080911 isa indystat - 24 hour memo - indianapolisindygov.org/egov/mayor/documents/isa indystat -...

TRANSCRIPT

1

Date: September 11, 2008 To: Mayor Ballard From: Michael Huber and Kristen Tusing, Office of Enterprise Development Re: IndyStat – ISA meeting Friday 9/12/08 CC: Paul Okeson, Chief of Staff

Sarah Taylor, Director of Constituent Services David Reynolds, Controller Chris Cotterill, Corporation Counsel Kevin Ortell, Interim Chief Information Officer The following issues were highlighted in the August 8th ISA IndyStat meeting and appeared in the ISA IndyStat follow-up memo: Financial Follow-up Action. What are ISA’s fixed assets? Provide a breakdown of expenses by category. Ordinance Follow-up Action. What jurisdiction does the current ordinance give to ISA? What issues arise from the ordinance? Applications/Implementation Follow-up Action. Provide the prioritization or ranking of current enterprise application implementation (property assessment system, business intelligence tool, etc.). How are applications prioritized on a regular basis? Does the ISA board or CIO set the prioritization of projects? User Fees/ Charge Backs Follow-up Action. How frequently is the user count audited for non-users? What is the rate per user? How are fees set? Helpdesk Costs Follow-up Action. What is the average cost per help desk phone call? What is ISA doing to reduce helpdesk phone calls by having users fix issues themselves?

Indy StatAccountability in Action for the City of Indianapolis

2

Online Services Follow-up Action. Provide information on what departmental services can be offered online, and are in the process of becoming online services to reduce operational costs. In what ways can we increase web visits? What aspects of the website can be improved? ERP Follow-up Action. Has a cost-benefit analysis been conducted on an ERP system? What were the results? What are the estimated costs of such a system? Potential Issues for Discussion

• Describe the division of labor between ISA’s major contractors (Northrop Grumman, Daniels and Associates) and ISA’s in-house staff. When do Northrop Grumman’s and Daniels and Associates’ contracts expire?

• How does ISA measure its own staff to determine their effectiveness? Does it use the

performance data displayed in this month’s IndyStat presentation to monitor staff performance?

• What is the difference between “enhancement requests” and “development requests”? It

appears that hours for enhancement requests have increased in 2008 while hours for development requests have decreased.

• Why are Average Page Views per Day down in 2008? What can we do to better promote

IndyGov.org? What is meant by Average User Sessions per Day?

• What is GIS’ primary role and what types of GIS requests are the most common? How can we better utilize GIS and/or communicate to City departments the capabilities of GIS?

ISA IndyStatSeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

Actual to Budgeted Operating Expenses

$0.00

$1,000,000.00

$2,000,000.00

$3,000,000.00

$4,000,000.00

$5,000,000.00

$6,000,000.00

$7,000,000.00

Jan-08Feb-08Mar-0

8Apr-0

8May-08

Jun-08Jul-08Aug-08Sep-08Oct-0

8Nov-0

8Dec-0

8

Actual Expenses

Projected Budget Based on Spend Rate from 2005, 2006 and 2007 expenses

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

Actual to Budgeted Revenues

$0.00

$1,000,000.00

$2,000,000.00

$3,000,000.00

$4,000,000.00

$5,000,000.00

$6,000,000.00

$7,000,000.00

$8,000,000.00

Jan-08Feb-08Mar-0

8Apr-0

8May-08

Jun-08Jul-0

8Aug-08Sep-08Oct-0

8Nov-0

8Dec-0

8

Actual Revenues

Projected Budget Based on Spend Rate from 2005, 2006 and 2007 revenues

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

Top Ten Vendors for July

$0.00 $200,000.00 $400,000.00 $600,000.00 $800,000.00 $1,000,000.00 $1,200,000.00

Dell Gov't Leasing & Lease Admin. Center

IBM Corporation

DELL GOVERNMENT LEASING

PVD NET LLC

Crowe Chizek

WOOLPERT, INC.

Ameritech Services, Inc. d/b/a AT&T Midwest Servic

DANIELS ASSOCIATES, INC.

CHASE EQUIPMENT LEASING

NORTHROP GRUMMAN - NGCIS

Series1

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

Staffing Levels

05

101520253035404550

Jan-08Feb-08Mar-0

8Apr-0

8May-08

Jun-08Jul-08Aug-08Sep-08Oct-0

8Nov-0

8Dec-0

8

UnfilledFilled

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

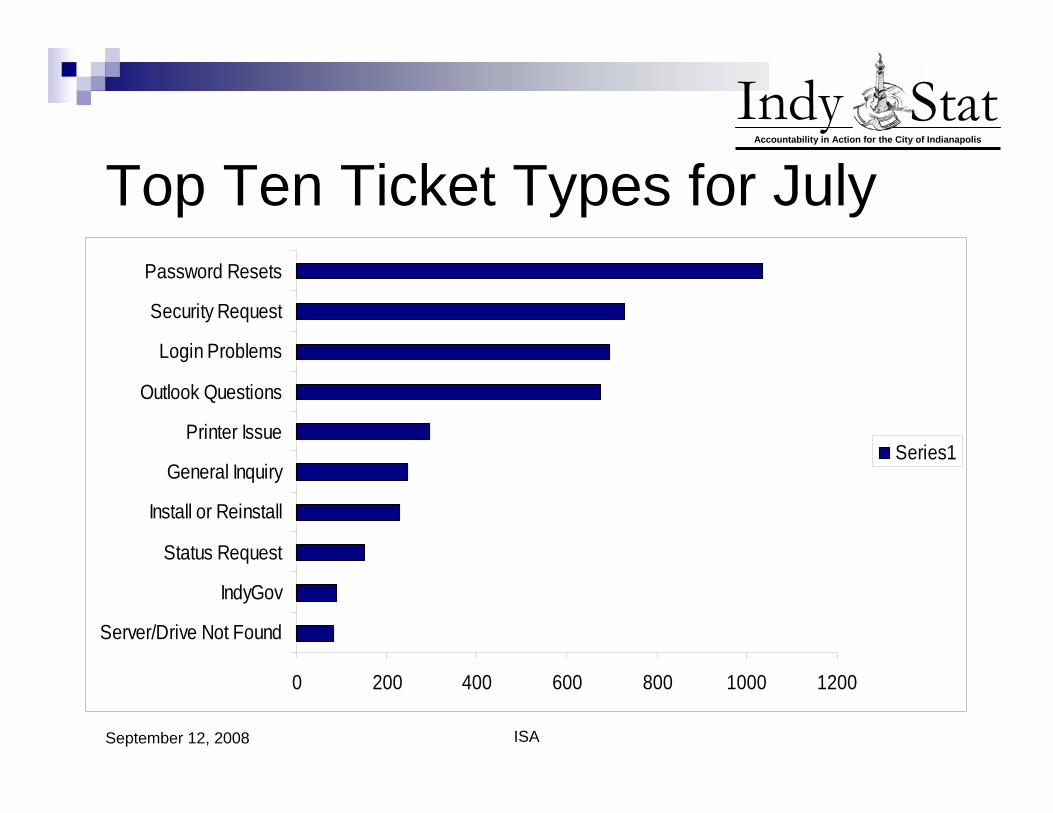

Top Ten Ticket Types for July

0 200 400 600 800 1000 1200

Server/Drive Not Found

IndyGov

Status Request

Install or Reinstall

General Inquiry

Printer Issue

Outlook Questions

Login Problems

Security Request

Password Resets

Series1

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of IndianapolisTop 10 Applications

Supported in July 2008

0.00 200.00 400.00 600.00 800.00 1,000.00 1,200.00

Tidemark/Siebel Interface

Siebel CRM

FileNet

Database Administration

GEAC HR E-Series Payroll/Personnel

Property System

Inheritance Tax System

Tidemark Advantage

JUSTIS

Multi-Application

Hours Spent

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

Top Ten Hours by Agency for July

0 100 200 300 400 500 600 700 800 900

County Treasurer

MAC

IMPD

OFM

County Assessor

DPW

DMD

ISA

Courts

Multi-Agency/Departments

Hours

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of IndianapolisTop Ten Departments

Requests for July

1041

736431

213

210

156

154

142

104

89 IMPDMCSDCourtsDPWProsecutorCriminal ProbationAssessorPublic DefenderIFDForensic Services

3276 Requests

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

Direct Customer Requests

0

1000

2000

3000

4000

5000

6000

7000

Aug-07Sep-07Oct-0

7Nov-0

7Dec-0

7Jan-08Feb-08Mar-0

8Apr-0

8May-08

Jun-08Jul-08

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

Average Speed to Answer

0

5

10

15

20

25

Aug-07

Sep-07

Oct-07

Nov-07

Dec-07

Jan-08

Feb-08

Mar-08

Apr-08

May-08Jun

-08Jul-0

8

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

Active Directory By Department

2130

1491

1189729614

537

500

372

343

287

2241IMPDMCSDIFDProbationProsecutorCourtsDPWPublic DefenderParksDMDOther

10433 Total Active

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

First Call Resolution

0%10%20%30%40%50%60%70%80%90%

100%

Aug-07Sep-07Oct-0

7Nov-0

7Dec-0

7Jan-08Feb-08Mar-0

8Apr-0

8May-08

Jun-08Jul-0

8

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of IndianapolisApplication Services-

Hours By Requested Type (April 2007- July 2008)

0.00

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

April 2

007

May 20

07Ju

ne 20

07Ju

ly 20

07Aug

ust 2

007

Septem

ber 2

007

Octobe

r 200

7

Novembe

r 200

7

Decembe

r 200

7

Janu

ary 20

08

Februa

ry 20

08Marc

h 200

8Apri

l 200

8May

2008

June

2008

July

2008

General Support RequestProblem RequestLogin/Password RequestEnhancement RequestDevelopment Request

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of IndianapolisApplication Services-

Service Request by Request Type (April 2007- July 2008)

050

100150200250300350400450

April 2

007

May 20

07Ju

ne 20

07Ju

ly 200

7Aug

ust 2

007

Septem

ber 2

007

Octobe

r 200

7

Novembe

r 200

7

Decembe

r 200

7

Janu

ary 20

08

Februa

ry 20

08Marc

h 200

8Apri

l 200

8May

2008

June

2008

July 2

008

General Support RequestProblem RequestLogin/Password RequestEnhancement RequestDevelopment Request

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

GIS Background Queries

0

10000

20000

30000

40000

50000

60000

70000

80000

Janu

aryFeb

ruary

March

April

May June July

Augus

tSep

tembe

rOcto

ber

Novembe

rDecem

ber

2008 Validation2008 Query2007 Validation2007 Query

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

Number of Telephone Work Orders

0

200

400

600

800

1000

1200

05/01/2007thru

05/31/2008

Jun-08 Jul-08 Aug-08

Number of Telephone WorkOrders

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of IndianapolisNumber of Telephone

Troubled Tickets

0

100

200

300

400

500

600

700

800

05/01/2007thru

05/31/2008

Jun-08 Jul-08 Aug-08

Number of Trouble Reports

ISASeptember 12, 2008

Indy StatAccountability in Action for the City of Indianapolis

Next ISA IndyStat MeetingFriday, October 10th

9:00amRoom 260

Information Services Agency (ISA)

CCiittyy ooff IInnddiiaannaappoolliiss--MMaarriioonn CCoouunnttyy

EEnntteerrpprriissee RReessoouurrccee PPllaannnniinngg

NNeeeeddss AAnnaallyyssiiss

IInnffoorrmmaattiioonn SSeerrvviicceess AAggeennccyy

FINAL

July, 2008

PPrreeppaarreedd ffoorr::

DDaavviidd RReeyynnoollddss –– OOFFMM CCoonnttrroolllleerr

SShhiittaall PPaatteell –– IISSAA CCIIOO

JJooiinnttllyy PPrreeppaarreedd bbyy::

TThhee IISSAA BBRRMM SSttaaffff && PPrreemmiiss CCoonnssuullttiinngg

GGrroouupp

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 2

TTaabbllee ooff CCoonntteennttss

1 Glossary of Terms ................................................................................. 3 2 Report Overview ................................................................................... 4

2.1 About this Report ...................................................................................................... 4 2.2 Related Documents ................................................................................................... 4

3 Executive Summary ............................................................................... 5 4 Current Situation ................................................................................... 7

4.1 Objectives & Benefits ................................................................................................ 7 4.2 Financial and Human Resources Systems at the City/County ................................... 7

5 ERP Analysis Findings ........................................................................... 9 5.1 Overview – Understanding Existing Processes .......................................................... 9 5.2 Current Budget Process Analysis ............................................................................ 10 5.3 Finding 1: Paperwork & Shadow Systems ............................................................... 13 5.4 Finding 2: Unsupported Technology ........................................................................ 14 5.5 Finding 3: Data Currency Issues ............................................................................. 15 5.6 Finding 4: Manual calculations, reconciliation & quality assurance ......................... 16 5.7 Finding 5: Labor Intensive Functions ...................................................................... 17

6 Market Research ................................................................................. 19 6.1 Overview ................................................................................................................ 19 6.2 Market Research Findings ....................................................................................... 19

7 Net Present Value (NPV) Analysis ....................................................... 21 7.1 NPV Overview ......................................................................................................... 21 7.2 NPV Findings .......................................................................................................... 21

8 Appendix ............................................................................................. 24 8.1 Appendix A: ERP Process Workflows ....................................................................... 24 8.2 Appendix B: Additional Findings ............................................................................. 45 8.3 Appendix C: ERP FTE Matrix .................................................................................... 49 8.4 Appendix D: Net Present Value (NPV) Charts.......................................................... 50 8.5 Appendix E: Misc Project Related Information ........................................................ 56

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 3

11 GGlloossssaarryy ooff TTeerrmmss

Word/Acronym Definition

ADPICS Advanced Purchase Inventory Control System (Purchasing

mainframe system)

BPREP Budget Preparation

(Budget mainframe system)

BRM Business Relationship Manager

CFO Chief Financial Officer

Enterprise Refers to the City/County agencies supported by ISA

ERP Enterprise Resource Planning - A management information

system that integrates areas such as manufacturing, planning,

purchasing, asset inventory, sales, marketing, finance, human

resources, etc.

ISA Information Services Agency

IT Technology supported by the Information Services Agency

FAACS Fixed Asset and Accounting Control System

(Asset Management mainframe system)

FAMIS Financial Accounting and Management Information System

(Financial mainframe system)

FOCUS Software program used to extract information from the

mainframe system

FTE Full Time Employees

INFOR Payroll mainframe system

MBE/WBE Minority Business Enterprise / Woman Business Enterprise

OFM Office of Finance and Management

OTIS Online Time Information System

RFP Request for Proposal

Shadow System Set of records maintained at a local level independent of the

official records, usually in Excel spreadsheet or an Access

Database

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 4

22 RReeppoorrtt OOvveerrvviieeww

22..11 AAbboouutt tthhiiss RReeppoorrtt

This report contains an analysis of the strategic and operational effectiveness of the City of

Indianapolis and Marion County‟s (here after referred to as “the City/County”) current financial

and resource planning systems and processes.

The purpose of this report is to provide the City/County leadership with a clear and substantiated

ERP Business Case/Needs Analysis and discussion document that highlight‟s the following:

The current state (strengths and weaknesses) of the systems, tools and processes used by

the City/County to function as an ERP system today

The current manual and automated processes (workflows) used as a means of identifying

how and which aspects of the current systems, tools and processes could be better served

(or replaced) by implementing an ERP system

A cursory review of ERP solutions available in the market today

A preliminary Net Present Value (NPV) analysis for implementing a new ERP system

Premis Consulting Group led the business process review workshops with the participation of the

BRMS in the lead departments: OFM, Auditor‟s Office, and HR. They documented the business

process workflows from those workshops, developed the FTE survey, provided the justification

criteria and spreadsheet for the NPV analysis and identified the support costs of the current

system.The BRMs developed the findings in this report, researched the ERP market, supplied the

supporting proof of the findings and wrote the resulting report.

22..22 RReellaatteedd DDooccuummeennttss

The related documents used in conjunction with this project are:

The ERP “Pre & Post” Workflows: Attached in Appendix A (also available in Visio and Adobe

Acrobat versions)

The ERP FTE Matrix: Attached in Appendix C

The ERP Net Present Value (NPV) Matrix: Attached in Appendix D

The ERP Needs Analysis – Planning Document: (available in MS word format)

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 5

33 EExxeeccuuttiivvee SSuummmmaarryy

The City/County has been working with an antiquated financial system that was introduced in the

1970‟s. With the exception of MCSD, which runs a legacy Personnel system on an unsupported

platform, the City/County is working without a human resource system. Since then, technology

and processes have substantially evolved, revealing significant shortcomings in the ability of the

City/County to manage its finances and human resources with the system. Because of this,

Information Services Agency (ISA) was asked to put together a business case to assess the

current status, needs and feasibility of implementing a new ERP system.

Over the past few years, elected officials and the City/County Council have agreed to allow the

financial oversight of nearly all local government to be administrated by OFM. The overall goal of

this unification is to create one standardized way of reporting, budgeting, processing transactions

and overseeing finances. However, the consolidation is not complete and there are still functions

outside the purview of OFM. Major functions managed by other agencies include timekeeping,

payroll, wage control and revenue collection. MCSD and IPD both have internally-developed

applications that manage these processes.

There are several computer systems and databases that manage the enterprise‟s financial

transactions, budgets, payroll and assets. FAMIS, ADPICS, FAACS, INFOR and BPREP, which

reside on the mainframe, allow for some enterprise interaction. However the lack of integration,

ease of use and functionality have resulted in the development of over 1100 shadow systems.

The cost of supporting these systems, both in manpower and processing power is substantial.

This report details supporting evidence for the consideration of the implemention an enterprise-

wide ERP system to consolidate and standardize business processes. This new ERP system would

provide the following:

33..11..11 BBeenneeffiittss::

A new, integrated suite of software that is both modernized and cost effective

A reduction of hundreds of shadow systems across the enterprise, such as Excel

spreadsheets and Access databases

A single, consolidated source for financial and human resource information to be stored,

reported, and shared across the enterprise

Approximately eight percent of the City/County employees directly or indirectly manage or

support these systems. In some cases, the financial support utilizes up to 90% of their time.

(See Section 4.3 for more detailed scope of FTE‟s along with Appendix C for a breakdown by

agency of FTE‟s)

In-depth interviewing and business process workshops were conducted to review the current

business processes of each agency, department and division involved. The amount of manual,

duplicate, and triplicate work done by administrative staff and the cost to the City/County for

continuing to support the current status offers evidence of a need for an ERP system. The section

below highlights the major findings.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 6

33..11..22 FFiinnddiinnggss::

Paperwork and Shadow systems. There are over 1100 shadow systems across the

enterprise causing multiple repeated data entries.

Unsupported Technology. Shadow systems are providing mission critical functions and

are unsupported as a result of the technology is becoming obsolete. (See Section 5.3 and

5.4 and Appendix B)

Data quality. Because of the tremendous about of manual inputs, calculations, and

reconciliation, quality assurance takes time and introduces error.

Data Currency. There is no central repository of information therefore seeing real-time

data is not available. This limits the visibility of progress on transactions/information

requests reducing decision-making ability, adding time and introducing errors.

Labor Intensive Functions. Numerous work around procedures create repetitive manual

functions such as maintaining paperwork, inputting processing, organizing, verifying

numbers and performing busy work that wastes time and introduces errors.

Along with the interviews, cursory market research was completed to provide a cost expenditure

model for the implementation of an ERP system. It was determined that on two successfully

implemented ERP models reviewed that the municipalities were very satisfied with their decision

to implement an ERP system. We performed analysis using two main cost structures. The

moderate cost for implementation would run around $4 million with an additional $1,000,000 in

annual maintenance support fees, while the lower cost structure would fall between $1-3 million

for implementation and on-going costs in the $1,000,000 range. These estimates assume both

financial and human resource modules would be implemented.

The NPV analysis of this study supports the financial feasibility of implementing a new

City/County ERP system, as the results recognize a positive investment as early as year three

with the assumption that all implementation costs are accounted for in year one. The varied

productivity rates of personnel who work with the systems are dependent on the breadth and

success of the implementation. For that reason, we analyzed three personnel productivity rates.

The rates affect the NPV, but in general the higher the productivity rate, the greater the benefit to

the City/County. By implementing a new ERP system, the total costs saved by year five are over

$11 million with the total benefit ranging from $16 million to $22 million based on the high

productivity – low cost cost structure used.

The full report documents the study‟s findings defining gaps of the current financial and human

resource systems and the need to fill those gaps and unify business process and information for

financial and human resource oversight and management. A great opportunity exists to improve

the financial system of local government making it a better business fit with department and

agency needs, providing for more strategic information, in a more affordable support structure for

the enterprise. Many cities and counties the size of the City/County have gone through the

process of modernizing their systems, validating that a proven solution is available. What is

paramount for the success of an ERP system in the City/County is having the political will to get it

done, cooperation by all stakeholders and the funding to implement and maintain it.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 7

44 CCuurrrreenntt SSiittuuaattiioonn

44..11 OObbjjeeccttiivveess && BBeenneeffiittss

The City of Indianapolis and Marion County is an association of many local government

departments and agencies. Uni-Gov was the beginning of consolidating like functions to reduce

duplication of services within government. Specifically, the financial oversight for city

departments is the responsibility of OFM. The financial oversight for county agencies, until

recently, was the responsibility of the Auditor‟s office. During the past few years elected officials

and the City/County Council agreed to allow the newly formed OFM to provide the financial

oversight for nearly all local government. The goal is to provide uniform reporting for budget,

standardized transaction processing and financial oversight.

The reality is that the consolidation of functions under OFM is not complete. Many county

agencies have unique financial processes that will take some time to assimilate. There are

several functions that are related but beyond the purview of OFM:

Timekeeping and payroll

Wage control

Revenue collection

Implementing an ERP system would improve coordination across functional departments and

increase efficiencies of doing business, but only if there is a total commitment to improve upon

existing processes. Technology is often used to automate processes, but it does no good to

automate a bad process because in the end those bad process still exist, only faster. Instead,

the enterprise must embrace the idea of improving processes by defining clear objectives and

creating a vision for the immediate benefits of a new ERP system:

Fully automated financial processes including cash management, accounts receivable and

payables

Integration of personnel, payroll and budget (to include wage control)

Accurate budget forecasts for strategic planning and reporting

Centralized management of contracts including MBE/WBE

Streamline of purchasing process and public bids

Single source of fixed assets

Access to real-time and historical data improving decision making

Reduced IT support

44..22 FFiinnaanncciiaall aanndd HHuummaann RReessoouurrcceess SSyysstteemmss aatt tthhee CCiittyy//CCoouunnttyy

FAMIS is the longtime mainframe financial transactions processing system for the City/County. It

has provided years of reliable accounting. However, FAMIS has limitations and many departments

and agencies created shadow systems to overcome the services that could not be provided. In

many cases they were simple spreadsheets. Although financial spreadsheets will always be useful

in performing “what if” scenarios, there is to much reliance in today‟s environment on the

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 8

hundreds of spreadsheets used to track everything from calculating payroll, capital improvement

projects to wage controls to revenue projections.

44..22..11 FFiinnaanncciiaall aanndd HHuummaann RReessoouurrccee TToooollss

Because of the disparate systems, it is not easy for decision makers within the City/County to get

information in a timely manner. Information requests flow from the Mayor‟s Office or City/County

Council to the agency head or OFM. If the information is not available in FAMIS a whole flurry of

activity begins as staff work to cobble together information. An example of this phenomena is the

tracking of MBE/WBE compliance. Staff new to this process, perceive the information is readily

available and that the request is simple. After understanding the reality of the systems available

to them, they begin to create new financial and HR systems to meet the information demands.

OFM is willing and skilled at providing information, but the design and limitations of the current

systems and lack of simple tools do not allow staff to gain access, manipulate and present

financial information on demand to meet information requests, do projections and essentially

manage financial and human resources.

44..22..22 FFiinnaanncciiaall aanndd HHuummaann RReessoouurrcceess SSyysstteemmss

FAMIS/ADPICS/INFOR/FAACS are applications on the mainframe. Strategically, the mainframe is

scheduled to be eliminated because of the higher cost it takes to support the dwindling number

of applications The software licensing, NG support, hardware maintenance and the need to keep

skills for the 3 major applications left on the platform is becoming proportionally larger. As the

other key applications on the mainframe (JUSTIS and Property) have migration plans developed,

the financial and payroll applications will be the lone reason to support the second platform. If no

suitable replacement for the core financial systems is identified, the mainframe will remain.

44..22..33 FFiinnaanncciiaall aanndd HHuummaann RReessoouurrcceess PPeerrssoonnnneell

When evaluating the need for an ERP solution it is important to understand how many employees

and hours are spent within the enterprise managing such functions as payroll, labor, benefits,

accounts payable, accounts receivable, asset management and revenue management. Collecting

the total employee headcount provides management the opportunity to review the numbers to

determine if employees are making the best use of their time because of access to relative and

timely information or if there is wasted labor in the enterprise.

A survey was sent to all City/County agencies to ascertain how many employees are primarily

engaged in the use the financial and human resource system. In addition, the number of

managers who depend on the information derived from these systems was collected, assuming

that there would be small benefit in productivity for those type of employees. Each Chief

Financial Officer (CFO) identified the number of people in their department and the percentage of

time spent managing these specific functions.

The FTE matrix identifies:

48 departments and agencies

92 employees with direct management over financial operations

196 non-management employees responsible for financial operations

288 employees who depend upon the financial information to manage their day to day

operations

It is interesting to note there are nearly two staff members responsible for financial activities for

every department. Validating the FTE survey results required an in-depth understanding as to

how the financial functions were performed.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 9

55 EERRPP AAnnaallyyssiiss FFiinnddiinnggss

55..11 OOvveerrvviieeww –– UUnnddeerrssttaannddiinngg EExxiissttiinngg PPrroocceesssseess

There are several hundred people employed at the City/County responsible for financial and

human resource information. This section addresses the business processes of how these

employees perform their jobs due to inflexibilities of the current financial and human resources

systems. Understanding the existing business processes provides the opportunity to identify

improvements and employees were happy to be given the opportunity to describe the existing

issues that exist within the current process. There is a significant amount of employee knowledge

in the enterprise and the following departments participated in workshops or interviews conducted

by Premis Consulting and the Business Relationship Managers:

Office of Finance and Management

Purchasing

Marion County Auditor

Marion County Clerk

Marion County Treasurer

Department of Public Works

Department of Metropolitan Development

Indianapolis Metro Police Department

Information Services Agency

Human Resources

Each department was asked to identify strengths and weakness of their current systems, describe

the process of accomplishing their duties and estimate how much time is spent on those

activities. Twenty business processes were documented into detailed workflow diagrams. These

diagrams illustrate how the departments perform their jobs today and identify what manual and

labor intensive tasks may be eliminated with the implementation of a new ERP system.

This section is arranged by individual findings, with supporting information from a sample of

departments to provide greater insight into how these burdensome administrative tasks result in

inefficiencies.

Five reoccurring findings emerged:

Paper documents and shadow systems are considered the primary source of information

Access databases provide mission critical functions. This technology is becoming rapidly

obsolete.

Data currency issues result in lack of timeliness

Manual calculations, reconciliation and quality assurance take time and introduce error

Functions are labor intensive and usually on paper, reduce decision-making ability, take

time and introduce errors

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 10

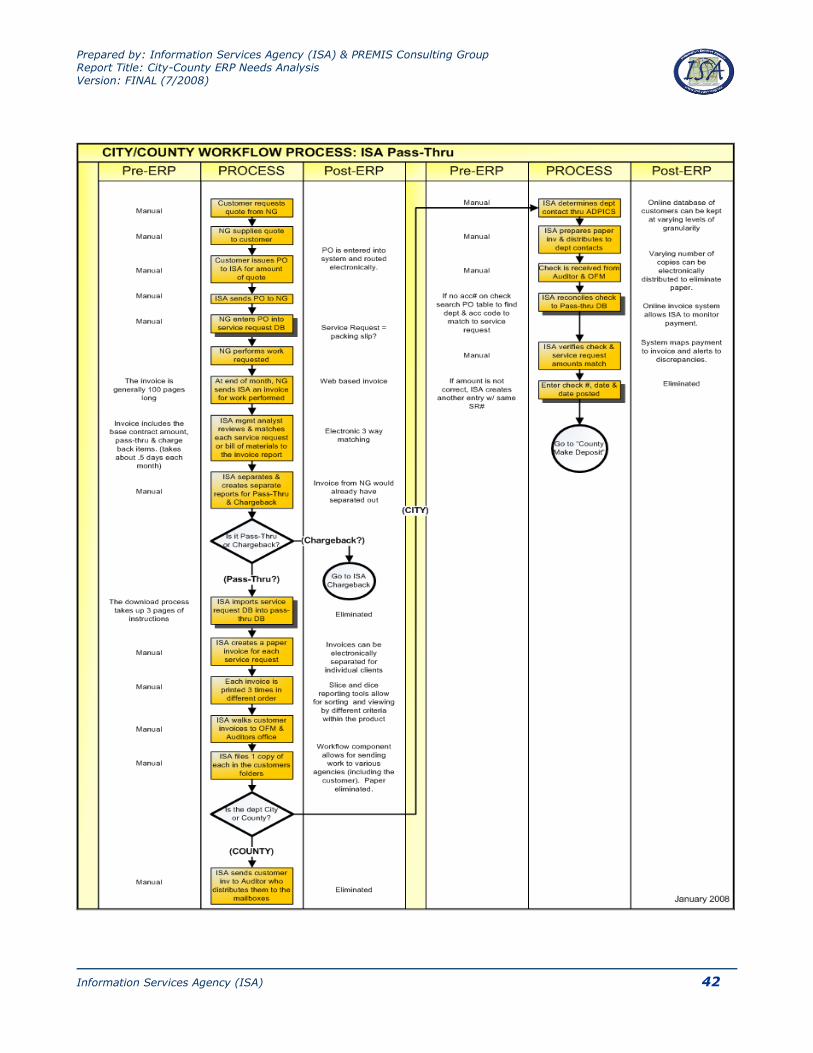

55..22 CCuurrrreenntt BBuuddggeett PPrroocceessss AAnnaallyyssiiss

In this section the business process for addressing the annual budget is described along with its

workflow diagram for reference. Although a total of 20 business processes were documented, the

annual budget was selected as a critical process to describe since the event represents the

beginning of the financial reporting process where every agency is a participant and common

points of pain are shared across the enterprise. It is also the least ambiguous of all the business

processes.

Description of the Budget Process:

The process begins with each agency‟s Excel spreadsheets and/or Access databases to

track expenditures internally. These shadow systems were created by agencies because

historical information is difficult to obtain from the financial system. Working from the

information contained within their shadow systems, the agencies update BPREP, a

component of the FAMIS program. BPREP has strict security within OFM and access is only

allowed to users during budget season (about 30 days).

Agencies such as ISA have technology budgets that must match supported agency

budgets. Therefore, it is imperative ISA understand what technology initiatives an agency

wishes to implement to properly submit their own budgetary numbers to the BPREP

program. In order to obtain this budget information from an agency, ISA created an online

web survey which is distributed to agency CFOs a few months prior to OFM‟s unlocked

release of BPREP.

After all agencies have submitted their initial budget figures to BPREP, it is closed. A

program called FOCUS extracts the budget information where it is then downloaded into

Access databases for analysis and manipulation by OFM.

OFM creates budget reports from these Access databases granting rights to agencies to

access the data. In theory, if changes need to be made, the agency will make updates

directly to these Access databases where it is then updated in BPREP. However, it is easier

for an agency to take the Access database and export the information into Excel. The

Department of Metropolitan Development‟s (DMD) grant division finds the process to be

cumbersome because they would prefer to run their own extract directly from FAMIS and

receive information that is most relevant to their grant budget reporting. Instead, they are

forced to back out the encumbrances and import the revised data from Access directly into

Excel, requiring an additional level of consolidation at the division level.

Next, OFM and CFO‟s meet to discuss the proposed budget reports for their agency. If no

changes are needed, the agency will write a narrative on how they would like to spend

their budget for the following year and send it to OFM. If the DMD Grants budget is

approved by OFM their Excel spreadsheet is uploaded back into BPREP.

Once all of the budget information and narratives are collected from each agency, OFM will

publish the proposed budget on the indygov.org Web site, print and advertise their rates

through the Indianapolis Star.

Examples of all five reoccurring findings occur within the annual budget process with the creation

of shadow systems, no historical trending, lack of data currency, manual functions resulting in

multiple data entries and vital financial information contained with an Access database.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 11

The budget workflow diagram is documented below along with recommendations of how an ERP

system will automate tasks, eliminate redundancies and provide business intelligence allowing for

better decision making. (See Appendix A to view the remaining workflow diagrams)

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 12

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 13

55..33 FFiinnddiinngg 11:: PPaappeerrwwoorrkk && SShhaaddooww SSyysstteemmss

One of the most alarming findings made during the interview process was the discovery of 1100

financial and human resource shadow systems in the enterprise today, consisting primarily of

Excel spreadsheets and Access databases. There is such a critical need for accurate and detailed

views of the current financial status and employees feel the available information is not available

to them or is too difficult to extract out of the system or question the integrity of the data.

Therefore, the majority of agencies have created their own shadow systems to help them manage

the information necessary to run their department.

In addition to the 1100 shadow systems agencies heavily rely on paperwork to keep track of

transactions because it is easily accessed and seen as the most reliable source of information.

The following conclusions can be made from the discovery of paperwork and shadow systems:

Detailed financial information such as revenue, assets, accounts payable, purchases and

grants for the City/County is truly maintained within individual Excel/Access and not

FAMIS/ADPICS.

Paperwork and shadow systems cause duplicate and triplicate data entry resulting in an

increase of human error, time and labor.

Lack of integration creates data silos across departments making information difficult to

share.

Many of the spreadsheets and databases are saved locally on an employee‟s desktop and

are not backed-up by ISA servers. Critical information would be non-recoverable should

the desktop fail. Locally saved databases often conflict with network standards and

requirements because they have not been converted to the latest standard 2003 version.

Here are specific agency examples of this finding (See Appendix B for additional examples):

55..33..11 OOFFMM -- CCoouunnttyy PPuurrcchhaasseess UUnnddeerr $$11000000

Each department uses ADPICS to create purchase orders but the tracking and maintenance of the

purchase order process is managed within their own internal Excel spreadsheet or Access

database. Departments feel ADPICS is not scalable enough to provide the level of detail needed

for their purchasing processes and some were never properly trained on how to track the

information within ADPICS. Therefore, they work around ADPICS by creating a shadow system to

track the information. Invoices are data entered into FAMIS as there is no direct interface from

ADPICS. The county‟s use of Adpics does not allow for online approvals, therefore is largely used

as a depository of information, as the workflow is done entirely on paper.

55..33..22 AAuuddiittoorr aanndd CCoouunnttyy DDeeppaarrttmmeennttss -- PPaayyrroollll

The Auditor‟s payroll department uses a mainframe application called INFOR, formerly known as

GEAC to process all county payroll. Each county agency is responsible for maintaining and

tracking their employees‟ hours, pay rates, benefit leave and providing the Auditor with a voucher

summary report of what needs to be paid. All of the vouchers are printed or hand written by each

county department and physically delivered to the Auditor‟s office where it is manually entered

into INFOR.

It takes two to two and a half days for two Auditor employees to input data from all of the county

department vouchers into INFOR. Processing includes reviewing, making changes where

necessary, such as new hires and address changes, and inputting data into the Access database.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 14

The Auditor‟s office notifies the Treasurer‟s office regarding taxes to be paid by sending a paper

form printed from INFOR creating what is known as Treasurer‟s ACH authorization.

55..33..33 HHuummaann RReessoouurrcceess –– RReeccoorrddss

The benefits section uses a third party Web-based application known as Benefits Connect. After

an employee completes their benefits submission online a paper file is printed and placed in their

employee record. Many departments and agencies keep a paper record of the employee record

including demographic information for future reference in the event the employee needs the

information at a later date.

55..44 FFiinnddiinngg 22:: UUnnssuuppppoorrtteedd TTeecchhnnoollooggyy

Inefficiencies of the current systems have caused employees to create numerous “work around”

procedures making it possible for employees to perform their jobs, which in turn have birthed

thousands of Access databases in the enterprise with 1100 shadow systems existing in the

financial community alone. Although there were advantages in allowing employees to create their

own Access shadow systems in the past, such as business processes could be enhanced

immediately with the expertise of an in-house (agency) developer, the disadvantages now

outweigh the advantages in today‟s environment.

Here are some of the disadvantages:

Access databases provide mission critical functions & are unsupported because the

technology is becoming obsolete with advances in programming development.

The databases were built by an in-agency designer who held the technical expertise and

knowledge of the workings of the database. Technical documentation about how the

database functions is non-existent. When the designer leaves City/County employment so

do the intimate details about the database modeling, triggers, and security settings

leaving the agency helpless to support their own systems.

Access databases are not meant to hold more than 150,000 records and therefore are not

scalable to an agency‟s growth. When a database begins to reach its record limit it will

begin to exhibit signs of failure such as corrupted records and non-recoverable entries.

Access databases are only meant to be used by a handful of users at a time, yet the

City/County has stretched Access to its limits by providing rights to these databases to

entire departments and multiple agencies. The majority of databases are saved locally on

a user‟s desktop creating multiple versions of the database and making it susceptible to

threats because it is not backed up.

ISA is asked to assist with redesigns and bug fixes, but cannot accommodate the majority

of requests due to a lack of employed Access developers and the sheer volume of

databases in the enterprise makes the task impossible. A movement has been made to

work with agencies to convert databases over to the new standard Microsoft .NET platform

giving ISA the responsibility of maintenance and enhancements, but the process of

identifying the most critical databases and gathering business requirements takes time. In

addition, is a costly endeavor that results in no gains in functionality.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 15

Below are specific agency examples of this finding (See Appendix B for additional examples):

55..44..11 AAuuddiittoorr –– FFiinnaanncciiaall RReeppoorrttiinngg

The Auditor uses many Access databases solely for reporting purposes and shares the information

with other county departments. The Auditor does not have the capacity to train the departments

on how to use the databases when someone asks for assistance. All of the databases were

created by a contract employee who no longer works for the Auditor and finding a developer in

today‟s environment who knows of the exact type of Access coding used to create the database

can be difficult.

55..44..22 OOffffiiccee ooff FFiinnaannccee aanndd MMaannaaggeemmeenntt –– RReevveennuuee aanndd CCaasshh MMaannaaggeemmeenntt

The revenue manager of OFM has built several Access databases to accommodate the growing

business processes of the agency. The databases are built according to the individual‟s

specifications and it would be difficult for ISA to offer support if it was requested because no

technical documentation about the databases exists.

55..55 FFiinnddiinngg 33:: DDaattaa CCuurrrreennccyy IIssssuueess

Another significant finding during the business process interviews was the lack of data currency.

When data is not relevant because it is inaccurate or out-of-date the enterprise runs the risk of

making misinformed business decisions based off of wrong information.

Many processes require manual approvals needing a wet signature which slows down the decision

making process making the data stale. A lack of automated workflow also increases the risk of

poor decision making because people are forced to manually route documents. The paperwork is

often left floating with no one person directly responsible for taking any action or resolution. As a

result, employees waste time hunting down information to determine what went wrong during the

approval process and what action needs to occur in order to move forward.

The following are examples of data currency issues which result in a lack of timeliness and poor

decision making abilities:

55..55..11 CCoouunnttyy PPuurrcchhaassiinngg -- PPuubblliicc BBiidd PPrroocceessss

Almost all of the processes performed are done individually by department without collaboration

on the bid development and are done in programs not relating to ADPICS or FAMIS. It is

impossible to know where the request for proposal (RFP) is in the process because there is not

one single system to track its status and not one single person responsible for monitoring the

process. Instead, there are multiple versions of RFPs and their respective vendor responses in

electronic and printed format. Some are printed on paper and sitting on desks and others are

stored in Outlook email inboxes or on shared drives.

For example, purchases over $150,000 require a department to submit a RFP allowing multiple

vendors the opportunity to bid on equipment or services. Purchasing specification writers work

with the department to create an RFP using Microsoft Word. The RFP process can take up to three

months to complete and there are many version control issues throughout the process because it

is impossible to know who has the latest version of the RFP.

When the RFP is finally ready to “hit the streets,” email notifications are sent to prospective

buyers and advertised. When the RFP receives a bid at a public opening it is tracked and

tabulated within Excel. After the bid is reviewed by a purchasing buyer it is scanned into PDF

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 16

format and emailed to the agency for review where it is printed out on paper and marked with

comments.

55..55..22 CCoouunnttyy PPuurrcchhaassiinngg –– PPuurrcchhaasseess uunnddeerr $$11,,000000

All requests for purchases over $1000 are done on paper with multiple signatures. Requisitions

and invoices are walked to the Auditor‟s office and back, opening the process up to error and not

allowing for visibility of progress of request.

55..66 FFiinnddiinngg 44:: MMaannuuaall ccaallccuullaattiioonnss,, rreeccoonncciilliiaattiioonn && qquuaalliittyy aassssuurraannccee

The enterprise is a breeding ground for potential errors when humans are responsible for

performing manual finance calculations, eyeing over spreadsheets to ensure balances match and

double checking each other‟s work as evidence of quality. From coding and data input errors to

misplaced decimals, when a person makes a mistake generally there is a supervisor present to

verify the information making the reconciliation process lengthy and redundant.

Another downfall to performing manual calculations over and over is how errors affect the ability

to make accurate decisions. Poor decisions are made every day because one department has

made a mistake which in turns affects the entire agency‟s decision making process causing a

snowball effect. That agency then makes poor decisions affecting another agency‟s ability to

make precise and informed decision. The process continues until the entire enterprise feels the

affects of “one person forgetting to carry over the one.”

During the interview process it was found that a large amount of the City/County payroll business

processes are performed by hand. Although OFM‟s payroll department prides itself on the fact it

has not missed a pay period in 20+ years, the checks and balances they have in place to catch

mistakes increase the payroll processing time frame by a week, as well as the cost of producing

an accurate payroll.

Below are examples of manual calculations and quality control procedures OFM and IMPD use

when processing payroll Additional examples can be found in Appendix B.

55..66..11 OOffffiiccee ooff FFiinnaannccee aanndd MMaannaaggeemmeenntt –– CCoouunnttyy PPaayyrroollll // NNoonn PPuubblliicc SSaaffeettyy

The Marion County Superior Courts and Treasurer‟s office use a program called Online Time

Information System (OTIS) which allows employees to enter their own payroll hours into an

electronic application. Supervisors review and double check the hours first before creating an

OTIS voucher report. This report is then walked to the Auditor‟s Office where the employee hours

are data entered back into INFOR. The administrative work and chances of a data entry are

somewhat reduced since initially the employee data enters their hours into the system, but

because no interface exists between INFOR and OTIS there is still duplicate data entry which

would be eliminated with an integrated, not just interfaced, system.

55..66..22 OOffffiiccee ooff FFiinnaannccee aanndd MMaannaaggeemmeenntt –– CCiittyy PPaayyrroollll // NNoonn PPuubblliicc SSaaffeettyy

There are over 200 benefit changes processed by OFM every two weeks. When there is a new

employee or a change to an existing employee‟s payroll deductions benefits paperwork must be

completed. The department‟s HR Manager then data enters the information into their internal

Excel spreadsheet or Access database. Next, the paperwork is delivered to OFM who calculates

by hand the new amounts and enters the rate changes, deductions or new employee information

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 17

into INFOR. The risk of human error is high because of the manual calculations and triplicate data

entry procedures.

Paper time cards are completed by over 2000 non-public safety employees every two weeks. The

time cards are collected by the departments‟ HR Manager who data enters the total hours worked,

over-time, sick leave and any benefit hours received into their payroll Excel spreadsheet or

Access database. The departments‟ HR managers hand deliver the time cards to the OFM payroll

supervisor. From there, two payroll coordinators manually data enter all 2000 time cards back

into INFOR resulting in triplicate data entry.

55..66..33 PPuubblliicc SSaaffeettyy –– HHRR aanndd PPaayyrroollll

While MCSD and IPD both have their own HR/Payroll systems, over time they become less

functional given the changes in union contracts and age, in the case of MCSD, of the platform it

runs on. MCSD and IPD both produce the pay for each employee and then send it to OFM or the

Auditor‟s Office to produce a paycheck.

While the system automates some function, there are still things left to be desired. For example,

after changes in certain requirements, some deductions and special pays are being calculated

manually.

The process is substantially manual, as the systems are depositories for information, but the

process to produce elements of pay is done outside of the system. For IMPD, to determine pay,

1600 paper timecards are alphabetized by hand and then each timesheet is evaluated

individually in a manual process to determine if the employee is eligible for shift differential. If

eligible, shift difference is calculated with a calculator, pencil and paper. A second pass of the

1600 timesheets is done to determine other types of additional pay, such as canine care. Again

this is calculated on paper. After all types of special pay are added, these numbers are then

manually entered into a separate Access database. The process is fraught with data entry errors

and requires several validation passes by hand.

MCSD timesheets are sorted and calculated in four different passes. Special and extra pay is data

entered into the Dec (the hardware) system. The actual payroll amount is calculated by hand and

each amount for each employee is handwritten on to the summary voucher report and hand

delivered to the Auditor‟s office where it is manually typed into the INFOR system.

55..77 FFiinnddiinngg 55:: LLaabboorr IInntteennssiivvee FFuunnccttiioonnss

There are many limitations of the current financial and human resource systems which have

forced employees to “work around” the problem. If the systems cannot provide the information

and IT budgets and resources are limited, then employees have to find a way to get it done using

their own means to accomplish the task. As a result, most employees are performing repetitive

manual functions such as maintaining paperwork, inputting, processing, organizing, verifying

numbers and performing busy work that wastes time, introduces errors and bogs down the

decision making process. Tracking historical information and reliable trends are other examples of

manual processes because the information simply does not exist within the system resulting in

head knowledge over system knowledge.

It may not seem serious if one person wastes 15 minutes per day trying to track down

information, but what does it cost if there are 10 people trying to track down the same

information throughout the year? Assuming a rate of $18hour and 1,1950 hours or work per year,

this issue has cost the City/County $87,750 within a year.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 18

The ERP interviews have forced agencies to take a hard look at their business processes. At a

minimum, it is suggested agencies begin thinking about re-engineering business processes in

order to shift time and resources from performing manual functions over to innovating, problem

solving, increasing efficiencies and improving customer service to each other and the constituents

of the City/County. Many of the inconsistent processes are due to not having a system to support

a streamlined business process, so improvements may be limited. Some improvements could

also be possible with policy change, which may not require systems to support it.

Examples of burdensome manual functions are described in detail below.

55..77..11 OOFFMM –– FFiinnaanncciiaall RReeppoorrttiinngg

There are several reports OFM is required to produce each year but the largest and most time

consuming report is called the Comprehensive Annual Financial Report (CAFR) and is required by

the State of Indiana. The CAFR report is very labor intensive and usually requires six months of

preparation because the information cannot be easily extracted. The process begins with an

extract from FAMIS received in printed format and then data entered into a master Excel

spreadsheet with approximately 30 worksheet tabs. The introduction to the report is also created

using a second Excel spreadsheet with approximately 24 worksheet tabs.

The budget is managed on a cash basis accounting system within FAMIS, but for reporting

purposes OFM must convert the numbers from cash basis to modified accrual and then into full

accrual. The conversions require an extreme level of attention to detail and in-depth knowledge

of accounting ledgers.

55..77..22 HHuummaann RReessoouurrcceess –– EEmmppllooyymmeenntt // NNoonn PPuubblliicc SSaaffeettyy

Currently HR has two systems for gathering employment applications, Vurve Express and an

Access database. Vurve Express is a hosted third party online application used to submit, accept,

review and processes 1,000 electronic applications per month at an average rate of three minutes

per application. Employment is using both Vurve Express and a previously created Access

database to process all of the applications until the entire enterprise is configured to Vurve

Express. Approximately 500 paper employment applications are accepted via fax, mail and walk

in per month and processed using the Access database at ten minutes per application. There are

approximately 8,500 applications stored in four large filing cabinets within their office and another

8,000 to 9,000 records that must be retained from two years prior stored in various locations

within the City/County building.

55..77..33 DDeeppaarrttmmeenntt ooff MMeettrrooppoolliittaann DDeevveellooppmmeennttss -- GGrraannttss

Nearly 100% of the work is done using an Access database and Excel spreadsheet. The

information can never be viewed in real-time because of the delays in data entry from FAMIS into

these shadow systems. Duplicate and triplicate data entry increases the chance of errors and

since the information is always re-entered back into FAMIS, employees must wait a full day after

FAMIS has been updated to obtain and validate their numbers. Lastly, there are seven employees

who need to work in the database at the same time and Access does not support concurrent

usage with that amount of people. People are forced to schedule their work within the database

resulting in wasted time and resources.

55..77..44 MMaarriioonn CCoouunnttyy TTrreeaassuurreerr -- IInnvveessttmmeennttss

There is no mechanism in place to perform various comparisons on investments. When a proposal

to invest is received all of the analysis is done using Excel spreadsheets leaving the analysis

approach up to the individual analyst. In addition if the data was ever lost and found

unrecoverable there would be no way to get historical analysis across several years.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 19

66 MMaarrkkeett RReesseeaarrcchh

66..11 OOvveerrvviieeww

The objective of this research was to identify ERP software vendors supplying solutions for cities

approximately the same population as Indianapolis. A cursory review suggests there are at least

five vendors with ERP applications suitable for this enterprise. These software modules include

(but are not limited to): government accounting, procurement, cash management, tax, revenue

management, contract management, fixed asset management, payroll, personnel and cashiering.

Initial contact was made with a number of municipalities to discuss basic cost and experience with

implementing an ERP. Conversations were documented with CIO‟s, CFO‟s, vendor ERP project

managers, senior government staffers and vendor marketing and sales executives. However,

given the time allocated to this task a complete picture of costs was not always possible.

Discussions from the governmental units solicited revealed these thoughts:

Many cities acknowledged it was a painful process (implementing/updating ERP systems)

and agreed to be contacted for advice and tips if needed.

For most, it was a difficult but fruitful experience lasting from 1 to 2 years. The users and

technology staff had different experiences. In some cases, users loved the features but

the tech staff had difficulty making it work. In other cases, the users clamored for more

training/support, but the technical staff had a good installation.

There was significant pre-installation consulting required to identify new policies and

changes in business process.

The cost and coordination for such a project requires the complete cooperation of the

executive, legislative and judicial agencies. Anything less means multiple financial

systems in the enterprise.

66..22 MMaarrkkeett RReesseeaarrcchh FFiinnddiinnggss

These findings were obtained by identifying key ERP software vendors in the market and

contacting customers with populations similar to the City/County.

66..22..11 MMiiccrroossoofftt//TTiieerr//FFAAMMIISS The incumbent vendor is Tier which provides FAMIS support. At the moment, Tier

is the FAMIS parent has a strategic partnership with Microsoft. Microsoft owns the

Dynamics GP (formerly Great Plains) suite of products. Tier has a version of

Dynamics GP, called Tier Financial Management System, specially packaged for

Government ERP.

The City/County is a Premier Microsoft customer, hence potentially, leading to

services and resources that can be leveraged.

Any move from the mainframe is going to be a major upgrade.

Tier estimates a City/County implementation cost of $3.4 million.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 20

66..22..22 OOrraaccllee//PPeeoopplleeSSoofftt//JJDD EEddwwaarrddss//SSiieebbeell

PeopleSoft was acquired by the City/County Human Resources in the mid 1990‟s but never

implemented. The coordination of funding and business processes between Human Resources

and city departments was never achieved. Oracle is a major vendor in the ERP arena. Oracle

supplies both database software and a suite of applications software. Our research focused on

the applications software.

Important notes:

ISA has Oracle database administrators (DBA) expertise and although the number of

Oracle-based database applications is decreasing, there is still a strong portfolio.

Oracle is an industry standard with a number of accounts that fit the bill – cities contacted

were: Oklahoma City, Denver, Redmond, WA and St Petersburg, FL

Oracle ERP solutions may be available on a Microsoft SQL database, which is the

City/County standard..

Siebel, the Constituent Relationship Management software used by the Mayor‟s Action

Center, was purchased by Oracle and is now part of its offerings.

66..22..33 TTyylleerr MMuunniiss

Tyler is an up-and-coming ERP software provider with a wide variety of public sector offerings and

has a number of customers that are major cities. Tyler is the parent of Odyssey, the court

management software selected by the State of Indiana.

The following four customers were contacted:

Buffalo, NY. Buffalo is a long time Tyler customer. They love the features and offerings

but had trouble in the early stages with „customization requests‟. It is a closed system and

such requests were considered from release to release.

Fort Wayne, IN. The employees contacted in this environment were extremely happy with

the system, and were satisfied with the implementation effort. The project took about 15

months from start to finish.

Franklin County, OH. They have been customers of Tyler for nearly ten years, and remain

“very satisfied” with the product. Franklln County is a similarly sized county as Marion.

Durham, NC. Durham implemented the product in 2005, and rates their satisfaction as

“very good.”

66..22..44 OOtthheerr VVeennddoorrss//SSAAPP//LLaawwssoonn EERRPP//IInnffoorr

These other vendors show great promise and should be included in further investigation.

SAP is frequently seen on websites providing ERP white papers. The City of Phoenix, AZ

was contacted. Phoenix has a full offering of many ERP modules. SAP and Oracle the

largest and similar market share.

Infor ERP has acquired Hansen, DPW‟s work management system and is the parent of

INFOR, the current payroll system. However, Infor was not shown to have a wide variety

of ERP software.

The North Central Texas Council of Governments (cities of Arlington, Grand Prairie and

Carrollton) use Lawson ERP and are very happy with it

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 21

77 NNeett PPrreesseenntt VVaalluuee ((NNPPVV)) AAnnaallyyssiiss

77..11 NNPPVV OOvveerrvviieeww

The net present value (NPV) analysis in this study is to equip decision-makers with real options to

gauge and react to risk over time. NPV is calculated based on the expected benefits/returns and

the expected costs of an investment, where these expected benefits and expenses are discounted

by a rate that reflects inflation and opportunity costs.

The spreadsheets found in Appendix E consist of benefits (costs avoided and personnel

productivity) and costs that would be eliminated by the implementation of a new ERP system.

These costs include maintenance and support of legacy systems, storage costs of shadow

systems, support of shadow systems (including Access and Excel) and mainframe retirement.

The personal productivity is calculated by taking FTE counts received from OFM for direct and

indirect users of the systems and multiplying that with the average salary and productivity rate.

Initial and on-going project costs were determined through market research of implemented

systems. The discount rate used was provided by the Indianapolis Bond Bank as the cost of

funds, estimated at 4.80% and the inflation rate was estimated at three percent.

The analysis reviewed two costs structures, moderate and low and varied productivity from low,

mid, and high within the two structures. A high cost structure was never obtained because of

difficulty in getting clients to further break down the numbers into hardware, software and

implementation. The costs structures were based on successfully implemented systems within

cities comparable to Indianapolis. Productivity was determined primarily by defining high

productivity as all direct and indirect beneficiaries operating at full utilization with all modules

purchased therefore receiving the full benefit. Moderate and low productivity was estimated by

defining different levels of implementation and adaptability of the system. Variables that could

impact the productivity figures are the number of modules purchased, training, user

understanding/knowledge of the system, support, implementation time, available budget and

process changes.

77..22 NNPPVV FFiinnddiinnggss

An analysis of each cost structure provides an NPV for the moderate cost structure ($12.8 million,

$9.3 million, and $7.1 million) along with the NPV for the low cost structure ($15.8 million, $12.3

million, and $9.6 million). The first section shows the information for moderate costs with high,

mid, low productivity, while the second section shows the information for the low costs with high,

mid and low productivity.

The results translate to the following conclusions:

Regardless of productivity or the cost model, the NPV is positive by year two (with the

assumption that all implementation costs are accounted for in year one) supporting the

idea this project would benefit the City/County and save money.

The low cost model will provide the greatest savings because of lower cost outlays.

In general, the higher the productivity rate, the greater the benefit to City County.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 22

Varied productivity rates will help project the actual NPV when scaling and implementing

the project.

The total costs saved annually by year five are over $11 million with the total benefit

ranging from $16 million to $22 million based on productivity.

For example, looking at the spreadsheet below within the moderate cost structure and mid

productivity, total costs avoided are fairly consistent starting at $2.7 million from year two and

going up to $2.8 million in year five. There are 92 management and 196 non-management

positions that are direct beneficiaries of the system and 289 management positions that are

indirect. The productivity for the personnel assumed a 10% direct beneficiary enhancement rate

whereas the indirect beneficiaries assumed only a 2% enhancement rate. Based on the

assumptions of hourly rates and numbers of hours worked, productivity increases from $1.9

million to $2.1 million by year five equaling a total of $8.2 in personnel productivity. Add in the

costs avoided and by year five, the total benefit to the City/County is close to $19 million.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 23

The initial costs in the spreadsheet total $3.8 which is the estimate for implementing the new ERP

system based on market research. After the initial costs, yearly on-going costs for maintenance

are around $1.4 million annually. This is half the cost of supporting the existing system. The

supporting NPV calculated realizes the positive investment in year three at $2.5 million. At year

five, the accumulated NPV is $9.2 million.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 24

88 AAppppeennddiixx

88..11 AAppppeennddiixx AA:: EERRPP PPrroocceessss WWoorrkkfflloowwss

Attached below are the completed ERP Workflows developed during the course of this analysis. In

addition to identifying the manual and automated aspects of the current City/County processes,

these workflows also provide an analysis of the “Pre” and “Post” ERP Implementation

environment.

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 25

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 26

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 27

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 28

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 29

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 30

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 31

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 32

Prepared by: Information Services Agency (ISA) & PREMIS Consulting Group Report Title: City-County ERP Needs Analysis Version: FINAL (7/2008)

Information Services Agency (ISA) 33

CITY/COUNTY WORKFLOW PROCESS: Prepare COUNTY Payroll (non-public safety)

Post-ERPPre-ERP

Eliminated;

replaced with

approval of

completed

timecards

Optional;

eliminated of

paper and data

entry reduces

errors

Systematically

doneManual

Very Manual

Optional;

elimination of

paper and data

entry reduces

errors

Depending upon

policy, employees

fill out exception

data; system

keeps track of

normal work hours

and shifts

Electronic

timekeeping

system allows for

web-based entry

of time

Electronic

Not needed

Electronically

routed to

supervisors

Pre-ERP Post-ERP

Electronic

approval

Manual

Voucher is

systematically

generated

Manual

Exceptions are

noted

systematically.

Should reduce

considerably

Manual

PROCESSPROCESS

January 2008

Eliminated

Exceptions are

noted

systematically;

timekeeping does

math electronically

ISA prints timecard

from timecard DB

NOTE: Some

depts copy old

timecard

Task takes about a

½ day every 2

weeks

Distribute paper

timecard to empl

mailboxes.

Agency prints out

new timecard

Empl’s fill in

timecard with

hours, benefit &

sick time, etc.

Task completed bi-

weekly

Empl’s give

timecard to

supervisor for

approval

Supervisor’s turn in

approved

timecards to Dept

Payroll Clerk (DPC)

DPC manually

audits each

timecard (w/ adding

machine)

DPC data enters

timecard into

Access DB.

DPC runs

official payroll

report of

completed

timecards

DPC runs test

payroll report