1 roadmap for investing wisely leslie lum [email protected]

Post on 22-Dec-2015

213 views

TRANSCRIPT

2

The Roadmap

• Save

• Focus on financial goals

• Understand returns

• Understand risk

• Evaluate and asset allocation

• Monitor your investments

3

You are the “influencers”

• Many of you can directly benefit from this presentation

• Many of you have successfully navigated the financial journey

• We need you to be the “influencers” of those around you

4

Rule #1: You can make more money saving aggressively than you can investing aggressively.

5

How much does a typical family make?

6

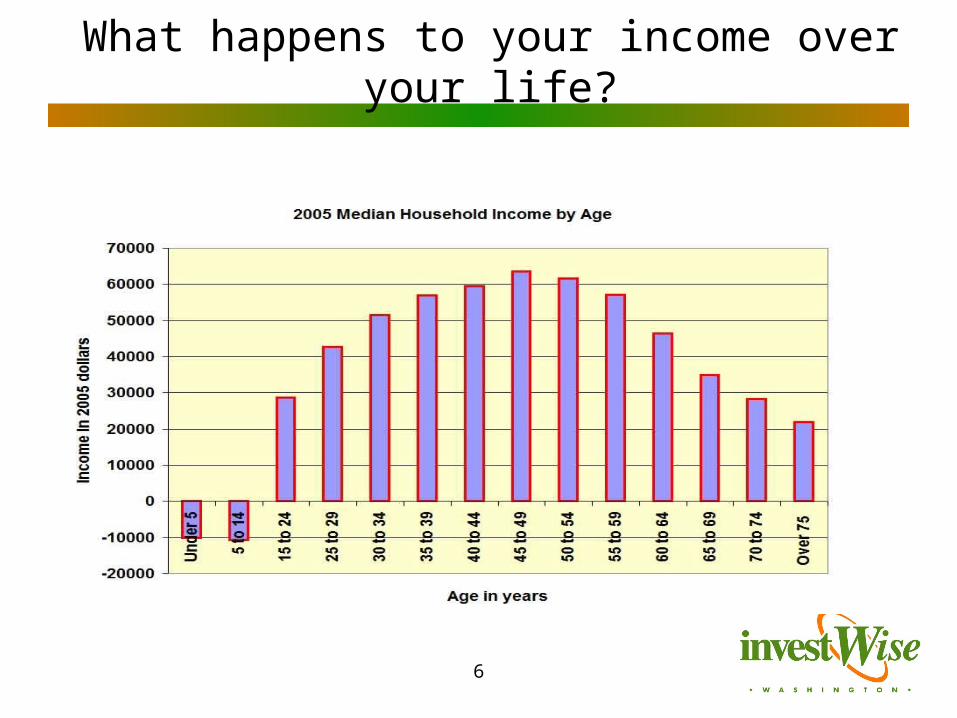

What happens to your income over your life?

7

How are we doing at savings?

Savings rate as a percent of disposable income

-5

0

5

10

15

20

25

30

1929 1934 1939 1944 1949 1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004

Source: http://www.bea.gov/bea/dn/nipaweb/TableView.asp#Mid

8

Could we save more?2004 Household Saving Rates

(as a percent of disposable income)

-4.0 -2.0 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0

Australia

Austria

Canada

Finland

France

Germany

Ireland

Italy

Japan

Korea

Netherlands

Norway

Sweden

Switzerland

United States

http://stats.oecd.org/WBOS/default.aspx?DatasetCode=REFSERIES

9

Rule #2: If you don’t have goals, you won’t achieve them.

10

Lay out your goals(Yours/your kids/your grandkids)

• Down payment on house

• Wedding

• College tuition

• Starting your own business

• Retirement

• Estate (Inheritance or charity)

11

Rule #3: Know how to measure returns (it will make you less

susceptible to fraud.)

12

Returns

Always calculate returns on an annualized basis

13

Calculate the return

• You will get your paycheck next week but you need $100 now. You arrange for a payday loan paying a fee of $15 for the use of $100. The payday loan company will collect the $100 electronically from your bank account when your pay check is deposited next week. What is the annual rate charged?

14

Calculate the lost return

You are a typical employee in your 20s who when you left your job in 2005 cashed out (66% do) your 401K account of less than $10,000. What is the cost of cashing out your account if your balance was $8000?

15

Rule #4: Understand risk

16

Investment Risks

• Market risk

• Business risk

• Interest rate

• Inflation risk

• Political risk

• Fraud risk

17

Cash

Annual Return on Cash (Treasury Bill Total Return 1971-2000)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

Source: Global Financial Data, www.globalfindata.com

Average 6.7%Standard Deviation 2.7%

About 70% of returns fall within one standard deviation of the average

18

BondsAnnual Return on Bonds (Total Return Government Bonds 1971-2000)

-10%

0%

10%

20%

30%

40%

50%

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

Source: Global Financial Data

Average 9.9%

Standard Deviation 9.3%

About 70% of returns fall within one standard deviation of the average

19

Annual Return on Stocks(Total Return S&P 500 1971-2000)

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

Source: Global Financial Data

Average 14.5%

Standard Deviation

16.5%

About 70% of returns fall within one standard deviation of the average

Stocks

20

The more return you need, the more risk you take.The more risk you take, the more return you need.

Major Asset Classes (1971-2000)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0% 2% 4% 6% 8% 10% 12% 14% 16%

Risk (Standard Deviation)

Return (Annual Return)

T-BillsAverage Return 6.7%

Standard Deviation 2.7%

BondsAverage Return 9.9%

Standard Deviation 9.3%

StocksAverage Annual Return 14.5%

Standard Deviation 16.5%

Lessons to learn:

If you want a higher return, you need to invest in riskier assets (stocks)

The more return, the more risk.

322% gain guaranteed?

Only if 322% loss guaranteed!

Return versus Risk

21

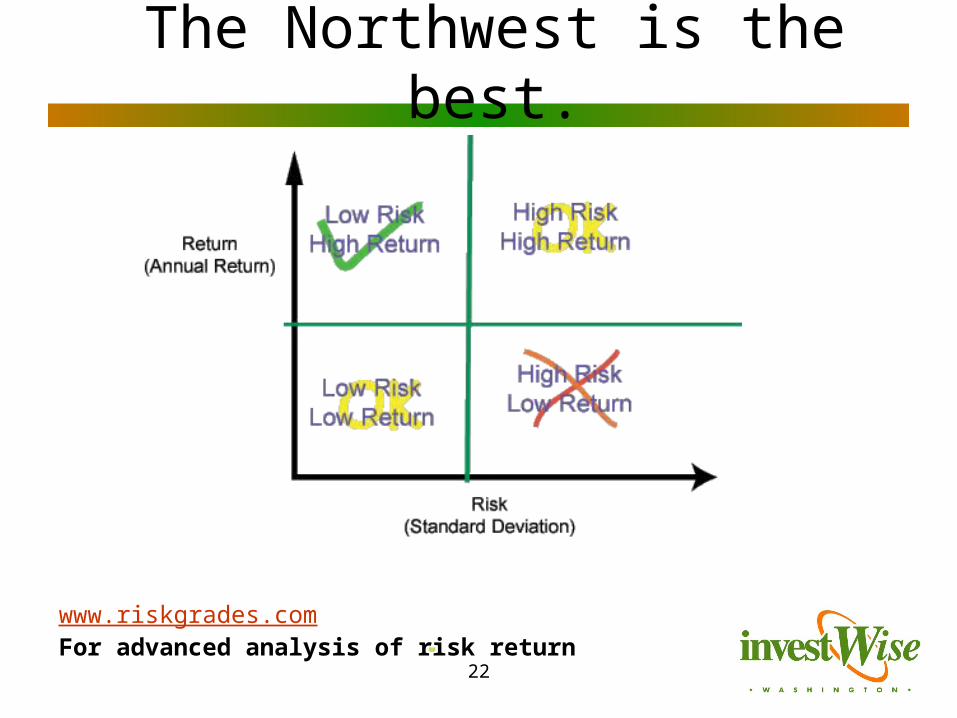

Given the same return, the investment with less risk is better

22

The Northwest is the best.

www.riskgrades.comFor advanced analysis of risk return

23

How do you get both a good return and low risk?

24

Risk of loss in stocks is high year to year

Annual Stock Price Changes from 1900 to 2006(Percent change year to year in S&P 500)

-55%

-35%

-15%

5%

25%

45%

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

25

Over 5 years, risk of loss is lower

Average Previous Five Years S&P 500 Gains

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

26

Over 10 years, risk of loss is small

Average Previous Ten Years S&P 500 Gains

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

27

Buy low, sell high or Buy high, sell low?

Source: John Bogle testimony to US Senate 11/3/03

28

Lesson?

• Buy and hold market index funds (doesn’t work for individual stocks)

• Have an emergency fund (3 to 6 months) to tide you over

• Have other sources of income so you don’t have to cash out during down markets

29

Rule #5: Asset allocate

30

All eggs in one basket?

• 34.6 percent of families had stock in only one company

• 59.5 percent had stock in three or fewer companies

• 9.5 percent had stock in fifteen or more companies

Source: 2004 Consumer Finance Survey

31

Two investments – double risk?

The key is having two

investments which aren’t correlated.

32

Adding a riskier investment to your portfolio

Adding 10% stock to a T-bill portfolio

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

2.0% 2.2% 2.4% 2.6% 2.8% 3.0% 3.2% 3.4% 3.6% 3.8% 4.0%

Risk (Standard Deviation)

Ret

urn

(A

vera

ge

An

nu

al %

)

90% T-Bill, 10% Stock

100% T-Bill

Increases return.

Reducesrisk!

Data based on 20 years of returns.

33

If you allocate the right amount you reduce risk and increase return!

Adding stock to a T-bill portfolio

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

21.0%

1.5% 3.5% 5.5% 7.5% 9.5% 11.5% 13.5% 15.5%

10% Stock

0% Stock

20% Stock

30% 40%

50%

60%

70%

80%

90%

100% Stock

Data based on 20 years of returns.

20% stock gives more return with about the same amount of risk

as 0% stock.

34

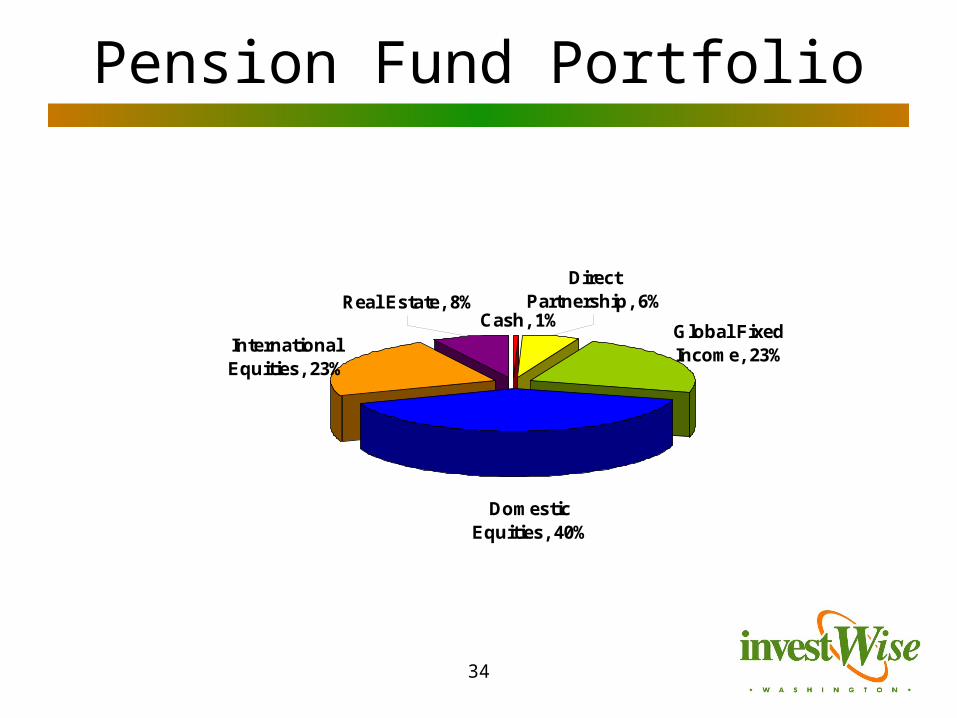

Pension Fund Portfolio

Cash, 1%International Equities, 23%

Domestic Equities, 40%

Global Fixed Income, 23%

Real Estate, 8%Direct

Partnership, 6%

California Pension System $230.3 Billion

Source: www.calpers.ca.gov Investment Portfolio Market Value as of Dec. 31, 2006

35

“Millionaires” Portfolio

Stocks45%

Bonds15%

Private Equity, 5%

International equities, 11%

Cash, 13%

Investment real estate, 7%

Other, 2%

Hedge Funds, 1%

Commodities, 1%

Households with investable assets

of $1 million to $10

million

Source: Fortune, 3/5/2007

36

401K Allocations by Age

20%

13%

13%

52%

Fixed Income

Company stock

Balanced funds

Equity funds

Asset allocation for participants in their 20s

Fixed Income, 38%

Company stock, 13%Balanced funds, 10%

Equity funds, 37%

Asset allocation for participants in their 60s

Source: Investment Company Institute

37

Lessons learned

• Don’t try to time the market• Allocate between asset classes based

on your income requirements, your financial goals and your time horizon

• Ladder your fixed income investments• Rebalance your portfolio (at least

annually) to sell at highs and buy at lows

38

Rule # 6: Always watch your money.

39

Evaluating funds

• Fund company/manager reputation

• Fund expenses

• Past performance (asset class)

• Fund risks

For information, check out www.morningstar.com

40

Use indices to monitor your portfolio

Annual Returns of Selected Asset Classes

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

2002 2003 2004 2005 2006

PhiladelphiaGoldSilver

S&P Midcap

Russell 2000 SmallCap

S&P 500

EAFE InternationalDeveloped

NAREIT RealEstate

41

Investment Advice

• According to the Consumer Federation about one-third of mutual fund investors rely completely on their advisors to choose investments and do not read about or research their investments

• Is this good?

42

• Spend time and take care in choosing your advisor

• Read all your statements, keep good records, and check for errors

• Only invest in what you understand (Warren Buffet rule #1)

• Assess your portfolio at least once a year against your cash requirements, financial goals and time horizon

Investment Advice

43

The Roadmap

• Save

• Focus on financial goals

• Understand returns

• Understand risk

• Asset allocation

• Monitor your investments