1. 2 pension funds - polish experiences sławomir pomarański head of division pension funds...

TRANSCRIPT

1

2

Pension Funds - Polish Experiences

Sławomir Pomarański

Head of Division

Pension Funds Supervision Department

3

Plan of presentation Social Security System in Poland Development of the market Second Pillar (private pension funds) Third Pillar (Employee pension plans) Superintendency of pension funds

4

Elements of the social security system in Poland

• I pillar - mandatory PAYG system

• II pillar - mandatory funded system

• III pillar - voluntary

(Employee Pension Schemes)

I AI A

I B

I pillar

II pillar

WORLD BANK WORLD BANK CONCEPTCONCEPT

OECD CONCEPTOECD CONCEPT

5

THREE PILARSSocialInsuranceFund

Savings and additional insurance

Open-ended Pension Funds

Fundedobligatory,capital,administered by privateinstitutions,individual accounts

Fundedvoluntary,capital,administered by privateinstitutions,individual accounts

PAYGobligatory,contract of generations,administered by thepublic institution,individual accounts

First Pillar Second Pillar Third Pillar

6

Age limitations in the begining in 1999

• People over 50 in 1999 have to save for their pension in old mandatory PAYG system exclusively (Defined Benefit),

• People between their 30 and 50 in 1999 had a right to choose reformed Social Insurance Institute or share their contribution between Open-ended Pension Funds (OPF) and Social Insurance Institute, (63% joined pension funds)

• For people less than 30 in 1999 PAYG and OPF are obligatory.

7

Basic principles

• Close correlation between contributions and benefits

• Combination of PAYG and the funde system

• In the future – financial indepencdency

8

Reformed PAYG

• Reformed Social Insurance Institute mandatory for all insured persons,

• System for all insured people covered by reform is based on defined contribution (DC) scheme,

• Individual accounts were created for insured,

9

Open-ended pension funds

• Funds started operations in 1999 - first contributions in May,

• Financing mechanism is based totally on funding,

• Funds are managed by the pension societies,

10

Open-ended pension funds

• Participants have a right to choose between privately managed funds,

• Contributions transfered by Social Insurance Institute,

• Posibility to change a open-ended fund.

11

Open-ended pension funds

• Pension Funds are part of public finance,

• First pensions from the Pension Funds will be paid in 2009,

• The target level of benefits from I and II pillar is about 40 - 60% of the salary.

12

Pension societies

• The society operate as a joint-stock company and have no business object other than that of creating and managing funds and representing the funds before third persons,

• The society manage the fund for a fee,

13

Pension societies

• The society has a share capital of no less than a zloty equivalent of

EURO 5,000,000

• One entity has a shareholder of no more than one pension society.

14

Pension funds

• The fund is created by none other than the society,

• Fund has no bankruptcy ability,• The main task of the fund activity is to

accumulate participants contributions and investing these assets to maximise the security and profit efficiency of investment,

• Participant contribution supplies monthly the individual account in the fund.

15

Elements of the funded part of system

SOCIAL INSURA-

NCE INSTI-TUTE(ZUS)

contribution to the II

pillar

DEPOSITARY BANK

Transfer Agent

Banking sector

IT SYSTEM

Information concerning fund assets

Information concerning fund liabilities

PENSION SOCIETY

Informationabout participants

Information about resources

managingPENSION

FUND

16

Development of the market

• As far 15* pension funds operate on the market,

• about 12.2 mln - members of the funds (more than 14 mln signed agreements)*,

• 3 funds have more than 1.8 milion affiliates.

* January, 2000 - 21 pensions funds

17

Development of the market

• Funds accumulated almost 62 billion zloty (it represents about 20.6 billion USD),*

• More than 50% of assets are currently invested in treasury bonds, and about 30% in shares.

* as Jnauary, 2005

18

Development of the market

Pension fund investment

32,12%29,72%

2,71%6,81%

2,07% 4,43%

56,97%61,22%

1,64%0,18%

0,00% 2,13%

0%

20%

40%

60%

80%

100%

Dec 31, 1999 Jan 2005

shares treasury bills bank deposits

treasury bonds other instruments foreign investements

19

OPF No. of members Nett assets (zloty)Commercial Union OFE BPH CU WBK 2 598 684 17 371 055 062,94OFE Nationale Nederlanden Polska 2 146 060 14 079 019 809,85OFE PZU Złota Jesień 1 981 480 8 695 143 616,92AIG OFE 1 040 619 5 334 993 408,04Generali OFE 431 184 2 101 419 005,25Bankowy OFE 449 468 1 985 702 575,28OFE Sampo 670 211 2 169 579 841,88OFE Skarbiec - Emerytura 618 679 2 029 563 163,04Credit Suisse L&P OFE 470 524 1 954 100 548,79OFE Allianz Polska 284 738 1 670 469 108,18OFE Ergo Hestia 471 546 1 343 616 369,14OFE Pocztylion 495 505 1 308 458 336,39Pekao OFE 298 297 1 013 825 413,85OFE DOM 263 815 1 011 153 785,76OFE Polsat 312 977 558 844 273,07TOTAL 12 533 787 62 626 944 318,38

20

Fund’s Investment Limitation (as % of assets value) I

• No limitation - bonds, bills and other securities issued by the State Treasury,

• 20% - bank deposits and bank securities (additionally - max. 5% in one entity, max. 7,5% in related entities),

• 40% - shares in companies listed on the regular stock market (additionally - max. 10% in one issue).

21

Fund’s Investment Limitation (as % of assets value)

• 10% - Shares of any other securities quoted on over the counter market or not quoted on the regulated market, but admitted to public trading,

• 15% - participation units disposed by open end investment funds or specialised open end investment funds (additionally - max. 5% of one entity),

22

Fund’s Investment Limitation (as % of assets value)

• 10% - Investment certificates issued by closed end or mixed investment funds (additionally max. 2% in single fund certificate),

• Additionally: 60% - shares in companies and investment funds certificates total.

• 40% - Bonds and other debt securities issued by communes, unions of communes or the City of Warsaw, and admitted to public trading,

23

Fund’s Investment Limitation (as % of assets value)

• 40% - fully secured bonds issued by entitles other than communes, unions of communes or the city of Warsaw and admitted to public trading.

• Investment in the categories of instruments mentioned above shall account cumulatively for no less than 95% of the pension fund’s assets.

24

Fund’s Investment Limitation (as % of assets value)

Other investments (maximum 10% total):• bonds and other debt securities issued by public companies

and not admitted to public trading,• other fully secured bonds not admitted to public trading, • bonds and other debt instruments issued by public

companies and not mentioned previously, • other investments which will be precised through the decree

of the Council of Ministers and Law of Public Trade of Securities.

25

Fees structure

• Front up fee - deducted by fund on up-front basis from contribution and transferred to society before convergence contribution amount on accounting units.

• Managing fee - deducted from assets.

• Other costs deducted from assets eg. brokerage fee and custodian fee.

26

Fees structureLevel of current fees:

• front up fee ranges from 7 (now) down to 3,5% (2014)

• managing fee: deducted from accumulated assets (max. 0.6% a year).

• transfer fee (for transfer before 2 years of participation, 80/160 zloty (approx. 26 – 52 USD).

27

• It is additional method for pension coverage after retirement,

• Savings accumulated under such plans should offer upper-standard pension benefits,

• Might be a kind of “perks” for employers.

Voluntary (Employee Pension Schemes)

28

Set of agreements, which employer must sign Set of agreements, which employer must sign to create an employee pension planto create an employee pension plan

corporate pension agreement(employers with employees)

agreement withinsurance company

or mutual insurance institution

agreementwith investment fund

statue of employeepension fund

employer agreement withfinancial institution

employee pension agreement

employee pension plan

Voluntary (Employee Pension Schemes)

29

Forms of voluntary (Employee Pension Schemes)

• employee pension fund,• agreement with investment fund,• agreement of group investment life insurance for

employees with insurance company,• agreement of group investment life insurance for

employees with mutual insurance institution under which employees become a member of that mutual institution.

30

Conditions which should be met to create an Employee Pension Scheme

• employer employ at least 5 employees,

• exception - when firm is operating for at least 3 years and employs 3 employees,

• employer has to register his firm at least one year before setting corporate pension agreement.

31

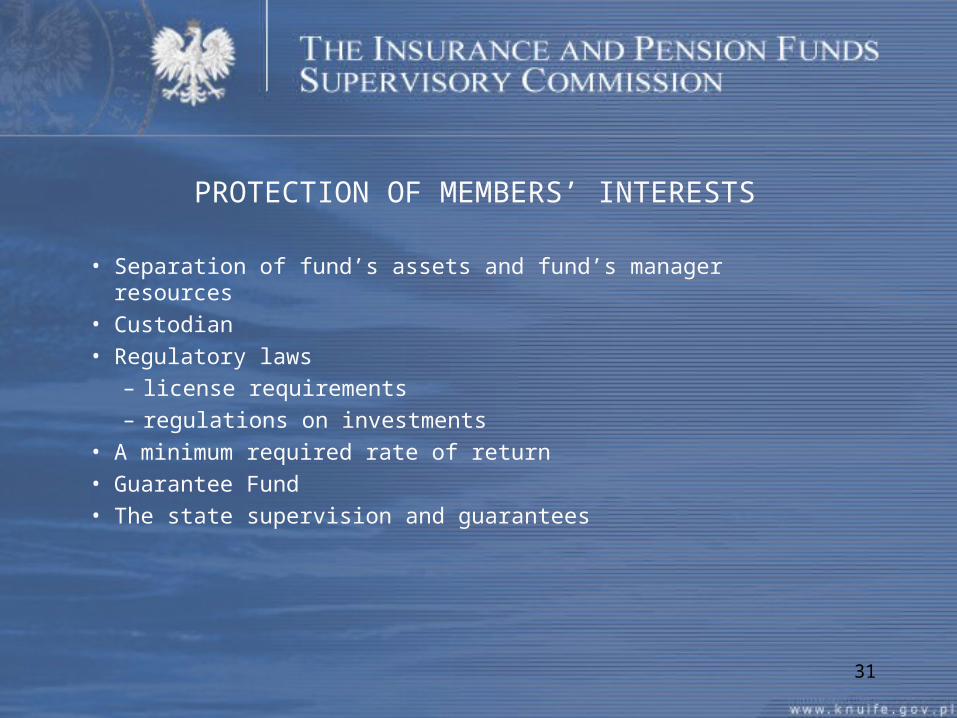

• Separation of fund’s assets and fund’s manager resources• Custodian• Regulatory laws

– license requirements– regulations on investments

• A minimum required rate of return• Guarantee Fund• The state supervision and guarantees

PROTECTION OF MEMBERS’ INTERESTS

32

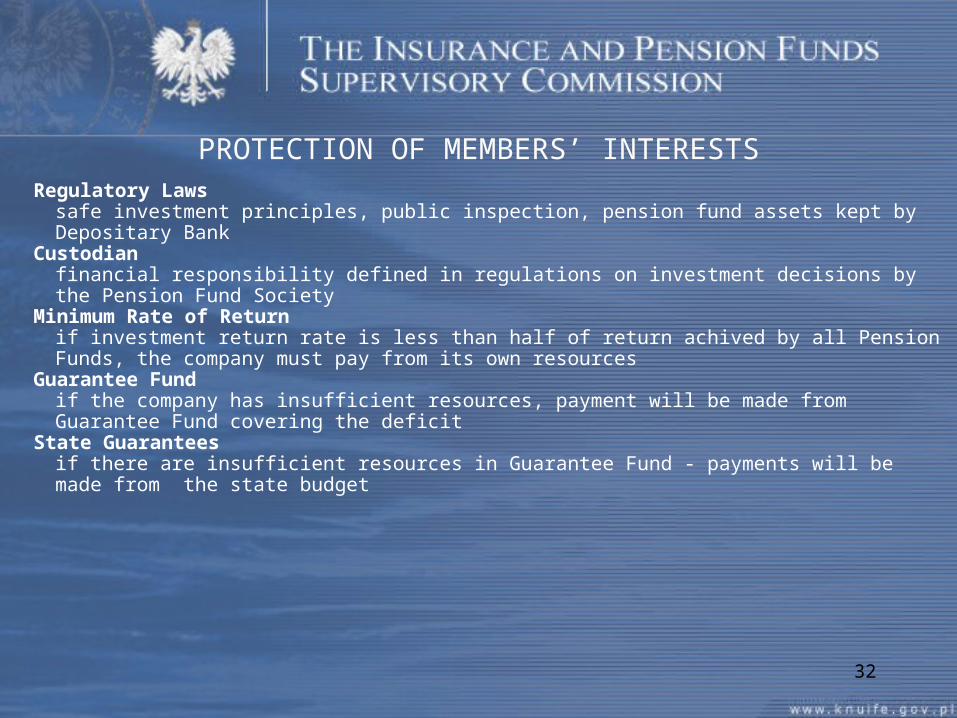

PROTECTION OF MEMBERS’ INTERESTSRegulatory Laws

safe investment principles, public inspection, pension fund assets kept by Depositary BankCustodian

financial responsibility defined in regulations on investment decisions by the Pension Fund SocietyMinimum Rate of Return

if investment return rate is less than half of return achived by all Pension Funds, the company must pay from its own resources

Guarantee Fundif the company has insufficient resources, payment will be made from Guarantee Fund covering the deficit

State Guaranteesif there are insufficient resources in Guarantee Fund - payments will be made from the state budget

33

The Insurance and Pension Funds Supervisory Commission

•General objectives:•1/ to safeguard the interests of the insured, pension funds and occupational pension schemes members•2/ to promote the security of the insurance system and pension saving•3/ to promote the development of efficient savings of national insurance system and pension structures

34

The Composition of the Commission’s Members

Voting members:Chairman - appointed by the Prime

MinisterDeputy Chairman - appointed by the

appropriate minister for financial institutions

Deputy Chairman - appointed by the appropriate minister for social security

Members:Chairman of the Securities and

Exchange Commission or his deputy

President of the Office for Competition and Consumer Protection or Vice President

Non-voting members:

Insurance Ombudsman

Person appointed by the President of the Republic of Poland

Inspector General of Banking Supervision

35

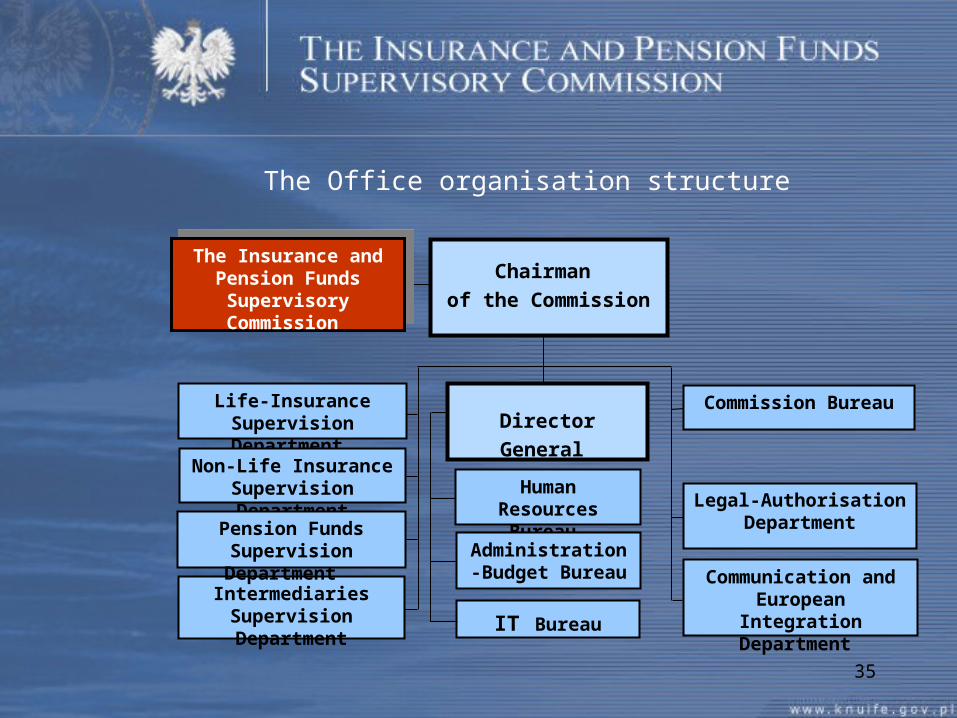

The Office organisation structure

Chairman

of the Commission

The Insurance and Pension Funds

Supervisory Commission

The Insurance and Pension Funds

Supervisory Commission

Commission BureauDirector General

Human Resources Bureau

Administration-Budget Bureau

Legal-Authorisation Department

Communication and European Integration

Department IT Bureau

Life-Insurance Supervision Department

(NA)Non-Life Insurance Supervision Department

Intermediaries Supervision Department

Pension Funds Supervision Department

36

Supervision of Pension Funds

The Supervisory Commission

Open-ended Funds Employeee Pension Funds

Depositary Banks

37

Exchanging of information between Supervisiors of financial Institutions

IPFSC

Securities Commission Banking Supervision

38

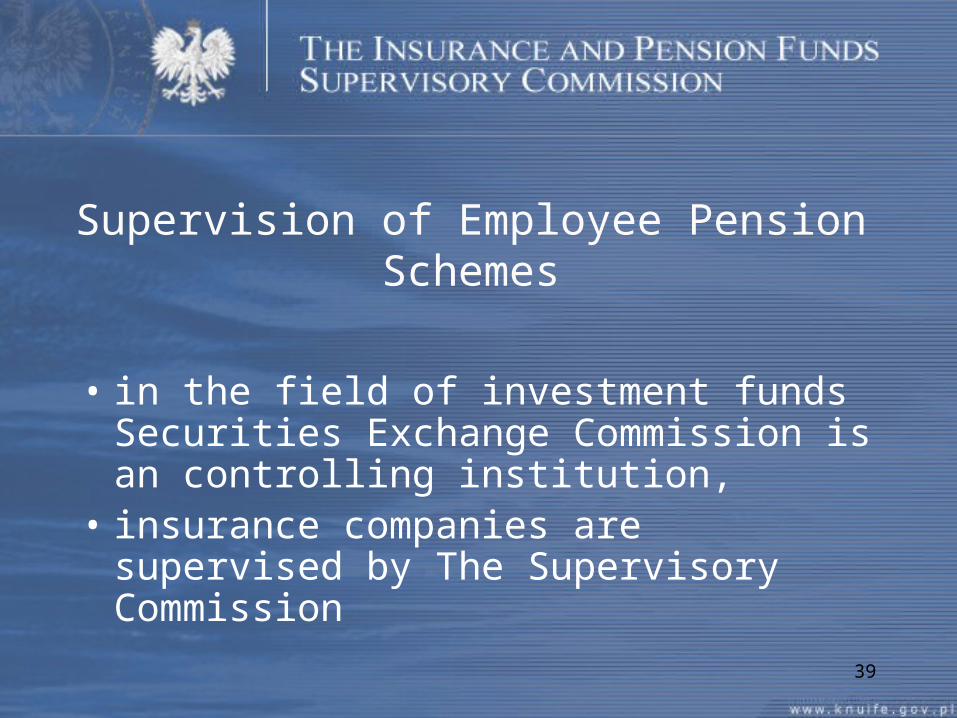

Supervision of Employee Pension Schemes

• The Supervisory Commission registers and supervises only legal side of plans,

• The Supervisory Commission supervises employers, not companies managing Pension Program,

39

Supervision of Employee Pension Schemes

• in the field of investment funds Securities Exchange Commission is an controlling institution,

• insurance companies are supervised by The Supervisory Commission

40

Supervision of Pension Funds

• Financial control of funds and more precisely transactions consist of:

buy/sell offers control,

control of done transactions and comparison with fund’s portfolio,

41

Supervision of Pension Funds

control of investment categories given by the law,

controlling of prices paid,

controlling the possibility of inside trading or illegal dealing agreements,

42

Supervision of Pension Funds

• transaction verification, whether investment policy is similar as this given by statue,

• verification of transaction results from participant point of view and his interest.

• Generally the main aim of investment policy is comparing the facts with adequate laws and decrees.

43

Supervision of Pension Funds

• Pension funds report to Superintendency on day-, month- and year basis (daily information contain funds activity, monthly concerning society, year information are inspected by auditor),

• Such system should help to protect funds against risky or illegal investment policy.

44

Complaints:

• Fund member may lodge with The Supervisory Commission a complaint against the fund,

• Inspection Unit was dealing with 2027 complaints in 1999, and 1362 in 2004.

45

Subject of complaints:

• Sales force mistakes, misinforming and law violations

• Social Insurance Institute operations e.g. problems with registration in ZUS data base

46

Subject of complaints :

• Pension funds operations

• Offering additional benefits for signing participation agreement with fund

• Misleading advertisement

47

The Supervisory Commission has the following rights:

• to request from the Pension Fund Society copies of all documents relating to the activities

• to request any information or interview any employees of the Society regarding the activities of the Fund

48

The Supervisory Commission has the following rights:

An inspection may be conducted on the premises of:

• a Pension Fund Society• a Depositary• an entity entrusted with keeping of the

register of the Fund members

49

The Supervisory Commission rights:

• The Supervisory Commission may administer upon the inspected party a fine of up to 500.000 zloty (which represents 125.000 USD),

50

Fine procedure:

1. On-site inspection,2. Superintendency Department presents project of

instruction or fine. The project is analysed by Legal-Licensing Department,

3. Legal-Licensing Dept. presents formal opinion about this project,

4. Superintendency Department recommends this decision Supervisory Commission to approval.

51

PENSION – NEW SYSTEM

• Paid from two or three sources

• Established from:– earnings from the whole period of work– length of working life– increase of employees’ wage funds– efficiency of investments in the second pillar– savings from the third pillar

• Guaranteed by the state

• Unrestricted earning possibilities for pensioners

52

The Insurance and Pension FundsSupervisory Commission

6 E Niedźwiedzia Str.02-737 Warsaw

Poland

tel. + 48 (0 22) 54 87 413fax. + 48 (0 22) 5487415

[email protected]://www.knuife.gov.pl