1 objectives for the day 1. review dr and cr 2. classify and define elements of the bal/sheet 3....

TRANSCRIPT

1

Objectives for the Day

1. Review Dr and Cr2. Classify and defineelements of the Bal/Sheet3. Compute some basic ratios based on Bal/Sheet

2

Objectives for the Day

4. Explore why and howBalance Sheets of differingindustries may differ.5. Explore some creative accounting on the balancesheet.6. Select day for presentation.

3

Debits and Credits

Chapter 3

4

The Mystery of Dr and Cr

The basic sentence of Accountese is a “journal entry” which uses very easy visuals to tell you what is debited (Left) and what is credited – an Indentation (Right)….Cash $1,000 Accounts Rec $1,000

5

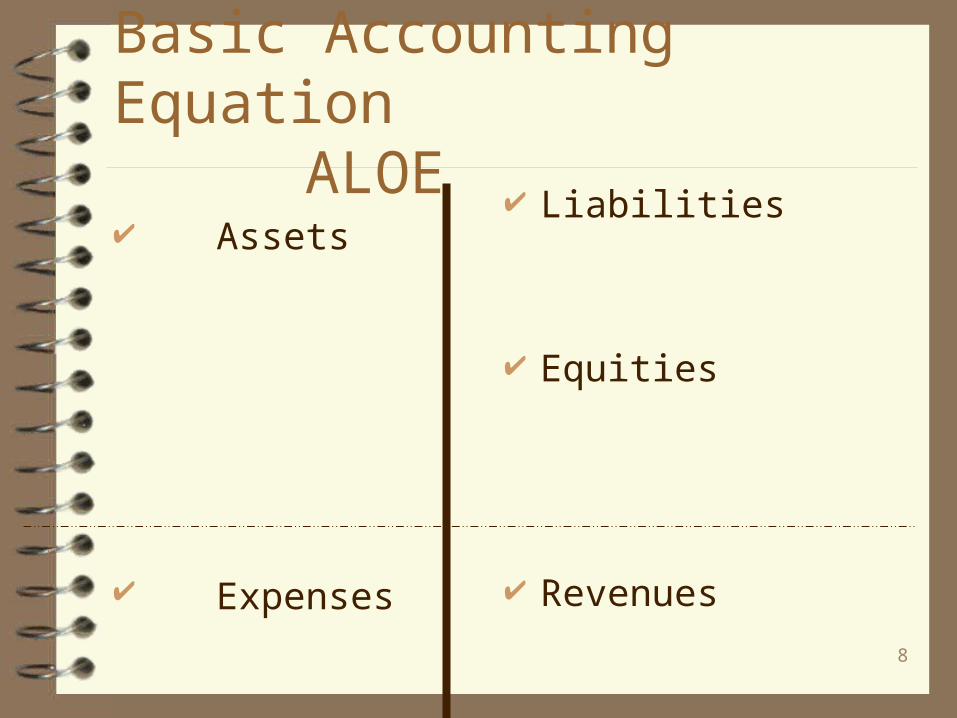

Basic Accounting Equation A LOE Assets

INCREASE DR

Expenses

Liabilities

INCREASE CR Equities

Revenues

6

The Mystery of Dr and Cr

For Assets & Expenses

Dr means INCREASE

Cr means DECREASE

7

The Mystery of Dr and Cr

For Liabilities, Equities & Revenues

Dr means DECREASE

Cr means INCREASE

8

Basic Accounting EquationALOE

Assets

Expenses

Liabilities

Equities

Revenues

9

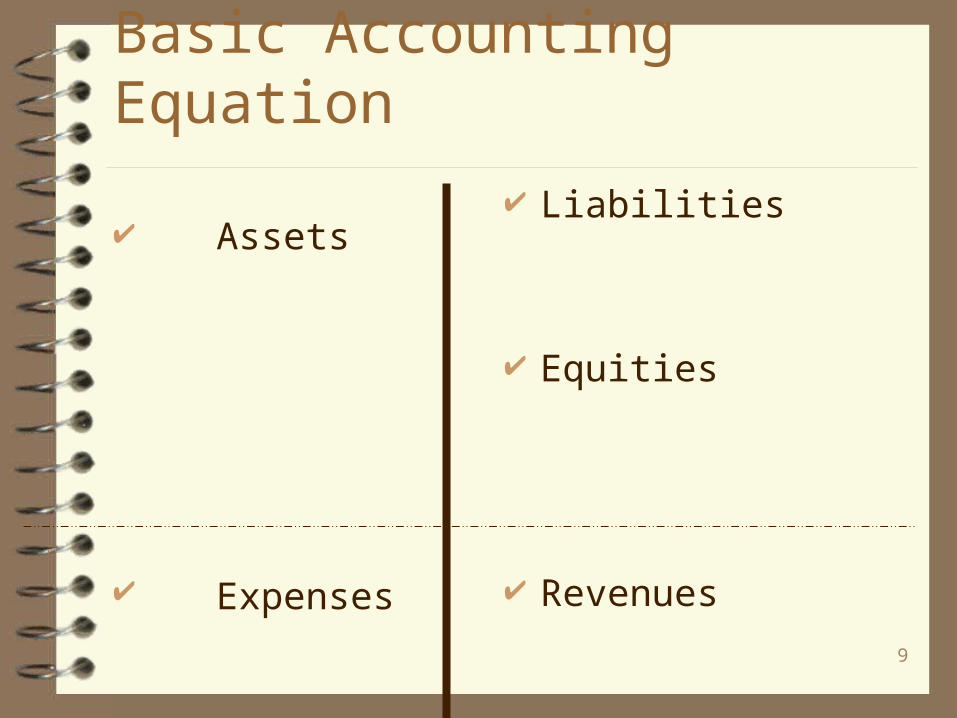

Basic Accounting Equation

Assets

Expenses

Liabilities

Equities

Revenues

10

The Balance Sheet

Chapter 4

11

Assets: A Company’s Resources

Assets are the

resources a company

owns or controls.

12

Assets: A Company’s Resources

Basic Rule: Assets are recorded at acquisition cost (also called Historical cost).

Acquisition cost includes all costs to acquire the asset and get it ready for its intended use.

13

Why does Valuation change? And why does it matter?

Acquisition IS Fair Value at the time an asset is acquired…but values may change. Valuation is the recognition of that fact. Important because..... Usually affects Income Can be very large in scope.

14

Balance Sheet: Current Assets

Assets the company expects to sell or

consume during the next year

15

Balance Sheet: Current Assets

1.Cash

2. S. T. Investments

3. Accounts Receivable

16

Balance Sheet: Current Asset Section

•Represents sales payments that are due after the goods are delivered and the customer is billed

•Amounts owed to the company by customers

Accounts

Receivable

17

Balance Sheet: Current Asset Section

Valuation: Net Realizable Value.

An allowance is deducted from accounts receivable to show the portion that is estimated to be uncollectible.

AccountsReceivable(lessallowance)

18

Balance Sheet: Current Asset Section

The aggregate cost of salable merchandise owned by the company that is available to meet customer demands. Also materials to be used to mfg goods or provide services

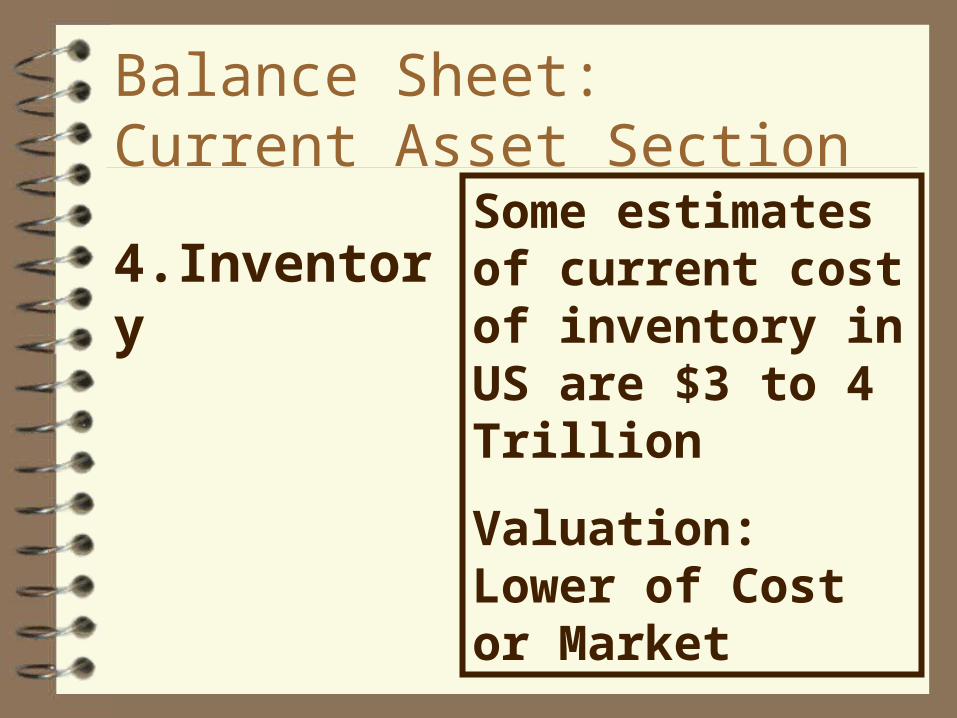

4.Inventory

19

Balance Sheet: Current Asset Section

Some estimates of current cost of inventory in US are $3 to 4 Trillion

Valuation: Lower of Cost or Market

4.Inventory

20

Balance Sheet: Current Asset Section

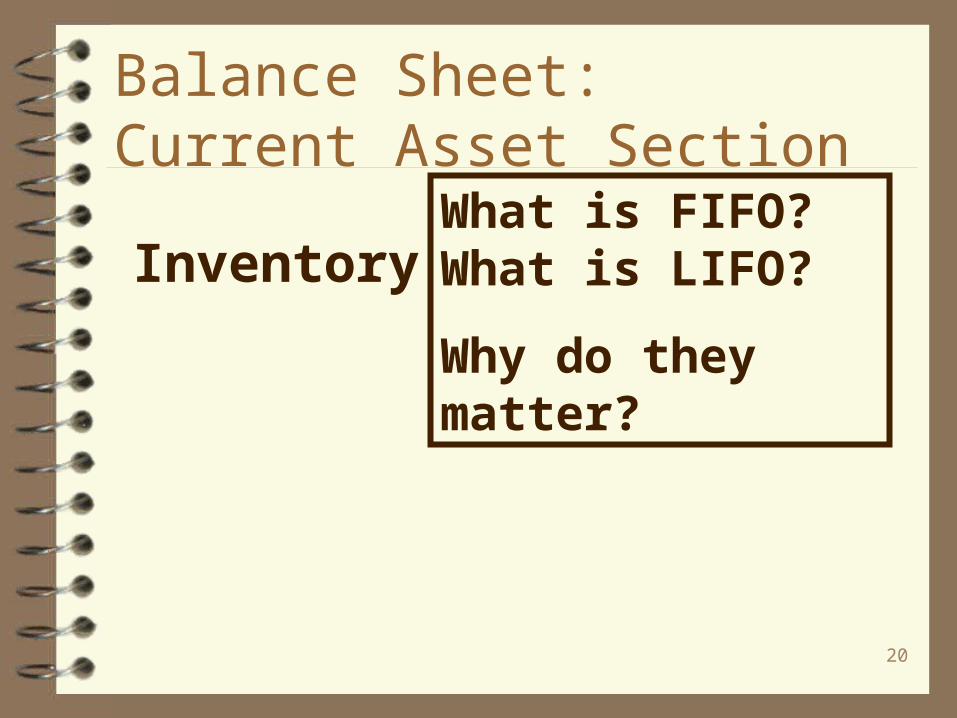

What is FIFO? What is LIFO?

Why do they matter?

Inventory

21

Balance Sheet: Current Asset Section

Expenditures for the

prepayment of items

such as rent, insurance, or

taxes.

5. PrepaidExpenses

22

NoncurrentNoncurrent Assets – Tangible or Fixed

Examples include:

Land

BuildingsEquipmentDelivery TrucksComputers

23

Tangible Assets - Depreciation

The cost of all long-term tangible assets except Land is charged (i.e.

expensed or debited) to net income over its

estimated useful life.

24

Tangible Assets - Depreciation

The entry requires a debit to Depreciation Expense and a credit

to a contra-asset called Accumulated Depreciation.

25

Tangible Assets - DepreciationDespite the term “Net BookValue” we consider depreciationa cost allocation and NOT an attempt to show current (fair)value.

26

Impairment

If asset declines in value below its carryingvalue, it should be writtendown and a loss should betaken.

27

Noncurrent Assets – Investments

Investments in other

companies’ stock or

bonds that will be

maintained for longer than the

coming year

28

Noncurrent Assets – Investments in AffiliatesReporting depends on theextent of ownership.You may see Minority Interestbeing subtracted because theentire sub’s results were included, but reporting co.does not own 100%.

29

Noncurrent Assets - Intangibles

Economic resources that lack physical

substance, such as

patents and copyrights.

30

Noncurrent Assets - Intangibles

The equivalent of depreciation is used…it has another name when we referto Intangible assets – Amortization.

Valuation is Net Book Valueunless an impairment occurs.

31

Noncurrent Assets – Intangibles -- Goodwill

Goodwill is the excess onecompany pays to acquireanother company beyondthe current market valueof the identifiable assetsof the acquired company.

32

Noncurrent Assets – Intangibles - Goodwill

Goodwill was amortizeduntil July of 2001.Now an impairment testmust be used.

33

Noncurrent Assets – Intangibles - Goodwill

Just how good isGoodwill?

Look at World.Com’srecent announcementregarding Goodwill.

34

What is missing?

Human beings aresometimes said to bea company’s most importantasset…..

35

Another way to thinkof this issue is that a) allocating HISTORICAL COST andb) recording current VALUE are NOT compatible goals...

Relevance and Reliability

36

Buckminster Fuller’s dictum

No such thing as a free lunchapplies to assets.

Assets - a key principle

37

Liabilities: A Company’s Obligations

Two categories:

1. Current

2. Noncurrent

38

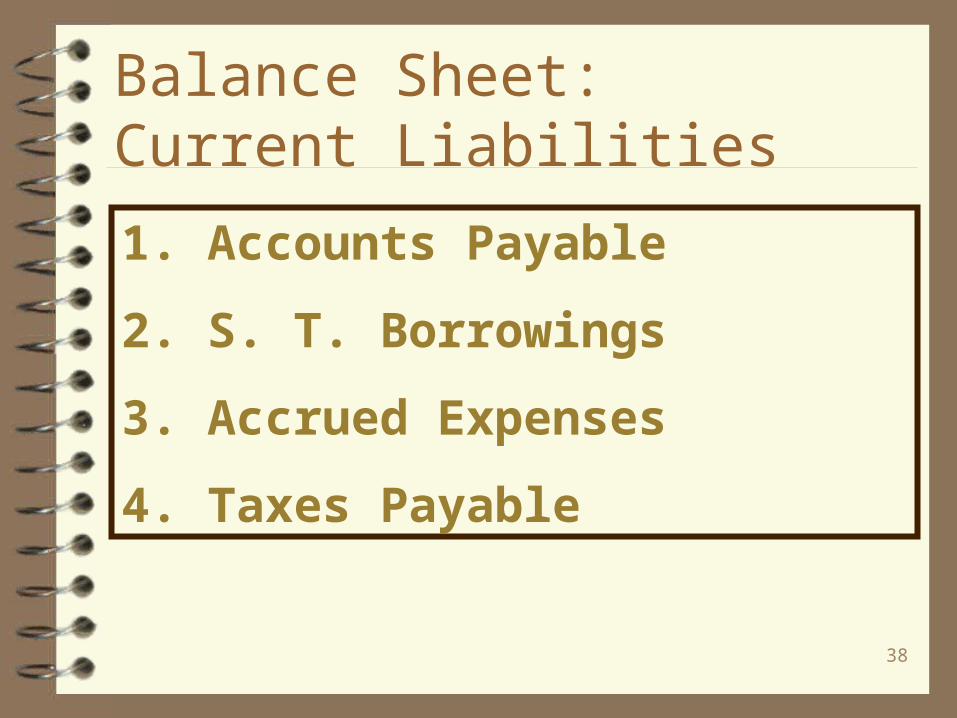

Balance Sheet: Current Liabilities

1. Accounts Payable

2. S. T. Borrowings

3. Accrued Expenses

4. Taxes Payable

39

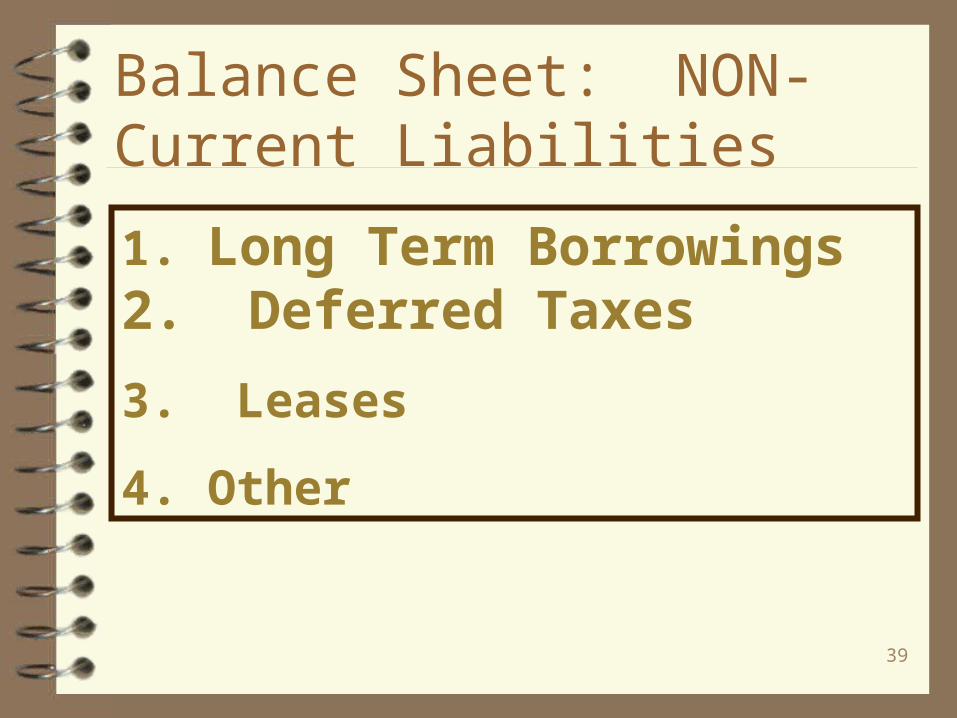

Balance Sheet: NON-Current Liabilities

1. Long Term Borrowings2. Deferred Taxes

3. Leases

4. Other

40

Long Term Liabilities

What you don’t see can hurt you…..issue of Capital versus operating leases.

41

Long Term Liabilities

Far more dangerous and more creative is what Enron used….

Special Purpose Entities…. i.e. the company was essentially borrowing long-term but found ways to avoid showing that debt on the balance sheet.

42

Shareholders’ Equity: The Owners’ Investment in a Company1.Capital Stock

CommonPreferred

2.Additional Paid in Capital3.Treasury Stock4.Retained Earnings5.Comprehensive Income

43

+ = ??

We lack a commonly valueddenominator…..

44

What are likely results of using a variety of valuation methods on interpreting financial statements?

Meaning of the Balance Sheet

45

Analyzing Financial Statements Ratio Analysis

– Examination of the relationships between pieces of information for a given accounting period

– Double entry accounting (using Dr and Cr) means that we should see relationships among various accounts in the balance sheet and the income statement.

– Cash Flow Statement and Equity statement are not generated directly by journal entries…so we tend not to use ratios as much to analyze them.

46

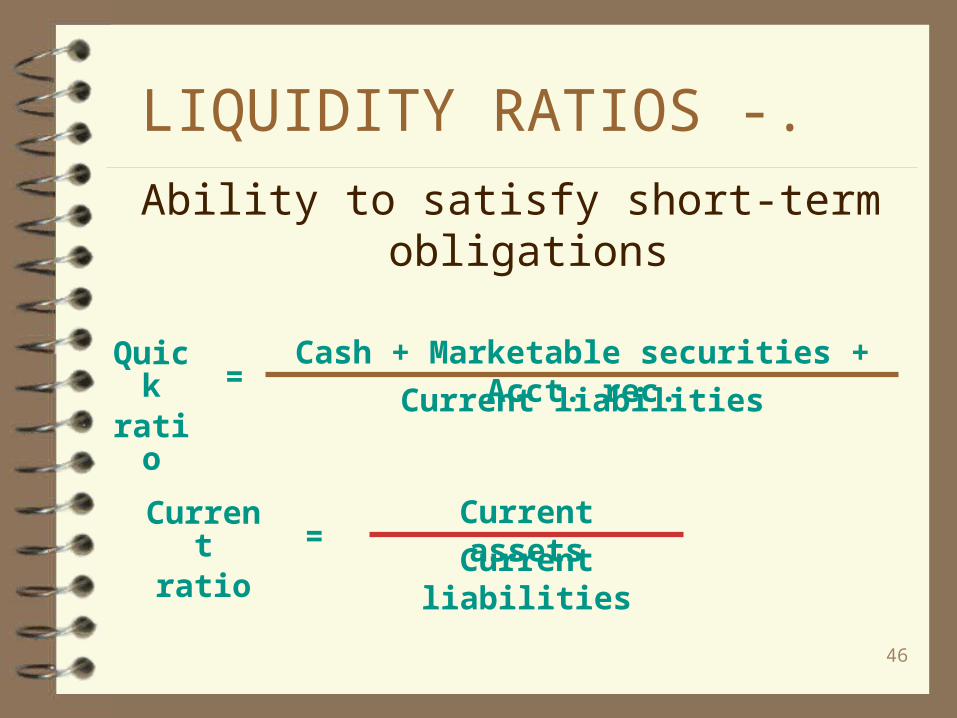

LIQUIDITY RATIOS -.

Ability to satisfy short-term obligations

Quickratio =

Cash + Marketable securities + Acct. rec.

Current liabilities

Currentratio =

Current assets

Current liabilities

47

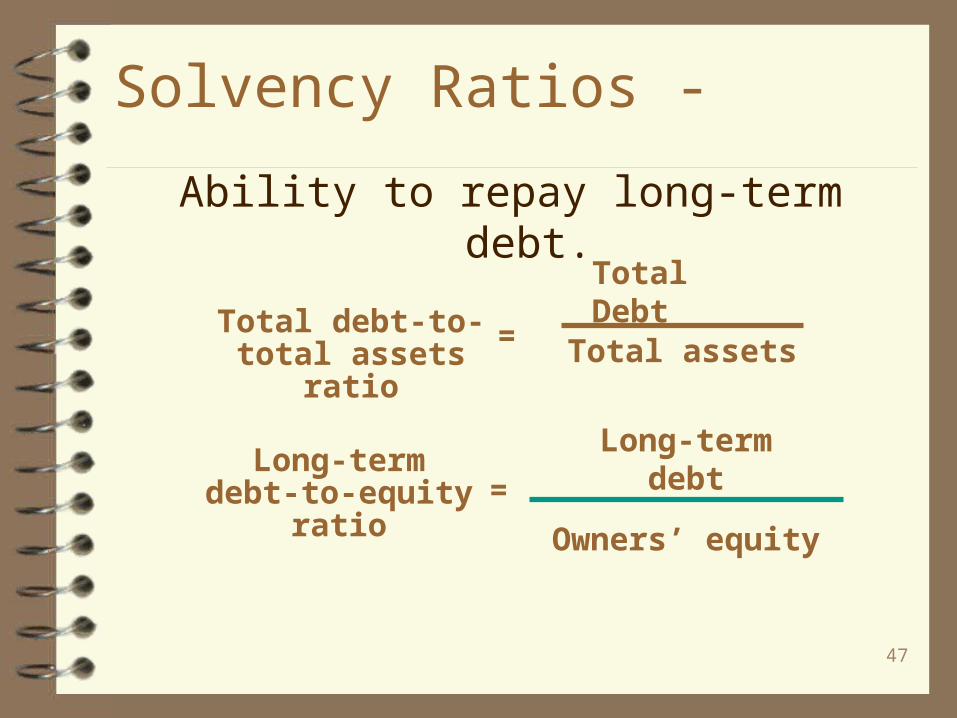

Solvency Ratios -

Ability to repay long-term debt.

Total debt-to-total assets ratio

= Total assets

Long-term debt-to-equity ratio =

Long-term debt

Owners’ equity

Total Debt

48

Solvency Ratios -

Ability to repay long-term debt.

Times-interest-earned ratio =

Interest Expense

Net income before income tax

Interest Expense+

Numerator called EBIT

49

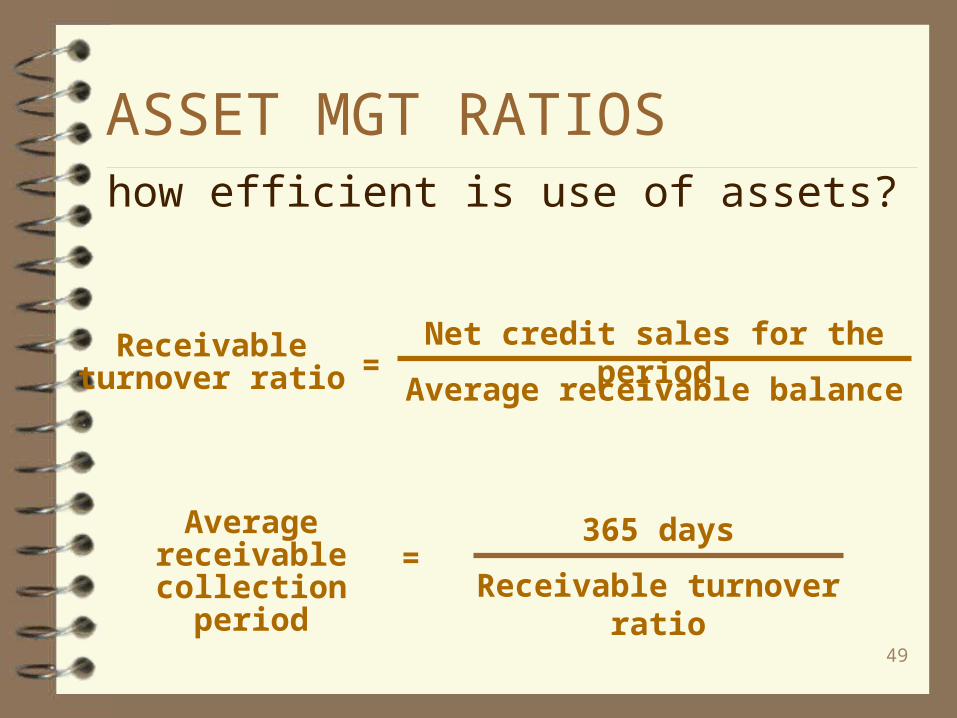

ASSET MGT RATIOShow efficient is use of assets?

Receivable turnover ratio =

Net credit sales for the period

Average receivable balance

Average receivable

collection period=

365 days

Receivable turnover ratio

50

how efficient is use of assets?

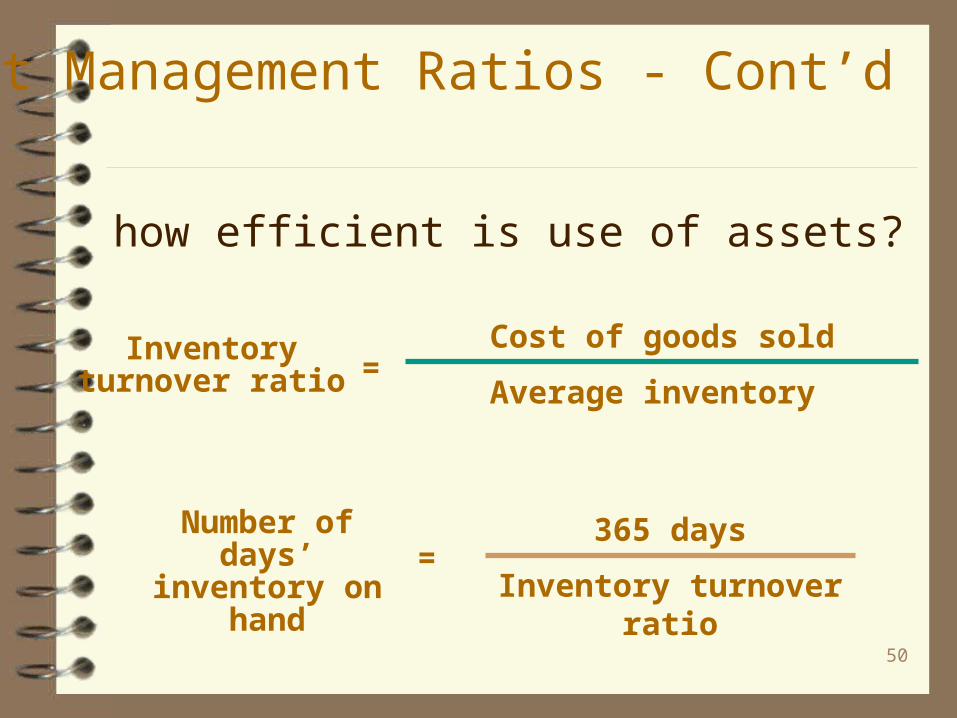

Number of days’ inventory on

hand=

365 days

Inventory turnover ratio

Inventory turnover ratio =

Cost of goods sold

Average inventory

Asset Management Ratios - Cont’d .

51

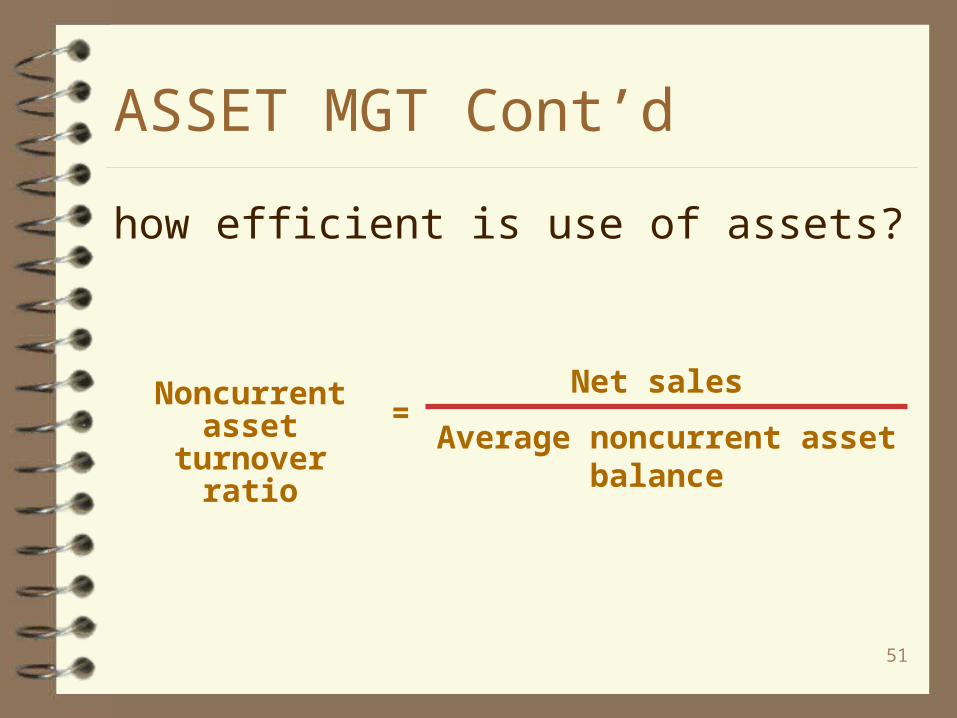

ASSET MGT Cont’d

how efficient is use of assets?

Noncurrent asset turnover

ratio

=Net sales

Average noncurrent asset balance

52

Analyzing Financial StatementsBeyond ratios….. Trend Analysis

– Examination of a company’s numbers over time

Common-size Financial Statements– Expressing all amounts in the financial

statements as a percentage of a base number (Usually total assets or total sales)

53

For Next Time…...

1.Do Homework2. Check out the

business press3. Select your company and industry if not yet done.

54

For Next Time…...

4. Read Chapter 5 andAOL case, which is on Web.

55

What are likely results of using a variety of valuation methods on interpreting financial statements?

Meaning of the Balance Sheet

56

+ = ??

We lack a commonly valueddenominator…..

57

Why do Assets Matter?

1. Valuations directly affect income.E.g. Accts Rec. allowance is Cr and Bad Debt Expense is Dr.

2.The non-current ones are significant for future costs.

58

Creative Accounting 101

59

How to be Creative with?

Assets are one paletteupon which people canbecome creative…a) recognize revenues inadvance & a RECEIVABLEis on the Balance sheet -Halliburton Corporation.

60

b) postpone costs….items that should be expensed

are capitalized (i.e.shown as a Non-current asset). What is

the effect onCurrent Income?

How to be Creative with?

61

1. Accounts Receivable when Allowance

2. Sales and A/R

Or Sales and A/R

Red Flags

62

3. Sales when Inventory

4. Debt and Assets

5. Other

Red Flags continued

63

6. Goodwill

7. Given my skepticism about Goodwill….

Red Flags continued