1 with eu contribution “arrangements and procedures on the sales of financial products: good...

TRANSCRIPT

1

With EU contribution

““Arrangements and procedures on the sales of financial products: Arrangements and procedures on the sales of financial products: Good practices (to follow) and Poor practices (to avoid) to strengthen Good practices (to follow) and Poor practices (to avoid) to strengthen social dialogue and industrial relations at European and company social dialogue and industrial relations at European and company level”level” VS/2010/0737VS/2010/0737

M.i.F.I.D. step by stepM.i.F.I.D. step by step … …

When the rules run up………. When the rules run up……….

Domenico Iodice – APF Research DepartmentDomenico Iodice – APF Research Department

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

2

The object of the analysisThe launch of the MiFID Directive 2004/39/EC (Market in Financial Instruments Directive) and Council of the European Parliament is the first level on the principles ……….

The second level (implementation measures: Directive 2006/73/EC, known as MiFID 2) defines the organizational requirements of investment firms and the mode of carrying out investment services and activities. The Regulation 1287/2006 rounds, regulating trading operations, trading and market transparency, admission of financial instruments to trading.

Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

3

The principles behind the system MiFIDMaximum harmonization: Member States may not introduce any additional requirements for investment firms. It is therefore defined an effective level playing field that facilitates cross-border competition.(DE) Regulation principles: the rules set out the objectives that firms are obliged to pursue, leaving wide discretion on how to do it. The institutional framework thus promotes process innovation and competition costs. Supervision of the country of origin on businesses that provide services in other EU countries.Abandonment of the principle of concentration of trading on regulated markets. Trading venues are put in competition with each other to help reduce costs.

Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

4

The trading venues in MiFID Regulated Marketmultilateral system operated and / or managed by a market operator, which brings together or facilitates the bringing together - in the system and according to its non-discretionary rules - of multiple purchase and sale of third parties relating to financial instruments, so that results in contracts relating to financial instruments admitted to trading under its rules and / or its systems

MTFmultilateral system, operated by an investment firm or a market operator which brings together - in the system and based on non-discretionary rules - in the interests of multiple third party buying and selling financial instruments, so results in a contract (eg EuroTLX Unicredit)

systematic internaliser

investment firm in an organized, frequent and systematic basis, deals on own account by executing client orders outside a regulated market or an MTF (eg, DB)

In financial markets have become much more complex than investors are likely to get lost. As a result of MiFID competition on the continent is 6846 shares listed on regulated markets open among 92 (the old stock markets), 65 MTFs and 11 systematic internalisers (intermediaries that perform their own customer orders).

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

5

Taxonomy of customer protectionMiFID requires investment firms to make a classification of its customers in order to modulate the disclosure requirements and

protections. There are therefore three categories of customers:Retail customer (or retail), defined as "contrary to" or as a professional client or eligible counterparty.Professional client is "a customer who possesses the experience, knowledge and expertise to make their own investment decisions and properly assess the risks involved" (All.2). Category to which belong the subjects of law referred to in the following slides.Counterparty qualified: it requires excellent knowledge of financial markets and products, and therefore a guarantee waiver of the rules of conduct MiFID. These investment firms, credit institutions and insurance companies, pension funds, central banks and international institutions. The list is not exhaustive: it can be completed by each state. Access to this category is not automatic, but the customer must confirm that you want to be treated as an eligible counterparty.Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

6

Retail customersThe MiFID requires the highest level of protection. Is required to verify the adequacy and affordability of financial products required or proposed. The company must ensure the competence of the customer in relation to the products and services, but also keep in mind the financial situation and his investment objectives. Apply all the rules of protection, information and transparency.Investment firms operating this classification now seen thanks to the information collected and to the objective characteristics of the customers.Customers are informed of the classification and assignment to a specific category

Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

7

MiFID: the sufficient information required

The classification of customers is, first, functional identification of the disclosure requirements to play. First there are the disclosure requirements in respect of all categories of customers and include:

the assigned classification;any conflicts of interest;fees paid to third parties;the description of the financial instruments;the execution policy;loss information.

.In addition, brokers must inform the retail customer about policies and measures for its protection, its assessment of the instruments of the client's portfolio and the costs of services provided. Whatever the category, the customer is entitled to sufficient information to make investment choices aware: honest, clear and not misleading.

Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

8

The adequacy and appropriateness testMiFID does not just include the disclosure requirements, but introduces mandatory tests. It was graded level of investor protection depending on the type of service provided.The test of adequacy of the service should be undertaken when the service financial advisory and portfolio management. The intermediary must ensure that the advice given is consistent with the investment objectives of the client to whom it is addressed and that is adequate to its capital resources. The intermediary must collect all the information necessary to understand where the skills and experience of the customer are also suitable for a correct assessment of the given advice.The test of appropriateness is expected for all other investment services. If you pay that other investment services (trading, placement of asset management products, etc..). In this case, the criteria are the information and experiences which the customer has with respect to the specific financial product and the general level of "financial literacy" possessed. This term indicates the assessment that the client has the experience and knowledge necessary to understand the risks are being evaluated.

Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

9

Evaluation of adequacyInterested category : retail clients and professionalThe operator must be sure that the client understands the nature of the transaction and the risks that are connected to it, without any kind of misunderstandings that occur.The operator has the obligation to obtain all the information necessary for the evaluation of skills and experience in the field of customer's investment. It is also necessary to know its financial position and its investment objectives in order to offer services or financial instruments cheaper in relation to his profile. In the event the customer fails to provide such information or would provide a partial, not to warn the operator must be able to determine whether the product or service in question is suitable for him.If the assessment of adequacy is negative, this would prevent the continuation of operations, because, if the operation is not adequate to the customer profile, the investment firm can not provide during the operation.The prosecution is not absolute, and any attempt to revisit the responses to the tests is a serious violation of the rule.

Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

10

Assessment of appropriatenessInterested category : retail and professional clients on requestThe operator will ask the client about his knowledge and experience on investment in relation to the product or service offered or required, to assess whether the product or service is convenient for him. He must warn, in relation to the information gathered, if the product or service in question is or is not appropriate for him.

In the event that the customer does not provide such information or suitability of the test is negative, contrary to what happens here for the "adequacy", the operation can be done, but only after the customer, informed of the "inappropriateness "operation, has signed a special “mall” document prepared by the firm.

Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

11

A special case of exonerationA special case is the way "execution only" in which you are required to perform the test of appropriateness and there are no disclosure requirements, if not at the customer's access to this mode. The execution only cover only non-complex financial instruments and must be specifically requested by the customer. If this occurs, the investment firm is obliged to point out that it will perform the test of appropriateness. Purpose: To reduce the time and cut costs.

The service is at the initiative of the client or potential client (not at the suggestion of the operator); it relates to shares admitted to trading on a regulated market or money market instruments, bonds or other debt securities, mutual funds

Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

12

In summary….

Only negotiation: the test of appropriateness is not required.Other investment: the test of appropriateness is necessary.Advice and portfolio management: the test of adequacy is necessary.

Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

13

The Advisory ServiceThe inclusion of the service of "investment advice" among the primary services of investment, is one of the main changes introduced by MiFID legislation, thus assuming the role of the advisory investment service.

In light of the changes introduced by the Directive first and second level of European origin, the Italian legislature (Legislative Decree no. 164/2007) has introduced art. TUF 1 of a 5-paragraph f as follows: “The investment advice is the provision of personal recommendations to a client, either upon request or at the initiative of the service, with respect to one or more transactions relating to a particular financial instrument.The recommendation is individual, when presented as suitable for the client or is based on the consideration of the characteristics of the client. A recommendation is not customized if it is disclosed to the public through distribution channels. "

Step ONE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

Step TWO

MiFID, Compliance e Codes of MiFID, Compliance e Codes of ethicsethics

The “MiFID Compliant” system

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

1515

ComplianceCompliance In each investment firm is established as a function of compliance (monitoring compliance with the obligations of fairness and transparency).This function must be independent, have adequate resources and facilities and must have access to all activities of the intermediary. Compliance is also involved in specifying the tasks of different stakeholders, to ensure the adequacy of internal communications and to retain records of their activities.The strengthening of the internal control system operates by introducing new levels of control and a more articulated set of rules.

Step TWO

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

16

The term regulatory compliance means compliance with certain standards, rules or standard indicates compliance with specific instructions given by the legislature, by official agencies, certification bodies and internal regulations of the companies themselves. In the bank's compliance function has the task of ensuring that "the procedures are consistent with the objective of preventing the violation of rules of eteroregolamentazione (laws and regulations) and self-regulation (codes of conduct, code of ethics)“

The order to avoid the risk of "incurring sanctions, financial loss or reputational damage as a result of violations of legislative, regulatory or self-regulation…" ..

Step TWO

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

17

Operational riskThe risk of losses….resulting from failures in processes, people and systems. This definition includes legal risk, but not the one and reputation. "

The main types of operational risk are:internal or external fraud;employment and safety – - (Eg: Claims by employees, violations of rules protecting the health and safety, trade union activity, discriminatory practices, civil liability);practices connected with customers, products and activities (eg, breach of fiduciary relationship, breach of confidential information, improper transactions made on behalf of the bank, money-laundering, sale of unauthorized products);damage to physical assets and shortcomings and failures of a technical nature;

Step TWO

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

18

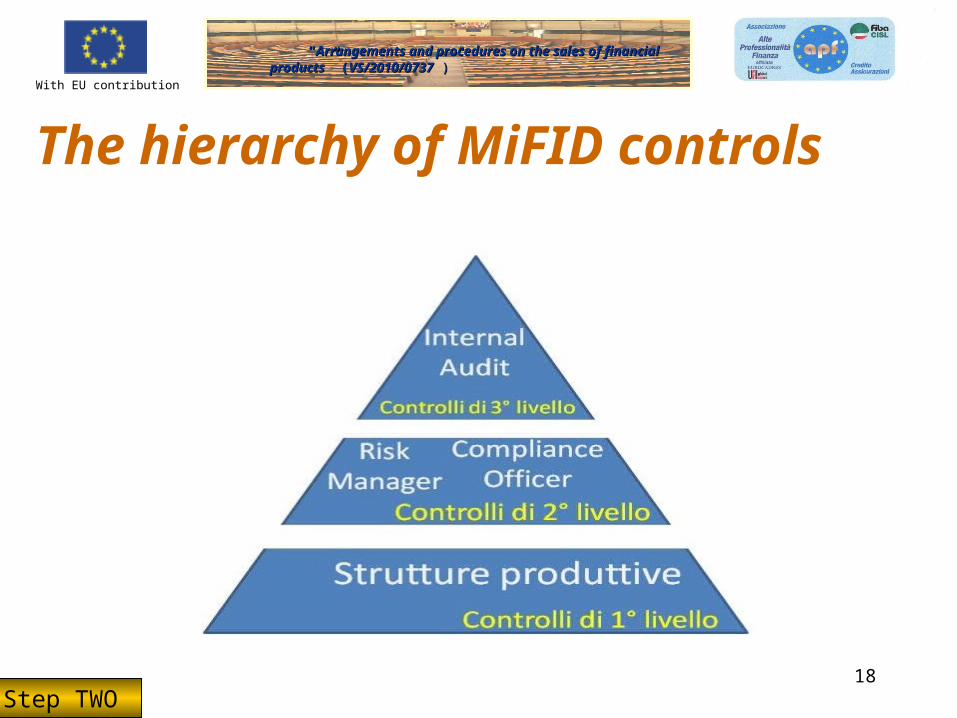

The hierarchy of MiFID controls

Step TWO

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

19

Each other's skills have now been clarified to avoid duplication:

The Compliance assesses the risk of non-compliance practicesto the protecting the customers in terms of servicesFinancial instruments (MiFID) and establishes the appropriate corrective action.The Internal Audit verifies the accuracy of company operations evaluating organizational effectiveness (powers, procedures, controls) and the associated financial risk, take disciplinary action against employees.

They require strong operational synergies (the "Service Agreement")

Step TWO

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

20

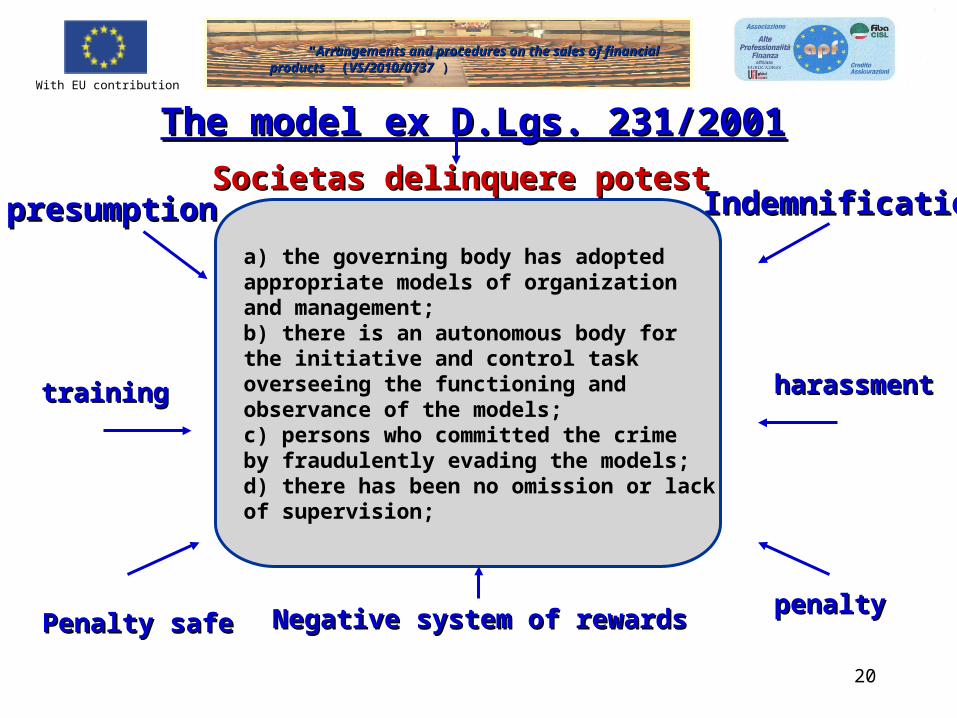

The model ex D.Lgs. 231/2001The model ex D.Lgs. 231/2001

trainingtraining

presumptionpresumption

Penalty safePenalty safe

IndemnificationIndemnification

Negative system of rewardsNegative system of rewards penaltypenalty

a) the governing body has adopted appropriate models of organization and management;b) there is an autonomous body for the initiative and control taskoverseeing the functioning and observance of the models; c) persons who committed the crime by fraudulently evading the models;d) there has been no omission or lack of supervision;

harassmentharassment

Societas delinquere potestSocietas delinquere potest

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

21

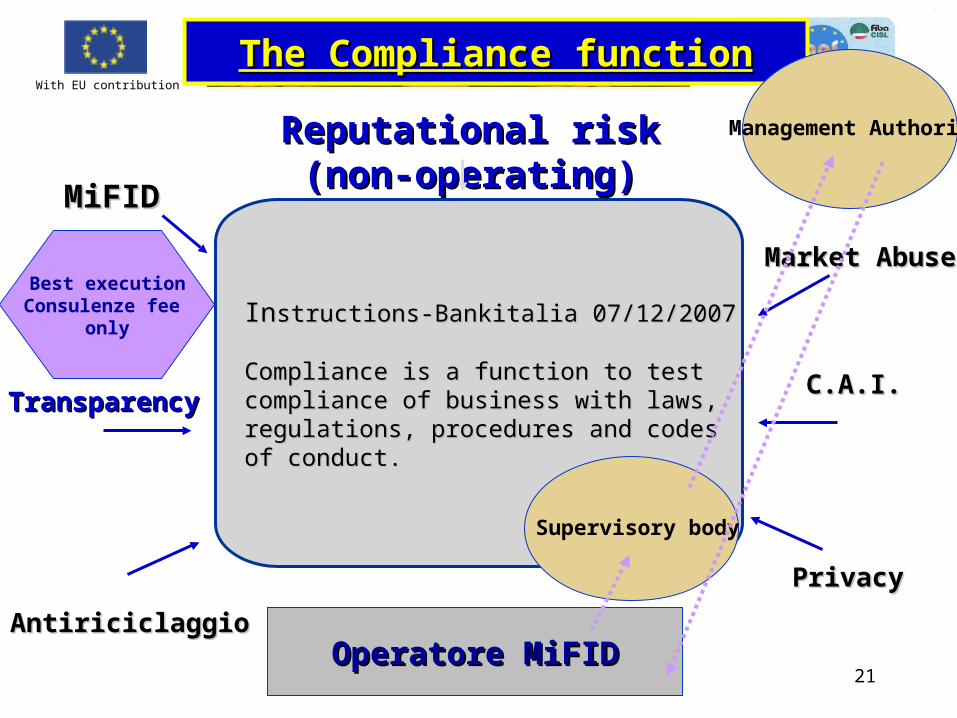

The Compliance functionThe Compliance function

TransparencyTransparency

MiFIDMiFID

Antiriciclaggio Antiriciclaggio

Market AbuseMarket Abuse

PrivacyPrivacy

InInstructions-Bankitalia 07/12/2007structions-Bankitalia 07/12/2007

Compliance is a function to test Compliance is a function to test compliance of business with laws, compliance of business with laws, regulations, procedures and codes regulations, procedures and codes of conduct.of conduct.

C.A.I.C.A.I.

Reputational riskReputational risk(non-operating)(non-operating)

Best executionConsulenze fee

only

Supervisory body

Management Authority

Operatore MiFIDOperatore MiFID

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

22

In implementation of Directive 2010/76/UE the Bank of Italy issued the "Provisions on remuneration policies and practices and incentives in banks and banking groups“

(Order dated March 31, 2011).The provisions of the Bank of Italy not only introduce the guidelines in principle, but implementation provisions, direct to the banks and then immediately binding.

Step TWO

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

23

The specific provisions of section 4.2, including the control functions, the duty of the Compliance Department of involvement in the process of definition of remuneration policies;is expressed in a case "on the compliance of the remuneration policies to the regulatory framework."the exercise of the function is mandatory and not discretionary; such control is preventive, that integrates the process of formation of the company, validating, not only the laws but also statutes, codes of ethics and / or conduct standards.

In practice, the system of exemption from liability of directors of banks, based on the Decree. 231/2001, applies only if the compliance function validates the incentive mechanisms.

Step TWO

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

The magma of MiF 2:The magma of MiF 2: financial crisis and regulatory financial crisis and regulatory

remediesremedies

Step THREE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

25

Optimism about the functioning of markets, capable of self-regulation, is the postulate of MiFID.The EU model of governance gives emphasis to the "shareholder value". It failed the objective of risk control and promotion of sustainable development in the long term.The EU company law, in particular based on "soft law" in the regulation of corporate governance, on the assumption that models other than Anglo-Americans are bad, because limiting the internal market.

This philosophy has been refuted by the facts

with the current global financial crisis, the context in which the MiFID 1 is based, collapsed.Step THREE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

26

The emergency plan (late)Recently (December 8, 2010), the European Commission Internal Market and Financial Services has launched a consultation, presenting its proposals for revision of MiFID, three years after its entry into force.

Proposals for legislative revision was expected in the first half of 2011.

The plan is divided into several points, in response to various critical

Step THREE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

27

Objectives of the reform in general

The goal is to make the Directive in step with technological advances, is adequate to cope with events like the financial crisis."The main purpose of the proposal is to ensure that all exchanges are regulated and are completely transparent," it said in the draft revision.

Step THREE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

28

Two parts, one goal

The reform of the MiFID is divided into two parts: the first concerns the structure of the market, while the second focuses on issues related to transparency.Many of the new rules will force banks to make important changes to their business practices.

Step THREE

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

29

MiF 2: Is this the expected revolution?MiF 2: Is this the expected revolution?

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

30

Phases and time of the reviewThe European Commission - Dec. 8 - has launched a consultation on the review of MiFID (2004/39/EC). The revision is necessary as a result of a rapid technological change and regulatory limits emerged after the crisis.

The aim of the consultation is to receive, by February 2, 2011, comments and suggestions from all stakeholders, to enable you to shape the Commission's legislative proposals.

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

31

Consultation: 4 key areasFirst, we consider the changes in structures and market practices. Given the complexity of financial markets (for selling arrangements, actors and products available), the Commission proposes to update the MiFID and provide a robust framework for regulating all financial services and products, in such a way to eliminate the activities not currently covered by the Directive.Secondly, the consultation concerns the transparency of markets, in order to ensure equal access to information by all participants. It is, therefore, to extend the rules of transparency, which currently do not cover certain products (such as OTC derivatives).Third, we consider the issue of supervision. Specifically, we ask what are the necessary changes in the perspective to best use the new system of supervision and the new European Authority (ESMA, active since January 2011).Finally, for the protection of investors, the consultation must be read in close connection with the initiatives on Corporate Governance and retail financial products.

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

32

From the draft of 18.8 to the official

The publication of the reform of MiFID by the European Commission took place October 20, 2011.However, the European Parliament and Member States in particular will have the last say in a fierce bargaining and is expected ... from YESTERDAY!

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

33

Stop speculatingBrussels, with the new revision to the Directive MiFID wanted to put a brake on the uncontrolled market, which also covers sovereign debt. Especially with the new crunch the EU Commission is trying to stem the perverse effects of fast and uncontrolled trading, such as those allowed by new technologies.

Electronic trading technology has reached such levels of sophistication to threaten global financial stability. Companies using these systems will be subject to stricter controls. Investment companies must abide by strict rules and management must possess the appropriate knowledge.

Strict control over derivative transactions, with the possibility of introducing limits, constraints more transparent, automatic actions on transactions by electronic (high frequency trading), systems of sanctions.

Special attention, with a stronger role entrusted to the regulatory authorities, will be dedicated to the commodity derivatives markets, where speculation can have uncontrolled socio-economic handicaps.Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

34

Statements of Michel Barnier

The European Commissioner Michel Barnier told the Financial Internal Market and Services, he wants to "put the real economy," the financial system,'We must restore morality when it is gone'‘, after the scandals of "bonuses" to managers and irresponsible assumption of excessive risks, then paid by government. "it’s the time that markets work for the real economy and not the other way."The package is a review of two EU directives, which deal with market abuse (Mad) and the Markets in Financial Instruments (MiFID), such as derivatives, which operate outside the stock market sector. For these financial instruments will be introduced a new "platform" under the control of the supervisory authorities, in particular as regards the formation of prices. There will, however, some exceptions for certain specific categories of transactions.Special attention, with a stronger role entrusted to the regulatory authorities, will be dedicated to the commodity derivatives markets, where speculation can have uncontrolled socio-economic handicaps.

Step FOUR

One year after the reform of U.S. financial markets after the crisis of 2008, now up to Europe.Three days after the EU summit on the debt crisis of the euro and the greek ...

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

35

The raid by the EU in criminal lawPut an end to the "kingdom of opacity '" bringing in a supervised 80% of financial transactions that now controls the escape is only possible if we discourage crime. How? with criminal penalties "harmonized.“All States shall ensure that the abuse of privileged information (insider dealing or trading) and handling of the financial market are punished as a criminal offense with prison terms. In addition, it also established the crime of 'attempted market manipulation'.In some countries, including Italy, are already provided for such measures, but there are some, such as Bulgaria, where everything 'permission.

It specifies which trading strategies are prohibited, such as placing orders with no intention to negotiate, but only for the purpose of disrupting the market ('Owl orders').

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

36

Why do we need an overdose of rules?pro-competitive effect of MiFID has been less effective than the U.S. market In fact, while the competition between the new trading platforms has resulted in the provision of services more efficient and innovative, on the other hand the contraction of the volume of trading on each trading platform has reduced the benefits of economies of scale and made less efficient the process of determining the price (price discovery).the situation of information asymmetry, attaching to the exemption from transparency requirements on dark pools, had a negative impact on the process of price formation for financial instruments.MiFID abolished the obligation of concentration of trading on regulated markets by introducing new trading systems and alternative platforms. Consequently, a significant part of the transaction flows no longer met the minimum requirements of transparency, thanks to an exemption granted by the City of London by the UK Financial Services Authority.

Step FOUR

La The British position is passed in the minority, has even isolated in the EU!

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

37

Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL (18/08/2011)

"The financial crisis has highlighted weaknesses in the transparency of financial markets. Increasing the transparency needed to strengthen the financial system. "(this means that the financial crisis we can not leave without common rules of transparency).All negotiations must be conducted in the organized and regulated sites to be completely transparent, both pre and post, in all trading venues and for all financial instruments. The transparency requirements should be calibrated for different types of instruments, including stocks, bonds, and derivatives.In the context of future European supervisory architecture, you need a single rule applicable to all financial institutions operating in the single market (a single market, a single set of financial instruments, a single set of rules).A unique code of transparency should take the form of law directly applicable to all investment firms (regulations rather than directives: Immediately mandatory)The unique code should reduce exemptions. ESMA should evaluate the compatibility of individual requests for uniform application. The competent authorities should then adhere to the evaluation of the ESMA.

“Considerandum”

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

38

What is ESMA?ESMA is an independent European Union contributes to maintain the stability of the financial system of the European Union, ensuring the integrity, transparency, efficiency and smooth functioning of securities markets, as well as improving the protection of investors. In particular, ESMA improves supervisory convergence both among securities regulators, and among financial sectors, working closely with other European supervisory authorities responsible for banking (EBA), and Insurance and Pensions Authority (EIOPA).

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

39

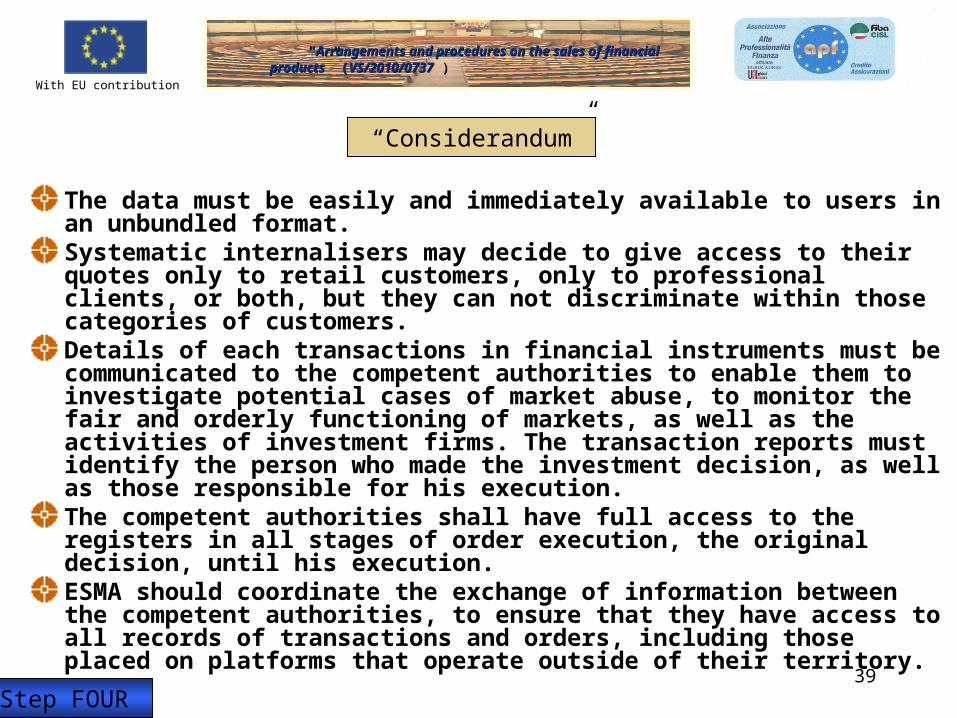

The data must be easily and immediately available to users in an unbundled format.Systematic internalisers may decide to give access to their quotes only to retail customers, only to professional clients, or both, but they can not discriminate within those categories of customers. Details of each transactions in financial instruments must be communicated to the competent authorities to enable them to investigate potential cases of market abuse, to monitor the fair and orderly functioning of markets, as well as the activities of investment firms. The transaction reports must identify the person who made the investment decision, as well as those responsible for his execution.The competent authorities shall have full access to the registers in all stages of order execution, the original decision, until his execution. ESMA should coordinate the exchange of information between the competent authorities, to ensure that they have access to all records of transactions and orders, including those placed on platforms that operate outside of their territory.

“Considerandum”

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

40

"Regulation" establishes uniform requirements for the reporting of trade data to the public, reporting to the competent authorities, authorization and under what conditions.

The regulation applies to investment firms, credit institutions authorized, regulated markets, counterparties.

The “Articulated”

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

41

How the system will work in practiceThe trading platform should ensure that, in exchange, all data are freely accessible within 15 minutes and disseminated in real time at a cost determined by the Commission "reasonable commercial basis". This measure would mark a step forward in price regulation.

The data should be stored for at least five years to allow supervisors to improve the monitoring of any abuses of the market. These data should also include details on the algorithms used, marking another "crack" than the high-frequency computerized trading.

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

42

Operational bondsThe obligations of pre and post-trade, so far limited to exchange of Ets and certificates, will be extended to bonds, structured finance and derivatives and emission certificates traded on regulated platforms.Among other points in the text, the regulation of crossing system, the exchanges that make intermediaries can connect the demand (customers who want to buy a title) with the supply (those who want to sell it); standardization of data on the negotiations and the requirement to use a particular intermediary, the exchange of OTC derivatives allowed only on regulated markets and MTFs or OTC, and the distinction between independent advice (no incentives), and advice "restricted” (which admits the incentives).

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

43

The regime of exceptions (Article 3)

the competent authority shall notify ESMA and other competent authorities of the purpose and the operating mode of each request, with an anticipation of at least 6 months.Within 3 months of receipt of the notification, the ESMA shall render a decision.ESMA monitor the application of exemptions and submit an annual report to the Commission on how they are used in practice.

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

44

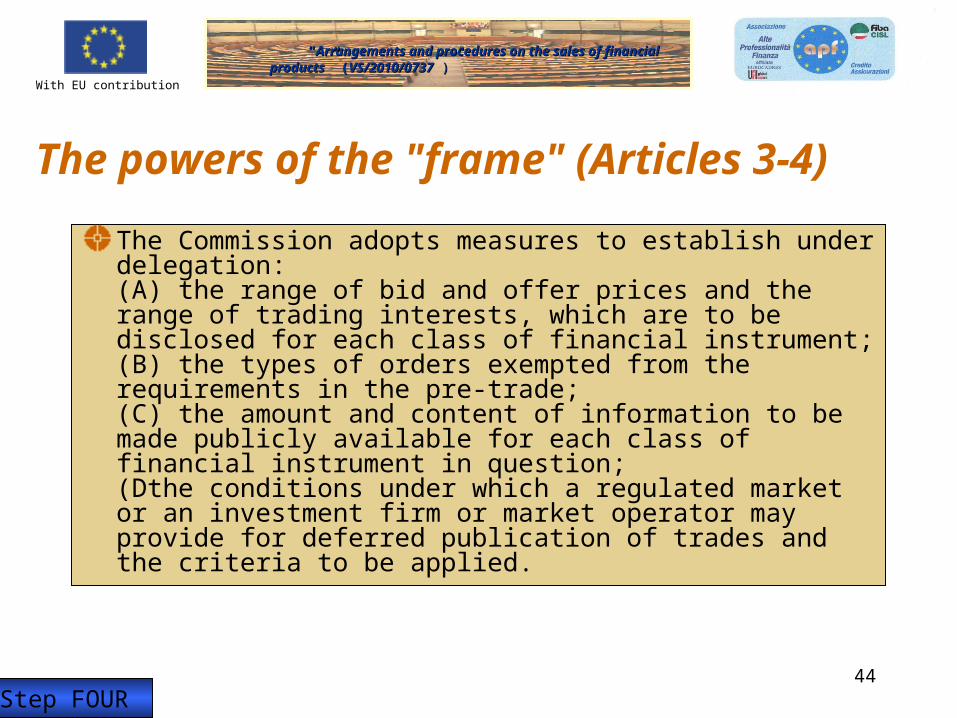

The powers of the "frame" (Articles 3-4)

The Commission adopts measures to establish under delegation:(A) the range of bid and offer prices and the range of trading interests, which are to be disclosed for each class of financial instrument;(B) the types of orders exempted from the requirements in the pre-trade;(C) the amount and content of information to be made publicly available for each class of financial instrument in question;(Dthe conditions under which a regulated market or an investment firm or market operator may provide for deferred publication of trades and the criteria to be applied.

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

45

Substitute powers of temporary intervention (Article 29)

ESMA may temporarily prohibit or restrict within the Union:(A) marketing, distribution or sale of certain financial instruments, or(B) a type of financial activity.ESMA takes a decision if all the following conditions are satisfied:(A) the proposed action faces a threat to the regular functioning and integrity of financial markets or the stability of the financial system of the Union;(B) Community standards applicable to financial instrument or activity does not provide sufficient answers to the threat;(C) the Authority or the competent Authorities have not taken measures to address the threat or the actions that were taken are not adequate.When ESMA takes an action it verifies that:(A) it does not have a negative effect on the efficiency of financial markets and investors, or at least this negative effect is not disproportionate to the benefits of action, and(B) it does not create a risk of regulatory arbitrage.

Regulatory arbitrage is defined as all the transactions through which banks increase progressively risky credit exposures characterized by a capital less than the actual absorption of capital as measured by their internal models-eg-securitizations.

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

46

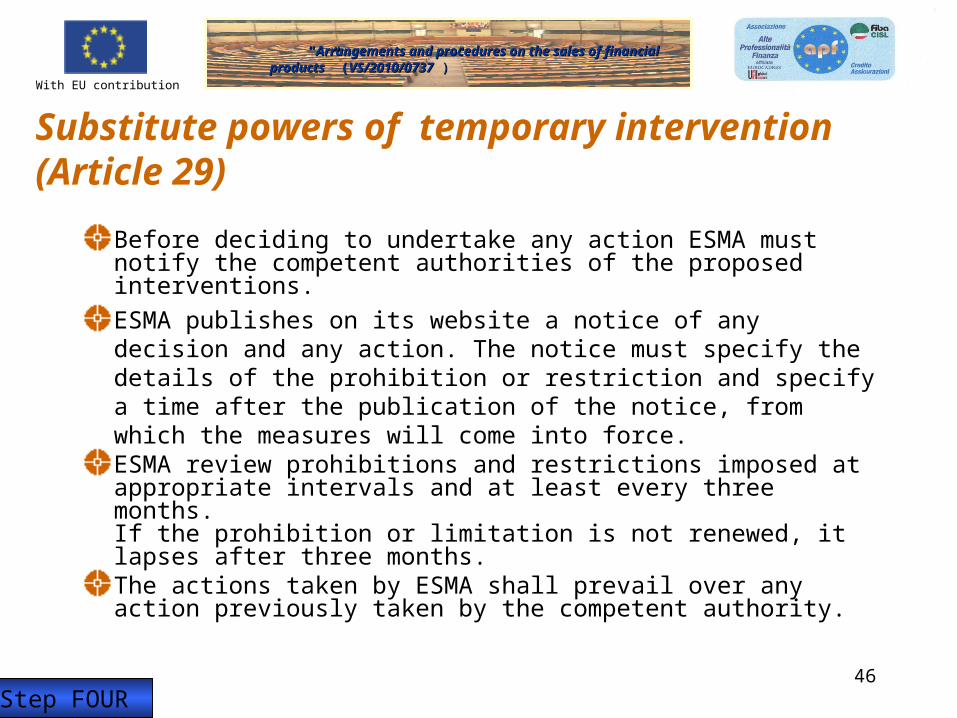

Before deciding to undertake any action ESMA must notify the competent authorities of the proposed interventions.ESMA publishes on its website a notice of any decision and any action. The notice must specify the details of the prohibition or restriction and specify a time after the publication of the notice, from which the measures will come into force.ESMA review prohibitions and restrictions imposed at appropriate intervals and at least every three months.If the prohibition or limitation is not renewed, it lapses after three months.The actions taken by ESMA shall prevail over any action previously taken by the competent authority.

Substitute powers of temporary intervention (Article 29)

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

47

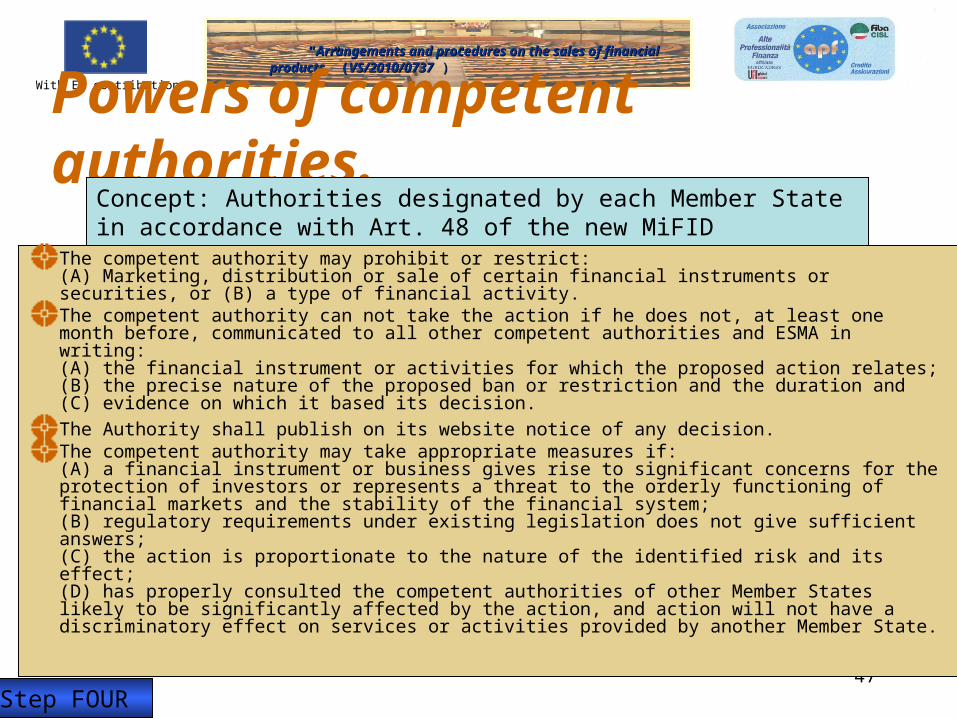

Powers of competent authorities.

The competent authority may prohibit or restrict:(A) Marketing, distribution or sale of certain financial instruments or securities, or (B) a type of financial activity.The competent authority can not take the action if he does not, at least one month before, communicated to all other competent authorities and ESMA in writing:(A) the financial instrument or activities for which the proposed action relates;(B) the precise nature of the proposed ban or restriction and the duration and(C) evidence on which it based its decision.The Authority shall publish on its website notice of any decision.The competent authority may take appropriate measures if:(A) a financial instrument or business gives rise to significant concerns for the protection of investors or represents a threat to the orderly functioning of financial markets and the stability of the financial system;(B) regulatory requirements under existing legislation does not give sufficient answers;(C) the action is proportionate to the nature of the identified risk and its effect;(D) has properly consulted the competent authorities of other Member States likely to be significantly affected by the action, and action will not have a discriminatory effect on services or activities provided by another Member State.

Concept: Authorities designated by each Member State in accordance with Art. 48 of the new MiFID

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

48

Coordination by ESMA (Art. 31)

After receiving the notification referred to in Article 30 of every action that should be imposed under that Article, ESMA adopt an opinion if it considers that the prohibition or limitation is justified and proportionate.If ESMA considers that the assumption of a measure by other competent authorities is required to manage the risk, it shall also state that in the opinion. The Opinion is available on the website of ESMA.If a competent authority intends to take, or takes any action contrary to an opinion of ESMA (under paragraph 2) or refuses to take any action contrary to the ESMA (an opinion under this paragraph) the Commission shall promptly publish in the its website a notice explaining fully its reasons for doing so

Step FOUR

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

49

Act directly on speculation in work on sovereign debt (effect of global markets).Message of the Commission to credit rating agencies: Brussels in November will propose to suspend the rating of the countries under the program and to reduce dependence on assessments of the 'Big Three' (Standard & Poor's, Moody's and Fitch).

Step FOUR

What can not do MiF 2 and what does not

With EU contribution

““Arrangements and procedures on the sales of Arrangements and procedures on the sales of financial productsfinancial products” (” (VS/2010/0737VS/2010/0737 )”)”

50

MiFID ... waiting for the next stepThese proposals, to take effect, shall be approved by Parliament and the Council of Ministers.Compared with MIF 1 adopted before the 2008 crisis, the balance of political forces in power has changed. The United Kingdom, the traditional ally of the big banks, has lost influence, as evidenced by its outvoted in the debate on derivatives.It promises to be a long negotiation: between the proposal from the Commission and the entry into force of MIF1, spent two years and a half .The urgency of market regulation may allow,this time, to pick up the pace ...We HOPE SO!

Step FOUR