09 may 2017 - ardonagh.com · uks leading mga with approximately 10% market share (3) underwriting...

TRANSCRIPT

KIRS Investor Presentation

09 May 2017

Disclaimer

This document and the presentation to which it relates (“Presentation”) do not constitute or form part of, and should not be construed as, an offer to sell or an issue for sale or subscription of, or solicitation of any offer or invitation to subscribe for, underwrite or otherwise acquire or dispose of, any securities of TIG Topco Limited (to be renamed KIRS Group Limited (“KIRS”)) or any of its subsidiaries in the United States or any state or any jurisdiction in which such offer, sale or solicitation would be unlawful nor should they or any part of them form the basis of, or be relied on in connection with, any contract or commitment whatsoever which may at any time be entered into by the recipient or any other person, nor do they constitute an invitation or inducement to engage in investment activity under section 21 of the Financial Services and Markets Act 2000 (“FSMA”). This document and the Presentation do not constitute an invitation to effect any transaction with KIRS or to make use of any services provided by KIRS.

By accepting this document and the Presentation you agree and acknowledge that this document and its contents may contain proprietary information belonging to KIRS.

This document and the Presentation may contain forward looking statements in relation to certain of KIRS’ plans and current goals and expectations, in particular but not limited to its future financial condition, performance and results. These forward looking statements can be identified by the use of forward looking terminology, including the words “aims”, “believes”, “estimates”, “anticipates”, “expects”, “intends”, “may”, “will”, “plans”, “predicts”, “assumes”, “shall”, “continue” or “should” or, in each case, their negative or other variations or comparable terminology or by discussions of strategies, plans, objectives, targets, goals, future events or intentions. By their very nature, all forward looking statements involve risk and uncertainty because they relate to future events and circumstances which are beyond KIRS’ control, including but not limited to insurance pricing, interest and exchange rates, inflation, competition and market structure, acquisitions and disposals, and regulation, tax and other legislative changes in those jurisdictions in which KIRS, its subsidiaries and affiliates operate. As a result, KIRS’ actual future financial condition, performance and results may differ materially from the plans, goals and expectations set out in any forward looking statement made by KIRS. KIRS has no obligation to update any forward looking statement contained in this document or the Presentation or any other document or any other forward looking statement KIRS may make. All subsequent written or oral forward looking statements attributable to KIRS or to persons acting on its behalf should be interpreted as being qualified by the cautionary statements included herein. As a result, undue reliance on these forward looking statements should not be placed.

Past performance cannot be relied upon as a guide to future performance.

The financial results in this document and the Presentation include certain financial measures and ratios, including EBITDA, Pro Forma Adjusted EBITDA and certain other ratios that are not presented in accordance with IFRS and are unaudited. The financial information included in this Presentation only includes 9 months of audited information from the year ended December 31, 2015 for Towergate. Towergate’s Q1 2015 financial results are unaudited and unreviewed and may not reflect what Towergate results would have been had the current group structure and management been in place from January 1, 2015.

No representation or warranty, express or implied, is or will be made by any person in relation to the accuracy, fairness or completeness of the information or opinions made in this document and the Presentation, which information and opinions should not be relied or acted on, whether by persons who do not have professional experience in matters relating to investments or persons who do have such experience. The information and opinions contained in this document and the Presentation have not been audited or necessarily prepared in accordance with international financial reporting standards and are subject to change without notice. No responsibility or liability whatsoever is or will be accepted by KIRS, its shareholders, subsidiaries or affiliates or by any of their respective officers, directors, employees or agents for any loss howsoever arising, directly or indirectly, from any use of this document or its contents or attendance at the Presentation.

This document is for distribution only in the United Kingdom and the Presentation is being made only in the United Kingdom to persons falling within Articles 19, 43, 47 and 49 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended), to persons who have professional experience in matters relating to investments or to persons in the United Kingdom to whom this document may otherwise be lawfully distributed. This document is being supplied and the Presentation made to you solely in that capacity for your information. This document may not be reproduced, redistributed or passed on to any other person, nor may it be published in whole or in part, for any purpose.

By accepting this document and the Presentation, you agree to be bound by the foregoing limitations, undertakings and restrictions.

2

Agenda

3

14:30 – 14:35 Introduction

14:35 – 14:40 Investment Thesis

14:40 – 15:10 KIRS Strategy and Business Highlights

15:10 – 15:25 KIRS Financial Highlights

15:25 - 15:30 Conclusion

15:30 – 16:00 Q&A

Investment Thesis

Investment Thesis

KIRS(1) will be the result of a carefully targeted acquisition and hiring strategy in the UK insurance market

Towergate, Autonet(2)(3), Price Forbes(2)(3), Direct Group(2)(3) and Chase Templeton(2)(3) were specifically targeted due to:

A. Strong management teams

B. Leading position in their respective market segments

C. Significant organic growth and acquisition opportunities

D. Ability to create additional value from portfolio effect without disruption or integration of underlying businesses

Presence across the entire insurance value chain will allow KIRS to optimise service to customers and maximise commission capture

KIRS will be the leading diversified independent insurance intermediary group in the UK and is positioned to capitalise on the significant benefits of scale across all its segments

Highly resilient and profitable business model with significant cash flow generation capabilities

5

1

2

3

4

5

(1) Represents the Project Name for the creation of the new group. The final group name will be published in due course when trademark process is finalised.(2) Price Forbes, Chase Templeton, Autonet and Direct Group transactions are signed and completion is subject to regulatory approval.(3) Majority ownership.

KIRS will be the leading diversified independent insurance intermediary group in the UK

Significant Strategic Investment By Core Shareholders

6

2015 2016Jun NovApr Dec

2017 2018Q3 – Q4

Creation of Nevada and

acquisition of majority stake in Price Forbes

Acquisition of majority stake

in Broker Network

MDP investment in Towergate and Nevada

Acquisition of majority stake

in Chase Templeton(1)

Acquisition of majority stake

in Direct Group(1)

Acquisition of majority stake in

Autonet

HPS investment in

Towergate

~£680m Total Investmentby Core Shareholders to Support

the Creation of KIRS

KIRS is the result of a carefully crafted acquisition strategy executed over the last 24 months

(1) Completion subject to regulatory and other customary approvals.

Dedicated Shareholder Base

7

Key shareholders have invested ~£680m in the development of KIRS and will own >95% of group equity

(1) As of April 1, 2017.(2) As of March 31, 2017 SEC filing.

Founded in 2007

>100 investment professionals globally

$39bn(1) asset under management

Joint owner of Watford Re, global insurance and reinsurance group, alongside Arch Capital and second largest shareholder in NFP Corp.

Founded in 1992

41 investment professionals

$12.5bn(2) asset under management

Largest shareholder of NFP Corp., a leading US insurance broker

Founded in 1976

>370 investment professionals globally

$98bn asset under management

Strong prior knowledge of the insurance sector having invested in Willis Group, Alliant Insurance Services and USI

Founded in 1998

>110 investment professionals globally

$24bn asset under management

Significant experience in the insurance sector, including investments in many US mid-market insurance brokers

KIRS Vision and Key Highlights

Highly Supportive Market Backdrop

9

Phase 1First period of consolidation

Phase 2 Financial crisis

Phase 3 Consolidation of the consolidators & increased focus on innovation

2008 – 2011

Credit crisis causes significant slowdown in acquisitions

Total Number of Large Broker Acquisitions

2005 – 2008

First wave of consolidation

2012 – Today

“Historical” consolidators being acquired, new leaders emerge

Clear consolidation opportunity in a highly fragmented market

c. 150 consolidator transactions backed by £17bn of private equity capital and cheap leverage

Insurer funding providing additional firepower to consolidators

Consolidation significantly slowed down

Focus on new avenues of organic growth (new products and channels)

Oval and Giles acquired by AJ Gallagher, Jelf and Bluefin acquired by Marsh

New consolidators emerge backed by fresh private equity capital

Latest transaction multiples reflect highly attractive opportunity in the sector

Focus on integration across the value chain development of strong technology / digital footprint

KIRS is ideally positioned to capitalise on latest market trends

31

59

14

2008 2009 2010 2011

KIRS Guiding Principle: Maximise Presence Across Value Chain

10

e.g. American Airlines, Exxon

e.g. Private Motor, Home

Customer Characteristics

CU

STOM

ER

Services (Policy Administration, Claims, Renewals)

Pe

rso

nal

Smal

l &

Me

diu

m

Co

mm

erci

al

Larg

e C

orp

ora

teC

om

ple

x

Aggregator

Affinity partner

Consultant

Reg Broker

Reg Broker

MGAInternational

Wholesale Broker

Reg Broker

MGA

LondonWholesale Broker

Reg Broker

Online Broker

MGA Retail Broker

Retail Broker

Wholesale BrokerMGA

High £ / Policy Low Volume

Low £/ Policy High Volume

Market Characteristics

CA

PIT

AL

Collectively we have created significant opportunities to disrupt the “traditional” value chain, and realise value across multiple channels and verticals

Multiple Avenues to Capture Incremental Commission

11

£100 £100 £100 £100 £100 £100

AdvisoryWholesale

DigitalCar & Van

UnderwritingSpecialty MGA

UnderwritingInternational

AdvisoryCommericalCombined Retail Household

Distribution Underwriting Wholesale

Services Other Income Premium to Carrier

KIRSEconomics

£15 £25 £30 £35 £40 £50

Illustrative purposes only

Integration across the value chain gives KIRS the opportunity to maximise commission per policy

KIRS Resulted from Highly Selective Investment Strategy

12

2015 2016Jun Nov

Apr

Dec2017 2018

Q3 – Q4

Carefully structured acquisition plan executed in parallel with execution of Fix / Build / Grow plan in Towergate

Build

(1) Price Forbes, Chase Templeton, Autonet and Direct Group transactions are signed and completion is subject to regulatory approval.(2) Majority ownership.(3) 20% ownership.

(3)

(1)(2)(1)(2)(1)(2)(1)(2)

Grow

Fix

KIRS Operating Framework

13

Distribution Wholesale Underwriting

Services

Leading UK broker services network and leading claims management and TPA platform

Leading UK insurance broker with strong online presence, extensive local

footprint and high margin specialist brands

International insurance and reinsurance broker with a diverse

international income stream

Leading MGA in the UK with diversified product focus

Digital / Direct Advisory

GEO

(3)(1) (2)

(1)(2)

London Market International(1)(2)

(1)(2)

Highly diversified and integrated insurance distribution, underwriting and services company

Note: Financial metrics reflect 2016A exclude unallocated Pro Forma Adjusted EBITDA of (£3m).(1) Price Forbes, Chase Templeton, Autonet and Direct Group transactions are signed and completion is subject to regulatory approval.(2) Majority Ownership.(3) 20% ownership.

KIRS Company Highlights

1. Leading diversified independent UK insurance intermediary group

14

2. Extensive local footprint combined with global reach

3. Large and diversified earnings base

4. Highly scalable operating platform

5. Stable and cash generative business model

6. Early and continued engagement with the FCA

7. Market leading, highly experienced management team

1. Leading Diversified Independent UK Insurance Intermediary Group

15

UK’s leading MGA with approximately 10% market share (3)

Underwriting

Wholesale

Price Forbes is a top five independent London and international wholesale broker(1)

Services

UK’s leading broker services network and leading claims management platform

(£ in millions)

UK Insurance Broker Rankings by Income (1)

Leading independent SME and specialty personal lines-focused UK broker, distributing 3rd party and own branded insurance products

UK’s leading provider of property related insurance products via mortgage brokers

Leading van broker in the UK with significant share

Strong provider of Buildings & Contents (B&C) and Mortgage Payment Protection Insurance

Leading private medical insurance intermediary in the UK

Distribution

KIRS has a strong position in the UK insurance intermediary market

Leading diversified independent broker and top 10 broker overall in the UK market with c.£2.8bn GWP

(1) Source: Insurance Times Top 50 Brokers 2016.(2) Income is pro forma for Bluefin and Jelf acquisitions.(3) Managing General Agents Association.

£953

£866

£758

£650 £601

£507 £488

£387

£285 £243 £229 £223 £219

£146 £131 £117 £109 £75 £69 £64 £63 £62 £61 £56 £55 £55 £41 £40 £38 £36 £36 £35 £32

International

Personal

Commercial

London

2. Extensive Local Footprint Coupled with Global Reach

16

Distribution

Wholesale

Underwriting

Services

Key

Distribution

Underwriting

Wholesale

Services

9 local offices serving local brokers

Highly efficient operations centre in Doncaster

Primary operations in Doncaster and Preston

7 national contact centers each with a product focus online and on the phone

81 local offices across the country serving local clients

London headquartered, in close proximity to Lloyd’s and London market

97% of premium in respect of non-UK risks sourced from an extensive network of global brokers

IrelandUnited

Kingdom

Extensive UK distribution network linked to international capital markets

Wholesale Markets

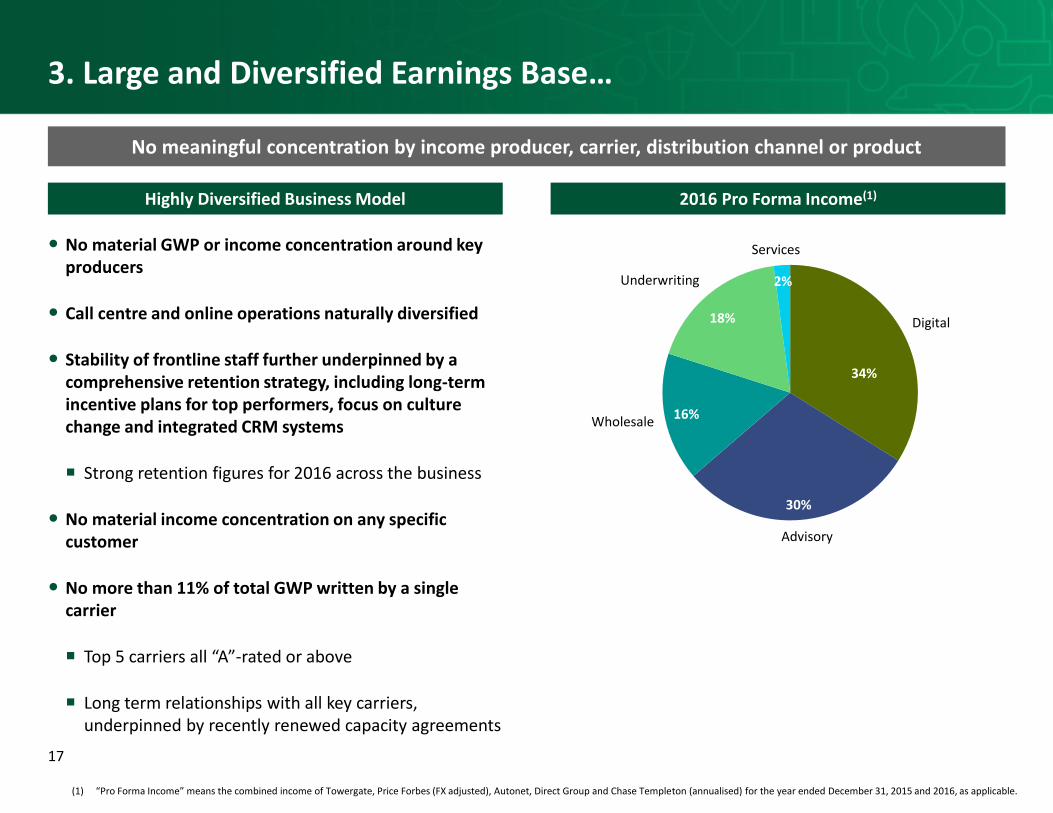

3. Large and Diversified Earnings Base…

No material GWP or income concentration around key producers

Call centre and online operations naturally diversified

Stability of frontline staff further underpinned by a comprehensive retention strategy, including long-term incentive plans for top performers, focus on culture change and integrated CRM systems

Strong retention figures for 2016 across the business

No material income concentration on any specific customer

No more than 11% of total GWP written by a single carrier

Top 5 carriers all “A”-rated or above

Long term relationships with all key carriers, underpinned by recently renewed capacity agreements

17

Highly Diversified Business Model 2016 Pro Forma Income(1)

Digital

Advisory

Wholesale

Underwriting

Services

34%

30%

16%

18%

2%

No meaningful concentration by income producer, carrier, distribution channel or product

(1) “Pro Forma Income” means the combined income of Towergate, Price Forbes (FX adjusted), Autonet, Direct Group and Chase Templeton (annualised) for the year ended December 31, 2015 and 2016, as applicable.

ExpertiseSpecialist knowledge

Partnerships

Strong customer relationships

“Stickiness” of specialist products

3. …With Numerous Niche Specialisms

18

A depth of specialist knowledge built-up over many years

Examples of Specialisms

Est. 1990

Property

Est. 1982

Marine

Est. 1998

Van

Est. 1907

Healthcare

Est. 2002

Medical

Est. 1983

Haulage

Est. 1985

Classic Car

4. Highly Scalable Operating Platform

19

Significant investments made across all KIRS businesses since early 2016 to optimise operating infrastructure and prepare the group for the next phase of growth

Key Programmes Include:

Premium and policy management

Renewals and administrative services

Offline sales and servicing

Coverage of the complete claims lifecycle

Platform provision

Optimisation of support functions (e.g. Finance, HR)

Key Areas of Focus:

IT Transformation Programme: £19m investment completing in Q2‘17 to create fit for purpose IT infrastructure

Finance Transformation Programme: £21m ongoing investment to maximise efficiency and integration vs. front end systems

Implementation of automated solutions in low complexity / high volume processes

Consolidation and simplification of property footprint and procurement function

Middle and Back Office Capabilities

Well-invested Claims and TPA platforms with significant spare capacity in existing systems

Services

Multiple investments underway focused on improving pricing capabilities and speed of product launches

Underwriting

Broad IT investment programme to upgrade and upscale existing infrastructure

Wholesale

Highly scalable, well invested online platform

Fast growing home insurance panel

Significant investment in new, consolidated front-end system

Distribution

5. Highly Stable and Cash Generative Business Model

20

Pro Forma Income(1)

Strong foundation, poised to achieve substantial growth and rapid organic deleveraging

Pro Forma Adjusted EBITDA(2)

% Margin 24% 27%

5.7x

Opening

£121£134

2015A 2016A

£491 £487

2015A 2016A

Rapid organic deleveraging driven by cost reduction

plans well under-way

(£ in millions)

Targeted Net Debt / Pro Forma Adjusted EBITDA

Note: The financial information included in this Presentation only includes 9 months of audited information from the year ended December 31, 2015 for Towergate. Towergate’s Q1 2015 financial results are unaudited and unreviewed and may not reflect what Towergate results would have been had the current group structure and management been in place from January 1, 2015.(1) “Pro Forma Income” means the combined income of Towergate, Price Forbes (FX adjusted), Autonet, Direct Group and Chase Templeton (annualised) for the year ended December 31, 2015 and 2016, as applicable.(2) “Pro Forma Adjusted EBITDA” means Towergate EBITDA, Autonet EBITDA, Price Forbes EBITDA, Direct Group EBITDA and Chase Templeton EBITDA, as adjusted for certain run rate cost savings and other exceptional

items as determined by management.

6. Early and Continued Engagement with the FCA

The FCA has been involved from the outset of the process, and remains supportive of the proposed new group

We have engaged with the FCA with full transparency and acted swiftly and appropriately when required

We continue to liaise with the FCA as the KIRS management team remains highly focused on completing the implementation of best in class risk and compliance policies and improvement of legacy operations

21

The FCA has been supportive of the development of KIRS

7. Market Leading, Highly Experienced Management Team

22

KIRS has attracted an experienced best of breed management team with a high profile in the market

Distribution Management

Wholesale Management

Underwriting and Services Management

Paul Dilley+25 years experience

Derek Coles+25 years experience

David Leatham+30 years experience

Andy Baughan+30 years experience

Andrew Bell+20 years experience

David Bruce+30 years experience

Scott Hough+20 years experience

Michael Donegan+35 years experience

David Baxter+40 years experience

Neil Pearce+20 years experience

James Masterton+25 years experience

Gordon Newman+50 years experience

Steve Anson+20 years experience

Joe Thelwell+15 years experience

Warren Dickinson+25 years experience

Craig Ball+10 years experience

Corporate Management

Kay Martin+25 years experience

Geoff Gouriet+20 years experience

Sarah Dalgarno+25 years experience

Antony Erotocritou+15 years experience

David Ross+26 years experience

Mark Mugge+20 years experience

Adrian Brown+28 years experience

Janice Deakin+16 years experience

Ian Donaldson+20 years experience

KIRS Financial Highlights

Strong EBITDA Growth

24

Strong EBITDA growth driven by efficiency improvements and income growth in Nevada

Growth

2015(2) 2016 £ %

Towergate £75 £84 £9 +12%

Nevada £46 £50 £4 +10%

KIRS Group £121 £134 £13 +11%

Pro Forma Income(1)

Pro Forma Adjusted EBITDA(3)

2015(2) 2016 Growth

Towergate 22% 26% +4%

Nevada 30% 31% +1%

KIRS Group 24% 27% +3%

Pro Forma Adjusted EBITDA Margin

(£ in millions)

Growth

2015(2) 2016 £ %

Towergate £340 £325 (£15) (4%)

Nevada £151 £163 £12 +8%

KIRS Group £491 £487 (£3) (1%)

(1) “Pro Forma Income” means the combined income of Towergate, Price Forbes (FX adjusted), Autonet, Direct Group and Chase Templeton (annualised) for the year ended December 31, 2015 and 2016, as applicable.(2) The financial information included in this Presentation only includes 9 months of audited information from the year ended December 31, 2015 for Towergate. Towergate’s Q1 2015 financial results are unaudited and

unreviewed and may not reflect what Towergate results would have been had the current group structure and management been in place from January 1, 2015.(3) “Pro Forma Adjusted EBITDA” means Towergate EBITDA, Autonet EBITDA, Price Forbes EBITDA, Direct Group EBITDA and Chase Templeton EBITDA, as adjusted for certain run rate cost savings and other exceptional

items as determined by management.

Towergate: Very Positive Income and Expense Trends

25

Income vs. Prior Year

Expenses vs. Prior Year

Second quarter of sustainable income growth and third quarter of EBITDA(1) growth

(7%) (7%)(5%)

2%

1%

(10%)

(5%)

0%

5%

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

5% 5% 5%

3%

(3%)

(0%)

(6%)(8%)

(4%)

(10%)

(5%)

0%

5%

10%

Q1'15 Q2'15 Q3'15 Q4'15 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Quarter 1 2017

Growth

2016 2017 £ %

Income £77 £78 +£1 +1%

Staff costs (£46) (£40) £6 14%

Op expenses (17) (19) (1) (8%)

Total expenses (£63) (£59) +£5 +8%

EBITDA(1) £14 £19 +£6 +42%

Margin 18% 25% +7%

New management team: expense savings started

(£ in millions)

Note: The financial information included in this Presentation only includes 9 months of audited information from the year ended December 31, 2015 for Towergate. Towergate’s Q1 2015 financial results are unaudited and unreviewed and may not reflect what Towergate results would have been had the current group structure and management been in place from January 1, 2015.(1) Pro Forma Adjusted EBITDA - “Pro Forma Adjusted EBITDA” means Towergate EBITDA, Autonet EBITDA, Price Forbes EBITDA, Direct Group EBITDA and Chase Templeton EBITDA, as adjusted for certain run rate cost

savings and other exceptional items as determined by management.

Towergate: Extensive Cost Reduction Programme

26

£56m cost savings identified and committed (20% reduction in 2015 cost base) with circa 1 yearaverage payback – 61% complete at end March 2017

programme essentially completed in Q1’17

Including server migration to Azure Cloud

Improvements to networks and telephony

Over 4,000 users upgraded to Windows 10

Contract signed with Accenture

Investment in robotics and process automation started

Completed initial process engineering activities

Closed Milton Keynes and Manchester locations

Footprint reduced by 21% with locations reduced from 140 to 98 (Jan‘15 to date)

Consolidated suppliers across cleaning, waste, repairs & maintenance and security

Back office operational process efficiency

Reduced reliance on agency and temporary staff

Commenced supplier rationalisation and procurement programme using external parties

Detailed implementation planning for consolidation of broker systems completed

First roll-outs commenced in 2017£5m

Total

IT Transformation £19m£7m

Finance Transformation

£21m£14m

SBU Turnaround £4m£7m

Property Cost Reduction

£1m£5m

InitiativeTotal One-off

Costs

Total Medium-

Term SavingsProgress to Date

Operational Efficiency

£2m£18m

Broker Systems Consolidation

£12m

£56m £59m

£6m

£4m

£7m

£4m

annualisedSavings toend Q1’17

£13m

--

£34m

£7m

£13m

£7m

£5m

annualisedSavings to end 2017

£16m

--

£48m Programme = 20% reduction in 2015 cost base

£13m cost savings already achieved in 2016 in-year result, 50% one-off spend paid before March’17

Additional Benefits Not Included in £134m EBITDA(1)

27

Medium-term identified and committed cost savings of £8m, signed contracts resulting in £6muplift in profitability and near-term revenue synergies of £2m have been excluded from EBITDA(1)

£8

Medium-term identified and committed cost savings

£6

Signed contracts resulting in profitability

step-change in 2017£2

Near-term identified and committed revenue

synergies

£16

Additional savings

(£ in millions)

(1) Pro Forma Adjusted EBITDA - “Pro Forma Adjusted EBITDA” means Towergate EBITDA, Autonet EBITDA, Price Forbes EBITDA, Direct Group EBITDA and Chase Templeton EBITDA, as adjusted for certain run rate cost savings and other exceptional items as determined by management.

Highly Cash Generative Business Model

28

Nevada is highly cash generative – Towergate capex and exceptional spend expected to reduce significantly post completion of the ongoing Transformation Programme

63%

90%

76%

Towergate Nevada KIRS Group

(1) Operating Cash Conversion defined as Operating and Investing Cash Flow (Adjusted EBITDA less Working Capital Movement and Maintenance Capex) over Adjusted EBITDA and excludes capex and exceptional costs related to cost reduction initiatives and other one-off costs.

2016 Operating Cash Conversion(1)

Indicative Capitalisation and Leverage

29

KIRS Group is expected to support circa £800m gross debt, with a net leverage of circa 5.7x,organically de-leveraging rapidly – we are exploring different financing options

Indicative Capitalisation & Leverage

2016A Pro Forma Adjusted EBITDA(1)

Towergate £84

Nevada £50

Total KIRS Group £134

Estimated Gross Debt £800

Estimated Cash (40)

Indicative Net Debt £760

Indicative Net Leverage 5.7x

Implied Transaction Equity Value(2) £655

(£ in millions)

(1) “Pro Forma Adjusted EBITDA” means Towergate EBITDA, Autonet EBITDA, Price Forbes EBITDA, Direct Group EBITDA and Chase Templeton EBITDA, as adjusted for certain run rate cost savings and other exceptional items as determined by management.

(2) Based on third party fairness opinion supporting Nevada roll-over contribution and price of Towergate's most recent rights issue.

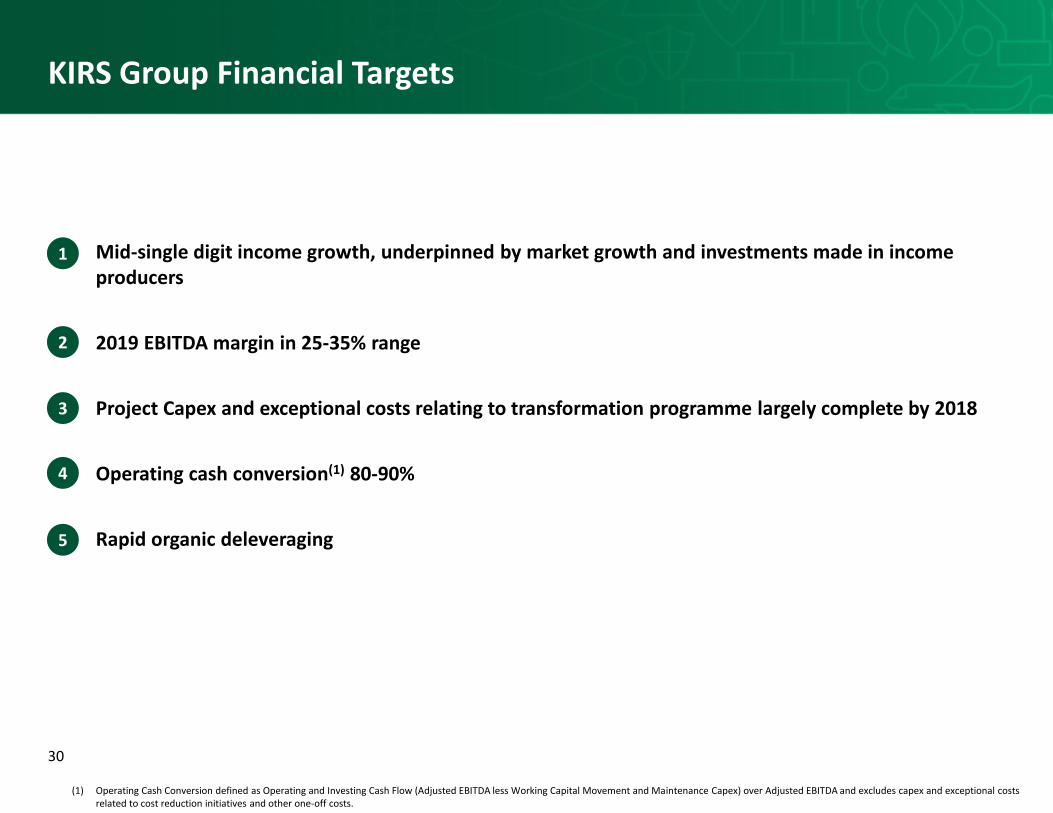

KIRS Group Financial Targets

Mid-single digit income growth, underpinned by market growth and investments made in income producers

2019 EBITDA margin in 25-35% range

Project Capex and exceptional costs relating to transformation programme largely complete by 2018

Operating cash conversion(1) 80-90%

Rapid organic deleveraging

30

1

2

3

4

5

(1) Operating Cash Conversion defined as Operating and Investing Cash Flow (Adjusted EBITDA less Working Capital Movement and Maintenance Capex) over Adjusted EBITDA and excludes capex and exceptional costs related to cost reduction initiatives and other one-off costs.

Conclusion

Conclusions

We are creating KIRS to capitalise on highly supportive market tailwinds in a structurally attractive sector

Transactions completed to date will combine into the largest independent player in the market, an ideal platform for future growth

Strong combination of market leading management teams, deep product expertise and wide presence across entire value chain

Highly resilient business model with great cash flow generation capabilities

HPS and MDP share management vision and are fully committed to supporting its implementation

32

1

2

3

4

5

KIRS will be the leading diversified independent insurance intermediary group in the UK

Q&A