1 - ris.org.inris.org.in/images/ris_images/pdf/thirdibsa-nassif.pdf · 2 india, brazil and south...

TRANSCRIPT

www.bndes.gov.br 1

www.bndes.gov.br 2

INDIA, BRAZIL AND SOUTH AFRICA: STRATEGIC ECONOMIC OPPORTUNITIES IN THE MAP OF

INTERNATIONAL SPECIALIZATION

André NassifBrazilian Development Bank (BNDES)*

Av. República do Chile, 100 – Sala 1401Rio de Janeiro (RJ) - [email protected]

Third India, Brazil and South Africa Summit. The Academic Forum: IBSA Partnership for Shared Prosperity and Inclusive Globalization

13-14 October 2008New Dehli - India

www.bndes.gov.br 3

The theoretical approach:

The sources of international specialization in a static framework:

Comparative advantage (Ricardo, 1817; Helpman and Krugman, 1985)

Imperfect competition (scale economies and/or product differentiation)

(Krugman, 1987; Helpman and Krugman, 1985)

www.bndes.gov.br 4

Trade according to comparative advantage and imperfect competition among developed and

developing countries

U n ite d S ta te s

E u ro p e a nU n io n

B ra z il

In tra – in d u s tr ia l tra d e

D iffe re n t ia te d g o o dsa n d s c a le -in te ns iv em a n u fa c tu rin gp ro d u c ts

A g ric u ltu ra l g o od s a n d re s o u rc e -b a s e d m a n u fa c tu r in g

D iffe re n t ia te d g o o dsa n d s c a le -in te ns iv em a n u fa c tu rin gp ro d u c ts

In tra – in d u s tr ia l tra d e

In tra – in d u s tria l tra d e

A g ric u ltu ra l g o od s a n d re s o u rc e -b a s e d m a n ufa c tu r in g

S o u rc e : F re e ly a d a p te d fro m K ru g m a n (1 9 8 7 )

www.bndes.gov.br 5

The sources of international specialization in a dynamic framework:

Technological change (dynamic comparative advantage) Dosi, Pavitt and Soete (1990)

Coordinated investments (big push)(Murphy, Shleifer and Vishny, 1989; Fujita, Krugman and Venables, 1999)

Both are driven by industrial and technological policies

www.bndes.gov.br 6

Export composition of goods of Brazil and India according to technological intensity

1989 1994 1999 2004 1989 1994 1999 2004Primary Products 11.14 10.76 11.05 13.75 6.7 5.19 5.04 4.42Manufactured Products 87.89 88.08 88.73 85.31 93.14 94.66 94.78 95.37 Resource-based 32.78 34.61 36.05 34.65 19.54 17.82 13.93 21.72 Low Technology 28.05 25.22 20.84 19.29 57.41 59.33 61.77 49.71 Medium Technology 21.61 23.72 22.81 24.07 11.68 13.83 14.24 18.61 High Tecnnology 5.44 4.52 9.01 7.29 4.5 3.66 4.82 5.31Other transactions 0.95 1.14 0.2 0.92 0.14 0.14 0.17 0.2Total Exports 100 100 100 100 100 100 100 100

Note: Elaborated according to the original classification proposed by Lall (2000). For more details, see the Appendix of Lall (2000). Source: Nassif (2007, based on Comtrade data, Unctad - United Nations (http://www.unctad.org)

Brazil IndiaDescription

www.bndes.gov.br 7

However, in the case of India, if we add the export of commercial services in the total export:

Note: Exports of goods refer to 2003 and exports of commercial services refer to 2002Source: Nassif (2007, based on Comtrade data - Unctad (http://www.unctad.org)

Textile products8,6%

Apparel7,8%

Food and beverage

6,5%

Other commercial services

9,8%

Software, communication and IT services

20,6%Chemistry

9,1%

Furniture, toys and jewels

12,9%Other goods

24,8%

www.bndes.gov.br 8

India, Brazil and South Africa in the map of international specialization

www.bndes.gov.br 9

• The data: degree of specialization of 159 countries according to Balassa Index (BI) of comparative advantage

BI > 1 (industry has comparative advantage)

BI < 1 (industry has no comparative advantage)

www.bndes.gov.br 10

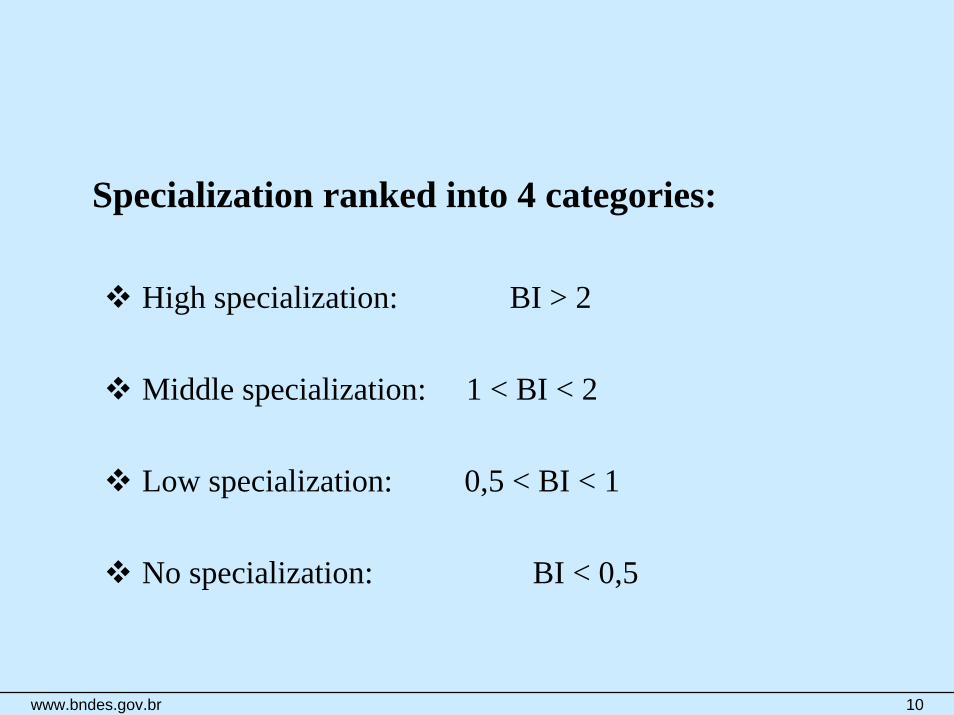

Specialization ranked into 4 categories:

High specialization: BI > 2

Middle specialization: 1 < BI < 2

Low specialization: 0,5 < BI < 1

No specialization: BI < 0,5

www.bndes.gov.br 11

Industries classified into 4 categories according to OECD taxonomy by technological intensity

Natural resource-based industries

Labor intensive industries

Capital intensive industries

High tech and science-based industries

“What you export matters for development”, Hausmann, Hwang and Rodrik, 2007:

www.bndes.gov.br 12

Map 1: Specialization in Natural Resource-Based Sectors – 2005*

* This year may differ for some countries. Source: UNComtrade (Puga and Nassif, 2008 ).

www.bndes.gov.br 13

Graph 2: Share of Natural Resource Based- Industries in Exports of SelectedCountries – 2005* (%)

0

10

20

30

40

50

60

70

80

Chi

na

US

A

Mex

ico

Tota

l

Indi

a

Can

ada

Braz

il

Chi

le

Aust

ralia

Arg

entin

a

Rus

sia

Farm Products Minning FuelsFood and Beverages Wood Pulp and PaperNon-Metal Mineral Manfct

9,3%15%

68%62%

56%

48%42%

29%26%

23%

71%

* This year may differ for some countries.

Source: UNComtrade (Puga and Nassif, 2008).

www.bndes.gov.br 14

Map 2: Specialization in Labor Intensive Sectors – 2005*

* This year may differ for some countries.

Source: UNComtrade (Puga and Nassif, 2008).

www.bndes.gov.br 15

Graph 3: Share of Labor Intensive Industries in Exports of Selected Countries –2005* (%)

0

5

10

15

20

25

30

35

40

Sout

h Af

rica

Braz

il

US

A

Ger

man

y

Mex

ico

Tota

l

Pol

and

Italy

Chi

na

Turk

ey

Indi

a

Textile Apparel Leather and Footwear Metal Products Furniture, Jewels, ...

6,4%

29%

23%

17%

8,5%7,5%

11%

6,7%10%

38%

32%

* This year may differ for some countries. Source: UNComtrade (Puga and Nassif, 2008) .

www.bndes.gov.br 16

Map 3: Specialization in Capital Intensive Sectors – 2005*

* This year may differ for some countries. Source: UNComtrade (Puga and Nassif, 2008).

www.bndes.gov.br 17

Graph 4: Share of Capital Intensive Industries in Exports of Selected Countries –2005* (%)

0

5

10

15

20

25

30

35

40

45

50

Chi

na

Rus

sia

Indi

a

Mex

ico

Bra

zil

Tota

l

USA

Hun

gry

Pol

and

Chi

le

Japa

n

Ger

man

y

Sou

th A

frica

Chemicals Rubber and Plastics Steel Industry Motor vehicles

14%

30%

24%

28% 29%

24%24%

42%

49%

41% 42%

32%35%

* This year may differ for some countries. Source: UNComtrade (Puga and Nassif, 2008).

www.bndes.gov.br 18

Map 4: Specialization in High Tech and Science-Based Sectors – 2005*

* This year may differ for some countries. Source: UNComtrade (Puga and Nassif, 2008).

www.bndes.gov.br 19

Graph 5: Share of High Tech and Science-Based Industries in Exports of SelectedCountries – 2005* (%)

0

10

20

30

40

50

Arge

ntin

a

Rus

sia

Aust

ralia

Indi

a

S. A

frica

Braz

il

Tota

l

Ger

man

y

Mex

ico

USA

Chi

na

Japa

n

Machinery and Equipments Office and Computing Machinery Electrical EquipmentComunications Equipments Precision and Optical Instrum. Aircraft, Ships, Raiways

48%47%

43%

38%

33%

11%

17%

8,5%8,3%3,9%3,9%

51%

* This year may differ for some countries. Source: UNComtrade (Puga and Nassif, 2008).

www.bndes.gov.br 20

Are there opportunities for strategic trade among IBSA?

If so, where?

www.bndes.gov.br 21

There are opportunities in industries with potential of intra-industrial trade and technological cooperation among India, Brazil and South Africa, mainly where the technological gaps are narrow.

www.bndes.gov.br 22

Brazil: “Política de Desenvolvimento Produtivo”(Policy for Industrial Development - 2008)

Brazilian Government targeted 35 industries for restructuring and/or industrial & technological policy

3 selected Areas:

Policies directed to strategic Areas: ICT Industries, Pharmaceuticals, Nuclear Energy, Biotechnology, among others

Policies directed to consolidate leadership: Aircraft, Oil, Ethanol, Metallurgy and Food Industries, among others

Policies to boost industrial competitiveness: Machinery and Equipment, Motor Vehicles, among others

www.bndes.gov.br 23

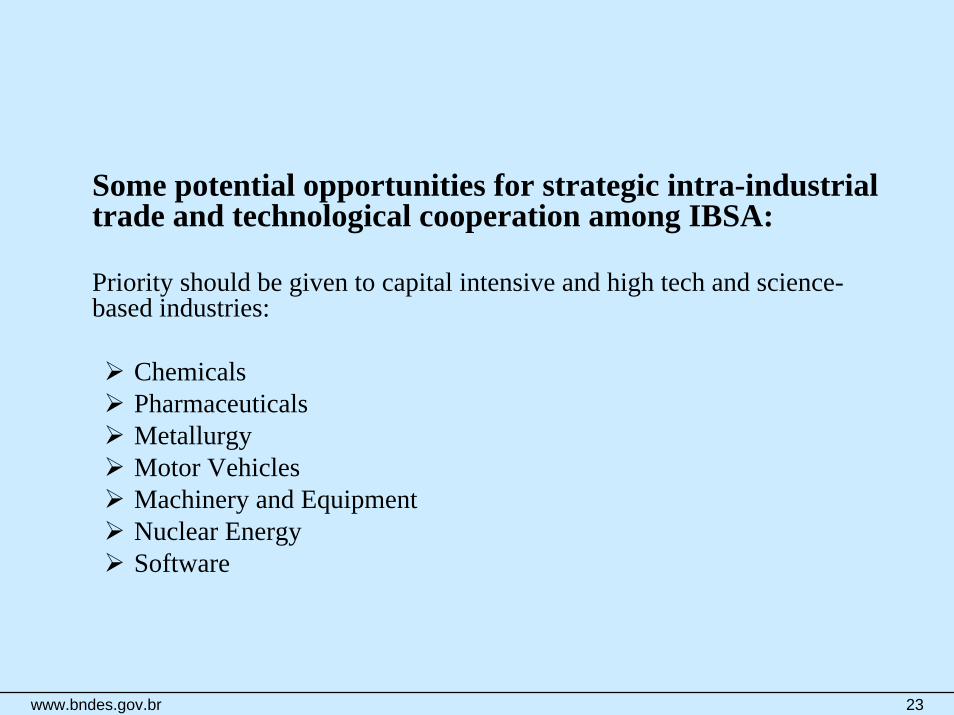

Some potential opportunities for strategic intra-industrial trade and technological cooperation among IBSA:

Priority should be given to capital intensive and high tech and science-based industries:

Chemicals PharmaceuticalsMetallurgyMotor VehiclesMachinery and EquipmentNuclear EnergySoftware

www.bndes.gov.br 24

THANK YOU VERY MUCH