheme. The idea of state banking was discredited for nearly a century, and Law

became a disgraced and bankrupt exile. For his efforts, he won the title of The Father

of Paper Money.

Concurrently in England, a similar scenario was being played out. The South Sea

Bubble is the name given to a speculative boom in England that also collapsed in

1720. The South Sea Company founded for trade in 1711 caused this financial

disaster. Stock in the company sold well, and by 1718 investors were receiving 100

percent interest. In 1720 the company proposed and Parliament accepted that it take

over much of the national debt. This move created a wave of speculation in the

company's stock, which rose from 128.5 pounds in January to 1,000 pounds in

August. In September the bubble burst. Stocks plummeted, banks failed, and investors

were ruined. A reader who wishes to learn more about this fascinating era can do so

by obtaining a book titled Extraordinary Popular Delusions and the Madness of

Crowds by Charles Mackay.

These twin disasters on each side of the English Channel marked the end of the bull

phase of Grand Super Cycle Wave 3 and ushered in Grand Super Cycle Wave 4, a

downward correction wave. Our knowledge of these waves must be entirely based on

historical evidence, since there are no readily available records of equity prices for the

period of the Renaissance. It is instructive to note this final (bull) phase of the Grand

Super Cycle 3 ended in the Mississippi Bubble in France and the South Sea Bubble in

England. Both have been described since then as notorious periods of excessive

speculative activity.

The aftermath of these bubbles left finance in extreme disrepute during the corrective

phase following the Renaissance Grand Super Cycle, which lasted from 1720 until

approximately 1775-1785 (GSC Wave 4). At this point we should especially take note

of the length of time required to overcome the excesses brought about at the end of

this Grand Super Cycle. It required about 60 years, at least one full generation

(perhaps more like two generations based on life expectancy at that time) before the

correction ended and a new GSC impulse wave could begin (GSC Wave 5).

Since we are again at the end of a GSC wave, this is the least duration we could

reasonably expect for the correction that is soon to be on us. What we can expect at

the end of a GSC5 wave, must await further analysis.

THE X-WAVE AND BEYOND

We have seen that the period of the Dark Ages was followed by three periods of about

350 years duration that correspond to three Grand Super Cycle impulse waves,

separated by relatively brief corrections of about 60 years duration – one correction at

the time of the Plague and the second correction as a result of the major speculative

bubbles in France and in England in the 18th century.

The duration of the Dark Ages was very much longer than these GSC corrections – so

much longer in fact that it has to be at least the next higher order X-wave correction,

or even of higher order. We can therefore assume that the start of the first GSC wave

in about 1000 AD was also the beginning of the next higher order X-wave.

This enables us to put together the schedule of the current X-wave, as follows:

GSC 1: 1000 – 1350

GSC 2: 1350 – 1400

GSC3: 1400 – 1720

GSC4: 1720 – 1780

GSC5: 1780 - 1999

Observe that this X-wave has a duration of exactly 1000 years, substantially longer

than the 350 years or so of Elliott's longest wave, the Grand Super Cycle.

The major components of the X-wave are shown in Figure 5 below.

FIGURE 5

The X-wave and its components

One of the keys to the further analysis of human history in terms of Elliott waves lies

in the duration of the Dark Ages. At more than 650 years, this period is far too long to

be merely an X-wave correction. It has to be at least a correction at the end of a Y-

wave, which then implies that the current X-wave that started in 1000 AD is X1 of a

new Y-wave. This also implies that the coming correction is not simply going to be a

GSC correction wave, such as at the time of the Plague or after the Mississippi and

South Sea bubbles; it will be more substantial and of longer duration.

This means that the current state of the markets deserve closer examination before we

continue the examination of the whole 12000 year history of settled human

civilization.

A MORE IN DEPTH ANALYSIS

Let's get some much-needed perspective of where we are and where we have been in

stock market prices. In July of 1998 the DJIA soared over the 9000 level and has since

gone over 11000. Many stock market pundits remark that the future looks rosy with

few problems lurking on the horizon. They predict continuing higher prices. Some

expect the DJIA to climb to 15000 or even 20000. We have seen this index surge over

11,000 since July 1998, while other broader indices have not been able to top their

1998 highs.

Looking back to as recently as early 1995, the DJIA had not breached the 4000 level,

which is obviously more than 50% lower than the peak in 1998. Needless to say, for

various reasons the DJIA advanced over 100% in a little over three years. A

spectacular achievement (evidence of an Elliott Extension in the market and extreme

speculation and overvaluation). In late 1996 while the DJIA was still under 7000,

Alan Greenspan issued his famous warning that the United States stock market was

displaying "Irrational Exuberance". The market swooned a little, and then continued

to race upward for another two years, gaining another roughly 50% in the process.

What allowed this to happen? Let's remember we have been in a Grand Super Cycle

bullish mode since about 1776, when the United States was born. The country grew

ever stronger and richer during the 220 odd years since that time. By the 1940's the

US had grown to the point where it was able to become the dominant power in the

world during and after WW II. Our riches and power continued to build during the

Cold War until by the last two decades of the Twentieth Century the United States

was the colossus of the world. A famous Wall Street personality, Abbey Cohen, in the

late 1990's described the economy of the United States as being similar to a loaded

crude oil supertanker cruising through the ocean. Which implies the United States has

so much bullish momentum built up that it would be as hard to stop or to change its

upward course as a supertanker (which is indeed very difficult).

The growth of the United States and attitudes like those of Abbey Cohen were the

causes for the explosive move up in the DJIA. This view is simplistic, and does not

account for other important factors which aided and abetted the rise such as the

computer revolution. Space will not allow a full discussion of all aspects of the

matters touched on in this article. The important point we need to make is that the

final upward surge in the last two decades of the 20th Century is the culmination of

220 odd years of economic growth and business activity. It constitutes an

unsustainable euphoria and enthusiasm for stocks, and deserves the description of a

"Bubble Economy"

This situation is comparable to the speculative frenzy described in the period leading

up to 1720 in the South Sea and Mississippi Bubbles, or the speculative frenzy of

1927-1929. The implication of this is that we can logically expect these speculative

excesses to be corrected by a major bear market move. This is all the more true since

we are not only completing a Grand Super Cycle of over 200 years, but are

completing the final Grand Super Cycle of an X-Wave which has very serious

implications. Namely a bear market correction which will be very deep and probably

over 100 years in length.

We must now ask ourselves what conditions have changed to stop this bull market, if

in fact it has changed from bull to bear. Our judgment based on Elliott analysis, Dow

Theory analysis, and other evidence, tells us that 1998 was the culmination of the

Grand Super Cycle which started over 200 years ago. Others disagree. Time will tell.

Looking back to 1994-95, some analysts felt the market had already reached the top at

that time. There was evidence which suggested that was the case. What was missed

was the supertanker analogy, and the fact that you don't turn a supertanker or a 200

plus year bull market around quickly. It takes time and work (quite often, as in this

case, such time and work takes on the aspects of a BUBBLE Market). There are times

when no specific trigger is needed to stop a bull market. The bull market just

continues upward until it loses momentum and starts to slide back down.

In the period of 1997-9, however, there were and still are many conditions in the US

and around the world, which have contributed to a market top. We will not try to

enumerate all of these items, because we feel certain anyone interested enough to read

this article is already aware of these items of concern. One item that needs mentioning

(But by no means the only one) is the Year 2000 Computer Date Problem, and how

that can perhaps initiate or exacerbate the bear market to come. This impact of the

Y2K problem may overshadow all of the other preceding problems in order of

magnitude.

At or near the end of a cycle, psychology plays a critical role. Let's look at something

Greenspan has said: "the fate of the markets is in the hand(s) of psychology". The

psychology at the end of a Grand Super Cycle bull market is without question,

insanely bullish and positive. Logic would say this is even more the situation at the

end of a higher level X-Wave. That bullish psychology may well be starting to

weaken. As a bear market progresses along its inevitable path, the bearish psychology

will build until a point down the road is reached when no one in their right mind

wants to own stocks. It is that attitude which held sway between 1720 and 1776 and

that extended the correction to over a generation of humans. Is there any reason why

something similar or worse won't happen again? Based on Elliott analysis we think it

will. The all-important question is how long will the bear market last and how low

will it go. In Part 5 we discuss some factors that could be implicated in the coming

long term bear market.

There is a quote we want to share with you that comes from Richard Russell, who

writes an authoritative stock market letter based on Dow Theory. Russell's warning:

"In a bear market, whatever can go wrong will go wrong. This adage explains why

bear markets often end up lower (more costly) than anyone thinks possible at their

inception."

Let's revisit Abbey Cohen and her supertanker analogy. It appears the supertanker US

stock market spent the spring and summer of 1998 slowing down, stopping, and

reversing direction. The rally from the lows made in the last half of 1998 was aided by

Federal Reserve policy when they were forced to bail out Long Term Capital

Management. Despite reaching new highs during 1999, in what we believe to be an

Elliott irregular top, that rally shows signs of weakening, and we may be on the verge

of another major downward move in stock prices.

Will the supertanker stock market and economy go down as persistently as it went up?

The question is, why not? We believe psychology will be just as bearish an influence

on the way down as it was bullish on the way up. That will be especially true when

psychology turns from bullish to bearish which is something that always happens at

turning points of this type. We feel certain there will be disagreement on this, so, only

time will tell. We do feel there is some very persuasive additional evidence for the

pessimism expressed above. It is code named Y2K.

Our supertanker economy stalled in mid 1998 for many reasons, some we have

mentioned. However, we have only slightly begun to feel the negative impact of Y2K

as this article is being written. We are not going to discuss Y2K in great detail

because the scope of the subject is too large to add to this narrative. If the reader is

unfamiliar with the problem we suggest you immediately get current information and

bring yourself up to date quickly.

In our considered opinion, Y2K will most likely turn out to be one of the biggest

problems civilization has faced since the beginning of recorded history on a global

scale. It will likely be the trigger, if another is needed, that could propel the world into

a chaotic and violent bear market worthy of the previous Grand Super Cycle (1776-

1998) and X-Wave (1000-2000) bull market it will correct. If the problems and

disruptions Y2K can inflict on humankind turn out to be anywhere near as bad as the

pessimists predict, and this trouble is piled on top of a world economy and world

stock markets already in trouble and headed lower, we can see the negative

ramifications. It will pay prudent individuals to monitor both Y2K and the current

stock market developments closely. People who live through the next few years

without taking reasonable precautions will fare much worse than those that do.

There is ample evidence that this market is way too high and should have a large

correction. As to how low the DJIA will go, we turn to the Elliott Principle. It says a

decline from this Grand Super Cycle Wave and X-Wave can and should ultimately

drop to 1000 points or below. The reader, who questions this, can go to the Elliott

writings for confirmation. This prediction is based on 1999 nominal dollars. If the

value of the dollar changes either up or down, that will alter the value of the DJIA in

nominal dollars at the time of the low. This is not an effort to hedge the prediction. On

the contrary, it is meant to clarify the situation.

What are prudent precautions people can take, you may ask? There are several. First

to preserve wealth one should exit most stock market investments. This will be hard

for many to do. In the last twenty years at the very least, the investing public has been

bombarded with the notion that the way to financial Valhalla is to buy stocks and keep

them for the long pull. It is easy to see why such an investment philosophy would take

hold during the fifth wave of a Super Cycle, which also is ending the fifth wave of a

Grand Super Cycle.

The problem here is that the wisdom of the "Buy and Hold" philosophy is based on

historical performance. If the bull market standpoint itself is history (evidence

suggests it is), then this "Buy and Hold" philosophy is all wrong. This suggests a

prudent individual will unlearn "Buy and Hold" and replace it with "Get Out and Stay

Out" until the start of the next bull market which history says will be a long time in

coming.

Where do you put the money you take from stocks? The answer to this question is

always very difficult. In the looming bear market it is further complicated by the Y2K

problem, which may change everything. The authors are not going to discuss in detail

the merits of various alternative investments to the stock market. It is again not within

the scope of this article. We will simply mention some possible alternative

investments and leave it to the reader to do his or her own research on what to do.

Some possibilities are bonds, cash, gold and other hard money assets, food and other

emergency supplies, and real estate, to name a few obvious choices. (A comment from

Richard Russell on the value of cash in a bear market: "In a bear market cash acts

almost like a short position since cash will buy more and more stocks as the bear

market progresses and equities decline").

There are undoubtedly other possibilities we do not know about. In all of your

considerations about alternative investments, one very important consideration to keep

firmly in mind is the vulnerability of fiat paper currencies. Recent history has

witnessed the extreme depreciation of various fiat paper currencies around the world.

All fiat paper currencies are vulnerable to one degree or another. This includes the US

dollar, which is a fiat paper currency whether we want to believe it or not. The

investment world during the next few years is going to be extremely dangerous to

your wealth, as well as your mental and physical health. Keep in mind that one way

governments could try to ameliorate the effects of the soon to come long term bear

market would be by printing money – a course of action that could result in serious

inflation and loss of purchasing power.

A GSC correction lasts about 50-60 years. We are looking now at not just a GSC bear

correction, but a correction commensurate with an X-Wave.

A review of Table 2 in the next part shows that history tells us a normal correction for

an X-Wave is 100 years or more. The implication we see from this information is that

we can expect a very deep and extended drop in stock prices from the apparent top

being completed in 1998-2000. More on that later. In addition, the correction should

severely depress the global economy for a period of many years (100 or more). From

the evidence of the Elliott count it is unreasonable to believe this correction will be

over in a few months, years or even a decade or two. We are correcting too long and

too large a cycle for it to be over in a hurry, or without inflicting major pain. Not

happy implications. However unhappy the implications may be, the evidence

presented in this article make them realistic.

SUMMARY

As we approach the end of the 20th Century, we find the world's economies,

currencies, stock markets, and politics in disarray. Leadership in world affairs is sadly

lacking. Both the IMF and the World Bank have fallen on hard times and dropped into

disfavor. When we evaluate the United States Stock Market with these facts in the

background, it should not come as a surprise to anyone that there is credible evidence

of a looming turn downward in stock market direction and psychology.

We have in fact tried very diligently to show in this article that there is good evidence

to suggest such a market turnaround from bull to bear is upon us. In addition we have

gone to great lengths to demonstrate the bear market we are facing is going to be

much more severe than 1987, 1974, or even 1929. We have stated our reasons to

suggest the bear market will resemble the bear market period between 1720 and 1776,

a period of a generation in length and of great severity in degree of market and

business decline. We have discussed why this bear market can be even worse that just

previously described, since we are ending an X-Wave. These are sobering thoughts to

contemplate in our current bullish and positive environment.

These are dire possibilities. This places us at a point where we must ask ourselves this

question: How much validity does the Elliott Wave Principle have and how seriously

should people take these horrible prospects? Based on our study of the Elliott

Principle over several decades, we can say the Principle has great enough validity to

convince us to watch its signals carefully and pay attention to them. Each reader will

have to decide how much weight to give the Elliott Principle, after examining the

evidence presented in this article, as well as other sources. We should all keep in mind

that Elliott Wave interpretations can change over time as more data is amassed and

evaluated. We feel fairly certain that any practitioner of this Principle has had to

change an analysis at sometime in his or her career.

The last item to cover in this summary is to remind ourselves that in a serious bear

market, which can last for many years, a "Buy and Hold" policy is not prudent

(contrary to popular belief as fostered by the Wall Street Community). A more

prudent approach is to exit most stock market investments and replace them with

alternative investments. Each investor must decide for himself or herself the best

course of action to take after careful consideration of the facts.

Let us reiterate one last time. The investment world during the next few years is going

to be extremely dangerous to your wealth, as well as your health.

BEYOND THE COMING BAD TIMES

It is terribly important at this phase of our analysis to go back to a thought that may

have gotten misplaced in all of the bearish gloom of the recent paragraphs. Each

correction wave, of any degree, does not go as low as the low of the previous cycle.

The correction only approaches the previous low. A most important and positive

thought to remember is that after the correction, the upward progress of humankind

resumes and new highs will ultimately be made.

If we remember that at the end of this century we are ending the first X-Wave of the

new Y-Wave of Z3-Wave, then we can look forward to the beginning of the third X-

Wave of this Y-Wave after a correction wave (X2) has been completed. This suggests

we are on one side of a valley of human achievement, and that once we have

negotiated the difficult valley, we can look forward to better times and new highs of

advancement on the other side. The end of civilization is not upon us, just a rather

lengthy pause in the upward march of civilization. Unfortunately, most people in 1999

can only see the beautiful highlands on the other side of the valley, and do not realize

there is a deep abyss to negotiate between where they now stand and the beautiful

future that is painted for humankind in the 21ST Century and beyond.

(C) 1999 By The Authors

All rights reserved

12,000 YEARS OF ELLIOTT WAVES

Part 4: Elliott Waves over the past 12000 years

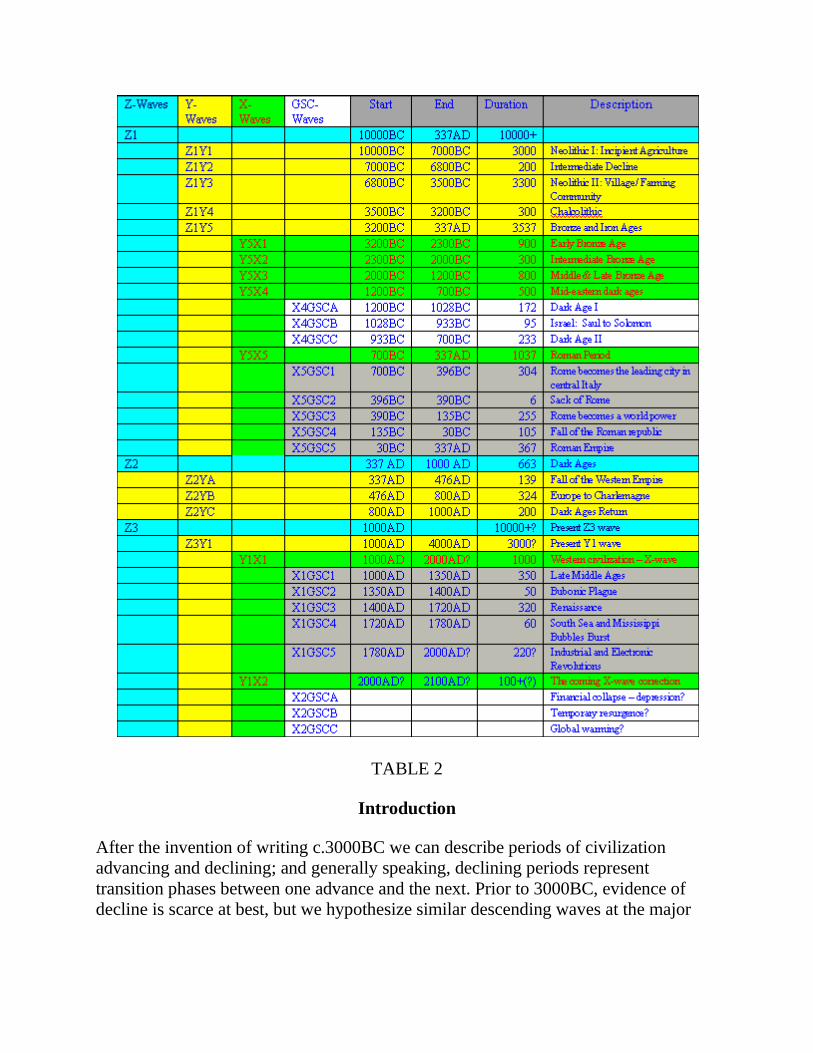

Table 2 below shows the full extent of Elliott waves from 10000 BCE. The notes that

follow discuss the work that underlies this presentation of history.

TABLE 2

Introduction

After the invention of writing c.3000BC we can describe periods of civilization

advancing and declining; and generally speaking, declining periods represent

transition phases between one advance and the next. Prior to 3000BC, evidence of

decline is scarce at best, but we hypothesize similar descending waves at the major

transition points between ascending waves of pre-history, based on the evidence of

later periods.

The earliest Sumerian literature, the Epic of Gilgamesh written soon after 3000BC, is

a semi-legendary account of a Sumerian king of Uruk, who lived a century or two

before the epic was written. The prior destruction of civilization is a central theme of

the epic, with tablet X describing a quest for the survivor of the Flood, and tablet XI

describing the Flood. Thus, the earliest human literature lends credence to the

hypothesis of pre-historic declines.

The ancient Egyptians also believed that civilizations rise and fall, as evidenced by

this passage in Socrates' discourse with Timaeus : "Thereupon one of the (Egyptian)

priests , who was of very great age, said, O Solon, Solon, you Hellenes are never

anything but children, and there is not an old man among you.

Solon in return asked what he meant.

I mean to say, he replied, that in mind you are all young; there is no old opinion

handed down among you by ancient tradition, nor any science which is hoary with

age. And I will tell you why. There have been, and will be again, many destructions of

mankind arising out of many causes; the greatest have been brought by the action of

fire and water, and other lesser ones by innumerable other causes."

Readers may view the outlook of this work as negative or fatalistic, but this is not our

intent. As for the charge of fatalism, history proves that strong individuals can buck

the prevailing trend, with examples shown here: Ramses III in Egypt, Tiglath-pileser I

in Assyria, and Marcus Aurelius in Rome. As for the charge of negativity, it should be

noted that whether a decline is caused by weaknesses in the preceding advance or by

forces external to that advance, the declining period lays the foundation for the next

upward wave. Therefore, these declines appear critically important to human

development.

One final note about dating. The abbreviation "c." (as in c.2000BC) means circa or

"roughly", and dates become rougher and less reliable the farther back we look. Even

in cases where "c." is omitted, it cannot be assumed that dates are exact. Different

sources give conflicting dates for the reigns of various kings, for example, and there

are numerous other dating problems. Our goal has been to achieve the maximum

accuracy possible, given these limitations, but we cannot be certain of the ancient

wave counts as presented, only the general pattern.

Z1: c.10000BC to 337AD.

This great ascending wave encompasses the period from the beginning of the

Neolithic Revolution to the height of the Roman Empire, a span of some 10,000 years.

Z1Y1 to Z1Y3: c.10000BC to c.3500BC. The Neolithic Age

During the Neolithic Revolution mankind began the domestication of plants and

animals, enabling the production of sufficient food to allow free time for other

pursuits. Neolithic man developed through two levels, each lasting some three

millenia, 1) Incipient Agriculture, and 2) The Village/Farming Community Level,

representing waves Z1Y1 and Z1Y3 respectively.

Z1Y1: c.10,000BC to c.7000BC. Incipient Agriculture

During this period man developed pottery, weaving, and improved tools, abandoning

the flint tools of the Old Stone Age for ground stone tools. Domesticated dog bones

have been found from c.8700BC.

Z1Y2: c.7000BC to 6800BC. Intermediate Decline

We hypothesize a period of decline between the two levels of the Neolithic, based on

evidence of decline at the later transition points. Based on the length of declines of

later X and Y waves, we judge that Z1Y2 must have lasted at least two to three

centuries. Because human progress in Z1Y1 was slow and modest, the depth of the

decline may also have been modest, leaving little or no evidence in the archaeological

record.

The Wave Principle suggests, furthermore, that Z1Y1 and Z1Y3, preceding and

following Z1Y2, were composed of lesser waves (X waves, grand super cycles

(GSCs), and super cycles (SCs). It is impossible for us to identify these smaller waves

and their associated declines, but we do understand the causes of decline during the

Neolithic. This is because the agricultural revolution brought a number of risks with

it, including:

1. Degradation of the soil. Overgrazing and failure to rotate crops caused

many of the earliest settled areas to become desolate regions even to this day. Much of the world's deserts are man-made.

2. Disease. Increasing human populations in closer proximity brought the risk of epidemic.

3. Famine. Man became dependant on weather. Crops were also at risk

from insects and other animals.

4. Pollution. Towns developed long before sanitation.

5. Loss of freedom. Freedom of movement was lost in the transition from nomadic to sedentary life.

6. Security problems. Sedentary life creates wealth, which in turn creates

security risks. The development of town walls testifies to this threat,

particularly from nomadic groups on the fringes of civilization. This was

a primary cause of the Bronze Age declines, and persisted as a threat at

least through the Mongol conquests in the 13th century AD.

7. Class strife. Sedentary life creates economic classes. This can lead to

oppression of the lower classes by the elites (evidenced in Gilgamesh) and uprisings by the lower classes against the elites.

Z1Y3: c.6800BC to c.3500BC. Village/Farming Community Level

Farming villages appeared first in the Fertile Crescent, then in Egypt c.5000BC.

Fertile Crescent phases are as follows:

1. Jarmo Phase (Iraq) by c.6750BC. Cultural exchanges existed over

hundreds of miles. Man was domesticating wheat, barley, pea, sheep, cattle, goats, pigs, and horses.

2. Hassunan Phase, to c.4800BC. Advanced architecture, larger villages,

improved and more aesthetic pottery.

3. Halafian Phase. Round "tholos" style houses, possible copper

metallurgy.

4. Eriduan Phase. Recognizable temple made of mudbrick.

5. Ubaidian Phase. Before c.4000BC. Threshold of urban life. Town-sized sites. Temples display some monumentality.

Z1Y4: c.3500 to c.3200BC. Chalcolithic

This transition between the Neolithic and Bronze Ages was a period of incipient

copper use, for decorations, tools, and weapons. Reference materials show an

extremely wide range of dates for the Chalcolithic, because a handful of metal objects

date from well before 3500BC. We have defined this period narrowly, corresponding

to the Two Kingdoms period in Egypt.

1. Sumeria (c.3200BC): Jemdat Nasr Period. A mildly declining

archaeological period prior to the reign of Gilgamesh that is associated

with the Flood legend.

2. Egypt (c.3500BC-c.3200BC): Upper and Lower Egypt were frequently at war with each other.

3. Anatolia (c.3500BC-3200BC): Sites from this period are more fortified

than previously and were often destroyed by violence (eg. Mersin and

Hacilar).

Z1Y5: c.3200BC to 337AD. Bronze and Iron Ages

Man learned to make bronze by mixing tin with copper, launching civilization to new

heights. Iron was discovered by the Hittites in the latter years of their empire and

maintained as a closely guarded secret. With the disintegration of the Hittites

c.1200BC, the use of iron spread to other countries, coinciding with the advent of a

long dark age.

Z1Y5X1: c.3200BC to c.2300BC. Early Bronze Age

1. Sumeria (c.3200BC-2325BC): While the emergence of Sumer can be

traced to c.4000BC or before, Bronze Age Sumeria ran from c.3200BC

to 2325BC. Sumeria reached the peak of its power under the reign of

Lugalzaggasi 2350BC to 2325BC, bordering the Mediterranean Sea and

Persian Gulf.

2. Egypt (c.3200BC-2281BC): Dynasties I-VI (Proto Dynastic and Old

Kingdom Periods). Menes, the first true historical figure, founded the

first dynasty by uniting Upper and Lower Egypt c.3200BC. This period

reached its peak during Dynasty VI, with trading , exploratory, and

military expeditions well beyond Egypt's borders. This superficial

greatness masked great underlying stresses, however, due primarily to

high taxation and over-centralization of power.

3. Anatolia (c.3200BC-c.2100BC): Local areas were consolidated under

the rule of kings. Troy levels I and II date from this period. Troy II was a

powerful fortress during the majority of the early Bronze Age. It rests

upon the ruins of a lesser settlement that may date from the late Chalcolithic.

Z1Y5X2: c.2300BC to c.2000BC. Intermediate Bronze Age

1. Sumeria (2325BC-c.2000BC): Sumeria was conquered at the height of

its power in 2325BC by Sargon of Akkad. The Sumerians temporarily

reasserted themselves c.2100BC during a period of turmoil throughout

Mesopotamia. Descending Elliott waves exhibit an A (down) B (up) C

(down) pattern, and the reassertion of the Sumerians c.2100BC may

represent the B wave of X2 for them. The Sumerians ceased to exist as a distinct people c.2000BC.

2. Egypt (2281BC-2050BC): Dynasties VII-X (First Intermediate Period).

Discontent and a spirit of rebellion at the end of wave X1 led to

destruction of the old order. Dynasty VII, which opened this period, was

an oligarchy of 70 men who ruled for a mere 70 days. Wave X2 is

characterized by banditry and internecine warfare, foreign invasion and

temporary occupation of the Delta, plunder of burial sites and decline of

religion, and a major transfer of wealth, impoverishing many nobles and

enriching some commoners. Not surprisingly, the writing of this period expresses a longing for the better days of the bygone era.

3. Anatolia (c.2100BC-c.1900BC): Dates are particularly hazy here. Many

of the early Bronze Age towns were looted and destroyed by 2000BC,

including Troy II. Troy levels III-V, associated with this period, had

smaller walls than Troy II. Small houses were confined within narrow lanes.

Z1Y5X3: c.2000BC to c.1200BC. Middle and Late Bronze Ages

1. S. Mesopotamia (c.2000BC-c.1200BC): The First Babylonian Empire

was founded c.2000BC, containing many cultural elements of the earlier Sumerians. It existed until c.1200BC.

2. N. Mesopotamia (c.2000BC-c.1200BC): The emergence of Assyria

dates from c.3000BC, but the period of their military development was

from c.2000BC to c.1200BC. (Assyrians invented the sword in this period.)

3. Egypt (2050BC-1167BC): Dynasties XI-XIX (ended 1200BC). After a

period of revival and another decline, Egypt achieved the height of its

power under the reign of Thutmosis III 1491BC-1449BC. The last great

pharoah was Ramses III 1198BC-1167BC, the second pharoah of Dynasty XX.

4. E. Anatolia (c.2000BC-c.1200BC): The Hittites existed as a people from

c.2000BC to c.1200BC. They developed in three phases, allowing us to

describe their grand super cycles roughly as GSC1&2) Early Hittites

c.2000BC-c.1700BC, GSC3&4) Hittite Kingdom c.1700BC-c.1430BC, and GSC5) Hittite Empire c.1430BC-c.1200BC.

5. W. Anatolia (c.1900BC-1200BC): Troy VI, founded c.1900BC, had

walls 16 feet thick, with several gates and towers. Buildings were

pretentious with numerous pillars and columns still in evidence.

Destroyed by earthquake c.1300BC, it was rebuilt as Troy VIIa, which is

considered the Troy of Homer's Iliad.

6. Greece (c.1900BC-c.1200BC): Achaean invaders conquered Greece

c.1900BC, establishing their principle city at Mycenae. They were conquered in turn by invading Dorians between 1200BC and 1100BC.

7. Crete (c.1950BC-c.1200BC): Middle and Late Minoan. The earliest

inhabitants of Crete date from c.3000BC, with Bronze Age villages

dating from c.2500BC. A sudden urbanization c.1950BC (probably

brought by Semitic peoples) began the Middle Minoan period , which is

considered the start of true Minoan civilization. Initially Minoan Crete

held sovereignty or influence over the Achaean Greeks, and a joint

culture developed between the two. Control passed to Greek hands

c.1400BC (destruction of Knossos) and Homer relates that King

Idumeneus of Crete fought under King Agamemnon of Mycenae at Troy

(c.1200BC).

8. Italy: c.2000BC the ancestors of the Latins brought the Bronze Age to

the peninsula.

Z1Y5X4: c.1200BC to 700BC. Early Iron Age - The First Dark Age

The advent of the Iron Age coincided with collapse of the Bronze Age civilizations.

Z1Y5X4A: c.1200BC to 1028BC. Early Dark Age - Destruction of the Bronze Age

Cultures

1. S. Mesopotamia: The First Babylonian Empire was destroyed by the

Hittites and/or Assyrians c.1200BC.

2. N. Mesopotamia: Assyrian power declined from c.1230BC to 1116BC.

Under the leadership of Tiglath-pileser I (1116BC-1093BC) Assyria

became the dominant state in the Middle East. Decline continued starting around 1050BC as a migratory wave of nomads swept the region.

3. Egypt: Invasion by Peoples of the Sea c.1200BC at the start of Dynasty

XX. Ramses III (1198BC-1167BC) repelled the invasion, as well as

threats from the Philistines and Libyans. This was a temporary respite, as Egypt began a long decline after Ramses' death.

4. E. Anatolia: The Hittites were destroyed c.1200BC by invasion of

Peoples of the Sea from the Aegean, and attacks from the mountainous Gashga tribes.

5. W. Anatolia: Troy VIIa was destroyed by fire c.1200BC.

6. Greece: Achaean culture destroyed by invading Dorians c.1200BC.

Athens alone survived. Mycenae was reoccupied by Achaeans, but destroyed by 1100BC.

Z1Y5X4B: 1028BC to 933BC. Israel - The Reigns of Saul, David, and Solomon

A corrective wave such as X4, massive both in depth and duration, should evidence a

discernable upward wave B in its center; and it is exactly at this point that the Bible

describes the wealth and glory of Solomon's reign in Israel (I Kings, Chapter 10).

Z1Y5X4C: 933BC to 700BC. Dark Age Continues

1. Mesopotamia: Assyria experienced a resurgence under Ashurnasirpal II

and Shalmaneser II (883BC-824BC), followed by continued decline

under weak successors. As this period was drawing to a close, Assyria

reached the height of its power under Tiglath-pileser III (745BC-

727BC). The Fall of Assyria was 612BC.

2. Egypt: Decline continued during this period. Conquered by Ethiopia c.730BC.

3. Greece: Early formation of the states that later comprised Classical Greece.

Z1Y5X5: 700BC to 337AD. The Roman X Wave - from the founding of Rome to

Constantine

Around 700BC, mankind resumed its upward march. Carthage was founded in the 8th

century; and as mentioned above, Assyria reached its peak in the decades leading up

to 700BC. The emergence of the Medes was near the beginning of this X wave; and

Persian history from Cyrus (559BC-530BC) to Xenophon's Anabasis/revolt of Cyrus

the Younger (401BC-400BC) completes the first grand super cycle (GSC1) of X5.

The New Babylonian Empire (612BC to 538BC) had its existence entirely within

GSC1, representing the third super cycle (SC3) of that grand super cycle. Spartan

history from Lycurgus (c.700BC) through the Peloponnesian War (ended 404BC)

corresponds with GSC1, and this grand super cycle also corresponds with Athenian

history from the end of monarchy in 683BC to the end of the Peloponnesian War. The

period of Olympic Games 776BC-393AD corresponds roughly with X5.

A critical phase of monetary history, the development of coinage, also corresponds

with GSC1 of X5. The first royal mint was established in Lydia c.700BC producing

the first crude coins made of electrum, a natural alloy of gold and silver. By the end of

GSC1, coinage dominated Mediterranean commerce, having reached the peak of

engraving and artistic quality. During GSC1, annual world silver production was

about 1.5 million ounces, with 2/3 coming from the Laurium mines near Athens.

From the standpoint of monetary history, GSC1 ended in 407BC, during the

Peloponnesian War. Sparta captured Laurium and freed 20,000 slaves there, thus

severing Athens from her money supply. Athens responded by issuing silver-plated

bronze coinage (406BC-405BC) and the populace began hoarding silver, the first

known application of Gresham's Law.

Because Roman history serves as the precursor to European history, we will follow

the wave patterns after 700BC through Rome. We have used DuPuy & DuPuy, The

Encyclopedia of Military History (p.12) as the authority on the founding date of the

city, as opposed to the more traditional date of 753BC. Better histories are available

for this X wave, allowing us to identify the super cycles and grand super cycles that

compose it.

GSC1: 700BC to 396BC. Rome becomes the leading city in central Italy

SC1 (700BC-c.600BC): Century of warfare with Etruscan neighbors.

SC2 (c.600BC): Defeat by the Etruscans.

SC3 (c.600BC-509BC): Prosperity under the Tarquins (Etruscan Kings).

SC4 (509BC-496BC): Revolt. Establishment of the Roman Republic in 509. Struggles

with relatives of the Tarquins attempting to regain the throne.

SC5 (496BC-396BC): Expansion of Rome. Rome became the leading city in central

Italy with the destruction of the Veii in 396BC

GSC2: 396BC to 390BC. The sack of Rome

In 390BC Rome was sacked by the Gauls, who occupied the city for months. The

Gauls failed to capture the citadel, which housed the Roman treasury, because the

cackle of geese warned the Romans of impending attack. In gratitude, a shrine was

dedicated to Juno Moneta, goddess of warning, and from this event we get the words

"mint" and "money".

GSC3: 390BC to 135BC. Rome becomes a world power

Rome continued its growth in three phases with many setbacks and near disasters

along the way, 1) the consolidation of Latium by 343BC, 2) The consolidation of Italy

by 265BC, and 3) the achievement of world power status by 146BC.

SC1 (390BC-343BC): Consolidation of Latium. Establishment of a Latin

confederacy.

SC2 (343BC-338BC): Uprising of Latin allies in the Latin War 340BC-338BC.

SC3 (338BC-265BC): Consolidation of Italy was completed with the conquest of

Rhegium in 270BC, and defeat of a Samnite uprising soon afterward.

SC4 (265BC-242BC): Early defeats in the First Punic War (Carthage). By 249BC

Rome had suffered four major disasters at sea losing over 200,000 men and 700

warships to storms alone. With the fleet rebuilt in 242BC, Carthage was defeated in

241BC. This victory provided Rome with her first province overseas, in western

Sicily (at the start of SC5).

SC5 (241BC-135BC): Rome becomes a world power. With the defeats of Macedonia,

Greece (Achaean War) and Carthage (Third Punic War), all in 146BC, Rome became

mistress of the Mediterranean world.

GSC4: 135BC to 30BC. Fall of the Roman Republic

Just as Rome achieved world power status she was ripped apart by internal disorders

and class warfare. This chaotic period includes the First Servile War 135BC-132BC,

assassination of the democratic tribune Tiberius Gracchus in 133BC, Revolt of

Fregellae (Roman allies) 124BC, Second Servile War 104BC-99BC, the Social War

91BC-88BC, Roman Civil War (Marius/democrats vs Sulla/aristocrats) 88BC-82BC,

Third Servile War (Spartacus) 73BC-71BC, the insurrection of Cataline during

Cicero's consulship 63BC, the Great Roman Civil War (Caesar/democrats vs Pompey

/aristocrats 50BC-44BC, Wars of the Second Triumvirate (following Caesar's

assassination) 43BC-34BC, assassination of Cicero by agents of the Second

Triumvirate, and the War of Octavian Against Anthony 33BC-30BC, all of which led

to the fall of the republic.

GSC5: 30BC to 337AD. The Roman Empire through Constantine

The Pax Romana period 30BC-162AD comprises the first 3 super cycles of GSC5.

The Julian Dynasty and the chaos following Nero's death comprise SC1 and SC2.

SC1 (30BC-54AD): Early Pax Romana, from Augustus to Claudius. This super cycle

also corresponds to the gold standard established by Augustus.

SC2 (54AD-69AD). Nero (54-68AD) plus the Year of Four Emperors (69AD). Nero

is known for his persecution of Christians, and for the burning of Rome as part of his

city planning scheme. He also ended the gold standard of Augustus, reducing the

weight and fineness of silver coinage, and the weight of gold coinage.

SC3 (69AD-162AD): Later Pax Romana, from Vespasian to the beginning of the

Eastern War.

SC4 (162AD-268AD): Decline of Empire. Marcus Aurelius (161AD-180AD) was the

best and last of the five "good" emperors of the Pax Romana. With his death in

180AD, the empire was clearly in decline, but the Pax Romana is considered to end in

162AD, since Marcus spent virtually his entire reign fending off external threats to the

empire.

SC5 (268AD-337AD): Revival under the Illyrian Emperors through Constantine.

Z2: 337AD to 1000AD. Correction Wave for Z1

Interpreting this wave is crucial to understanding 1999 from an Elliott Wave

standpoint. From 1000 to 1999 civilization has advanced for a millenium, and it is

fairly easy to define this as an X-wave composed of 5 grand super cycle waves. But is

the current X-wave the first X-wave of the current Y-wave, or could it be the third or

fifth X-wave?

A key to answering this question lies in the length and severity of the decline that

preceded 1000. This decline continued for seven centuries, which is too long to

represent the correction of the Roman X Wave, a mere 1000-year advance. This must

be the correction of a higher order wave, either Y or Z. Our interpretation, looking at

all of the advances and declines of mankind, is that this wave corrected the entire

10,000 years that preceded it. Therefore, we judge the present X-wave (1000-1999) as

the first X-wave of the first Y-wave of Z3.

Z2A: 337AD to 476AD. Fall of the Western Empire

After Constantine the decline of empire continued until the abdication of Romulus

Augustus, the last emperor, in 476. By 366 Roman money was so debased that the

government refused to accept its own coinage in payment of taxes. The city of Rome

was sacked by the Vandals in 455, and by 476 the western empire was no more than a

pitiful shell. This A wave corrected the entire Roman X Wave (Z1Y5X5).

Z2B: 476AD to 800AD. Early European History to Charlemagne

This period marked the early development of European states culminating in the

crowning of Charlemagne as Holy Roman Emperor in 800. At the height of the B

wave, as we would expect, there is some faint semblance of the former glory of Rome.

Charlemage played a role for Christendom in Z2B similar to Solomon's role for the

ancient world in Z1Y5X4B, providing a brief moment of glory in the midst of an

otherwise bleak age. The Vikings began raiding Europe in 809, near the end of

Charlemagne's reign (771-814).

Z2C: 800AD to 1000AD. The Dark Ages

The Encyclopaedia of Military History (p.243) says this about the period: "This, the

darkest period of the Middle Ages, was characterized by aimless and anarchic strife."

This final horrible decline corrected not only X5 (Roman history), but the prior X and

Y waves of Z1 as well.

Z3: 1000AD to c.11000AD. Present Z Wave

"The farther back one looks, the farther in the future one may see," Winston Churchill.

Z3Y1: 1000AD to c.4000AD. Present Y Wave.

Z3Y1X1: 1000AD to c.2000AD. Present X Wave: Modern Man

Description of this period is contained in Parts 2 and 3. Additional notes follow.

GSC1: 1000AD to 1350AD. Late Middle Ages

Coalescence of European states, particularly England and France. Rise of the Italian

maritime powers: Venice, Genoa, and Pisa. Because the Renaissance (GSC3) began in

Italy, we will follow the Italian wave patterns in GSC1.

SC1 (1000-1096): Venice dominated the Adriatic after defeat of Dalmatian pirates in

1000 and capture of Bari from the Moslems 1002. Pisa and Genoa drove the Moslems

from Sardinia 1005-1016.

SC2 (1097-1102): Venice lost the Dalmatian coast during a war with Hungary.

SC3 (1102-1170): Pisa at the height of its power in the 1100s.

SC4 (1171-1196): Venetian setbacks. Defeated in war with Byzantium 1171. Failed

efforts to retake Dalmatia 1172-1196.

SC5 (1197-1359): Commercial rivalry of Genoa and Venice. The Republic of

Florence issued the gold florin in 1252, the first European gold coin since the fall of

Rome. Genoese nobles overthrown 1359 and replaced with an elected Doge.

GSC2: 1350AD to 1400AD. The Black Death (Bubonic and Pneumonic Plague)

Southern Europe was stricken in 1347, with Western Europe stricken in 1348 and

Northern Europe stricken in 1349. By the end of 1350 two thirds of all Europeans had

contracted the plague with a mortality rate of 50%, resulting in 25 million deaths.

Europe was struck by succeeding waves every few years through 1398, with declining

mortality rates in each wave. Local outbreaks continued into the 1700s. The epidemic

was a disaster economically in the latter half of the 14th century as inflation raged and

commerce ground to a near halt during the acute labor shortage. During this period

there were mass mental aberrations, agrarian revolts, a moral decline, and a reduced

level of education.

GSC3: 1400AD to 1720AD. Renaissance

SC1 (1400-1479): Early Renaissance SC2 (1479-1495): Setbacks for the Italian states

1. Venice: declined following defeat by the Turks and loss of territory in

1479.

2. Naples: French invasion 1494-1495.

3. Rome: Reign of Pope Alexander VI 1492-1495. His son, Caesar Borgia,

wrecked the power of the wealthy families of Rome.

4. Pisa: Failed to regain independence from Florence.

SC3 (1491-1588): The Spanish Century, from the unification of Spain under

Ferdinand and Isabella (conquest of Granada) in 1491 to the Spanish Armada in 1588.

Colonization of the New World. The Colombian (cultural) Exchange. Spanish

dominance of Europe.

SC4 (1588-1618): Spanish power went into decline after the Armada. Banking

crisis/bank failures in northern Italy in the late 1500s.

SC5 (1619-1720): The Century of Fiat Credit. Venice established a state bank, Banco

della Piazzo del Rialto, in response to the Italian banking crisis. Venice then invented

fiat credit in 1619 by creating another bank, Banco del Giro, with credit against the

state rather than a deposit of specie. The Bank of England was established 1693 near

the end of the super cycle. Holland's Tulipmania was during this super cycle, and the

South Sea Bubble and Mississippi Scheme brought the period to a close.

GSC4: 1720AD to 1780AD. South Sea and Mississippi Bubbles Burst

The dates chosen for GSC4 correspond to the bear market in England following the

collapse of the South Sea Bubble in 1720. In France, the collapse of the Mississippi

Scheme the same year led to great financial distress. By the reign of Louis XVI (1774-

1791), the worsening financial crisis and a succession of finance ministers culminated

in the calling of the States-General in 1789 to address the problem. We consider the

French Revolution, beginning with the calling of the States-General, to be the start of

GSC5 in France.

GSC5: 1780AD to c.2000AD. Industrial and Electronic Revolutions