1 profitability analysis an extended look dr. nancy mangold california state university, east bay

TRANSCRIPT

1

Profitability AnalysisAn Extended Look

Dr. Nancy Mangold

California State University, East Bay

2

Interpreting ROAs

• What factors explain the consistly high or consistently low ROAs of some industries compared to the average of all industries

• What factors explain the fact that– certain industries have high profit margins and

low assets turnovers while– other industries experience low profit margins

and high assets turnovers

3

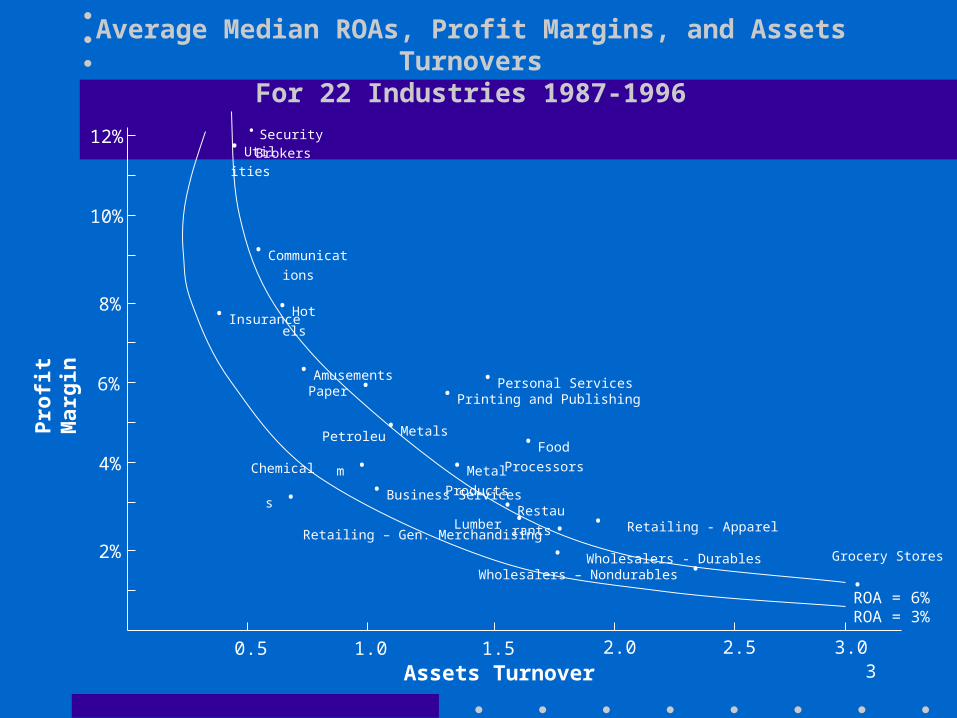

Pro

fit

Mar

gin

Assets Turnover

12%

6%

2%

4%

8%

10%

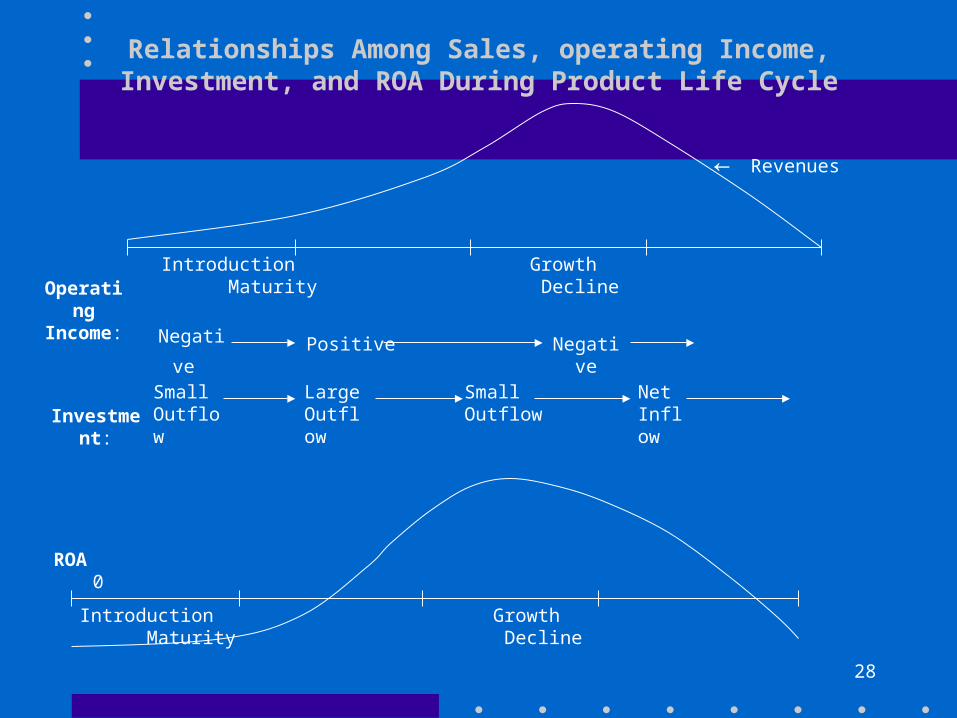

3.02.52.01.51.00.5

·Security Brokers·Utilitie

s

·Communication

s

·Insurance·Hotel

s

·AmusementsPaper · ·Personal Services·Printing and Publishing

·Metals ·Food

Processors

Petroleum

· ·Metal

Products

Chemicals

· ·Business Services·Restaurant

sLumber · · Retailing - ApparelRetailing – Gen. Merchandising ·

· Wholesalers - DurablesWholesalers – Nondurables ·

Grocery Stores

·ROA = 6%ROA = 3%

Average Median ROAs, Profit Margins, and Assets TurnoversFor 22 Industries 1987-1996

4

Operating Leverage

• Firms operate with different mixtures of fixed and variable costs in their cost structures

5

Operating Leverage

• Firms with high proportions of fixed costs

• High operating leverage firms

• Capital intensive industries– Utilities– Communications– Hotels– Petroleum– Chemical

6

Operating Leverage

• Firms with high proportions of variable costs

• Low operating leverage firms]

• Less capital intensive industries– Retailers– Wholesalers

7

Operating Leverage

• Firms with high proportions of fixed costs

• Significant increase in NI as sales increase– Fixed costs spread over a larger number of

units sold– average unit cost decreased

• Sharp decreases in NI when sales decrease

8

Operating Leverage

• High level of operating leverage

• Greater risk in their operations

• Should earn higher rates of return

9

Operating Leverage

• Unfortunately firms do not publicly disclose information about their fixed and variable cost structures

• One approach is to study the various cost items of a firm and attempt to identify the items that are likely to behave as fixed costs

10

Committed Fixed Costs

• Fixed costs committed regardless of actual level of activity during a period– Depreciation– Amortization– Rent – Lease payments

11

Discretionary Fixed Costs

• Firms can alter the amount of some other costs in the short run in response to operating conditions– R & D expenses– Maintenance– Advertising– Central corporate staff expenses

• Classify as FC or VC depending on behavior in a particular firm

12

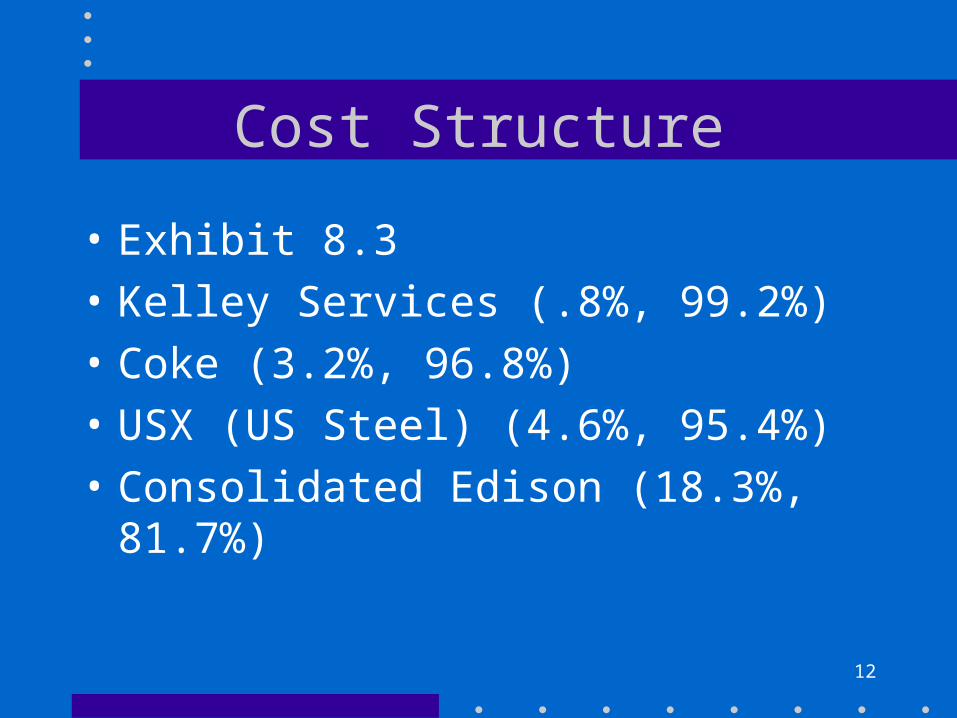

Cost Structure

• Exhibit 8.3

• Kelley Services (.8%, 99.2%)

• Coke (3.2%, 96.8%)

• USX (US Steel) (4.6%, 95.4%)

• Consolidated Edison (18.3%, 81.7%)

13

Cyclicality of Sales

• The sales of certain goods and services are sensitive to conditions in the economy– Construction services– Industrial equipment– Computers– Automobiles– Other durable goods

14

Cyclicality of Sales

• When the economy is in an upswing– Healthy GNP growth– low unemployment– Low interest rate

• Customers purchase high-priced items

• Sales of these firms grow

15

Cyclicality of Sales

• When the economy enters a recession

• Customers curtail their purchases

• The sales of these firms drop significantly

16

Noncyclical Sales

• Industries sell products that most consumers consider necessities– Grocery stores– Food processors– non-fashion clothing producers– electric utilities

• Products have lower per unit costs

17

Cyclicality of Sales

• Firms with cyclical sales patterns incur more risk

• Firms with non-cyclical sales patterns incur less risk

18

Cyclicality of Sales

• A firm can reduce its risk by

• Incorporate high proportion of variable cost in its cost structure– Pay employee hourly wage vs fixed salary– Rent building and equipment under short-term

cancelable leases instead of purchasing facilities

• Airlines, railroads

19

Cyclicality of Sales

• A noncyclical sales pattern can compensate for high operating leverage and neutralize risk

• Electric utilities

• Telecommunication firms

20

Product Life Cycle

• Product life cycle– Introduction– Growth– Maturity– Decline

21

Introduction & Growth

• Product development– High R & D spending

• Capacity enlargement– Capacity spending

• high uncertainty regarding the market viability of a firm’s products

22

Maturity Phase

• Firms have gained market acceptance– Reduce capital expenditures on operating

capacity

• More intense competition-reducing costs through– improved capacity utilization (economies of

scale)– more efficient production

23

Decline Phase

• Firms exit the industry as sales decline and profit diminish

24

Product Life Cycle & ROA

• Introduction & early growth phase

• Negative ROAs– high expenditures on product development,

marketing, capital expenditure– Low sales– operating losses

• Higher risk

25

Product Life Cycle & ROA

• High growth phase

• Positive ROAs– Positive operating income

• ROA does not grow as rapidly as sales– Product development– marketing– depreciation– heavy capital expenditures to build capacity for

expected higher future sales

26

Product Life Cycle & ROA

• Maturity phase

• ROA increases significantly– Economies of scale– learning curve benefits– curtailment of capital expenditures

• Lower risk

27

Product Life Cycle & ROA

• Declining phase

• ROA deteriorates– operating income decreases– may remain positive

28

Relationships Among Sales, operating Income, Investment, and ROA During Product Life Cycle

← Revenues

Introduction Growth Maturity DeclineOperatingIncome:

Negative Positive Negative

Investment:

SmallOutflow

LargeOutflow

SmallOutflow

Net Inflow

ROA 0

Introduction Growth Maturity Decline

29

Product Life Cycle - Industry Level

• Computer industry in all phases– Overall in high growth phase

• Soft drinks and food processing industries– maturity phase– constantly introduces new products

• Steel industry– declining phase– modernize production to stave off decline

30

Consistent ROAs in Exhibit 8.1

• Amusements industry- high ROA -– High operating leverage, growth, dominant

market positions

• Apparel Retailers - low ROA– risk of fashion obsolescence

• Insurance companies - low ROA– low operating leverage, low sales cyclicality– less risk of life cycle

31

Inconsistent ROAs in Exhibit 8.1

• Petroleum, Chemical and Hotel industries

• Lower ROA– high operating leverage– risk of sales cyclicality

• Due to excess capacity and obsolete plant assets

32

ROA and GAAP

• Food processors

• Major assets - Brand names

• GAAP – expensed advertising and development costs– Assets understated– ROA overstated

33

ROA and GAAP

• Publishing industry– Value of copyrights not recognized

• Service firms– Value of employees not an asset

• Reverse the immediate expensing of advertising, R & D, recognize it as assets

34

Differences in Profit Margin and Assets Turnover

• Microeconomic theory

• Firms and industries characterized by capacity constraint (heavy fixed capacity costs, lengthy periods to add new capacity)– Upper limit on the size of assets turnover– Must generate high profit margin to attract

sufficient capital (Area A in Exhibit 8.5)

35

Differences in Profit Margin and Assets Turnover

• Firms achieve high profit margin by

• entry barrier– large required capital outlays– high risks– regulations

• Explain communications, utilities, hotels, and amusements industries in Exhibit 8.1

36

Differences in Profit Margin and Assets Turnover

• Lack of entry barrier

• Excess capacity

• Explains low ROA for chemical and petroleum industries

37

Differences in Profit Margin and Assets Turnover

• Firms– Products are commodity-like in nature– Few entry barriers– Intense competition– Operate under competitive constraint

• Upper limit on achievable profit margin

• Strive for high asset turnovers to attract sufficient capital (Area C in Exhibit 8.5)

38

Differences in Profit Margin and Assets Turnover

• Firms achieve higher asset turnovers by– minimize fixed overhead costs– purchase in sufficient quantities to realize

discounts– integrate vertically or horizontally to obtain

cost savings

• Explains retailers and wholesalers

39

Differences in Profit Margin and Assets Turnover

• A area in Exhibit 8.5– Give up large profit margin to obtain asset

turnover– Emphasize actions to increase profit margin

• C area in Exhibit 8.5– Give up large assets turnover to achieve a

higher profit margin– Emphasize actions to increase assets turnover

40

Differences in Profit Margin and Assets Turnover

• Business Strategy

• Product differentiation– Product capabilities, quality, service, channels

of distribution

• Low cost leadership– economies of scale, production efficiencies,

outsourcing

41

Differences in Profit Margin and Assets Turnover

• Specialty retailers-

• Differentiation strategy

• Higher profit margin than general merchandise stores and grocery stores

42

Differences in Profit Margin and Assets Turnover

• External factors– Degree of competition– extent of regulation– entry barriers

• Internal strategic choices– Product differentiation– Low-cost leadership

43

Profit Margin Assets Turnover ROAForest Products IndustryLumber 3. 10% 1. 56% 5. 90%Paper Processing 6. 10% 1. 12% 6. 90%Printing and Publishing 6. 10% 1. 21% 7. 50%Apparel IndustryTextile Manufacturing 4. 30% 1. 45% 6. 10%Apparel Retailing 3. 90% 1. 74% 6. 40%Apparel Manufacturing 3. 10% 2. 26% 6. 90%Food IndustryFood Processors 4. 70% 1. 48% 7. 20%Grocery Stores 1. 90% 3. 27% 6. 30%Restaurants 3. 30% 1. 53% 5. 40%

EXHIBIT 8.7Average Annual Median Profit Margins, Assets Turnovers, and ROAs

for Selected Industries, 1987 to 1996

44

ROA and Value Chain Analysis

• Forest Products Industry

• Lumber– low profit margin (commodity product)– higher asset turnover

• Forest assets reported at acquisition costs

• Undervaluation of fixed assets

• overstates assets turnover

45

ROA and Value Chain Analysis

• Forest Products Industry

• Paper processing – higher profit margin than lumber– Capital intensive paper processing facilities– lower assets turnover

46

ROA and Value Chain Analysis

• Forest Products Industry

• Printing and Publishing– Higher profit margin

• Non-differentiated and differentiated products

– Capital intensive printing facilities– lower assets turnover– Highest ROA in industry

47

ROA and Value Chain Analysis

• Apparel industry

• Textile manufacturing – higher profit margin

• undifferentiated products - fabrics

– Lower asset turnover• capital intensive

• Risk of diseconomies of scale in capital-intensive manufacturing facilities

48

ROA and Value Chain Analysis

• Apparel industry

• Apparel manufacturing

• Higher profit margin– outsource manufacturing to lower wage rate

countries and– outsource to the brand names of apparel products

• Risk of exchange rate changes, political risk and fashion changes

49

ROA and Value Chain Analysis

• Apparel Industry

• Apparel Retailing

• Lower profit margin– small value-added activity– mixture of branded apparel and discount apparel

firms

• Risk of fashion changes and swings in consumer spending

50

ROA and Value Chain Analysis

• Food Industry

• Food processors– Highest profit margins - brand-name products– Lower asset turnovers - capital intensive in

food manufacturing

51

ROA and Value Chain Analysis

• Food Industry

• Grocery stores– Low profit margins - undifferentiated products– Higher asset turnover - less investment in

buildings and space

52

ROA and Value Chain Analysis

• Food Industry

• Restaurants

• Higher profit margin – brand name recognition– intense competition

• Lower asset turnover– investment in land and restaurant buildings

53

Supplementing ROA

• Analyzing Retailers

• Some own and some lease their stores

• Express sales, operating expenses, and operating income on a per square foot basis

• Exhibit 8.8

54

The GAP The LimitedPer Square FeetSales $418 $304Cost of Goods Sold (243) (202)Selling and Administrative (100) (65)Operating Income $75 $37Profit Margin for ROA 11. 2% 8. 0%Assets Turnover 1. 13 0. 99ROA 12. 6% 7. 9%

Profitability Ratios for The GAP and The Limited

EXHIBIT 8.8

55

Supplementing ROA

• Analyzing airlines

• Compute revenues and expenses– per available seat mile and– per seat miles flown

56

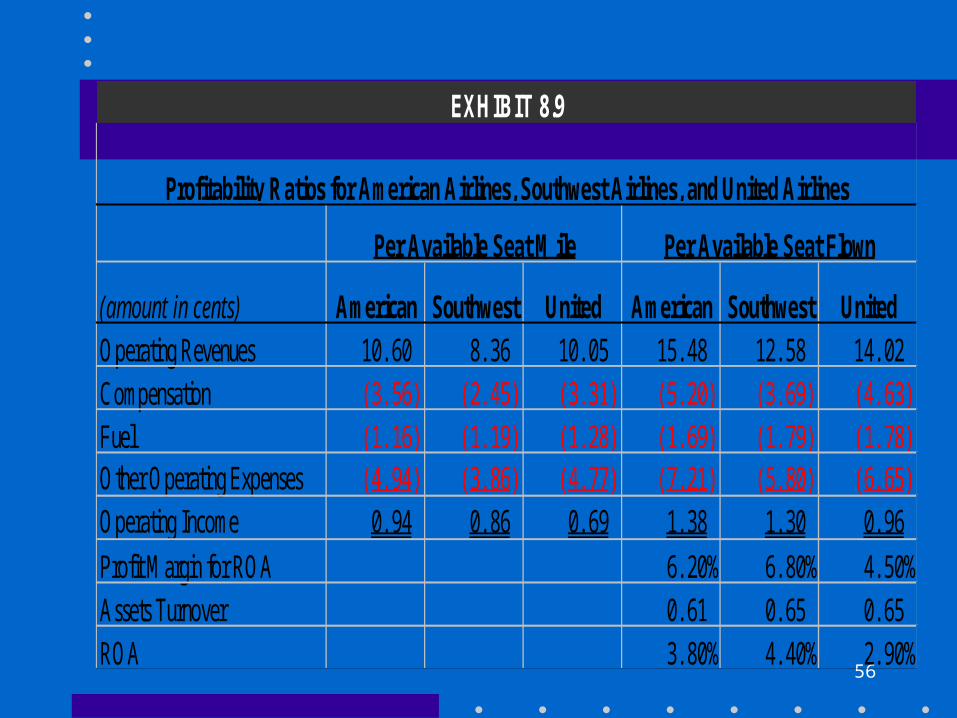

(amount in cents) American Southwest United American Southwest UnitedOperating Revenues 10. 60 8. 36 10. 05 15. 48 12. 58 14. 02Compensation (3. 56) (2. 45) (3. 31) (5. 20) (3. 69) (4. 63)Fuel (1. 16) (1. 19) (1. 28) (1. 69) (1. 79) (1. 78)Other Operating Expenses (4. 94) (3. 86) (4. 77) (7. 21) (5. 80) (6. 65)Operating Income 0. 94 0. 86 0. 69 1. 38 1. 30 0. 96Profit Margin for ROA 6. 20% 6. 80% 4. 50%Assets Turnover 0. 61 0. 65 0. 65ROA 3. 80% 4. 40% 2. 90%

Per Available Seat Mile Per Available Seat Flown

EXHIBIT 8.9

Profitability Ratios for American Airlines, Southwest Airlines, and United Airlines

57

Supplementing ROA

• Analyzing Advertising Firm

• Analyze income data on per employee basis

58

Interpublic Group Omni Group Grey AdvertisingPer EmployeeOperating Revenues $116, 936 $116, 373 $121, 508Compensation (61, 946) (68, 527) (75, 347)Administrative Expenses (36, 653) (33, 460) (36, 870)Operating Income before Income Taxes $18, 337 $14, 386 $9, 291Profit Margin for ROA 9. 7% 9. 2% 4. 6%Assets Turnover 0. 56 0. 70 0. 75ROA 5. 4% 6. 4% 3. 9%

EXHIBIT 8.10

Profitability Data for Interpublic Group, Omnicom Group and Grey Advertising

59

Supplementing ROA

• Analyzing Technology-Based Firms

• Two important resources not reported as assets– People– Technology (R & D expensed)

• Assets and net income understated