1 time value of money many financial decisions require comparisons of cash payments at different...

Post on 20-Dec-2015

214 views

TRANSCRIPT

1

Time Value of Money

Many financial decisions require comparisons of cash payments at

different dates

Example: 2 investments that require an initial investment of $100

Timing Inv 1 Inv 2

After 1 year $30 $20

After 2 years $30 $20

After 3 years $30 $40

After 4 years $30 $60

If you should choose one of them, which would you choose?

2

Compounding

Future Value: amount to which an investment will grow after earning interest

Compounding: the process of accumulating interest in an investment over time to earn more interest

Compound interest: Interest earned on both the initial principal and the reinvested interest from prior periods

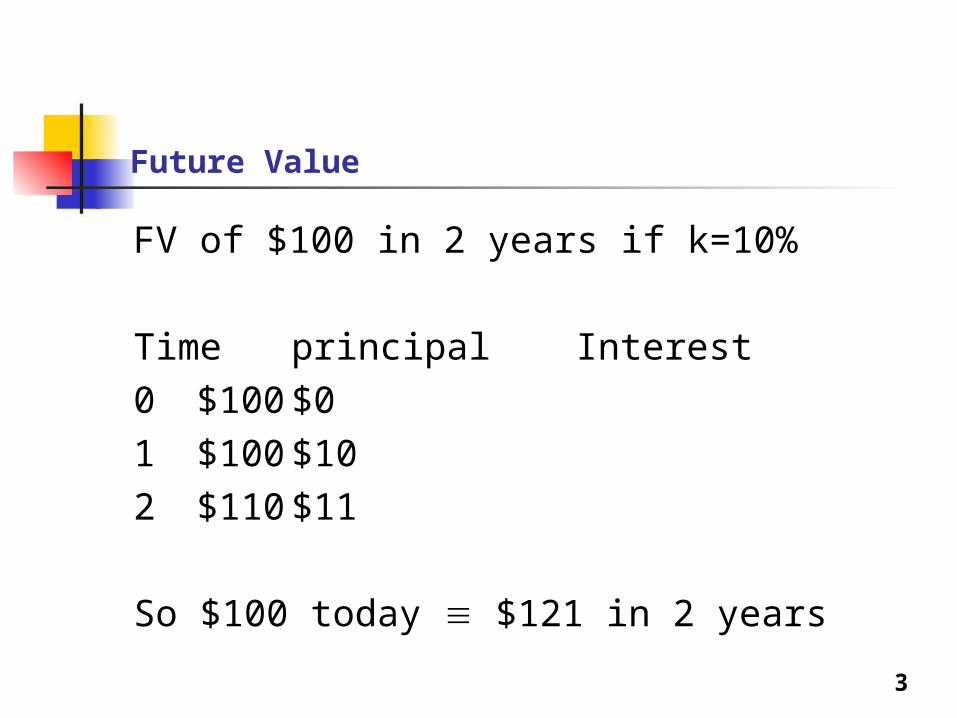

3

Future Value

FV of $100 in 2 years if k=10%

Time principal Interest0 $100 $01 $100 $102 $110 $11

So $100 today $121 in 2 years

4

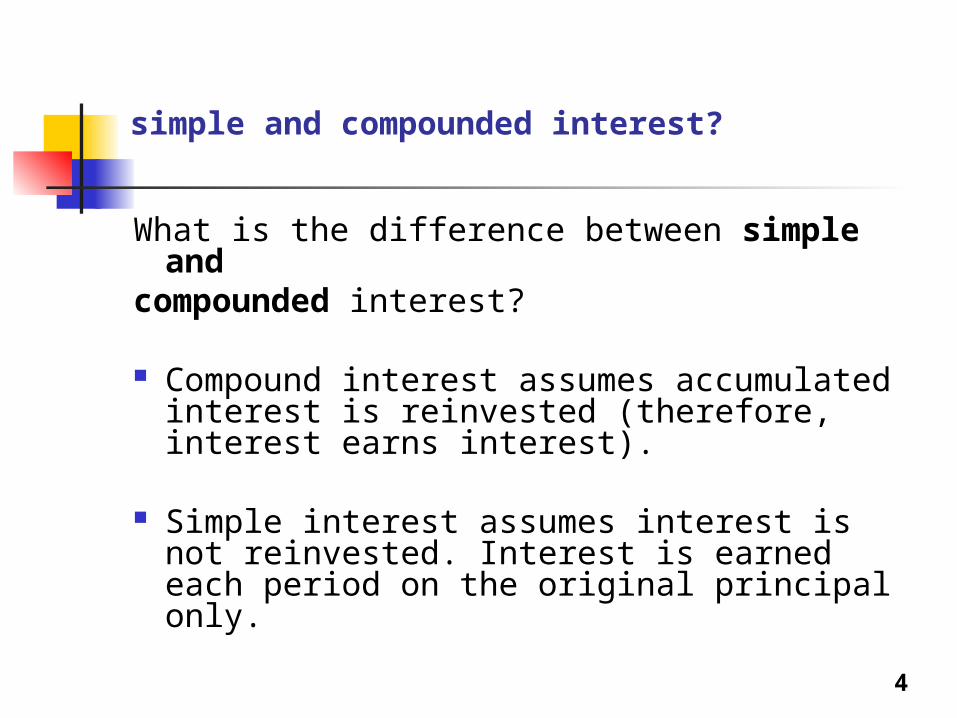

simple and compounded interest?

What is the difference between simple and

compounded interest?

Compound interest assumes accumulated interest is reinvested (therefore, interest earns interest).

Simple interest assumes interest is not reinvested. Interest is earned each period on the original principal only.

5

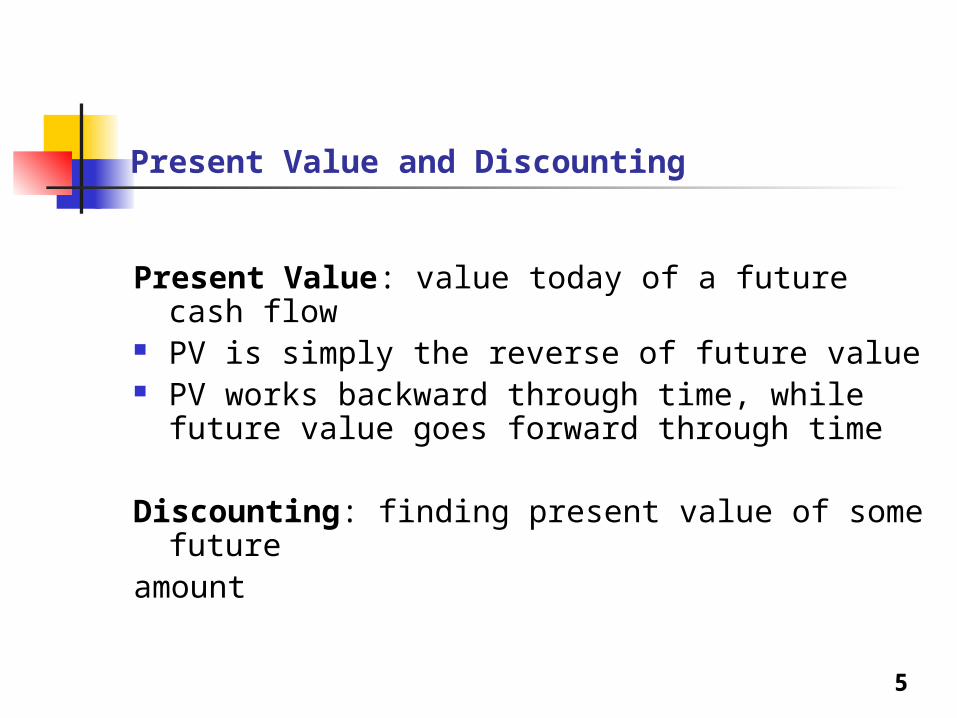

Present Value and Discounting

Present Value: value today of a future cash flow

PV is simply the reverse of future value PV works backward through time, while future

value goes forward through time

Discounting: finding present value of some future

amount

6

Example

3 different ways to find future value of a single cash flow

Find FV of $100 in 2 years @ 10%

FV2= 100*(1+10%)2 formula = 100 FVIF2,10% table100 PV 10 i 2 n FV financial calculator

in general FVn= PV (1+i)n

PV, FV formulas are based on this equation

4 variables given any 3, you can calculate the 4th

7

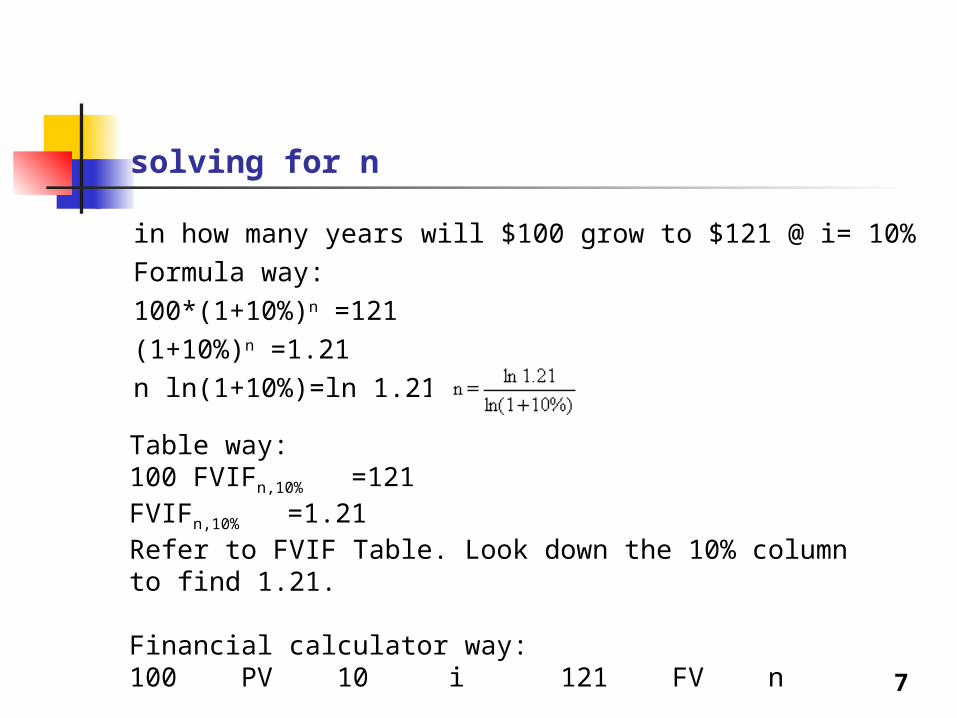

solving for n

in how many years will $100 grow to $121 @ i= 10%Formula way:100*(1+10%)n =121 (1+10%)n =1.21 n ln(1+10%)=ln 1.21

Table way:100 FVIFn,10% =121FVIFn,10% =1.21Refer to FVIF Table. Look down the 10% column to find 1.21.

Financial calculator way:100 PV 10 i 121 FV n

8

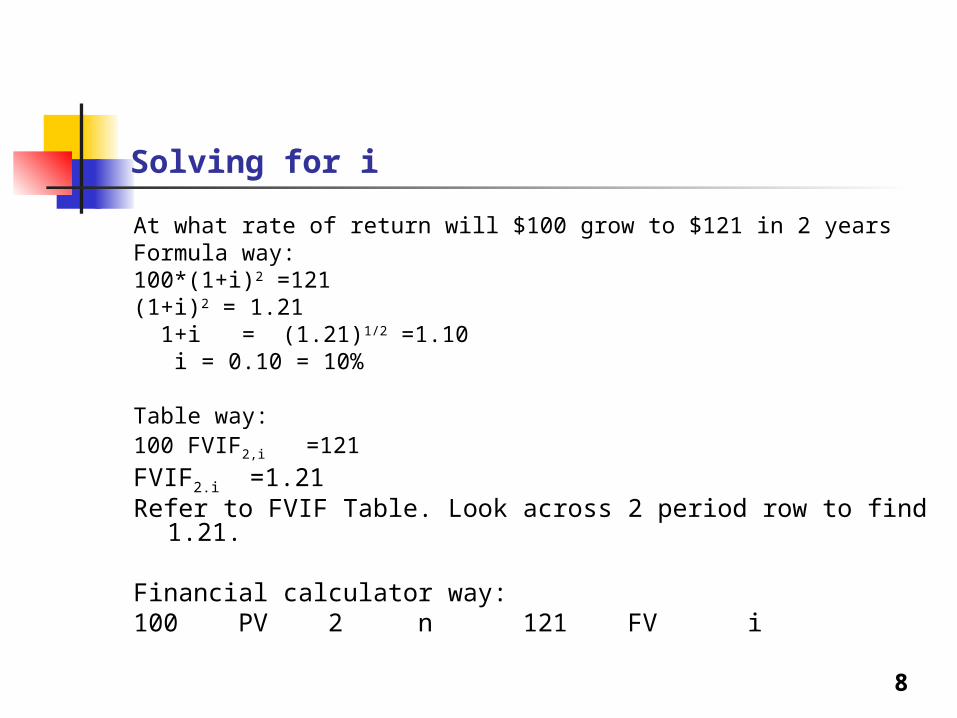

Solving for i

At what rate of return will $100 grow to $121 in 2 yearsFormula way:100*(1+i)2 =121 (1+i)2 = 1.21 1+i = (1.21)1/2 =1.10 i = 0.10 = 10%

Table way:100 FVIF2,i =121

FVIF2.i =1.21Refer to FVIF Table. Look across 2 period row to find 1.21.

Financial calculator way:100 PV 2 n 121 FV i

9

Present and future value of multiple cash flows

Calculate PV(FV) of each cash flow and add them up: e.g. i=10%

PV = 100/(1+10%)+ 300/(1+10%)2 + 400/(1+10%)3 formula way

PV = 100 PVIF1,10% + 300 PVIF2,10% + 400 PVIF3,10% table way

10 i 0 CFi 100 CFi 300 CFi 400 CFi NPV financial calculator

10

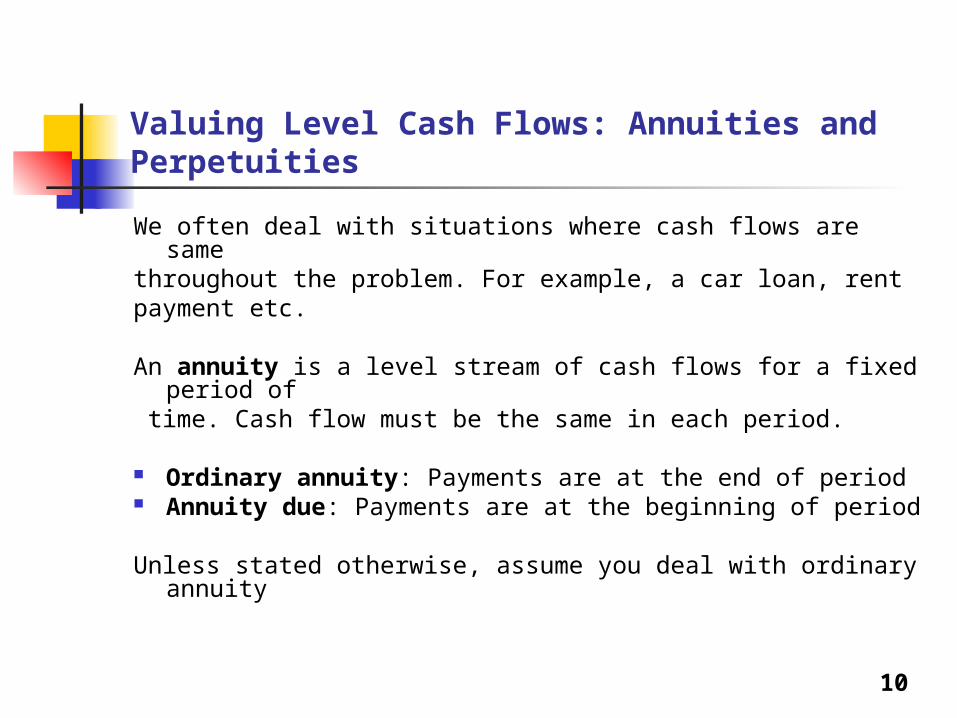

Valuing Level Cash Flows: Annuities and Perpetuities

We often deal with situations where cash flows are same throughout the problem. For example, a car loan, rent payment etc.

An annuity is a level stream of cash flows for a fixed period of

time. Cash flow must be the same in each period.

Ordinary annuity: Payments are at the end of period Annuity due: Payments are at the beginning of period

Unless stated otherwise, assume you deal with ordinary annuity

11

Future value of an annuity

FVA3 = A (1+i)2 + A (1+i) + A formula way = A {(1+i)2 + (1+i) + 1} = A FVIFA3,i% table way

A PMT r i 3 n FV financial calculator way

again given any 3, we can solve for the 4th

12

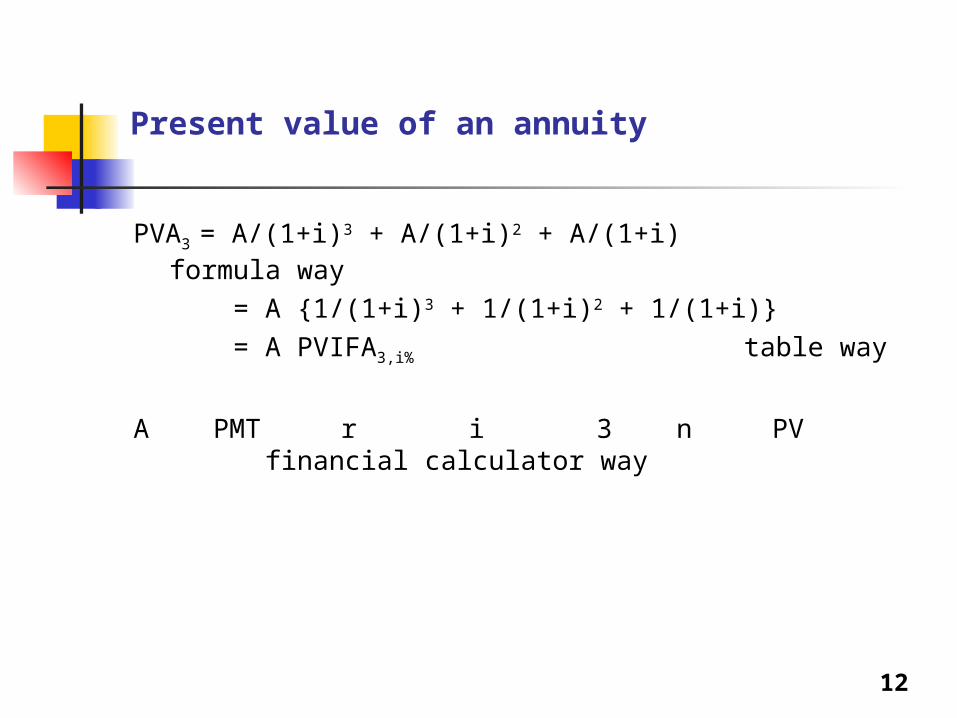

Present value of an annuity

PVA3 = A/(1+i)3 + A/(1+i)2 + A/(1+i) formula way

= A {1/(1+i)3 + 1/(1+i)2 + 1/(1+i)} = A PVIFA3,i% table way

A PMT r i 3 n PV financial calculator way

13

deriving the PVIFA3,i% formula

use sum of infinite geometric series formula: asa one can show that

14

deriving the PVIFA3,i% formula

15

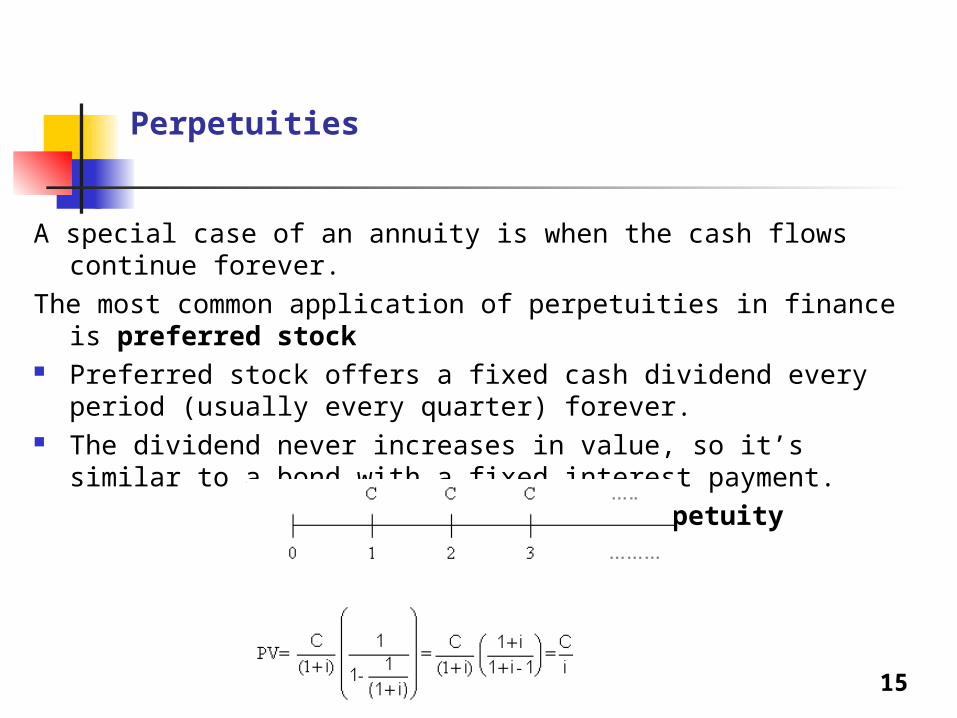

Perpetuities

A special case of an annuity is when the cash flows continue forever.

The most common application of perpetuities in finance is preferred stock

Preferred stock offers a fixed cash dividend every period (usually every quarter) forever.

The dividend never increases in value, so it’s similar to a bond with a fixed interest payment.

Present value of a perpetuity

16

Comparing Interest Rates

How do you compare interest rates?Rates can be quoted monthly, annually or something in

between, and it quickly becomes confusing to try and determine the “real” interest rate.

Stated Rate ( also called APR, Quoted Rate, Nominal Rate): rate before considering any compounding effectse.g. 10% APR quarterly compounding

Periodic Rate: APR/(# of times compounding occurs in a year)It is the effective or “real” rate. It considers the compounding effects.

17

Effective Annual Rate

Effective Annual Rate (EAR)Rate on an annual basis that reflects all

compounding effects

EAR= (1+APR/n)n – 1

You can compare different interest rate quotations

by using EAR

18

Note: in TVM problems

Timing of cash flows tells you what the period is

Find and use the periodic rate that is consistent with the period definition

19

Loan Amortization: There are many different kinds of loans available

Pure discount loan With such a loan, the borrower receives

money today and repays a single lump sum at some time in the future.

Interest-only loans This kind of loan repayment plan calls for the

borrower to pay interest each period and repay

the entire principal at some point in the future.

20

different types of loans

Amortized loans With a pure discount or interest-only loan, the

principal is paid all in once. An alternative is an amortized loan where the lender may require the borrower to repay parts of the loan amount over time. The process of paying off a loan by making

regular principal reductions is called amortizing the loan.

Partially amortizing loan Similar to amortized loan except the borrower

makes a single, much larger final payment called a “balloon” to pay off the loan.

21

Example

You get a $10,000 car loan. It is a five year amortized loan with

annual installments. 12% is the interest rate charged by the bank.

Develop the amortization schedule.