1 omb update office of federal financial management office of management and budget northern...

TRANSCRIPT

1

OMB Update

Office of Federal Financial Management

Office of Management and Budget

Northern Virginia AGA - Spring TrainingMarch 24, 2015

2

Internal Controls• 1981/1982/1983 –

− OMB Issued Circular No. A-123, Internal Control Systems and Internal Control Guidelines− Federal Managers Financial Integrity Act

• 1986 – OMB Required Management Control Plans to guide efforts

• 1995 – OMB updated A-123, Management Accountability and Control to reflect GPRA, CFO Act, IG Act

• 2004 – OMB updated A-123, Management’s Responsibility for Internal Control and added Appendix A, Internal

Control Over Financial Reporting

• OMB’s vision for 2015 Update – transform and evolve existing internal control compliance frameworks so that it creates a more value added, integrated, risk based, and less burdensome set of requirements for agencies. The revised guidance will:− Clarify technical terminology to help program managers better understand and implement internal controls− Introduce ERM concepts as defined by the COSO framework− Replace “check the box” compliance approach with risk management-based approaches to support agency

missions− Streamline assurance statement reporting− Build on successful implementation of internal controls over financial reporting− Be put out for comment in Spring 2015 with an implementation date of 2016

ERM and Internal Controls

3

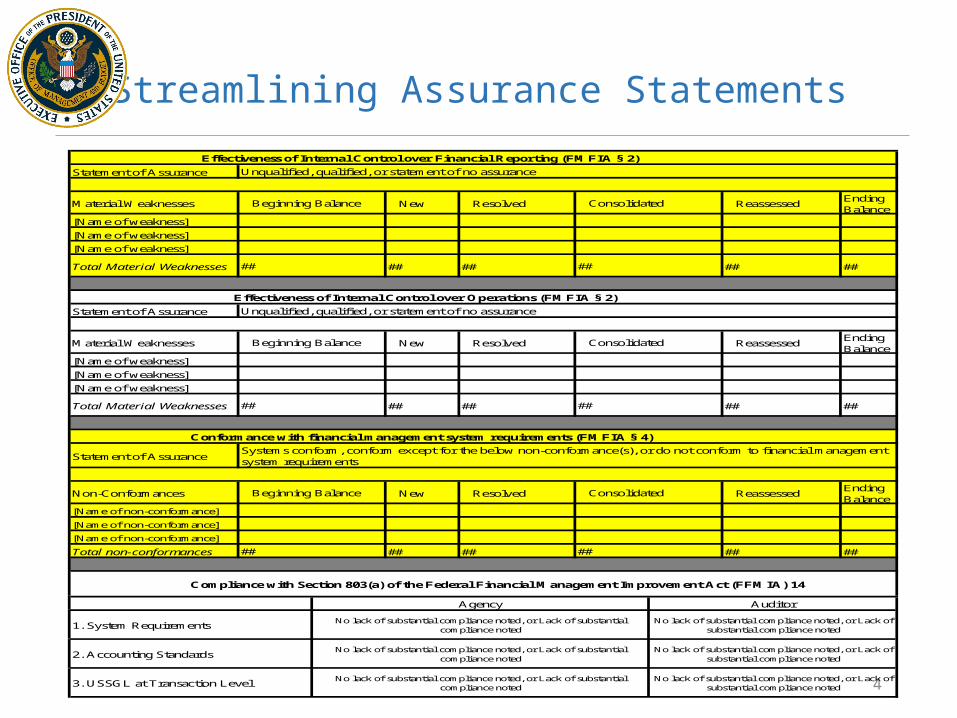

Streamlining Assurance Statements

4

Statement of Assurance

Material Weaknesses New Resolved ReassessedEnding Balance

[Name of weakness]

[Name of weakness]

[Name of weakness]

Total Material Weaknesses ## ## ## ##

Statement of Assurance

Material Weaknesses New Resolved ReassessedEnding Balance

[Name of weakness]

[Name of weakness]

[Name of weakness]

Total Material Weaknesses ## ## ## ##

Statement of Assurance

Non-Conformances New Resolved ReassessedEnding Balance

[Name of non-conformance]

[Name of non-conformance]

[Name of non-conformance]

Total non-conformances ## ## ## ##

2. Accounting StandardsNo lack of substantial compliance noted, or Lack of substantial

compliance notedNo lack of substantial compliance noted, or Lack of

substantial compliance noted

3. USSGL at Transaction LevelNo lack of substantial compliance noted, or Lack of substantial

compliance notedNo lack of substantial compliance noted, or Lack of

substantial compliance noted

Agency Auditor

1. System RequirementsNo lack of substantial compliance noted, or Lack of substantial

compliance notedNo lack of substantial compliance noted, or Lack of

substantial compliance noted

## ##

Compliance with Section 803(a) of the Federal Financial Management Improvement Act (FFMIA) 14

Beginning Balance Consolidated

## ##

Conformance with financial management system requirements (FMFIA § 4)

Systems conform, conform except for the below non-conformance(s), or do not conform to financial management system requirements

Effectiveness of Internal Control over Operations (FMFIA § 2)

Unqualified, qualified, or statement of no assurance

Beginning Balance Consolidated

## ##

Effectiveness of Internal Control over Financial Reporting (FMFIA § 2)

Unqualified, qualified, or statement of no assurance

Beginning Balance Consolidated

Additional Considerations

• Service Organizations

• Internal Controls in Disaster Situations

• Fraud

• Internal Controls over Financial Assistance (i.e., Grants)

5

6

Improper Payments - Brief History

• November 2002 – Improper Payments Information Act (IPIA)− Created basic framework for identifying and reporting improper payments

• November 2009 – Executive Order 13520

− Improved agency accountability− Increased transparency

• July 2010 – Improper Payments Elimination and Recovery Act (IPERA)

− Put into law specific thresholds for identifying high-risk programs− Strengthened corrective action plans− Expanded payment recapture audits− Established annual OIG compliance reviews

• January 2013 – Improper Payments Elimination & Recovery Improvement Act (IPERIA)

− Codified EO 13520 requirements− Improved agency estimation and recovery of improper payments− Reinforced and accelerated the Administration’s “Do Not Pay” efforts

7

A-123 Appendix C Update

• Vision: transform improper payment compliance framework to create a more unified, comprehensive, and less burdensome set of requirements for agencies and OIGs

• IPERIA required OMB to issue new guidance—we approached it as an opportunity to overhaul Appendix C of OMB Circular A-123

• Process: as we drafted the new Appendix C, we had to consider the following:

– The three statutes and the Executive Order

– Previous Appendix C version (M-11-16)

– Input from agencies, OIGs, GAO, and OMB

8

New Appendix C Highlights

• The updated guidance reconciles IPERIA requirements that are identical to requirements from EO 13520

• Consolidates and streamlines reporting requirements for agencies and OIGs– Agencies can incorporate most of their reporting into AFR or PAR– OIGs for agencies with high-priority programs are no longer required to issue

separate reports under EO 13520 and IPERA—one report will suffice

• Provides a more detailed categorization of improper payments

• Adds an internal control framework for addressing improper payments

• Provides guidance to agencies—as required by IPERIA—to strengthen the statistical validity of estimates and include payments to Federal employees in the definition of improper payments, among other things

9

New Improper Payment Categories

Overpayments Underpayments

1

2

Death Data 3

Financial Data 4

Excluded Party Data 5

Prisoner Data 6

Other Eligibility Data (explain) 7

Federal Agency 8

State or Local Agency 9

Other Party (e.g., participating lender, health care provider, or any other organization administering Federal dollars)

10

11

12

13

A B

Other Reason (explain)

Medical Necessity

Failure to Verify:

Administrativeor ProcessError Made by:

Inability to Authenticate Eligibility

Insufficient Documentation to Determine

Type of Improper Payment

Reason for Improper Payment

Program Design or Structural Issue

• Previously only three categories; not very useful

• New guidance establishes new categories for reporting improper payments

• Provides more granularity on estimates, leading to:– More effective

corrective actions at the program level

– More focused strategies for reducing improper payments at the government-wide level

– Better communication about the nature of improper payments

10

• We are conducting an analysis to identify program-specific corrective actions with the highest return-on-investment or potential for substantially reducing improper payments

• Questions we are interested in:

• Which current corrective actions are the most effective in reducing improper payments in your programs?

• Could you list one or two things that your programs are not already doing (but could realistically do) that would lead to a significant decrease in improper payments?

• What, if any, are the barriers preventing your agency from taking these actions, and what would it take to overcome those barriers?

• If you implemented these actions, by how much could the improper payment rate go down for your programs?

• How has your agency advanced data analytics and improved technology to prevent and reduce improper payments ?

Corrective Actions

11

Internal Control over Improper Payments

Internal Control Standards Program A Program B Program C Program D Program E

Control Environment 3 2 2 4 1Risk Assessment 4 1 4 4 1Control Activities 4 3 2 2 2Information and Communication 3 1 3 1 2Monitoring 2 1 4 3 1

Legend:4 = Sufficient controls are in place to prevent improper payments3 = Controls are in place to prevent improper payments but there is room for improvement2 = Minimal controls are in place to prevent improper payments1 = Controls are not in place to prevent improper payments

• Agencies reporting improper payments will summarize the status of internal control over improper payments in their AFR or PAR

• Purpose is to provide a thoughtful analysis linking agency efforts in establishing internal controls with reported improper payment rates

DATA Act Main Update Overview

• OMB and Treasury are working in partnership to implement the DATA Act

• Today’s presentation:• Context of Federal spending transparency• Overview of the DATA Act• Progress thus far• Next steps

12

13

• Federal Funding Accountability and Transparency Act (FFATA)

• Recovery Act• Government Accountability and Transparency

Board (GATB)• Data Accountability and Transparency Act (DATA

Act)

Federal Spending Transparency History

• Purpose: to establish government-wide financial data standards and increase the availability, accuracy, and usefulness of Federal spending information.

• Passed Congress on April 28. Signed into law on May 9, 2014 (P.L. 113-101).

• Amends the Federal Funding Accountability and Transparency Act (FFATA) to require full disclosure of Federal agency expenditures.

• It also requires the development of Government-wide data standards, takes steps to simplify financial reporting, and improves the quality of the spending data.

14

DATA Act Summary

15

Data-centric • Avoid massive system changes, focus on managing data

Incremental • Release data as it becomes available

Reuse• Maximize and leverage use of existing processes and investments

Collaborative • Feedback drives improvements

Iterative/Agile• Conduct many small scale pilots

DATA Act Implementation Approach

Accomplishments-to-date Assumed program responsibility over USAspending.gov Successfully piloted “Intelligent Data” prototype Conducted “Award ID linkage” feasibility study

Vision and Goals

16

VisionProvide reliable, timely, secure, and consumable financial management data for the purpose of promoting transparency, facilitating better decision making, and improving operational efficiency.

Better Data, Better Decisions, Better GovernmentGoals Capture and make available financial management data to enable the data consumers to

follow the complete life cycle of Federal spending -- from appropriations to the disbursements of grants, contracts, and administrative spending

Standardized information exchanges – definitions and format – to enable timely access to discoverable and reusable detail transaction level data

Congress

BudgetFormulation

BudgetExecution

Award

Payment

Appropriation

Apportionment

Warrant

Allotment (Allocation)

Commitment

Obligation

Disbursement

Receipts/Financing

How much money did Congress authorize the government to spend?

What programs, projects, and activities did Congress fund?

OMB, Treasury, and Agency

How did the President, through the Executive Branch, allocate and monitor the funding to ensure that programs comply with spending limits and use funds only for the purposes authorized by Congress?

Agency

What goods and services did the government purchase, for what reason, and from who?

What grants and loans did the government make, for what reason, and for who?

Treasury,Agency

What was the amount, payment date, and who was the recipient of the payment?

Treasury

How much did revenue did the government raise and how much is the government borrowing?

360 Spending Transparency

17

DATA Act in Context of Spending Life Cycle

Appropriation

Apportionment

Allotment (Allocation)

Commitment

Obligation

Payment

360 Spending Life Cycle

DATA Act

FFATA (USAspending.gov)Award

18

Receipts/Financing

19

Data Definition Standards

Accomplishments-to-date Compiled list of FFATA and DATA Act elements which must be defined according to DATA Act Established Interagency Advisory Committee (IAC) to coordinate cross-community

collaboration within Federal government

Importance• Other elements of DATA Act are dependent on data standards• Effects all stakeholders and downstream recipients of Federal funds

Goals

Standardize data definitions – collaborate with Federal and non-Federal stakeholders to define common data elements across communities

Look at industry standards – during implementation, carefully examine common practices and uses to maximize positive impact

Consider implications – use collaboration tools and outreach processes to understand and consider potential implications for stakeholders in their future reporting and compliance based on standards

• Requires ongoing high level support in multiple sectors to push for transformational changes and innovative thinking

• Short implementation timeline – requires fast, early action and reporting on results

• Limited resources – no additional funding for implementation

• Requires collaboration and active participation across federal communities, including procurement, grants, financial management, budget

• Diverse and broad set of stakeholders including, congress, state & local governments, private industry, general public, transparency advocacy groups, and international community

20

Challenges

• GitHub page: http://fedspendingtransparency.github.io/

• Town Hall last Fall – all presentations on GitHub

• Speaking engagements and trainings such as today’s discussion

• Collaboration with non-Federal partners

• Future webcasts about DATA Act implementation and/or DATA Act section 5 pilot

21

Stakeholder Engagement

Next Steps

• Finalize the plan to implement the DATA Act

• Consult with public and private stakeholders in establishing the data standards

• Standardize the data element definitions

• Develop a blueprint of the data elements based on the standard definitions

• Continue pilot efforts on data exchange standards and publication options, and on reducing reporting burden

• Upcoming Dates:

• March 27, 2015: Webcast on DATA Act implementation

• March 20 and 27, 2015: Updated information posted on GitHub

• April 1, 2015: Webcast on Section 5 Pilot

• May 2015: OMB and Treasury issue guidance on data definitions and exchange

• May 2015: Section 5 pilot is launched 22

♫ Are You Ready for This ? The New Uniform Guidance

2 CFR 200

Guidance Reform History

Nov. 2009: Executive Order: Reduce

Improper Payments

Feb 2012: Advance Notice of Proposed

Guidance (public comments)

Dec 2013: Final Uniform Guidance

† April 2013

December 2013: Uniform Guidance Published

June 2014: Agencies Submit Draft Rules to OMB,

Continued Outreach on Implementation

December 2014: Final Guidance Effective,

Baseline Metrics Collected, Case Studies of Best Practices Published

Guidance Reform History

Fall 2014: Metrics, Additional FAQs and Webcast

Eliminating Duplicative and Conflicting Guidance

AwardsReceiv

ed

•A-102 & A-89•A-87•A-133 &A-50Subawar

ds to universiti

es

•A-110•A-21Subawar

ds to nonprofi

ts

•A-110•A-122

INSERT YOUR STATE OR AGENCY

HERE

Now: All OMB guidance streamlined in 2 CFR 200.

Then:

2 CFR 200 -Basic Layout

• 6 Subparts A through F• Subpart A, 200.XX – Acronyms & Definitions• Subpart B, 200.1XX – General• Subpart C, 200.2XX – Pre Award - Federal• Subpart D, 200.3XX – Post Award – Recipients• Subpart E, 200.4XX – Cost Principles • Subpart F, 200.5XX – Audit

• 11 Appendices - I through XI

Top Ten Impact Changes

• 200.1 through 99 Standard Definitions• 200.205, Review of risk of applicants

• Must have framework for evaluating risks• Should consider financial stability, performance

history, audit reports

• 200.314, Supplies (computing devices)• 200.320, Procurement Standards• 200.331, Requirements for pass-through entities

Top Ten Impact Changes

• 200.407, Prior Written Approval (22 items)• 200.413, Direct Costs• 200.414, Indirect Costs

• Must accept approved negotiated rates (some exceptions)• 10% of MTDC de minimis IDC• One time four-year extension of current approved rate (final and pre-

determined rates only)

• 200.430, Compensation – Personal Services • 200.5XX, Single Audits

• Higher Threshold (200.501)• Better Transparency (200.512)• More Focus on Risk (200.518)

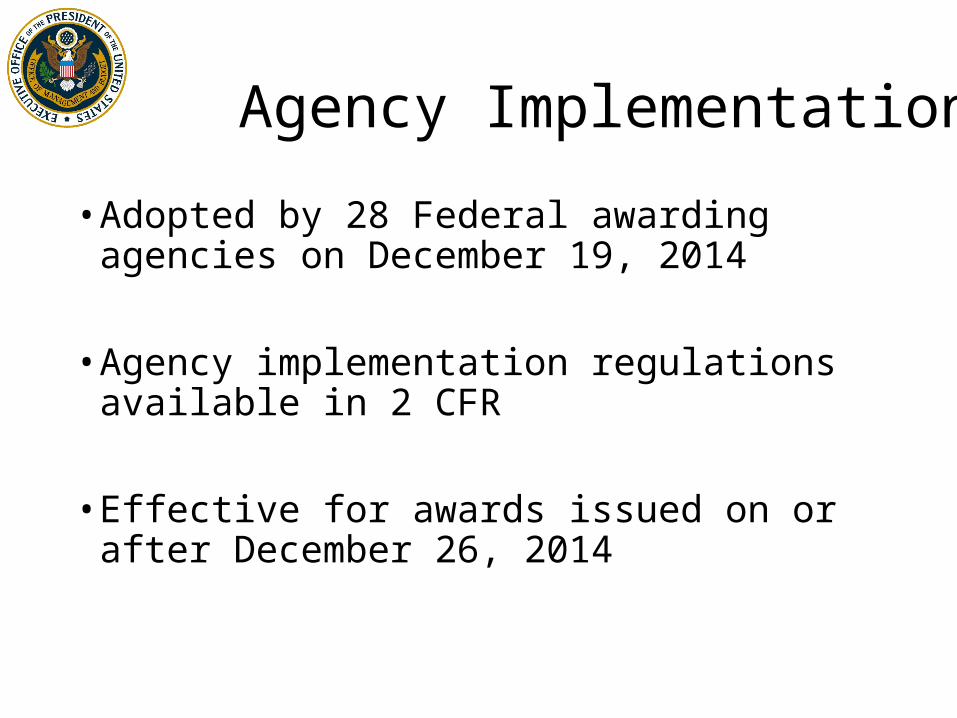

Agency Implementation

• Adopted by 28 Federal awarding agencies on December 19, 2014

• Agency implementation regulations available in 2 CFR

• Effective for awards issued on or after December 26, 2014

Resources

• The COFAR website is available at: https://cfo.gov/cofar/

• Includes:• FAQs• Webcasts• Crosswalk to agency exceptions and additions

“I like the dreams of the future better than the history of the past…” T. Jefferson