1 presentation to the standing committee on finance developments in the regulation of non-banking...

TRANSCRIPT

1

PRESENTATION TO THESTANDING COMMITTEE

ON FINANCE

Developments in the regulation of non-banking

financial institutions

2

THE FSB TEAM

DUBE TSHIDI EXECUTIVE OFFICER

JONATHAN DIXON DEPUTY EXECUTIVE OFFICER:

INSURANCE

JURGEN BOYDDEPUTY EXECUTIVE OFFICER:

RETIREMENT FUNDS

GERRY ANDERSONDEPUTY EXECUTIVE OFFICER: MARKET CONDUCT AND

CONSUMER EDUCATION

3

AGENDA

ROLE OF THE FSB IN THE FINANCIAL SECTOR

LESSONS FROM THE FINANCIAL CRISIS

STATUS AND MAJOR INITIATIVES IN FSB REGULATED SECTORS

–INSURANCE–INVESTMENT INSTITUTIONS AND CAPITAL MARKETS–RETIREMENT FUNDS–FINANCIAL ADVISORY AND INTERMEDIARY SERVICES (FAIS)

TREATING CUSTOMERS FAIRLY (TCF)

FINANCIAL INCLUSION–MICROINSURANCE

ENFORCEMENT

CONSUMER EDUCATION - (ACCOMPANYING PRESENTATION)

4

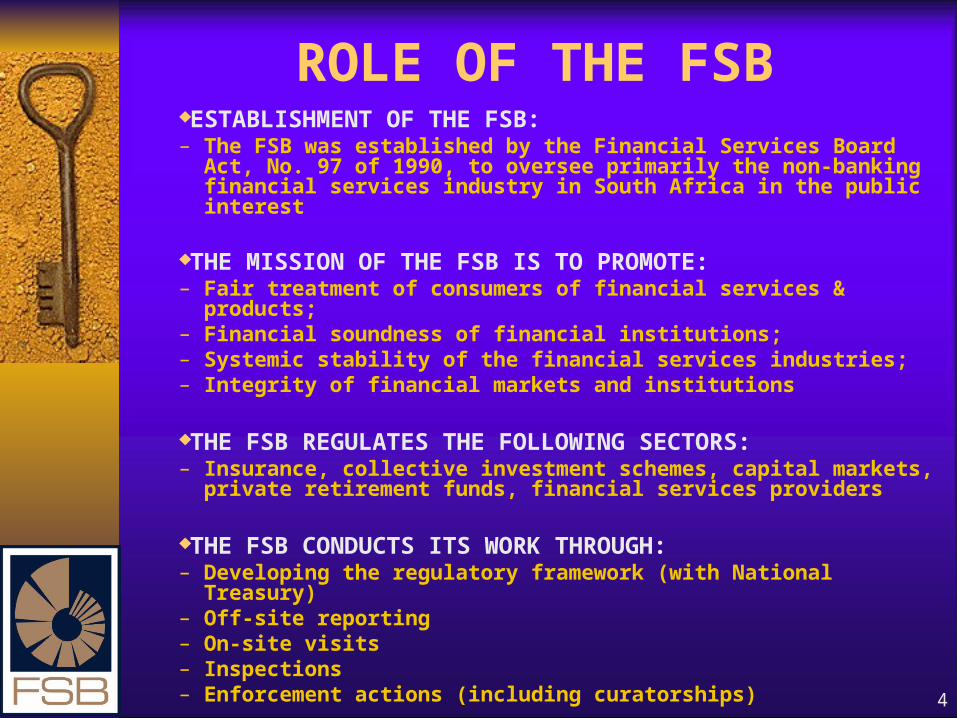

ROLE OF THE FSBESTABLISHMENT OF THE FSB:– The FSB was established by the Financial Services Board Act,

No. 97 of 1990, to oversee primarily the non-banking financial services industry in South Africa in the public interest

THE MISSION OF THE FSB IS TO PROMOTE:– Fair treatment of consumers of financial services & products;– Financial soundness of financial institutions;– Systemic stability of the financial services industries;– Integrity of financial markets and institutions

THE FSB REGULATES THE FOLLOWING SECTORS:– Insurance, collective investment schemes, capital markets,

private retirement funds, financial services providers

THE FSB CONDUCTS ITS WORK THROUGH:– Developing the regulatory framework (with National Treasury)– Off-site reporting– On-site visits– Inspections– Enforcement actions (including curatorships)

5

LESSONS FROM THE FINANCIAL CRISIS

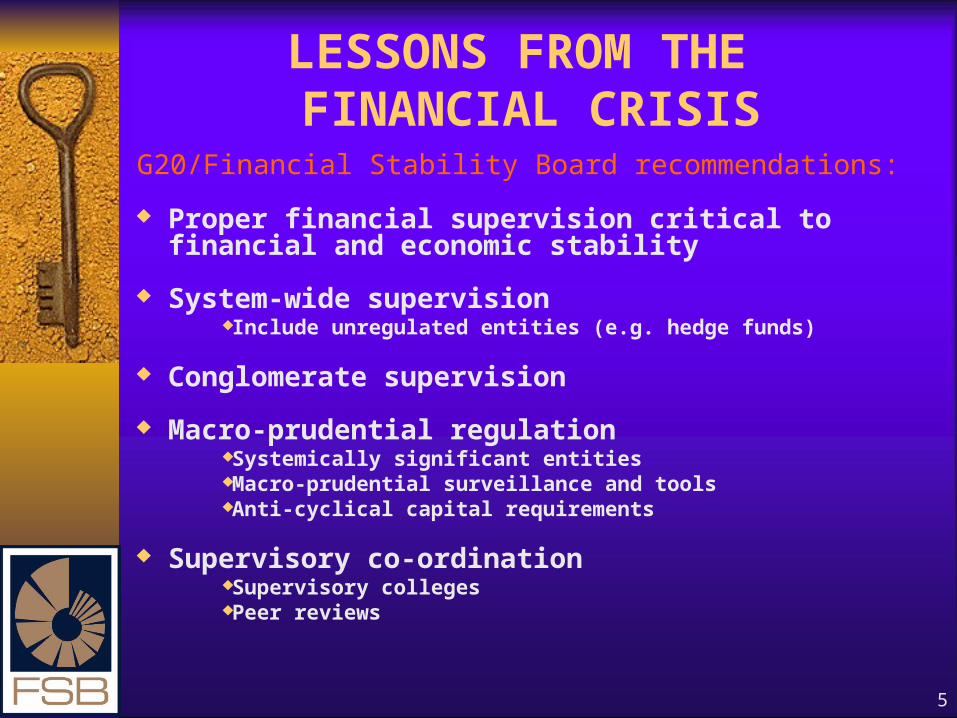

G20/Financial Stability Board recommendations:

Proper financial supervision critical to financial and economic stability

System-wide supervisionInclude unregulated entities (e.g. hedge funds)

Conglomerate supervision

Macro-prudential regulationSystemically significant entitiesMacro-prudential surveillance and toolsAnti-cyclical capital requirements

Supervisory co-ordinationSupervisory collegesPeer reviews

6

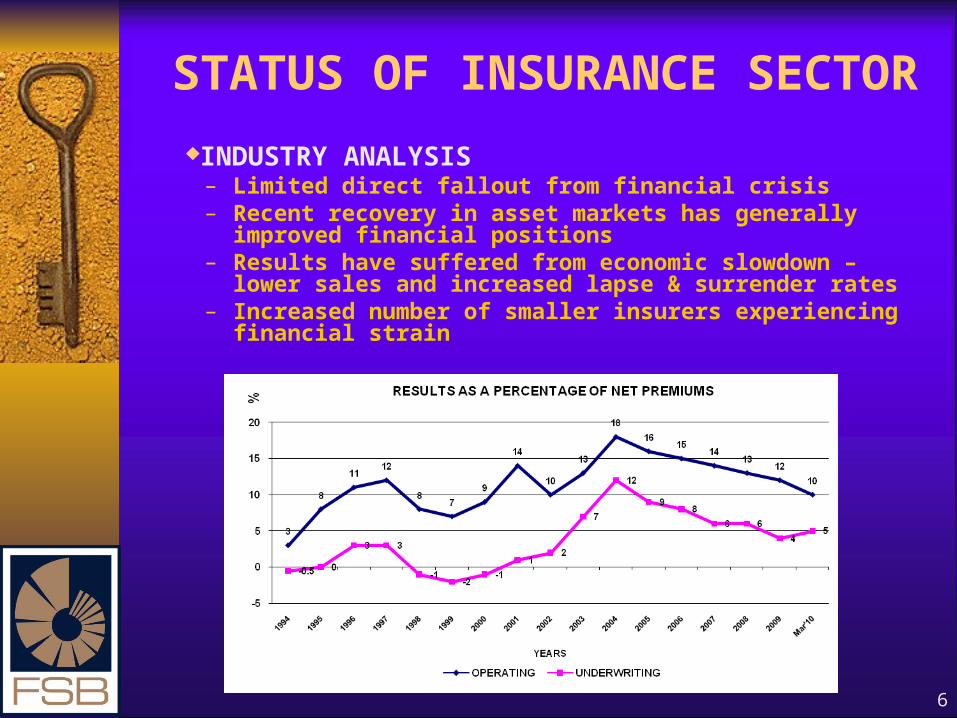

STATUS OF INSURANCE SECTOR

INDUSTRY ANALYSIS– Limited direct fallout from financial crisis– Recent recovery in asset markets has generally improved

financial positions– Results have suffered from economic slowdown – lower sales

and increased lapse & surrender rates– Increased number of smaller insurers experiencing financial

strain

7

INSURANCE SECTOR: FSB INITIATIVES

SOLVENCY ASSESSMENT AND MANAGEMENT (SAM)– Responding to IMF/World Financial Sector Assessment Program

(FSAP) recommendations– A revised, risk-based solvency regime for insurers to meet

international standards, but adapted for SA circumstances– Covers technical provisions, regulatory capital requirements, risk

management and reporting– Targeted implementation date January 2014– Inclusive project involving industry and other stakeholders

INSURANCE GROUP SUPERVISION– Legislative provisions– Reporting– Supervisory co-ordination

CONDUCT OF BUSINESS– Binder regulations: oversight over outsourced functions

MICROINSURANCE

8

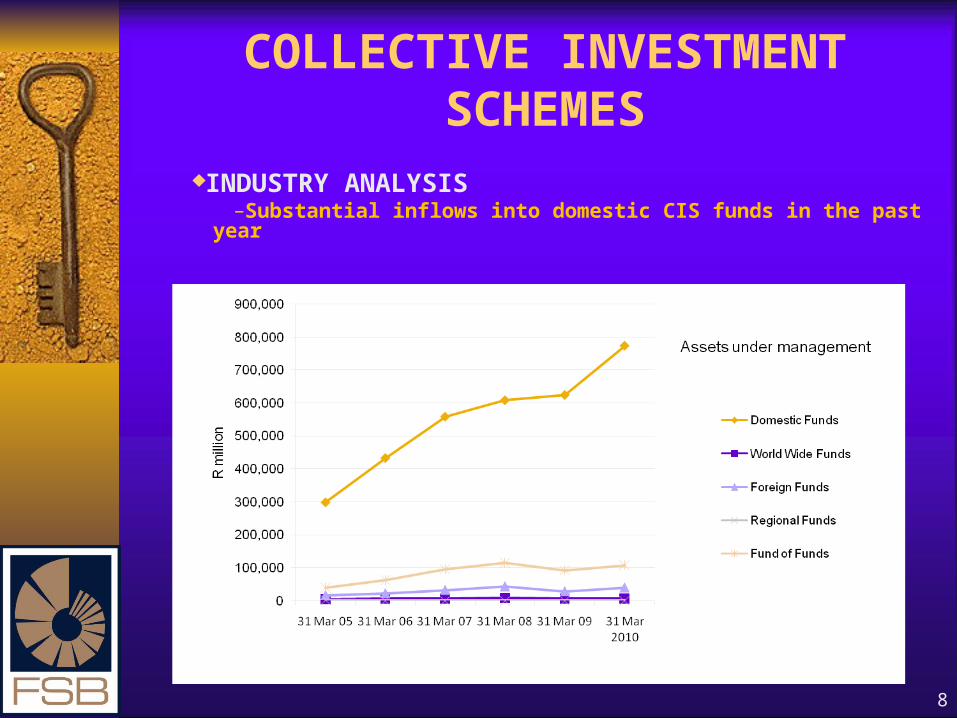

COLLECTIVE INVESTMENT SCHEMES

INDUSTRY ANALYSIS–Substantial inflows into domestic CIS funds in the past year

9

INVESTMENT INSTITUTIONS AND CAPITAL MARKETS: FSB INITIATIVES

COLLECTIVE INVESTMENT SCHEME ISSUES– Well-regulated sector, considerable inflows– Looking at: “white label” funds, “black box” products and types of

investments under Notice 1503

HEDGE FUND REGULATION– Joint NT/FSB working group developing regulatory proposals based

on international best practice (IOSCO and FSB/G20 guidance)

OVER THE COUNTER (OTC) DERIVATIVES– Working group established with representation from stakeholders

(NT, industry) to investigate the need for regulation of OTC products

CREDIT RATING AGENCIES– Discussion paper and draft Bill on regulation of credit rating

agencies submitted to the NT for consideration, informed by international best practice (IOSCO and FSB/G20 guidance)

JSE/BESA MERGER

JSE TRADING FAILURES

IOSCO CONFERENCE 2011

10

MARKET ABUSEDIRECTORATE OF MARKET ABUSE (DMA)

Committee of the Board of the FSB responsible for combating abuse in capital markets

Looks at issues such as insider trading, market manipulation and publication of false or misleading statements related to listed companies

During financial crisis, number of market manipulation cases linked to single stock futures increased

Post crisis, number of insider trading cases increased

Number of cases:

11

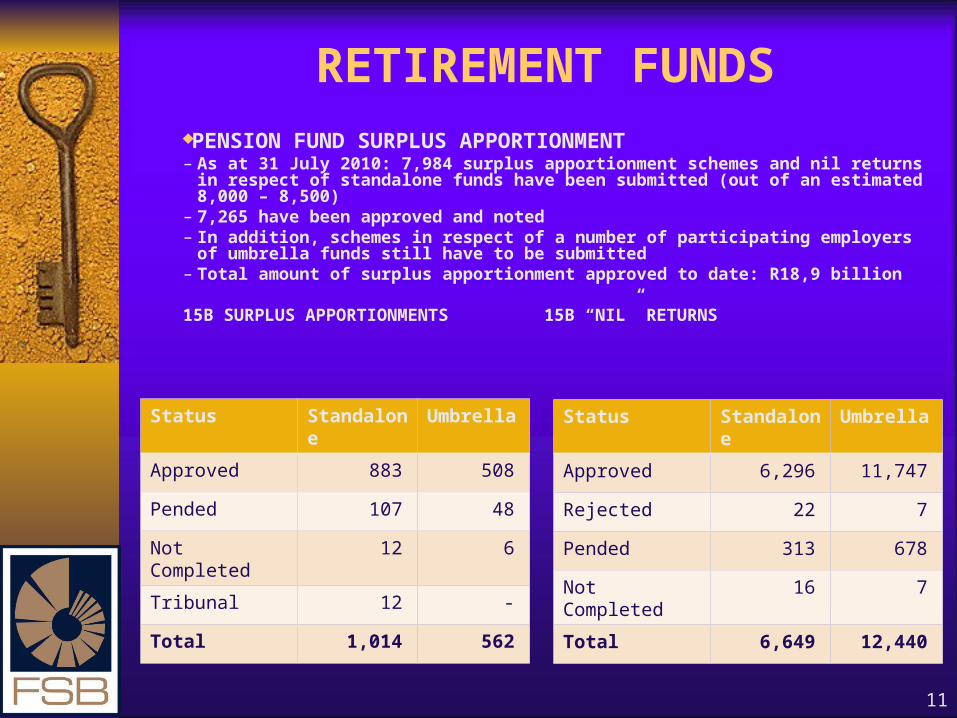

RETIREMENT FUNDSPENSION FUND SURPLUS APPORTIONMENT– As at 31 July 2010: 7,984 surplus apportionment schemes and nil returns in respect

of standalone funds have been submitted (out of an estimated 8,000 – 8,500)– 7,265 have been approved and noted– In addition, schemes in respect of a number of participating employers of umbrella

funds still have to be submitted– Total amount of surplus apportionment approved to date: R18,9 billion

15B SURPLUS APPORTIONMENTS 15B “NIL” RETURNS

Status Standalone Umbrella

Approved 883 508

Pended 107 48

Not Completed 12 6

Tribunal 12 -

Total 1,014 562

Status Standalone Umbrella

Approved 6,296 11,747

Rejected 22 7

Pended 313 678

Not Completed 16 7

Total 6,649 12,440

12

RETIREMENT FUNDS: FSB INITIATIVES

TRUSTEE GOVERNANCE– PF130 dealing with good trustee governance being

converted to a directive (becomes mandatory)

TRUSTEE TRAINING– Web-based Trustee Training Toolkit being developed– Implementation by mid-2011

13

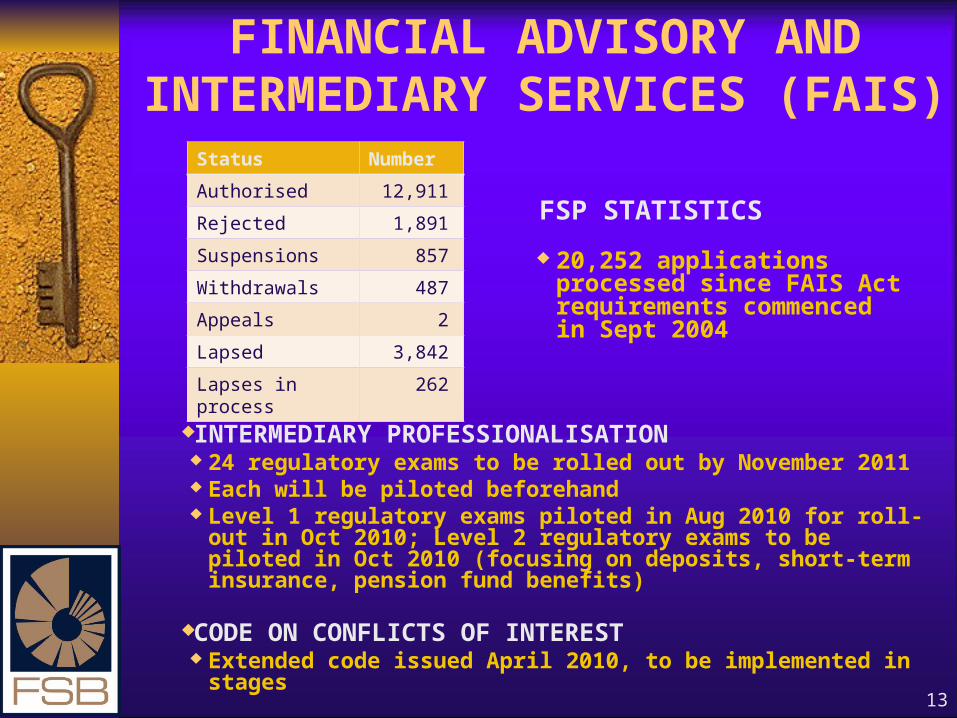

FINANCIAL ADVISORY AND INTERMEDIARY SERVICES (FAIS)

INTERMEDIARY PROFESSIONALISATION 24 regulatory exams to be rolled out by November 2011 Each will be piloted beforehand Level 1 regulatory exams piloted in Aug 2010 for roll-out in Oct

2010; Level 2 regulatory exams to be piloted in Oct 2010 (focusing on deposits, short-term insurance, pension fund benefits)

CODE ON CONFLICTS OF INTEREST Extended code issued April 2010, to be implemented in stages

Status Number

Authorised 12,911

Rejected 1,891

Suspensions 857

Withdrawals 487

Appeals 2

Lapsed 3,842

Lapses in process 262

FSP STATISTICS

20,252 applications processed since FAIS Act requirements commenced in Sept 2004

14

TREATING CUSTOMERS FAIRLY (TCF)

An outcomes-focused approach to ensuring that companies have an embedded culture of treating their customers fairly throughout the product life cycle

Based on UK Financial Services Authority (FSA) approach, adapted to SA circumstances

Behavioral change will be a multi-year project and requires: Clear regulatory guidance Self-assessment by financial institutions of their TCF culture Effective supervisory approach Visible enforcement

Discussion Paper issued April 2010

Further guidance by end-2010

15

FINANCIAL INCLUSION

MICROINSURANCE Response to problems of unregistered insurance business

and consumer abuse NT/FSB Policy position paper – September 2010 Dedicated legislative framework aimed at reducing regulatory

barriers to broadening access to insurance by low income consumers

Encouraging informal players (e.g. funeral parlours) to formalise

Visible enforcement

16

ENFORCEMENT

ENFORCEMENT COMMITTEE (EC) Established in terms of the Financial Institutions (Protection of

Funds) Act EC used to deal solely with sanctions arising from the

Directorate of Market Abuse, but mandate expanded with effect from November 2008

Registrar may refer contraventions of any FSB law, regulations, directives and codes of conduct to the EC

EC may impose unlimited penalties and make compensation and cost orders

EC determinations are published EC is a major step forward for FSB enforcement as it allows for

speedy administrative sanction EC has adjudicated on cases against 63 respondents, and

imposed a total of approximately R17 million in penalties, since 2006.

17

CONCLUSION

WE WOULD BE PLEASED TO ANSWER ANY QUESTIONS

THANK YOU