1 may, 2010 central bank of the republic of turkey macroeconomic policy challenges in turkey: the...

TRANSCRIPT

1

May, 2010

CENTRAL BANK OF THE REPUBLIC OF TURKEY

MACROECONOMIC POLICY CHALLENGES IN TURKEY:

THE POLICY MAKER’S VIEW

Huseyin ZAFER

EXECUTIVE DIRECTOR

2

I. Turkey’s Resilience to the crises

II. Effect of Crisis on Financial Stability

III. Monetary Policy Stance

IV. Latest Developments in the Turkish Economy

V. Inflation Outlook

VI. Exit Strategy

I. Turkey’s Resilience to the crises

II. Effect of Crisis on Financial Stability

III. Monetary Policy Stance

IV. Latest Developments in the Turkish Economy

V. Inflation Outlook

VI. Exit Strategy

OUTLINE

3

I. Turkey’s Resilience to the Crisis

4

Strength of Financial Sector and Macroeconomic Reforms

The macroeconomic reforms implemented and strenghtening of financial sector’s supervision and

regulation in the aftermath of 2001 crisis are the main reason behind the robustness of Turkish financial

system in recent financial crisis.

I. The regulations implemented afterwards of 2001 crisis have provided Turkish banks with strong level of capital adequacy, and healthy balance sheet structure.

II. Sustained high primary surplus and fiscal discipline helped supporting higher growth path and disinflation process. It also helped reducing public debt burden well below Maastricht Criterium and supported the banking system to resume their intermediation function.

III. Establishing independence and implementing floating exchange rate regime provided the CBRT to apply more active monetary policy and achieve an impressive disinflation record. The CBRT has also pursued an ambitious reserve accumulation that addresses Turkey’s external balance sheet vulnerabilities.

IV. The severity of the 2001 crisis generated the political momentum to put in place sound macroeconomic policies and enact critical structural reforms. Prospects for a positive economic performance have benefited from political support for the foundation of independent and strong institutions, improvement in transparency (especially in the fiscal area), and the wide range of legislative reforms in economic areas. This reform momentum has also been supported by EU accession process.

I. The regulations implemented afterwards of 2001 crisis have provided Turkish banks with strong level of capital adequacy, and healthy balance sheet structure.

II. Sustained high primary surplus and fiscal discipline helped supporting higher growth path and disinflation process. It also helped reducing public debt burden well below Maastricht Criterium and supported the banking system to resume their intermediation function.

III. Establishing independence and implementing floating exchange rate regime provided the CBRT to apply more active monetary policy and achieve an impressive disinflation record. The CBRT has also pursued an ambitious reserve accumulation that addresses Turkey’s external balance sheet vulnerabilities.

IV. The severity of the 2001 crisis generated the political momentum to put in place sound macroeconomic policies and enact critical structural reforms. Prospects for a positive economic performance have benefited from political support for the foundation of independent and strong institutions, improvement in transparency (especially in the fiscal area), and the wide range of legislative reforms in economic areas. This reform momentum has also been supported by EU accession process.

5

II. Global Crisis and Signs of Recovery

6

Turkish financial markets were quite resilient during the global financial crisis. Recovery in the

global risk perceptions from spring 2009 has favourably affected Turkey’s risk indicators,

domestic interest rates and exchange rate volatility.

Financial markets were resilient...

FX Rate Volatility and Benchmark Rate(January 2008 – May 6, 2010, %)

* Source: CBRT, Bloomberg

Risk Indicators and ISE(January 1, 2008 – May 6, 2010, bps)

Source: CBRT, Bloomberg

EMBI-TUR

EMBI+

ISE-100 (right axis)

0

100

200

300

400

500

600

700

800

900

1000

01.0

8

03.0

8

06.0

8

09.0

8

12.0

8

02.0

9

05.0

9

08.0

9

11.0

9

01.1

0

04.1

0

0

10000

20000

30000

40000

50000

60000

70000

0.12

TL/USD, monthly Volatility (rhs)

21.55%

Nominal Interest Rate

Real Interest Rate

0

5

10

15

20

25

01.0

8

04.0

8

07.0

8

10.0

8

01.0

9

04.0

9

07.0

9

10.0

9

01.1

0

04.1

0

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

Beginning of Policy Rate Cut Cycle (Nov 20, 2008), aftermath of Lehman Collapse.

7

Credit Ratings were increased

Recently, the risk premia of countries with high debt level have risen significantly.

Turkey’s risk premium, on the other hand, has sustained its stable course

thanks to her solid financial system and low level of indebtedness.

Source: Bloomberg, CBT

CDS Premia of Selected Countries(Jan 2009 – May 6, 2010, 1 Oct 2009 = 100)

Sovereign Ratings and Changes in Risk Premia(September 12, 2008 – May 6, 2010, bps)

Source: CBRT, Bloomberg

Turkey0

100

200

300

400

500

600

700

800

900

1000

01.0

9

02.0

9

03.0

9

04.0

9

05.0

9

06.0

9

07.0

9

08.0

9

09.0

9

10.0

9

11.0

9

12.0

9

01.1

0

02.1

0

03.1

0

04.1

0

05.1

0

Greece

Portugal

Turkey

Spain

Brazil

ChileColombia

Czech R.Hungary

Indonesia

MexicoPoland

Greece

S. AfricaS. Korea Turkey

Portugal

Spain

-200

0

200

400

600

800

0 1 2 3 4 5 6 7 8 9 10 11 12 13Fitch Sovereign Credit Ratings (1=AAA, 13= BB-)

Cha

nge

in C

DS

(bp

s)

8

III. Monetary Policy Stance

9

Monetary Policy Stance

The strength of the financial system in Turkey has enabled the CBRT to focus on restraining the

adverse effects of the financial crisis without conflicting with the primary objective of maintaining

price stability. CBRT’s policy rates are the main determinant of market rates in Turkey indicating the improved effectiveness of monetary policy.

Source: CBRT, Reuters, Bloomberg

Policy Rates and CDS Change(*September 12, 2008 – May 6, 2010)

Policy Rate and Benchmark Bond Yield(*January 2007- May 6, 2010)

Source: ISE, CBRT

Brazil

Chile

Czech Rep.

Hungary

Mexico

Poland

S. Africa

Russia

Colombia

S. Korea

IndonesiaTurkey-70

-50

-30

-10

10

30

50

70

90

110

130

150

-12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1Change in Policy Rates (pps)

Cha

nge

in C

DS

(bp

s)

5

10

15

20

25

30

01.0

7

04.0

7

07.0

7

10.0

7

01.0

8

04.0

8

07.0

8

10.0

8

01.0

9

04.0

9

07.0

9

10.0

9

01.1

0

04.1

0

CBRT Policy Rate (compounded)

Benchmark Bond Yield (compounded)

10

1. Measures to decrease uncertainty and volatilty:

• In October-November 2008, the spread between

CBRT O/N lending and borrowing rates decreased

from 3.5 to 2.5 points.

• Starting from October 2008, CBRT began to

provide liquidity more than needed by the market.

2. Measures for decreasing permanent liquidity

shortage and supporting credit market:

• CBRT resumed its repo auctions with 3-month

maturity as of June 2009.

• TL required reserve ratio was decreased from 6%

to 5% as of October 2009.

3. Policy interest rate decisions:

• As the global crisis deepened, by forecasting that

the inflation would decrease, CBRT decreased

borrowing interest rate from 16.75% to 6.50%.

Measures taken for TL markets by CBRT

In an environment of increased volatility in international financial markets, the Central Bank has provided liquidity to the market in order to mitigate the adverse effects and to minimize concerns that may arise in money markets,

In an environment of increased volatility in international financial markets, the Central Bank has provided liquidity to the market in order to mitigate the adverse effects and to minimize concerns that may arise in money markets,

Policy Rate and Repo Rate(September 2008 – May 6, 2010, %)

Source: CBRT

4

6

8

10

12

14

16

18

20

22

09.0

8

11.0

8

01.0

9

03.0

9

05.0

9

07.0

9

09.0

9

11.0

9

01.1

0

03.1

0

05.1

0

Weekly Repo Rate

CBRT Policy Rates

11

1. FX buying auctions were suspended in October 2008.

2. FX selling auctions were taken between 24-27 October

2008.

3. In October 2008, CBRT restarted its intermediary

activities in FX Deposit Markets again.

4. Transaction limits for banks increased to USD 10.8

billion, and the maturity of FX deposits borrowed by

banks was increased from 1 week to 1 month.

5. Moreover, lending rate of 10 % was reduced to 7% in

USD and 9% in Euro.

6. In February 2009, the maturity of FX deposit

transactions was raised from 1 month to 3 months and

CBRT lending rate was decreased to 5.5% in USD and

6.5% in Euro.

7. FX required reserve ratio was decreased from 11% to

9% as of December 2008, limits for export rediscount

credits were raised.

Measures taken for FX markets by CBRT

In order to curb potential problems in the Turkish financial markets that may arise from global developments during crisis, the Central Bank implemented a set of measures to increase the efficiency of the Turkish banking system and to strengthen the FX liquidity of banks.

In order to curb potential problems in the Turkish financial markets that may arise from global developments during crisis, the Central Bank implemented a set of measures to increase the efficiency of the Turkish banking system and to strengthen the FX liquidity of banks.

Source: CBRT

-1.1

-0.6

-0.1

0.4

0.9

1.4

01-0

802

-08

03-0

804

-08

05-0

806

-08

07-0

808

-08

09-0

810

-08

11-0

812

-08

01-0

902

-09

03-0

904

-09

05-0

906

-09

07-0

908

-09

09-0

910

-09

11-0

912

-09

01-1

002

-10

03-1

0

1.40

1.50

1.60

1.70

1.80

1.90

2.00

2.10

FX Buying and Selling Auctions against TRY and FX Basket

(Jan 2008 – Mar 2010)

FX Buying Auctions(USD 6.2 billion)

FX Selling Auctions (USD 1 billion)

Equally weighted US Dollarand Euro Basket (right axis)

12

IV. Latest Developments in the

Turkish Economy

13

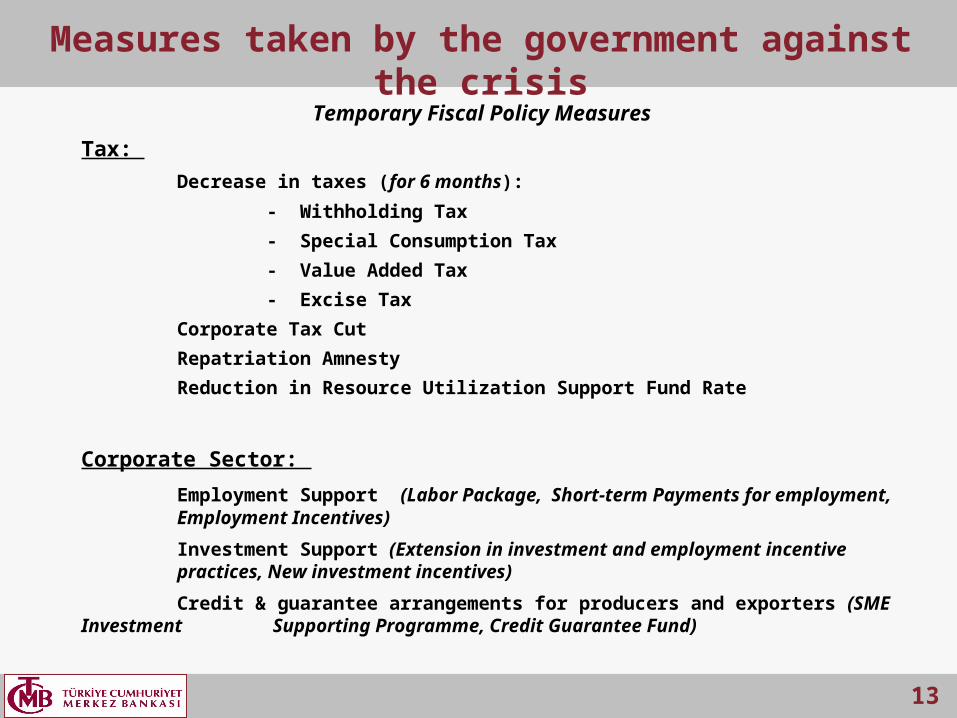

Measures taken by the government against the crisis

Temporary Fiscal Policy Measures

Tax:

Decrease in taxes (for 6 months):

- Withholding Tax

- Special Consumption Tax

- Value Added Tax

- Excise Tax

Corporate Tax Cut

Repatriation Amnesty

Reduction in Resource Utilization Support Fund Rate

Corporate Sector:

Employment Support (Labor Package, Short-term Payments for employment, Employment Incentives)

Investment Support (Extension in investment and employment incentive practices, New investment incentives)

Credit & guarantee arrangements for producers and exporters (SME Investment Supporting Programme, Credit Guarantee Fund)

14

Strong Growth Momentum After 2001 Crisis...

Source: TURKSTATSource: TURKSTAT

27-quarter Uninterrupted Growth

(quarterly, yoy % change)

Following sharp contraction of economic activity in 2001, Turkish economy experienced a strong growth cycle thanks to wide ranging reform process.

The cornerstones of the reform agenda were fiscal discipline, sound banking sector, independent monetary policy and structural reforms.

Currently, the macroeconomic policy framework continues to stand on mainly fiscal discipline and price stability together with ongoing structural reforms.

-15

-10

-5

0

5

10

15

2000

Q4

2001

Q4

2002

Q4

2003

Q4

2004

Q4

2005

Q4

2006

Q4

2007

Q4

2008

Q4

2009

Q4

80

90

100

110

120

130

140

150

2000

Q4

2001

Q4

2002

Q4

2003

Q4

2004

Q4

2005

Q4

2006

Q4

2007

Q4

2008

Q4

2009

Q4

Seasonally Adjusted GDP

(2001Q1=100)

15

Better Readings Compared to European Peers Except Q1

Source: TURKSTAT, EUROSTATSource: TURKSTAT, EUROSTAT

Among European peers, GDP growth performance of Turkey was on average in the first quarter of 2009.

However, GDP performance were better than the European countries following the fiscal and monetary policy responses in the remainder of the year.

GDP Growth – 2009Q1

(qoq, seasonally adjusted, %)

GDP Growth – 2009Q2, 2009Q3 & 2009Q4

(qoq, seasonally adjusted, %)

-7

-16

-14

-12

-10

-8

-6

-4

-2

0

2

LT LV EE SK TR SI CZ HU PT ES GR PL

-4

-2

0

2

4

6

8

234 234 234 234 234 234 234 234 234 234 234 234

LT LV EE SK SI CZ HU PT ES GR PL TR

16

Unemployment: Limiting Factor on Domestic Demand

Source: TURKSTAT

The Breakdown of Higher Unemployment Ratio (yoy, pps)

Unemployment ratio increased considerably but the increase was mainly driven by higher labor

force participation.

Contraction in economic activity resulted in employment losses in non-agricultural sectors.

Change in Non-agricultural Employment (000, yoy change ) GDP Growth (yoy change)

4.2 4.4 3.2 0.5

Source: TURKSTAT

3.93.0

3.3

2.1

-1.6

-0.1

0.31.4

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

2009Q1 2009Q2 2009Q3 2009Q4

Higher Labor Force Participation Decrease in Employment

-6

-4

-2

0

2

4

6

8

10

2005 2006 2007 2008 2009

-600

-400

-200

0

200

400

600

800

1000

GDP Growth (lhs)

Change in Non-agricultural Employment

17

Source: PEP 2009

Growth Prospects: 2010 and onwards...

Growth Forecasts (yoy, % change)

Turkish economy is expected to record positive growth rates in 2010. Stock changes will make positive contribution to GDP growth after the destocking behaviour in 2009. Along with the return of positive growth rates contribution of net export is expected to turn to negative.

Growth Forecasts (yoy, pps contribution)

Source: PEP 2009

2.6 2.4

7.6

4.2

5.4

3.32.8

7.17.5

2.2

10.4

6.5

9.3

6

4.8

0

2

4

6

8

10

12

Private Con. Public Con. Gross FixedCapital

Formation

Export Import

2010 2011 2012

3.7 4.2

5.9

0.30.2

-0.4 -0.5 -0.9

3.5

5.0

4.0

-2

0

2

4

6

8

10

2010 2011 2012

Net Export

Stock Changes

Domestic Demand

GDP Grow th

18

Public Finance

Public Debt and Budget Deficit of Turkey and Other Developing Countries (2003-2012, percent)

Public Debt and Budget Deficit of Turkey and Developed Countries

(2003-2012, percent)

Public debts and budget deficits have increased on a worldwide scale (particularly in advanced economies) due to the expansionary fiscal policies and decreasing tax incomes.

20

40

60

80

100

-2 0 2 4 6 8 10

2012

2003 2003

2012

2008

2008

Budget Deficit/GDP

Pu

blic

De

bt/G

DP

35

40

45

50

55

60

65

70

-2 0 2 4 6 8 10

2012

2003 2003

2012

2008

2008

Budget Deficit/GDP

Pu

blic

De

bt/

GD

P

Average of Developed Countries

Turkey

Average of Developing Countries

Turkey

Source: IMF, Ministry of Finance, Undersec.of Treasury MTP (2010-2012), 2009 Program. Source: IMF, Ministry of Finance, Undersec.of Treasury MTP (2010-2012), 2009 Program.

19

The medium term program outlines an exit strategy from fiscal crisis intervention measures.

Public debt ratios are expected to decline in 2011 and onwards mildly well below theMaastricht debt criterion.

However, the realization of the budget deficit and public debt ratios will be better than MTP (2009) targets due to the higher growth rates in the medium term.

Medium term fiscal framework is consistent and achievable

*: In MTP, the ratio of EU-Defined Debt to GDP projection for 2009 was 47,3%.

Source: Medium Term Programme , Treasury, IMF

EU-Defined Public Debt and Medium-Term Targets(2002 – 2012, ratio to GDP, percent)

Maastricht Criteria: 60%2008 2009 2010* 2011* 2012*

Budget Expenditures 23,8 28 27,9 26,7 25,6 Non-Interest Expenditures 18,5 22.4 22,4 21,8 21,1

Interest Expenditures 5,3 5.6 5,5 4,9 4,5Budget Revenues 22,0 22.5 23,0 22,6 22,4 Tax Revenues 17,7 18.1 18,8 18,8 18,7Budget Balance -1,8 -5.5 -4,9 -4,0 -3,2Primary Balance 3,5 0.1 0,7 0,9 1,3

Central Government Budget Realizations and (as percent of GDP)

* Target

73.7

67.4

59.2

52.3

46.1

39.4 39.5

45.5 44.5 44.3 43.5

0

10

20

30

40

50

60

70

80

2002 2003 2004 2005 2006 2007 2008 2009* 2010** 2011** 2015*

20

Balance of Payments

The crisis led to a decrease in the current account deficit of Turkey.

With the help of declining energy prices during the global crisis, Turkey’s current account balance excluding net energy imports was positive.

Sluggish growth expectations for the Euro area and rising commodity prices might widen the current account deficit in the medium term.

CAB and Net Energy Imports(2001-2009, as percent of GDP)

Source: TURKSTAT

-2,3

-6,1

1,91,9

-1,3 -1,4

5,9

-7,0

-5,0

-3,0

-1,0

1,0

3,0

5,0

7,0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

CAB/GDP(CAB excl.energy)/GDP

Source: IMF - WEO

CAB/GDP Ratios(2009, percent)

-30 -25 -20 -15 -10 -5 0 5 10

BulgariaCyprusGreecePortugal

Slovak Rep.Malta

IcelandSloveniaHungary

ItalyPoland

Czech R.U.K.

TurkeyFranceBelgiumFinland

LithuaniaDenm.

EstoniaAustria

GermanyLatvia

Sw edenNetherl.

Luxemb.

21

Banking Sector

The gross banking sector NPL ratio started to fall slightly from 5.2% in early January 2010 to 5.0% in mid-March, which is a supporting development for profitability of the banking sector in the coming period.

The gross banking sector NPL ratio started to fall slightly from 5.2% in early January 2010 to 5.0% in mid-March, which is a supporting development for profitability of the banking sector in the coming period.

Despite the global crisis, CAR is still well above ( 20 % as of February 2010) both the minimum requirement of 8 % and the target ratio of 12 %.

Despite the global crisis, CAR is still well above ( 20 % as of February 2010) both the minimum requirement of 8 % and the target ratio of 12 %.

Non Performing Loans(% of total loans, as of April 2010)

Capital Adequacy Ratio(%, as of February 2010)

2.80

4.80

6.80

8.80

10.80

12.80

12.0

3.20

04

08.1

0.20

04

06.0

5.20

05

02.1

2.20

05

30.0

6.20

06

26.0

1.20

07

24.0

8.20

07

21.0

3.20

08

17.1

0.20

08

15.0

5.20

09

06.1

1.20

09 0

5

10

15

20

25

30

35

12.0

2

06.0

3

12.0

3

06.0

4

12.0

4

06.0

5

12.0

5

06.0

6

12.0

6

06.0

7

12.0

7

06.0

8

12.0

8

06.0

9

12.0

9

CAR

Minimum Rate, 8%

Target Rate, 12%

Source: BRSA Source: BRSA

22

V. Inflation Outlook

23

The sharp contraction in aggregate demand, fall in commodity prices and breaking of inertia in services prices with the help of tax cuts have led to decline in inflation rates in 2009.

However, rise in energy and food prices, base effects of the last year and tax hikes at the beginning of 2010 led to an increase in annual inflation in the the first 4 months of 2010.

Core indicators show that this increase is due to base effects and temporary factors.

Inflation Developments

Inflation Developments(y-o-y, % change)

Source: TUIK, CBRT*SCA-H: CPI excluding unprocessed food products, energy, alcoholic beverages, tobacco products and gold SCA-I: CPI excluding energy, food and non-alcoholic beverages, alcoholic beverages and tobacco products and gold

4 4

6.5

10.19

5.17

5.65

5

5.5

7.5

0

2

4

6

8

10

12

14

01.0

7

04.0

7

07.0

7

10.0

7

01.0

8

04.0

8

07.0

8

10.0

8

01.0

9

04.0

9

07.0

9

10.0

9

01.1

0

04.1

0

07.1

0

10.1

0

01.1

1

04.1

1

07.1

1

10.1

1

01.1

2

04.1

2

07.1

2

10.1

2

CPI

SCA-H*

SCA-I*

Inflation Target

%

24

The inflation realizations parallel to the CBRT’s inflation outlook support the disinflation

process, and inflation expectations follow a path parallel with CBRT forecasts.

Inflation expectations are in line with the monetary policy outlook

Inflation Expectations(January 2006- April, 2010, %)

Source: TUIK, CBRT

Inflation Forecasts(year-end forecasts, %)

5

4 4

7.5

6.5

5.5

5

0

2

4

6

8

10

12

14

01

.06

06

.06

11.0

6

04

.07

09

.07

02

.08

07

.08

12

.08

05

.09

10

.09

03

.10

08

.10

01

.11

06

.11

11.1

1

04

.12

09

.12

CPI 12-month expectation 24-month expectation Inflation Targets

April Inflation: 10.19%

7.2

3.6

5.4

8.4

5

9.6

7.2

0

2

4

6

8

10

12

2009 2010 2011 2012

%

25

IX. Exit Strategy of the Central Bank

26

CBRT has provided ample TRY liquidity to the banking system since 09Q2. On April

14, 2010 the CBRT announced the framework of its Exit Strategy.

Turkish Lira Liquidity

Source: CBT

-20

-15

-10

-5

0

5

10

15

20

25

30

01-0

8

02-0

8

03-0

8

04-0

8

05-0

8

06-0

8

07-0

8

08-0

8

09-0

8

10-0

8

11-0

8

12-0

8

01-0

9

02-0

9

03-0

9

04-0

9

05-0

9

06-0

9

07-0

9

08-0

9

09-0

9

10-0

9

11-0

9

12-0

9

01-1

0

02-1

0

03-1

0

Weekly REPO Funding

3 Month REPO Funding

Drawn from Interbank

Net Liquidity Provided

Market Liquidity (Jan 2008 – Apr 2010, billion TRY)

27

Exit Strategy – FX Liquidity

• Gradual and moderate hikes in the reserve requirement ratio

on FX deposits.

• Accordingly, FX reserve requirement ratio was increased from

9 % to 9.5 % on April 26, 2010

• Increase in the interest rate on FX liability facilities (depending

on the developments in global interest rates)

• Discontinuation of the intermediary role in the FX depo market

and reduction in the maturity of the FX depo facility from 3

months to one week (after assessing the impact of exit

strategies of other central banks).

28

Example: Liquidity Provided to the Banking System and Central Bank Operations During The Implementation of Exit Strategy

Source: CBT

Exit Strategy – Turkish Lira Liquidity

REPO Funding

Drawn from Money Market

NET Open Market Operations

STEP-I STEP-II

Technical Interest Rate Adjustment ProcessApr 15

Initial Stage

We intend to gradually reduce the excess TRY funding in the money market. A slight

increase in one-week repo rates may be observed.

29

In the 2nd stage of our Exit Strategy, we will start using one week repo rate as

our policy rate --- initially set at 50 bp above our O/N borrowing rate. O/N borrowing

and lending rates will not change.

Example: Technical Interest Rate Adjustment – First Step

Technical Interest Rate Adjustment

HourHour

CBT Lending Rate

10:00 16:00 17:00

CBT Borrowing Rate

Interbank Late Liquidity Window

11:00

250 bp

50 bp

200 bp

Late Liquidity Lending Rate

Late Liquidity Borrowing Rate

TCMB POLİTİKA FAİZ ORANIHaftalık Repo İhale Faiz Oranı

CBT POLICY RATEOne Week REPO Auction Interest Rate

30

As the liquidity shortage increases in line with expectations, the margin between

CBT borrowing and one week repo auction rates may be widened. Secondary market

average overnight rate will be targeted to fluctuate around the one week repo auction rate.

Example: Technical Interest Rate Adjustment – Second Step

Technical Interest Rate Adjustment – Second Step

HourHour

CBT Lending Rate

10:00 16:00 17:00

CBT Borrowing Rate

Interbank Late Liquidity Window

11:00

250 bp

50 bp

200 bp

Late Liquidity Lending Rate

Late Liquidity Borrowing Rate

TCMB POLİTİKA FAİZ ORANIHaftalık Repo İhale Faiz Oranı

CBT POLICY RATEOne Week REPO Auction Interest Rate

31

May, 2010

CENTRAL BANK OF THE REPUBLIC OF TURKEY

MACROECONOMIC POLICY CHALLENGES IN TURKEY:

THE POLICY MAKER’S VIEW

Huseyin ZAFER

EXECUTIVE DIRECTOR