1 cbeb3101 business ethics lecture 6 semester 1, 2011/2012 prepared by zulkufly ramly 10-1

TRANSCRIPT

1

CBEB3101 Business Ethics Lecture 6

Semester 1, 2011/2012Prepared by Zulkufly Ramly

10-1

Topic 6Ethics in Accounting and Financial Services

210-2

Contents of Topic 6

Accountants and auditors as gatekeepers

Fiduciary duty / responsibility

Ethical issues in accounting and auditing -conflicts of interests, creative accounting and earnings management

Ethical issues in financial markets – insider trading, deception, churning and conflict of interest

310-3

Learning Outcomes

1. Explain the role of accountants and finance professionals as “gatekeepers.”

2. Explain the concept of fiduciary responsibility and its relevance to accounting and finance professions.

3. Describe how conflicts of interests can arise for accounting and financial markets professionals

4. Explain the meanings of creative accounting techniques and earnings management.

5. Define insider trading and evaluate its potential for unethical behavior. 4

10-4

Ethics Scandals (1)

510-5

Ethics scandals (2)

Each of these companies, organisations, accounting firms and investment firms has been implicated in some ethically questionable activity, activities that have resulted in fines or criminal convictions.

Ethics in the governance and financial arenas - most visible issues in business ethics.

Issue: Accounting and investment firms were expected to be the guardians of integrity in financial dealings have violated their fiduciary responsibilities.

610-6

Enron Changes Everything

Ethics of finance and accounting first became prominent after the collapse of Enron and its accounting firm Arthur Andersen.

The Enron case has caused more havoc on the accounting industry than any other case in U.S. history, including the demise of Arthur Andersen.

Enron’s demise brought into focus the necessity of the independence of auditors and the responsibilities of accountants like never before.

7

Finance and Accounting Functions

Financial Transactions

8

Accounting

Auditing

Financial Transactions

Process by which the flow of money through an organisation is handled

E.g. receiving money from customers and using that money to pay employees, suppliers and all other creditors (taxes, etc.)

Whatever balance can be taken as profit that can either be reinvested back into the business or paid out to owners/shareholders.

9

Accounting

The process by which any business keeps track of its financial activities by recording its debits and credits and balancing its accounts."

A system of rules and principles, which govern the format and content of financial statements.

It is hoped that adherence to these principles will result in fair and accurate reporting of this information.

10

The Accounting Function

Offers a system of rules and principles that governs the format and content of financial statements.

Keeps track of all those financial transactions by documenting the money coming in (credits) and the money going out (debits) and balancing the accounts at the end of the period.

Handled by accounting professionals or outside accounting firms or usually a combination of the two.

11

Auditing

Completed financial statements must be

reported to numerous stakeholders.

Stakeholders will want to see financial

statements have been certified as accurate by

an impartial third party professional.

That certification is offered by auditors.12

Accounting Professionals as “Gatekeepers”

Ensure market players follow

rules so that market functions as

it is supposed to function. i.e.

ensure fair play

Safeguard the interest of

stakeholders

We accept responsibilities based

on our roles

Ethical obligations originate in

part from their roles as

accountants1310-13

Most Important Ethical Issue for Gatekeepers: Conflicts of Interest

A conflict of interest exists when a person holds a position of trust

involves in a situation where his personal interests and/or

obligations are incongruent with the interests of those who give him the

trust

14

Example 1

An auditor agrees to issue a “clean audit” despite raising some concerns the auditor has about the financial statements.

1510-15

Example 2

An audit partner has a business partnership with the CEO of firm he audited

1610-16

Fiduciary Responsibility (1)

• Fiduciary duty is a duty of trust and care towards one or more interested parties.

• Given in trust e.g. the

accountants and auditors occupy a position of trust

1710-17

Fiduciary Responsibility (2)

• As trustees – auditors/accountant must ensure accuracy and reliability of financial statements on behalf of shareholders.

• A trustee = a fiduciary

• A fiduciary = accountants/investment bankers cannot make a personal profit from their position.

1810-18

To whom?19

Traditional view –towards shareholders only.

Reason: Shareholders contribute funds to the company but unable to take part in running the business.

Contemporary view: towards not only shareholders but also other stakeholders.

1910-19

FD of accounting and finance professionals

20

Professionals are said to have fiduciary duties—a professional and ethical obligation—to their clients, duties that override their own personal interests

2010-20

21

In summary …

2110-21

The Ethics of Accounting Profession

A unique profession because the accountant is responsible for giving the financial pictures that are necessary for companies to stay in existence.

The auditors who are responsible for verifying that the pictures are accurate and truthful. i.e. give assurance

The difficulties facing accountants in being objective and independent were not unknown before the Enron debacle, though.

22

Ethical Issues in Accounting and Auditing

23

Conflicts of interest

Creative bookkeeping techniques

Conflicts of Interest in Accounting

Expected to exercise highest degree of integrity and trustworthiness.

There is no real, tangible product to sell, nor is there the ability to "try before you buy."

Therefore, treating clients fairly and building a reputation for fair dealing may be a finance professional's greatest asset.

Conflicts – real or perceived - can erode trust, and often exist as a result of varying interests of stakeholders.

24

Example: Dual roles

Arthur Andersen – entrusted to produce an objective audit

But, its Consulting Division also handled multiple million-dollar projects for Enron

‘Conflict of interest’ = any questioning of Enron’s accounting practices by Auditing Division would automatically place consulting revenue in danger.

Auditors were unable to be objective in their audit when their colleagues in the Consulting Division were encouraging them to ‘keep the client happy’

25

Playing dual roles led to compromise thoroughness and quality of audit To protect lucrative

consulting revenues from Enron auditors avoid making bad comments on financials

Auditors reluctant to self-criticise

Now, Sarbanes-Oxley Act 2002 – Prohibits dual roles 26

Example: More on dual roles

10-26

Enron’s employees shared offices for long periods and socialised together.

Also, AA engaged in regular exchanges of employees with Enron.

Evidence of violation of auditing standards regarding personal relationships with client.

Example: Other conflicts of interest

27

Creative bookkeeping techniques

Creative accounting

28

Financial reports that push the limits of accounting standards

Most common reason: to overstate corporate earnings

Use ambiguities in accounting rules to

produce results that serve some

particular interest

Earnings management

Use of accounting rules and financial

manipulations to meet goals or to make their

earnings smooth

10-28

Example: Earnings management

29

Deferring income and/or expenses to manipulate tax liability

Recognizing future income as present income to boost revenue numbers;

Hiding debt in off-balance sheet transactions – all of which Enron did

Issuing fake invoices for services/sales that never took place – Transmile did this

10-29

Example

Creative accountingCookie Jar Accounting

Former accountant in Enron admitted in court that he reduced reserves by $14 million and added it to income in 2000.

Results: EPS was higher by 2 cents than what analysts predicted

3010-30

Culture and Accounting Ethics

Profit-at-any cost culture

Focus on increasing shareholders’ value – higher PE ratios

Higher profit = higher executive bonus / increment

31

How to achieve profit?Pushed to smoothen the earnings – manipulate

financials

The board of directors together with

accountant professionals need to set the ‘tone-

at-the-top’ to avoid the culture of financial

manipulation10-31

Meaning of ‘tone-at-the-top’

The top management and accounting professionals talk about ethics, behaving ethically and encouraging employees to do the same

So, conduct of the accountants / top executives must be exemplary

AND

Must comply with the company’s standards, rules and regulations

3210-32

Ethics in the Financial Markets (1)

Focus on financial markets – stock exchanges, commercial banks, investment banks

33

Deception

Churning

Insider trading

Conflict of interest

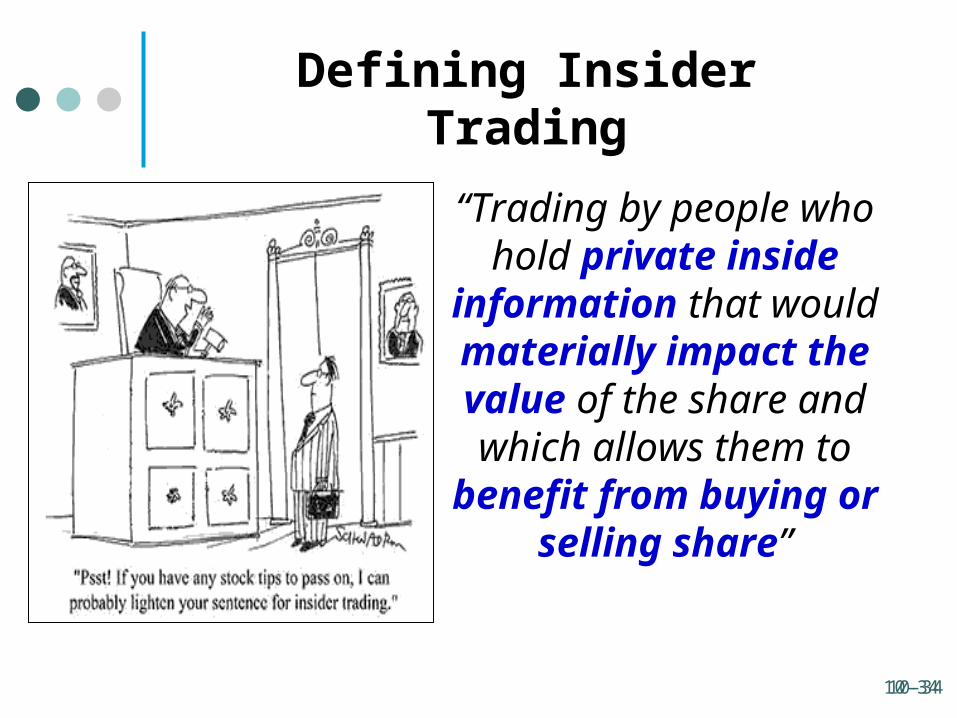

Defining Insider Trading

“Trading by people who hold private inside information that would materially

impact the value of the share and which

allows them to benefit from buying or selling share”

10-3410-34

More on Insider Trading …

Also when corporate insiders provide "tips" to family

members, friends, or others, AND

Those parties buy or sell the company's share based on that information.

3510-35

More on Insider Trading…

“Private information” privileged information which has not yet been released to the public

36

“Material information”

may have financial impact - short or long-term performance or important to prudent

investor 10-36

What’s so bad about it? (1) (The cons)

Whoever does this put his own interests before those of his shareholders – violating fiduciary duty

Unfair because the two parties do not have equal information two parties do not have equal access to information it prevents fair pricing due to a ‘uneven playing

field’

Inside information is company/shareholders’ ‘property’ - a form of theft

3710-37

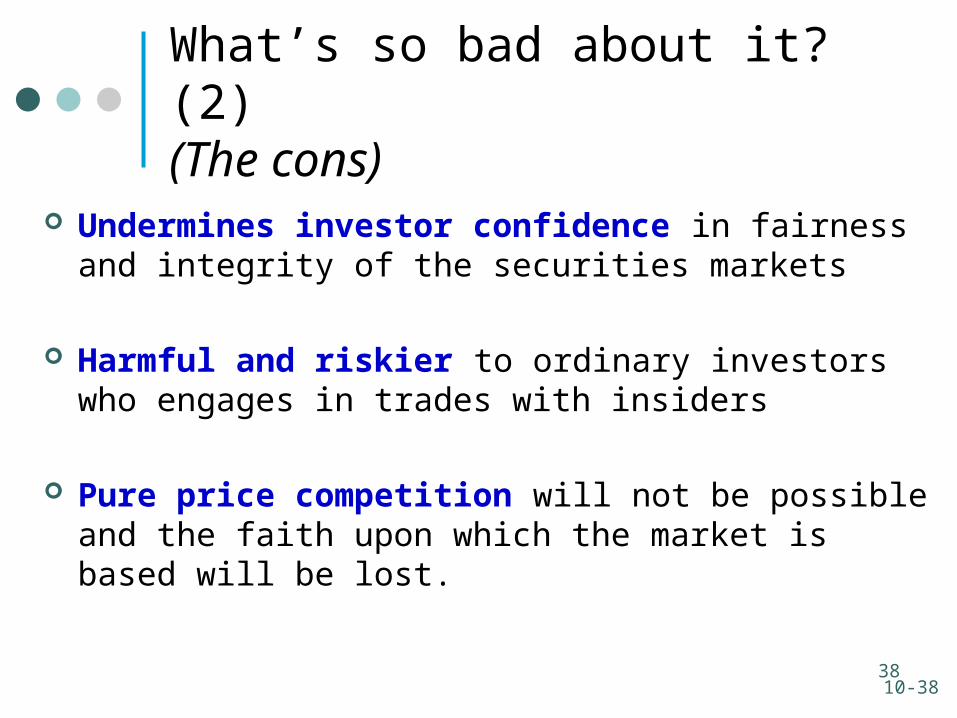

What’s so bad about it? (2) (The cons)

Undermines investor confidence in fairness and integrity of the securities markets

Harmful and riskier to ordinary investors who engages in trades with insiders

Pure price competition will not be possible and the faith upon which the market is based will be lost.

3810-38

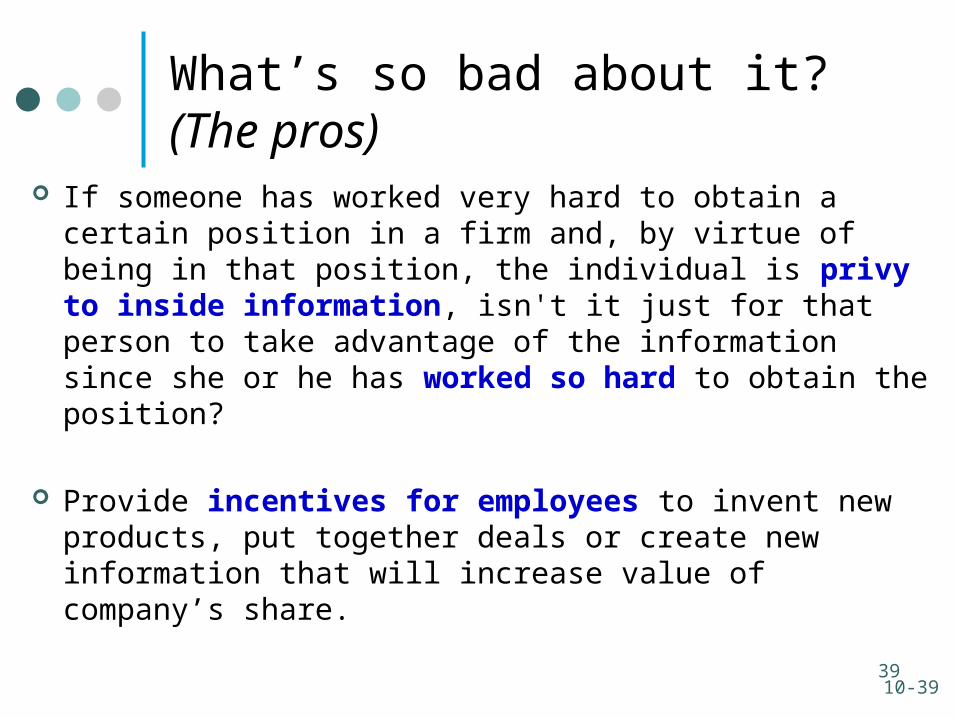

What’s so bad about it?(The pros)

If someone has worked very hard to obtain a certain position in a firm and, by virtue of being in that position, the individual is privy to inside information, isn't it just for that person to take advantage of the information since she or he has worked so hard to obtain the position?

Provide incentives for employees to invent new products, put together deals or create new information that will increase value of company’s share.

3910-39

What’s so bad about it?(The pros)

Accelerates flow of positive and negative info about the share to other shareholders and investors

Info can be quickly reflected in the share price – good for the market

4010-40

Deception

Failure of sales people to fully explain all the relevant information truthfully at the point of making a sale.

E.g. concealment of material information on the sales materials on the projected performance of an investment fund.

E.g. Emphasizing the strengths of the product and saying less about the weaknesses

E.g. Administrative fees were not disclosed

41

Churning

An excessive or inappropriate trading for a client’s account for the purpose of generating commissions for the broker

Why unethical? Breach fiduciary responsibility – must act in the best interest of a client.

4210-42

Conflicts of Interest

Concept is the same as the conflict of interest in accounting

Example 1: Research and investment departments.

Companies that engaged in investment banking would pressure their research analysts to give high ratings to companies whose shares they were issuing, whether those ratings were deserved or not.

Example 2: A financial planner who accepts kickbacks from a brokerage firm

To guide clients into certain investments fails in her or his professional responsibility by putting personal financial interests ahead of client interest.

4310-43