1 use these materials in conjunction with the fi program guide and the fi instructor guide. use the...

TRANSCRIPT

1

Use these materials in conjunction with the FI Program Guide and the FI Instructor Guide. Use the slides to prepare visuals (flipcharts, overheads, slides) and use the notes as your guide in leading the seminar.

This work is published under Creative Commons Attribution 3.0 License. Please see www.financialintegrity.org for rights

restrictions.

Financial Integrity Seminar

2

Financial Integrity

Transforming Your Relationship with Money

3

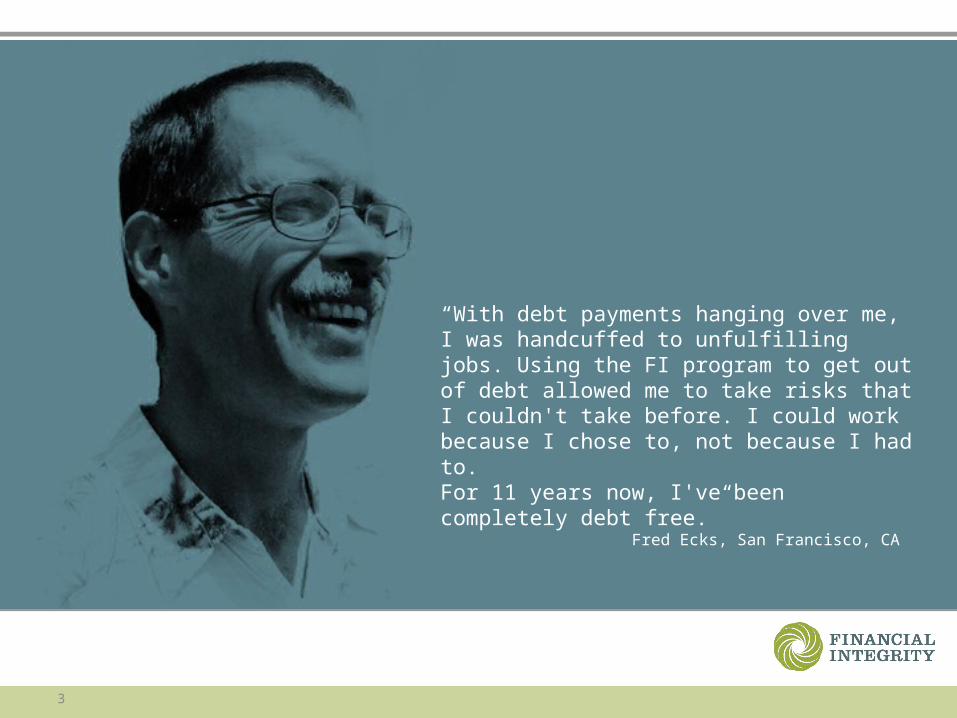

“With debt payments hanging over me, I was handcuffed to unfulfilling jobs. Using the FI program to get out of debt allowed me to take risks that I couldn't take before. I could work because I chose to, not because I had to. For 11 years now, I've been completely debt free.”

Fred Ecks, San Francisco, CA

4

"The FI Program has been one of the most empowering experiences of my life. I started in college, and it helped me craft a life based on my values rather than financial anxiety.”

Alan Seid, Maple Falls, WA

5

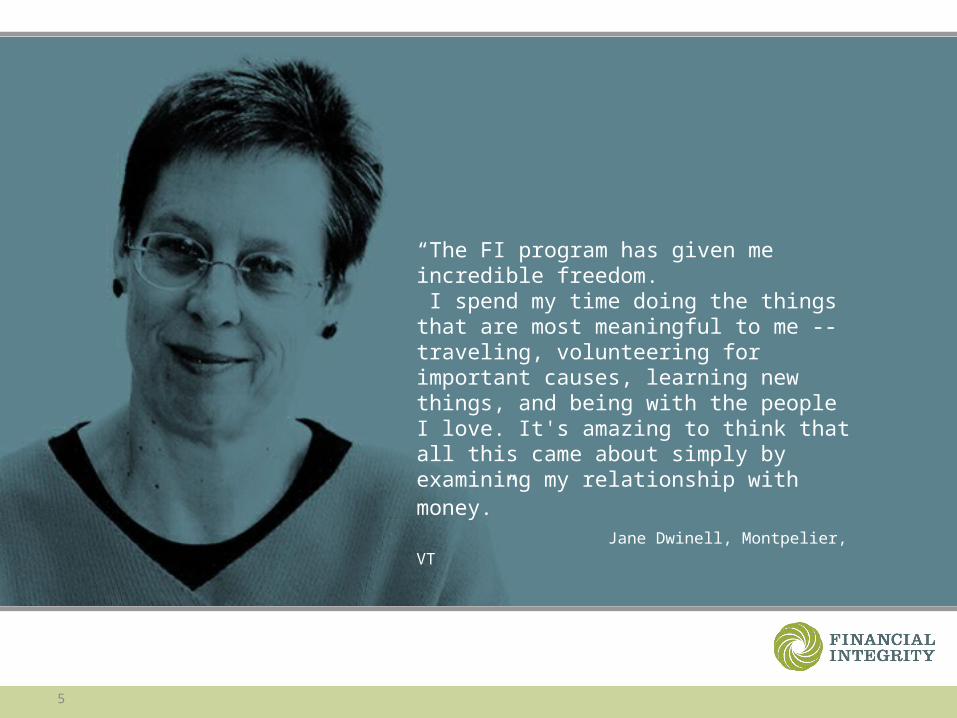

“The FI program has given me incredible freedom. I spend my time doing the things that are most meaningful to me -- traveling, volunteering for important causes, learning new things, and being with the people I love. It's amazing to think thatall this came about simply by examining my relationship with money.”

Jane Dwinell, Montpelier, VT

6

Parking Lot

7

“Ground Rules”

• Treat all personal information confidentially

• No shame, no blame

• Pay attention when you feel resistance. Take some time to ask yourself WHY you are reacting or rejecting

• Take care of your own physical comfort needs

8

Introduce Yourself

• Your name

• Your location (city, town, neighborhood)

• The main reason you are here

9

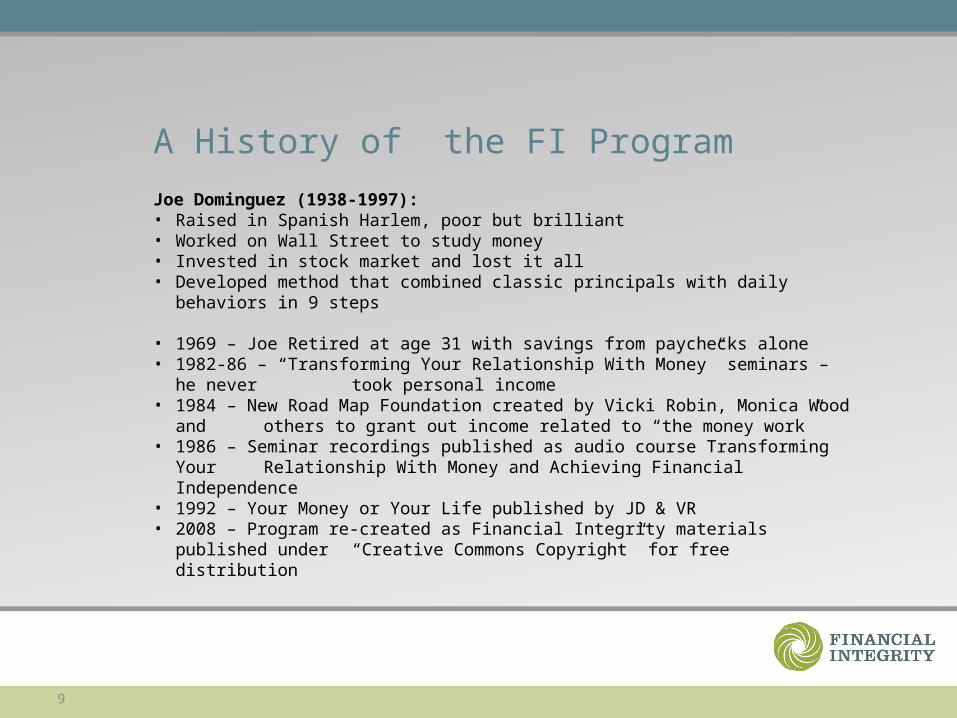

A History of the FI Program

Joe Dominguez (1938-1997):• Raised in Spanish Harlem, poor but brilliant• Worked on Wall Street to study money• Invested in stock market and lost it all• Developed method that combined classic principals with daily behaviors in 9

steps

• 1969 – Joe Retired at age 31 with savings from paychecks alone• 1982-86 – “Transforming Your Relationship With Money” seminars – he never

took personal income• 1984 – New Road Map Foundation created by Vicki Robin, Monica Wood and

others to grant out income related to “the money work” • 1986 – Seminar recordings published as audio course Transforming Your

Relationship With Money and Achieving Financial Independence• 1992 – Your Money or Your Life published by JD & VR• 2008 – Program re-created as Financial Integrity materials published under

“Creative Commons Copyright” for free distribution

10

Joe’s Framework

Financial Intelligence

rational and responsible

Financial Independence

meet your basic needs without paid employment

Financial Integrity

???

11

What is integrity?

12

What is integrity?

• Soundness

• Sturdy, sure, security

• Ethical

• Appropriateness

• Truthful

• Stability

• With an incorruptible foundation

13

Joe’s Framework

Financial Intelligence

rational and responsible

Financial Independence

meet your basic needs without paid employment

Financial Integrity

awareness, wise decisions, alignment

14

Why the Financial Integrity program?• Reduce stress about money

• Have more clarity about money

• Feel more in control

• Get out of debt

• Live within my means and save

• Be able to do the work I want to do

• Reconnect with my purpose in life

15

(transition to 9 circles exercise)

16

The 9 Circles Exercise

17

The 9 Circles Exercise - Solution

18

(transition to Money is …)

19

Money is …

20

Money is …

• Security

• Scarce, hard to get, don’t have enough

• Burden, responsibility, stress

• Don’t deserve it

• Makes me happy

• Can get great things with it

• Freedom, joy

• A necessary evil

21

(transition to Fulfillment Curve …)

22

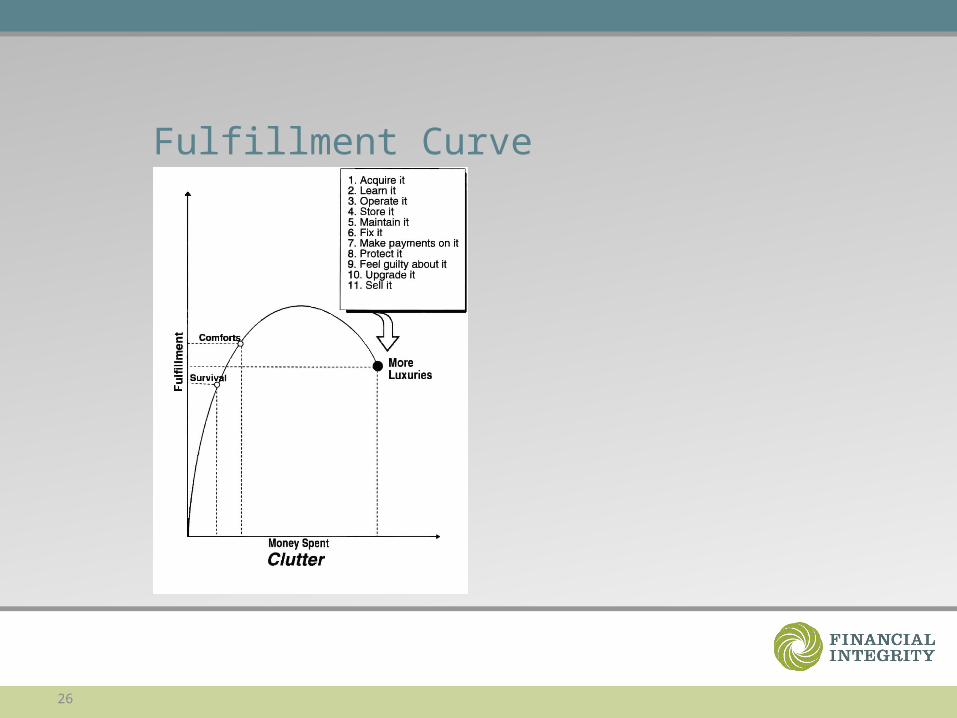

Fulfillment Curve

23

Fulfillment Curve

24

Fulfillment Curve

25

Fulfillment Curve

26

Fulfillment Curve

27

Fulfillment Curve

28

Inventory Exercise

Visualize a “public” room.

List 9 objects and categorize them as:

Needs, Comforts, Luxuries, Clutter

Report out to the group.

29

Inventory Exercise – Report Out

Needs

Comforts

Luxuries

Clutter

“Enough”

30

Inventory Exercise – Sample

Needs - table, chairs

Comforts – upholstered chairs, leather couch, photos,

Luxuries – big screen TV, art work

Clutter – (depends on audience!)

**Some people will categorize similar items in different categories!

31

Enough

It takes certain skills and qualities

• to reach enough,

• to recognize when you’ve reached enough,

• and to stay near that peak of the Fulfillment Curve, without falling back into deprivation or down into gluttony

32

Real Hourly Wage & Tracking

Monthly Tabulation

Three Questions

Wall ChartMinimizing Spending

Maximizing Income

Capital & Crossover

Managing Investments

Lifetime Income & Personal Balance Sheet

The Nine Step Process

33

Break

34

(transition to Step 1 …)

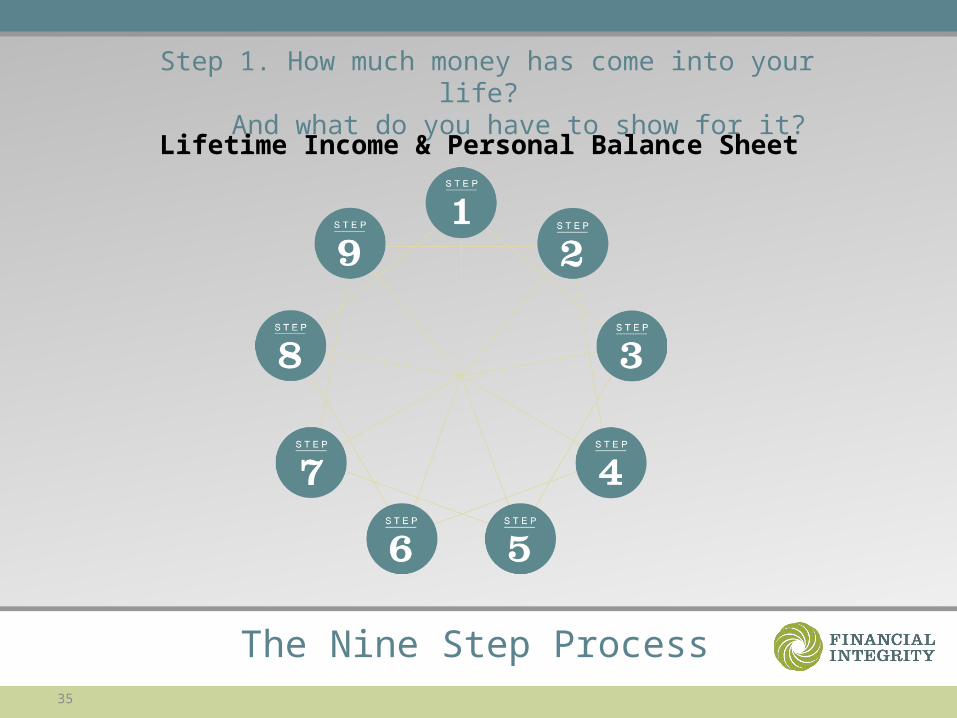

35

Step 1. How much money has come into your life?

And what do you have to show for it?Lifetime Income & Personal Balance Sheet

The Nine Step Process

36

Step 1. Lifetime Income

Financial Sources: Amount

Total Lifetime Earnings $

Lifetime Income Worksheet

37

Step 1. Lifetime Income - sample

Financial Sources: Amount

Taxed income (SSA report)

Untaxed jobs

Selling stuff (cars, CDs)

Allowance/"spending money"

Gifts

Interest on savings

…

Total Lifetime Earnings $

Lifetime Income Worksheet

38

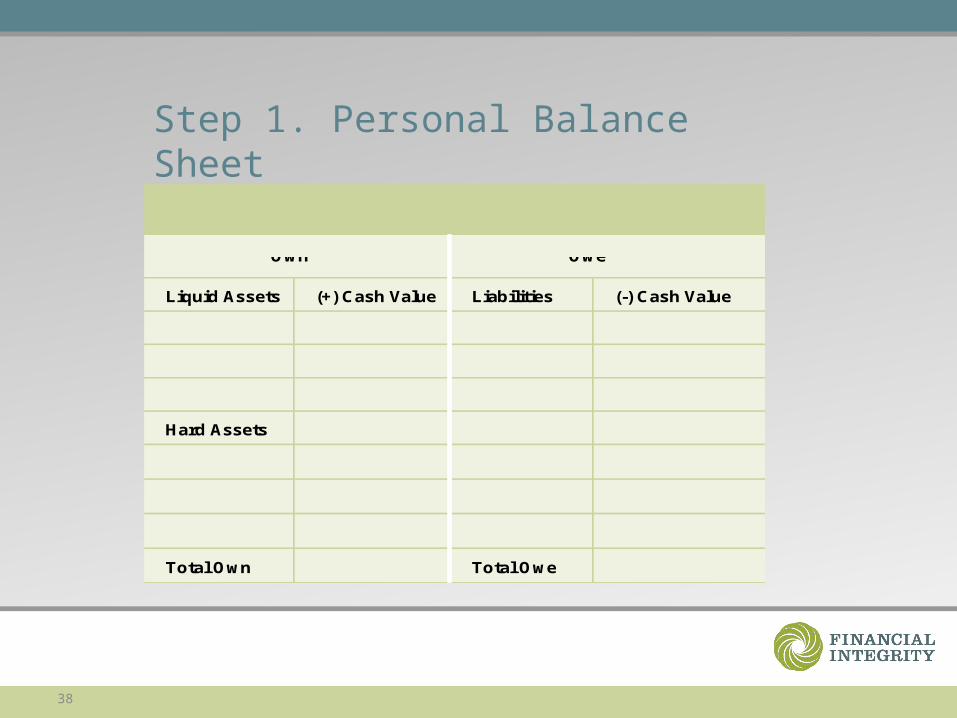

Step 1. Personal Balance Sheet

Liquid Assets (+) Cash Value Liabilities (-) Cash Value

Hard Assets

Total Own Total Owe

Personal Balance Sheet

Own Owe

Personal Balance Sheet

Own Owe

Personal Balance Sheet

Own Owe

39

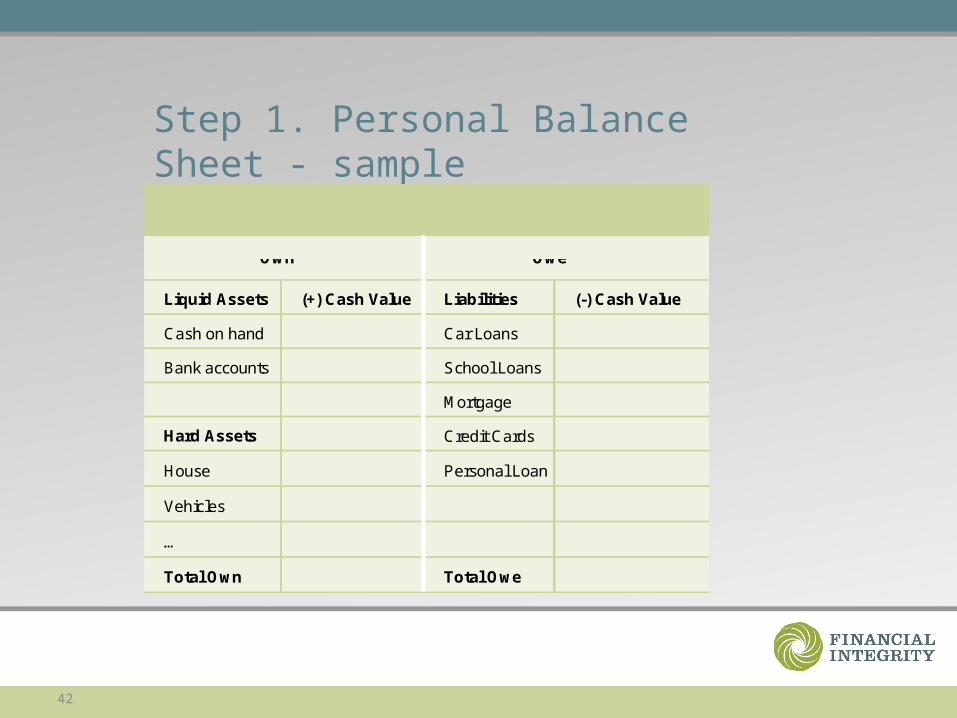

Step 1. Personal Balance Sheet - sample

Liquid Assets (+) Cash Value Liabilities (-) Cash Value

Cash on hand Car Loans

Bank accounts School Loans

Mortgage

Hard Assets Credit Cards

House Personal Loan

Vehicles

…

Total Own Total Owe

Personal Balance Sheet

Own Owe

Personal Balance Sheet

Own Owe

40

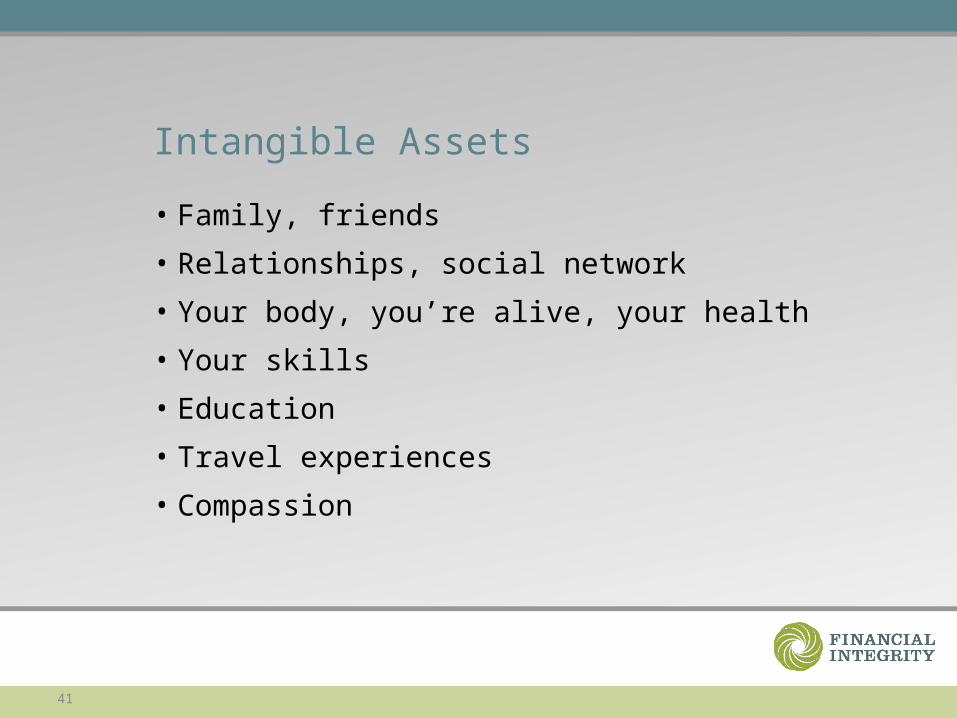

Intangible Assets

41

Intangible Assets

• Family, friends

• Relationships, social network

• Your body, you’re alive, your health

• Your skills

• Education

• Travel experiences

• Compassion

42

Step 1. Personal Balance Sheet - sample

Liquid Assets (+) Cash Value Liabilities (-) Cash Value

Cash on hand Car Loans

Bank accounts School Loans

Mortgage

Hard Assets Credit Cards

House Personal Loan

Vehicles

…

Total Own Total Owe

Personal Balance Sheet

Own Owe

Personal Balance Sheet

Own Owe

43

(Step 1 Reflection …)

44

(transition to Step 2 …)

45

Money is …

• Security

• Scarce, hard to get, don’t have enough

• Burden, responsibility, stress

• Don’t deserve it

• Makes me happy

• Can get great things with it

• Freedom, joy

• A necessary evil

46

Money is … a means of exchange

47

Money is … a means of exchange

What are you trading?

You trade your precious time for money!

Money = Life Energy

48

Money = Life Energy

Just how much of your life energy

are you trading for money?

49

Real Hourly Wage & Tracking

Step 2. Being in the Present:Tracking Your Life Energy

The Nine Step Process

50

Step 2. Real Hourly Wage

Dollars ÷ Hours = $ per hour

Base Annual Wage/Salary $ ÷ 2080 hours =

+ Adjustments + Adjustments

- Adjustments - Adjustments

Real Hourly Wage $ ÷ ____ hours =

Real Hourly Wage

51

Step 2. Real Hourly Wage - sample

Dollars ÷ Hours = $ per hour

Base Annual Wage/Salary $ ÷ 2080 hours =

+ Adjustments + Adjustments

insurance(s) benefits $$$$

transit pass $$$

free meals $$$

- Adjustments - Adjustments

clothing, uniforms $$$$ commuting time xxx hours

tools, computers $$$ work lunches xxx hours

office niceties $$$ shopping time xxx hours

insurance premiums $$$$

Real Hourly Wage $ ÷ ____ hours =

Real Hourly Wage

52

Step 2. Is it worth it?

Every dollar you spend = the amount of your life energy it took to get it.

Every time I spend about $_______ I am trading about an hour of my life energy.

When I buy ______ , I am trading _____ hours of my life.

The key question: Is it worth it?

53

Step 2 – Tracking

• Tracking the flow of money into and out of your life• Where does it come from?• Where is it all going?

54

Step 2 – Tracking Methods

55

Step 2 – Tracking Methods

• Keep a small notebook – jot down everything• Download transactions from online banking• Quicken or other money manager software• Check book• Use debit card, and track cash on notebook.

56

Step 2 – Sample Tracking12/10/07 ALBERTSONS -$88.4012/10/07 TRADER JOE'S -$42.2912/11/07 THE HOME DEPOT -$57.1612/12/07 AMC Movies -$31.9512/12/07 GUITAR CENTER -$19.5812/12/07 ALBERTSONS -$11.0012/12/07 QFC -$21.4612/12/07 USPS -$6.5512/14/07 COMCAST CABLE -$47.4412/14/07 SHELL OIL -$44.0212/14/07 ALBERTSONS -$48.3512/16/07 RITE AID STORE -$66.9012/16/07 CHEVRON -$63.0612/17/07 ALBERTSONS -$60.6612/18/07 BEST BUY -$49.0512/18/07 ALBERTSONS -$47.5412/18/07 QFC -$28.9512/18/07 USA WATER POLO -$65.0012/19/07 SHELL OIL -$31.1712/19/07 ALBERTSONS -$34.6312/19/07 THE UPS -$21.0912/20/07 AMAZON -$18.9712/20/07 BERT'S RED APPLE -$14.5112/20/07 QFC -$22.1712/24/07 OLD NAVY -$7.5012/24/07 BEST BUY -$105.7112/24/07 TARGET -$31.5612/24/07 TERIYAKI KITCHEN -$30.0012/26/07 ALBERTSONS -$55.8012/26/07 RUBBER STAMP & BUTTON -$11.2012/27/07 ALBERTSONS -$15.7312/30/07 BEST BUY $10.8812/30/07 TARGET -$40.9012/31/07 ALBERTSONS -$30.9812/31/07 QFC -$31.67

57

Step 2 - Tracking vs. Budgeting

• What practices (budgets, envelopes, spending restrictions) have you tried in the past to help manage your finances? What were your experiences and feelings with those?

• How is tracking different from budgeting?

58

(Step 2 Reflection …)

59

End of Session 1

60

Welcome Back!

Financial IntegrityTransforming Your Relationship with Money

Session 2

61

Monthly Tabulation

Step 3. Where is it all going?

The Nine Step Process

62

Step 3 –Add Your Categoriescategory description amountcable COMCAST CABLE -$47.44cellphone T-MOBILE -$136.79drugstore RITE AID STORE -$66.90entertainment HOLLYWOOD VIDEO -$17.31gas SHELL OIL -$44.02gas CHEVRON -$63.06gas SHELL OIL -$31.17gifts NETWORK FOR GOOD -$31.42gifts AMC Movies -$31.95gifts GUITAR CENTER -$19.58gifts BEST BUY -$49.05gifts AMAZON -$18.97gifts OLD NAVY -$7.50gifts BEST BUY -$105.71gifts TARGET -$31.56gifts BEST BUY $10.88groceries ALBERTSONS -$32.33groceries SAFEWAY -$39.81groceries ALBERTSONS -$88.40groceries TRADER JOE'S -$42.29groceries ALBERTSONS -$11.00groceries QFC -$21.46groceries ALBERTSONS -$48.35groceries ALBERTSONS -$60.66groceries ALBERTSONS -$47.54groceries QFC -$28.95groceries ALBERTSONS -$34.63groceries BERT'S RED APPLE -$14.51groceries QFC -$22.17groceries ALBERTSONS -$55.80groceries ALBERTSONS -$15.73groceries ALBERTSONS -$30.98groceries QFC -$31.67office THE HOME DEPOT -$57.16office RUBBER STAMP & BUTTON -$11.20office TARGET -$40.90postal USPS -$6.55postal THE UPS -$21.09restaurant TERIYAKI KITCHEN -$30.00sports USA WATER POLO -$65.00

63

Step 3 – Sum by Categoriescategory description amountcable COMCAST CABLE -$47.44cellphone T-MOBILE -$136.79drugstore RITE AID STORE -$66.90entertainment HOLLYWOOD VIDEO -$17.31gas SHELL OIL -$44.02gas CHEVRON -$63.06gas SHELL OIL -$31.17gifts NETWORK FOR GOOD -$31.42gifts AMC Movies -$31.95gifts GUITAR CENTER -$19.58gifts BEST BUY -$49.05gifts AMAZON -$18.97gifts OLD NAVY -$7.50gifts BEST BUY -$105.71gifts TARGET -$31.56gifts BEST BUY $10.88groceries ALBERTSONS -$32.33groceries SAFEWAY -$39.81groceries ALBERTSONS -$88.40groceries TRADER JOE'S -$42.29groceries ALBERTSONS -$11.00groceries QFC -$21.46groceries ALBERTSONS -$48.35groceries ALBERTSONS -$60.66groceries ALBERTSONS -$47.54groceries QFC -$28.95groceries ALBERTSONS -$34.63groceries BERT'S RED APPLE -$14.51groceries QFC -$22.17groceries ALBERTSONS -$55.80groceries ALBERTSONS -$15.73groceries ALBERTSONS -$30.98groceries QFC -$31.67office THE HOME DEPOT -$57.16office RUBBER STAMP & BUTTON -$11.20office TARGET -$40.90postal USPS -$6.55postal THE UPS -$21.09restaurant TERIYAKI KITCHEN -$30.00sports USA WATER POLO -$65.00

category amountcable -$47.44cellphone -$136.79drugstore -$66.90entertainment -$17.31gas -$138.25gifts -$284.86groceries -$626.28office -$109.26postal -$48.73restaurant -$30.00sports -$65.00

64

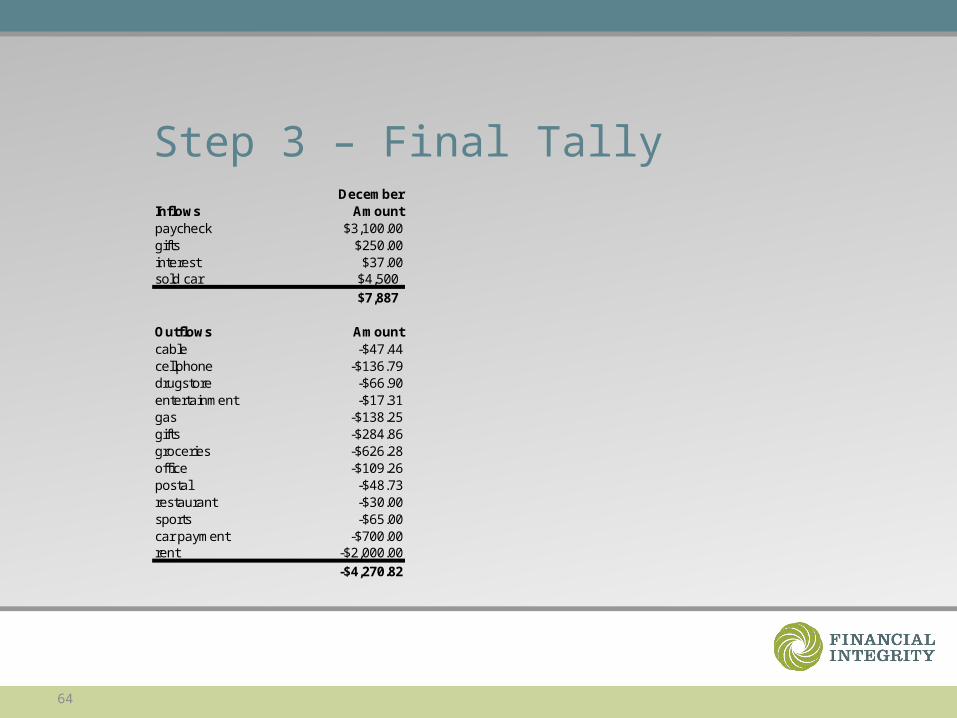

Step 3 – Final TallyDecember

Inflows Amountpaycheck $3,100.00gifts $250.00interest $37.00sold car $4,500

$7,887

Outflows Amountcable -$47.44cellphone -$136.79drugstore -$66.90entertainment -$17.31gas -$138.25gifts -$284.86groceries -$626.28office -$109.26postal -$48.73restaurant -$30.00sports -$65.00car payment -$700.00rent -$2,000.00

-$4,270.82

65

Step 3 – Check TotalsActualBeginning of Month DecemberChecking $2,000.00Saving $5,000.00Cash on hand $100.00

$7,100.00

DecemberInflows Amountpaycheck $3,100.00gifts $250.00interest $37.00sold car $4,500

$7,887

Outflows Amountcable -$47.44cellphone -$136.79drugstore -$66.90entertainment -$17.31gas -$138.25gifts -$284.86groceries -$626.28office -$109.26postal -$48.73restaurant -$30.00sports -$65.00car payment -$700.00rent -$2,000.00

-$4,270.82

End of Month should be: $10,716.18

Actual End of Month Checking $3,000.00Saving $7,435.00Cash on hand $157.00

$10,592.00

Unaccounted for: $124.18

66

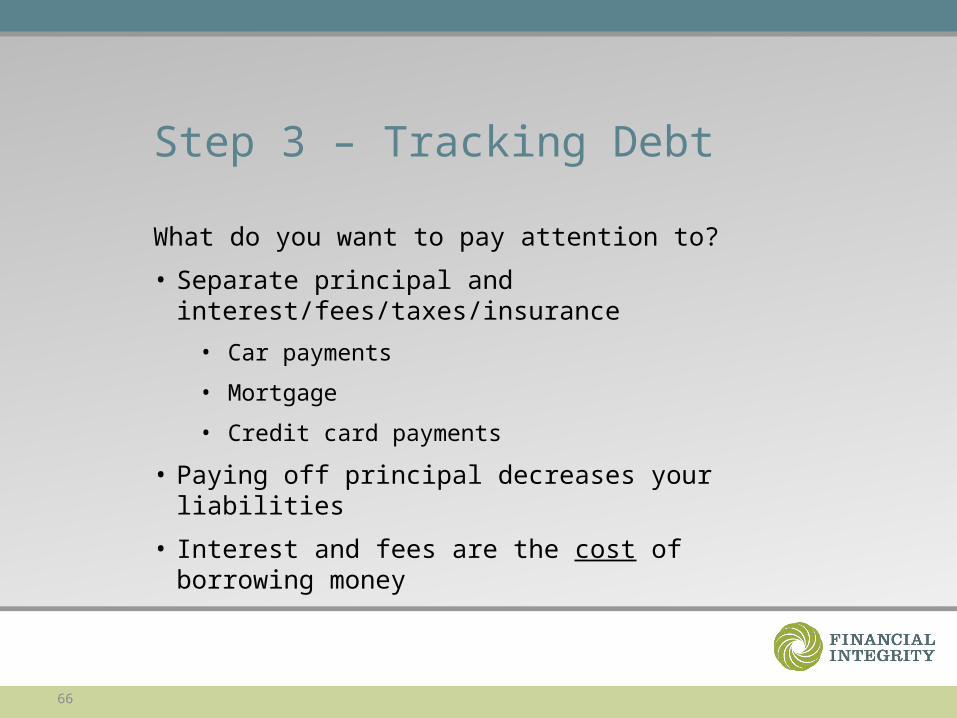

Step 3 – Tracking Debt

What do you want to pay attention to?

• Separate principal and interest/fees/taxes/insurance

• Car payments

• Mortgage

• Credit card payments

• Paying off principal decreases your liabilities

• Interest and fees are the cost of borrowing money

67

Step 3 – Categories Patterns

• Why keep track of your totals each month?

• Discover behaviors and patterns to gain awareness.

68

Step 3 – Gazingus Pins

• Those unnecessary things you buy automatically, because it’s a habit, or because they make you feel a certain way.

• You can create categories to track gazingus pins and to monitor when you make unconscious choices out of emotion or habit, and start building awareness for making conscious choices. .

• What do gazingus pins provide that you can get in other ways in your life? Comfort, connection, security, fun.

69

Step 3 – Gazingus Pins Exercise

• How do you decide something is a gazingus pin?

• Where would this item be on the fulfillment curve when I first buy it?

• Where would this item be in another month? Two months? A year?

• What are your gazingus pins?

70

Step 3 – Add Life EnergyDecember RHW = $10

Inflows Amount Life Energypaycheck $3,100.00gifts $250.00interest $37.00sold car $4,500

$7,887

Outflows Amountcable -$47.44cellphone -$136.79drugstore -$66.90entertainment -$17.31gas -$138.25gifts -$284.86groceries -$626.28office -$109.26postal -$48.73restaurant -$30.00sports -$65.00car payment -$700.00rent -$2,000.00

-$4,270.82

71

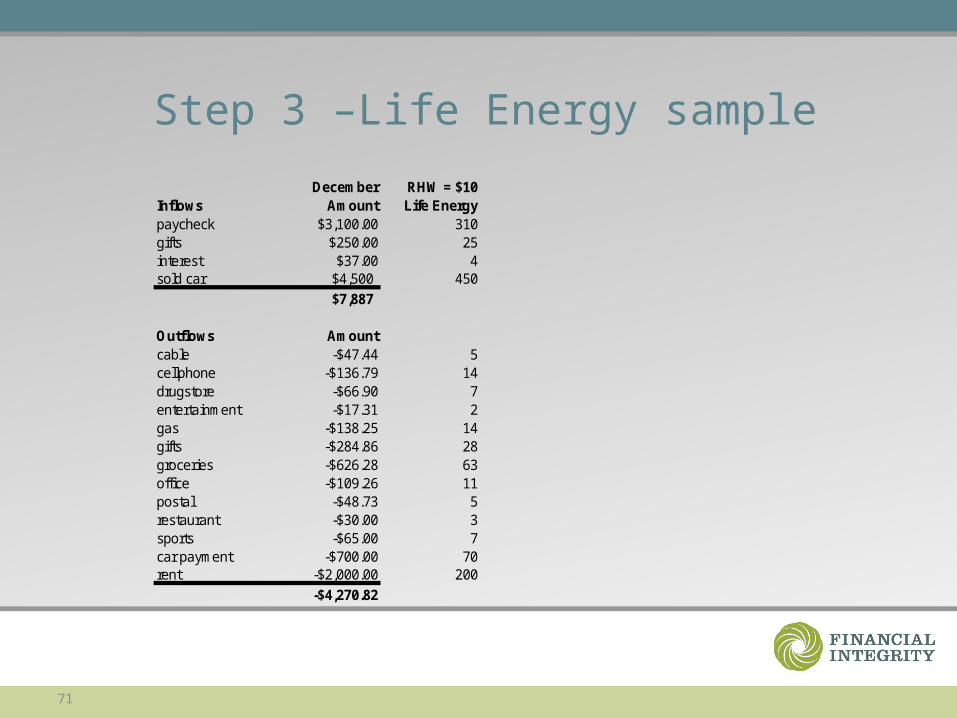

Step 3 –Life Energy sample

December RHW = $10Inflows Amount Life Energypaycheck $3,100.00 310gifts $250.00 25interest $37.00 4sold car $4,500 450

$7,887

Outflows Amountcable -$47.44 5cellphone -$136.79 14drugstore -$66.90 7entertainment -$17.31 2gas -$138.25 14gifts -$284.86 28groceries -$626.28 63office -$109.26 11postal -$48.73 5restaurant -$30.00 3sports -$65.00 7car payment -$700.00 70rent -$2,000.00 200

-$4,270.82

72

(Step 3 Reflection …)

73

Break

74

Three Questions

Step 4. Three Questions That Will Transform Your Life

The Nine Step Process

75

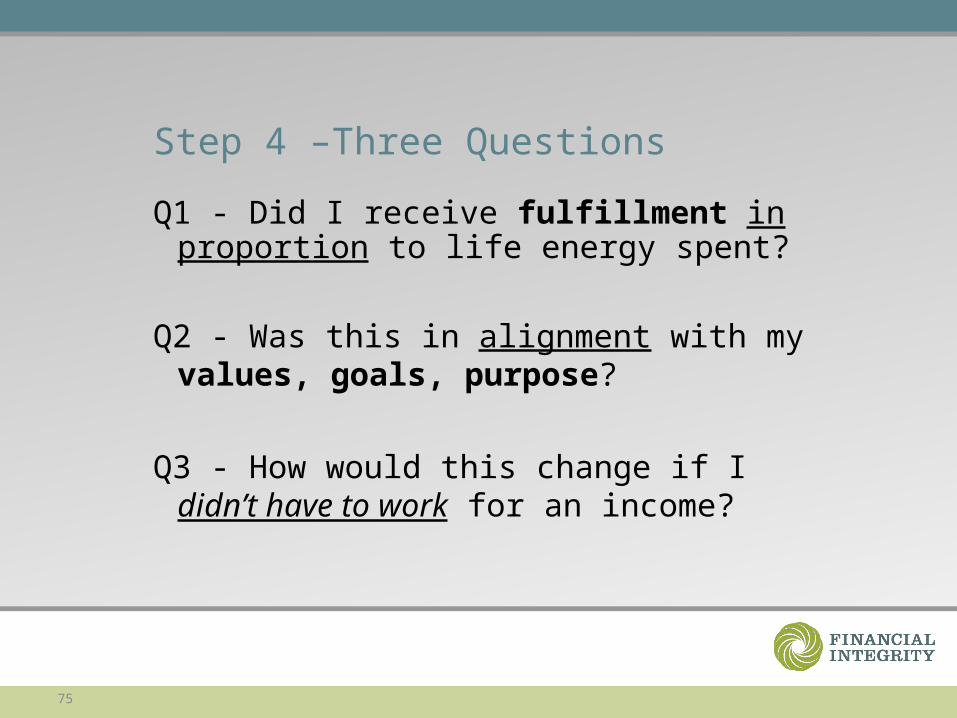

Step 4 –Three Questions

Q1 - Did I receive fulfillment in proportion to life energy spent?

Q2 - Was this in alignment with my values, goals, purpose?

Q3 - How would this change if I didn’t have to work for an income?

76

Step 4 –Add the Three QuestionsDecember RHW = $10 Q1 Q2 Q3

Inflows Amount Life Energy fulfillment alignment fin indep

paycheck $3,100.00 310

gifts $250.00 25interest $37.00 4sold car $4,500 450

$7,887

Outflows Amountcable -$47.44 5cellphone -$136.79 14drugstore -$66.90 7entertainment -$17.31 2gas -$138.25 14gifts -$284.86 28groceries -$626.28 63office -$109.26 11postal -$48.73 5restaurant -$30.00 3sports -$65.00 7car payment -$700.00 70rent -$2,000.00 200

-$4,270.82

77

Q1 –Fulfillment in Proportion

78

Step 4 – Rate Categories for Q1December RHW = $10 Q1 Q2 Q3

Inflows Amount Life Energy fulfillment alignment fin indep

paycheck $3,100.00 310

gifts $250.00 25interest $37.00 4sold car $4,500 450

$7,887

Outflows Amountcable -$47.44 5cellphone -$136.79 14drugstore -$66.90 7entertainment -$17.31 2gas -$138.25 14gifts -$284.86 28groceries -$626.28 63office -$109.26 11postal -$48.73 5restaurant -$30.00 3sports -$65.00 7car payment -$700.00 70rent -$2,000.00 200

-$4,270.82

79

Q2 –Alignment

80

Step 4 – Rate Categories for Q2December RHW = $10 Q1 Q2 Q3

Inflows Amount Life Energy fulfillment alignment fin indep

paycheck $3,100.00 310

gifts $250.00 25interest $37.00 4sold car $4,500 450

$7,887

Outflows Amountcable -$47.44 5cellphone -$136.79 14drugstore -$66.90 7entertainment -$17.31 2gas -$138.25 14gifts -$284.86 28groceries -$626.28 63office -$109.26 11postal -$48.73 5restaurant -$30.00 3sports -$65.00 7car payment -$700.00 70rent -$2,000.00 200

-$4,270.82

81

Q3 –Financial Independence

82

Step 4 – Rate Categories for Q3December RHW = $10 Q1 Q2 Q3

Inflows Amount Life Energy fulfillment alignment fin indep

paycheck $3,100.00 310

gifts $250.00 25interest $37.00 4sold car $4,500 450

$7,887

Outflows Amountcable -$47.44 5cellphone -$136.79 14drugstore -$66.90 7entertainment -$17.31 2gas -$138.25 14gifts -$284.86 28groceries -$626.28 63office -$109.26 11postal -$48.73 5restaurant -$30.00 3sports -$65.00 7car payment -$700.00 70rent -$2,000.00 200

-$4,270.82

83

Step 4 – Inventory Exercise

• Review your items from the Inventory Exercise.

(Needs, Comforts, Luxuries, Clutter)

• What value or goal (other than utility) motivated you to buy those items?

84

(Step 4 Reflection …)

85

Wall Chart

Step 5. Making Your Life Energy Visible

The Nine Step Process

86

Step 5 – Wall Chart

0

1000

2000

3000

4000

5000

6000

7000

8000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

income

expenses

87

Step 5 – Creating a 4-line Wall Chart

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Inflows

Outflows

Short-term Debt

Short-term Savings

88

(Step 5 Reflection …)

89

End of Session 2

90

Welcome Back!

Financial Integrity Transforming Your Relationship with Money

Session 3

91

Minimizing Spending

Step 6. Respecting Your Life Energy

The Nine Step Process

92

Step 6 – Why do we spend money?

What ------------------ Why?

93

Step 6 – Why do we spend money?

What ______________ Why?

Eat out Hungry (necessity)

Pay rent Shelter (necessity)

Gadgets For fun (luxury, clutter?)

New car Transportation (comfort?)

Cleaning service Comfort, convenience?

94

Step 6 – Conscious Actions

• Conscious Elimination

• Conscious Consuming

95

Step 6 – Conscious Elimination

• Eliminate consumer debt

• Develop maintenance skills

• Eliminate unnecessary medical costs

• Eliminate costly entertainment.

• Rent or borrow whenever possible.

• Eliminate gazingus pins.

• Find other ways of meeting the need

96

Step 6 – Conscious Consuming

• Wait for second generation/buy refurbished

• Look for quality

• Evaluate the value of add-ons

• Shop thrift stores (value for less money)

97

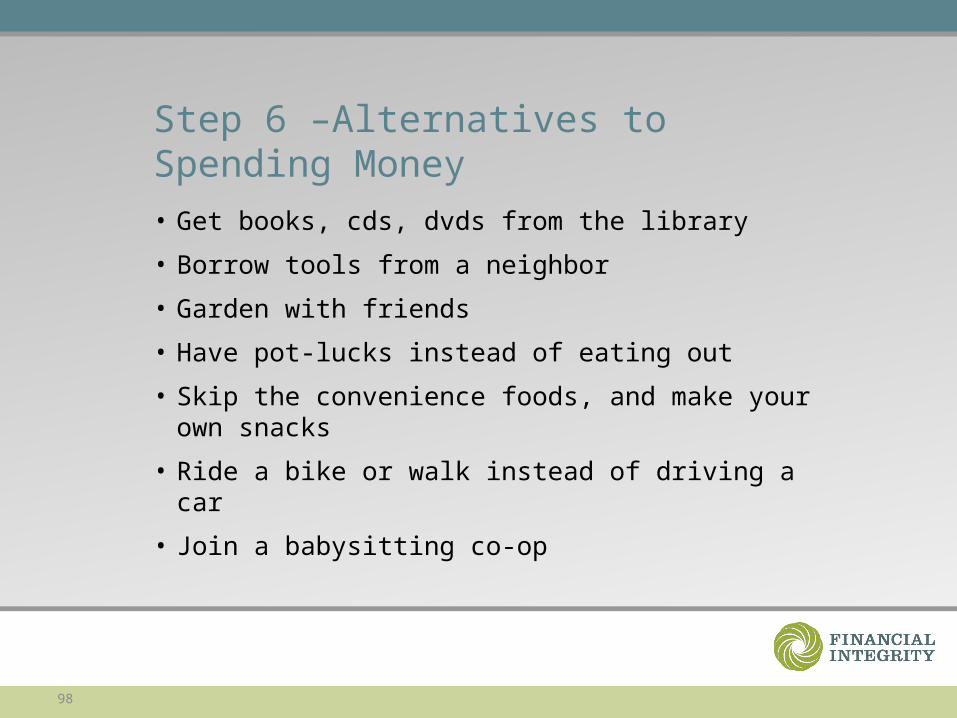

Step 6 –Alternatives to Spending Money

98

Step 6 –Alternatives to Spending Money• Get books, cds, dvds from the library

• Borrow tools from a neighbor

• Garden with friends

• Have pot-lucks instead of eating out

• Skip the convenience foods, and make your own snacks

• Ride a bike or walk instead of driving a car

• Join a babysitting co-op

99

(Step 6 Reflection …)

100

Maximizing Income

Step 7. Respecting Your Life Energy

The Nine Step Process

101

Step 7 – Maximizing Your Income

* Move toward the highest possible income

* commensurate with your integrity and health

* for a finite period of time

102

Step 7 – Conserving Life Energy

103

Step 7 –Why Work?

Why do people work?

Or …

What is the purpose of paid employment?

104

Step 7 –Why do people work?

Status

Contribute to society• To pay the bills

Get out of the house

Tradition• Health benefits, insurance

Stimulation

Be in contact with people

Meaning in my life

105

Step 7 – Income vs. Work

When we break the connection between income and work, we can look at our job and ask:

Is this really what I want to be doing

with my life energy?

106

Step 7 – Maximizing Your Income

Move toward the highest possible income

107

Step 7 – Maximizing Your Income

Move toward the highest possible income

commensurate with your integrity and health

108

Step 7 – Maximizing Your Income

Move toward the highest possible income

commensurate with your integrity and health

What are ways to increase your income, commensurate with your integrity and health?

109

Step 7 – Ways to Increase your Income What are ways to increase your income, commensurate

with your integrity and health?

• Research going rate

• Ask for raise or promotion (research prevailing wage for your area first)

• Take a second job

• Move to job that maximizes your sense of engagement as well as your income, rather than staying put merely for the sake of “security”

• Live within your means

110

Step 7 – Maximizing Your Income

Move toward the highest possible income

commensurate with your integrity and health

for a finite period of time

111

(Step 7 Reflection …)

112

Capital & Crossover

Step 8. Capital and the Crossover Point

The Nine Step Process

113

Step 8 – Living Within Your Means

0

1000

2000

3000

4000

5000

6000

7000

8000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

income

expenses

114

Step 8 – Compound Interest

The power of saving with compound interest

Wall Chart Investment with Compound Interest (pink)

0

2500

5000

7500

10000

12500

15000

17500

20000

22500

25000

27500

30000

year0

year2

year4

year6

year8

year10

year12

year14

year16

year18

year20

year22

year24

year26

year28

year30

Months

Money

115

Step 8 – “Independence” Income

My Wall Chart

-

1,000

2,000

3,000

4,000

5,000

6,000

Inflows

Outflows

Investment Income

116

Step 8 – What is Inflation?

Defined by society:

The statistical inflation rate is based upon the purchases of the average wage-earner. But, how average are you?

Defined by you:

117

(Step 8 Reflection …)

118

Managing Investments

Step 9. Securing Your Financial Independence

The Nine Step Process

119

Step 9 – Financial Independence

• Knowledgeable• Adept• Sophisticated

about appropriate investment vehicles

120

Step 9 – The 3 Pillars

The 3 Pillars of Financial Independence

• Cushion• Capital• Cache

121

Step 9 – Disintermediation

Taking responsibility for:• Knowing how to invest in alignment with your

goals and values• Implementing and managing those

investments

Dis-inter-mediation• “No middle man”• Going directly to the source

122

Step 9 – Investment Criteria

What investment criteria would you suggest?

123

Step 9 – Investment Criteria

• Safety• Guaranteed stable Income• Liquidity• Minimized costs (money)• Minimized costs (time)• Long-Term

124

How the Financial Integrity Program Works

All steps are interdependent.

The process is reflective and action based.

Each step is important to the whole.

You will see results even if you don’t do every step.

125

(transition to Participation …)

126

Independence vs. Inter-dependence

127

What are YOUR next steps?

128

Financial Integrity: Tips for Success• Create a place for your materials. • Customize the steps as you need to.• Be patient - change can be hard. • Keep a journal - record your changes over

time. • Check out resources.• Find support and friendship

129

Thank you for participating!