1 wendy jeffus harvard summer school international business

Post on 22-Dec-2015

225 views

TRANSCRIPT

1

Wendy Jeffus

Harvard Summer School

International Business

2

Remember Handout Globalization Debate

3

Introduction Participation Ranking… Discuss Trade Game (Video by Pong Trinidad)

– http://courses.fas.harvard.edu/sum/32584

Chapter 9: The Foreign Exchange Market– International Finance Extras

Nestlé Presentation Chapter 10: The International Monetary System Chapter 11: The Global Capital Market A Note on Microfinance (time permitting)

4

Participation Ranking 1st Jaime 2nd Jade 3rd Erika, Enrique, Johannes & Shekinah

Next MondayFantastic Participation Opportunity:“The Great Globalization Debate”

http://www.elko.k12.nv.us/jackpot/users/lolson/images/Students%20in%20Classroom%20clip%20art.gif

5

The Trade Game… Summary Were there any trade blocks created? At the end of the game the richest group was a

Tier II country with $44,000 in cash the poorest group was a Tier III country with $8,000 in cash.

If you could play the game again – what would you do differently?

6

Wendy Jeffus

Harvard Summer School

Chapter 10: The International Monetary System

7

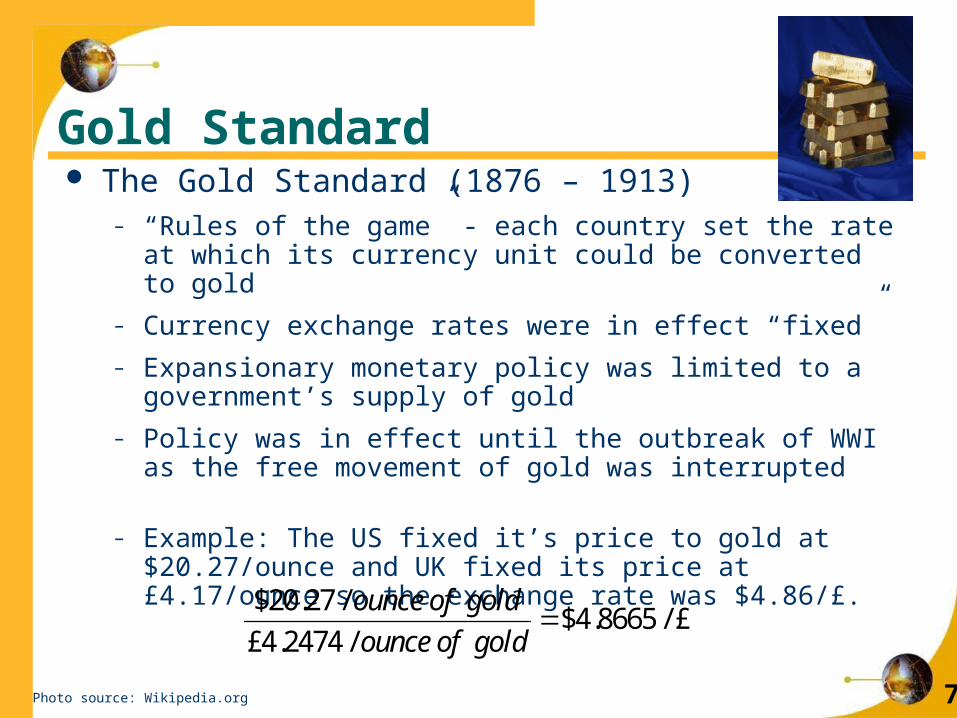

Gold Standard The Gold Standard (1876 – 1913)

– “Rules of the game” - each country set the rate at which its currency unit could be converted to gold

– Currency exchange rates were in effect “fixed”

– Expansionary monetary policy was limited to a government’s supply of gold

– Policy was in effect until the outbreak of WWI as the free movement of gold was interrupted

– Example: The US fixed it’s price to gold at $20.27/ounce and UK fixed its price at £4.17/ounce so the exchange rate was $4.86/£.

Photo source: Wikipedia.org

$20.27 /$4.8665 / £

£4.2474 /

ounce of gold

ounce of gold

8

History of the IMS The Inter-War Years & WWII (1918-1944)

– During this period, currencies were allowed to fluctuate over a fairly wide range in terms of gold and each other

– Increasing fluctuations in currency values became realized as speculators sold short weak currencies

– The US adopted a modified gold standard in 1934

During WWII and its chaotic aftermath the US dollar was the only major trading currency that continued to be convertible to gold.

9

How Bretton Woods reshaped the world In the summer of 1944, delegates from 44

countries met in the midst of World War II to reshape the world's international financial system.

The location of the meeting - The Mount Washington Hotel in rural Bretton Woods, New Hampshire – was to ensure that the delegates would have no distractions and no pressure from lobbyists or congress, as they worked on their plans for post-war reconstruction.

http://www.mountwashingtonresort.com/

10

Never again… The meeting was born out of the determination by US

President Franklin D Roosevelt and UK Prime Minister Winston Churchill to ensure post-war prosperity through economic co-operation, avoiding the economic conflicts between countries in the 1930s that they believed contributed to the drift to war.

One of the chief negotiators was John Maynard Keynes “We have had to perform at one and the same time the tasks appropriate to the economist, to the financier, to the politician, to the journalist, to the propagandist, to the lawyer, to the statesman-even, I think, to the prophet.”

11

2 Key Issues President Roosevelt told the conference: "The

economic health of every country is a proper matter of concern to all its neighbors, near and distant."

THE UK'S JOHN MAYNARD KEYNES ARGUED FOR A SINGLE WORLD CURRENCY

Two key issues: 1. How to establish a stable system of exchange rates2. How to pay for rebuilding the war-damaged economies of Europe

http://news.bbc.co.uk/2/hi/business/7725157.stm

12

History of the IMS Bretton Woods and the

International Monetary Fund (IMF) (1944)

– Countries agreed to peg their currencies to US$ which was convertible to gold at $35/oz

– Agreed not to engage in competitive devaluations for trade purposes and defend their currencies

– Weak currencies could be devalued up to 10% w/o approval

– Created two new institutions the International Monetary Fund (IMF) and the World Bank

Photo Source: Anti-WTO website (http://www.thirdworldtraveler.com/WTO_MAI/WTO.html)

13

History of the IMS The International Monetary Fund (IMF) is a key

institution in the new international monetary system and was created to:

– Help countries defend their currencies against cyclical, seasonal, or random occurrences

– Assist countries having structural trade problems if they promise to take adequate steps to correct these problems

The International Bank for Reconstruction and Development (World Bank) helped fund post-war reconstruction and has since then supported general economic development.

– The United States, Japan, Canada, Italy, France, Germany, Britain and Russia -- are among the bank's largest shareholders.

14

International Monetary Fund International Monetary Fund (IMF)

– Purpose: Maintain order in international monetary system To avoid a repetition of the competitive devaluations of the 1930s To control price inflation by imposing monetary discipline on countries

– Ready to lend funds to countries to help fight speculative pressure or to help correct fundamental disequilibrium in BOP position

Problems– Inappropriate policies

The IMF’s ‘one-size-fits-all’ approach to macroeconomic policy is inappropriate for many countries

– Moral hazard Countries behave recklessly when they know they will be saved if things go

wrong– Lack of Accountability

The IMF has become too powerful for an institution that lacks any real mechanism for accountability

15

IMF

http://www.imf.org/external/np/exr/center/action/eng/devalue/index.htm

16

Collapse of the Fixed Exchange System Factors that led to the collapse of the fixed

exchange system include– President Johnson financed both the Great Society

and the Vietnam war by printing money– High inflation and high spending on imports– On August 8, 1971, President Nixon announces dollar

no longer convertible into gold Countries agreed to revalue their currencies against the

dollar– On March 19, 1972, Japan and most of Europe

floated their currencies– In 1973, Bretton Woods fails because the key

currency (dollar) is under speculative attack

17

History of the IMS An Eclectic Currency Arrangement (1973 –

Present)– Since March 1973, exchange rates have become

much more volatile and less predictable than they were during the “fixed” period

– There have been numerous, significant world currency events over the past 30 years.

18

Exchange Rates Since 1973 Exchange rates have been more volatile for a number of

reasons including:– Oil crisis -1971– Loss of confidence in the dollar - 1977-78– Oil crisis – 1979, OPEC increases price of oil– Unexpected rise in the dollar - 1980-85

Trade deficit, but economic growth, high real interest rates and flight to quality

– Rapid fall of the dollar - 1985-87 and 1993-95– Partial collapse of European Monetary System - 1992– Asian currency crisis – 1997– 2001 – 2002 general economic slowdown in the U.S.– 2004 – lowest value of the dollar since 1973– 2008 – Subprime crisis

19

Gold Prices

Source: http://goldprice.org/gold-price-history.html

20

Fixed Vs. Flexible Exchange Rates Countries would prefer a fixed rate regime for the

following reasons:– Stability in international prices– Inherent anti-inflationary nature of fixed prices

However, a fixed rate regime has the following problems:– Need for central banks to maintain large quantities of hard

currencies and gold to defend the fixed rate– Fixed rates can be maintained at rates that are inconsistent with

economic fundamentals

21

Exchange Rate Regimes Exchange arrangements with no separate legal tender (Ecuador,

Panama, & EUl)– The currency of another country circulates as the sole legal tender or the

member belongs to a monetary or currency union in which the same legal tender is shared by the members of the union.

Currency board arrangements (Bosnia and Herzegovina)– Based on an explicit legislative commitment to exchange domestic currency

for a specified foreign currency at a fixed exchange rate, combined with restrictions on the issuing authority.

Conventional fixed peg arrangements (Kuwait & Qatar)– The country pegs its currency within margins of ±1 percent or against

another currency or a basket of currencies, where the basket is formed from the currencies of major trading or financial partners and weights reflect the geographical distribution of trade, services, or capital flows.

The monetary authority maintains the fixed parity through direct intervention (i.e., via sale/purchase of foreign exchange in the market) or indirect intervention (e.g., via the use of interest rate policy, imposition of foreign exchange regulations, exercise of moral suasion that constrains foreign exchange activity, or through intervention by other public institutions).

Check the exchange rate regime for your final project here: http://www.imf.org/external/np/mfd/er/2006/eng/0706.htm

4%

22%

26%

22

Exchange Rate Regimes Crawling pegs (Costa Rica)

– The currency is adjusted periodically in small amounts at a fixed rate or in response to changes in selective quantitative indicators, such as past inflation differentials vis-à-vis major trading partners, differentials between the inflation target and expected inflation in major trading partners.

The rate of crawl can be set to adjust for measured inflation or other indicators (backward looking), or set at a preannounced fixed rate and/or below the projected inflation differentials (forward looking).

Managed floating with no predetermined path for the exchange rate (Argentina, Sudan, & Thailand)

– The monetary authority attempts to influence the exchange rate without having a specific exchange rate path or target. Indicators for managing the rate are broadly judgmental (e.g., balance of payments position, international reserves, parallel market developments), and adjustments may not be automatic. Intervention may be direct or indirect.

Independently floating (Chile, Canada, & Brazil)– The exchange rate is market-determined, with any official foreign

exchange market intervention aimed at moderating the rate of change and preventing undue fluctuations in the exchange rate, rather than at establishing a level for it.

Source: http://www.imf.org/external/np/mfd/er/2006/eng/0706.htm

28%

14%

6%

23

Attributes of the “Ideal” Currency Possesses three attributes, often referred to as

the Impossible Trinity:– Exchange rate stability– Full financial integration– Monetary independence

The forces of economics do not allow the simultaneous achievement of all three

Monetary AutonomyMonetary Autonomy

24

Why Not?

Monetary AutonomyMonetary Autonomy

If a government chooses fixed exchange rates (Exchange Rate Stability) and capital mobility, it has to give up monetary autonomy.

– Examples: Ecuador, Panama If it chooses monetary

autonomy and capital mobility, it has to go with floating exchange rates.

– Examples: Brazil, United States

Finally, if it wishes to combine fixed exchange rates with monetary independence, it has to limit capital mobility.

– Example: Venezuela

25

Strong Dollar The Honorable Paul O’Neill Secretary of the Treasury Washington DC 20220 June 4, 2001Dear Mr. Secretary:We are writing to tell you that at current levels the exchange value of the dollar is having a strong negative impact on manufacturing exports,

production, and employment. A growing number of American factory workers are now being laid off principally because the dollar is pricing our products out of markets – both at home and abroad. Small firms are being affected as well as large ones. As you balance your responsibilities for international monetary stability and domestic economic growth, we ask that you take into account the growing burden an overvalued dollar is imposing on U.S. manufacturing.

Since early 1997 the dollar has appreciated by 27 percent. Industries such as aircraft, automobiles and parts, paper and forest products, machine tools, medical equipment, steel, and other capital goods-as well as consumer goods producers-are being affected very significantly. No amount of cost cutting can offset a nearly 30 percent dollar markup.

The total effect on the U.S. economy is staggering. These output losses are particularly serious at this time, as they coincide with a general economic slowdown. The economic fundamentals have changed dramatically in the last six months. Production and profitability are down, and manufacturing employment has fallen by more than a half million jobs since mid-2000. Yet, in the face of slowing economic growth, declining interest rates, and rising manufacturing unemployment, the dollar has remained high.

In our view, a clarification of Treasury policy is in order, to be certain that it is not seen as endorsing an ever stronger dollar irrespective of the economic fundamentals. We urge the Treasury to make it clear that the value of the dollar should be consistent with economic reality and market conditions. This policy should be joined by a commitment to further reductions in interest rates and to cooperating in exchange markets as appropriate. Moreover, it is vital that the Treasury not condone currency manipulation by trading partners seeking to make their exports more competitive.

Mr. Secretary, 18 million workers and their families depend directly on the continued strength and competitiveness of American manufacturing. Many more Americans rely on stockholding in our companies for their retirement income. We would like to meet with you to describe more fully the effects the value of the dollar is having on us. We hope you will be able to accommodate our request.

Respectfully,Jerry J. Jasinowski, President John W. Douglas, President and CEO National Association of Manufacturers Aerospace Industries Association W. Henson Moore, President and CEO Don Carlson, PresidentAmerican Forrest and Paper Association The Association for Manufacturing TechnologyStephen Collins, President Christopher M. Bates, President & CEOAutomotive Trade Policy Council Motor Equipment Manufacturers Association

26

Bernanke Breakhttp://www.youtube.com/watch?v=3u2qRXb4xCU

Image Source: http://abluteau.files.wordpress.com/2009/02/printing-money.jpg

27

Crises 1994 – Mexico 1997 – Thailand 1998 – Russia 1999 – Brazil 2001 – Turkey 2002 – Argentina 2008 – U.S.

Cartoon: Copyright Christopher Weyant, Latin Finance, March 1999“Brazil's currency, the real, crashes and loses 30% of its value and threatens to drive the economy into recession and reignite inflation.” Source: www.latinfinance.com/default.asp?page=36&ISS=6458&SID=308098&YEAR=1999

28

Predicating Crisis On Black Wednesday (September 16, 1992), Soros

became immediately famous when he sold short more than $10 billion worth of pounds, profiting from the Bank of England's reluctance to either raise its interest rates to levels comparable to those of other European Exchange Rate Mechanism countries or to float its currency.

– The Bank of England was forced to withdraw the currency out of the European Exchange Rate Mechanism and to devalue the pound sterling, and Soros earned an estimated US$ 1.1 billion in the process. He was dubbed "the man who broke the Bank of England."

In 1997, during the Asian financial crisis, then Malaysian Prime Minister accused Soros of using the wealth under his control to punish ASEAN for welcoming Myanmar as a member. He has been called "an economic war criminal" who "sucks the blood from the people."

Source: wikipedia.org, http://www.bloggernews.net/wp/wp-content/uploads/2007/09/g_soros.jpg

29

Predicting Crisis Soros' 2008 book, The New Paradigm for

Financial Markets, describes a "superbubble" that has built up over the past 25 years and is now ready to collapse. This is the third in a series of books he's written that have predicted disaster. As he states:

– “I have a record of crying wolf…. I did it first in The Alchemy of Finance (in 1987), then in The Crisis of Global Capitalism (in 1998) and now in this book. So it's three books predicting disaster. (After) the boy cried wolf three times . . . the wolf really came.”

Source: wikipedia.org, http://www.greekshares.com/uploaded/files/george_soros.jpghttp://aftermathnews.files.wordpress.com/2008/04/soros-psychonut.jpg

30

Crisis Management by the IMF The IMF’s activities have expanded because periodic

financial crises have continued to hit many economies– Currency crisis

When a speculative attack on a currency’s exchange value results in a sharp depreciation of the currency’s value or forces authorities to defend the currency

– Banking crisis Loss of confidence in the banking system leading to a run on the

banks– Foreign debt crisis

When a country cannot service its foreign debt obligations

31

Mexico: The Tequila Crisis December 20, 1994 – Currency Devaluation

– Following the December 20 devaluation, the peso fell by 50 percent in one week. Argentina and Venezuela’s currencies also depreciated. Causes:

– An overvalued fixed exchange rate, – A non-independent Central Bank, – Weak financial regulation, – Short-term dollar-denominated debt, – Political assassinations.

As foreign reserves declined throughout 1994, investors started to fear that the Mexican government could not afford to maintain the peg against the US dollar.

Massive runs on the banks weakened the peso even further - with severe consequences for the country's business infrastructure, as well as its population.

http://www2.gsb.columbia.edu/ipd/j_bankingMXN.html

32

The Asian Crisis July 1997 - Thailand allowed its currency to float (and the baht fell 20%) This spread to the Philippines, Malaysia, S. Korea and Singapore. Indonesia held out, but on October 1, 1997 the rupiah eventually fell 6.5%. Causes:

– Deteriorating balance-of payments position The transition of many Asian nations from being net exporters to net importers.

– Speculative overbuilding & excess investment (dollar denominated debt)

– Cronyism

As the investment “bubble” expanded, some market participants questioned the ability of the economy to repay the rising amount of debt and the Thai bhat came under attack.

Mid 1997 several key Thai financial institutions were on the verge of default– The IMF offered Thailand 17.2 billion in loans.

33

Explain Contagion? Think of it this way… Imagine a father with several sons. Each son

thinks that his father will support him in his time of need. But, if one son needs support then the father has fewer resources for the other children. The value of the support option has diminished. Now the other sons will look a lot less creditworthy.

Source: When Genius Failed

34

The Russian Crisis August 17, 1998 Russia declared a debt moratorium.

– The government decided it would rather use its rubles to pay its workers than Western bondholders.

Europe (London fell 3%, Spain fell 6%), Turkey, Brazil (fell 10%) and Venezuela followed.

Causes: Artificial low prices in Communist era Shortage of goods & liberalized price controls

– Too many rubles chasing too few goods Growing public sector debt

The IMF structured a $22.6B bailout, but most of the money went to politicians and the wealthy.

George Soros’s fund lost $2B from Russia’s collapse.

●

35

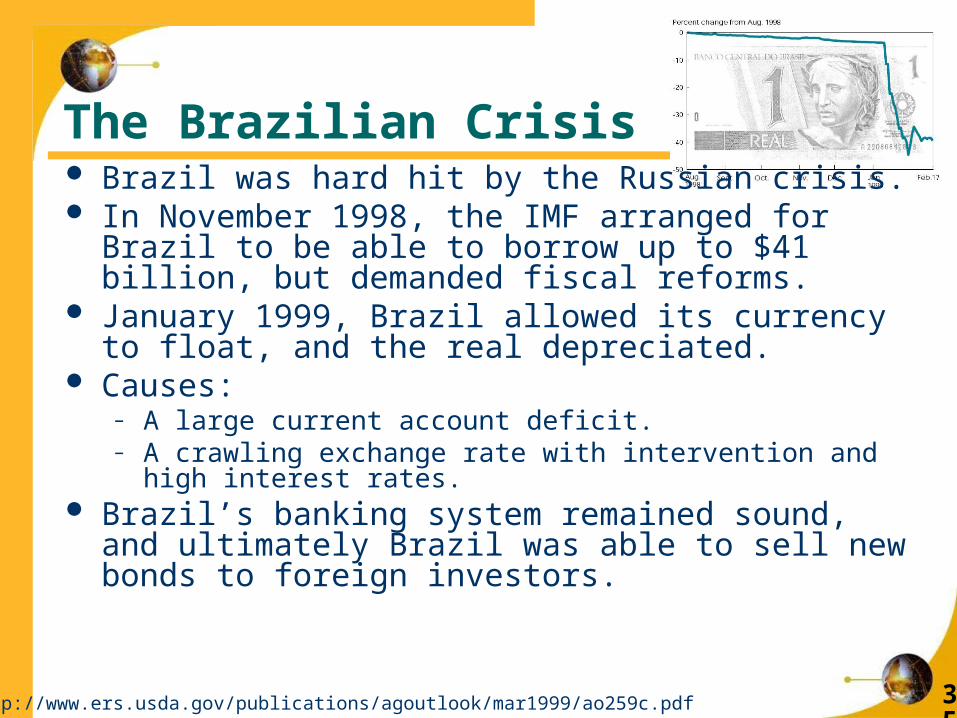

The Brazilian Crisis Brazil was hard hit by the Russian crisis. In November 1998, the IMF arranged for Brazil to be

able to borrow up to $41 billion, but demanded fiscal reforms.

January 1999, Brazil allowed its currency to float, and the real depreciated.

Causes:– A large current account deficit.– A crawling exchange rate with intervention and high interest

rates. Brazil’s banking system remained sound, and ultimately

Brazil was able to sell new bonds to foreign investors.

http://www.ers.usda.gov/publications/agoutlook/mar1999/ao259c.pdf

36

The Turkish Crisis, 2001 Turkey had borrowed continually from the IMF since

1958. In January 2000, Turkey borrowed $8 billion more

from the IMF and World Bank. As part of the deal, Turkey pledged to:

– Reduce its inflation rate (100%)– Improve bank regulation– Privatize state-owned businesses– End subsidies– Reduce its fiscal deficit– Adopt a crawling exchange rate, pegged to the euro and

dollar

37

The Turkish Crisis Turkey made progress on inflation, but

(Causes):– Continued to run large budget and current account

deficits (fixed exchange rates)– Suffered more bank corruption– Foreign lenders pulled back– Overnight interest rates rose to 2000%– February 2001, the government was in gridlock

over passing reforms,

38

The Argentine Crisis In 1991 the Argentine peso had been fixed to the US

dollar at a one-to-one rate of exchange. In January 2002, the peso was devalued as a result of

enormous social pressures resulting from deteriorating economic conditions and substantial runs on banks.

Causes:– The Argentine Peso was overvalued– A currency board regime had eliminated monetary policy

alternatives for macroeconomic policy– The Argentine government budget deficit – and deficit spending

– was out of control

39

Banking Crises 2008

Decline inCredibilityof Current

Exchange Rate

BankingCrisis

Downturn inEconomic

Development

CostlyFiscal

Bailout

CapitalFlight

DramaticallyEasier

MonetaryPolicy Decline in

Central Bank’sForeign Currency

Reserves

CurrencyCrisis

Decline inCredibilityof Current

Exchange Rate

BankingCrisis

Downturn inEconomic

Development

CostlyFiscal

Bailout

CapitalFlight

DramaticallyEasier

MonetaryPolicy Decline in

Central Bank’sForeign Currency

Reserves

CurrencyCrisis

Not all crises are preceded by banking crises, but banking crises tend to aggravate the crisis.

Source: Exchange Rate Determination

40

Sub Prime Lending Loans to people in low economic standing at high rates.

– Similar to “Pay Day Loans” working against people who can’t afford the loans.

– In a market with rising housing prices, some investors believed that the price of the house would offset the high cost of these loans (liar loans, NINJAs “no income, no job, no assets,” “stated income,” “no-documentation,” and “100 percent financing” loans)

– Banks were securitizing loans quickly… It’s a game of pass the risk… (sort of like “hot potato”)

– Remember the “Greater Fool Theory”

http://www.fool.co.uk/money-talk/your-money/2007/09/25/how-the-credit-crunch-could-hurt-you.aspx

http://www.boston.com/business/personalfinance/articles/2007/08/29/credit_crunch_means_more_foreclosures_and_much_tougher_loan_terms/

41

http://2.bp.blogspot.com/_1V7wnZxPqok/RsqMqBot9NI/AAAAAAAAGXo/mpN0yZTf2tc/s400/cartoon%2Bmortgage.png

42

What does this mean? Between 2000 and 2006 mortgage lenders in the U.S.

relaxed standards… In 2007 the bubble burst House prices started decreasing. Defaults and

foreclosures, increased. Mortgage financing has become tougher.

– BUT as more homeowners are forced into foreclosure -the surge of bargain homes on the market will further depress prices.

Auto loans and credit cards may also become more expensive for consumers.

Note those with above-average credit ratings will fare well in the purge of the riskiest kinds of mortgages from lender portfolios.

http://www.boston.com/business/personalfinance/articles/2007/08/29/credit_crunch_means_more_foreclosures_and_much_tougher_loan_terms/

43

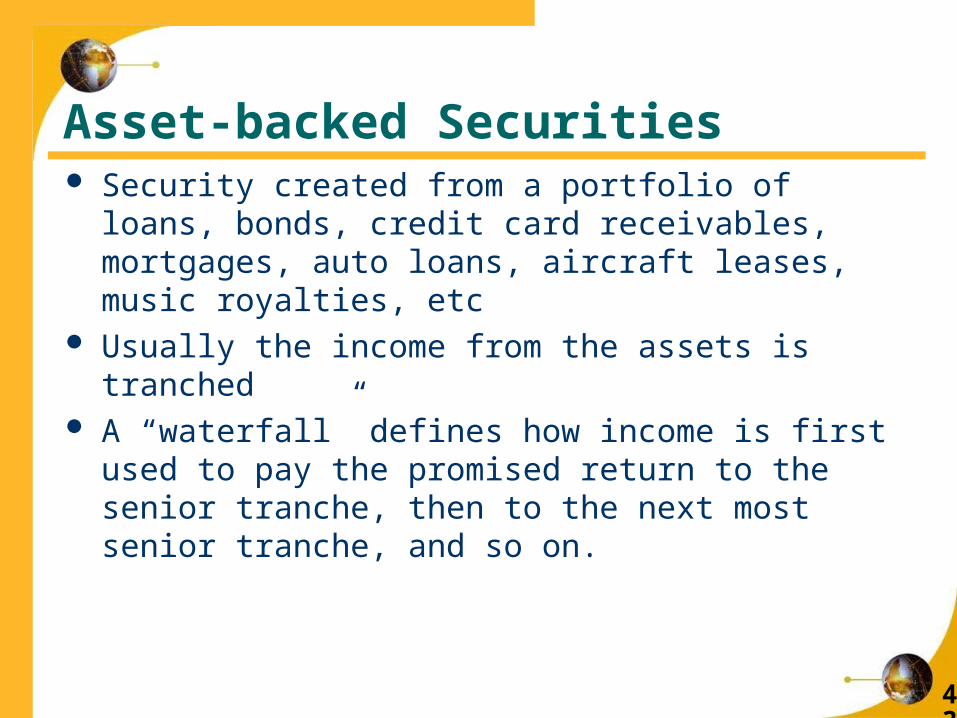

Asset-backed Securities Security created from a portfolio of loans, bonds, credit

card receivables, mortgages, auto loans, aircraft leases, music royalties, etc

Usually the income from the assets is tranched A “waterfall” defines how income is first used to pay the

promised return to the senior tranche, then to the next most senior tranche, and so on.

44

Possible StructurePossible Structure

Asset 1Asset 2Asset 3

Asset n

Principal=$100 million

SPV

Tranche 3(super senior)

Principal=$75 millionYield = 6%

Tranche 2(mezzanine)

Principal=$20 millionYield = 10%

Tranche 1 (equity)

Principal=$5 millionYield = 30%

Imagine a bank has several auto loans, the loans are classified as “prime” “non prime” and “subprime”The bank may decide to take it’s 10,000 non prime loans and sell them to a Special Purpose Vehicle (SPV)

The bank will collect a fee for originating and servicing the loans

The credit riskassociatedwith the loansis passed on to the investors

Total $100 Million

AAA

BBB

45

The Mezzanine Tranche The Mezzanine Tranche is Most Difficult to Sell…is Most Difficult to Sell…

45

Subprime Mortgage Portfolio Equity Tranche (5%)

Not Rated

Mezzanine Tranche (20%)BBB

Super Senior Tranche (75%)AAA

Super Senior Tranche (80%) AAA

Mezzanine Tranche (15%) BBB

Equity Tranche (5%)

The mezzanine tranche is repackaged with other similar mezzanine tranches

Asset 1 (mezzanine)Asset 2 (mezzanine)Asset 3 (mezzanine)

Asset n (mezzanine)

Principal=$100 million

… Since the Mezzanine tranche is difficult to sell, dealers began to put the Mezzanine tranches together.The dealer may decide to take 20 mezzanine tranches from asset backed securities and sell them

AAA?!

Source; (Figure 23.3 Options, Futures and Other Derivatives by Hull)

46

http://www.1stmillionat33.com/2007/08/

47

Tulip Mania: Is a Tulip worth $76K? In 1593. Conrad Guestner imported the first tulip bulb into Holland from Constantinople, in present

day Turkey. – Tulip bulbs became a status symbol of the rich. The tulip craze spread to Germany where a few tulip bulbs

contracted a non-harmful plant virus called mosaic. (This virus caused tulip petals to display beautiful “flames” of color – increasing the value)

Rapidly rising price attracted speculators looking to profit. By 1634, tulip mania had spread to the Dutch middle class.

Soon everybody was dealing in tulip bulbs, looking to make a quick fortune. The majority of the tulip bulb buyers had no intentions of even planting these bulbs! The whole Dutch nation was caught up in tulip mania, people traded in their land, livestock, farms and life savings to acquire 1 single tulip bulb!

– In less than one month, the price of tulip bulbs went up twenty-fold! To put that into perspective, if you had invested $1,000 and came back on month later, your investment would have ballooned

to $20,000! In 1636, tulips were trading hands on the Amsterdam stock exchange as well as on exchanges

– Exchanges started to offer option contracts to speculators. These option contracts allowed tulip bulbs to be speculated on for a fraction of the price of a real tulip bulb (this allowed people of lower means to speculate). Options allowed for leverage - buyers were now able to control larger amounts of tulip bulbs.

Before a $1,000 dollar investment would have yielded $20,000 in one month with option leverage the same investment of $1,000 could to balloon to $100,000 in a month!

– Unfortunately, leverage is a double-edged sword. If the tulip bulb price moved downwards ever so slightly, the option buyer’s investment would be lost and they might even owe money! But at this point, it was commonly believed that the tulip market was immune to crashing and that it would “always go up”.

– The Dutch government started to develop regulation to help control the tulip craze. It was at this point that a few informed speculators started liquidating their tulips bulbs and contracts. It was these people, or

the “smart money,” that secured large profits that were now in the form of cold hard cash. – In addition, more tulip bulbs were added to the supply. Suddenly tulip bulbs weren’t quite as rare as before.

The tulip market began a slight down trend, but shortly after started to plummet. – Suddenly the market began a widespread panic when everyone started realizing that tulips were not worth the

prices people were paying for them. In less than 6 weeks, tulip prices crashed by over 90%. Fortunes were lost. Bankruptcies were everywhere due to the negative side of option leverage. People that traded in farms and live savings for a tulip bulb were left holding a worthless plant seed.

http://www.stock-market-crash.net/tulip-mania.htm

48

Tulip Mania! These valuable items

COMBINED only equaled the value of 1 tulip bulb! The modern day value of these items is over $40,000!

– four tons of wheat– eight tons of rye– one bed– four oxen– eight pigs– 12 sheep– one suit of clothes– two casks of wine– four tons of beer– two tons of butter– 1,000 pounds of cheese– one silver drinking cup

= 1

Source: http://www.stock-market-crash.net/tulip-mania.htm http://www.touchofnature.com/Fall%20Pictures/bulb_tulip.jpg

49

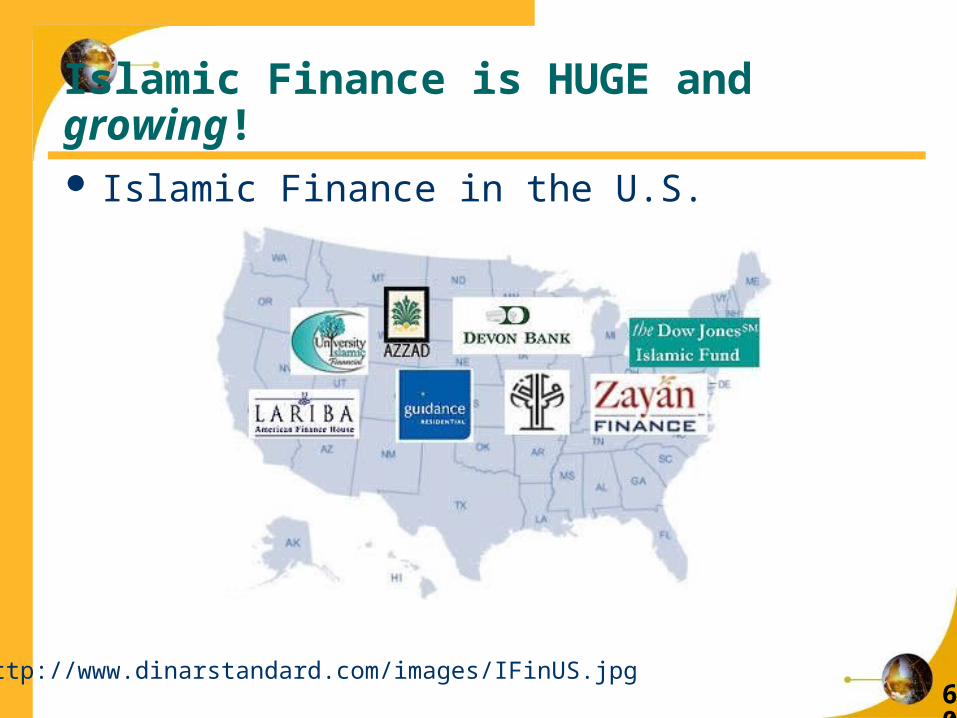

Islamic Finance is HUGE and growing! Islamic Finance in the U.S.

http://www.dinarstandard.com/images/IFinUS.jpg

50

Islamic Finance The Muslim population represent 1/4th of the world’s

population. Under Islam, the following beliefs affect business and

finance:– Making money from money is not permissible– Earning interest is prohibited– Profit and loss should be shared– Speculation is prohibited– Investments should only support activities that are legal under

Islamic law

51

Islamic Finance An Islamic bank cannot pay interest to depositors who

are Muslim.– So depositors are considered shareholders and the returns they

receive are a function of the bank’s investments.– Returns are not guaranteed, because profit and loss must be

shared. To buy a home under Islamic law:

– The buyer selects a property which is purchased by the bank.– The bank then resells the property to the buyer at a higher price

and the buyer is allowed to pay off the bank over a period of time.

– One problem: in the U.S. and the U.K. the difference is not a tax deductible expense for the homeowner.

52

Islamic Banking… Update Kuwait's commerce minister, Ahmad Baqer, was quoted

as saying that the global crisis will prompt more countries to use Islamic principles in running their economies.

U.S. Deputy Treasury Secretary Robert M. Kimmet, said experts at his agency have been learning the features of Islamic banking.

Though the trillion-dollar Islamic banking industry faces challenges with the slump in real estate and stock prices, advocates say the system has built-in protection from the kind of runaway collapse that has afflicted so many institutions.

– For one thing, the use of financial instruments such as derivatives, blamed for the downfall of banking, insurance and investment giants, is banned. So is excessive risk-taking.

http://www.isna.net/articles/News-Briefs/ISLAMIC-BANKING-STEADY-IN-SHAKY-TIMES.aspx

53

"The beauty of Islamic banking and the reason it can be used as a replacement for the current market is that you only promise what you own. Islamic banks are not protected if the economy goes down -- they suffer -- but you don't lose your shirt," said Majed al-Refaie, who heads Bahrain-based Unicorn Investment Bank.

http://www.isna.net/articles/News-Briefs/ISLAMIC-BANKING-STEADY-IN-SHAKY-TIMES.aspx

54

"In Islamic finance you cannot make money out of thin air," said Amr al-Faisal, a board member of Dar al-Mal al-Islami, a holding company that owns several Islamic banks and financial institutions. "Our dealings have to be tied to actual economic activity, like an asset or a service. You cannot make money off of money. You have to have a building that was actually purchased, a service actually rendered, or a good that was actually sold."

http://www.isna.net/articles/News-Briefs/ISLAMIC-BANKING-STEADY-IN-SHAKY-TIMES.aspx

55

He has also borrowed from an Islamic bank, to buy a building. Even if he's late in his payments, he said, he will not have to pay cumulative interest or a larger sum than the one agreed upon. But he notes that under this system, it can be harder to get a loan than from a conventional bank. Islamic banks have stricter lending rules and require that their borrowers provide more collateral and have higher income.

http://www.isna.net/articles/News-Briefs/ISLAMIC-BANKING-STEADY-IN-SHAKY-TIMES.aspx

56

Islamic finance first sparked interest in the United States in the late 1990s. The Dow Jones Islamic Index was established in 1999, and the Dow Jones Islamic Fund, which invests in sharia-compliant companies, the following year.

In 2004, the first Islamic bank opened in Britain, which now has six Islamic financial institutions, including a retail bank

http://www.isna.net/articles/News-Briefs/ISLAMIC-BANKING-STEADY-IN-SHAKY-TIMES.aspx

57

Islamic banking has grown by about 15 percent a year since its modern inception in the 1970s, fueled by the Middle East oil boom of that decade.

Islamic finance now accounts for about 1 percent of the global market, according to Majid Dawood, chief executive of Yasaar, a Dubai-based sharia financing consultancy. "We had expected to be at 12 percent of the global market by 2025, but now with this financial crisis, we expect to get there much faster," he said in a telephone interview from New York, where he was speaking at a conference on Islamic banking.

http://www.isna.net/articles/News-Briefs/ISLAMIC-BANKING-STEADY-IN-SHAKY-TIMES.aspx

58

Australian Minister to Attract Islamic Finance

06/08/09 – (Bloomberg) Australia may seek to attract more Islamic financing to Sydney to beat the global recession.

Australia, could create jobs and wealth by attracting a percentage of the Islamic finance market.

http://www.bloomberg.com/apps/news?pid=20601081&sid=aaZcnbc95yb0&refer=australia

59

Japan's Nomura Securities to list $100M Sukuk on Malaysia Exchange

07/13/10 - Japan's top securities firm Nomura will list its inaugural 100 million dollars of Islamic bonds on Bursa Malaysia as the company looks to diversify its funding sources…

Nomura is the second foreign issuer to house its sukuk on the Malaysian bourse.

Last November, General Electric Capital Corp., the world’s biggest non-bank finance company, sold 500 million dollars of sukuk in Malaysia.

http://www.google.com/hostednews/afp/article/ALeqM5iUvqppc36UrLZa60cG5QMYJ-7g0Q

60

Islamic Finance is HUGE and growing! Islamic Finance in the U.S.

http://www.dinarstandard.com/images/IFinUS.jpg

61

Take a Break… MTV & Nestlé teams if you haven’t done so, load

your presentations on the desktop, grab a drink, meet your classmates…

see you in 10 min.

Image source: http://www.graduatejunction.net/images/take_a_break.jpg

If you haven’t already…Discover 5 things you have in commonwith your assigned groups.

62

Wendy Jeffus

Harvard Summer School

Chapter 11: The Global Capital Market

63

Global Cost & Availability of Capital Global integration of capital markets has given

many firms (and individuals) access to new and cheaper sources of funds beyond those available in their home markets.

Yen Photo Source: http://www.bloomberg.com/apps/news?pid=20601101&sid=aRjgeKZTGkJU&refer=japan

In Hungary some home mortgages are issued in Swiss Francs

In Latvia and Romania some home mortgages are issued in Yen.

Why? Switzerland & Japan have some of the lowestinterest rates, allowing home buyers to save as muchas 5% a year (as long as the currency does not appreciate)

64

Global Cost of Capital What are the benefits of achieving a lower

cost and greater availability of capital?– A firm can accept more long term projects and invest

more in capital improvements and expansion because of the lower hurdle rate in capital budgeting and the lower marginal cost of capital as more funds are raised.

65

Why do companies seek global equity? Improved liquidity Possible higher share price Increase the firm’s visibility “Acquisition currency” Compensate foreign management

66

Eurocurrency Markets Eurocurrency – any currency banked outside of its

country of origin. Eurodollars – dollars banked outside of the U.S.

– Euroyen, europound, euro-euro

In 1950 Eurocurrency Market was born as Eastern Europeans were afraid to deposit $ in the U.S. fearing that they would be seized to finance lost business from the Communist takeover of Europe.

– London was happy to take the money and paid higher interest rates (see the next slide).

67

Comparative Spreads Between Lending and Deposit Rates in the Eurodollar Market

3.000 %

7.000 %DomesticLoan Rate

DomesticDeposit Rate

Domestic Spreadof 4.000%

Eurodollar Loan Rate

Eurodollar Deposit Rate

Eurodollar Spread of 0.500%

Interest Rate

4.625 %

4.125 %

Source: Multinational Business Finance Exhibit 11.4

68

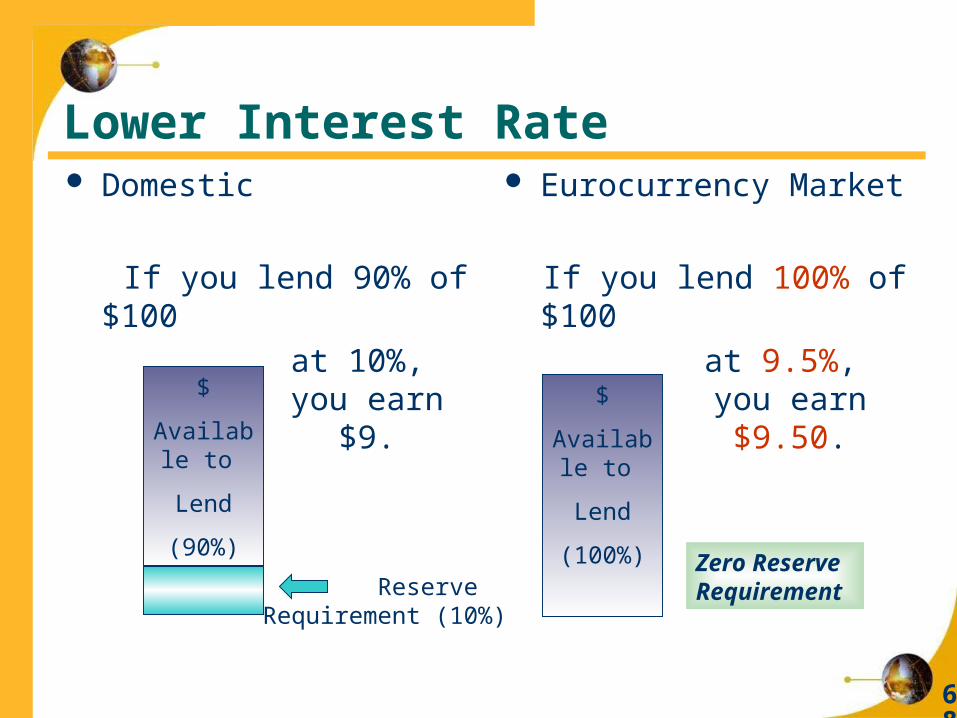

Lower Interest Rate Domestic

If you lend 90% of $100

$

Available to

Lend

(90%)

Reserve Requirement (10%)

at 10%, you earn

$9.

Eurocurrency Market

If you lend 100% of $100

$

Available to

Lend

(100%)

at 9.5%, you earn

$9.50.

Zero Reserve Requirement

69

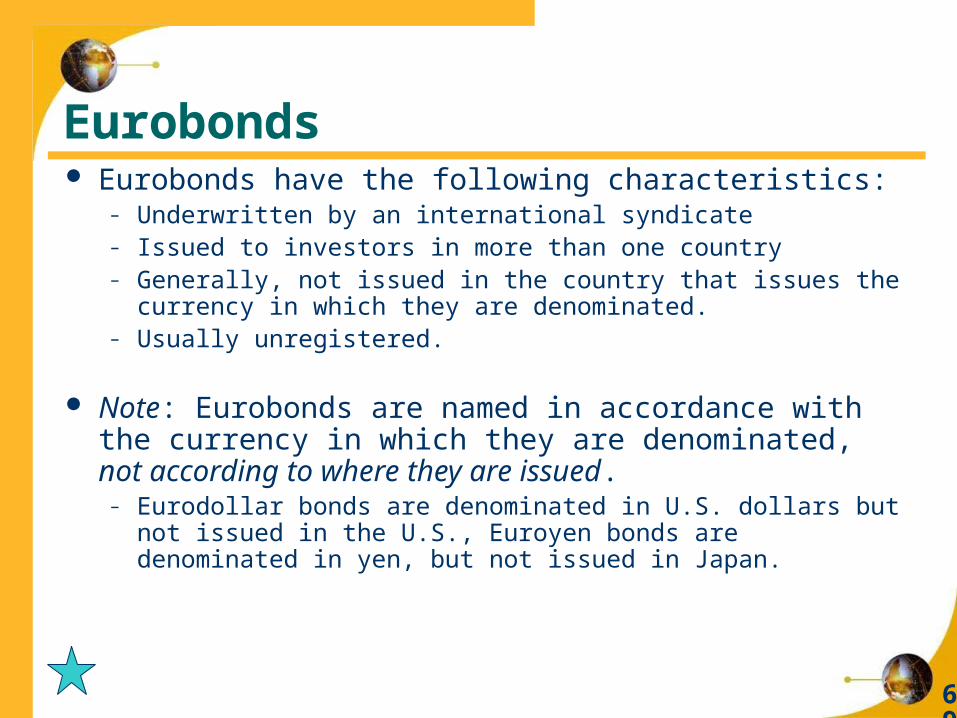

Eurobonds Eurobonds have the following characteristics:

– Underwritten by an international syndicate– Issued to investors in more than one country– Generally, not issued in the country that issues the currency in

which they are denominated.– Usually unregistered.

Note: Eurobonds are named in accordance with the currency in which they are denominated, not according to where they are issued.

– Eurodollar bonds are denominated in U.S. dollars but not issued in the U.S., Euroyen bonds are denominated in yen, but not issued in Japan.

70

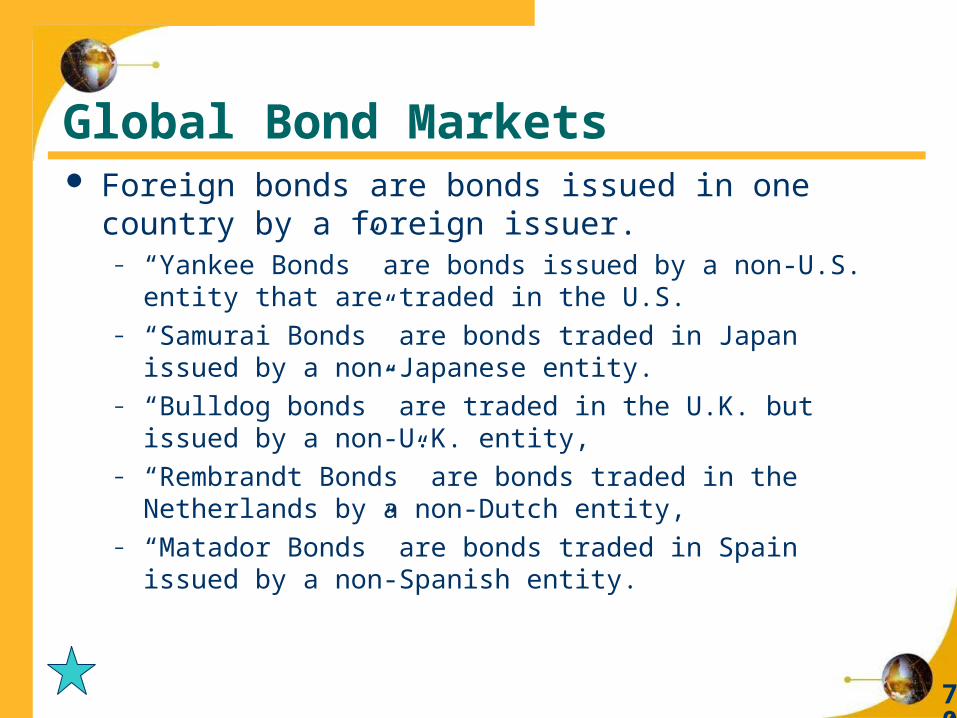

Global Bond Markets Foreign bonds are bonds issued in one country by a

foreign issuer. – “Yankee Bonds” are bonds issued by a non-U.S. entity that are

traded in the U.S. – “Samurai Bonds” are bonds traded in Japan issued by a non-

Japanese entity. – “Bulldog bonds” are traded in the U.K. but issued by a non-U.K.

entity, – “Rembrandt Bonds” are bonds traded in the Netherlands by a

non-Dutch entity,– “Matador Bonds” are bonds traded in Spain issued by a non-

Spanish entity.

71

Global Equity Markets

The 10 biggest stock markets in the world

by domestic market capitalization in 2006

(USD bn)

1 NYSE Group 15,421.2

2 Tokyo Stock Exchange 4,614.1

3 Nasdaq Stock Market 3,865.0

4 London Stock Exchange 3,794.3

5 Euronext 3,708.2

6 Hong Kong Exchanges 1,715.0

7 TSX Group 1,700.7

8 Deutsche Börse 1,637.6

9 BME Spansih Exchanges 1,322.9

10 SWX Swiss Exchange 1,212.3

Source: world-exchanges.org

72

World Stock Exchanges www.world-exchanges.org

– In April 2007 the New York Stock Exchange (NYSE) completed its merger with Euronext, itself formed from the union of the Paris, Amsterdam, Brussels and Lisbon bourses.

– NYSE has also signed alliances with Tokyo and India's National Stock Exchange

Buy, buy, buy May 24th 2007 | NEW YORKFrom The Economist print edition

For your final project, what is the major exchange within the country you aretargeting?

73

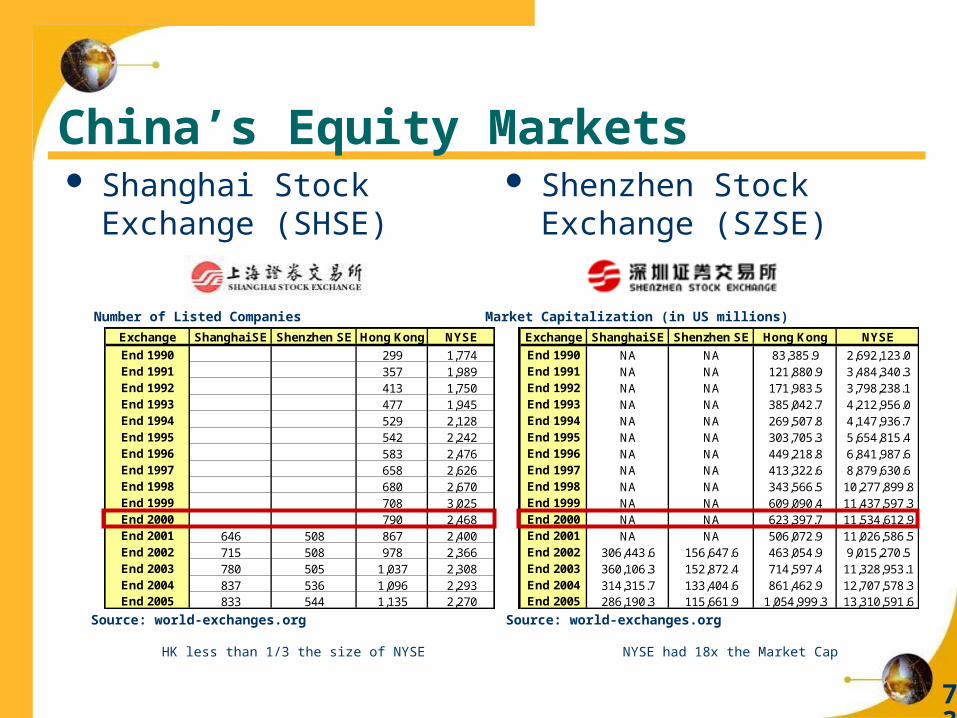

China’s Equity Markets Shanghai Stock

Exchange (SHSE)

Shenzhen Stock Exchange (SZSE)

Exchange Shanghai SE Shenzhen SE Hong Kong NYSE

End 1990 299 1,774End 1991 357 1,989End 1992 413 1,750End 1993 477 1,945End 1994 529 2,128End 1995 542 2,242End 1996 583 2,476End 1997 658 2,626End 1998 680 2,670End 1999 708 3,025End 2000 790 2,468End 2001 646 508 867 2,400End 2002 715 508 978 2,366End 2003 780 505 1,037 2,308End 2004 837 536 1,096 2,293End 2005 833 544 1,135 2,270

Number of Listed Companies

Source: world-exchanges.org

Exchange Shanghai SE Shenzhen SE Hong Kong NYSE

End 1990 NA NA 83,385.9 2,692,123.0End 1991 NA NA 121,880.9 3,484,340.3End 1992 NA NA 171,983.5 3,798,238.1End 1993 NA NA 385,042.7 4,212,956.0End 1994 NA NA 269,507.8 4,147,936.7End 1995 NA NA 303,705.3 5,654,815.4End 1996 NA NA 449,218.8 6,841,987.6End 1997 NA NA 413,322.6 8,879,630.6End 1998 NA NA 343,566.5 10,277,899.8End 1999 NA NA 609,090.4 11,437,597.3End 2000 NA NA 623,397.7 11,534,612.9End 2001 NA NA 506,072.9 11,026,586.5End 2002 306,443.6 156,647.6 463,054.9 9,015,270.5End 2003 360,106.3 152,872.4 714,597.4 11,328,953.1End 2004 314,315.7 133,404.6 861,462.9 12,707,578.3End 2005 286,190.3 115,661.9 1,054,999.3 13,310,591.6

Market Capitalization (in US millions)

Source: world-exchanges.org

HK less than 1/3 the size of NYSE NYSE had 18x the Market Cap

74

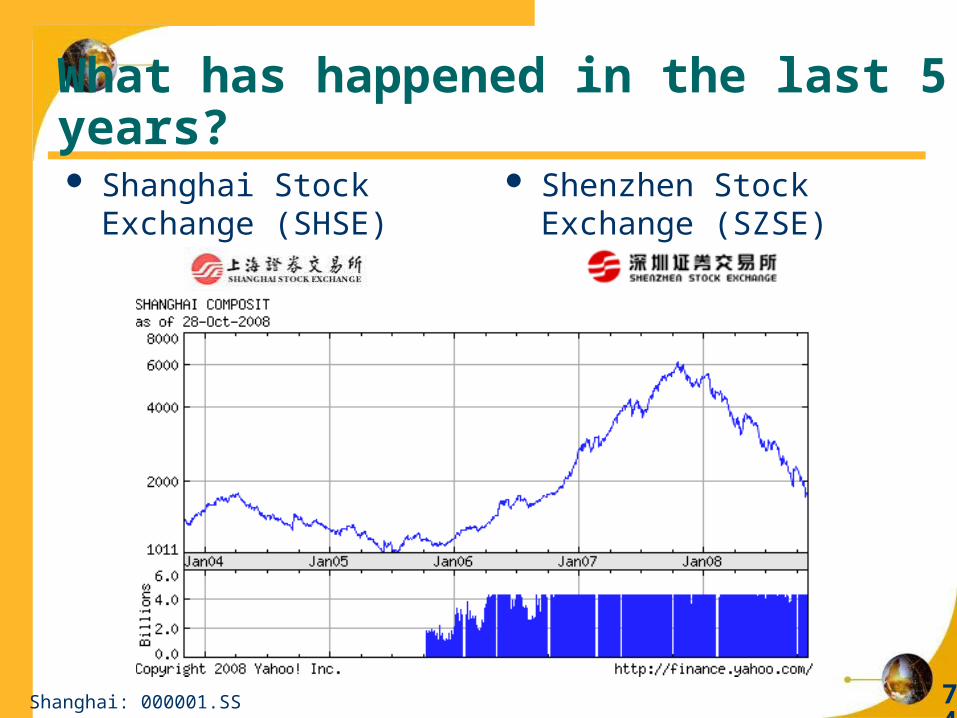

What has happened in the last 5 years? Shanghai Stock

Exchange (SHSE)

Shenzhen Stock Exchange (SZSE)

Shanghai: 000001.SS

75

Sourcing Equity Globally Designing a Strategy to Source Equity Globally

American depository receipts (ADRs) are certificates traded in the United States and denominated in US dollars.

– ADRs are sold, registered, and transferred in the US in the same manner as any share of stock with each ADR representing some multiple of the underlying foreign share (allowing for ADR pricing to resemble conventional US share pricing between $20 and $50 per share).

For your final project, are there any ADRs listed in the U.S. from your target country?see www.adr.com

76

ADRs Levels Level I

– OTC only

Level II– Listed on a U.S. stock exchange.

New York Stock Exchange (NYSE), NASDAQ, and the American Stock Exchange (AMEX).

Level III– Firm can also raise money

77

Popular ADRs

Bank of New York: www.adrbny.comJP Morgan: www.adr.com

Novartis – Biotech SwedenHSBC – Banking UKNestle – SwitzerlandLan.com – Airline ChileEricsson – Telecom Switzerland Vodafone – Telecom UKWipro – IT IndiaNokia – Telecom FinlandElan – Biotech Ireland

78

Implications for Managers Global Market Opportunities Currency Management

– Forecasting & Hedging Activities– Strategic Flexibility

Dispersed Production Outsourcing

Image Source: http://1stattorneys.com/worldmoney2.jpg

79

“International finance is the art of passing currency from hand to hand until it disappears”

Anonymous Author

80

Who is this guy?

81

Nobel Peace Prize 2006: Microfinance Dr. Muhammad Yunus

Lecture by

Wendy M. Jeffus

82

Dr. Muhammad Yunus Won the Nobel Peace Prize in 2006

– Established the Grameen Bank in Bangladesh in 1976 (with $27).

Microfinance – also called "banking for the poor" means providing poor families with very small loans (i.e. to buy cows, chickens or a cell phone) to help them start and grow businesses.

– The loans are typically less than 200 US dollars. – No collateral is needed and repayment is based on an

honor system.– Anyone can qualify for a loan - the average is about

$200 - but recipients are put in groups of 5. Once 2 members of the group have borrowed money, the other 3 must wait for the funds to be repaid before they get a loan.

– This helps people emerge from poverty and encourages sustainable peace.

Thirty years later, the bank has 6.6 million borrowers, of which 97% are women.

http://news.bbc.co.uk/1/hi/world/europe/6047020.stmhttp://www.un.org/apps/news/story.asp?NewsID=20649&Cr=nobel&Cr1=prizehttp://www.npr.org/templates/story/story.php?storyId=6262679

83

The “Eureka Moment” Dr. Yunus was chatting to a shy woman weaving

bamboo stools in 1974.– Sufia Begum was a 21-year-old mother of 3.

Dr. Yunus asked her how much she earned. – She replied that she had borrowed about five taka (nine cents)

from a middleman for the bamboo for each stool.– She earned only 2 cents on each stool.

Dr. Yunus said “I thought to myself, my God, for five takas she has become a slave…. I couldn’t understand how she could be so poor when she was making such beautiful things.”

84

856 taka (about 27 dollars) The following day, Dr. Yunus and his students did a

survey in the woman’s village, Jobra, and discovered that 43 of the villagers owed a total of 856 taka (about $27).

Dr. Yunus said “I couldn’t take it anymore. I put the $27 out there and told them they could liberate themselves, and pay [me] back whenever they could.”

– The idea was to buy their own materials and cut out the middleman.

– They all paid him back, day by day, over a year, and his spur-of-the-moment generosity grew into a full-fledged business concept that came to fruition with the founding of Grameen Bank in 1983.

http://www.msnbc.msn.com/id/15246216/

85

Microcredit Worldwide, microcredit financing is estimated to have

helped 92 million families in 2006 alone.– Today, the bank is a model of micro-financing has inspired

similar efforts around the world.– The success has allowed Grameen Bank to expand its credit to

include housing loans, financing for irrigation and fisheries as well as traditional savings accounts.

Ole Danbolt Mjoes, chairman of the Nobel committee that awarded the prize, said “We are saying microcredit is an important contribution that cannot fix everything, but is a big help.”

86

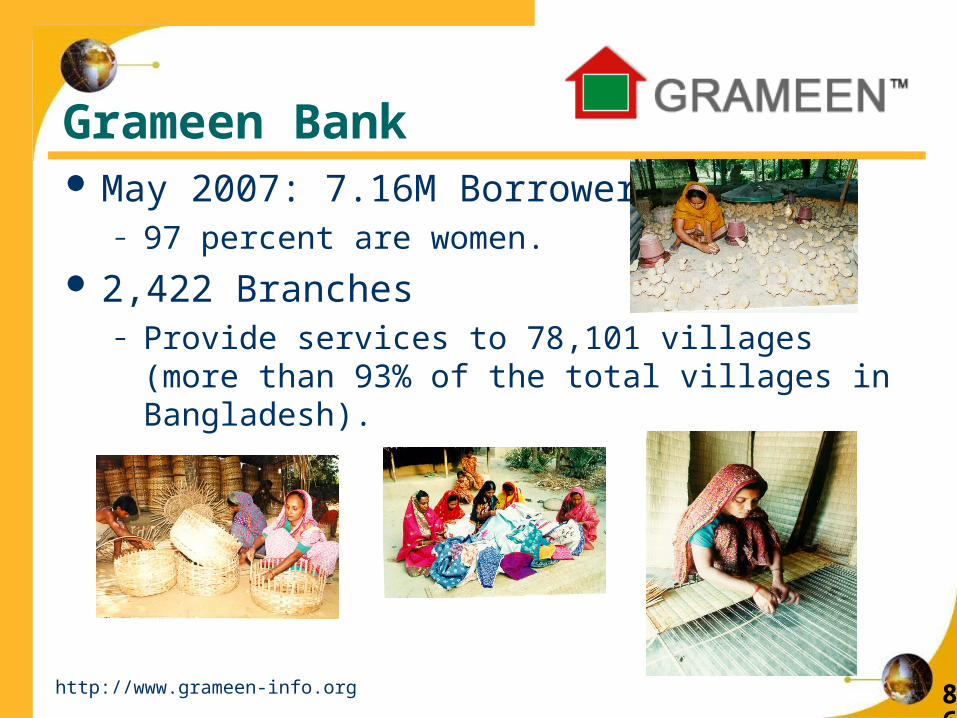

Grameen Bank May 2007: 7.16M Borrowers.

– 97 percent are women.

2,422 Branches– Provide services to 78,101 villages (more than 93% of

the total villages in Bangladesh).

http://www.grameen-info.org

87

88

89

Additional Resources www.kiva.org

90

Next Week: Great Globalization Debate!

http://cinie.files.wordpress.com/2009/02/negotiation1.jpg

91

Is Globalization A Good Thing? The Great Globalization Debate

– Bring Your Cameras!

Remember: NEXT MONDAY!!!

http://www.youtube.com/watch?v=jS7O9RhNa18