1 financial $uccess presented by: name family financial education specialist university of missouri...

TRANSCRIPT

1

Financial $uccess

Presented by:

NameFamily Financial Education SpecialistUniversity of Missouri ExtensionWebsite: http://extension.missouri.edu/hes/Phone:E-mail:

2

1. Goals and Decisions2. Managing Financial Resources3. Managing Credit4. Managing Risk5. Consumer Information

Financial $uccess

3

What Matters Most?

Family Well-being(Primary Objective)

Use ofLimited Resources

Trade Offs

VALUES

Needs Vs.Wants

GOALS

4

Decision Making Process

• Why must I decide?

• Making WISE decisions What is the decision?

Inform yourself

Select the “best” alternative

Evaluate the outcome

5

Activity

• How Do I Decide?

6

Short-Term GoalsShort-Term Goals == Within next 6 monthsWithin next 6 monthsMid-Term GoalsMid-Term Goals == Within next 2 yearsWithin next 2 yearsLong-Term GoalsLong-Term Goals == More than 2 years from nowMore than 2 years from now

Time Limited

Relevant

Specific

Measurable Attainable

Setting SMART Financial Goals

7

Activity

• What My Family Wants to Accomplish

• Setting Financial Goals– Short-term– Mid-term– Long-term

8

1. Goals and Decisions

2. Managing Financial Resources

3. Managing Credit

4. Managing Risk

5. Consumer Information

Financial $uccess

9

Identifying Financial Resources

Income - money from earnings or other sources

Savings - money from past income

Credit - money from future anticipated income• borrowed from future income

at a price (interest rate)

10

Net Worth:Your Financial Snapshot

Net Worth = Assets – Liabilities

1. Add up value of what you own (assets)

2. Add up value of what you owe (liabilities)

3. Subtract liabilities from assets

Aim – positive net worth

Review net worth regularly

11

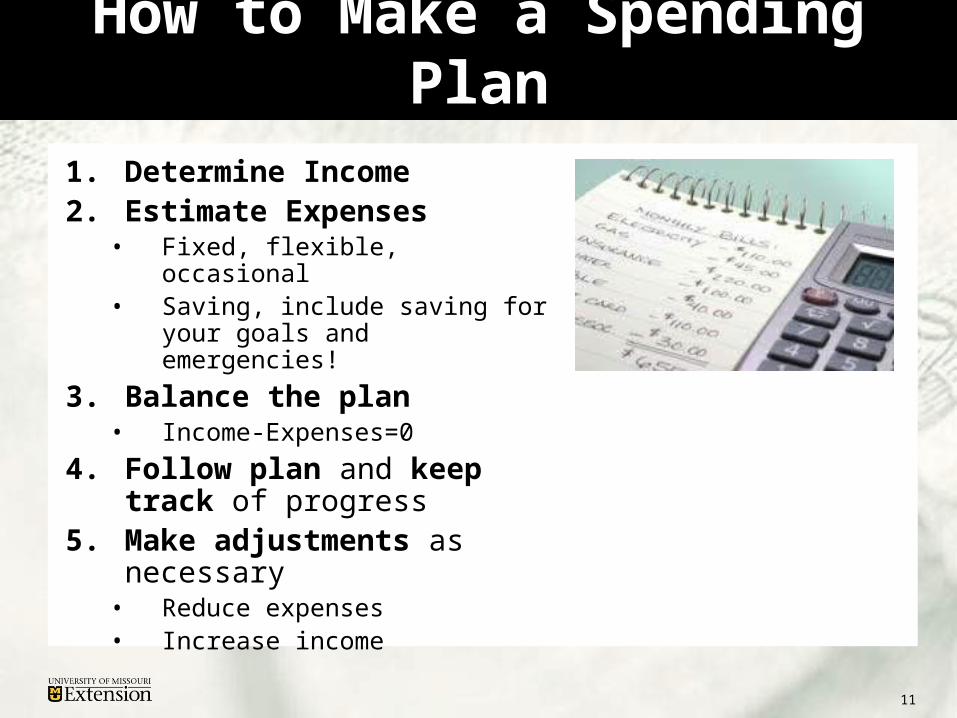

How to Make a Spending Plan

1. Determine Income 2. Estimate Expenses

• Fixed, flexible, occasional• Saving, include saving for your

goals and emergencies!

3. Balance the plan• Income-Expenses=0

4. Follow plan and keep track of progress

5. Make adjustments as necessary

• Reduce expenses• Increase income

12

Determine Income

Money for use today comes from several sources Paycheck Public assistance Social security Relatives Sale of goods Alimony or child support Investments or savings Credit

13

Estimate Expenses

Fixed expensesare the same each month.

Flexible expenseschange each month.

Occasional expensesoccur 1-3 times a year.

14

Activity

• Developing a Spending Plan

• Financial $uccess depends on:– knowing where you are now,– knowing where you

want to be, and– having a specific plan

for getting there.

15

Record Keeping

• What records to keep

• Where to keep records

• How long to keep records

16

1. Goals and Decisions

2. Managing Financial Resources

3. Managing Credit

4. Managing Risk

5. Consumer Information

Financial $uccess

17

What is Credit?

Using your future income in the present.

Types of Credit– Installment Credit– Service Credit– Revolving Credit

• Credit cards

18

Sources of Credit

• Banks, S&L, credit unions• Credit cards, department

stores• Mortgage companies• Utilities• Rent-to-own stores• Refund anticipation loan

(RAL)• Title loans, payday loan

companies• Pawn shops

19

Costs of Credit

• Annual percentage rate (APR)

• Annual fees

• Late fees

• Over-the-limit fees

• Transaction fees

• Penalty APRs

20

Costs of Credit

Balance APR Total $$ Payoff Time

$2,500 18% $3,157 31+ months $2,500 22% $3,375 33+ months $5,000 12% $5,782 28+ months $5,000 18% $6,314 31+ months $5,000 22% $6,750 33+ months $10,000 18% $12,627 31+ months $20,000 18% $25,254 31+ months

Based on minimum payment of 4% of the original balance, with no new debt added

Example: Credit Card

21

Activity

• Shop for Credit

22

Danger Signs

• Paying bills late

• Fees and penalties on bills

• Creditors calling

• Checks bouncing

• Juggling payments

• High debt-to-income ratio

23

Appropriate Use of Credit

It may be appropriate to use credit:• when you pay balances in full

and make payments on time• when you have a financial emergency• for convenience or safety

of a credit card• for additional security for

a purchase• when cash is not appropriate

(such as with on-line purchases)

24

Alternatives to Credit

• Rethink your goals

• Pay cash

• Save for emergencies and goals

• Use a debit card

• Postpone or do without

25

Activity

• When to Use Credit

26

What is a Credit Report?

Your financial management report card:

• Financial information

• Personal information

• Bankruptcy filings

27

Who Uses my Credit Report?

• Potential employers

• Rental landlords

• Lenders

• Insurance agencies

• Credit card companies

• Retailers

28

Who Provides Credit Reports?

• 3 major credit reporting bureaus are:– Equifax– Trans Union– Experian

Can I see a copy of my credit report?• One free annual report per person from each credit

reporting bureau

29

What if There is a Mistakeon my Credit Report?

• Contact the credit bureau

• Contact the creditor directly

• Write a 100 wordstatement

• Beware of “creditrepair” scams

30

Your Credit Score (FICO)

Payment History

35%Debt Load

30%

Length of Credit

15%

Other Factors10% New Credit

10%

31

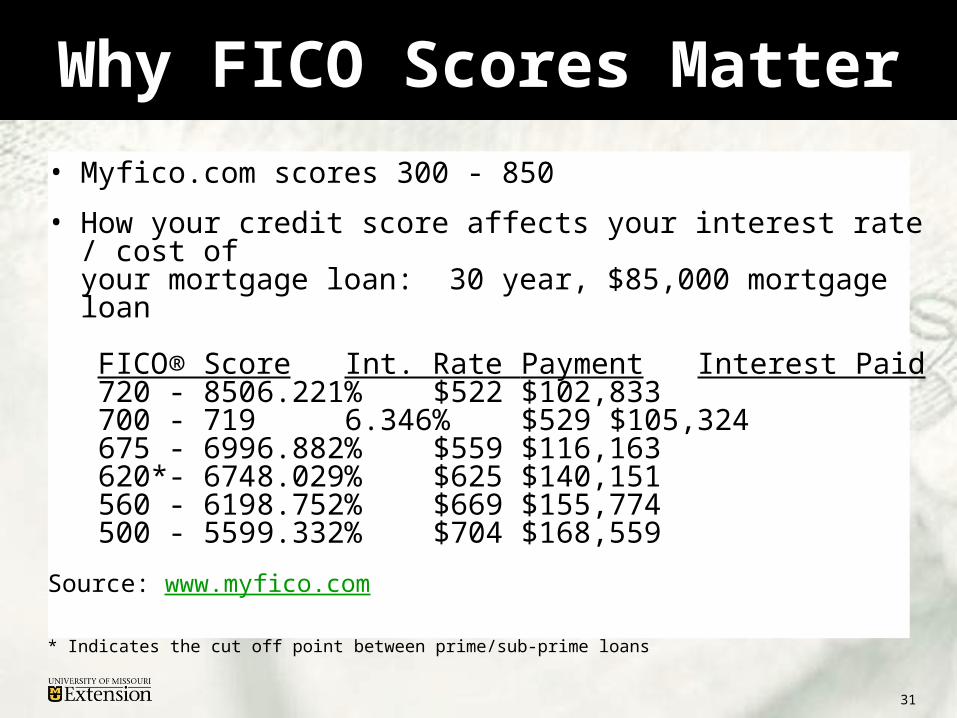

Why FICO Scores Matter

• Myfico.com scores 300 - 850

• How your credit score affects your interest rate / cost ofyour mortgage loan: 30 year, $85,000 mortgage loan

FICO® Score Int. Rate Payment Interest Paid 720 - 850 6.221% $522 $102,833 700 - 719 6.346% $529 $105,324 675 - 699 6.882% $559 $116,163 620*- 674 8.029% $625 $140,151 560 - 619 8.752% $669 $155,774 500 - 559 9.332% $704 $168,559

Source: www.myfico.com

* Indicates the cut off point between prime/sub-prime loans

32

Rebuilding Your Credit

• Check your credit report regularly

• Pay bills on time• Set up a financial plan• Apply for a secured credit card• Have someone co-sign a loan• If one lender turns you down,

try another

33

Credit and Bankruptcy

• Following bankruptcy, pay more for a loan• Automobile loans may be available

– You could face an APR = 20% or 22%, compared to 7%, prior to bankruptcy.

• Monthly payments for a $25,000 car, for 4 years would be – $760.76, at 20% (Total = $36,516.48)– $598.66, at 7% (Total = $28,735.68)

34

How Can I Protect my Credit?

• Keep personal information safe

• Shred or destroy receipts, applications and documents

• Report stolen cards immediately

35

• Truth in Lending

• Fair Credit Reporting

• Fair and Accurate Credit Transactions Act

• Equal Credit Opportunity

• Fair Debt Collection Practices

• Fair Credit Billing

Consumer Credit Laws

36

1. Goals and Decisions

2. Managing Financial Resources

3. Managing Credit

4. Managing Risk

5. Consumer Information

Financial $uccess

37

What is at Risk?

• What is at risk?– The possibility of

financial loss from events we do not anticipate

– Risk is everywhere

38

How to Manage Risk

• Methods of handling risk– Avoid (e.g., do not

participate)– Reduce (e.g., use

precautions)

39

How to Manage Risk

– Transfer(e.g., buy insurance)

– Retain(e.g., establish emergency fund)

40

Common Insurance Policy Terms

• Policy = contract

• Coverage = what insurancepays for

• Term = length of contract

• Premium = cost of contract

• Deductible = what you pay before insurance company pays

• Claim = request for payment

41

How Insurance Works:Term Life Insurance

• Application– Private history– Demographics

• Underwriting– Company tries to match the probability of

paying out with the premium

• Policy delivery

• Pay the premiums to continue coverage

42

Term Life Insurance…continued

• 2 possibilities– The term of the policy

ends; no dependents to take care of.

– Death, life insurance pays out the face value to take care of the dependents.

43

Activity

• Life’s Big Gamble

44

Types of Risk & Insurance• Loss of Property

– Auto Insurance– Homeowners/Renters Insurance

• Loss of Health– Health Insurance

• Loss of Income– Life Insurance– Disability Income Insurance

• Liability– Auto Insurance– Homeowners/Renters Insurance

• Living too Long– Retirement Savings– Annuities

45

Types of Insurance

• Other– Flood– Travel/AD&D– Long term

care/disability– Burial

46

Generally Unnecessary Insurance

• Credit insurance (e.g., life, disability, unemployment)

• Life insurance on the lives of children

• Dread disease (e.g., cancer insurance)

• “Double Indemnity” insurance riders

• Hospital indemnity policies

• Flight insurance

• Car rental collision-damage waivers

47

Shopping For Insurance

• Decide coverage you need

• Decide risk you want to retain

• Get three quotes for each type of insurance

• Try several different marketing channels

– Agents

– Mail order

– Online

– Insurance Broker

48

1. Goals and Decisions

2. Managing Financial Resources

3. Managing Credit

4. Managing Risk

5. Consumer Information

Financial $uccess

49

Consumer Information

• Opt out numbers:– Pre-approved credit card offers

• 1-888-5OPTOUT (1-888-567-8688)

– No call list• 1-866-662-2551 • http://www.ago.state.mo.us/nocalllaw/nocalllaw.htm

• ID Theft Clearinghouse • 1-877-438-4338• www.consumer.gov/idtheft

50

Consumer Information

• MU Extension– http://extension.missouri.edu/

• Federal Citizen Information Center (FCIC)– http://www.pueblo.gsa.gov/– 888-8 PUEBLO (888-878-3256)

• Missouri Attorney General’s Office– http://www.ago.state.mo.us/consumers.htm– Consumer Protection Hotline 800-392-8222

• National Fraud Information Center– http://www.fraud.org/– 800-876-7060

51

Creating Financial $uccess

• Make SMART goals and WISE decisions

• Every small step makes a difference

• Pay yourself first for goals and emergencies

• Consider future income before seeking credit

• Follow “The Rule of Three”

• Recognize your own personal needs and wants

• Buy insurance for large financial risks

• Develop a workable spending plan

• Start now on the road to financial success!