1 the fourth asian roundtable on corporate governance shareholder rights and the equitable treatment...

TRANSCRIPT

1

The Fourth Asian Roundtable on Corporate Governance

Shareholder rights and the Equitable Treatment of Shareholders

Kenichi OsugiProfessor of Commercial Law at Tokyo Metropolitan University

Protecting Minority Shareholders during Shifts in Corporate Control

Mumbai, India

11-12 November 2002

2

Two main topics

1) “A birth of outside shareholders”2) “Formation of controlling power”

I. The Theme

3

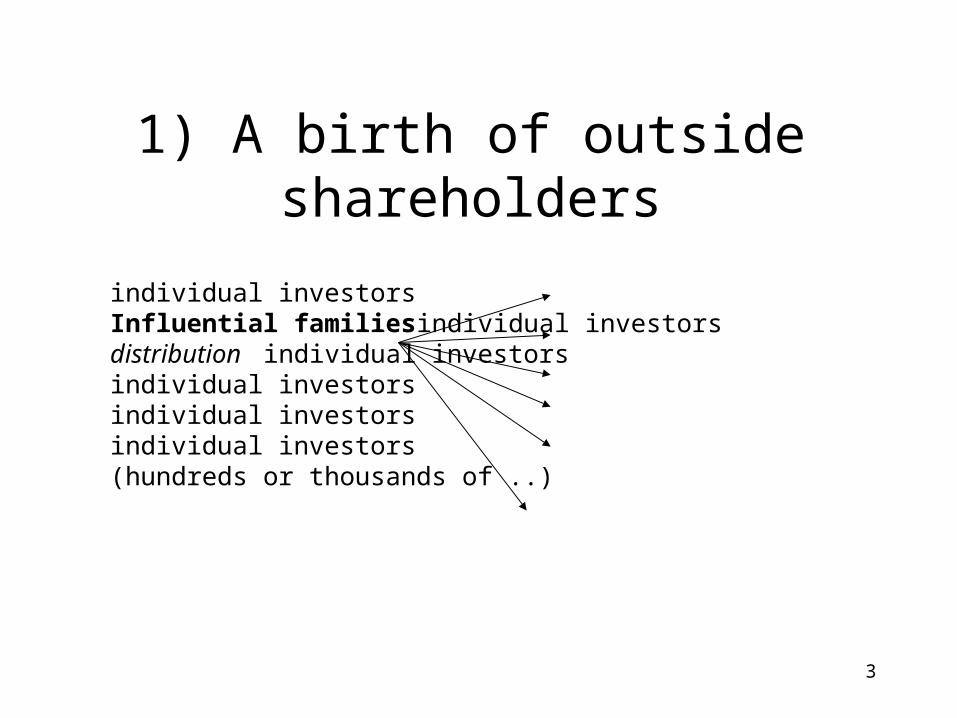

1) A birth of outside shareholders

individual investorsInfluential families individual investors

distribution individual investorsindividual investorsindividual investorsindividual investors

(hundreds or thousands of ..)

4

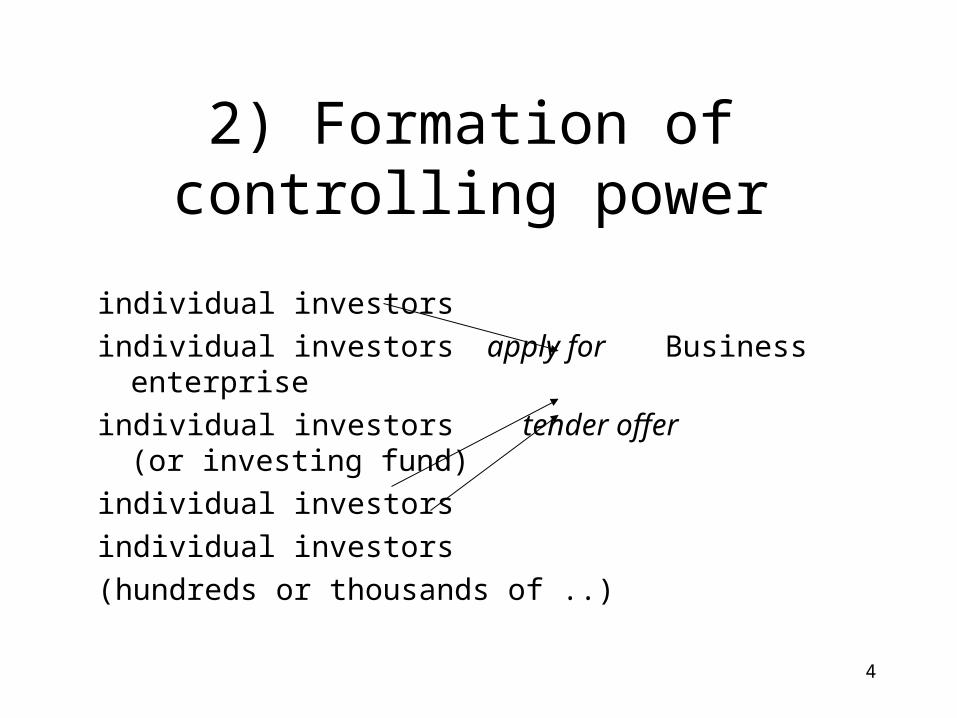

2) Formation of controlling power

individual investors

individual investors apply for Business enterprise

individual investors tender offer (or investing fund)

individual investors

individual investors

(hundreds or thousands of ..)

5

Two items:1. Asia is not unique in large ownership

2. OECD Principles of Corporate Governance, * No single model of good corporate governance * Emphasis on efficient and transparent markets for corporate control

6

II. Controlled Companies in the process of Going Public

- A Birth of Outside Shareholders

7

A birth of outside shareholders

individual investorsInfluential families individual investors

distribution individual investorsindividual investorsindividual investorsindividual investors

(hundreds or thousands of ..)

8

A large shareholder may abuse this controlling position after the outside shareholders participate in the company.

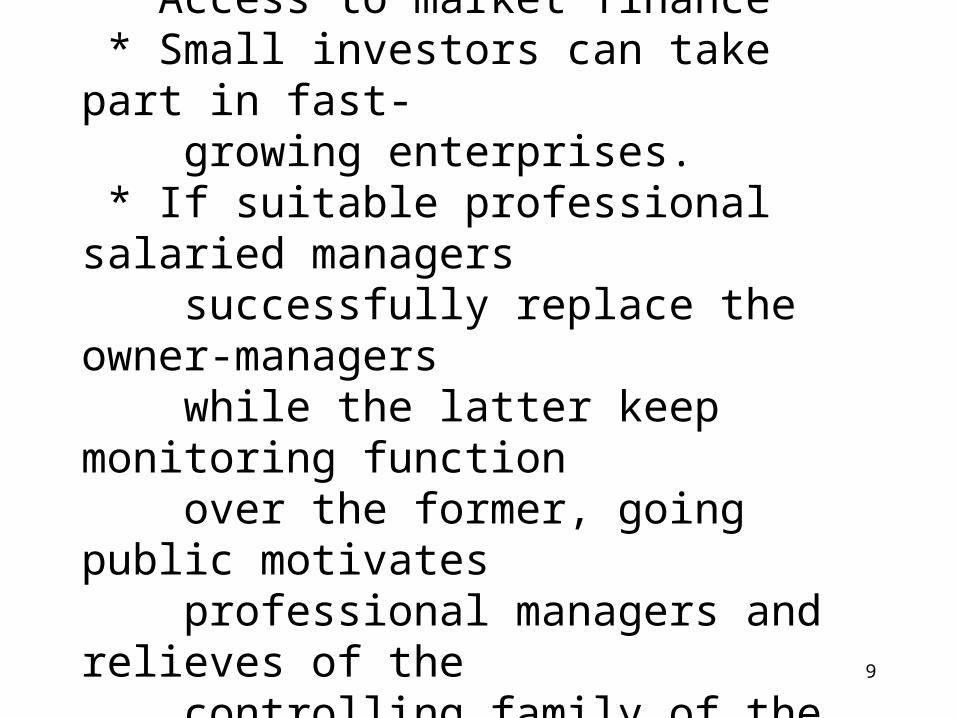

Going public could have several advantages.

9

* Access to market finance * Small investors can take part in fast- growing enterprises. * If suitable professional salaried managers successfully replace the owner-managers while the latter keep monitoring function over the former, going public motivates professional managers and relieves of the controlling family of the burden

10

Legal issues during listing process

Legal issues after listing process inter-related !

In the countries where post-listing protection is bad, law should limit the scope of listing of controlled companies,

e.g., law should prohibit a large owner selling less than [two-thirds] of her shares

11

However, better to have

Greater freedom when going public and tightening post-listing regulations, rather than narrower listing policy and looser post-listing regulations

1) Mandatory disclosure2) Penal and civil sanctions

12

3) “equality” policy = shareholders’ rights enjoyed by controlling shareholders and those enjoyed by the investing public shall be the same.

Flexibility necessary, since, some publishing companies legitimately want managers’ listing standards of stock exchanges

1) multiple classes of shares, distribute non-voting shares2) arrangement of disproportionately large control

13

III. Buyouts - Formation of Controlling Power

a new trend “hands on”

14

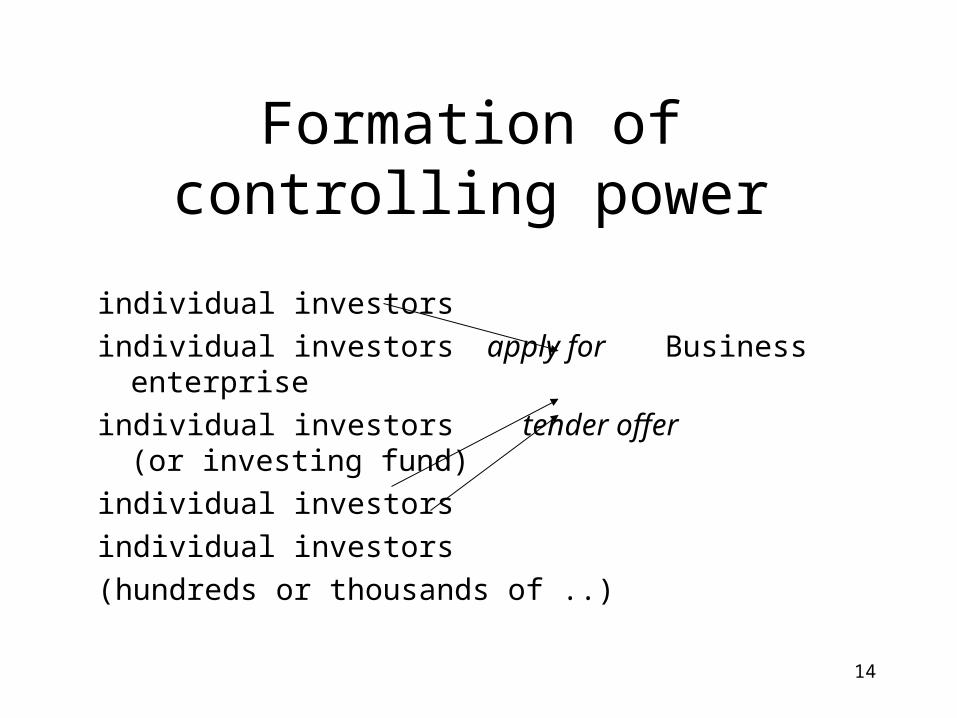

Formation of controlling power

individual investors

individual investors apply for Business enterprise

individual investors tender offer (or investing fund)

individual investors

individual investors

(hundreds or thousands of ..)

15

Suppose shares are traded at USD 100.A tender offer of $ 120. Shareholders believe the fair value should be more than $ 150. However, they feel oppressed, since their share value will decrease after the consummation of the offer.

“To sell, or not to sell.” decision is often distorted.Law shall intervene in buyouts to prevent.

16

Section 14 (e) of the 1934 US ActThe reason to have substantive regulations

Section 14 (d)(7) provides that the an acquirer shall not exclude any shareholders, and shall, if he raises the share price at a later date, give this higher price even to the shareholders who responded to the offer before the revision was made (best price rule).

17

Nevertheless, US regulation is not perfect. A partial tender offer, leftover minority shareholders fear the companies “going private” * Court judges review the transaction which forecloses leftover shareholders, * Prohibit the acquirer from buying minority shares at lower prices for [3 or 5 years] .

More sensible solution: an appraisal right on minority shareholders when a birth or change of a controlling shareholder.

18

Similarly essential is disclosure of a large block.

Section 13 (d) requires a blockholder with 5 % or more share holding to disclose her ownership and its increase or decrease. Because buying or selling by blockholders affects the market price of the company.

19

IV. Concluding Remark

“Long-term value for the entire shareholders” is the closest index of development of a national economy. Especially when evolution and dynamics is more important than stability in corporate management, creative destruction rather than a stable order.

20

Function is more important than form.

eg. Japan’s “venture bubbles.” = Creating a stock market and letting large companies enlist will not necessarily increase national wealth.

21

Western companies (especially investment funds) buying out Asian companies.

Collision of cultures* The Asian side needs to show patience and have an open mind, * The Western side should fulfil their moral obligation to explain and care for fair distribution of the fruits of economic success.

22

Shifts in Corporate Control

= Crossroads where Eastern and Western capitalism meet each other, filled with unknown possibilities and risks.

THE END