1 exploring the life cycle of costs: budget to audit jerry fife mary ellen sheridan jane youngers

Post on 22-Dec-2015

214 views

TRANSCRIPT

1

Exploring the Life Cycle of Costs:Budget to Audit

Jerry Fife

Mary Ellen Sheridan

Jane Youngers

2

A Seamless Enterprise

• Budget

• Spend

• Closeout

• Report

• Audit

3

Description of Handouts

• Project Summary

• PI’s suggested budget

• Selected readings from A-21

4

Focus on Federal $

• A 21 Cost Principles

• A-110 Administrative Requirements

• Cost Accounting Standards

• A-133 Audit

5

Take Home Point #1

• Communication

• Communication

• Communication

6

Proposal Budgeting: Start With the Basics

• A-21 (our costing “bible”, incorporates Cost Accounting Standards)

• A-110 (cost sharing and matching requirements)

7

Proposal Budgeting: Start With the Basics

• programmatic requirements

• institutional policies and procedures

8

Proposal Budgeting: A-21/Cost Accounting

Standards• To be allowable, costs must be:

- allocable- reasonable- consistent

9

Proposal Budgeting: A-21/Cost Accounting

Standards• To be allowable, costs must be:

- consistency requirement reinforced in CAS 501

10

Cost Accounting Standards (CAS)

• The basics

–Began in 1994, extended to Grants & Cooperative Agmt. in 1996 (A-21)

11

–Four Standards and Disclosure Statement

–Standards apply to all federally sponsored agreements

–Disclosure statement applies to institutions receiving $25M

12

• Only two of the Standards apply to our conversation today–501 Consistency in

Estimating, Accumulating and Reporting Costs

–502 Consistency in Allocating Costs Incurred for the Same Purpose

13

CAS 501

• Your budgeting practices need to be aligned with your accounting/reporting system

14

CAS 502

• Cannot Assign as Direct Cost if Included in Indirect Cost Pool

• Cannot Assign to Indirect Cost Pool if Charged as Direct Costs

15

CAS 502• “Normal” Indirect Costs

–Administrative/Clerical Salaries

–Office Supplies–Postage

16

CAS 502• “Normal” Indirect Costs

–Basic (Local) Telephone Charges

–Memberships

17

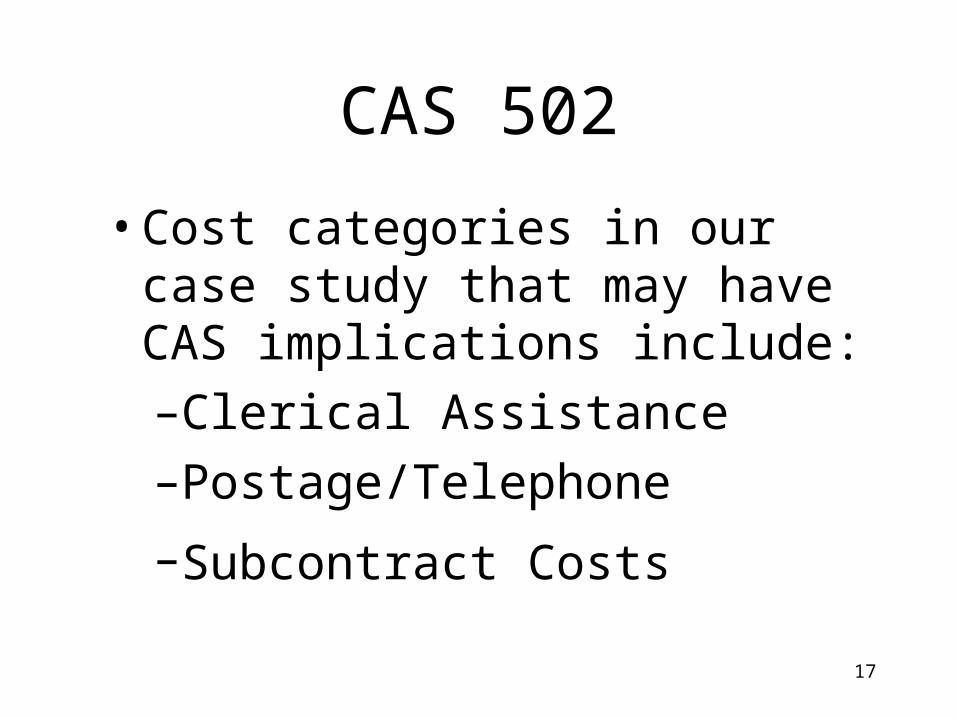

CAS 502

• Cost categories in our case study that may have CAS implications include:

–Clerical Assistance

–Postage/Telephone

–Subcontract Costs

18

CAS Take Home Message

• Know your institution’s CAS policies and follow them consistently

• If your institution does not have a policy refer to A-21

19

Proposal Budget: A-21

Other important areas of A-21:

• “j” section

• f.4 - .9 especially f.6.b.

20

Budget Construction

• Familiarize yourself with sponsor proposal guidance–allowable costs–format–cost justifications

21

Budget Construction

• Stay in communication with PI

– Unless NIH modular grant, costs can usually be lumped into major categories

22

Budget Construction

• Stay in communication with PI– Degree of itemization within

categories depends on sponsor (and sometimes on type of potential award)

23

Major Budget Categories

• Personnel costs (salaries and benefits)

• Consultants

• Equipment

• Supplies

24

Major Budget Categories

• Travel

• Other

• Subawards

• F & A

25

Personnel Costs: Salaries and Wages

• Faculty salaries

–institutional policy on academic year recovery

–summer salary

26

Personnel Costs: Salaries and Wages

• Faculty salaries–committed effort–salary cap (NIH)

27

Personnel Costs: Salaries and Wages

• Technical support

• Graduate research assistants

• Admin/clerical support

• Quote hourly rates? (almost never)

28

Personnel Costs: Benefits

• Approved vs. budgeting rates

• Do you have different rates for different types of personnel?

29

Consultants

• Rate of pay (NSF cap)

• IRS tests

• Travel costs for consultants

• Consultant agreements

30

Equipment

• What is your institutional capitalization policy?

• Sponsor’s definitions of equipment

• General purpose equipment

• Documentation of cost sharing

31

Supplies

• How much to itemize?

• What about office supplies?

• What is software?

• What are pc’s?

32

Travel

• Adhere to:

–institutional policy

–agency guidelines

• Okay to cost on per trip basis

33

Other

• Catchall category for most misc. costs–human subject fees–maintenance contracts–printing/postage

34

Other

• Catchall category for most misc. costs

–animal per diem–phone charges

• Watch out for unallowables

35

Subawards

• Subawardee budget incorporated into prime budget in toto

• Review subawardee costs for allowability

• Get rate agreements

36

F & A Costs

• Consult program guidelines for allowability/amount

• Use negotiated rate agreement

• On or off campus

37

F & A Costs

• Type of project

• Use correct direct cost base

• Fixed for life of award

38

Cost Sharing & Matching

• Don’t offer if you don’t have to

• A-110 offers guidance

• A-21 clarification regarding faculty committed effort

39

Cost Sharing & Matching

• Must be able to document for audit purposes

• Must be for costs within the project period

40

Jane’s Take Homes on Budgeting

• Prepare budgets with audits in mind

• Just because something is in budget doesn’t mean that it will be an allowable expenditure

41

Jane’s Take Homes on Budgeting

• Don’t cost share (including faculty committed effort) unless you have to

• Costs that will be unallowable as direct charges will also be unallowable as cost sharing

42

Getting the Award

•Meet with PI to Review Award Notice

•Identify Special Terms & Conditions

•Plan Project - Project/Budget must overlay

43

Setting up new account

• Use the award notice

• Check begin and end date

• Track cost sharing

• Use accounting system- subaccounts/object codes

44

Advance Accounts

• Pre-award Expenditures –Expanded Authority(90 days)

• Beware of regulated research- human subjects, animals

45

How many accounts?

–Associate accounts (aka “Parent-Child”)

–Simplify project management through accounting

46

Personnel

• PI – Over the cap salary

• Verify effort commitments

• Work with human resources

• Consulting

47

“Watch out” Categories

• Research subject fees

• Service center/recharge operations

48

Subrecipient• Approved if in the award budget

• Verify agreement has been executed

• Monitor invoicing- confirm technical process with PI

• A-133 sub recipient monitoring (letter, no findings)

49

Equipment

• Documentation per A-110

• Bidding

• Sole Source

50

Travel

• Foreign travel – is prior approval necessary?

• Use of US carrier/code sharing

51

Cost Sharing Diligence

• Document expenditures as they occur – avoid charge transfers

• Voluntary Committed Cost Share – Faculty effort

52

Cost Sharing Diligence

• Share of equipment purchase• Monitor compliance with award

requirements

53

Daily Life of Account Management

–Rebudgeting flexibility – Expanded Authority

–Consistency

–Reasonableness

–Allowability/Allocabilty

54

Letter of Credit

• After the fact- Avoid payment of interest to FEDS

–Chicago uses a weekly balance

• In advance- Interest due on cash balances that exceed 3 days

55

Mary’s Top Ten Award Management Take

Homes:

1. Communicate

2. Read award notice

56

3. Set up account correctly & completely

4. Finalize all required certifications & agreements

5. Review ledgers monthly6. Prepare for closeout well in

advance

57

7. Update account distributions promptly

8. Make transfers immediately

9. Confirm all charges are within project period

10. If in doubt, Ask! Ask! Ask!

58

Close Out Phase

• Keys for Success

–Good communication between department & central offices

–An early alert system

–“Do it right the first time” philosophy

59

Close Out Phase

–Management reporting to anticipate reporting workload

–Maintain a strategy for prioritizing reports

–Subcontracts reporting 60 days after termination

60

Close Out Phase

–Strategy for dealing with trailing charges

61

Close Out Phase

• Financial Reporting

– Final review of costs for:Allowability W/in grant/contract periodAllocability

62

Close Out Phase

• Financial Reporting

– Other possible reviews:CASCost sharingCorrect F&A rate applied?

63

Close Out Phase

• Other possible reviews/activities–NIH salary cap compliance–Budget restriction compliance–Proper object code assignment–Send back any unused funds

64

Close Out Phase

• Other activities

–Encumbrances

–Cost Overruns

–Subcontracts

–Parent/Child accounts

65

Close Out Phase

• Other Reports

–Property

–Patent/Inventions

–Other close out documents

66

Close Out Phase

• “The report is submitted, now what needs to be done”?–Freeze/lock–Make sure balance is zero

67

Close Out Phase

• “The report is submitted, now what needs to be done”?

–Prepare file for archiving

–Make sure it is marked to achieve proper retention requirements

68

Close Out Phase

• Consequences of late or poor financial reporting–Sanctions–Withholding of awards–A-133 audit findings

69

Close Out Phase

• Consequences of late or poor financial reporting–Exceptional Status–Lost of credibility with sponsors

70

Audit Phase

• “Audit Me First” Costs

–Inappropriate/Unauthorized costs

–Unallowable costs

–Improper cost allocations

71

Audit Phase

–Equipment purchased at the end of the project

–Overdrafts–Assignment of costs based on fund

availability or project expiration–Late cost transfers

72

Audit Phase

• Possible scenarios for audit in today’s environment

–A-133

–Whistleblower

–Contract Close out

–Random Audit (Your lucky day!)

73

Audit Phase

• Question: When should I be prepared for an audit?

• Answer: Always be prepared for an audit!

74

Audit Phase

• How should I prepare for/handle an audit?–Review file in advance of audit–Know if you have any

weaknesses

75

Audit Phase

• How should I prepare for/handle an audit?–Designate a central contact for all

audit activities –Always have a person accompany

auditors when visiting departments/faculty

76

Audit Phase

• How should I prepare for/handle an audit?–Always have a person accompany

auditors when visiting departments/faculty

–Always be truthful

77

Audit Phase

• How should I prepare for/handle an audit?

–Answer questions concisely but don’t be chatty

–Always request an entrance/exit interview

78

Audit Phase

• How should I prepare for/handle an audit?

–Accept the fact that there may be differences and know the avenues for resolution

–Keep your boss informed

79

Supplemental handout #4