(1) capita alternative fund services (guernsey) limited ... capita [20… · incorporated in the...

TRANSCRIPT

Neutral Citation Number: [2011] EWHC 2336 (Comm)

Case No: 2009 FOLIO 977

IN THE HIGH COURT OF JUSTICE

QUEEN'S BENCH DIVISION

COMMERCIAL COURT

Royal Courts of Justice

Strand, London, WC2A 2LL

09/09/2011

B e f o r e :

THE HONOURABLE MR JUSTICE EDER ____________________

Between:

(1) CAPITA ALTERNATIVE FUND SERVICES

(GUERNSEY) LIMITED

(formerly known as Royal & SunAlliance Trust

(Channel Islands) Limited)

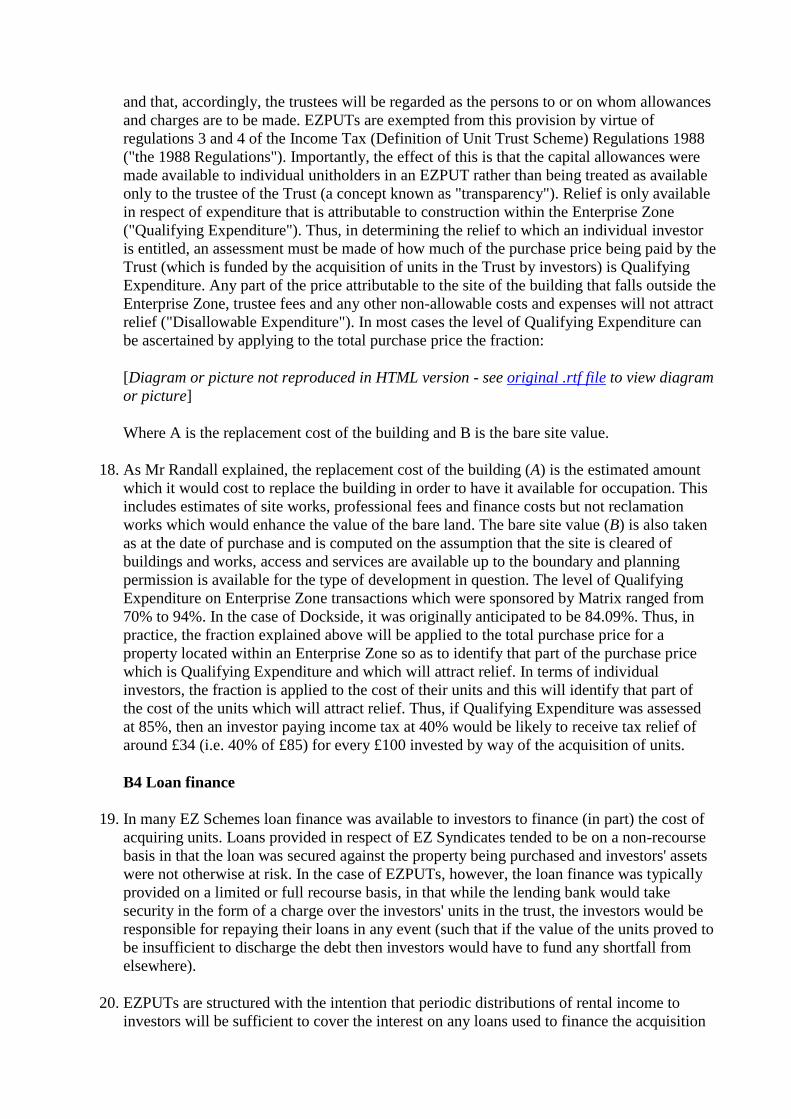

(2) MATRIX-SECURITIES LIMITED Claimant

- and -

DRIVERS JONAS (A FIRM) Defendant

____________________

Ms Sue Carr Q.C., Mr Graham Chapman and Ms Lucy Colter (instructed by Bond Pearce

LLP) for the Claimant

Mr Roger Stewart Q.C. and Ms Sian Mirchandani (instructed by Berrymans Lace Mawer

LLP) for the Defendant

Hearing dates: 5, 6, 9, 10, 11, 12, 16, 17, 18, 19, 24, 25 May 2011 ____________________

HTML VERSION OF JUDGMENT

____________________

Crown Copyright ©

Mr Justice Eder:

Section A: INTRODUCTION

A1 Introduction

1. This is a substantial claim for professional negligence. The claim arises out of a failed

investment in a factory outlet shopping centre ("FOC") which was to be developed from a

Grade II* listed structure known as the "Boiler Shop" situated at Chatham Historic

Dockyard, Medway, Kent ("Dockside"). Dockside was acquired for the residue of a 155

year leasehold term on 5 April 2001 by the First Claimant ("Capita") which was then known

as Royal & SunAlliance Trust (Channel Islands) Limited. Capita is trustee of The Matrix

Chatham Maritime Trust ("the Trust") which was an investment vehicle established to

enable 480 individual investors to invest in Dockside. The Second Claimant ("Matrix")

sponsored the creation of the Trust and was responsible for establishing and promoting the

investment. Capita paid the vendors of Dockside total consideration in the sum of

£62,850,000 in order to acquire its interest in Dockside. Capita was appointed as trustee of

the Trust by a Trust Deed dated 2 April 2001 which was executed by Capita and Matrix. The

Trust is in the form of an Enterprise Zone Property Unit Trust ("EZPUT") although, for

reasons set out below, it is resident in Guernsey. Matrix is the Trust Manager under the

terms of the Trust.

2. The Claimants say that they retained the Defendants, who were at the material time a firm of

chartered surveyors and property consultants, to advise them in relation to the acquisition of

Dockside; and that pursuant to such retainer the Defendants provided positive advice about

Dockside's commercial prospects and valued Dockside in the sum of £62,850,000 (with the

benefit of Enterprise Zone tax allowances) and £48,150,000 (without the benefit of

Enterprise Zone tax allowances). The Claimants say that they relied upon this and, in

particular, that Capita relied on this advice when it acquired its interest in Dockside. Capita

retains the long leasehold interest in Dockside that it acquired on 5 April 2001. The

Defendants received fees totalling in excess of £500,000 for their work on the project, of

which nearly £400,000 was, according to the Defendants' invoice, for "investment and

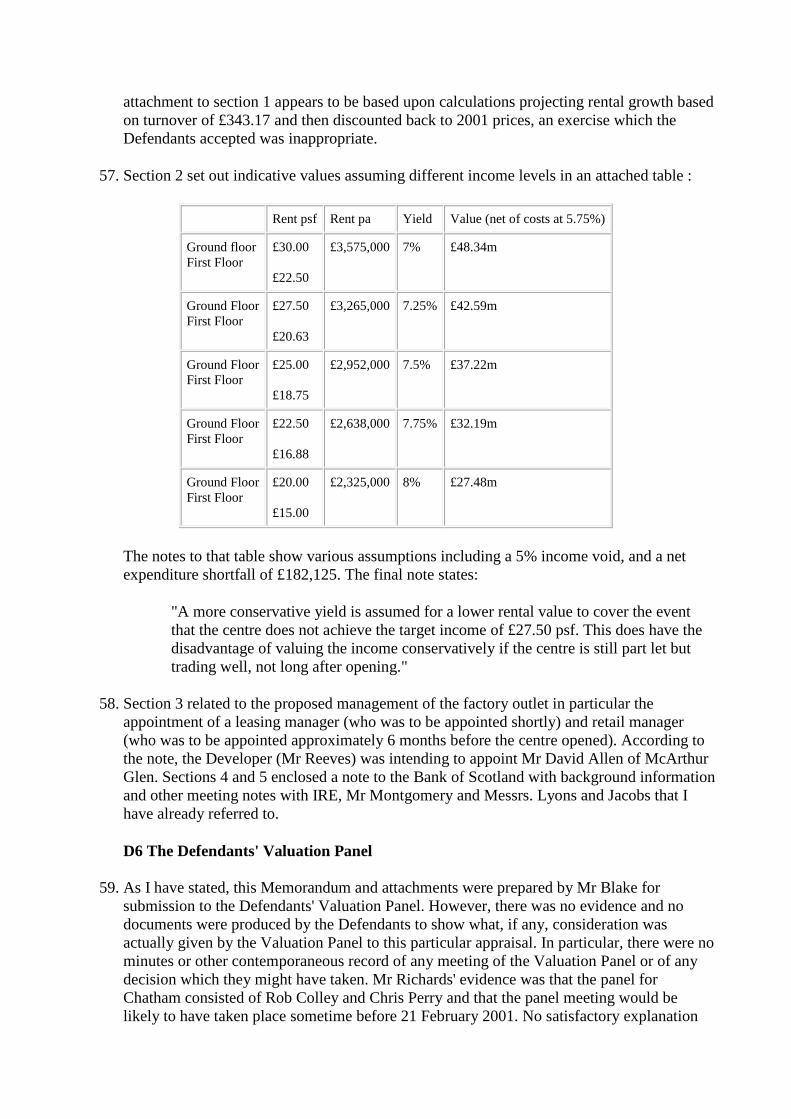

valuation advice". The Claimants contend that the Defendants' advice substantially

overstated the commercial prospects and also the value of Dockside and that, in short, the

Defendants' approach to assessing the commercial prospects and value of Dockside was

fundamentally flawed. They say that this is an "advice" case where the Defendants were

effectively advising the Claimants whether or not to proceed with the transaction. The

Claimants say that provision of advice on the attractiveness of the investment represented by

Dockside is, on the facts here, unremarkable: this is precisely the sort of advice that the

Defendants had provided to Matrix and equivalent trustees with regard to very many earlier

transactions, as well as being what they were retained to provide in respect of this particular

transaction. Further, the provision of advice on the commercial viability of a new-build FOC

is, the Claimants say, natural once it is understood that the ability of a FOC to secure and to

retain tenants and, further, the level of rent that it is able to demand from those tenants

depends on the commercial viability and success of the FOC itself. There is no "rack rent"

for a FOC: instead the rent paid is a mix of a base rent and turnover rent. As is explained

below, turnover rent is, as the name suggests, calculated as a percentage of the turnover

earned by a tenant per square foot of the unit occupied. The tenant pays the higher of base

rent and the turnover rent. Accordingly, the rent payable by the tenants and receivable by the

owner of the FOC depends on the success of the FOC and its tenants in attracting consumers

to the centre and encouraging those consumers to spend money at its stores. Thus, if a FOC

is not able to attract sufficient consumer spend through its doors then it will not attract, or

will find it more difficult to attract, tenants and the rent that those tenants will be prepared to

pay (both as base rent and as a percentage of their turnover) will be lower than at a

successful FOC. The value of the FOC is assessed on a discounted cashflow basis by

reference to an evaluation of the income (in the form of rent) that it is likely to be able to

receive.

3. An important element of the Claimants' case is that the exercise of assessing the value of a

FOC cannot begin until an assessment of that FOC's likely ability to attract consumer spend

has been undertaken. Such an assessment has been referred to in the present case as a "CACI

Report" or a "CACI-type Report", the abbreviation CACI referring to the name of a

company that specialises in the production of such an assessment. Without such a report, the

Claimants say it is impossible to predict or to assess the likely rental levels that the FOC will

be able to achieve and it is the income stream represented by the rents that then drives the

capital valuation of the FOC. The Claimants say that the Defendants' failure to appreciate

this and/or to undertake any such exercise competently lies at the heart of this case. Their

resulting failure to make a competent assessment of the likely level of turnover rents that

Dockside might achieve led them to overstating substantially the rent, value and commercial

prospects of Dockside. In addition, the Defendants made a series of failures relating to their

assessment of the attractiveness of the location and design of Dockside and as to the

competence and experience of the Developer to be able to operate Dockside successfully.

According to the Claimants, there is a ready explanation for these failings: the Defendants

did not possess the necessary expertise to advise on Dockside and this lack of expertise led

them to make fundamental errors in their approach to valuing and assessing the commercial

prospects of Dockside which ultimately led to their advice to the Claimants being woefully

inadequate.

4. The main monetary claim is that advanced by Capita viz Capita claim damages from the

Defendants in respect of these breaches of duty in relation to all of the losses they have

suffered as a result of entering into the transaction. Capita calculate these on the basis of the

difference between (a) the price paid for Dockside (£62,850,000) together with interest at

base rate plus 1% from 5 April 2001 to date and the expenses and losses incurred in

operating Dockside to date and (b) any profits earned from Dockside to date and its current

market value (pleaded at no more than £9,650,000 and in fact most recently valued at

£7,200,000). Alternatively, they claim damages on the basis of the difference between the

price paid for Dockside and its true value as at April 2001 (either including or excluding the

benefit of Enterprise Zone tax allowances). On any footing the damages claimed exceed

£16,000,000. In addition, Matrix claim an indemnity in respect of potential claims by

investors.

5. The Defendants deny liability and causation and put quantum in issue.

6. As will already be plain from this overview, this is not a simple valuation case where a

surveyor is said to have reached the wrong figure for the value of a commercial property.

Both the Claimants and the Defendants say that the case has very special features. On the

Claimants' side, it is said that the Defendants (a) introduced the transaction to Matrix with a

view to Matrix structuring it as an Enterprise Zone investment scheme; (b) purported to

conduct due diligence on the potential acquisition and, further, undertook the negotiation of

the commercial terms of the transaction with the vendor and its agent; and (c) in addition to

advising on value, provided advice to the Claimants on the commercial viability of Dockside

as a FOC and, further, advice on the merits of the commercial investment proposition

represented by the Dockside development. So, it is said by the Claimants that this is a case

where the Defendants were effectively advising Capita and Matrix as to whether or not to

proceed with the transaction at all and, if so, at what price and on what terms. On the

Defendants' side, it is said that this was, in effect, a speculative venture driven in large part

by the desire to obtain for the individual investors extremely valuable tax allowances at the

very end of the 2000-2001 tax year; that the Claimants were fully aware of the risks in

investing in such a venture which involved the acquisition and transformation of a listed

building and the set-up of what was a completely new and specialised shopping outlet with

multiple units; that although the Defendants played a certain role in providing advice, such

role was much more limited than the Claimants now say; that the venture was "conceived in

a boom but born in a bust"; and that the reasons for the failure of the investment were not

due to any actionable fault on their part.

A2 The Evidence at the Trial

7. The main events occurred in the early part of 2001 ie over 10 years ago. This gap in time

gave rise to some difficulty. Some documents which one might assume would have existed

then were not produced. Questions arose as to whether such documents had ever existed or

were no longer available. Perhaps unsurprisingly, the memory of at least some of the

witnesses was, in some important respects, hazy or non-existent.

8. I list below the witnesses who gave evidence on behalf of the Claimants. (Their witness

statements had been carefully prepared with prodigious references to the contemporary

documents. Most, if not all, had had the benefit of "witness training".)

i) Mr Robert Randall. Mr Randall is a director of Matrix Group Limited and had

conduct of the Dockside transaction at the material time on behalf of Matrix.

ii) Mr Jonathan Putsman. At the material time, Mr Putsman was Head of Property

Legal at Matrix.

iii) Mr Nigel Peters. Mr Peters was employed at the material time by Royal & Sun

Alliance Trust Company Limited ("RSA") as a Trust Administrator. RSA was

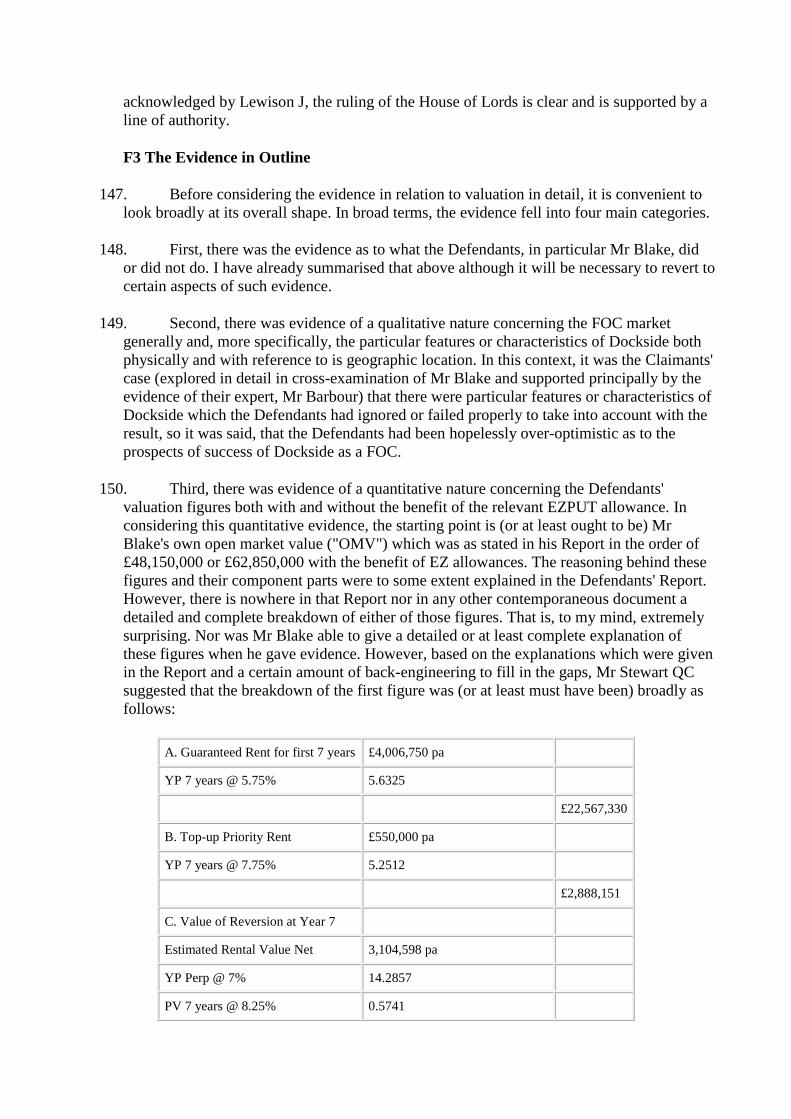

acquired by The Capita Group plc on 17 May 2001. It subsequently changed its

named to Capita Trust Company Limited.

iv) Mr Anthony O'Keeffe. He was and is employed by entities within the Capita

group of companies (formerly the Royal & SunAlliance group of companies). He is

currently the CEO of Capita Fiduciary Group Limited.

v) Mr James Kaberry. He was and is an IFA who introduced some of the investors to

the investment based on Dockside. He now represents the interests of 49 investors

who between them had around 13.73% of the Trust.

vi) Mr Colin Brooks. Mr Brooks is managing director of REALM Limited

("Realm"), a leading FOC operator. He has been in that position since Realm was

incorporated in the latter part of 2001. Mr Brooks previously worked for some 14

years with MEPC PLC ("MEPC") in London on various retail development projects.

In 1998, he was asked by MEPC to head up their in-house outlet centre management

team and, in particular, to consider co-funding the acquisition and development of

Dockside. Subsequently, MEPC decided to set up a discrete FOC management

business which became Realm.

vii) Mr Paul Nicholls. He was at the material time employed by Matrix as Senior

Asset Manager for the Matrix EZPUTS and was responsible for Dockside after

completion of its acquisition.

viii) Mr Anthony Sutton. Mr Sutton is the Centre Manager at Dockside. He has held

that position for over 6 years since October 2004.

ix) In addition, the Claimants relied on the expert evidence of Mr Ian Barbour (FOC

valuation and commercial prospects/viability), Mr Daniel Parr (retail performance

and scenario analysis) and Mr Jeremy Wessels (Guernsey law).

9. The following witnesses gave oral evidence on behalf of the Defendants

i) Mr Ian Blake. He was previously employed by the Defendants for a period of 9

years from 1992 to July 2001. He was employed by the Defendants as a Partner in

the Investments Team. He was the individual who had the conduct of the Dockside

transaction on behalf of the Defendants at the time and was primarily responsible for

providing advice and carrying out the evaluation of Dockside in 2000 and early

2001. Mr Blake left the Defendants to join Matrix shortly after the transaction

completed. He remains employed by Matrix which has, for the avoidance of doubt,

made it clear both to Mr Blake and the Defendants that he has been and is free to co-

operate with the Defendants in any way he wishes. Although he was plainly the

crucial factual witness, I should mention that the statement which he signed and

which was served prior to the commencement of the trial was extremely vague and,

in some respects, very unsatisfactory. In particular, it appears that it was prepared

hastily and, surprisingly, without him having recourse to the underlying

documentation including (it would seem) even the advice and Reports that he had

prepared. Although he had since had full access to his files, no attempt was made to

serve a supplemental statement from him or to fill in what seemed some obvious

gaps. Furthermore, when he came to give evidence, it was plain that he had some

difficulty in explaining why what had been done was satisfactory and competent.

ii) Mr Howard Richards. He qualified as a chartered surveyor in 1979 and is a fellow

of the Royal Institution of Chartered Surveyors. He has been involved in investment

transaction work since that date. He previously worked at DTZ and became an equity

partner of the Defendants in 1994. He took over the Investment Team of the

Defendants in 1998. At the time of the valuation in 2001 (and at all times since then)

he had a general supervisory role over the Investment Team. Mr Richards had

considerable experience. He was keen wherever possible to support the work that the

Defendants (including Mr Blake) had done at the time and was resistant to any

suggestion of shortcomings on the part of the Defendants. However he had little

direct involvement in relevant events and therefore his evidence was in the event of

marginal value.

iii) Mr Robert Scott. He qualified as a chartered surveyor in October 1997 and is a

member of the Royal Institution of Chartered Surveyors. He joined the Defendants

as a graduate in August 1996 starting out in the property management team. In

around June 1997 he moved to DJ Finance (a wholly owned subsidiary of the

Defendants) in which he worked closely with the Investment Team headed by Mr

Richards. From June 1997 until July 2001, he worked very closely with Mr Blake.

However, like Mr Richards, Mr Scott had little direct involvement in relevant events.

He came to the project late and was only really concerned with assessing the

location. Thus, his evidence was also of little assistance.

iv) Mr Peter Woolley. He began his career as an accountant at Coopers & Lybrand in

September 1983. From November 1996 to January 2008 he was Finance Director of

Freeport Plc ("Freeport"). In that capacity he entered serious negotiations between

1999/2000 with the vendors of Dockside for the purchase development and running

of an FOC at that site.

v) In addition, the Defendants relied on the expert evidence of Mr Alan Sargent

(FOC valuation), Mr Martin Farr (Enterprise Zone valuation) and Mr Gareth Bell

(Guernsey law). So far as relevant my comments in relation to these witnesses are set

out below.

10. As I have mentioned, Mr Brooks worked for Realm and Mr Woolley for Freeport. Both

were active in the FOC market at the material time as employees of two of the three

operators that dominated the market; and both supported the Claimants' case as to:

i) The importance of spend and a proper analysis of spend when appraising and

valuing a new FOC.

ii) The availability and use of "full" CACI retail analysis reports for that purpose.

Both obtained them before purchasing a site or FOC.

iii) The maturity of the FOC market in 2001 and the dearth of new development

opportunities.

iv) The absence of any boom in the FOC market in 2001.

v) The softening of yields for FOC properties in 2000/2001.

11. Notwithstanding the absence of development opportunities, neither Mr Brooks nor Mr

Woolley proceeded with Dockside. The former discounted it almost immediately on grounds

that mirror what the Claimants say ought to have been included in competent advice from

the Defendants. The latter pursued the deal for a period (although probably at a stage well

before the Claimants' involvement) but, in the event, withdrew on the ground of price and,

did so, at a stage prior to obtaining a full CACI report

Section B: EZ SCHEMES

B1 Introduction

12. Enterprise Zones were established by the government in 1981 in order to encourage

investment into deprived areas of the country with the aim of regenerating those areas. Each

Enterprise Zone was administered by an Enterprise Zone Authority ("EZA"). In order to

attract investment into the new Enterprise Zones, the zones were afforded a number of

advantages. In particular, developments in the zones were subject to a simplified and

accelerated planning process and expenditure on such developments received favourable tax

treatment. These tax incentives took two forms: (a) relief from development land tax (which

was abolished in any event in 1985) and, (b) the availability of 100% capital allowances for

(qualifying) capital expenditure on the construction of commercial and industrial buildings

within an Enterprise Zone. The availability of these capital allowances effectively reduced

the net cost of investing in the construction of commercial and industrial buildings in an

Enterprise Zone thus making such an investment more attractive than might otherwise be the

case. As Mr Randall of Matrix explained, the capital allowances in effect provided a

"buffer" which partly reduced or off-set the risk of investment because any losses on such an

investment would have to exceed the value of the allowances received before the investment

represented a net or overall loss. As this makes clear, the rationale for investment in an

Enterprise Zone was still, of course, the expectation of making a profit. The availability of

tax relief simply provided some comfort as regards the downside risk of making that

investment.

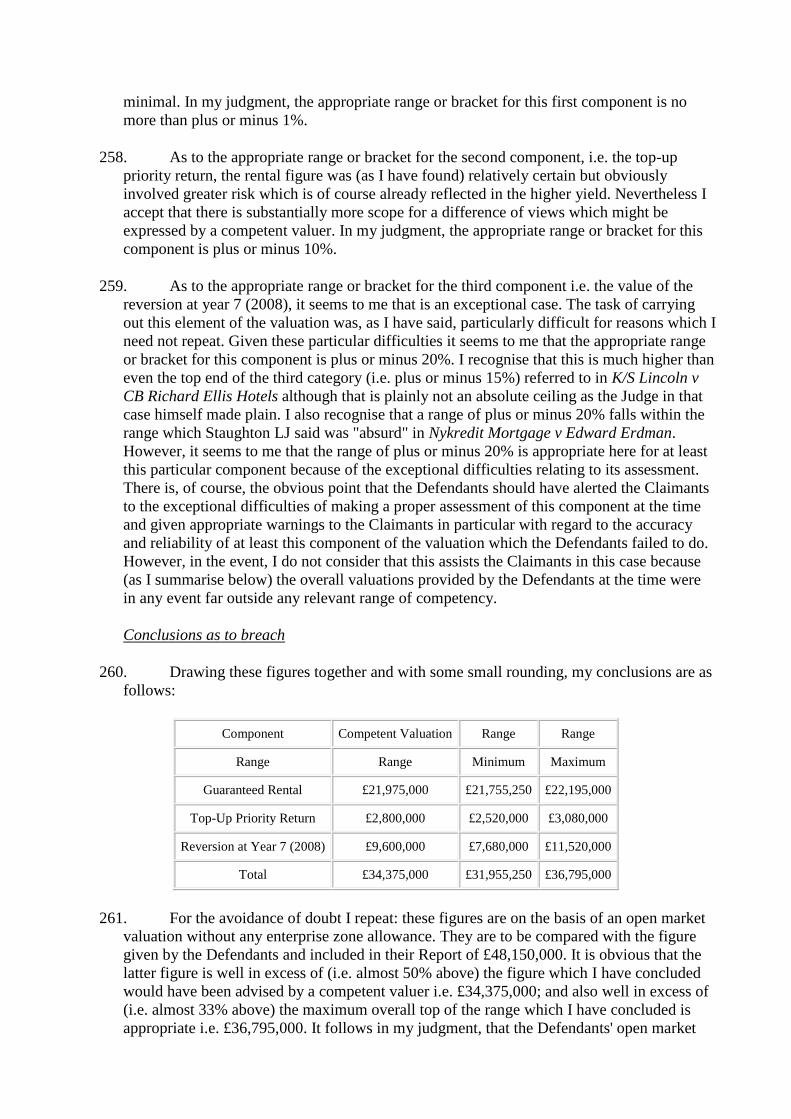

13. Generally, Enterprise Zone developments were of relatively high value, precluding the

opportunity for individuals to make their own investments in them in the absence of some

sort of investment structure employing unitisation. In this regard, one of two structures was

habitually employed: either an EZ Syndicate or an EZPUT. In general terms an EZ

Syndicate is structured as a trust for land in which each member will have an interest in the

property purchased in the Enterprise Zone; an EZPUT is a unit trust scheme in which the

trust acquires the property and each investor acquires units in the trust with each unit in turn

carrying with it an entitlement to a pro-rata share in the underlying trust property.

Whichever structure is employed, investors were required to retain their interest for at least

7 years in order to benefit from the capital allowances.

14. A further point arises in relation to timing. In general, an area was only designated as an

Enterprise Zone for a period of 10 years and capital allowances were only available during

that 10 year period. However, where a person has incurred capital expenditure on the

acquisition of an industrial or commercial building situated in an expired zone, that person is

treated as incurring capital expenditure on the construction of the building, provided (i) the

building was acquired from someone carrying on a trade which consisted, in whole or in

part, of the construction of buildings with a view to their sale and (ii) the expenditure on the

construction was incurred in the course of such a trade under a contract entered into before

the Enterprise Zone designation expired. Thus the availability of capital allowances could be

preserved even after the Enterprise Zone designation had expired if these two conditions

were met. The second condition was met if a building contract was entered into before

expiry of the Enterprise Zone designation. Such contracts became known as "Golden

Contracts". Just such a contract was entered into here in relation to Dockside.

B2 The North West Kent Enterprise Zone and Dockside

15. Dockside is located in the former North West Kent Enterprise Zone. The EZA for this zone

is the South East England Development Agency ("SEEDA"). The Enterprise Zone

designation for North West Kent expired on 9 October 1996. Nevertheless, the availability

of capital allowances in respect of expenditure on Dockside was preserved by a golden

contract. Thus, on 8 October 1996 prior to expiry of the Enterprise Zone designation,

SEEDA entered into an agreement with Chatham Maritime J3 Developments Limited ("the

Developer") for the development of Dockside. On the same day, the Developer entered into

a building contract in respect of the building works required to develop Dockside with

Chatham Maritime J3 Construction Limited ("the Contractor"). The broad effect of these

arrangements was that the Developer was obliged to develop Dockside in accordance with

the terms of the development agreement and would be entitled to a long lease (granted by

SEEDA) on completion of the development. The building contract set out the specification

and design of the FOC and, importantly, represented the golden contract which preserved

the availability of capital allowances.

16. These arrangements were put in place by SEEDA in order, in effect, to preserve the position

as it was prior to expiry of the Enterprise Zone. The Developer and the Contractor were

special purpose vehicles created by SEEDA. Until shortly before completion of the

Dockside transaction both the Developer and the Contractor were wholly owned by SEEDA.

Latterly, SEEDA agreed that the site would in fact be developed by Dockside Developments

Limited ("DDL"), a company owned and controlled by a Michael Hewitt and Steven

Reeves. As explained further below, SEEDA transferred the ownership of both the

Developer and the Contractor to DDL. Save where it is necessary to distinguish between

them, references to "the Developer" are to each of Chatham Maritime J3 Developments

Limited, DDL and Messrs Reeves and Hewitt. The structure that was in fact put in place was

as follows:

i) Capita, Matrix, the Developer and DDL entered into a Purchase and Development

Agreement dated 5 April 2001 ("the PDA") pursuant to which the price payable by

Capita to the Developer was £62,850,000.

ii) On completion of the PDA, the Developer procured that SEEDA granted Capita a

long lease with a term of 155 years of the Dockside site for a premium of £4,000,000

(which sum was paid from the total price of £62,850,000) and a peppercorn rent.

iii) At the same time, the Developer covenanted with Capita that the FOC on the

Dockside site would be constructed in accordance with the building contract. The

development was to be carried out pursuant to the building contract by the

Contractor sub-contracting the works to a building contractor, Galliford (UK)

Limited, which provided a direct warranty in respect of the building works to Capita.

Capita appointed the Defendants as its monitoring agent to monitor the progress of

the development works.

iv) Immediately following completion, Capita granted the Developer a sub-lease of

Dockside for a term of 17 years at an initial rent of £4,006,750 plus additional rent

(or priority return) of £550,000 per annum. The priority return was payable as the

first £550,000 of rent earned from the occupational tenants of Dockside after the

deduction of the Developer's allowable expenses. Any priority rent that was deferred,

attracted interest at the rate of 7.25%.

B3 The calculation of capital allowances

17. As set out above, tax relief was available on certain qualifying expenditure made within an

Enterprise Zone. Section 469 of the Income and Corporation Taxes Act 1988 ("ICTA 1988")

provides in like terms to its predecessor (being section 354A of the Income and Corporation

Taxes Act 1970) that ordinarily income arising to the trustees of a unit trust scheme will be

treated as income of the trustees and not of the unitholders for the purpose of the Tax Acts

and that, accordingly, the trustees will be regarded as the persons to or on whom allowances

and charges are to be made. EZPUTs are exempted from this provision by virtue of

regulations 3 and 4 of the Income Tax (Definition of Unit Trust Scheme) Regulations 1988

("the 1988 Regulations"). Importantly, the effect of this is that the capital allowances were

made available to individual unitholders in an EZPUT rather than being treated as available

only to the trustee of the Trust (a concept known as "transparency"). Relief is only available

in respect of expenditure that is attributable to construction within the Enterprise Zone

("Qualifying Expenditure"). Thus, in determining the relief to which an individual investor

is entitled, an assessment must be made of how much of the purchase price being paid by the

Trust (which is funded by the acquisition of units in the Trust by investors) is Qualifying

Expenditure. Any part of the price attributable to the site of the building that falls outside the

Enterprise Zone, trustee fees and any other non-allowable costs and expenses will not attract

relief ("Disallowable Expenditure"). In most cases the level of Qualifying Expenditure can

be ascertained by applying to the total purchase price the fraction:

[Diagram or picture not reproduced in HTML version - see original .rtf file to view diagram

or picture]

Where A is the replacement cost of the building and B is the bare site value.

18. As Mr Randall explained, the replacement cost of the building (A) is the estimated amount

which it would cost to replace the building in order to have it available for occupation. This

includes estimates of site works, professional fees and finance costs but not reclamation

works which would enhance the value of the bare land. The bare site value (B) is also taken

as at the date of purchase and is computed on the assumption that the site is cleared of

buildings and works, access and services are available up to the boundary and planning

permission is available for the type of development in question. The level of Qualifying

Expenditure on Enterprise Zone transactions which were sponsored by Matrix ranged from

70% to 94%. In the case of Dockside, it was originally anticipated to be 84.09%. Thus, in

practice, the fraction explained above will be applied to the total purchase price for a

property located within an Enterprise Zone so as to identify that part of the purchase price

which is Qualifying Expenditure and which will attract relief. In terms of individual

investors, the fraction is applied to the cost of their units and this will identify that part of

the cost of the units which will attract relief. Thus, if Qualifying Expenditure was assessed

at 85%, then an investor paying income tax at 40% would be likely to receive tax relief of

around £34 (i.e. 40% of £85) for every £100 invested by way of the acquisition of units.

B4 Loan finance

19. In many EZ Schemes loan finance was available to investors to finance (in part) the cost of

acquiring units. Loans provided in respect of EZ Syndicates tended to be on a non-recourse

basis in that the loan was secured against the property being purchased and investors' assets

were not otherwise at risk. In the case of EZPUTs, however, the loan finance was typically

provided on a limited or full recourse basis, in that while the lending bank would take

security in the form of a charge over the investors' units in the trust, the investors would be

responsible for repaying their loans in any event (such that if the value of the units proved to

be insufficient to discharge the debt then investors would have to fund any shortfall from

elsewhere).

20. EZPUTs are structured with the intention that periodic distributions of rental income to

investors will be sufficient to cover the interest on any loans used to finance the acquisition

of units and, further, will enable the outstanding balances on those loans to be reduced with

a view to the loans being repaid in full on exit (after the 7 year lock in period) upon a sale of

the property. Any sums over and above those necessary to repay the loans represent profits

to investors on their investments. It is here that the availability of allowances and the

"buffer" becomes relevant. Take, for example the case (not unlike Dockside) where the tax

relief available on an investment of £100 is £34 and the loan is £67. Once the arrangement

fee on the loan of 1% is taken into account, the investment is cash neutral for the investor

but the investor has a liability to repay the £67 loan (which liability may be reduced by rents

received). In effect, the investor replaces a tax liability (as to £34) with a property

investment risk. Even if the loan is not reduced over the term of the investment, investors

need the property to realise 67% of its acquisition cost in order to discharge their loans.

Thus, on the facts of Dockside, if the acquisition cost is £62.85m, and open market value

£48.15m, net proceeds of sale of approximately £42.11m were needed in order to provide

investors with sufficient to repay their loans. Provided the open market value of £48.15m

was correct, and assuming sale costs of, say, £1m, there was effectively a "buffer" of

approximately £5m before investors would suffer a loss on exit. Plainly, if the proceeds of

sale are insufficient to cover the outstanding loan liabilities then investors suffer a loss on

their investments and are left with any residual liability to the bank.

21. The Claimants say that the foregoing is important because it undermines the Defendants'

refrain to the effect that the sole or main reason for investing was the tax relief. On the

contrary, the Claimants say that the investment had to be a success in order not only for

investors to secure a return on their investment but also to avoid a loss on that investment.

B5 The effect of allowances on purchase price

22. The availability of capital allowances will often influence the purchase price that a particular

purchaser will be prepared to pay for a property within an Enterprise Zone. The effect of

those allowances will mean that, if the purchaser pays only the open market value of the

property, then, once the allowances are taken into account, the net cost of the property will

be below (and, indeed, perhaps substantially below) its true open market value. Thus, a

purchaser might well be prepared to pay more than the open market value: how much more

will depend on its view of the commercial viability of the property and the strength of the

investment represented by it. As set out above, the availability of allowances operates in

effect as a "buffer" against losses on the investment. How large a "buffer" a purchaser will

require will depend on its view of the risk of the buffer being required. In general terms, the

more confident the purchaser is in the investment proposition represented by the property,

the more it will be prepared to pay with the result that the net cost of the property once the

allowances have been taken into account becomes closer to its open market value. By

contrast, if the purchaser is less enthusiastic about the prospects of the property then it will

demand a larger "buffer" such that the gross purchase price it is prepared to pay will be

closer to the open market value and the net cost (after allowances) will represent a greater

discount to the open market value.

23. The vendor will, of course, have its own view about the attractiveness of the commercial

proposition that it is seeking to sell and will set its pricing demands accordingly. The

stronger the investment proposition, the more able the vendor is to demand a purchase price

which, after taking account of the allowances, produces a net cost that is closer to the open

market value of the property.

24. To take an example, if the investment proposition is viewed with confidence and the open

market value of the property is £80, then the purchase price might be agreed at £100 on the

basis the capital allowances will be available on 85% of the £100 (giving total relief of £34).

This produces a net cost to the purchaser of £66 i.e. £14 less than the open market value. In

this example, the available allowances of £34 are effectively "shared" between the purchaser

(which receives £14 of benefit because it pays £14 less than the open market value for the

property) and the vendor (which receives the remaining £20 of the allowances because it

receives £20 more than the open market value of the property). By contrast, if the

investment proposition is viewed as being more speculative, then using the same

assumptions in the foregoing example as to open market value and qualifying expenditure,

the purchaser might only be prepared to pay £90, producing a net cost of £59.40 (total relief

being 85% x £90 x 40% = £30.60). At this net cost, the purchaser is purchasing at a discount

of £20.60 to the open market value while the vendor is receiving only £10 more than the

open market value of the property. In this example, the purchaser receives the greater share

of the benefit of the allowances and secures a larger "buffer" in the form of a greater

discount to the open market value of the property.

25. For these reasons, and as Mr Randall explained, in structuring an investment into an

Enterprise Zone, three figures are considered in conjunction with their associated yields:

i) the open market value of the property without the benefit of capital allowances;

ii) the gross value of the property with the benefit of capital allowances and

purchaser's costs: effectively the purchase price; and

iii) the post-tax value of the property, being the net cost once capital allowances have

been taken into account.

26. What this reveals is that there is no particular magic introduced by the EZ structuring of a

purchase of property: as with any other purchase of retail property, the value of the property

is determined by its open market value and its commercial prospects, and it is the open

market value and the view taken on the commercial prospects that then drives the particular

considerations or facets of the structuring that arise from the EZ nature of the transaction.

Section C: FOCs

C1 Introduction

27. In summary, a FOC is a shopping centre where the goods offered are sold at discounts to

their original price of between 30% and 70%. The name "factory outlets" reflects their

historical origins in sites adjacent to factories (one of the first schemes being next to the

C&J Clark shoe factory in Street) and does not now accurately reflect their location or the

buildings in which they are housed. By 2001 the FOC concept had developed such that

FOCs tended to be purpose-built centres or "villages" with a wide-range of tenants,

including some of the most well-known brand names from the high street selling discounted

goods. In effect, there were two groups of tenants: high street retailers selling their own

goods at a discount and specialist FOC tenants selling discounted goods. While the range of

goods offered in FOCs is relatively wide, ordinarily planning conditions restrict the range to

less than that offered on traditional high streets so as to offer a degree of protection to the

latter.

28. By 2001 there were 36 FOCs trading in the United Kingdom with several more under

development and a number at the proposal stage. The market was dominated by three large

operators namely McArthurGlen Group ("McArthurGlen"), MEPC Limited (which later

became known as Realm) and Freeport. As I have already mentioned, Mr Woolley was the

finance Director of Freeport from 1996 – 2008.

C2 Lease structure

29. A novel, and, in this case, particularly important feature, of FOCs is the lease structure that

they employ. Traditional high street shops and shopping centres generally employ a "rack"

rent lease structure where a rent is agreed between the parties (usually with reference to

comparable shops or centres) and paid quarterly in advance with five yearly rent reviews.

By contrast, FOCs usually employ a turnover lease structure such that rent comprises two

elements viz (i) base rent; and (ii) turnover rent which is calculated as a percentage of the

turnover which the tenant earns at its unit. The rent actually paid will be the higher of the

base rent and the turnover rent. The turnover rent is thus sometimes referred to as "top up"

rent because it "tops up" the base rent. Ordinarily, base rent will be paid in advance and

turnover rent in arrears. As a general rule, lease terms at FOCs will be shorter than on the

high street or at other shopping centres and will usually be for 5 years. In addition to rent,

tenants will be required to pay a service charge and a contribution to marketing and

promotional costs (which is usually calculated as a rate per square foot subject to any other

caps or terms agreed). Self-evidently, as a result of this lease structure the rent earned by the

owner of the FOC will depend on the financial performance and success of its tenants and,

in particular, the success both of the FOC and its tenants in attracting consumers to the FOC

and persuading them to spend money there.

Section D: THE RELEVANT FACTS

D1 The Defendants' relationship with Matrix

30. Prior to the Dockside transaction, Matrix had sponsored investments into at least 15 other

EZPUTs and 25 EZ Syndicates. The Defendants were retained in at least 27 of these

transactions as property adviser. Matrix and the Defendants had developed a close working

relationship over the course of these transactions. In particular, a good relationship had

developed between the team at Matrix, led by Mr Randall, and the Defendants, in particular

Mr Blake. The relationship dated back to at least 1995 when Matrix instructed the

Defendants to act as property advisers to an earlier EZ Property Trust in Sunderland. The

Claimants rely in particular on a letter dated 16 February 1995 sent by Matrix to the

Defendants (i.e. Mr Blake) setting out the scope of the Defendants' role in relation to that

Trust (ie to advise both Matrix and the Trustee of that Trust "on all property related

matters") and stating that the Defendants' work would include (amongst other things)

"acquisition advice", "letting report" and a "valuation report". The Defendants countersigned

that letter indicating their agreement. The Claimants rely on this letter to indicate generally

what the Defendants' role was including with regard to Dockside.

31. Save for their signed acceptance of the engagement letter on the first transaction in 1995 for

the Matrix Sunderland Trust it would appear that the Defendants did not record their

instructions in writing (other than in their reports) in respect of any of the earlier

transactions or in respect of the Dockside transaction itself. The advice provided by the

Defendants in respect of these earlier transactions took a similar form. The Claimants say

this is relevant when it comes to considering the terms of the Defendants' retainer and the

duties they owed in respect of the Dockside transaction. The existing close relationship

between the parties, founded, as it was, on repeat instructions to provide similar advice in

respect of Enterprise Zone property transactions, informed the negotiation and agreement of

the retainer in relation to Dockside. In short, both parties knew what was expected of the

Defendants and so the negotiation of the terms of the retainer could and did take place

informally over a series of conversations between Mr Randall and Mr Blake. In addition to

providing advice in relation to the transactions, the Defendants were also often responsible

for introducing the transactions to Matrix. In every case, the Claimants say that the

Defendants were not simply retained to provide a valuation of the subject property but to

provide their "views and recommendations on the terms of the purchase".

D2 Negotiations in relation to Dockside

32. Chatham is located in North Kent, part of Kent's largest urban area, the Medway Towns.

Chatham is located approximately 35 miles to the south west of London and 10 miles to the

north of Maidstone. The development was situated within the area of the Chatham Maritime

Regeneration project which comprised a total of 350 acres in and around the former Royal

Naval Dockyards to the north of Chatham town centre and on the west bank of the River

Medway. The Developer was Chatham Maritime J3 Developments Ltd. The site comprised

approximately 5.25 acres including the structure known as the Boiler Shop. The proposed

development involved the construction of a factory outlet centre in and around the listed

structure including a number of extensions which would, on completion, provide a total net

lettable internal floor area of approximately 145,700 square foot with a minimum of 800 car

parking spaces and the potential to increase to 1500.

33. Although Matrix had been generally aware of the proposed development of Dockside, it was

introduced formally to Matrix as a potential investment opportunity by Mr Blake in the latter

part of 2000. It would appear that Mr Blake had himself been approached by the Developer's

agent, Michael Brodtman of Insignia Richard Ellis ("IRE") specifically with a view to Mr

Blake then presenting the project to Matrix with the aim that Matrix would then agree to put

in place an EZ structure for the development. (IRE subsequently became CBRE but will be

referred to as IRE for convenience.) Mr Brodtman and IRE were effectively seeking to sell

the development to Mr Blake and his clients.

34. Mr Blake presented the potential investment to Mr Randall at a meeting held in or around

September 2000 and it was agreed that Mr Blake and the Defendants would carry out further

discussions with the Developer and IRE through which the potential of Dockside would be

explored. Pursuant to this agreement, the Defendants then explored both the investment and

its structure with the Developer and IRE. The contemporaneous documents clearly show

that the Defendants were heavily engaged in negotiating the proposed terms of the

transaction with the Developer and IRE. The pattern was one of the Defendants formulating

proposals, reporting back to Matrix on these and on the progress being made with the

Developer and of the Defendants undertaking the negotiation of terms with IRE.

35. The initial negotiations with the Developer envisaged that Matrix, as sponsor, would be

entitled to a substantial fee of 7.5 %. On 5 January 2001, the Defendants wrote to the

Developer setting out the expenditure covered by Matrix's fee of 7.5 % (including fees to

independent financial intermediaries, its own sponsor's fee, site stamp duty, legal fees and

property acquisition and valuation advice) and what was described as "the response of key

financial intermediaries which Matrix have consulted." As to the latter, the Defendants

stated as follows:

"Feedback From Financial Intermediaries

The feedback we have received supports our pricing of 6%. Whilst the

factory outlet scheme presents an unusual and in many respects "real

property" investment opportunity compared to other transactions there are

risks, in particular:-

i) It is a speculative development and whilst a level of letting may be anticipated at

practical completion there is no assurance of this at the time of funding.

ii) The scheme is being compared to existing successful developments such as the

McArthur Glen and Freeport centres. However, the centre will not be managed by an

operator who has an established track record and "pulling power" from operating a

portfolio of centres to help secure tenants.

iii) The building is a listed structure which in the event that a factory outlet scheme is

not successful will have minimal residual values.

iv) A lot size in the order of £66.8m is very large for a transaction funded with full

recourse facilities.

Having regard to the feedback received from the market we believe the

pricing structure is appropriate. It provides your client with a lower initial

yield than anticipated for speculative developments but the unique

characteristics of the development and opportunity for enhanced returns

compensate for this. On balance, we are confident that the development can

be funded but recognise it will not be an easy job and require considerable

placing power."

A copy of this letter was provided to Mr Randall.

36. Following further negotiations, the Defendants prepared draft heads of terms and submitted

these to Matrix for its approval on 16 January 2001. The Defendants sent draft heads of

terms to IRE later the same day. In summary these proposed:

i) The purchase would be by a property Enterprise Zone unit trust sponsored by

Matrix.

ii) The proposed development would be of a FOC comprising not less than 145,000

net internal square feet with 100,000 on the ground floor and 45,000 on the first

floor. The Developer would enter into an agreement with the trust to construct the

development.

iii) The trust would acquire a long leasehold interest from SEEDA.

iv) The gross purchase price would be £66,800,000 less fees paid to Matrix resulting

in a net price to the Developer of £61,790,000.

v) On completion, the trust would leaseback the entire development on a full

repairing lease to another company, Dockside Factory Outlet Ltd, for a term of 15

years subject to a mutual break option on the 7th

anniversary.

vi) The trust would receive rent of £4,006,750 per annum for a term of 7 years, the

payment of which was to be secured by cash deposited by the Developer in an

interest bearing account. In addition, the Developer would also pay a rent equal to

the first £700,000 pa received from occupation leases.

vii) Matrix was to be granted an exclusivity period in which it could market the

investment.

37. Negotiations continued on the draft heads of terms throughout the remainder of January.

These were conducted by the Defendants with the pattern again being one of the Defendants

conducting the negotiations and reporting back to Matrix. It was inherent in the Defendants'

role in negotiating the terms of the transaction that they were, at the same time, advising

Matrix on those terms generally as regards the commercial prospects and attractiveness of

the transaction and, specifically, as regards the purchase price/value. This advice included

considering the capital allowances that might be available in respect of the transaction and,

in this regard, the Defendants liaised directly with SJ Berwin.

38. Given that the proposed structure of the transaction as an EZ Scheme envisaged the use of

loan finance, Matrix took steps at an early stage to ascertain whether the Bank of Scotland

("the Bank") would be prepared in principle to offer the necessary funding. It was always

envisaged that the Bank would need valuation advice before agreeing to lend.

D3 The Defendants' Research

39. During this period, the Defendants carried out research with regard to turnover levels at

other factory outlet centres with a view to assessing the likely rental income at Dockside.

According to Mr Blake's written statement, Dockside was unusual and difficult to value. As

set out in that statement, this was because Dockside was the only FOC in an Enterprise

Zone; in terms of comparables, this was a "very young market"; there were some established

FOC's at that time but many of them were still under construction; and it was not clear what

the saturation point of the market would be. Further, according to Mr Blake's statement, it

was not possible to get detailed letting terms in relation to other factory outlet centres

because of the commercial sensitivity of the information. There was, according to Mr Blake,

a further complication viz (and I quote from Mr Blake's statement):

"18 ….no single person had both the essential skills for doing this valuation, i.e. no-

one had experience in valuing both FOCs and developments in Enterprise Zones.

Had there being such a person, Drivers Jonas may, albeit reluctantly, have agreed to

pass over the task to them, or more likely we would have to subcontract that person

to help us in producing the valuation. However, there was no such person.

19. In essence, the valuation of this centre hinged on the viability of this

development as compared to other FOCs. Drivers Jonas did not have anyone with

specific retail background in FOCs but we recognised this and obtain reports from

CBRE [i.e. IRE], who did have relevant retail experience. In any event, I struggle to

think of anyone else who could have provided a valuation in the circumstances. The

most relevant comparable information regarding rents being achieved at other FOCs

was very sensitive and full details such as rent free periods and tenant incentives

were very difficult to obtain and not available for the major FOC developments of

McArthur Glen and Freeport."

40. However, the Defendants did carry out certain research which can be summarised as

follows.

Discussions with Mr Montgomery

41. First, on about 19 January 2001 Mr Blake spoke on the telephone to a Mr Simon

Montgomery who was a letting agent at Rapleys. Mr Montgomery had previously been with

DTZ where he had been letting agent for MEPC and also the Whiteley Development. The

Defendants' file note of that conversation records that Mr Montgomery told Mr Blake

(amongst other things):

a. Turnover averages for Division 1 FOCs (Clarks, Bicester and Cheshire Oaks) were

between £300-£450 per square foot.

b. Turnover averages for Division 2 FOCs (Swindon, Bridgend, Ashford, Braintree,

Freeport, Gunwharf (anticipated) and Whiteleys (expected)) were between £250 -

£300 per square foot.

c. Turnover averages for Division 3 FOCs (Clacton, Ebbw Vale, Stoke Freeport and

Yorkshire Outlet) were under £250 per square foot.

d. Cash incentives are generally required or rent free periods.

e. To induce an international name such as The Gap, Polo and Nike to take units of

approximately 10,000 square foot a budget figure would be £1 million.

f. UK tenants taking typically 1,000-2,000 square foot units are today commanding

incentives in the order of £80,000, a year ago £140,000-£150,000.

g. Marketing was generally in the order of £250,000 - £300,000 per annum.

Maximum recovery from tenants is generally in the order of £1.50 per square foot.

This usually creates a shortfall.

h. It is a "fickle market".

42. Shortly thereafter, Mr Blake had a meeting with Mr Montgomery. The Defendants' file note

of that meeting records (amongst other things):

i) Mr Montgomery agreed that the catchment demographics for Dockside were

attractive and that a target rent of £27.50 per square foot (base rent and turnover) was

realistic.

ii) Mr Montgomery was of the view that the market had become more competitive

and that turnover percentages which were traditionally 12% had been reduced to

10%. Big traders often have turnovers of only 5%-6% and Nike have no turnover.

iii) Mr Montgomery stated traders liked to deal with managers who knew their

business.

iv) Mr Montgomery warned about the potential problems of trading on more than

one floor.

Investigations by Mr Perry

43. Second, Mr Perry contacted the letting agents for a number of FOCs to obtain information.

Mr Perry was at the time about 22 years old and employed by the Defendants as a graduate

trainee; but he did not have any professional qualifications. Mr Perry did not give evidence.

However, Mr Perry's note of these calls indicates (amongst other things) conversations with

letting agents of the following FOCs and the advice received.

i) McArthur Glen Centres (Ashford, Bridgend, Cheshire Oaks, Derby, Swindon,

York): quoting terms are the greater of a base rent of £30 psf or 13% of turnover.

ii) Freeport Leisure Centres (Braintree, Castleford, Fleetwood, Hornsea, Talke and

West Calder): quoting terms are the greater of £25 psf or 15% of turnover.

iii) Mr Sargent at Colliers CRE who was involved in the valuation of FOCs

including the Freeport portfolio. His remarks included that base rents range between

£15-£25 psf and that turnover rents can range between 7.5% - 15% of turnover. He

also stated: "The market has become increasingly competitive with the UK nearing

saturation point… diversification such as the incorporation of leisure centres has

been found to benefit factory outlets….." [I should mention that Mr Sargent was the

expert instructed to give evidence on behalf of the Defendants in the present case. I

refer to that evidence below.]

iv) MEPC FOCs (including Bideford Street, Kendal, Loch Lomond, Royal Quays

and Doncaster). The quoting terms are the greater of £20 psf base rent or 12% of

turnover – 13.5% inclusive of service charges etc with the exception of Street where

the base rent is £30 psf.

v) Guinea Group and Rocheagle FOCs (Clacton, Jacksons Landing, Hartlepool,

Festival Park, Ebbw Vale and a number of smaller schemes including Wilton

Village). The quoting terms are the greater of £20 psf base rent or 10% of turnover.

vi) Bicester FOC: The quoting terms are the greater of £40 – 45 base rent or 12.5%

of turnover.

vii) Brighton Marina: quoting rent of £20 psf or 10% of turnover.

viii) Hatfield Galleria: quoting rent of £25 psf base rent or 10-12% turnover (Mr

Perry noted that this was an unusual scheme as it included leisure uses and some full

price retail).

ix) Ramsgate Boulevard: This was in course of construction with completion

anticipated by Easter 2002. Quoting terms were the greater of £15-16 psf base rent or

10% of turnover with 3 months rent free.

x) Whiteley Village Southampton: This FOC was newly opened in November 1999

with 85% occupancy in 2001. According to Mr Perry's note, the centre was "yet to

fully establish". Quoting rents are the greater of £15 psf base rent or 8-12% of

turnover.

44. On the basis of this information, Mr Perry produced various tables comparing the data

broken down into three main sections viz premier centres (turnover £300 psf plus),

successful centres (turnover £250-£300 psf) and secondary centres (turnover under £250

psf).

Discussions with IRE

45. Third, the Defendants sought information from IRE. In particular, on 23 January, Mr Blake

had a meeting with Mr Brodtman and Ms Louise Songeur who was an Associate Director of

the City Centre Retail Team at IRE. According to the Defendants' note of that meeting, there

was a general discussion of rental levels at various FOCs including at Ashford (where

Aroma took a lease at a base rent of £30 psf) and Gunwharf which was due to open for

trading in spring. Mr Blake was told that the minimum base rent there was £15 psf with a

maximum inducement of no more than 6 months rent although by that time the anchor

tenants had already been secured and the terms of their incentives were not clear. Following

that meeting, IRE sent to the Defendants under cover of a letter dated 25 January 2001, a

copy of report dated 23 November 2000 which they (i.e. IRE) had previously obtained from

a company called Illumine. This contained certain demographic and consumer expenditure

data potentially relevant to Dockside. In addition, it appears that at the meeting on 23

January, Mr Blake must have asked Ms Songeur to provide written comments of IRE's view

of the letting prospects of Dockside. These were set out in IRE's letter to Mr Blake dated 31

January. In that letter she commented on what she described as various "particular

attractions" of Dockside including:

i) Location ("…..readily accessible from A2/M2. Its catchment includes large areas

of dense urban population and the 60 minute drive time area includes much of south

and south east London as well as most of the urban areas of Kent").

ii) Immediate environment ("The Boiler Shop is adjacent to attractive areas of

nature, including an active marina and adjacent to interesting historic attractions and

a significant potential leisure development. It will be served by a large car park and

linked to town centres and the railway station by a regular bus service").

iii) Competition ("Braintree and Ashford have both been extremely

successful…These developments have both attracted a significant number of tenants

and the strength of demand from retailers suggests substantial unsatisfied demand

that would be available for Chatham").

As to the proposed average rent of £27.50 psf leading to a total rent of just over £4

million pa, Ms Songeur's letter stated: "….subject to analysis of the detailed

configurations of the development we would expect this to be achievable."

Reference was also made to (lower) rentals achieved at other FOCs and the potential

necessity to pay capital contributions and "key money". The letter concluded:

"We believe that the Boiler Shop is well suited to its future use as a factory

outlet centre and that there is strong retail demand for such proposals. The

size, configuration and location of the development would appear to have

been well considered and we would expect the scheme to be highly attractive

to retailers in current market considerations."

Discussions with Messrs Lyons and Jacobs

46. Fourth, on 25 January 2001 Mr Blake (together with Mr Randall and representatives from

Dockside) met representatives (Mr Lyons and Mr Jacobs) of a company called Bed & Bath

Works who were traders at a number of other FOCs and were, they said, interested in

investing in Dockside. According to the Defendants' note of that meeting, they also offered

assistance in particular with regard to marketing and teaming up with people that they said

they knew, some of whom would take space others of whom could operate the centre. In

particular, they indicated that of their immediate trading contacts, they would be able to

secure lettings of at least 20,000 square feet; they also said they had contacts with other

traders that they knew well that would expand this further.

47. Mr Lyons and Mr Jacobs also told Mr Blake that they would take space in Dockside for Bed

& Bath Works. Their unit requirement was from 3-5000 square feet. They said that they

would prefer a base rent of £15 psf rather than £25. This was followed by a general

discussion with regard to rents. Mr Blake explained that the Defendants' exit rent

assumption was £27.50 psf on ground floor and 75% of this at first floor level. Mr Jacobs

said that they were "comfortable with this assumption". Furthermore, he was more relaxed

about trading rates at the first floor when he recognised there was a reasonable level of space

which would create its own and attractive trading environment and could accommodate, for

example, the food court which would draw people to this level. According to the note, both

Mr Lyons and Mr Jacobs were "very enthusiastic about the building"; they thought that the

structure was interesting and a good advantage for a shopping environment; they were very

interested in the historic dockyard and the alternative activity and leisure destination that

Chatham provided alongside the factory outlet scheme; and both thought that the location

was good now that road infrastructure was in place. Mr Jacobs' parting comment was

apparently "that it was a better location than Ashford".

Information from the internet

48. Fifth, in addition to the above, it appears that the Defendants probably also had available or

obtained information from other sources including the internet both as regards demographics

in the vicinity of Chatham and the state generally of the FOC market. This included one

report from the internet "The Factory Outlet Phenomenon" dated 28 June 2000 and

apparently downloaded on 2/2/2001 which contained data from the UK showing both total

number of FOCs and total floor space over the period 1992 – 2000, other data from the USA

and commentary generally with regard to the FOC market. The recap in that report stated:

"Increasing competition between existing and planned sites in the UK in maturing market

close to saturation". A similar internet report from "Retail Week" apparently downloaded by

the Defendants from the internet in October 2000 had a headline: "Factory outlets worth £1

billion as sector nears saturation" and, in the body of the report, similarly stated: "Retail

Intelligence forecasts that the UK market will shortly reach saturation and the focus of

development will shift to mainland Europe".

Investigations as to the status and experience of the Developer

49. I should also mention that about this time, the Defendants made certain investigations as to

the status and experience of the Developer including the owner of the company, Steven

Reeves. They appear to show (amongst other things) that Mr. Reeves had developed a

detailed understanding of the factory outlet shopping centre and its role as a destination and

had been involved in the development of 7 projects around the UK.

D4 The Bank of Scotland

50. During this period, the Defendants and Matrix were both in contact with the Bank. In

particular, the Defendants' views as to Dockside's value and prospects were set out in a

document sent by Mr Blake to the Bank on 26 January 2001. The document is divided into

four sections: Location Summary, Demand Considerations, Income Commentary and

Appraisal Commentary. It assumes rental levels after 7 years to be approximately

£3,630,000 capitalised at an initial yield of 7%. It considers this to be "conservative" and to

be based on a number of assumptions including rent across the ground floor of £27.50 psf

and on the first floor of 75% of that and an exit value net of purchase costs at approximately

£49,000,000 or £336 psf. A range of rental values was included from £22.50 psf overall to

£35.00 overall psf.

D5 Mr Blake's Memorandum dated 31 January 2001

51. On 31 January 2001, Mr Blake produced a Memorandum and a set of documents containing

what were described as the Defendants' "draft appraisals and supporting information". These

documents were prepared for submission to and approval by the Defendants' Valuation

Panel.

52. The Defendants' panel process was described by Mr Richards in his witness statement as

follows:-

"DJ (i.e. the Defendants) has a robust panel process in respect of all valuations. Each

panel consists of two people, usually a Partner and an Associate, but sometimes two

partners. The job of the panel is to review the valuation and decide whether it is

realistic and reasonable. In general terms, the surveyors who undertake the valuation

would provide to the panel their valuation figures and perhaps a draft valuation

report. A meeting between the panel and the valuers is then held where the valuation

is discussed and challenged as necessary. The meetings would generally last around

half an hour.

What was ordinarily produced as a result of the panel meeting was a single sheet of

paper, including the name of the producer, the term, the valuation and the members

of the panel.

In terms of the importance of the panelling process, it is rare that the panelling

process would lead to an alteration in the valuation. Indeed, I cannot recall an

instance of an individual transaction such as Chatham where the valuation changed

as a result of the panelling process, although it may have happened where you were

dealing with a large portfolio of a variety of different properties. DJ had well trained

staff carrying out precise valuation procedures and it should not be seen as surprising

that the panel process did not lead to alterations of valuations."

53. The Memorandum dated 31 January 2001 was addressed to Chris Matthew and Rob Colley.

It comprised five sections.

54. Section 1 was "Appraisals for Valuations". The Memorandum stated: "We will be required

to produce a valuation report addressed to the investors and bank". A brief explanation was

given as to the structure of the proposed deal. The Memorandum stated:

"A valuation is required with the benefit of enterprise zone allowances and without

the benefit of enterprise zone allowances. The purchase price and therefore valuation

with the benefit of enterprise zone allowances is £66.8m inclusive of purchase costs.

Our indicative value of the development without the benefit of enterprise zone

allowances that has been reported to the bank and Matrix is £50m."

55. The attachment to section 1 contained a brief description of Dockside and a summary of the

purpose of the appraisal status, assumptions, limitations and restrictions including the

following:

"THE BOILER SHOP, CHATHAM MARITIME

Description:

The property comprises a Grade II* listed building dating from 1850s. The property

has outline planning consent for the refurbishment of the building as a factory outlet

centre comprising approximately 145,700 sq.ft NIA retail. The retail would be on

two floors with approximately 100,000sq.ft on the ground floor. Approximately 800

car parking spaces would be provided initially, increasing to 1,500 in due course.

The property occupies a very prominent position at a major junction to the south of

the Medway Tunnel. Associated development is uncertain but may take the form of a

cinema etc.

Purpose of Appraisal:

Indicative appraisal for potential acquisition by a client of DJ.

Status:

Draft – indicative only and subject to a number of assumptions set out below. Our

appraisals are very sensitive to changes in inputs as illustrated in our sensitivity

analysis.

Assumptions:

The only information provided has been in the form of investment particulars

prepared by Insignia Richard Ellis – no floor plans have been provided. Property has

not been inspected. We have assumed that the property is complete and available for

occupation. We have therefore assumed that all necessary (planning, listed building

regulations etc) have been obtained.

No investigations have been undertaken to verify the proposed developments on

adjoining sites. This will be important when looking at the sustainability of the

location.

Brief information has been provided by IRE on other factory outlet centres to

substantiate some of the values they have noted in their particulars. This information

has been taken at face value, and IRE will provide further and more detailed

information in due course if the purchase goes ahead. Our appraisal and sensitivity

analysis is for the completed centre and our appraisals take no account of any

development costs, either on or off-site.

Limitations and Restrictions:

This appraisal has been prepared based on limited information and is subject to a

number of special assumptions. "

56. In addition, there was included in the attachment to section 1, a table showing various

calculations which indicated an appraisal figure on exit of £50 million. This figure was

based on a gross income of £3,628,625, a yield of 7% less costs of 5.75%. This calculation

and the figure of £50 million seems to me likely to have been the basis of the £50 million

indicative value referred to in section 1 of the body of the Memorandum. However, when

Mr Blake gave evidence he had no recollection of this and the Defendants' position was that

this was not, or not necessarily, the case. I was somewhat baffled by this because it seems to

me that the documents are quite clear. The explanation may be that the table in the

attachment to section 1 appears to be based upon calculations projecting rental growth based

on turnover of £343.17 and then discounted back to 2001 prices, an exercise which the

Defendants accepted was inappropriate.

57. Section 2 set out indicative values assuming different income levels in an attached table :

Rent psf Rent pa Yield Value (net of costs at 5.75%)

Ground floor

First Floor £30.00

£22.50

£3,575,000 7% £48.34m

Ground Floor

First Floor £27.50

£20.63

£3,265,000 7.25% £42.59m

Ground Floor

First Floor £25.00

£18.75

£2,952,000 7.5% £37.22m

Ground Floor

First Floor £22.50

£16.88

£2,638,000 7.75% £32.19m

Ground Floor

First Floor £20.00

£15.00

£2,325,000 8% £27.48m

The notes to that table show various assumptions including a 5% income void, and a net

expenditure shortfall of £182,125. The final note states:

"A more conservative yield is assumed for a lower rental value to cover the event

that the centre does not achieve the target income of £27.50 psf. This does have the

disadvantage of valuing the income conservatively if the centre is still part let but

trading well, not long after opening."

58. Section 3 related to the proposed management of the factory outlet in particular the

appointment of a leasing manager (who was to be appointed shortly) and retail manager

(who was to be appointed approximately 6 months before the centre opened). According to

the note, the Developer (Mr Reeves) was intending to appoint Mr David Allen of McArthur

Glen. Sections 4 and 5 enclosed a note to the Bank of Scotland with background information

and other meeting notes with IRE, Mr Montgomery and Messrs. Lyons and Jacobs that I

have already referred to.

D6 The Defendants' Valuation Panel

59. As I have stated, this Memorandum and attachments were prepared by Mr Blake for

submission to the Defendants' Valuation Panel. However, there was no evidence and no

documents were produced by the Defendants to show what, if any, consideration was

actually given by the Valuation Panel to this particular appraisal. In particular, there were no

minutes or other contemporaneous record of any meeting of the Valuation Panel or of any

decision which they might have taken. Mr Richards' evidence was that the panel for

Chatham consisted of Rob Colley and Chris Perry and that the panel meeting would be

likely to have taken place sometime before 21 February 2001. No satisfactory explanation

was provided by the Defendants as to the absence of any documentary record in relation to

the valuation panel process for Dockside. At a very late stage of the trial, the Defendants

produced certain guidance notes relating generally to the Defendants' panel review process.

These indicated that for capital valuations above £50 million and rental valuations above £2

million pa the panel should have consisted of a minimum of two partners in each case one

from list 1A and one from list 1B. Mr Colley was a partner on list 2A but he was not on

either of the stipulated lists. Mr Perry was not a partner and not on either list. Thus, even on

the basis of Mr Richards' own evidence, it would seem that the Defendants' own guidance

notes with regard to the valuation process were not followed.

D7 Further Negotiations

60. Initially the investment was to be in the form of an EZ Syndicate as opposed to EZPUT.

This was later revised during negotiation in February 2001. The gross value of the

investment had until that point been placed at £66.8m. This figure was negotiated down by

Mr Randall and Mr Blake at a meeting with the Developer and IRE sometime in mid-

February 2001. (I should mention that there was some uncertainty as to whether Mr Blake

was present at that meeting. This does not seem a crucial point but so far as may be relevant,

I accept the evidence of Mr Randall and Mr Putsman that Mr Blake was probably present.)

D8 The Draft Short-Form Valuation Report

61. On 21 February 2001 the Defendants wrote to Matrix enclosing what was described as "our

short form valuation certificate for the Chatham Trust without the benefit of Enterprise zone

allowances." The covering letter continued: "As noted in the valuation certificate our full

report including the basis of valuation and definition of open market value will be forwarded

in due course". The document attached to that letter carried the header "The Boiler Shop –

Chatham Maritime Draft short-form Valuation". I shall refer to this as the "Draft Short-Form

Valuation Report". It was four pages long and contained 3 main sections, viz (1)

Introduction; (2) Valuation and (3) Main Assumptions. The most important parts were as

follows:

"Instructions

1.1 Drivers Jonas has been asked to prepare a valuation of The Boiler Shop,

Chatham Maritime, on the basis of various assumptions, which are set out in this

short-form report. A full valuation report will be provided in due course when

requested.

The report has been prepared for the benefit of the Matrix Chatham Maritime Trust

(the Investor) and Bank of Scotland (the Bank). The valuation is required for loan

security and investment purposes………

Basis of Valuation

The basis of the valuation is Open Market Value (OMV), defined in the RICS

Appraisal and Valuation Manual (the "Red Book"). The definition of OMV will be

included in the final report."

Short-form report

At this stage in the investment structuring process, we have been requested only to

supply a short-form report, which summarises our opinion of value and our main

assumptions. Our final report will include full valuation, property description,

approach and methodology, valuation commentary, basis of valuation and limitation

sections. It will also contain an appendix entitled sources and verification of