1 1 executive summary core assets programming networks distribution ad sales financial appendix...

TRANSCRIPT

11

• Executive Summary

• Core Assets

• Programming

• Networks

• Distribution

• Ad Sales

• Financial Appendix

Agenda

22

Short-form Programming by Channel and Content TypeShort-form Programming by Channel and Content Type

Library

New Access

Acquisition

Original

UGV

[Emphasize that Minisode and Screening Room will leverage library; most original content will be against

Funny Bone / AXN; Crackle will be mostly UGV with potential for some

premium content]

33

• Executive Summary

• Core Assets

• Programming

• Networks: Digital

• Distribution

• Ad Sales

• Financial Appendix

AgendaAgenda

[CONSOLIDATION OF 5-6 MARKET SLIDES IN “DIGITAL NETWORKS” SECTION PROCESS]

44

ContentContent

Without Digital Networks, SPT Loses Influence and RevenueWithout Digital Networks, SPT Loses Influence and Revenue

DistributionDistribution

AdvertisingAdvertising

• Traditional networks aggressively build online & mobile audiences, replicating position & distribution advantage in the digital world

• Difficult to secure real estate on digital MSOs for SPT’s a la carte content, with limited spots available in digital MSO tiers

• Digital MSOs increasingly dictate business models and product development without SPT input

• SPT content continues to build and benefit other parties’ networks, replicating the current creation-distribution ecosystem

• Talent, seeking multi-platform exposure and marketing of productions, turns elsewhere

• Opportunity cost to not making library available online

$0

$500

$1,000

$1,500

$2,000

2005 2006 2007 2008 2009 2010 2011

Source: Adams Media Research, 2007

TV: $568 m

MusicVideo: $447 m

News &Sports: $433 m

Other: $145 m

UGV: $137 m

• Ad dollars shifting from traditional TV to online

• By 2011, TV content captures largest share of online ad spending:

55

Strategy: Create Digital Networks to Address Digital LandscapeStrategy: Create Digital Networks to Address Digital Landscape

Why Digital Networks?Why Digital Networks?

Generate RevenueBuild Assets

• Capture share of developing revenue streams (IP and mobile)

• Unlock and monetize SPT’s vast library

• Give SPT seat at table to shape digital products and business models

• Create program franchises with follow-on windows (e.g. DVD, Direct to Mobile)

• Establish 21st century network / distribution assets for SPT

• Build foundation for SPTAS to bring-in new partners and expand lines of business

• Provide long-term distribution leverage for SPT content

• Provide outlets for new content and talent

66

Four Networks Will Activate SPT’s Multi-Billion Dollar Library*Four Networks Will Activate SPT’s Multi-Billion Dollar Library*

Your favorite feature length, contemporary classic films across all major genres: comedy, action, drama, family, sci-fi and cult

• Episodes from the heyday of sit-coms

• Outrageous shorts and busted pilots

• Originals by contemporary comedians

• SPT’s “middle tail” content is hard to find

• Deep classic comedy library

• Demand for short form, original comedy exploding online

Classic hard-hitting action TV series and original takes on today’s favorite action movies and stars

• Deep action-themed library

• SPE relationships with

celebrity action stars and film franchises

• Key young male action demo also early adopter of digital tech- nology

• SPE’s 3,500+ feature library

What: 2 Popular Genres, 2 Popular FormatsWhat: 2 Popular Genres, 2 Popular Formats

Why: We matched our assets with market demandWhy: We matched our assets with market demand

Favorite retro TV shows told in in 4-6 minute “minisodes”

• Extensive library of much-loved shows

• Format appeals to today’s “bite sized” video consumption

• Edited to meet the demo’s ironic, camp sensibility

• Popular TV format (Turner, USA, AMC, etc.) embraced by audiences but not yet translated to digital

*Five including SPT’s investment in FearNet and SPT Mobile’s distribution of FearNet Mobile

77

Programming Philosophy Based on 4 Building BlocksProgramming Philosophy Based on 4 Building Blocks

Acquisition

Original Production

Library

New Shows

Star-Driven

Branded Ent.

Traffic Creating

New Access

SPE Film

SPT TV

Prosumer

Short & longform

Credence WalkerWTF with

Penn Jillette

Busted Pilots

Short-Lived Series

88

Distribution PhilosophyDistribution Philosophy

Network Distribution Approach

Partners D2C

Online Mobile Online Mobile

• Portals / Aggregators

• Syndicators

• Social Networks

• Virtual Worlds

• Carriers

• Non-Carrier Aggregators

Other

• MSOs & IPTV

• SCE: PS3, PSP

• SEL: Bravia, VAIO

• Vertical sites

• Originals sites

• WAP

• Application

• Text

Emphasis on Syndication

99

Digital Networks Digital Networks andand Crackle Complete SPT’s Offering Crackle Complete SPT’s Offering

Distribution

Networks are syndicated to digital “MSOs” (e.g., Joost, AOL, MySpace, Yahoo, MSN) in their player/environment

Distribution

Crackle’s website and Crackle player central to the strategy

Originals

Original programming is more linear in nature, uses high-end talent and is professionally selected and produced

Originals

Short-form programming is largely meant to spur UGV development for the purposes of individual exposure / fame

Content - selection

Content is all pre-screened for quality (like a network) – an “upfront” mentality where we are the buyer

Content - selection

Editorial and user-based rankings of content drive pyramid

•Library play•Original

programming will also appear on Grouper

•User involvement play

•User involvement occurs on and is enabled by Grouper

1010

Digital Networks FinancialsDigital Networks Financials

$2.0

$6.0

$8.0

$4.0

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

FY07 FY08 FY09 FY10

($ in MM)

$10.0

$20.0

$25.0

$15.0

$0

$5

$10

$15

$20

$25

$30

FY07 FY08 FY09 FY10

($ in MM)

EBIT Revenue

[Placeholder Numbers]

1111

• Executive Summary

• Core Assets

• Programming

• Networks: Crackle

• Distribution

• Ad Sales

• Financial Appendix

AgendaAgenda

[CONSOLIDATION OF 5-6 MARKET SLIDES IN “CRACKLE” SECTION PROCESS]

1212

Crackle’s Strategic FocusCrackle’s Strategic Focus

• Discuss high-level market issues / trends

• Outline Crackle’s position in marketplace

1313

Crackle Strategy OverviewCrackle Strategy Overview

Content / ChannelsContent / Channels

Platform / ProductPlatform / Product

Partners / DistributionPartners / Distribution

MonetizationMonetization

Differentiate service

Build audience

Generate revenue

Goals

Summary level strategy for

these key issues

1414

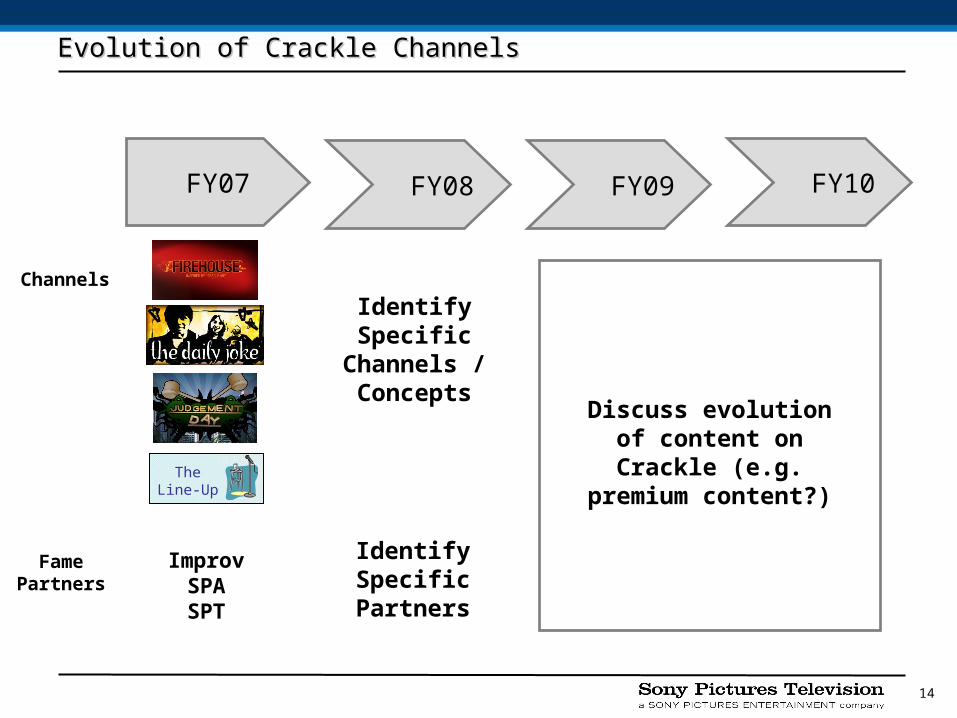

Evolution of Crackle ChannelsEvolution of Crackle Channels

FY07 FY09 FY08 FY10

Channels

FamePartners

TheLine-Up

ImprovSPASPT

Identify Specific

Channels / Concepts

Discuss evolution of content on Crackle

(e.g. premium content?)

Identify Specific Partners

1515

Crackle Platform DevelopmentCrackle Platform Development

Device Support

New Features

FY07

• Expansion of embedded player

–Integrate search, upload, comments and “shoutout” features into player

• Syndication via 1-Click publishing (e.g., Digg, EBay)

• Online editing functionality

• Branded channel templates (framework for premium producers, sponsors)

• Family Filter

• Initial camera integration (Pure Digital)

• Initial R&D for Sony devices: PS3, VAIO

FY08/09

• Continue expansion of embedded player

–Add real-time community features including chat

• Add geographic data and search

• Personalized recommendations/channel

• Customized functionality

–User profiles, instant messaging

• Mobile phone integration

• Hardware integration (e.g., PCs, Cameras, Camcorders, Cell Phones, Set-top Boxes)

1616

Expansion of Crackle’s Distribution NetworkExpansion of Crackle’s Distribution Network

Cross-Sony Partnerships

MarketingDistribution Partners

User Driven “1 Click”

Digital Imaging

• Power video uploads

• Embed screensaver and software

• Users syndicate playlists via embedded player

• Embed Grouper player on partner sites

• Distribute content “pyramids”

• Purchase advertising on high traffic web sites

• Drive users back to Grouper.com

1717

Crackle Revenue PlanCrackle Revenue Plan

• Overall trends in sales of advertising against UGV content

• Ad units (pre-roll / post-roll, overlays, banners)

• Sales strategy

• Sponsorship concepts

• Traction to-date with advertisers

1818

Key Crackle MetricsKey Crackle Metrics

[Placeholder Numbers]

[Include Key Crackle Metrics]

1919

Crackle FinancialsCrackle Financials

-$18.0

$5.0

$15.0

-$15.0

-$20

-$15

-$10

-$5

$0

$5

$10

$15

$20

FY07 FY08 FY09 FY10

($ in MM)

$13.0

$40.0

$60.0

$20.0

$0

$10

$20

$30

$40

$50

$60

$70

FY07 FY08 FY09 FY10

($ in MM)

EBIT Revenue

[Placeholder Numbers]

2020

• Executive Summary

• Core Assets

• Programming

• Channels

• Distribution

• Ad Sales

• Financial Appendix

AgendaAgenda

2121

Digital Distribution Landscape: Growing DemandDigital Distribution Landscape: Growing Demand

• Media conglomerates have licensed their content for digital sell-through

• Networks/labels have extended their brands online

– ABC.com: ad-supported full episodes of primetime shows

– Launched AOL In2TV, ad-supported classic TV episodes

– Warner Music Group to distribute library of music videos via YouTube

– CBS to offer wide variety of short-form video programming (news, sports, entertainment) on YouTube

102

527

1,086

1,864

64

171

348

558

23

45

106

242

6401,070

1,500

2,271

433

2006 2007 2008 2009 2010

U.S. Consumer/Advertiser Spending ($M) CAGR%

$477$477

$829$829

$4,934$4,934

Online videoadvertising

DST

IP-VOD

Subscription VOD

$1,812$1,812

$3,040$3,040

131%131%

120%120%

51%51%

254%254%

Total 79%79%

Source: Adams Media Research, Veronis Suhler, eMarketer

2222

Digital DistributionDigital Distribution

SPT Strategy & Financials

Total Revenue

• Aggressively build the distribution network– Strike partnerships across the complete spectrum of traditional and on-line players

• Continue to expand the overall content offering– Broaden selection of film and TV product– Introduce the most compelling short-form/original content into the offering

• Continue to lead the market in innovating the digital product offering and usage models– Focus on Digital Sell-Through as foundational/core product

• Build a strong, retail-focused organization – Create innovative marketing and promotional programs – Continue to lead the industry with respect to asset delivery and digital operations

2323

Mobile OverviewMobile Overview

• Taken responsibility for game development from SPDE and coordinating greenlights with SPTI– Slating 8 games per year

• Now directly responsible for personalization products focusing on– Tones/graphics based on film/TV properties– Packages based on compelling brands/themes

• Market approach– Close carrier relationships and marketing support– Consistent product development– Reinvigorate the library

SPT Strategy & Financials

$2.0

$6.0

$8.0

$2.0

$4.0

$6.0

$8.0

$4.0

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

Q2/ BGT FY08 FY09 FY10

($ in MM)

$15.0

$25.0

$30.0

$15.0

$20.0

$25.0

$30.0

$20.0

$0

$5

$10

$15

$20

$25

$30

$35

FY07 FY08 FY09 FY10

($ in MM)EBIT Total Revenue

[Placeholder Numbers]

Budget/Prior MRPQ2/MRP