1. the light vehicle market, advertising & the economy phil brady, nada president national...

TRANSCRIPT

1

The Light Vehicle Market, Advertising & the Economy

Phil Brady, NADA PresidentNational Automobile Dealers Association, McLean, VAwww.nada.org

Television Bureau of AdvertisingAnnual Forecast ConferenceNew York CitySeptember 5, 2002

2

Franchised Auto Dealers are a Vital Cog in the U.S. Economy

Franchised Auto Dealers are a Vital Cog in the U.S. Economy

• At around a trillion dollars per year, the auto retailing business is the largest retail industry in America. Franchised New Car Dealers account for over $700 billion, or 70 percent

• Twenty-two percent of retail sales in the U.S. today are generated at franchised new car dealerships

• New light vehicle sales have enjoyed the 3 best years in history, 1999 - 2001.

• NADA expects 2002 to be 4th best sales year

• At around a trillion dollars per year, the auto retailing business is the largest retail industry in America. Franchised New Car Dealers account for over $700 billion, or 70 percent

• Twenty-two percent of retail sales in the U.S. today are generated at franchised new car dealerships

• New light vehicle sales have enjoyed the 3 best years in history, 1999 - 2001.

• NADA expects 2002 to be 4th best sales year

3

Source: NADA Industry Analysis

4

6

8

10

12

14

16

18

20

Mill

ion

s o

f U

nit

s

2001 = 17.1 million units (New)2002E = 16.8 million units (New)

2001 = 13.3 million units (Used)2002E = 13.2 million units (Used)

New Car & Light Duty Truck Sales were Well Above the Trend Line in Recent Years

(millions of units)

New Car & Light Duty Truck Sales were Well Above the Trend Line in Recent Years

(millions of units)

4

Source: NADA Industry Analysis

0

2

4

6

8

10

12

14

16

18

20

Mill

ion

s o

f U

nit

s

Cars Lt. Trucks

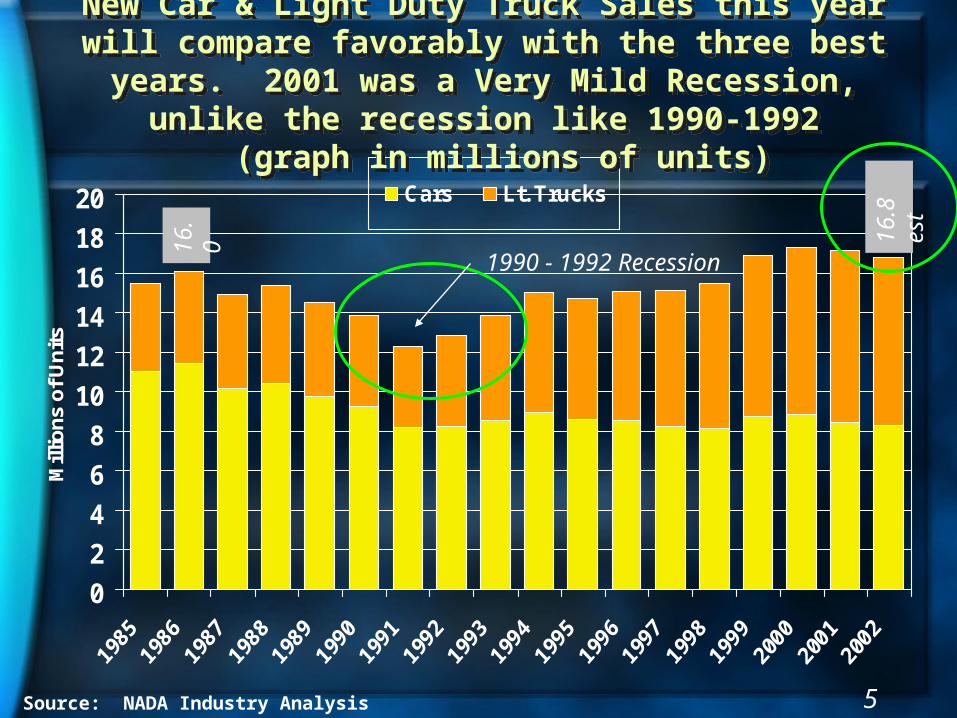

New Car & Light Duty Truck Sales this year will compare favorably with the three best years. 2001 was a Very Mild

Recession, unlike the recession like 1990-1992 (graph in millions of units)

New Car & Light Duty Truck Sales this year will compare favorably with the three best years. 2001 was a Very Mild

Recession, unlike the recession like 1990-1992 (graph in millions of units)

1990 - 1992 Recession

16.8

es

t

16.

0

5

Source: NADA Industry Analysis

0

2

4

6

8

10

12

14

16

18

20

Mill

ion

s o

f Un

its

Lt. Trucks

Cars

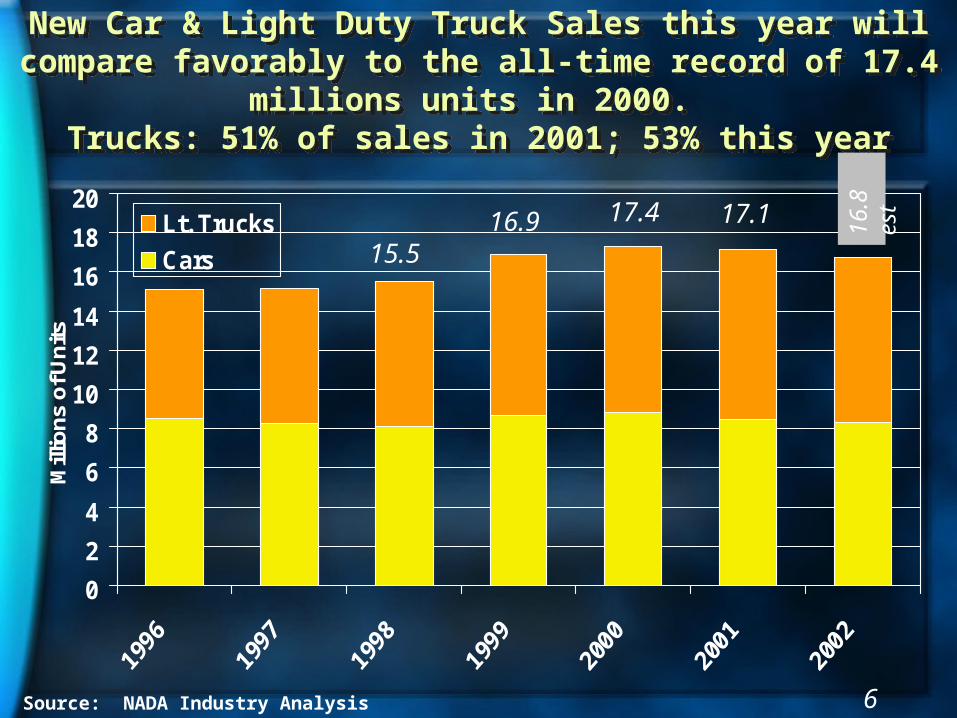

New Car & Light Duty Truck Sales this year will compare favorably to the all-time record of 17.4 millions units in 2000.

Trucks: 51% of sales in 2001; 53% this year

New Car & Light Duty Truck Sales this year will compare favorably to the all-time record of 17.4 millions units in 2000.

Trucks: 51% of sales in 2001; 53% this year

16.8

es

t

15.516.9 17.4 17.1

6

“Crossover” sales, a subset of SUVs, Show Most of the Growth in Sales and a Strong Change in U.S. Segment Share of New Light-Vehicle Sales (YTD July 2002 Vs YTD July 2001).Truck-based SUVs and Luxury Cars gained slightly in share.

“Crossover” sales, a subset of SUVs, Show Most of the Growth in Sales and a Strong Change in U.S. Segment Share of New Light-Vehicle Sales (YTD July 2002 Vs YTD July 2001).Truck-based SUVs and Luxury Cars gained slightly in share.

-1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0%

Small Car

Mid Car

Large Car

Luxury Car

Crossover Utility Vehicles

Truck-Based SUV's

Van

Pickup

Percentage Point Change in Share of Sales, YTD July 2002 and YTD July 2001

Source: Ward’s Automotive *Crossover Utility Vehicles are built on unitized car platforms 7

Korea and other lower volume countries show the largest Change in Sales by Country of Origin Share Change in U.S. New Light-Vehicle Sales, YTD July 2002 Vs. YTD July 2001

Korea and other lower volume countries show the largest Change in Sales by Country of Origin Share Change in U.S. New Light-Vehicle Sales, YTD July 2002 Vs. YTD July 2001

-2.5% -2.0% -1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5%

North America(Domestic)

Germany

Japan

S. Korea

Others

Percentage Point Change in Share of Sales, YTD July 2002 and YTD July 2001

Source: Ward’s Automotive 8

Source: Ward’s Automotive

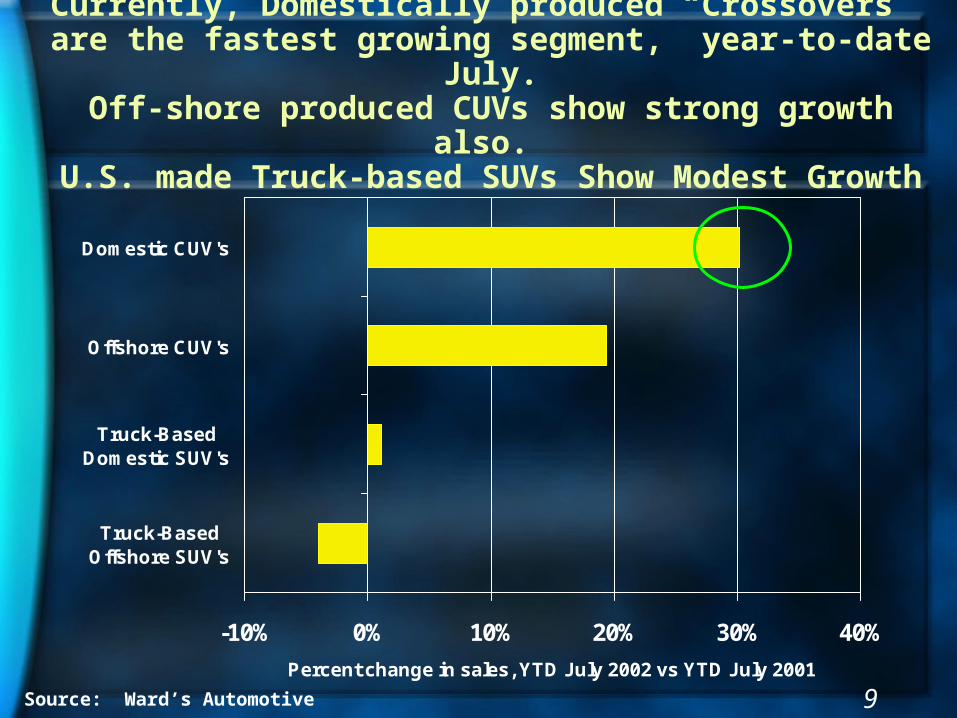

Currently, Domestically produced “Crossovers” are the fastest growing segment, year-to-date July.Off-shore produced CUVs show strong growth also. U.S. made Truck-based SUVs Show Modest Growth

-10% 0% 10% 20% 30% 40%

Truck-BasedOffshore SUV's

Truck-BasedDomestic SUV's

Offshore CUV's

Domestic CUV's

Percent change in sales, YTD July 2002 vs YTD July 2001

9

Net Household Wealth = Total Financial Assets - Total Liabilities

(excludes home equity but includes all mortgage debt)

Source: Federal Reserve Flow of Funds Data, Z.1., Table L.10.

$0

$5

$10

$15

$20

$25

$ T

rill

ion

sU.S. Household Net Financial Assets Doubled

from 1994 through 1999 (5 years)Then the impact of Equity Market Corrections ensued

U.S. Household Net Financial Assets Doubled from 1994 through 1999 (5 years)

Then the impact of Equity Market Corrections ensued

10

Net Household Wealth = Total Financial Assets - Total Liabilities

Source: Federal Reserve Flow of Funds Data, Z.1., Table L.10., Ward’s Automotive

$12

$14

$16

$18

$20

$22

$24

$ T

rilli

on

s

350000

370000

390000

410000

430000

450000

470000

490000

510000

Un

its

Net Houshold Assets (wealth) Luxury Vehicle Sales (right axis)

Looking at the Correction by Quarters:U.S. Net Household Assets fell during Stock Market

Corrections, which subdued Luxury Light Vehicle Sales(Blue Line)

Looking at the Correction by Quarters:U.S. Net Household Assets fell during Stock Market

Corrections, which subdued Luxury Light Vehicle Sales(Blue Line)

estim

ate

d

Incentives for Luxury Makes Have Helped Increase Sales Recently

11

How Have Light Vehicle Sales Remained So Strong?Total Dealership Advertising Spending Jumped

with Record Vehicle Sales

$0

$1

$2

$3

$4

$5

$6

$7

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

Bil

lio

ns

of

do

lla

rs

Source: NADA Industry Analysis 12

Franchised Dealers’ Overall Ad Spending increased 3.7% in 2001 compared with 2000,

shown below by media

Franchised Dealers’ Overall Ad Spending increased 3.7% in 2001 compared with 2000,

shown below by media

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

Newspapers Radio TV & CableTV

Direct Mail Internet Other

Ad

Sp

end

ing

200

1 vs

200

0 (m

illi

on

s o

f d

oll

ars)

2000 2001

Source: NADA Industry Analysis

*Other includes items such as Community/Event Sponsorship,

Billboard/Transit Ads, Yellow Pages/Shopper Flyers,

and Magazines

13

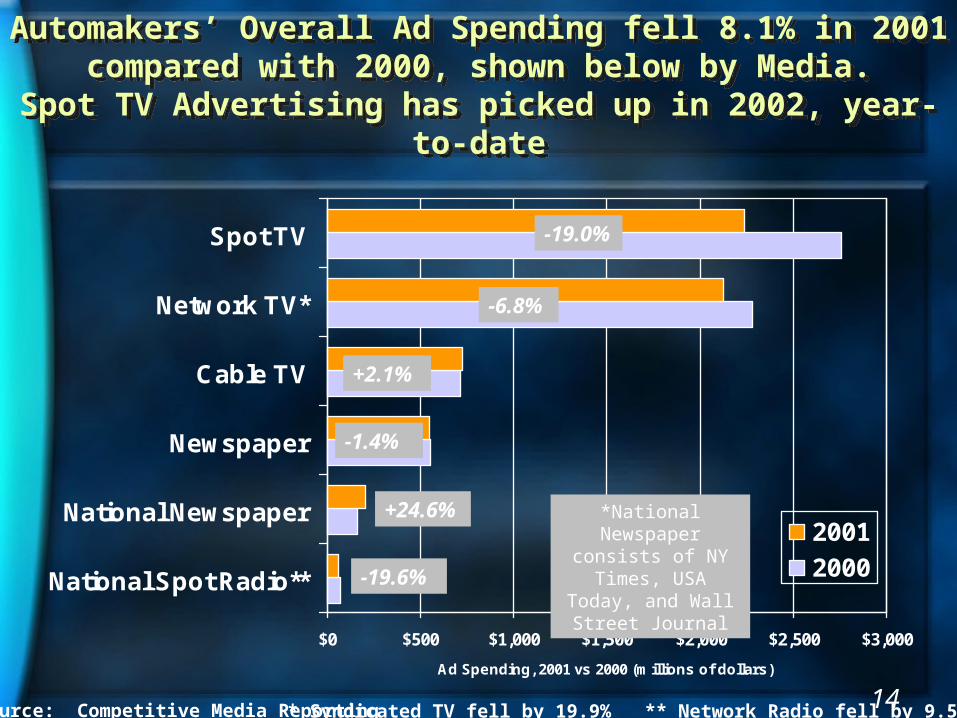

Automakers’ Overall Ad Spending fell 8.1% in 2001compared with 2000, shown below by Media.

Spot TV Advertising has picked up in 2002, year-to-date

Automakers’ Overall Ad Spending fell 8.1% in 2001compared with 2000, shown below by Media.

Spot TV Advertising has picked up in 2002, year-to-date

$0 $500 $1,000 $1,500 $2,000 $2,500 $3,000

National Spot Radio**

National Newspaper

Newspaper

Cable TV

Network TV*

Spot TV

Ad Spending, 2001 vs 2000 (millions of dollars)

2001

2000

Source: Competitive Media Reporting

*National Newspaper consists of NY

Times, USA Today, and Wall Street

Journal

14* Syndicated TV fell by 19.9% ** Network Radio fell by 9.5%

-19.0%

-6.8%

+2.1%

-1.4%

+24.6%

-19.6%

40

60

80

100

120

140

160

180

1977 III 1982 III 1987 III 1992 III 1997 III 2002

NA

DA

Ind

ex M

easu

re

Optimism

Sales

Source: NADA Industry Analysis

NADA Dealer Optimism Index in July Reflects Market Concerns, but Overall Consumer Confidence is still

Reasonably Strong

NADA Dealer Optimism Index in July Reflects Market Concerns, but Overall Consumer Confidence is still

Reasonably Strong

15

89 % of Dealerships now have a Website, Up from 47 % in 1997

Internet will help Future New Light Vehicle Sales

61%

82%89%

74%

47%

87%81%

52%

37%

69%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1997 1998 1999 2000 2001

WebsiteInteractive Website

Source: NADA Industry Analysis 16

More Services are Offered on Dealership Websites in 2001 compared with 1997

More Services are Offered on Dealership Websites in 2001 compared with 1997

22%

9%

28%

26%

24%

26%

44%

55%

25%

27%

56%

57%

65%

73%

76%

89%

0% 20% 40% 60% 80% 100%

Order on-line

Link to fin'l., ins. & auto sites

Schedule sales appt

Fill out finance

Schedule service appt

View MSRP

Link to mfr web site

View stock

2002

1997

Source: NADA Industry Analysis 17

18