1 tricorn group plc final results for year ended 31st march 2013 june 2013

TRANSCRIPT

1

Tricorn Group plc Final Results

For year ended 31st March 2013

June 2013

Highlights

• Significant progress in developing global capability

• First shipments made from China facility

• US acquisition provides strong platform for growth

• Progressive dividend policy maintained

2

3

Financial review – facilitating growth

Previous strengthening of our financial position• Improved operating margins

• Managed working capital and reduced inventories

• March 2012 net funds position-£586k

…. has allowed significant investment in global operations• US acquisition made for £1.98m (net book value of assets - £2.8m)

• Invested £0.69m in China facility

• Continued investment in ongoing capital programme

.....and positioned the Group for further growth• Secured invoice discounting and working capital facilities in

January 2013 with HSBC

• Balance sheet still free of term debt

….whilst delivering on our progressive dividend policy• Full year dividend increased 50% to 0.3p (2012: 0.2p)

4

Financial review-overview

* - Before acquisition related costs, China start up costs, restructuring costs, intangible asset amortisation, share based payment charges, foreign exchange derivative valuation and interest collar gain.

FY 2012/13

£’000

FY 2011/12

£’000

Change

Revenue 21,850 24,706 (12)%

Operating profit* 1,668 1,771 (6)%

Operating profit margin %*

7.6% 7.2% 6%

Profit before tax* 1,614 1,622 -

Earnings Per Share* 4.02p 3.78p 8%

Dividend 0.3p 0.2p 50%

Cash and equiv 697 2,468 (72)%

Net (Debt)/Funds (1,908) 586 (425)%

5

£’000 2013 Total Group

2013 US Acquisition

2013 Excl

Acquisitions

2012 Change %

Total Fixed Assets 4,785 1,525 3,260 2,777 72

Inventory 3,863 1,266 2,597 2,929 (11)

Trade & other receivables 5,590 947 4,643 5,823

Trade & other payables (4,143) (1,095) (3,048) (4,580)

Net working capital 5,310 1,118 4,192 4,172 -

Taxation & other creditors (459) (542)

Net (Debt)/Funds (1,908) 586

Net Assets 7,728 6,993

Gearing (total debt/equity) 24.7% -

Financial review-net assets

• Increase in fixed assets driven by US and China investments• Inventories reduced, down 11% year on year before acquisitions• No term debt• Gearing based on short term borrowing at 24.7%

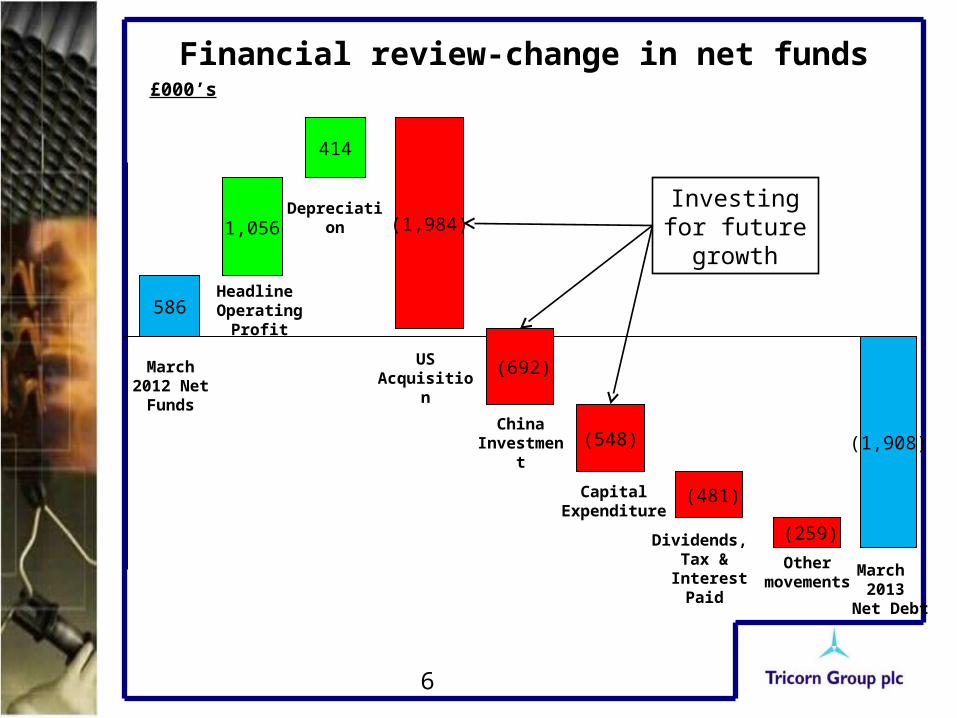

6

414

(1,908)(548)

March 2012 Net Funds

Headline Operating

Profit

Financial review-change in net funds

586

March 2013

Net Debt

(1,984)Depreciation

China Investment

Capital Expenditure

(481)

Dividends, Tax &

Interest Paid

(259)

Other movements

£000’s

(692)US Acquisition

1,056

Investing for future growth

Energy & Utilities Division

• Sales up on previous year• Operating margin significantly

improved• New business secured• Some restructuring underway

£’000 2013 2012

Sales 9,071 10,691

Operating margin %

8.9 9.2

PBT 782 923

7

• New business secured on large diameter fabrications

• Investment in semi-automated paint plant generating efficiency gains

• Softening in some end markets in H2 2013

£’000 2013 2012

Sales 5,768 5,334

Operating margin % 5.3 1.0

PBT 280 25

• 2012 demand particularly high due to impending emissions legislation

• Some improvement in demand through final quarter

• SQEP certication award by major customer

Transportation Division

£’000 2013 2012

Sales 7,011 8,681

Operating margin* % 8.2 8.8

PBT* 572 763

Aerospace Division

Business Review

*excluding China start up costs

US Acquisition

• Whitley had been producing specialist pipe systems since 1965

– Predominantly diesel engine tube systems– Blue chip OEM customer base

• Manufacturing facilities in Franklin NC and Plymouth IN

• Highly capable management team and engaged workforce in place at Franklin

• Key customers prepared to consider business transfer from Plymouth to Franklin

• Tricorn acquired the Franklin facility (60,000 sq ft), together with plant and equipment from the Plymouth facility

• Consideration paid of £1.98m. Net book value of £2.8m

8

US Acquisition Update

• Formed Franklin Tubular Products Inc.• Successful completion of business and

equipment transfer from Plymouth• Supply chain re-established• No customer disruption through the process

from Franklin site• Supporting infrastructure in place including IT

transfer• Opportunities for low cost country sourcing• First new business nominations have now

been awarded• Strong platform for US growth

9

China Manufacturing Facility

4,500 sq m of manufacturing spaceAnother 2,000 sq m under constructionExternal Area fully refurbishedEstablishing a world class facility

China Manufacturing Update

• Utilises our well established supply base and resources in China

• Customer led: supports our customers in their localisation of supply

• First shipments made• Nominations for supply from a wider customer base• Production lines being developed• Advanced stages of establishing China JV enhancing

capabilities further

11

Outlook

MTC LTD MAXPOWER WUXIRMDG LTDMAXPOWER LTD

FTP Inc.

• Developing a global platform in tube solutions capability– 5 manufacturing facilities on 3 continents

– Around 90% of product destined for markets outside the UK

• Well positioned for substantial growth– Providing high quality services and products to customers

through design, innovation and integrated supply

• Confident about future prospects