1 chapter 4 financial intermediation ©thomson/south-western 2006

TRANSCRIPT

1

Chapter 4

FINANCIAL INTERMEDIATION

©Thomson/South-Western 2006

2

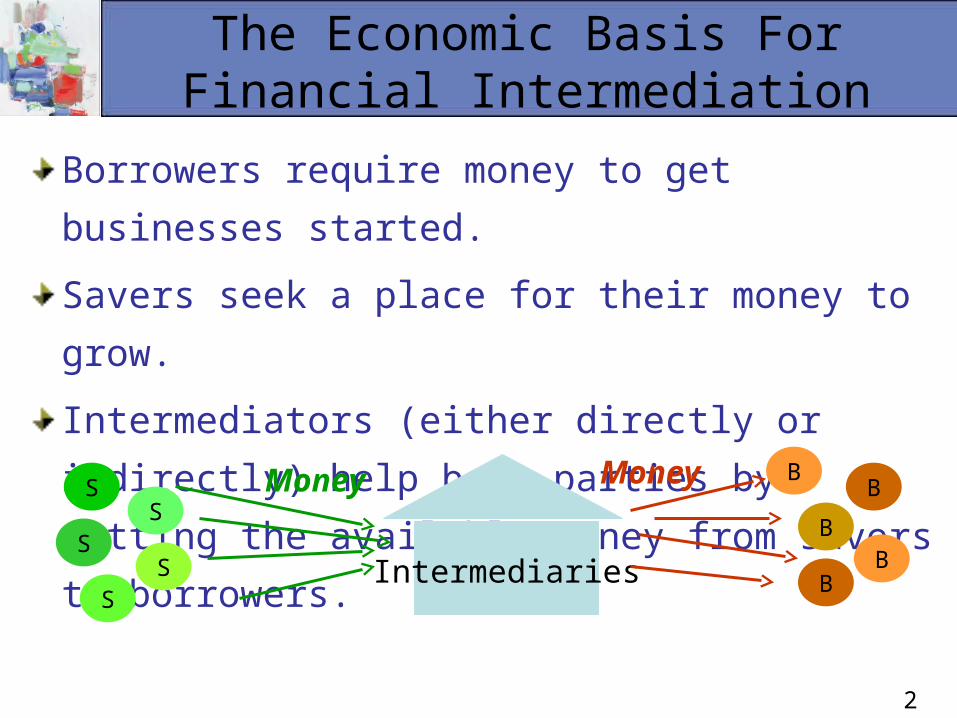

The Economic Basis For Financial Intermediation

Borrowers require money to get businesses

started.

Savers seek a place for their money to grow.

Intermediators (either directly or indirectly)

help both parties by getting the available

money from savers to borrowers.

Intermediaries

Money Money BB

BB

B

SS

SS

S

3

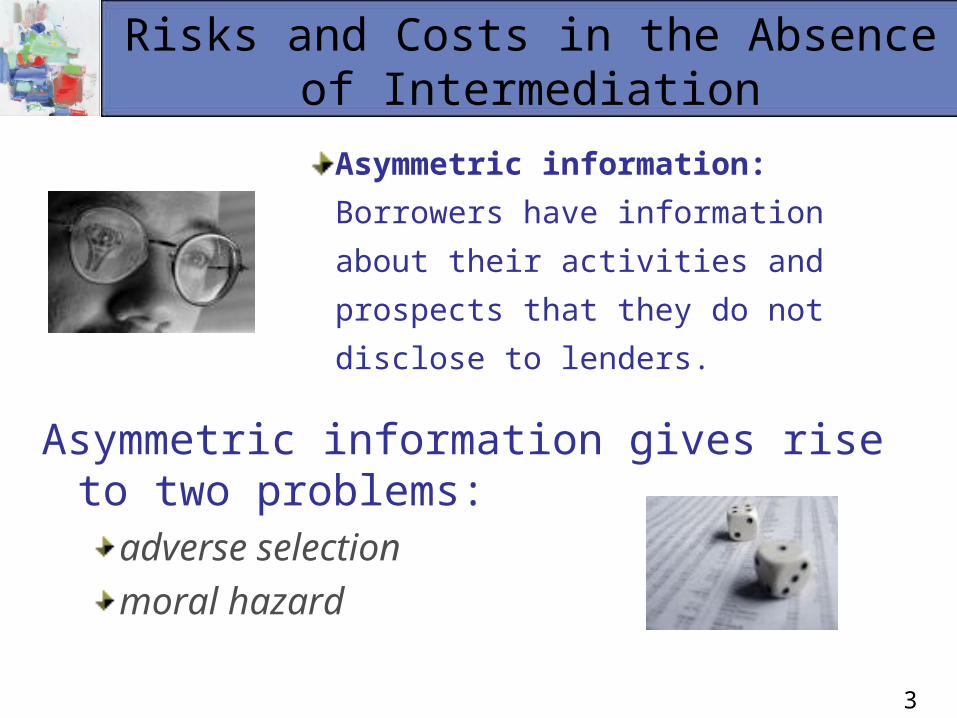

Risks and Costs in the Absence of Intermediation

Asymmetric information:

Borrowers have information about

their activities and prospects that

they do not disclose to lenders.

Asymmetric information gives rise to two problems:

adverse selection moral hazard

4

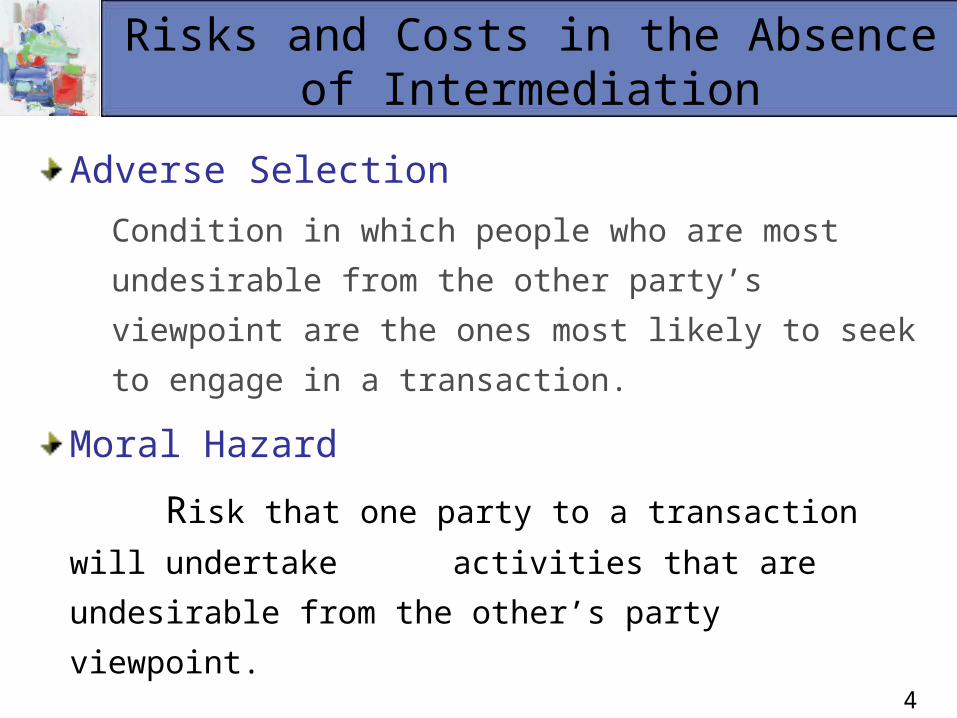

Risks and Costs in the Absence of Intermediation

Adverse Selection

Condition in which people who are most

undesirable from the other party’s viewpoint are

the ones most likely to seek to engage in a

transaction.

Moral Hazard

Risk that one party to a transaction will

undertake activities that are undesirable from the

other’s party viewpoint.

5

How Intermediation Helps

Financial intermediaries:

have superior ability to deal with

asymmetric information and the

associated problems of adverse

selection and moral hazard;

specialize in assessing the credit risks of

prospective borrowers;

have access to such private information

are better equipped to monitor

borrowers’ activities after the loan is

made.

6

Transactions Costs

Transactions costs: money and time spent carrying out financial transactions

Costs associated with asymmetric information

By pooling funds, financial intermediaries can exploit economies of scale.

By reducing transactions costs, financial intermediaries benefit both savers and deficit spenders.

7

Benefits of Intermediation

Benefits to Savers

From savers’ viewpoint, financial intermediaries

pool thousands of individuals’ funds and can

overcome certain obstacles that stop savers from

purchasing primary claims directly.

Allows individual savers to diversify

8

Benefits of Intermediation

Benefits to Deficit Units

From borrowers/spenders’ perspective,

financial intermediaries broaden the range of

instruments, denominations, and maturities

that an institution is able to issue, borrowing

costs – borrowers can tailor instruments to

best fit their needs.

9

Classification & Growth Of Financial Intermediaries

Financial Intermediaries issue (secondary) claims

against themselves to the public in order to obtain

funds with which to purchase (primary) claims issued

by deficit-spending units.

Three categories:

1. depository institutions,

2. contractual savings institutions,

3. investment-type intermediaries.

10

Table 4-1

1

2

3

11

Table 4-1

1

2

3

12

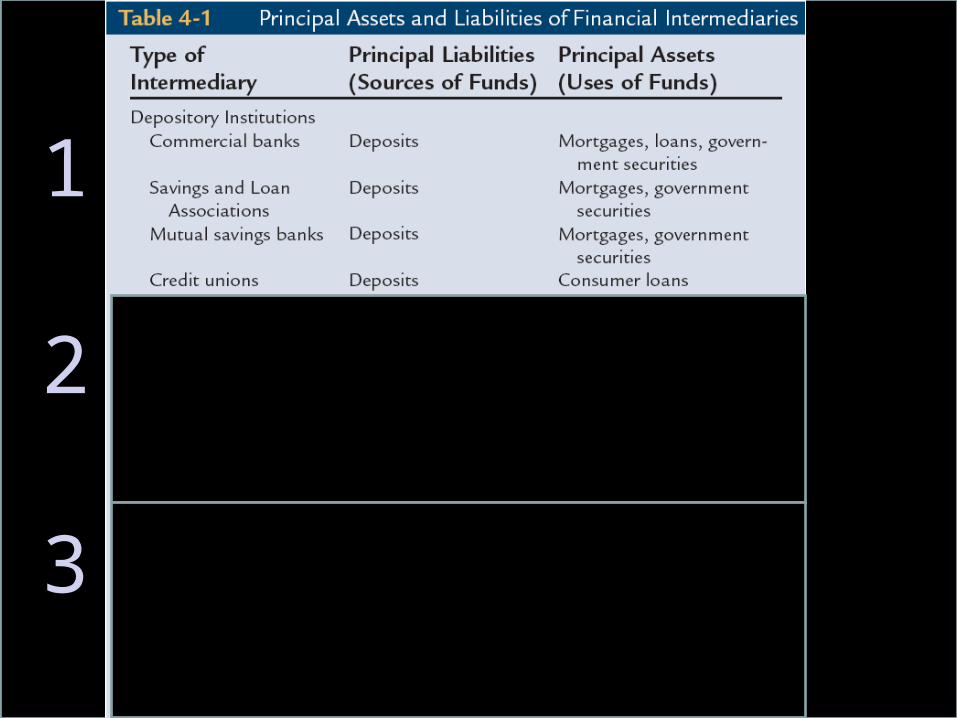

1. Depository Institutions

Types

1.1 Commercial banks

1.2 Savings & loan associations

1.3 Mutual savings banks

1.4 Credit unions

They:

issue checking, savings, and time deposits;

use the funds obtained to make various types of loans and to purchase securities.

Deposits issued by these institutions have no market risk because the principal does not fluctuate in nominal value.

13

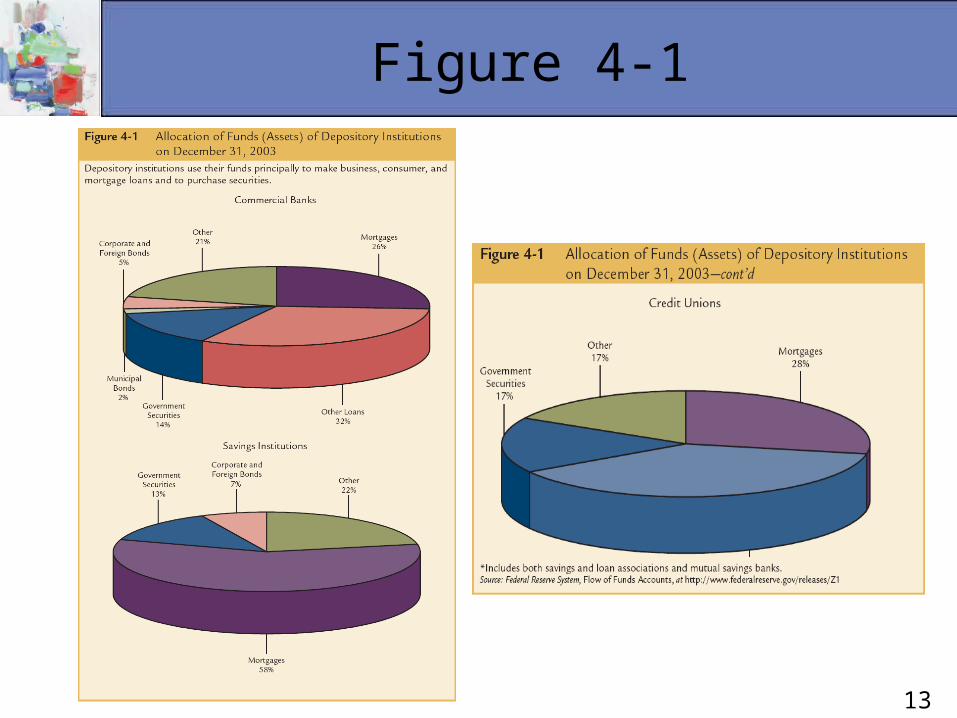

Figure 4-1

14

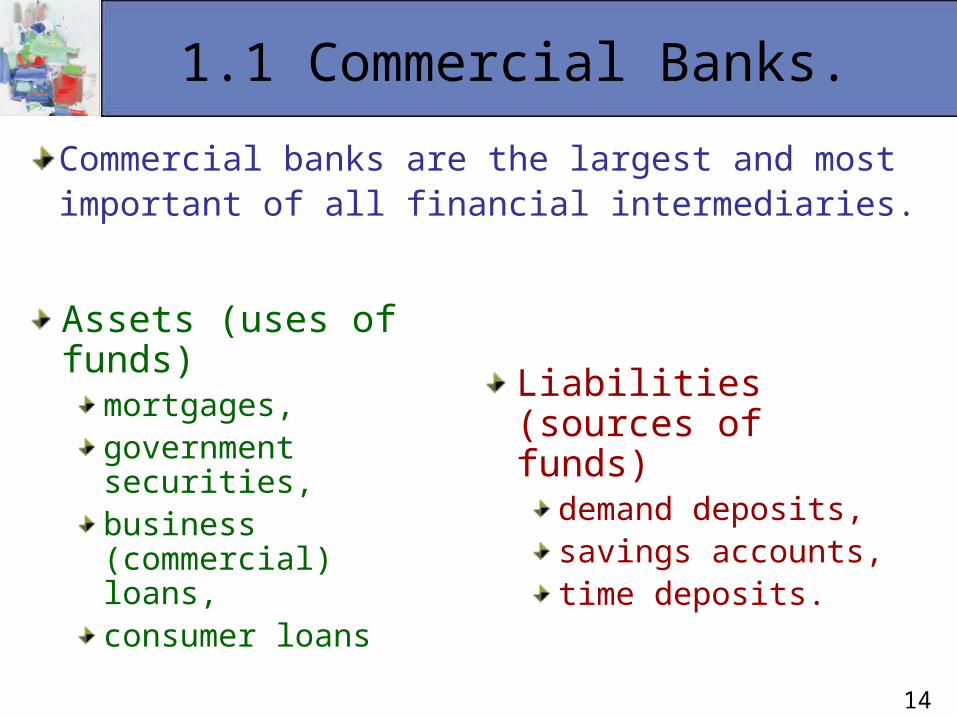

1.1 Commercial Banks.

Commercial banks are the largest and most important of all financial intermediaries.

Liabilities (sources of funds)

demand deposits, savings accounts, time deposits.

Assets (uses of funds)

mortgages, government securities, business (commercial) loans, consumer loans

15

1.2 Savings & Loan Associations (S & Ls)

S&Ls were first formed on the East Coast in the 1830s

by groups of people seeking to foster home ownership.

Individuals would pool their savings and make loans to

a few members to finance the purchase of a few

homes.

The federal government established the Federal

Housing Administration to insure mortgages, and to

encourage the issue of amortized mortgages through

S&Ls.

16

Other Institutions

1.3 Mutual Savings Banks (MSBs)

encourage working class employees to save

1.4 Credit Unions (CUs)

not-for-profits

for members

17

Table 4-1

1

2

3

18

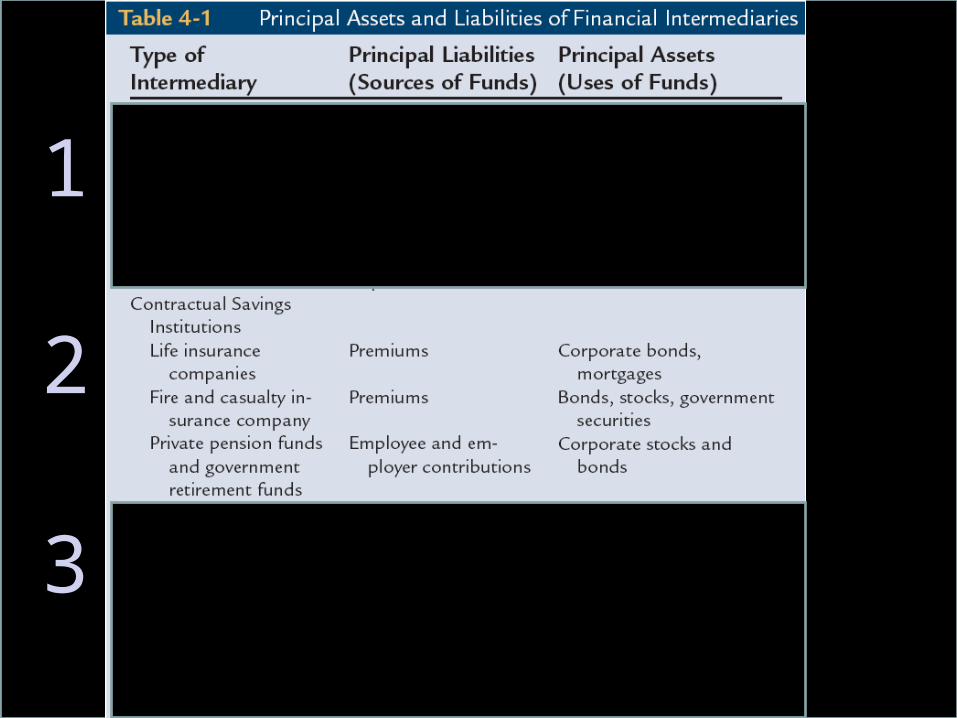

2. Contractual Savings Institutions

2.1 Insurance companies Life insurance

Non-Life insurance

2.2 Private pension funds

2.3 State & local government retirement funds

19

2.1 Life Insurance Companies

Life insurance companies:

Issue policies to customers

Collect premiums as a continuing source of funds

Invest > two-thirds of the funds in corporate bonds and equities

Typically regulated by the state insurance commissioner.

Life insurance policies:

have a specified cash surrender value--policyholders can obtain that cash on request.

20

2.2 Fire & Casualty Insurance Companies

Fire and casualty insurance companies sell protection against loss resulting from fire, theft, accident, natural disaster, malpractice suits, and other events.

They obtain funds from: premiums, retained earnings, and new stock share issues.

Property losses are more difficult to predict, so fire and casualty companies’ assets must be more liquid than life insurance companies’ assets.

21

2.3 Private Pension Funds & Government Retirement Funds

Pension funds manage portfolios more

efficiently than individuals by providing:

financial expertise,

economies of scale,

reduced transactions costs, and

diversification.

22

2.3 Private Pension Funds & Government Retirement Funds

The U.S. tax code encourages pension plans--

income is nontaxable until retirement.

Employers withhold the funds from workers'

paychecks and send them to a pension fund.

The retirement fund invests the contributions

in

corporate stocks, bonds and U.S.

government bonds.

23

Table 4-1

1

2

3

24

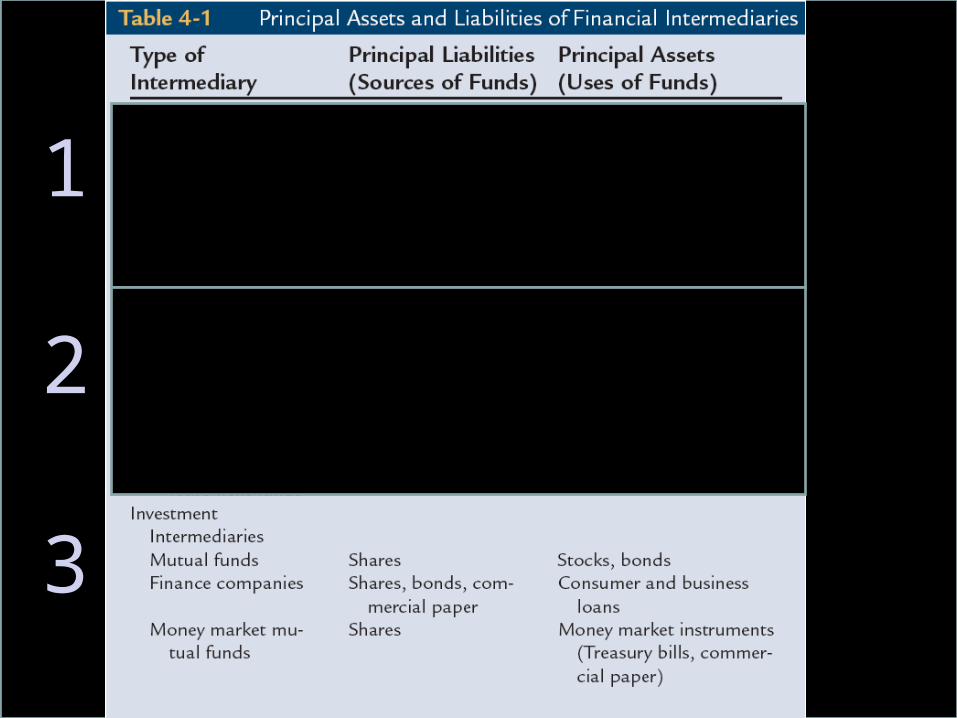

3. Investment-Type Financial Intermediaries

3.1 Mutual funds

3.2 Finance companies

3.3 Money market mutual funds

25

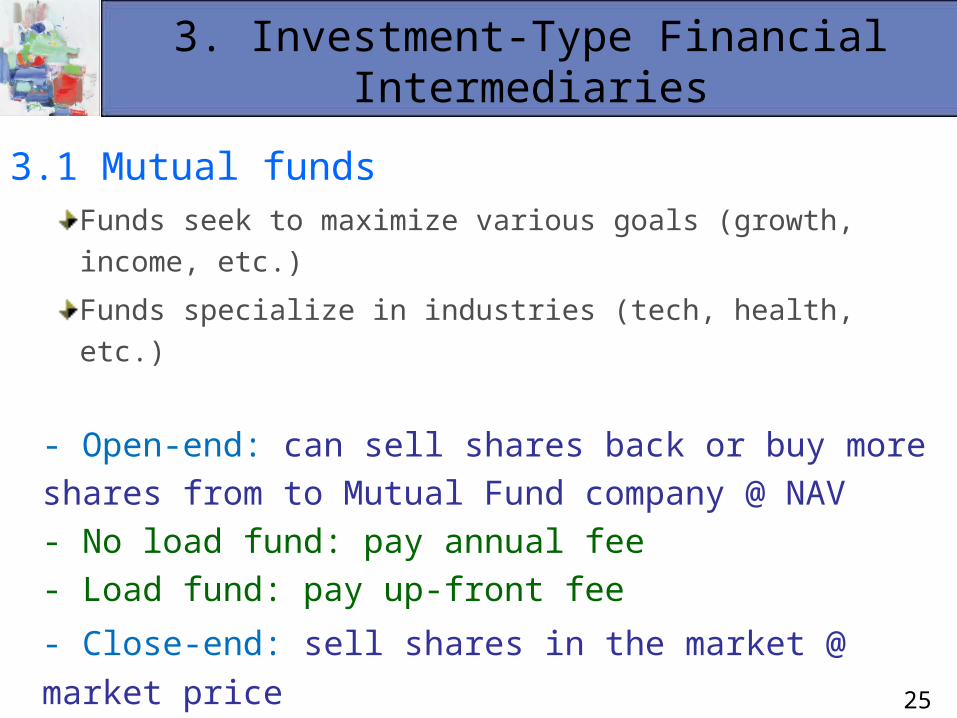

3. Investment-Type Financial Intermediaries

3.1 Mutual fundsFunds seek to maximize various goals (growth, income, etc.)

Funds specialize in industries (tech, health, etc.)

- Open-end: can sell shares back or buy more shares from to Mutual Fund company @ NAV

- No load fund: pay annual fee- Load fund: pay up-front fee

- Close-end: sell shares in the market @ market

price

26

3. Investment-Type Financial Intermediaries

3.2 Finance companies

sales finance companies

consumer finance companies

business finance companies

3.3 Money market mutual funds

same as mutual funds but short-term

invest in highly liquid assets

27

3. Investment-Type Financial Intermediaries

These intermediaries provide:

low transactions costs,

the financial expertise & experience supplied by mutual fund management,

increased diversification relative to that

feasible for a typical individual.