1. pre-shipment export credit - reserve bank of india · pdf file · 2004-04-281....

TRANSCRIPT

1. PRE-SHIPMENT EXPORT CREDIT

1.1 Rupee Pre-shipment Credit/Packing Credit

1.1.1 Definition

'Pre-shipment/Packing Credit' means any loan or advance grantedor any other credit provided by a bank to an exporter for financing thepurchase, processing, manufacturing or packing of goods prior toshipment, on the basis of letter of credit opened in his favour or infavour of some other person, by an overseas buyer or a confirmed andirrevocable order for the export of goods from India or any otherevidence of an order for export from India having been placed on theexporter or some other person, unless lodgement of export orders orletter of credit with the bank has been waived.

1.1.2 Period of Advance

(i) The period for which a packing credit advance may be given bya bank will depend upon the circumstances of the individualcase, such as the time required for procuring, manufacturing orprocessing (where necessary) and shipping the relative goods. Itis primarily for the banks to decide the period for which apacking credit advance may be given having regard to thevarious relevant factors so that the period is sufficient toenable the exporter to ship the goods .

(ii) If pre-shipment advances are not adjusted by submission ofexport documents within 360 days from the date of advance, theadvances will cease to qualify for concessive rate of interest tothe exporter ab initio.

(iii) RBI would provide refinance only for a period not exceeding180 days.

1.1.3 Disbursement of Packing Credit(i) Ordinarily, each packing credit sanctioned should be maintained

as separate account for the purpose of monitoring period ofsanction and end-use of funds.

(ii) Banks may release the packing credit in one lumpsum or instages as per the requirement for executing the orders/LC.

(iii) Banks may also maintain different accounts at various stages ofprocessing, manufacturing, etc. depending on the types of goodsto be exported, e.g. hypothecation, pledge, etc., accounts andmay ensure that the outstanding balance in accounts are adjustedby transfer from one account to the other and finally by proceedsof relative export documents on purchase, discount, etc.

(iv) Banks should continue to keep a close watch on the end-use ofthe funds and ensure that credit at lower rates of interest is usedfor genuine requirements of exports. Banks should also monitorthe progress made by the exporters in timely fulfilment ofexport orders.

1.1.4 Liquidation of Packing Credit

(i) GeneralThe packing credit /pre-shipment credit granted to an exportermay be liquidated out of proceeds of bills drawn for theexported commodities on its purchase, discount etc. therebyconverting pre-shipment credit into post-shipment credit.Further, subject to mutual agreement between the exporter andthe banker it can also be repaid/prepaid out of balances inExchange Earners Foreign Currency A/c ( EEFC A/c ) as alsofrom rupee resources of the exporter to the extent exports haveactually taken place. If not so liquidated /repaid, banks shouldcharge the rate of interest for ECNOS- pre-shipment asindicated in paragraph 5.2.1(4) from the date of advance.

(ii) Packing credit in excess of export value

(a) Where by-product can be exportedWhere the exporter is unable to tender export bills ofequivalent value for liquidating the packing credit due tothe shortfall on account of wastage involved in theprocessing of agro products like raw cashew nuts, etc.,banks may allow exporters, inter alia, to extinguish theexcess packing credit by export bills drawn in respect ofby-product like cashew shell oil, etc.

(b) Where partial domestic sale is involvedHowever, in respect of export of agro-based products liketobacco, pepper, cardamom, cashew nuts, etc., the exporterhas necessarily to purchase a somewhat larger quantity ofthe raw agricultural produce and grade it into exportableand non-exportable varieties and only the former isexported. The non-exportable balance is necessarily solddomestically. For the packing credit covering such non-exportable portion, banks are required to chargecommercial rate of interest applicable to the domesticadvance from the date of advance of packing credit andthat portion of the packing credit would not be eligible forany refinance from RBI.

(c) Export of deoiled/defatted cakesBanks are permitted to grant packing credit advance toexporters of HPS ground nut and deoiled/defatted cakes tothe extent of the value of raw materials required even thoughthe value thereof exceeds the value of the export order. Theadvance in excess of the export order is required to be

adjusted either in cash or by sale of residual by-product oilwithin a period not exceeding 30 days from the date ofadvance to be eligible for concessional rate of interest.

(iii) Banks have, however, operational flexibility to extend thefollowing relaxations to their exporter clients who have a goodtrack record:(a) Repayment/liquidation of packing credit with proceeds of

export documents will continue; however, this could bewith export documents relating to any other ordercovering the same or any other commodity exported bythe exporter. While allowing substitution of contract inthis way, banks should ensure that it is commerciallynecessary and unavoidable. Banks should also satisfyabout the valid reasons as to why packing credit extendedfor shipment of a particular commodity cannot beliquidated in the normal method. As far as possible, thesubstitution of contract should be allowed if the exportermaintains account with the same bank or it has theapproval of the members of the consortium, if any.

(b) The existing packing credit may also be marked-off withproceeds of export documents against which no packingcredit has been drawn by the exporter. However, it ispossible that the exporter might avail of EPC with onebank and submit the documents to another bank. In view ofthis possibility, banks may extend such facility afterensuring that the exporter has not availed of packing creditfrom another bank against the documents submitted.

(c) These relaxations should not be extended to transactionsof sister/associate/group concerns.

1.1.5 'Running Account' Facility

(i) As stated above, pre-shipment credit to exporters is normallyprovided on lodgement of L/Cs or firm export orders. It isobserved that the availability of raw materials is seasonal insome cases. In some other cases, the time taken for manufactureand shipment of goods is more than the delivery schedule as perexport contracts. In many cases, the exporters have to procureraw material, manufacture the export product and keep the sameready for shipment, in anticipation of receipt of letters ofcredit/firm export orders from the overseas buyers. Havingregard to difficulties being faced by the exporters in availing ofadequate pre-shipment credit in such cases, banks have beenauthorised to extend Pre-shipment Credit ‘Running Account’facility in respect of any commodity, without insisting on priorlodgement of letters of credit/firm export orders, depending onthe bank’s judgement regarding the need to extend such afacility and subject to the following conditions:

(a) Banks may extend the ‘Running Account’ facility only to thoseexporters whose track record has been good as also Export OrientedUnits (EOUs)/Units in Free Trade Zones/ Export Processing Zones (EPZs)and Special Economic Zones (SEZs).

(b) In all cases where Pre-shipment Credit ‘Running Account’ facility hasbeen extended, letters of credit/firm orders should be produced within areasonable period of time to be decided by the banks.

(c) Banks should mark off individual export bills, as and when they arereceived for negotiation/collection, against the earliest outstanding pre-shipment credit on 'First In First Out' (FIFO) basis. Needless to add that,while marking off the pre-shipment credit in the manner indicated above,banks should ensure that concessive credit available in respect ofindividual pre-shipment credit does not go beyond the period of sanctionor 360 days from the date of advance, whichever is earlier.

(d) Packing credit can also be marked-off with proceeds of exportdocuments against which no packing credit has been drawn by theexporter.

(ii) If it is noticed that the exporter is found to be abusing the facility, the facilityshould be withdrawn forthwith.

(iii) In cases where exporters have not complied with the terms and conditions,the advance will attract commercial lending rate ab initio. In such cases, bankswill be required to pay higher rate of interest on the portion of refinance availedof by them from the RBI in respect of the relative pre-shipment credit. All suchcases should be reported to the Monetary Policy Department, Reserve Bank ofIndia, Central Office, Mumbai 400 001 which will decide the rate of interest tobe charged on the refinance amount.

(iv) Running account facility should not be granted to sub-suppliers .

1.1.6 Interest on Packing CreditInterest rate structure and instructions in regard thereto are detailed in paragraph5.

1.1.7 Export Credit against Proceeds of Cheques, Drafts, etc. Representing AdvancePayment for Exports

(i) Where exporters receive direct remittances from abroad by means of cheques,drafts, etc. in payment for exports, banks may grant export credit at concessiveinterest rate to exporters of good track record till the realisation of proceeds ofthe cheque, draft etc. received from abroad, after satisfying themselves that it isagainst an export order, is as per trade practices in respect of the goods inquestion and is an approved method of realisation of export proceeds as perextant rules.

(ii) If, pending compliance with the above conditions, an exporter has beengranted accommodation at normal commercial interest rate, banks may giveeffect to concessive export credit rate retrospectively once the aforesaidconditions have been complied with and refund the difference to the exporter.

1.2 Rupee Pre-shipment Credit to Specific Sectors/Segments

1.2.1 Rupee Export Packing Credit to Manufacturer Suppliers for Exports Routedthrough STC/MMTC/Other Export Houses, Agencies, etc.

(i) Banks may grant export packing credit to manufacturer suppliers who do nothave export orders/letters of credit in their own name, and goods are exportedthrough the State Trading Corporation/Minerals and Metal Trading Corporationor other export houses, agencies, etc.

(ii) Such advances will be eligible for refinance, provided the followingrequirements are complied with apart from the usual stipulations:

(a) Banks should obtain from the export house a letter setting out thedetails of the export order and the portion thereof to be executed by thesupplier and also certifying that the export house has not obtained and willnot ask for packing credit in respect of such portion of the order as is to beexecuted by the supplier.

(b) Banks should, after mutual consultations and taking into account theexport requirements of the two parties, apportion between the two i.e. theExport House and the Supplier, the period of packing credit for which theconcessionary rate of interest is to be charged. The concessionary rates ofinterest on the pre-shipment credit will be available upto the stipulatedperiods in respect of the export house/agency and the supplier puttogether.

(c) The export house should open inland L/Cs in favour of the suppliergiving relevant particulars of the export L/Cs or orders and theoutstandings in the packing credit account should be extinguished bynegotiation of bills under such inland L/Cs. If it is inconvenient for theexport house to open such inland L/Cs in favour of the supplier, the lattershould draw bills on the export house in respect of the goods supplied forexport and adjust packing credit advances from the proceeds of such bills.In case the bills drawn under such arrangement are not accompanied bybills of lading or other export documents, the bank should obtain throughthe supplier a certificate from the export house at the end of every quarterthat the goods supplied under this arrangement have in fact been exported.The certificate should give particulars of the relative bills such as date,amount and the name of the bank through which the bills have beennegotiated.

(d) Banks should obtain an undertaking from the supplier thatthe advance payment, if any, received from the exporthouse against the export order would be credited to thepacking credit account.

1.2.2 Rupee Export Packing Credit to Sub-Suppliers(i) Packing credit can be shared between an Export Order Holder

(EOH) and sub-supplier of raw materials, components, etc. ofthe exported goods as in the case of EOH and manufacturersuppliers, subject to the following:(a) Running Account facility is not contemplated under the

scheme. The scheme will cover the L/C or export orderreceived in favour of Export Houses/Trading Houses/StarTrading Houses, etc. or manufacturer exporters only. Thescheme should be made available to the exporters withgood track record.

(b) Bankers to an EOH will open an inland L/C specifying thegoods to be supplied by the sub-supplier to the EOHagainst the export order or L/C received by him as a part ofthe export transaction. On the basis of such a L/C, the sub-supplier's banker will grant EPC as working capital toenable the sub-supplier to manufacture the componentsrequired for the goods to be exported. On supplying thegoods, the L/C opening bank will pay to the sub-supplier'sbanker against the inland documents received on the basisof inland L/C. Such payments will thereafter become theEPC of the EOH.

(c) It is upto the EOH to open any number of L/Cs for thevarious components required with the approval of hisbanker/leader of consortium of banks within the overallvalue limit of the order or L/C received by him. Takinginto account the operational convenience, it is for the L/Copening bank to fix the minimum amount for opening suchL/Cs. The total period of packing credit availed by the sub-supplier(s), individually or severally and the EOH shouldbe within normal cycle of production required for theexported goods. Normally, the total period will becomputed from the date of first drawal of packing credit byany one of the sub-suppliers to the date of submission ofexport documents by EOH.

(d) The EOH will be responsible for exporting the goods asper export order or overseas L/C and any delay in theprocess will subject him to the penal provisions issuedfrom time to time. Once the sub-supplier makes availablethe goods as per inland L/C terms to the EOH, hisobligation of performance under the scheme will be treatedas complied with and the penal provisions will not beapplicable to him for delay by EOH, if any.

(e) The scheme is an additional window besides the existingsystem of sharing of packing credit between EOH andmanufacturer in respect of exported goods as detailed inparagraph 1.2.1 above. The scheme will cover only thefirst stage of production cycle. For example, amanufacturer exporter will be allowed to open domesticL/C in favour of his immediate suppliers of componentsetc. that are required for manufacture of exportable goods.The scheme will not be extended to cover suppliers of rawmaterials/components, etc. to such immediate suppliers. Incase the EOH is merely a trading house, the facility will beavailable commencing from the manufacturer to whom theorder has been passed on by the Trading House.

(f) EOUs/EPZ/SEZ units supplying goods to anotherEOU/EPZ/SEZ unit for export purposes are also eligiblefor rupee pre-shipment export credit under this scheme.However, the supplier EOU/EPZ/SEZ unit will not beeligible for any post-shipment facility as the scheme doesnot cover sale of goods on credit terms.

(g) The scheme does not envisage any change in the totalquantum of advance or period. Accordingly, the creditextended under the system will be treated as export creditfrom the date of advance to the sub-supplier to the date ofliquidation by EOH under the inland export L/C systemand upto the date of liquidation of packing credit byshipment of goods by EOH and will be eligible forrefinance from RBI by the respective banks for theappropriate periods. It has to be ensured that no doublefinancing of the same leg of the transaction is involved.

(h) Banks may approach the ECGC for availing suitable coverin respect of such advances.

(i) The scheme does not envisage extending credit by a sub-supplier to the EOH/manufacturer and thus, the payment tosub-suppliers has to be made against submission ofdocuments by L/C opening bank treating the payment asEPC of the EOH.

1.2.3 Rupee Pre-shipment Credit to Construction Contractors

(i) The packing credit advances to the construction contractors tomeet their initial working capital requirements for execution ofcontracts abroad may be made on the basis of a firm contractsecured from abroad, in a separate account, on an undertakingobtained from them that the finance is required by them forincurring preliminary expenses in connection with the executionof the contract e.g., for transporting the necessary technical staffand purchase of consumable articles for the purpose ofexecuting the contract abroad, etc..

(ii) The advances should be adjusted within 180 days of the date ofadvance by negotiation of bills relating to the contract or byremittances received from abroad in respect of the contractexecuted abroad. To the extent the outstandings in the accountare not adjusted in the stipulated manner, banks may chargenormal rate of interest on such advance.

(iii) The exporters undertaking project export contracts includingexport of services may comply with the guidelines/instructionsissued by Reserve Bank of India, Exchange ControlDepartment, Central Office, Mumbai from time to time.

1.2.4 Export of Consultancy Services(i) Some of the Indian consultancy firms have taken up export of

consultancy services in connection with the setting up ofindustrial and other projects in foreign countries. Where suchconsultancy services form part of turnkey projects or jointventures set up abroad, banks are considering suitable creditfacilities at the pre-shipment and post-shipment stages. Theexporters may need financial assistance from banks even incases where consultancy services alone are exported,particularly, if no advance payments are received.

(ii) Banks may consider granting suitable pre-shipment creditfacilities against consultancy agreements to consultancy firmsfor meeting the expenses of the technical and other staffemployed for the project and purchase of any materials requiredfor the purpose as well as for export of computer software, bothstandard and custom built software programs, subject to theusual conditions of packing credit scheme.

(iii) While deciding the pre-shipment facilities, advance paymentsreceived against the contract must be taken into account.

(iv) Banks may consider issuing suitable guarantees to exporters ofconsultancy services of high value with large advance payment,taking into account the competence of the firm to undertake theassignment in question and other related aspects.

1.2.5 Export of IT Service and software

Pre-shipment or post-shipment finance can be provided to exportersof IT and software services in case of specific orders from abroad." ITservice" is defined as any service which results from the use of any ITsoftware over a system of IT products for realising value addition.

Various segments of Information Technology and Software Industrycould be broadly classified into four categories.

(ii) The advances should be adjusted within 180 days of the date ofadvance by negotiation of bills relating to the contract or byremittances received from abroad in respect of the contractexecuted abroad. To the extent the outstandings in the accountare not adjusted in the stipulated manner, banks may chargenormal rate of interest on such advance.

(iii) The exporters undertaking project export contracts includingexport of services may comply with the guidelines/instructionsissued by Reserve Bank of India, Exchange ControlDepartment, Central Office, Mumbai from time to time.

1.2.4 Export of Consultancy Services(i) Some of the Indian consultancy firms have taken up export of

consultancy services in connection with the setting up ofindustrial and other projects in foreign countries. Where suchconsultancy services form part of turnkey projects or jointventures set up abroad, banks are considering suitable creditfacilities at the pre-shipment and post-shipment stages. Theexporters may need financial assistance from banks even incases where consultancy services alone are exported,particularly, if no advance payments are received.

(ii) Banks may consider granting suitable pre-shipment creditfacilities against consultancy agreements to consultancy firmsfor meeting the expenses of the technical and other staffemployed for the project and purchase of any materials requiredfor the purpose as well as for export of computer software, bothstandard and custom built software programs, subject to theusual conditions of packing credit scheme.

(iii) While deciding the pre-shipment facilities, advance paymentsreceived against the contract must be taken into account.

(iv) Banks may consider issuing suitable guarantees to exporters ofconsultancy services of high value with large advance payment,taking into account the competence of the firm to undertake theassignment in question and other related aspects.

1.2.5 Export of IT Service and software

Pre-shipment or post-shipment finance can be provided to exportersof IT and software services in case of specific orders from abroad." ITservice" is defined as any service which results from the use of any ITsoftware over a system of IT products for realising value addition.

Various segments of Information Technology and Software Industrycould be broadly classified into four categories.

growing of flowers, grapes, etc., provided banks are in aposition to clearly identify such activities as export-related andsatisfy themselves of the export potential thereof, and theactivities are not covered by direct/indirect finance schemes ofNABARD or any other agency, subject to the normal terms &conditions relating to packing credit such as period, quantum,liquidation, etc.

(iii) Export credit should not be extended for investments, such as,import of foreign technology, equipment, land development, etc.or any other item which cannot be regarded as working capital.

1.2.7 Export Credit to Processors/Exporters-Agri-Export Zones

(i) Government of India have set up Agri- Export Zones in thecountry to promote Agri Exports. Agri- Export Oriented Units(processing) are set up in Agri- Export zones as well as outsidethe zones and to promote such units, production and processingare to be integrated. The producer has to enter into contractfarming with farmers and has to ensure supply of quality seeds,pesticides, micro-nutrients and other material to the group offarmers from whom the exporter would be purchasing theproducts as raw material for production of the final products forexport. The Government, therefore, suggested that such exportprocessing units may be provided packing credit under theextant guidelines for the purpose of procuring and supplyinginputs to the farmers so that quality inputs are available to themwhich in turn will ensure that only good quality crops are raised.The exporters will be able to purchase/import such inputs inbulk which will have the advantages of economies of scale.

(ii) Banks may treat the inputs supplied to farmers by exportersas raw material for export and consider sanctioning the lines ofcredit/export credit to processors/exporters to cover the cost ofsuch inputs required by farmers to cultivate such crops topromote export of agri products. The processor units would beable to effect bulk purchases of the inputs and supply the sameto the farmers as per a pre-determined arrangement.

(iii) Banks have to ensure that the exporters have made therequired arrangements with the farmers and overseas buyers inrespect of crops to be purchased and products to be exportedrespectively. The financing banks will also appraise theprojects in agri export zones and ensure that the tie-uparrangements are feasible and projects would take off within areasonable period of time.

(iv) They have also to monitor the end-use of funds, viz.distribution of the inputs by the exporters to the farmers forraising the crops as per arrangements made by theexporter/main processor units.

(v) They have to further ensure that the final products are exportedby the processors/exporters as per the terms and conditions ofthe sanction in order to liquidate the pre-shipment credit as perextant instructions.

2. POST-SHIPMENT EXPORT CREDIT

2.1 'Post-shipment Credit' means any loan or advance granted or any other creditprovided by a bank to an exporter of goods from India from the date ofextending credit after shipment of goods to the date of realisation of exportproceeds and includes any loan or advance granted to an exporter, inconsideration of, or on the security of any duty drawback allowed by theGovernment from time to time.

2.2 Post-shipment advance can mainly take the form of -

(i) Export bills purchased/discounted/negotiated.

(ii) Advances against bills for collection.

(iii) Advances against duty drawback receivcable from Government.

2.3 Post-shipment credit is to be liquidated by the proceeds of export bills receivedfrom abroad in respect of goods exported.

2.4 Rupee Post-shipment Export Credit

2.4.1 Period

(i) In the case of demand bills, the period of advance shall be theNormal Transit Period (NTP) as specified by FEDAI.

(ii) In case of usance bills, credit can be granted for a maximumduration of 180 days from date of shipment inclusive ofNormal Transit Period (NTP) and grace period, if any.However, banks should closely monitor the need for extendingpost-shipment credit upto the permissible period of 180 daysand they should influence the exporters to realise the exportproceeds within a shorter period.

(iii) 'Normal transit period' means the average period normallyinvolved from the date of negotiation/purchase/discount till thereceipt of bill proceeds in the Nostro account of the bankconcerned, as prescribed by FEDAI from time to time. It is notto be confused with the time taken for the arrival of goods atoverseas destination.

(iv) An overdue bill -(a) in the case of a demand bill, is a bill which is not paidbefore the expiry of the normal transit period, and(b) in the case of a usance bill, is a bill which is not paid onthe due date.

2.4.2 Interest Rate Structure

Interest rate structure on post-shipment credit and instructions inregard thereto are detailed in paragraph 5.

2.4.3 Advances against Undrawn Balances on Export Bills

In export of certain commodities where exporters are required to drawthe bills on the overseas buyer upto 90 to 98 percent of the FOB valueof the contract, the residuary amount being 'undrawn balance' ispayable by the overseas buyer after satisfying himself about thequality/ quantity of goods. Payment of undrawn balance is contingentin nature. Banks may consider granting advances against undrawnbalances at concessional rate of interest based on their commercialjudgement and the track record of the buyer. Such advances are,however, eligible for concessional rate of interest for a maximumperiod of 90 days only to the extent these are repaid by actualremittances from abroad and provided such remittances are receivedwithin 180 days after the expiry of NTP in the case of demand bills anddue date in the case of usance bills. For the period beyond 90 days, therate of interest specified for the category 'ECNOS' at post-shipmentstage may be charged.

2.4.4 Advances against Retention Money

(i) In the case of turnkey projects/construction contracts,progressive payments are made by the overseas employer inrespect of services segment of the contract, retaining a smallpercentage of the progressive payments as retention moneywhich is payable after expiry of the stipulated period from thedate of the completion of the contract, subject to obtention ofcertificate(s) from the specified authority.

(ii) Retention money may also be sometimes stipulated against thesupplies portion in the case of turn-key projects. It may like-wise arise in the case of sub-contracts. The payment of retentionmoney is contingent in nature as it is a defect liability.

(iii) The following guidelines should be followed in regard to grantof advances against retention money:(a) No advances may be granted against retention moneyrelating to services portion of the contract.(b) Exporters may be advised to arrange, as far as possible,provision of suitable guarantees, instead of retentionmoney.

(iv) An overdue bill -(a) in the case of a demand bill, is a bill which is not paidbefore the expiry of the normal transit period, and(b) in the case of a usance bill, is a bill which is not paid onthe due date.

2.4.2 Interest Rate Structure

Interest rate structure on post-shipment credit and instructions inregard thereto are detailed in paragraph 5.

2.4.3 Advances against Undrawn Balances on Export Bills

In export of certain commodities where exporters are required to drawthe bills on the overseas buyer upto 90 to 98 percent of the FOB valueof the contract, the residuary amount being 'undrawn balance' ispayable by the overseas buyer after satisfying himself about thequality/ quantity of goods. Payment of undrawn balance is contingentin nature. Banks may consider granting advances against undrawnbalances at concessional rate of interest based on their commercialjudgement and the track record of the buyer. Such advances are,however, eligible for concessional rate of interest for a maximumperiod of 90 days only to the extent these are repaid by actualremittances from abroad and provided such remittances are receivedwithin 180 days after the expiry of NTP in the case of demand bills anddue date in the case of usance bills. For the period beyond 90 days, therate of interest specified for the category 'ECNOS' at post-shipmentstage may be charged.

2.4.4 Advances against Retention Money

(i) In the case of turnkey projects/construction contracts,progressive payments are made by the overseas employer inrespect of services segment of the contract, retaining a smallpercentage of the progressive payments as retention moneywhich is payable after expiry of the stipulated period from thedate of the completion of the contract, subject to obtention ofcertificate(s) from the specified authority.

(ii) Retention money may also be sometimes stipulated against thesupplies portion in the case of turn-key projects. It may like-wise arise in the case of sub-contracts. The payment of retentionmoney is contingent in nature as it is a defect liability.

(iii) The following guidelines should be followed in regard to grantof advances against retention money:(a) No advances may be granted against retention moneyrelating to services portion of the contract.(b) Exporters may be advised to arrange, as far as possible,provision of suitable guarantees, instead of retentionmoney.

(c) Banks may consider, on a selective basis, granting ofadvances against retention money relating to the suppliesportion of the contract taking into account, among others,the size of the retention money accumulated, its impact onthe liquid funds position of the exporter and the pastperformance regarding the timely receipt of retentionmoney.

(d) The payment of retention money may be secured by L/C orBank Guarantee where possible.

(e) Where the retention money is payable within a period ofone year from the date of shipment, according to the termsof the contract, banks should charge prescribed concessiverate of interest upto a maximum period of 90 days. Therate of interest prescribed for the category 'ECNOS' atpost-shipment stage may be charged for the period beyond90 days.

(f) Where the retention money is payable after a period of oneyear from the date of shipment, according to the terms ofthe contract and the corresponding advance is extended fora period exceeding one year, it will be treated as post-shipment credit given on deferred payment termsexceeding one year, and the rate of interest for thatcategory will apply.

(g) Advances against retention money will be eligible forconcessional rate of interest only to the extent the advancesare actually repaid by remittances received from abroadrelating to the retention money and provided suchpayments are received within 180 days from the due dateof payment of the retention money, according to the termsof the contract.

2.4.5 Export on Consignment Basis

(i) General

(a) Export on consignment basis lends scope for a lot ofmisuse in the matter of repatriation of export proceeds.

(b) Therefore, export on consignment basis should be at parwith exports on outright sale basis on cash terms in mattersregarding the rate of interest to be charged by banks onpost-shipment credit. Thus, in the case of exports onconsignment basis, even if extension in the period beyond180 days is granted by the Exchange Control Departmentfor repatriation of export proceeds, banks will chargeappropriate concessive rate of interest only upto thenotional due date (depending upon the tenor of the bills),subject to a maximum of 180 days.

(ii) Export of precious and semi-precious stones

Precious and semi-precious stones, etc. are exported mostly onconsignment basis and the exporters are not in a position toliquidate pre-shipment credit account with remittances receivedfrom abroad within a period of 180 days from the date ofadvance. Banks may, therefore, adjust packing credit advancesin the case of consignment exports, as soon as export takesplace, by transfer of the outstanding balance to a special (post-shipment) account which in turn, should be adjusted as soon asthe relative proceeds are received from abroad but not later than180 days from the date of export or such extended period asmay be permitted by Exchange Control Department, ReserveBank of India. Balance in the special (post-shipment) accountwill not be eligible for refinance from RBI.

(iii) Consignment exports to CIS and East European Countries

(a) RBI (ECD) is allowing in deserving cases, on applicationby individual exporters with satisfactory track record, alonger period of upto 12 months for realisation of proceedsof export on consignment basis in convertible currencies toCIS (former USSR) and East European Countries. Banksmay extend post-shipment credit to such exporters for alonger period ab initio. Accordingly, the interest rateapplicable will be as follows:

Period of Post-shipment CreditRate of Interest

Upto 90 days from the dateThe rate applicable for

of advanceusance bills for period

upto 90 days

Beyond 90 days and uptoThe rate applicable for

12 months from the date ofusance bills beyond 90

shipmentdays and upto 6 months

from the date of shipment

(b) It is expected that sale proceeds of goods exported onconsignment basis to the above countries would be realisedwithin the permitted period of upto 12 months and post-shipment credit liquidated. In case the sale proceeds arenot realised within the said period, the higher rate ofinterest as applicable for bills realised beyond 6 monthsfrom the date of shipment i.e. ECNOS - Post-shipment willapply for the entire period beyond 6 months.

(c) Refinance to banks against export credit would, however,be available from RBI upto a period of 180 days only eachat pre-shipment and post-shipment stages.

(iv) Consignment exports to Russian Federation againstrepayment of State Credit in rupees(a) RBI (ECD) is allowing on application, Export Houses/

Trading Houses/Star Trading Houses/Super Star TradingHouses with satisfactory track record, a longer period ofupto 360 days from the date of shipment for realisation ofproceeds of exports of permitted goods as announced bythem from time to time to the Russian Federation onconsignment basis against repayment of State Credits inrupees. For the procedure to be followed, reference may bemade to AD(GP Series) Circular No. 5 dated May 31, 1999and subsequent instructions, if any, issued in this regard byExchange Control Department, Reserve Bank of India.Banks may extend post-shipment credit to such exportersfor a longer period ab initio. Accordingly, the interest rateapplicable will be as follows:

Period of Post-shipment CreditRate of Interest

Upto 90 days from the dateThe rate applicable for

of advanceusance bills for period

upto 90 days

Beyond 90 days and uptoThe rate applicable for

360 days from the date ofusance bills beyond 90

shipmentdays and upto 6 months

from the date of shipment

(b) In case, sale proceeds are not realised within the saidperiod, the higher rate of interest as applicable for billsrealised beyond 6 months from the date of shipment willapply for the entire period beyond 6 months.

(c) The refinance to banks against export credit would,

however, be available from RBI upto a period of 180 daysonly each at pre and post shipment stages.

2.4.6 Exports through the Warehouse-cum-Display Centres Abroad

(i) Some Indian organisations/exporters are permitted by RBI (ECD)to establish warehouses abroad for storing the goods exportedfrom India to enable them to arrange off-the-shelf sales forachieving greater penetration in the overseas markets. Sinceexports to these warehouses are in anticipation of orders from thebuyers overseas, the prescribed period of realisation of proceedsof such export has been fixed upto fifteen months from the dateof shipment as against the normal period of six months in othercases.

(ii) In view of longer period of realisation permitted, ab initio, theinterest rates on the post-shipment credit in rupee againstexports through approved warehouses are as follows:

Period of Post-shipment CreditRate of Interest

Upto 90 days from the date ofThe rate applicable for

advanceusance bills for period upto

90 days

Beyond 90 days and upto 15The rate applicable for

months from the date ofusance bills beyond 90 days

shipmentand upto 6 months from the

date of shipment

(iii) In case sale proceeds are not realised within the said period, thehigher rate of interest as applicable for bills realised beyond 6months from the date of shipment i.e. ECNOS - Post-shipmentwill apply for the entire period beyond 6 months.

(iv) Refinance to the bank against export credit would be availablefrom RBI upto a period of 180 days only each at pre-shipmentand post-shipment stages.

2.4.7 Export of Goods for Exhibition and Sale

Banks may provide finance to exporters against goods sent forexhibition and sale abroad in the normal course in the first instance,and after the sale is completed, allow the benefit of the concessive rateof interest on such advances, both at the pre-shipment stage and at thepost-shipment stage, upto the stipulated periods, by way of a rebate.Such advances should be given in separate accounts.

2.4.8 Post-shipment Credit on Deferred Payment Terms

Banks may grant post-shipment credit on deferred payment terms for aperiod exceeding one year, in respect of export of capital and producergoods as specified by RBI (ECD) from time to time.

2.5 Post-shipment Advances against Duty Drawback Entitlements

2.5.1 Banks may grant post-shipment advances to exporters against theirduty drawback entitlements as provisionally certified by CustomsAuthorities pending final sanction and payment.

2.5.2 The advance against duty drawback receivables can also be madeavailable to exporters against export promotion copy of the shippingbill containing the EGM Number issued by the Customs Department.Where necessary, the financing bank may have its lien noted with thedesignated bank and arrangements may be made with the designatedbank to transfer funds to the financing bank as and when dutydrawback is credited by the Customs.

2.5.3 These advances granted against duty drawback entitlements would beeligible for concessional rate of interest and refinance from RBI upto amaximum period of 90 days from the date of advance.

2.6 ECGC Whole Turnover Post-shipment Guarantee Scheme

2.6.1 The Whole Turnover Post-shipment Guarantee Scheme of the ExportCredit Guarantee Corporation of India Ltd. (ECGC) providesprotection to banks against non-payment of post-shipment credit byexporters. Banks may, in the interest of export promotion, consideropting for the Whole Turnover Post-shipment Policy. The salientfeatures of the scheme may be obtained from ECGC.

2.6.2 As the post-shipment guarantee is mainly intended to benefit thebanks, the cost of premium in respect of the Whole Turnover Post-shipment Guarantee taken out by banks may be absorbed by the banksand not passed on to the exporters.

2.6.3 Where the risks are covered by the ECGC, banks should not slackentheir efforts towards realisation of their dues against long outstandingexport bills.

3. DEEMED EXPORTS - CONCESSIVE RUPEE EXPORT CREDIT3.1 Banks are permitted to extend rupee pre-shipment and post-supply rupee export

credit at concessional rate of interest to parties against orders for supplies inrespect of projects aided/financed by bilateral or multilateral agencies/funds(including World Bank, IBRD, IDA), as notified from time to time byDepartment of Economic Affairs, Ministry of Finance under the Chapter"Deemed Exports" in Exim Policy, which are eligible for grant of normal exportbenefits by Government of India.

3.2 Packing Credit provided should be adjusted from free foreign exchangerepresenting payment for the suppliers of goods to these agencies. It can also berepaid/prepaid out of balances in Exchange Earners Foreign Currency account(EEFC A/c), as also from the rupee resources of the exporter to the extentsupplies have actually been made.

3.3 Banks may also extend rupee(i) pre-shipment credit, and(ii) post-supply credit (for a maximum period of 30 days or upto the actualdate of payment by the receiver of goods, whichever is earlier).to other categories of supply of goods specified as 'Deemed Exports' under thesame Chapter of Exim Policy from time to time.

3.4 The post-supply advances would be treated as overdue after the period of 30days. In cases where such overdue credits are liquidated within a period of 180days from the notional due date (i.e. before 210 days from the date of advance),the banks are required to charge, for such extended period, interest prescribedfor the category 'ECNOS' at post-shipment stage. If the bills are not paid withinthe aforesaid period of 210 days, banks should charge from the date of advance,the rate prescribed for 'ECNOS' - Post-shipment.

3.5 Banks would be eligible for refinance from RBI for such rupee export creditsextended both at pre-shipment and post-supply stages.

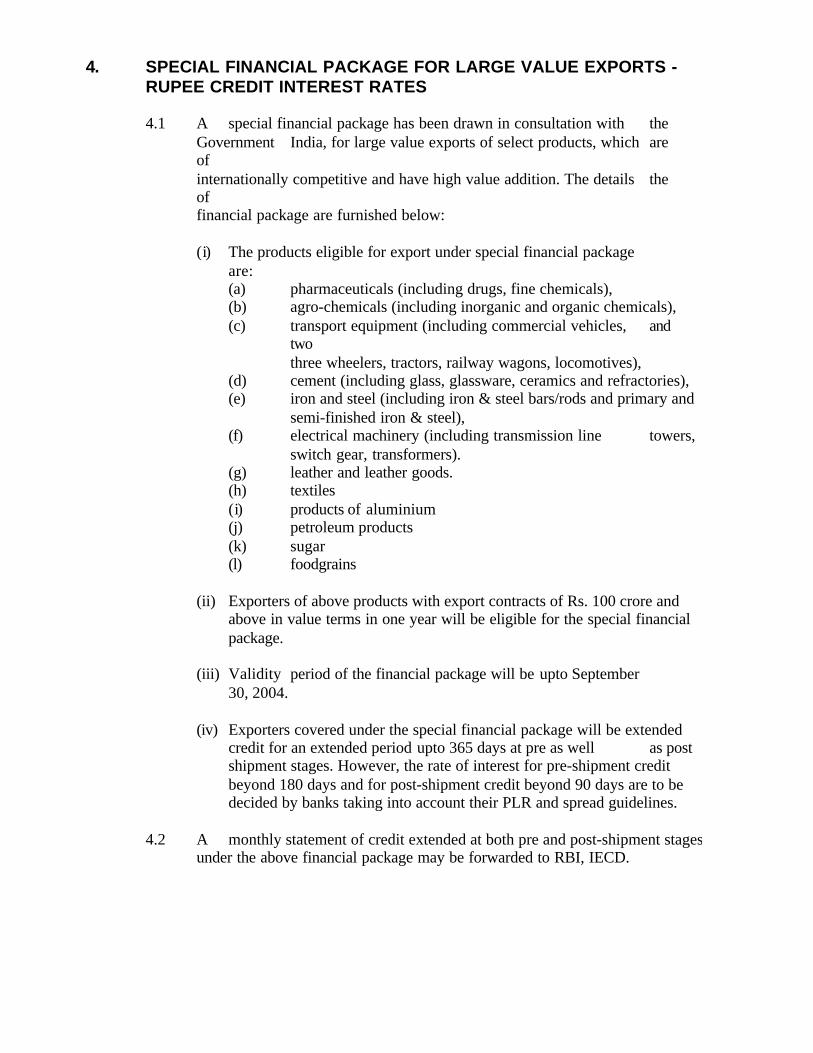

4. SPECIAL FINANCIAL PACKAGE FOR LARGE VALUE EXPORTS -RUPEE CREDIT INTEREST RATES

4.1 A special financial package has been drawn in consultation with theGovernmentof

India, for large value exports of select products, which are

internationally competitive and have high value addition. The detailsof

the

financial package are furnished below:

(i) The products eligible for export under special financial packageare:(a) pharmaceuticals (including drugs, fine chemicals),(b) agro-chemicals (including inorganic and organic chemicals),(c) transport equipment (including commercial vehicles,

twoand

three wheelers, tractors, railway wagons, locomotives),(d) cement (including glass, glassware, ceramics and refractories),(e) iron and steel (including iron & steel bars/rods and primary and

semi-finished iron & steel),(f) electrical machinery (including transmission line towers,

switch gear, transformers).(g) leather and leather goods.(h) textiles(i) products of aluminium(j) petroleum products(k) sugar(l) foodgrains

(ii) Exporters of above products with export contracts of Rs. 100 crore andabove in value terms in one year will be eligible for the special financialpackage.

(iii) Validity period of the financial package will be upto September30, 2004.

(iv) Exporters covered under the special financial package will be extendedcredit for an extended period upto 365 days at pre as well as postshipment stages. However, the rate of interest for pre-shipment creditbeyond 180 days and for post-shipment credit beyond 90 days are to bedecided by banks taking into account their PLR and spread guidelines.

4.2 A monthly statement of credit extended at both pre and post-shipment stagesunder the above financial package may be forwarded to RBI, IECD.

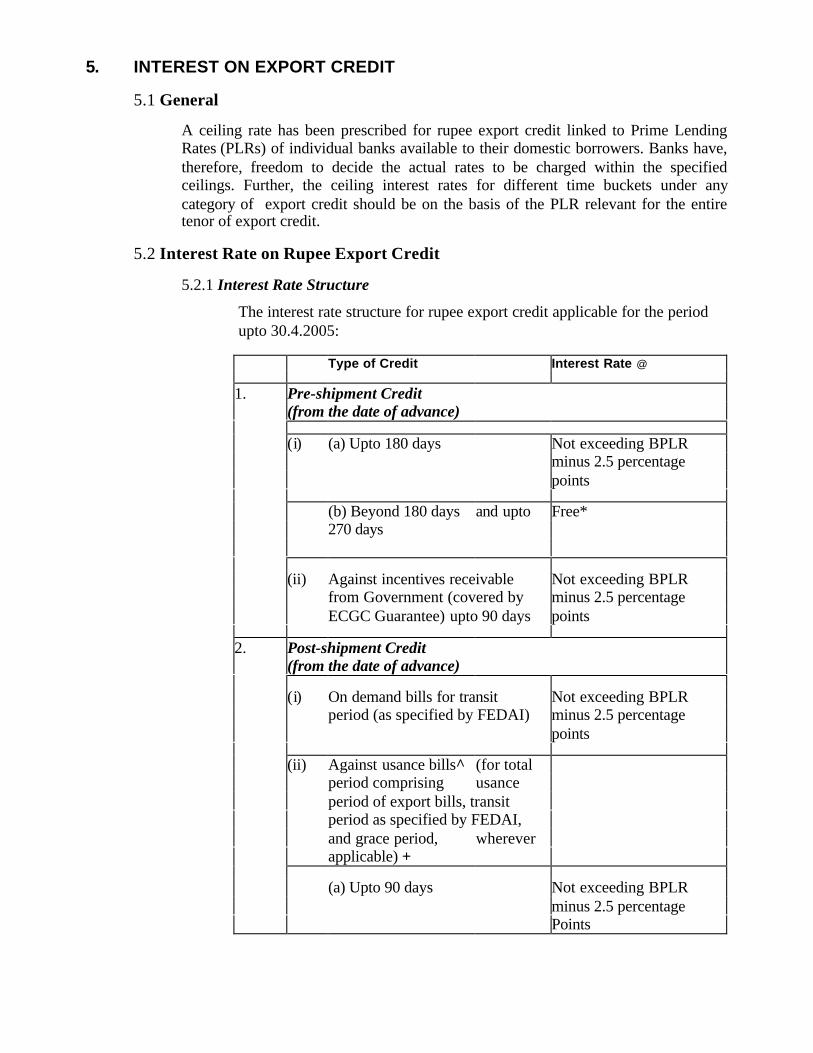

5. INTEREST ON EXPORT CREDIT

5.1 General

A ceiling rate has been prescribed for rupee export credit linked to Prime LendingRates (PLRs) of individual banks available to their domestic borrowers. Banks have,therefore, freedom to decide the actual rates to be charged within the specifiedceilings. Further, the ceiling interest rates for different time buckets under anycategory of export credit should be on the basis of the PLR relevant for the entiretenor of export credit.

5.2 Interest Rate on Rupee Export Credit

5.2.1 Interest Rate Structure

The interest rate structure for rupee export credit applicable for the periodupto 30.4.2005:

Type of Credit Interest Rate @

1. Pre-shipment Credit(from the date of advance)

(i) (a) Upto 180 days Not exceeding BPLRminus 2.5 percentagepoints

(b) Beyond 180 days and upto Free*270 days

(ii) Against incentives receivable Not exceeding BPLRfrom Government (covered by minus 2.5 percentageECGC Guarantee) upto 90 days points

2. Post-shipment Credit(from the date of advance)

(i) On demand bills for transit Not exceeding BPLRperiod (as specified by FEDAI) minus 2.5 percentage

points

(ii) Against usance bills^ (for totalperiod comprising usanceperiod of export bills, transitperiod as specified by FEDAI,and grace period, whereverapplicable) +

(a) Upto 90 days Not exceeding BPLRminus 2.5 percentagePoints

Type of Credit Interest Rate @

(b) Beyond 90 days and upto Free*6 months from the date ofshipment

(iii) Against incentives receivable Not exceeding BPLRfrom Govt. (covered by ECGC minus 2.5 percentageGuarantee) upto 90 days points

(iv) Against undrawn balances - do -(upto 90 days)

(v) Against retention money (for - do -supplies portion only) payable

within one year from the dateof shipment (upto 90 days)

3. Deferred Credit

Deferred credit for the period beyond Free *90 days

4. Export Credit Not OtherwiseSpecified (ECNOS)

(i) Pre-shipment credit Free*

(ii) Post-shipment credit Free*

^ upto notional due date or actual due date, whichever is earlier.+ Interest rate for credit beyond 90 days from the date of advance has to

be charged slab-wise (1-90 days and 91-180 days).@ Since these are ceiling rates, banks would be free to charge any rate

below the ceiling rates.* Banks are free to decide the rate of interest, keeping in view the PLR

and spread guidelines.

5.2.2 Application of Interest Rates

The revision in interest rates made from time to time is made applicable to freshadvances as also to the existing advances for the remaining period of credit.

5.2.3 Interest on Pre-shipment Credit

i) Banks should charge interest on pre-shipment credit upto 180 days at the rateto be decided by the bank within the ceiling rate arrived at on the basis of PLRrelevant for the entire tenor of the export credit under the category. The period ofcredit is to be reckoned from the date of advance.

ii) If pre-shipment advances are not liquidated from proceeds ofbills on purchase, discount, etc. on submission of exportdocuments within 360 days from the date of advance, theadvances will cease to qualify for concessive rate of interest abinitio .

iii) In cases where packing credit is not extended beyond the originalperiod of sanction and exports take place after the expiry ofsanctioned period but within a period of 360 days from the dateof advance, exporter would be eligible for concessional creditonly upto the sanctioned period. For the balance period, interestrate prescribed for ECNOS at pre-shipment stage will apply.Further, the reasons for non-extension of the period need to beadvised by banks to the exporter.

iv) In cases where exports do not take place within 360 days fromthe date of pre-shipment advance, such credits will be termed as‘Export Credit Not Otherwise Specified’ (ECNOS) and banksmay charge interest rate prescribed for ‘ECNOS – pre-shipment’from the very first day of the advance.

v) If exports do not materialise at all, banks should charge onrelative packing credit domestic lending rate plus penal rate ofinterest, if any, to be decided by the banks on the basis of atransparent policy approved by their Board.

5.2.4 Interest on Post-shipment Credit

(i) Early payment of export bills(a) In the case of advances against demand bills, if the bills

are realised before the expiry of the normal transit period(NTP), interest at the concessive rate shall be chargedfrom the date of advance till the date of realisation of suchbills. The date of realisation of demand bills for thispurpose would be the date on which the proceeds getcredited to the banks' Nostro accounts.

(b) In the case of advance/credit against usance export bills,interest at concessive rate may be charged only upto thenotional/actual due date or the date on which exportproceeds get credited to the bank’s Nostro account abroad,whichever is earlier, irrespective of the date of credit tothe borrower's/exporter's account in India. In cases wherethe correct due date can be established before/immediatelyafter availment of credit due to acceptance by overseasbuyer or otherwise, concessive interest can be appliedonly upto the actual due date, irrespective of whatevermay be the notional due date arrived at, provided theactual due date falls before the notional due date.

(c) Where interest for the entire NTP in the case of demandbills or upto notional/actual due date in the case of usancebills as stated at (b) above, has been collected at the time

of negotiation/purchase/discount of bills, the excessinterest collected for the period from the date ofrealisation to the last date of NTP/notional due date/actualdue date should be refunded to the borrowers.

5.2.5 Overdue Export Bills(i) In case of export bills, the rate of interest decided by the bank

within the ceiling rate stipulated by RBI will apply upto the duedate of the bill (upto NTP in case of demand bill and specifiedperiod in case of usance bills).

(ii) For the period beyond the due date viz. for the overdue period,the rate fixed for ‘Export Credit Not Otherwise Specified’(ECNOS) at post-shipment stage will apply and no penalinterest should be charged additionally.

(iii) Banks should ensure that the additional interest by way ofoverdue interest (ECNOS) should not be levied where there hasbeen no advance (pre or post shipment) taken by the exporter.

5.2.6 Interest on Post-shipment Credit Adjusted from Rupee ResourcesBanks should adopt the following guidelines to ensure uniformity incharging interest on post-shipment advances which are not adjusted inan approved manner due to non-accrual of foreign exchange andadvances have to be adjusted out of the funds received from the ExportCredit Guarantee Corporation of India Ltd. (ECGC) in settlement ofclaims preferred on them on account of the relevant export consignment:

(a) In case of exports to certain countries, exporters are unable torealise export proceeds due to non-expatriation of the foreignexchange by the Governments/Central Banking Authorities ofthe countries concerned as a result of their balance of paymentproblems even though payments have been made locally by thebuyers. In these cases ECGC offer cover to exporters for transferdelays. Where ECGC have admitted the claims and paid theamount for transfer delay, banks may charge interest asapplicable to ‘ECNOS - Post-shipment’ even if the post-shipment advance may be outstanding beyond six months fromthe date of shipment. Such interest would be applicable on thefull amount of advance irrespective of the fact that the ECGCadmit the claims to the extent of 90 percent/75 percent and theexporters have to bring the balance 10 percent/25 percent fromtheir own rupee resources.

(b) In a case where interest has been charged at commercial rate orECNOS if export proceeds are realised in an approved mannersubsequently, the bank may refund to the borrower the excessamount representing difference between the quantum of interestalready charged and interest that is chargeable taking intoaccount the said realisation after ensuring the fact of such

realisation with satisfactory evidence. While making adjustmentsof accounts it would be better if the possibility of refund ofexcess interest is brought to the notice of the borrower.

5.2.7 Change of Tenor of Bill

(i) In terms of para C.14 of the AP DIR series Circular No. 12FEMA Notification issued by RBI (ECD), banks have beenpermitted, on request from exporters, to allow change of thetenor of the original buyer/ consignee, provided inter alia, therevised due date of payment does not fall beyond six monthsfrom the date of shipment.

(ii) In such cases as well as where change of tenor upto six monthsfrom the date of shipment has been allowed, it would be in orderfor banks to extend the concessional rate of interest upto therevised notional due date, subject to the interest rates Directiveissued by RBI.

Note:

(Ceilings rates of interest on credit extended to exporters as prescribedin the circular are lower than the maximum lending rates normallycharged to other borrowers and are, therefore, indicated as concessivein this sense).

Appendix

Master CircularRUPEE EXPORT CREDIT

List of Circulars consolidated by the Master Circular

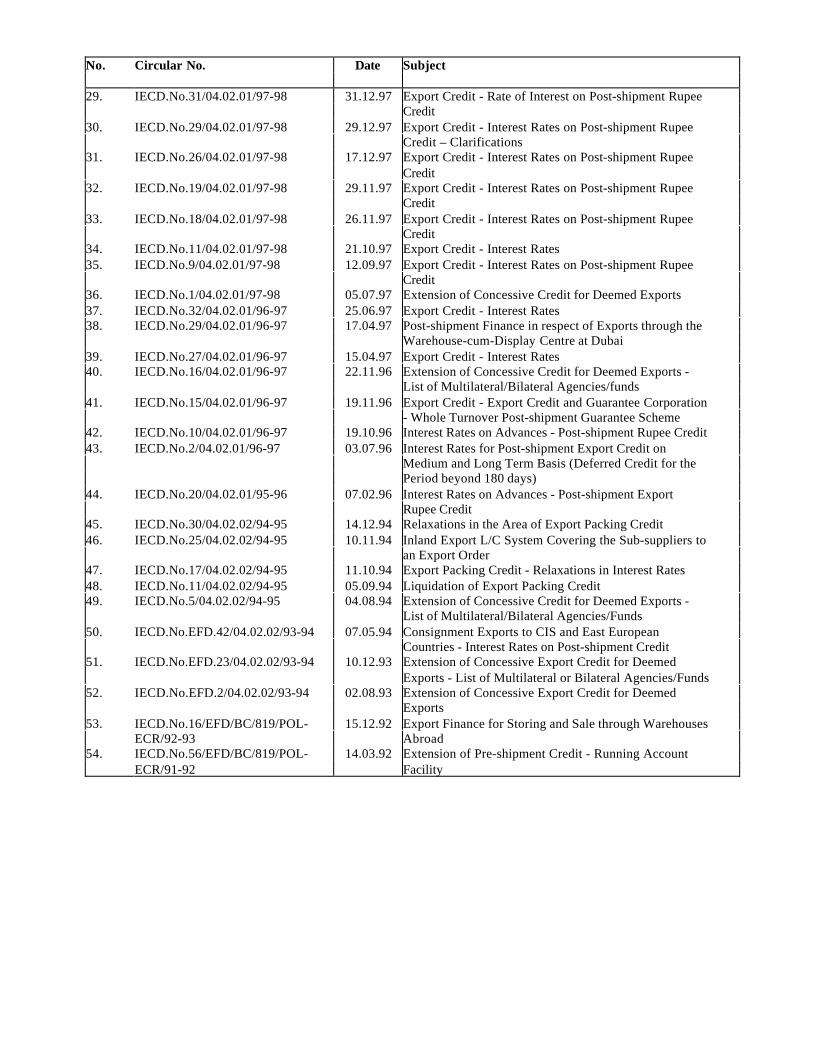

No. Circular No. Date Subject

1. IECD No. 5/04.02.01/2003-04 31.10.2003 Rupee Export Credit Interest Rates2. IECD No. 2/04.02.02/2003-04 7.10.2003 Special Financial Package for Large Value Exports3. IECD No. 18/04.02.01/2002-03 30.04.03 Rupee Export Credit Interest rates4. IECD No.16/04.02.02/2002-03 01.04.03 Export Credit - SEZ Units5. IECD No. 8/04.02.01/2002-03 28.09.02 Special Financial Package for Large value Exports6. IECD No. 7/04.02.01/2002-03 23.09.02 Rupee Export Credit Interest rates7. IECD.No.24/04.02.01/2001-02 06.06.2002 Special Financial Package for Large Value Exports8. IECD No.19/04.02.01/2001-02 19.04.2002 Special Financial Package for Large Value Exports –

Rupee Credit Interest rates9. IECD.No.17/04.02.01/2001-02 15.03.2002 Rupee Export Credit Interest Rates10. IECD.No.15/04.02.02/2001-02 03.01.2002 Export Credit to Processors/Exporters-Agri-Export

Zones11. IECD.No.12/04.02.01/2001-02 22.11.2001 Special Financial Package for Large Value Exports –

Rupee Credit Interest Rates12. IECD.No.5/04.02.01/2001-02 24.09.2001 Special Financial Package for Large Value Exports –

Rupee Credit Interest Rates13. IECD.No.4/04.02.01/2001-02 24.09.2001 Rupee Export Credit Interest Rates14. IECD.No.13/04.02.01/2000-01 19.04.2001 Rupee Export Credit Interest Rates15. IECD.No.9/04.02.01/2000-2001 05.01.2001 Interest Rate on Export Credit16. IECD.No.15/04.02.01/99-2000 25.05.2000 Export Credit - Interest Rates17. IECD.No.14/04.02.02/1999-2000 17.05.2000 Consignment Exports to Russian Federation against

Repayment of State Credits - Interest Rates on Post-shipment Credit in Rupees

18. IECD.No.12/04.02.01/1999-2000 15.03.2000 Export Credit Interest Rate – Clarifications19. IECD.No.6/04.02.01/99-2000 29.10.99 Export Credit - Interest Rates20. IECD.No.23/04.02.01/98-99 12.04.99 Change of Tenor of Bill - Applicability of Concessional

Rate of Interest21. IECD.No.19/04.02.01/98-99 03.03.99 Export Credit - Interest Rates22. IECD.No.16/04.02.01/98-99 25.02.99 Advance against Duty Drawback Claims23. IECD.No.11/04.02.01/98-99 13.01.99 Export Credit - Floriculture, Grapes and Other Agro

Products24. IECD.No.6/08.12.01/98-99 08.08.99 Guidelines for Sanction of Working Capital Finance to

Information Technology (IT) and Software Industry25. IECD.No.5/04.02.01/98-99 06.08.98 Export Credit - Interest Rates26. IECD.No.41/04.02.01/97-98 29.04.98 Export Credit - Interest Rates27. IECD.No.38/04.02.02/97-98 02.03.98 Post-shipment Finance in respect of Exports through the

Warehouse-cum-Display Centre at Dubai28. IECD.No.32/04.02.01/97-98 31.12.97 Export Credit - Rate of Interest on Overdue Export Bills

No. Circular No. Date Subject

29. IECD.No.31/04.02.01/97-98 31.12.97 Export Credit - Rate of Interest on Post-shipment RupeeCredit

30. IECD.No.29/04.02.01/97-98 29.12.97 Export Credit - Interest Rates on Post-shipment RupeeCredit – Clarifications

31. IECD.No.26/04.02.01/97-98 17.12.97 Export Credit - Interest Rates on Post-shipment RupeeCredit

32. IECD.No.19/04.02.01/97-98 29.11.97 Export Credit - Interest Rates on Post-shipment RupeeCredit

33. IECD.No.18/04.02.01/97-98 26.11.97 Export Credit - Interest Rates on Post-shipment RupeeCredit

34. IECD.No.11/04.02.01/97-98 21.10.97 Export Credit - Interest Rates35. IECD.No.9/04.02.01/97-98 12.09.97 Export Credit - Interest Rates on Post-shipment Rupee

Credit36. IECD.No.1/04.02.01/97-98 05.07.97 Extension of Concessive Credit for Deemed Exports37. IECD.No.32/04.02.01/96-97 25.06.97 Export Credit - Interest Rates38. IECD.No.29/04.02.01/96-97 17.04.97 Post-shipment Finance in respect of Exports through the

Warehouse-cum-Display Centre at Dubai39. IECD.No.27/04.02.01/96-97 15.04.97 Export Credit - Interest Rates40. IECD.No.16/04.02.01/96-97 22.11.96 Extension of Concessive Credit for Deemed Exports -

List of Multilateral/Bilateral Agencies/funds41. IECD.No.15/04.02.01/96-97 19.11.96 Export Credit - Export Credit and Guarantee Corporation

- Whole Turnover Post-shipment Guarantee Scheme42. IECD.No.10/04.02.01/96-97 19.10.96 Interest Rates on Advances - Post-shipment Rupee Credit43. IECD.No.2/04.02.01/96-97 03.07.96 Interest Rates for Post-shipment Export Credit on

Medium and Long Term Basis (Deferred Credit for thePeriod beyond 180 days)

44. IECD.No.20/04.02.01/95-96 07.02.96 Interest Rates on Advances - Post-shipment ExportRupee Credit

45. IECD.No.30/04.02.02/94-95 14.12.94 Relaxations in the Area of Export Packing Credit46. IECD.No.25/04.02.02/94-95 10.11.94 Inland Export L/C System Covering the Sub-suppliers to

an Export Order47. IECD.No.17/04.02.02/94-95 11.10.94 Export Packing Credit - Relaxations in Interest Rates48. IECD.No.11/04.02.02/94-95 05.09.94 Liquidation of Export Packing Credit49. IECD.No.5/04.02.02/94-95 04.08.94 Extension of Concessive Credit for Deemed Exports -

List of Multilateral/Bilateral Agencies/Funds50. IECD.No.EFD.42/04.02.02/93-94 07.05.94 Consignment Exports to CIS and East European

Countries - Interest Rates on Post-shipment Credit51. IECD.No.EFD.23/04.02.02/93-94 10.12.93 Extension of Concessive Export Credit for Deemed

Exports - List of Multilateral or Bilateral Agencies/Funds52. IECD.No.EFD.2/04.02.02/93-94 02.08.93 Extension of Concessive Export Credit for Deemed

Exports53. IECD.No.16/EFD/BC/819/POL- 15.12.92 Export Finance for Storing and Sale through Warehouses

ECR/92-93 Abroad54. IECD.No.56/EFD/BC/819/POL- 14.03.92 Extension of Pre-shipment Credit - Running Account

ECR/91-92 Facility

No. Circular No. Date Subject

55. IECD.No.55/EFD/BC/819/POL- 12.03.92 Pre-shipment Credit for Periods Beyond 180 DaysECR/91-92

56. IECD.No.53/EFD/BC/819/POL- 29.02.92 Interest Rates on Export CreditECR/91-92

57. IECD.No.47/EFD/BC/819/POL- 25.01.92 Packing Credit - Running Account FacilityECR/91-92

58. IECD.No.31/EFD/BC/819/POL- 20.11.91 Extension of Packing Credit - Running Account FacilityECR/91-92

59. IECD.No.25/EFD/BC/819/POL- 09.10.91 Interest Rates on Export CreditECR/91-92

60. IECD.No.22/EFD/BC/819/POL- 27.09.91 Interest Rates on Post-shipment Export CreditECR/91-92

61. IECD.No.11/EFD/BC/819/POL- 05.08.91 Interest Rates on Advances - Export CreditECR/91-92

62. IECD.No.2/EFD/BC/819-POL/ 09.07.91 Export Credit (Interest Subsidy) Scheme, 1968 - InterestECR/91-92 on Post-shipment Credit Adjusted from Rupee Resources

63. IECD.No.EFD.BC.49/819-POL/ 22.04.91 Interest Rates on Advances - Export CreditECR/91

64. IECD.No.EFD/BC/48/819/POL- 02.04.91 Interest Rates on Advances - Export CreditECR/91

65. IECD.No.EFD/BC/47/819/POL- 01.04.91 Interest Rates on Advances - Export CreditECR/90-91

66. IECD.No.EFD.BC.44/DDB(P)-91 26.03.91 Duty Drawback Credit Scheme, 1976 - Grant of Interest-free Advances against Duty Drawback Entitlementsunder Brand Rate

67. IECD.No.EFD.BC.8/819-POL/ 28.09.89 Export Credit (Interest Subsidy) Scheme, 1968 - NormalECR/89-90 Transit Period - Demand Bills

68. IECD.No.EFD.BC.253/819-POL- 27.05.89 Export Credit (Interest Subsidy) Scheme, 1968 - InterestECR/89 on Post-shipment Credit Adjusted from Rupee Resources

69. IECD.No.EFD.BC.250/380- 29.04.89 Duty Drawback Credit Scheme, 1976DDB(P)-89

70. IECD.No.EFD.BC.248/819-POL- 13.03.89 Packing Credit for Imports against Entitlements underECR-89 Advance Licence/Import-Export Pass Book Scheme

71. IECD.No.EFD.BC.240/819-POL- 03.03.89 Export Credit (Interest Subsidy) Scheme, 1968 -ECR-89 Provision of Concessive Credit against Proceeds of

Cheques, Drafts, etc. Received Directly towardsAdvance Payment of Exports

72. IECD.No.EFD.215/822-WGM- 12.08.88 Overseas Civil Engineering Construction Contracts -NOD-88 Consultancy Services

73. IECD.No.EFD.197/822-WGM- 30.01.88 Project Exports - Grant of Credit Facilities to IndianNOD-88 Contractors

74. IECD.No.EFD.BC.188/819-POL- 06.11.87 Export Credit (Interest Subsidy) Scheme, 1968 - PackingECR-87 Credit relating to the Export of Cashew nuts and Other

Agro-based Products75. IECD.No.EFD.BC.181/819-POL- 10.08.87 Export Credit Guarantee Corporation of India Ltd.

ECR-87 (ECGC) - Realisation of Long Outstanding Export Bills -Recovery Efforts by Banks

76. IECD.No.EFD.BC.163/819-POL- 04.03.87 Export Credit (Interest Subsidy) Scheme, 1968 -ECR-87 Clarification regarding 'Normal Transit Period'

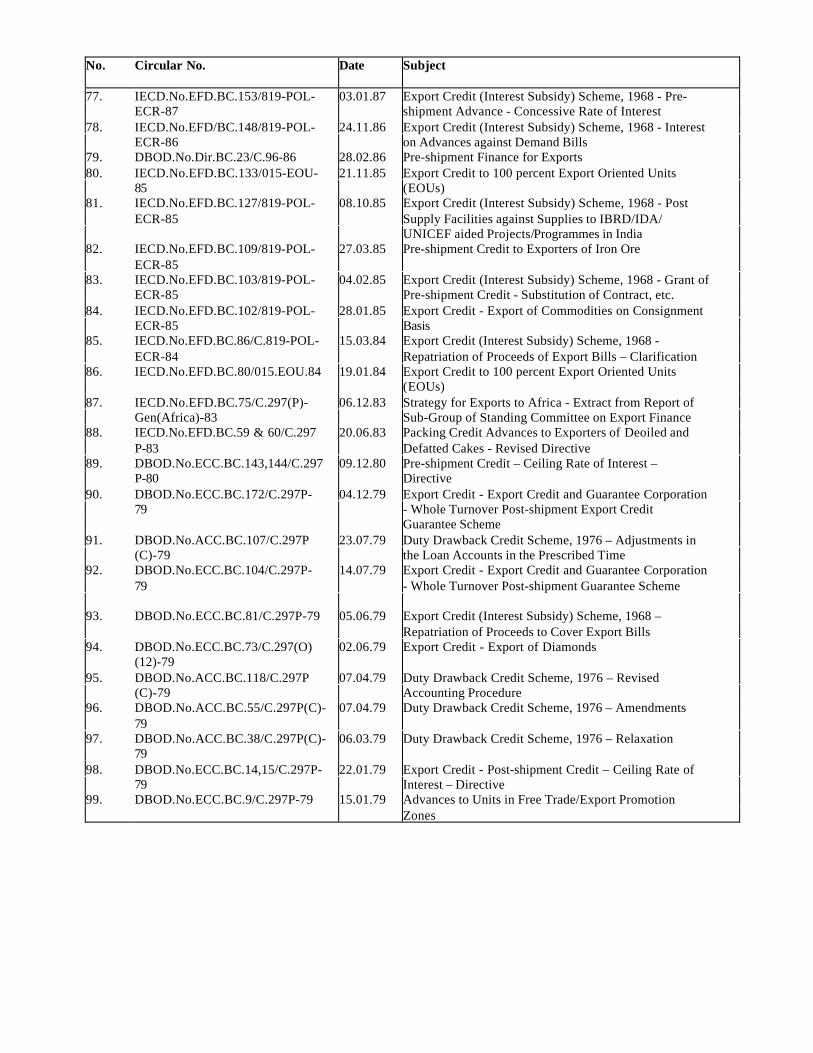

No. Circular No. Date Subject

77. IECD.No.EFD.BC.153/819-POL- 03.01.87 Export Credit (Interest Subsidy) Scheme, 1968 - Pre-ECR-87 shipment Advance - Concessive Rate of Interest

78. IECD.No.EFD/BC.148/819-POL- 24.11.86 Export Credit (Interest Subsidy) Scheme, 1968 - InterestECR-86 on Advances against Demand Bills

79. DBOD.No.Dir.BC.23/C.96-86 28.02.86 Pre-shipment Finance for Exports80. IECD.No.EFD.BC.133/015-EOU- 21.11.85 Export Credit to 100 percent Export Oriented Units

85 (EOUs)81. IECD.No.EFD.BC.127/819-POL- 08.10.85 Export Credit (Interest Subsidy) Scheme, 1968 - Post

ECR-85 Supply Facilities against Supplies to IBRD/IDA/UNICEF aided Projects/Programmes in India

82. IECD.No.EFD.BC.109/819-POL- 27.03.85 Pre-shipment Credit to Exporters of Iron OreECR-85

83. IECD.No.EFD.BC.103/819-POL- 04.02.85 Export Credit (Interest Subsidy) Scheme, 1968 - Grant ofECR-85 Pre-shipment Credit - Substitution of Contract, etc.

84. IECD.No.EFD.BC.102/819-POL- 28.01.85 Export Credit - Export of Commodities on ConsignmentECR-85 Basis

85. IECD.No.EFD.BC.86/C.819-POL- 15.03.84 Export Credit (Interest Subsidy) Scheme, 1968 -ECR-84 Repatriation of Proceeds of Export Bills – Clarification

86. IECD.No.EFD.BC.80/015.EOU.84 19.01.84 Export Credit to 100 percent Export Oriented Units(EOUs)

87. IECD.No.EFD.BC.75/C.297(P)- 06.12.83 Strategy for Exports to Africa - Extract from Report ofGen(Africa)-83 Sub-Group of Standing Committee on Export Finance

88. IECD.No.EFD.BC.59 & 60/C.297 20.06.83 Packing Credit Advances to Exporters of Deoiled andP-83 Defatted Cakes - Revised Directive

89. DBOD.No.ECC.BC.143,144/C.297 09.12.80 Pre-shipment Credit – Ceiling Rate of Interest –P-80 Directive

90. DBOD.No.ECC.BC.172/C.297P- 04.12.79 Export Credit - Export Credit and Guarantee Corporation79 - Whole Turnover Post-shipment Export Credit

Guarantee Scheme91. DBOD.No.ACC.BC.107/C.297P 23.07.79 Duty Drawback Credit Scheme, 1976 – Adjustments in

(C)-79 the Loan Accounts in the Prescribed Time92. DBOD.No.ECC.BC.104/C.297P- 14.07.79 Export Credit - Export Credit and Guarantee Corporation

79 - Whole Turnover Post-shipment Guarantee Scheme

93. DBOD.No.ECC.BC.81/C.297P-79 05.06.79 Export Credit (Interest Subsidy) Scheme, 1968 –Repatriation of Proceeds to Cover Export Bills

94. DBOD.No.ECC.BC.73/C.297(O) 02.06.79 Export Credit - Export of Diamonds(12)-79

95. DBOD.No.ACC.BC.118/C.297P 07.04.79 Duty Drawback Credit Scheme, 1976 – Revised(C)-79 Accounting Procedure

96. DBOD.No.ACC.BC.55/C.297P(C)- 07.04.79 Duty Drawback Credit Scheme, 1976 – Amendments79

97. DBOD.No.ACC.BC.38/C.297P(C)- 06.03.79 Duty Drawback Credit Scheme, 1976 – Relaxation79

98. DBOD.No.ECC.BC.14,15/C.297P- 22.01.79 Export Credit - Post-shipment Credit – Ceiling Rate of79 Interest – Directive

99. DBOD.No.ECC.BC.9/C.297P-79 15.01.79 Advances to Units in Free Trade/Export PromotionZones

No. Circular No. Date Subject

77. IECD.No.EFD.BC.153/819-POL- 03.01.87 Export Credit (Interest Subsidy) Scheme, 1968 - Pre-ECR-87 shipment Advance - Concessive Rate of Interest

78. IECD.No.EFD/BC.148/819-POL- 24.11.86 Export Credit (Interest Subsidy) Scheme, 1968 - InterestECR-86 on Advances against Demand Bills

79. DBOD.No.Dir.BC.23/C.96-86 28.02.86 Pre-shipment Finance for Exports80. IECD.No.EFD.BC.133/015-EOU- 21.11.85 Export Credit to 100 percent Export Oriented Units

85 (EOUs)81. IECD.No.EFD.BC.127/819-POL- 08.10.85 Export Credit (Interest Subsidy) Scheme, 1968 - Post

ECR-85 Supply Facilities against Supplies to IBRD/IDA/UNICEF aided Projects/Programmes in India

82. IECD.No.EFD.BC.109/819-POL- 27.03.85 Pre-shipment Credit to Exporters of Iron OreECR-85

83. IECD.No.EFD.BC.103/819-POL- 04.02.85 Export Credit (Interest Subsidy) Scheme, 1968 - Grant ofECR-85 Pre-shipment Credit - Substitution of Contract, etc.

84. IECD.No.EFD.BC.102/819-POL- 28.01.85 Export Credit - Export of Commodities on ConsignmentECR-85 Basis

85. IECD.No.EFD.BC.86/C.819-POL- 15.03.84 Export Credit (Interest Subsidy) Scheme, 1968 -ECR-84 Repatriation of Proceeds of Export Bills – Clarification

86. IECD.No.EFD.BC.80/015.EOU.84 19.01.84 Export Credit to 100 percent Export Oriented Units(EOUs)

87. IECD.No.EFD.BC.75/C.297(P)- 06.12.83 Strategy for Exports to Africa - Extract from Report ofGen(Africa)-83 Sub-Group of Standing Committee on Export Finance

88. IECD.No.EFD.BC.59 & 60/C.297 20.06.83 Packing Credit Advances to Exporters of Deoiled andP-83 Defatted Cakes - Revised Directive

89. DBOD.No.ECC.BC.143,144/C.297 09.12.80 Pre-shipment Credit – Ceiling Rate of Interest –P-80 Directive

90. DBOD.No.ECC.BC.172/C.297P- 04.12.79 Export Credit - Export Credit and Guarantee Corporation79 - Whole Turnover Post-shipment Export Credit

Guarantee Scheme91. DBOD.No.ACC.BC.107/C.297P 23.07.79 Duty Drawback Credit Scheme, 1976 – Adjustments in

(C)-79 the Loan Accounts in the Prescribed Time92. DBOD.No.ECC.BC.104/C.297P- 14.07.79 Export Credit - Export Credit and Guarantee Corporation

79 - Whole Turnover Post-shipment Guarantee Scheme

93. DBOD.No.ECC.BC.81/C.297P-79 05.06.79 Export Credit (Interest Subsidy) Scheme, 1968 –Repatriation of Proceeds to Cover Export Bills

94. DBOD.No.ECC.BC.73/C.297(O) 02.06.79 Export Credit - Export of Diamonds(12)-79

95. DBOD.No.ACC.BC.118/C.297P 07.04.79 Duty Drawback Credit Scheme, 1976 – Revised(C)-79 Accounting Procedure

96. DBOD.No.ACC.BC.55/C.297P(C)- 07.04.79 Duty Drawback Credit Scheme, 1976 – Amendments79

97. DBOD.No.ACC.BC.38/C.297P(C)- 06.03.79 Duty Drawback Credit Scheme, 1976 – Relaxation79

98. DBOD.No.ECC.BC.14,15/C.297P- 22.01.79 Export Credit - Post-shipment Credit – Ceiling Rate of79 Interest – Directive

99. DBOD.No.ECC.BC.9/C.297P-79 15.01.79 Advances to Units in Free Trade/Export PromotionZones

No. Circular No. Date Subject

118. DBOD.ECC.BC.91/C.297P-75 23.10.75 Export Credit - Export of Goods for Exhibition-cum-Sale- Concessional Rate of Interest to be Charged by Banksfor Manufacture of Products for Sale and ExhibitionAbroad

119. DBOD.ECC.BC.57/C.297P-75 14.08.75 Export Credit - Export of Consultancy Services -Sanction of Credit Limits by Banks against ConsultancyAgreements for Meeting Expenses of the Technical andOther Staff

120. DBOD.ECC.BC.33/C.297P-75 19.04.75 Post-shipment Credit on Deferred Payment Terms -Advice to Banks to Charge the Interest at a ConcessionalCeiling Rate of 8 percent p.a. for a Period ExceedingOne Year

121. DBOD.BM.BC.7/C.297P-74 12.01.74 Export Credit - Advice to Banks to Keep a Close Watchon the Utilisation of Export Credit with Reference toboth the Quantum and the Period

122. DBOD.BM.BC.81/C.297M-73 18.07.73 Pre-shipment Credit Scheme and Export Credit (InterestSubsidy) Scheme, 1968 - Packing Credit Facilitiesagainst Supplies to IBRD/IDA/ UNICEF aidedProjects/Programmes in India Eligible for both forRefinance and Interest Subsidy

123. DBOD.BM.BC.58/C.297P-73 31.05.73 Pre-shipment Credit Scheme - Export of Precious andSemi-precious Stones, Pearls and Synthetic Stones –Clarification that Packing Credit Advances may beAdjusted by Transfer of the Outstanding Balance to aSpecial (Post-shipment) Account

124. DBOD.BM.BC.120/C.297P-72 06.12.72 Packing Credit Advances to Miners of Iron Ore in Goawho Supply Ore to Exporters for Export

125. DBOD.BM.BC.97/C.297(M)-72 30.10.72 Pre-shipment Credit Scheme and Export Credit (InterestSubsidy) Scheme, 1968 - Cash Incentives, DutyDrawbacks, etc. - Clarification regarding ECGC Scheme

126. DBOD.BM.BC.74/C.297(M)-72 30.08.72 Pre-shipment Credit Scheme and Export Credit (InterestSubsidy) Scheme, 1968 - Cash Incentives, DutyDrawbacks, etc.

127. DBOD.BM.BC.70/C.297P-72 09.08.72 Packing Credit Advances relating to Export of MineralOres

128. DBOD.BM.BC.62/C.297(M)-71 21.05.71 Pre-shipment Credit Scheme and Export Credit (InterestSubsidy) Scheme, 1968 - Advice to Banks to keep aclose watch not only on the end-use of the finance butalso for the timely fulfilment of Export Orders and toScrutinise Applications for Extension of time carefully

129. DBOD.Sch.BC.51/C.96-71 16.04.71 Packing Credit and Post-shipment Credit – Interest RatesStructure - Ceiling of 7 percent per annum for PackingCredit and Post-shipment Credit other than CreditsProvided for Exporters on Deferred Payment Terms

130. DBOD.BM.64/C.297P-70 12.01.70 Pre-shipment Credit Scheme - Export of Precious, Semi-precious Stones, Pearls and Synthetic Stones

131. DBOD.BM.1152/C.297(M)-69 11.07.69 Advances to Scheduled Banks under Section 17(3A) ofRBI Act - Advances to Exporters who do not haveLetters of Credit or Export Orders in their Own Nameand who Route their Exports through State TradingCorporation, Minerals and Metals Trading Corporationand other Export Houses – Clarification

No. Circular No. Date Subject

132. DBOD.BM.1064/C.297P-69 01.07.69 Pre-shipment Credit Scheme in respect of Export ofDiamonds

133. DBOD.BM.1040/C.297P-69 27.06.69 Pre-shipment Credit Scheme - Advances to Tanners whoSupply Leather Goods to State Trading Corporation forFeeding Leather Articles to be Exported - To be treatedas Packing Credit

134. DBOD.BM.984/C.297P-69 19.06.69 Pre-shipment Credit Scheme - Certain Advances toConstruction Contractors to be treated as Packing Credit

135. DBOD.BM.682/C.297K-69 07.04.69 Export Credit - Charging of Interest136. DBOD.BM.588/C.297A-69 26.03.69 Refinancing of Packing Credit Advances relating to

Export of Ores through Minerals and Metals TradingCorporation

137. DBOD.BM.254/C.297A-69 14.02.69 Packing Credit Advances - Clarification - Grant of suchAdvances should not be Conditional on a Letter of Creditbeing Opened

138. DBOD.BM.1489/C.297A-68 07.11.68 Packing Credit Advances - Period for which suchAdvances may be given – Clarification

139. DBOD.BM.1179/C.297A-68 19.08.68 Refinancing of Packing Credit Advances relating toExport of Cashew nuts - Stage from which MaximumRate of Interest Applicable - Further Clarification

140. DBOD.BM.974/C.297A-68 27.06.68 Packing Credit Facilities relating to Export of Cashewnuts

141. DBOD.BM.785/C.297A-68 18.05.68 Packing Credit Facilities relating to Export of Cashewnuts

142. DBOD.BM.558/C.297A-68 06.04.68 Packing Credit Facilities to Exporters143. DBOD.BM.2732/C.297K-63 13.03.63 Export Bills Credit Scheme - Salient Features of the

Scheme – Procedure

Master Circular

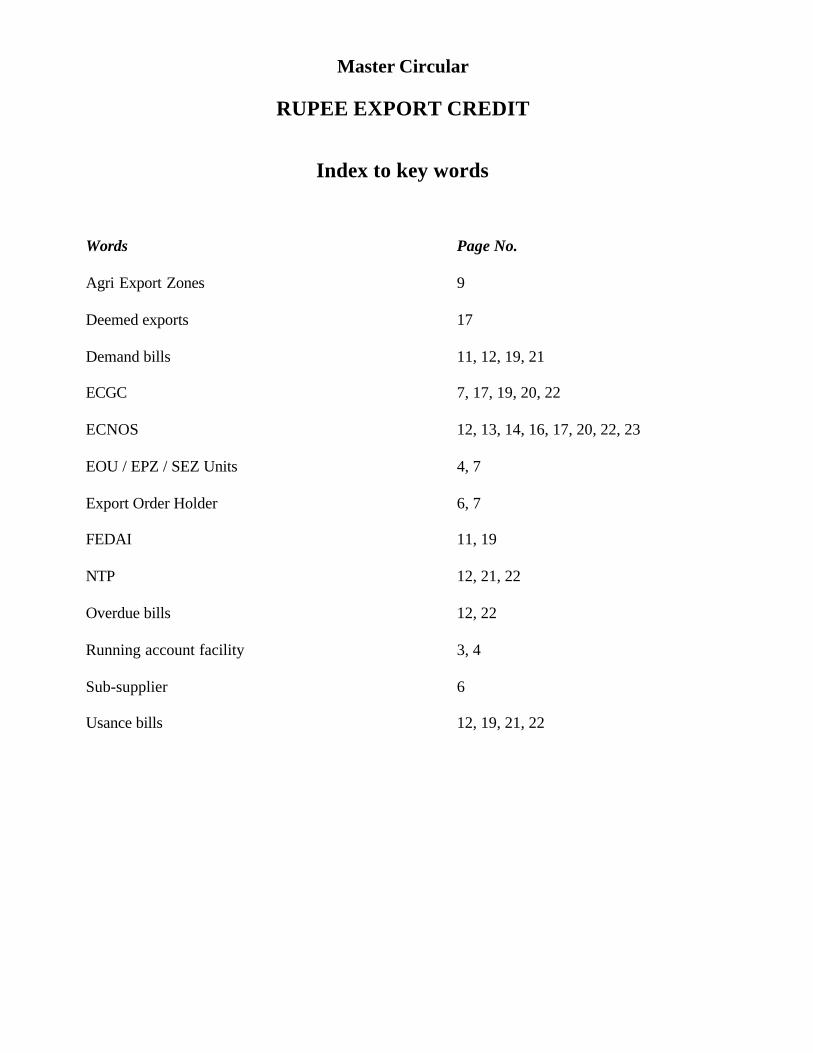

RUPEE EXPORT CREDIT

Index to key words

Words Page No.

Agri Export Zones 9

Deemed exports 17

Demand bills 11, 12, 19, 21

ECGC 7, 17, 19, 20, 22

ECNOS 12, 13, 14, 16, 17, 20, 22, 23

EOU / EPZ / SEZ Units 4, 7

Export Order Holder 6, 7

FEDAI 11, 19

NTP 12, 21, 22

Overdue bills 12, 22

Running account facility 3, 4

Sub-supplier 6

Usance bills 12, 19, 21, 22