100022 - exstatic.zbgedu.com

TRANSCRIPT

Hot line: 400-699-1716

Q & A E-mail: [email protected]

Complaint E-mail: [email protected]

ACCA connect: http://www.accaglobal.com/contancts/connect/

Address: 北京市朝阳区广渠路金泰国际大厦 C 座(100022)

ACCA 官方电话:+44 (0)141 582 2000

ACCA- FR 2021-2022 Content

CONTENT

FR Introduction ........................................................................................................................................... 3

1. Aim of paper ............................................................................................................................................ 3

2. Main capabilities ...................................................................................................................................... 3

3. The syllabus .............................................................................................................................................. 4

4. Exam format ............................................................................................................................................. 4

5. Linking to other papers ............................................................................................................................ 5

6. Examinable documents Sep 2021 to Jun 2022 ........................................................................................ 5

Part A FRAMEWORK ....................................................................................................................................... 7

Chapter 1 IASB Framework .................................................................................................................................. 7

1. The IASB conceptual framework for financial reporting .......................................................................... 7

2. Regulatory framework ........................................................................................................................... 11

3. Not-for-profit and public sector entities ................................................................................................ 13

Part B IFRS STANDARDS (ACCOUNTING STANDARDS) ..................................................................................... 15

Chapter 2 IAS1 Presentation of Financial Statements ....................................................................................... 15

1. A complete set of financial statements comprises ................................................................................ 15

2. Single entity financial statements .......................................................................................................... 15

3. Illustration of group financial statements .............................................................................................. 18

Chapter 3 Non-Current Assets ........................................................................................................................... 21

1. IAS 16 Property, plant and equipment ................................................................................................... 22

2. IAS 40 Investment property ................................................................................................................... 27

3. IAS 38 Intangible assets ......................................................................................................................... 28

4. IAS 36 Impairment of assets .................................................................................................................. 32

5. IAS 23 Borrowing costs .......................................................................................................................... 35

6. IAS 20 Government grants ..................................................................................................................... 36

7. IFRS 5 Non-current assets held for sale and discontinued operations .................................................. 38

Chapter 4 Revenue............................................................................................................................................. 43

1. IFRS15 Revenue from contracts with customers ................................................................................... 43

2. IFRS15 Part construction contracts ........................................................................................................ 47

Chapter 5 Other Standards ................................................................................................................................ 52

1. IAS 8 Accounting policies, changes in accounting estimates and errors ................................................ 52

2. IAS 2 Inventories .................................................................................................................................... 54

3. IAS 41 Agriculture .................................................................................................................................. 56

4. IFRS 13 Fair value measurement ............................................................................................................ 58

Chapter 6 Financial Instruments ........................................................................................................................ 59

1. Need for IFRS Standards ........................................................................................................................ 59

2. IAS 32 Financial instruments: Presentation ........................................................................................... 59

3. IFRS 9 Financial instruments .................................................................................................................. 60

Chapter 7 Leases ................................................................................................................................................ 67

1. Objective of IFRS 16 leases .................................................................................................................... 67

2. Accounting by lessee.............................................................................................................................. 67

3. Accounting treatment ............................................................................................................................ 69

1

ACCA- FR 2021-2022 Content

Chapter 8 Taxation ............................................................................................................................................. 72

1. IAS 12 Income tax................................................................................................................................... 72

2. Current tax ............................................................................................................................................. 72

3. Deferred tax ........................................................................................................................................... 72

Chapter 9 Foreign Currency Transactions and Entities ...................................................................................... 78

1. Why adjustments for foreign currency transactions are necessary ....................................................... 78

2. Functional and presentation currency ................................................................................................... 78

3. Accounting for individual transactions designated in a foreign currency .............................................. 78

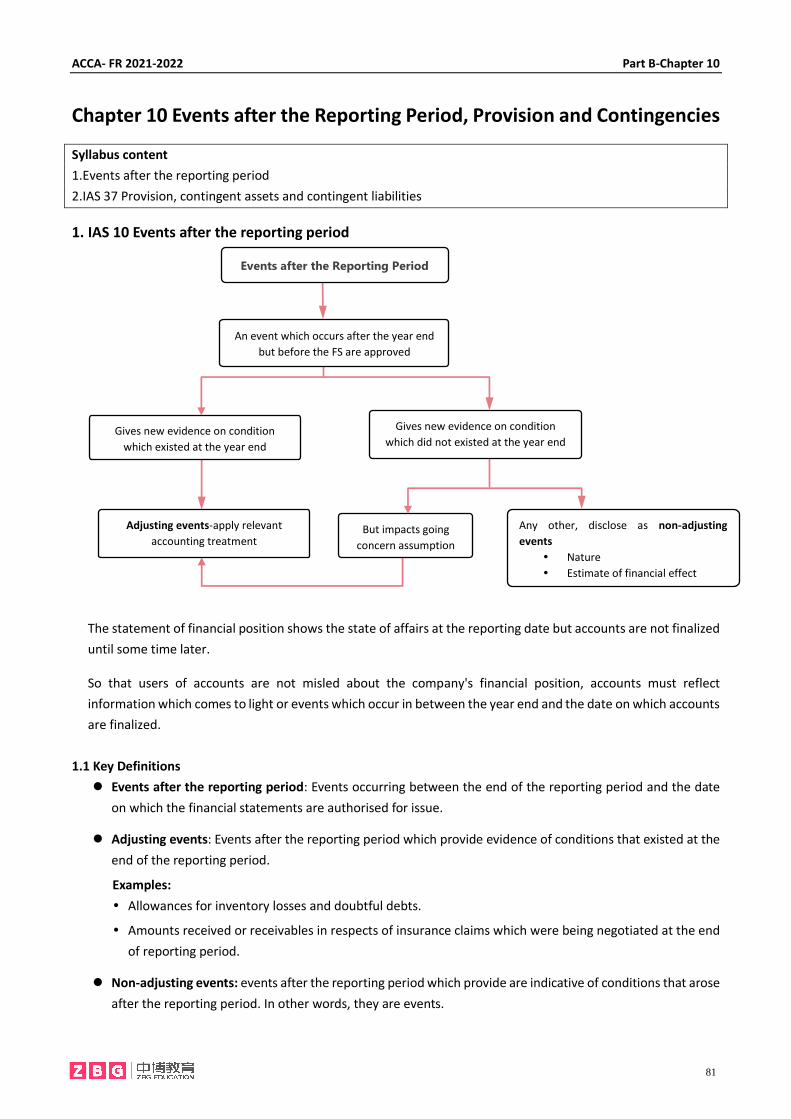

Chapter 10 Events after the Reporting Period, Provision and Contingencies .................................................... 81

1. IAS 10 Events after the reporting period ............................................................................................... 81

2. IAS 37 Provision, contingent assets and contingent liabilities ............................................................... 83

Chapter 11 Earning per Share ............................................................................................................................ 90

1. Introduction ........................................................................................................................................... 90

2. Basic EPS ................................................................................................................................................ 90

3. Diluted earnings per share ..................................................................................................................... 93

4. The importance of EPS & DEPS .............................................................................................................. 95

5. Limitations of EPS as a performance indicator ...................................................................................... 95

Chapter 12 Statement of Cash Flows ................................................................................................................. 96

1. The need for a statement of cash flows ................................................................................................. 96

2. Definitions .............................................................................................................................................. 96

3. Preparation of statement of cash flows ................................................................................................. 97

4. Interpretation of cash flow .................................................................................................................... 99

5. Limitations of the statement of cash flow ........................................................................................... 101

Part C CONSOLIDATION ACCOUNTS .............................................................................................................. 105

Chapter 13 The Consolidation Statement of Financial Position ...................................................................... 105

1. The nature of business combination ................................................................................................... 105

2. Accounting issues ................................................................................................................................. 106

3. The single entity concept ..................................................................................................................... 106

4. Basic principle of consolidation financial statement ........................................................................... 107

5. Basic for consolidation statement of financial position ....................................................................... 107

6. Explanations of group account--IFRS 3 business combination ............................................................ 109

Chapter 14 The Consolidated Statement of Profit or Loss and Other Comprehensive Income ...................... 122

1. Accounting for subsidiary companies .................................................................................................. 122

2. Accounting for disposal of a subsidiary ............................................................................................... 125

Chapter 15 Accounting for Associates ............................................................................................................. 127

1. Defining an associated undertaking ..................................................................................................... 127

Part D ANALYSING AND INTERPRETING FINANCIAL STATEMENTS OF SINGLE ENTITIES AND GROUPS .............. 131

Chapter 16 Interpretation of Financial Statements ......................................................................................... 131

1. Interpreting financial information ....................................................................................................... 131

2. Ratio analysis ....................................................................................................................................... 132

2

ACCA- FR 2021-2022 Introduction

FR Introduction 1. Aim of paper

To develop knowledge and skills in understanding and applying IFRS Standards(Accounting standards) and the

theoretical framework in the preparation of financial statements of entities, including groups and how to analyze

and interpret those financial statements.

2. Main capabilities

On successful completion of this exam, candidates should be able to:

A Discuss and apply a conceptual and regulatory frameworks for financial reporting.

B Account for transactions in accordance with IFRS Standards.

C Analyse and interpret financial statements.

D Prepare and present financial statements for single entities and business combinations in accordance with IFRS

Standards.

E Demonstrate employability and technology skills

Computer-based exams

The syllabus is assessed by a three hour computer based examination.

All questions are compulsory. The exam will contain both computational and discursive elements. Some

questions will adopt a scenario/case study approach.

Section A of the computer-based exam comprises 15 objective test questions of 2 marks each plus additional

content as per below.

Section B of the computer-based exam comprises three questions each containing five objective test questions

plus additional content as per below.

Section C of the exam comprises two 20 mark constructed response questions.

The 20 mark questions will examine the interpretation and preparation of financial statements for either a

single entity or a group. The section A questions and the other questions in section B can cover any areas of

the syllabus.

The conceptual and regulatory framework for

financial reporting ( A )

Preparation of financial statements ( D )

Accounting for transactions in financial

statements ( B )

Analysing

and

interpreting

financial

statements( C )

Employability

and

technology

skills ( E )

3

ACCA- FR 2021-2022 Introduction

3. The syllabus

3.1 The conceptual and regulatory framework for financial reporting

3.1.1 The need for a conceptual framework the characteristics of useful information

3.1.2 Recognition and measurement

3.1.3 Regulatory framework

3.1.4 The concepts and principles of groups and consolidated financial statements

3.2 Accounting for transactions in financial statements

3.2.1. Tangible non-current assets

3.2.2. Intangible assets

3.2.3. Impairment of assets

3.2.4. Inventory and biological assets

3.2.5. Financial instruments

3.2.6. Leasing

3.2.7. Provisions and events after the reporting period

3.2.8. Taxation

3.2.9. Reporting financial performance

3.2.10. Revenue

3.2.11. Government grants

3.2.12. Foreign currency transactions 3.3 Analysing and interpreting financial statements of single entities and groups

3.3.1. Limitations of financial statements

3.3.2. Calculation and interpretation of accounting ratios and trends to address users’ and stakeholders’ needs

3.3.3. Limitations of interpretation techniques

3.3.4. Specialised, not-for-profit, and public sector entities 3.4 Preparation of financial statements

3.4.1. Preparation of single entity financial statements

3.4.2. Preparation of consolidated financial statements including an associate 3.5 Employability and technology skills

Use computer technology to efficiently access and manipulate relevant information

Work on relevant response options, using available functions and technology, as would be required in the

workplace.

Navigate windows and computer screens to create and amend responses to exam requirements, using the

appropriate tools.

Present data and information effectively, using the appropriate tools.

4. Exam format

Format of the paper

Marks

Section A – 15 MCQs 30

Section B – three case questions (10 marks each) 30

Section C – two constructed response questions (20 marks each) 40

100

4

ACCA- FR 2021-2022 Introduction

5. Linking to other papers

6. Examinable documents Sep 2021 to Jun 2022

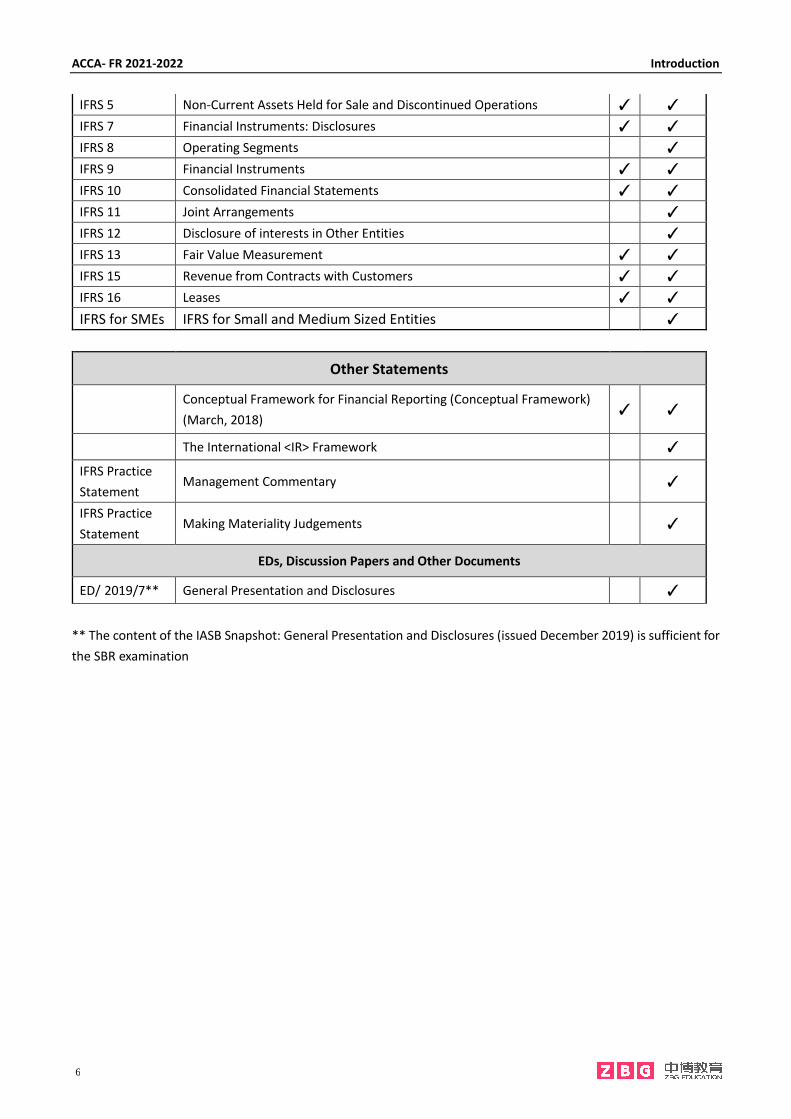

Title FR SBR INT

and UK

International Accounting Standards (IAS standards)/International

Financial Reporting Standards (IFRS standards)

IAS 1 Presentation of Financial Statements ✓ ✓

IAS 2 Inventories ✓ ✓

IAS 7 Statement of Cash Flows ✓ ✓

IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors ✓ ✓

IAS 10 Events after the Reporting Period ✓ ✓

IAS 12 Income Taxes ✓ ✓

IAS 16 Property, Plant and Equipment ✓ ✓

IAS 19 Employee Benefits ✓

IAS 20 Accounting for Government Grants and Disclosure of Government

Assistance ✓ ✓

IAS 21 The Effects of Changes in Foreign Exchange Rates ✓ ✓

IAS 23 Borrowing Costs ✓ ✓

IAS 24 Related Party Disclosures ✓

IAS 27 Separate Financial Statements ✓ ✓

IAS 28 Investments in Associates and Joint Ventures ✓ ✓

IAS 32 Financial Instruments: Presentation ✓ ✓

IAS 33 Earnings per Share ✓ ✓

IAS 34 Interim Financial Reporting ✓

IAS 36 Impairment of Assets ✓ ✓

IAS 37 Provisions, Contingent Liabilities and Contingent Assets ✓ ✓

IAS 38 Intangible Assets ✓ ✓

IAS 40 Investment Property ✓ ✓

IAS 41 Agriculture ✓ ✓

IFRS 1 First-time Adoption of International Financial Reporting Standards ✓

IFRS 2 Share-based Payment ✓

IFRS 3 Business Combinations ✓ ✓

Strategic Business Reporting

( SBR )

Strategic Business Leader

(SBL )

Financial Accounting ( FA )

Corporate and Business

Law ( LW )

Audit and Assurance

( AA ) Financial Reporting ( FR )

5

ACCA- FR 2021-2022 Introduction

IFRS 5 Non-Current Assets Held for Sale and Discontinued Operations ✓ ✓

IFRS 7 Financial Instruments: Disclosures ✓ ✓

IFRS 8 Operating Segments ✓

IFRS 9 Financial Instruments ✓ ✓

IFRS 10 Consolidated Financial Statements ✓ ✓

IFRS 11 Joint Arrangements ✓

IFRS 12 Disclosure of interests in Other Entities ✓

IFRS 13 Fair Value Measurement ✓ ✓

IFRS 15 Revenue from Contracts with Customers ✓ ✓

IFRS 16 Leases ✓ ✓

IFRS for SMEs IFRS for Small and Medium Sized Entities ✓

Other Statements

Conceptual Framework for Financial Reporting (Conceptual Framework)

(March, 2018) ✓ ✓

The International <IR> Framework ✓

IFRS Practice

Statement Management Commentary ✓

IFRS Practice

Statement Making Materiality Judgements ✓

EDs, Discussion Papers and Other Documents

ED/ 2019/7** General Presentation and Disclosures ✓

** The content of the IASB Snapshot: General Presentation and Disclosures (issued December 2019) is sufficient for

the SBR examination

6

ACCA- FR 2021-2022 Part A-Chapter 1

Part A FRAMEWORK

Chapter 1 IASB Framework

Content

1. The IASB conceptual framework for financial reporting

2. Regulatory framework

3. Not-for-profit and public sector entities

1. The IASB conceptual framework for financial reporting

1.1 The meaning of a conceptual framework

A conceptual framework is a coherent system of interrelated objectives and fundamental principles. These

theoretical principles provide the basis for the development of new IFRS Standards and the evaluation of those

already in existence. The financial reporting process is concerned with providing information that is useful in

the business and economic decision-making process. Therefore a conceptual framework will form the

theoretical basis for determining which events should be accounted for, how they should be measured and

how they should be communicated to the user.

⚫ There are two main approaches to accounting:

A principles-based or conceptual framework approach such as that used by the IASB.

A rules-based approach such as that used in the US.

⚫ Why has a conceptual framework?

There are a variety of arguments for having a conceptual framework.

It enables IFRS Standards and generally accepted accounting practice(GAAP) to be developed in

accordance with agreed principles.

It avoids ‘fire-fighting’, whereby IFRS Standards are developed in a piecemeal way in response to specific

problems or abuses. ‘Fire-fighting’ can lead to inconsistencies between different IFRS Standards, and

between IFRS Standards and legislation.

Lack of a conceptual framework may mean that certain critical issues are not addressed, e.g. until recently

there was no definition of basic terms such as ‘asset’ or ‘liability’ in any accounting standard.

As transactions become more complex and businesses become more sophisticated it helps preparers and

auditors of accounts to deal with transactions which are not the subject of an accounting standard. 1.2 Objectives of Framework

⚫ Defines the objective of financial reporting; identifies the qualitative characteristics that make

information in financial statements useful; and

⚫ Defines the basic elements of financial statements and the concepts for recognizing and measuring them

in financial statements. 1.3 Objective of Financial Statements

⚫ The objective of financial statements is to provide information about the financial position, financial

performance and cash flows of an entity that is useful to a wide range of users in making economic decisions.

Financial statements also show the results of the management’s stewardship of the resources entrusted to

it.

7

ACCA- FR 2021-2022 Part A-Chapter 1

⚫ The Conceptual Framework makes it clear that this information should be prepared on an accruals basis.

Accruals basis. The effects of transactions and other events are recognised when they occur (and not as

cash or its equivalent is received or paid) and they are recorded in the accounting records and reported

in the financial statements of the periods to which they relate.

1.4 Underlying Assumptions

The Framework sets out the going concern assumptions of financial statements:

⚫ Going Concern assumes that the entity has neither the need nor the intention to liquidate or curtail

materially the scale of its operations. If this is not the case then the financial statements would be prepared

on a different basis.

1.5 Qualitative Characteristics of Financial Statements

If financial information is to be useful, it must be relevant and faithfully represent what it purports to represent.

The usefulness of financial information is enhanced if it is comparable, verifiable, timely and understandable.

⚫ The fundamental qualitative characteristics are relevance and faithful representation.

⚫ Comparability, verifiability, timeliness and understandability are qualitative characteristics that enhance

the usefulness of information that is relevant and faithfully represented.

1.5.1 Fundamental qualitative characteristics

⚫ Relevance

Relevant information is capable of making a difference in the decisions made by users. It is capable of

making a difference in decisions if it has predictive value, confirmatory value or both. The relevance of

information is affected by its nature and its materiality.

Materiality. Information is material if omitting it or misstating it could influence decisions that users

make on the basis of financial information about a specific reporting entity.

⚫ Faithful representation

To be a perfectly faithful representation, a depiction would have three characteristics. It would be

complete, neutral and free from error.

A complete depiction includes all information necessary for a user to understand the phenomenon

being depicted, including all necessary descriptions and explanations.

A neutral depiction is without bias in the selection or presentation of financial information. This

means that information must not be manipulated in any way in order to influence the decisions of

users.

Free from error means there are no errors or omissions in the description of the phenomenon and

no errors made in the process by which the financial information was produced. It does not mean

that no inaccuracies can arise, particularly where estimates have to be made.

Substance over form is not a separate qualitative characteristic under the conceptual Framework.

The IASB says that to do so would be redundant because it is implied in faithful representation.

Faithful representation of a transaction is only possible if it is accounted for according to its

substance and economic reality.

8

ACCA- FR 2021-2022 Part A-Chapter 1

1.5.2 Enhancing qualitative characteristics

⚫ Comparability

Comparability is the qualitative characteristic that enables users to identify and understand similarities

in, and differences among, items. Unlike the other qualitative characteristics, comparability does not

relate to a single item. A comparison requires at least two items.

⚫ Verifiability

Verifiability helps assure users that information faithfully represents the economic phenomena it

purports to represent. It means that different knowledgeable and independent observers could reach

consensus that a particular depiction is a faithful representation.

⚫ Timeliness

Timeliness means having information available to decision-makers in time to be capable of influencing

their decisions. Generally, the older the information is the less useful it is. However, some information

may continue to be timely long after the end of a reporting period because, for example, some users

may need to identify and assess trends.

⚫ Understandability

Classifying, characterising and presenting information clearly and concisely makes it understandable.

Some phenomena are inherently complex and cannot be made easy to understand. Excluding

information about those phenomena from financial reports might make the information in those

financial reports easier to understand. However, those reports would be incomplete and therefore

potentially misleading.

Financial reports are prepared for users who have a reasonable knowledge of business and

economic activities and who review and analyse the information diligently. At times, even well-

informed and diligent users may need to seek the aid of an adviser to understand information about

complex economic phenomena.

1.6 The Elements of Financial Statements

Financial statements portray the financial effects of transactions and other events by grouping them into broad

classes according to their economic characteristics. These broad classes are termed the elements of financial

statements.

⚫ The elements directly related to financial position (statement of financial position) are:

Assets

Liabilities

Equity

⚫ The elements directly related to performance (statement profit or loss and other comprehensive income)

are:

Income

Expenses

⚫ The statement of cash flows reflects both income statement elements and changes in statement of financial

position elements.

9

ACCA- FR 2021-2022 Part A-Chapter 1

1.6.1 Definitions of the elements

⚫ Financial position

Asset. An asset is a present economic resource controlled by the entity as a result of past events.

Liability. A liability is a present obligation of the entity to transfer an economic resource as a result

of past events.

Equity. Equity is the residual interest in the assets of the enterprise after deducting all its liabilities.

⚫ Performance

Income. Income is increases in assets, or decreases in liabilities, that result in increases in equity,

other than those relating to contributions from holders of equity claims.

Expense. Expenses are decreases in assets, or increases in liabilities, that result in decreases in

equity, other than those relating to distributions to holders of equity claims.

1.6.2 Recognition of the elements of financial statements

⚫ An asset or liability is recognised only if recognition of that asset or liability and of any resulting income,

expenses or changes in equity provides users of financial statements with information that is useful, ie

with:

Relevant information about the asset or liability and about any resulting income, expenses or

changes in equity and

A faithful representation of the asset or liability and of any resulting income, expenses or changes

in equity.

⚫ Recognition is subject to cost constraints: the benefits of the information provided by recognising an

element should justify the cost of recognising that element.

1.6.3 Measurement of the elements of financial statements

⚫ Measurement involves assigning monetary amounts at which the elements of the financial statements

are to be recognised and reported.

⚫ The framework acknowledges that a variety of measurement bases are used today to different degrees

and in varying combinations in financial statements, including:

Historical cost

Fair value

Value in use

Current cost

⚫ Historical cost

An asset when it is acquired or created is the value of the costs incurred in acquiring or creating the

asset, comprising the consideration paid to acquire or create the asset plus transaction costs.

The historical cost of a liability when it is incurred or taken on is the value of the consideration

received to incur or take on the liability minus transaction costs.

Recent standards use the concept of fair value, which is defined by IFRS 13 as ‘the price that would be

received to sell an asset or paid to transfer a liability in an ordinary transaction between market

participants at the measurement date’.

10

ACCA- FR 2021-2022 Part A-Chapter 1

⚫ Current Value

Fair value

· Fair value is the price that would be received to sell an asset, or paid to transfer a liability, in an

orderly transaction between market participants at the measurement date.

Value in use

· Value in use is the present value of the cash flows, or other economic benefits, that an entity

expects to derive from the use of an asset and from its ultimate disposal.

· Fulfilment value is the present value of the cash, or other economic resources, that an entity

expects to be obliged to transfer as it fulfils a liability.

Current cost

· An asset is the cost of an equivalent asset at the measurement date, comprising the

consideration that would be paid at the measurement date plus the transaction costs that

would be incurred at that date.

· A liability is the consideration that would be received for an equivalent liability at the

measurement date minus the transaction costs that would be incurred at that date.

2. Regulatory framework

2.1 The regulatory framework

⚫ The regulatory framework of accounting in each country which uses IFRS is affected by a number of legislative

and quasi-legislative influences as well as IFRS:

National company law

EU directives

Security exchange rules

⚫ Why a regulatory framework is necessary?

Regulation of accounting information is aimed at ensuring that users of financial statements receive a

minimum amount of information that will enable them to make meaningful decisions regarding their

interest in a reporting entity. A regulatory framework is required to ensure that relevant and reliable

financial reporting is achieved to meet the needs of shareholders and other users.

IFRS Standards on their own would not be a complete regulatory framework. In order to fully regulate

the preparation of financial statements and the obligations of companies and directors, legal and market

regulations are also required.

2.2 Principles-based and rules-based framework

2.2.1 Principles-based framework:

⚫ Based upon a conceptual framework such as the IASB’s Framework.

⚫ IFRS Standards are set on the basis of the conceptual framework.

2.2.2 Rules-based framework:

⚫ ‘Cookbook’ approach.

⚫ IFRS Standards are a set of rules which companies must follow.

In the UK there is a principles-based framework in terms of the Statement of Principles and IFRS Standards and

a rules-based framework in terms of the Companies Act, EU directives and stock exchange rulings.

11

ACCA- FR 2021-2022 Part A-Chapter 1

2.3 The structure is set out below: (Optional)

2.3.1 International Financial Reporting Standards (IFRS) Foundation

The IFRS Foundation is the supervisory body for the IASB and responsible for governance issues and

ensuring each body is properly funded.

The objective of the IFRS Foundation include:

⚫ Develop a set of global IFRS Standards high quality which are understandable and enforceable.

⚫ Promote using and applying these standards.

⚫ Bring about the convergence of national and IFRS Standards.

2.3.2 International Accounting Standards Board (IASB)

The IASB is solely responsible for issuing International Financial Reporting Standards (IFRSs).

2.3.3 IFRS Interpretations Committee (IFRS IC)

IFRS IC issues rapid guidance on accounting matters where divergent interpretations of IFRSs have arisen

and these must be approved by the IASB. The interpretations cover both:

⚫ Newly identified financial reporting issues not specifically dealt with in IFRSs; or

⚫ Issues where unsatisfactory or conflicting interpretations have developed, or seem likely to develop in

the absence of authoritative guidance, with a view to reaching a consensus on the appropriate

treatment.

2.3.4 IFRS Advisory Council (IFRS AC)

The IFRS AC provides a forum for the IASB to consult a wide range of interested

parties affected by the IASB’s work, with the objective of :

⚫ Advising the Board on agenda decisions and priorities in the Board’s work,

⚫ Informing the Board of the views of the organizations and individuals on the council on major

standard-setting projects, and

⚫ Giving other advice to the Board or to the Trustees.

IFRS Foundation

IFRS IC

IFRS AC IASB

12

ACCA- FR 2021-2022 Part A-Chapter 1

2.4 IASB’s Standard setting process

The procedure for the development of an IFRS is as follows:

⚫ Setp1: During the early stages of a project, the IASB may establish an Advisory Committee to give advice on

issues arising in the project.

⚫ Step 2: IASB may develop and publish Discussion Papers for public comment.

⚫ Step 3: Following the receipt and review of comments, the IASB could issue a final International Exposure

Draft for public comment.

⚫ Step 4: Following the receipt and review of comments, the IASB could issue a final International Financial

Reporting Standard.

3. Not-for-profit and public sector entities

3.1 The main aims of not-for-profit and public sector entities are very different to those of profit-orientated entities:

Profit-orientated sector Not-for-profit / public sector

⚫ Financial aim is to make profit and increase

shareholder wealth.

⚫ Directors are accountable to shareholders.

⚫ External finance freely available in the form of

loans and share capital.

⚫ Financial aim is to achieve value for money /

provide service.

⚫ Managers are accountable to trustees /

government / public.

⚫ Finance limited to donations / government

subsidies.

3.2 IFRS Standards and not-for-profit and public sector entities

3.2.1 IFRS Standards are designed to:

⚫ Measure financial performance accurately and consistently.

⚫ Report the financial position accurately and consistently.

⚫ Account for the director’s stewardship of the resources and assets.

3.2.2 Not-for-profit and public sector organizations:

⚫ Do not aim to achieve a profit but will have to account for their income and costs.

⚫ Will have to account for their effectiveness, economy and efficiency.

⚫ Do not have to produce financial statements for the public (but in many cases may do so).

⚫ Some IFRS Standards will be relevant such as those relating to inventory, non-current assets, leasing,

etc. Others relating purely to reporting such as earnings per share (EPS) will not be so relevant.

13

ACCA- FR 2021-2022 Part A-Chapter 1

Example 1 Conceptual framework (Referred to Dec 2014 Q3)

Although most items in financial statements are shown at their historical cost, increasingly the IASB is requiring or

allowing current cost to be used in many areas of financial reporting.

Drexler acquired an item of plant on 1 October 20X2 at a cost of $500,000. It has an expected life of five years

(straight-line depreciation) and an estimated residual value of 10% of its historical cost or current cost as appropriate.

As at 30 September 20X4, the manufacturer of the plant still makes the same item of plant and its current price is

$600,000.

What is the correct carrying amount to be shown in the statement of financial position of Drexler as at 30

September 20X4 under historical cost and current cost?

Historical cost Current cost

$ $

A 320,000 600,000

B 320,000 384,000

C 300,000 600,000

D 300,000 384,000

Example 2 Regulatory framework

Which one of the following would not be an advantage of adopting IFRS?

A It would be easier for investors to compare the financial statements of companies with those of foreign

competitors.

B Cross-border listing would be facilitated.

C Accountants and auditors would have more defenses in case of litigation.

D Multinational companies could more easily transfer accounting staff across national borders.

14

ACCA- FR 2021-2022 Part B-Chapter 2

Part B IFRS STANDARDS (ACCOUNTING STANDARDS)

Chapter 2 IAS1 Presentation of Financial Statements

Content

1. A complete set of financial statements comprises

2. Single entity financial statements

3. Illustration of group financial statements

1. A complete set of financial statements comprises

⚫ Statement of financial position (SOFP)

⚫ Statement profit or loss and other comprehensive income (SPL&OCI; SOCI)

⚫ Statement of changes in equity (SOCIE)

⚫ Statement of cash flows (SOCF)

⚫ Accounting policies and explanatory notes

The first three statements are shown below; the cash flow statement will be discussed in much greater detail

later.

These formats are in the Implementation Guidance that accompanies IAS 1. They are not obligatory, but are

obviously of vital examination importance.

2. Single entity financial statements

2.1 Statement of financial position

XYZ Company

Statement of Financial Position as at 31 December 20X9

ASSETS $ $

Non-current assets

Property, plant and equipment X

Other intangible assets X

Investments in associates X

Investments X

X

Current assets

Inventories X

Trade receivables X

Cash and cash equivalents X

X

Total assets X

15

ACCA- FR 2021-2022 Part B-Chapter 2

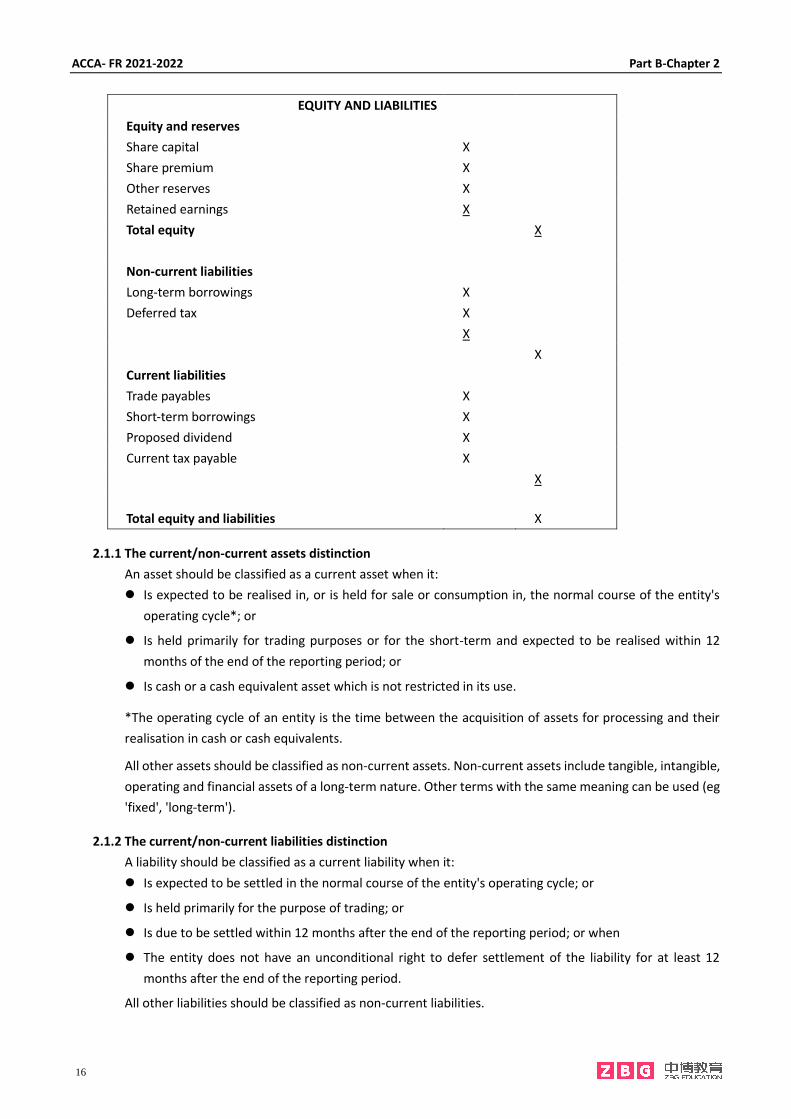

EQUITY AND LIABILITIES

Equity and reserves

Share capital X

Share premium X

Other reserves X

Retained earnings X

Total equity X

Non-current liabilities

Long-term borrowings X

Deferred tax X

X

X

Current liabilities

Trade payables X

Short-term borrowings X

Proposed dividend X

Current tax payable X

X

Total equity and liabilities X

2.1.1 The current/non-current assets distinction

An asset should be classified as a current asset when it:

⚫ Is expected to be realised in, or is held for sale or consumption in, the normal course of the entity's

operating cycle*; or

⚫ Is held primarily for trading purposes or for the short-term and expected to be realised within 12

months of the end of the reporting period; or

⚫ Is cash or a cash equivalent asset which is not restricted in its use.

*The operating cycle of an entity is the time between the acquisition of assets for processing and their

realisation in cash or cash equivalents.

All other assets should be classified as non-current assets. Non-current assets include tangible, intangible,

operating and financial assets of a long-term nature. Other terms with the same meaning can be used (eg

'fixed', 'long-term').

2.1.2 The current/non-current liabilities distinction

A liability should be classified as a current liability when it:

⚫ Is expected to be settled in the normal course of the entity's operating cycle; or

⚫ Is held primarily for the purpose of trading; or

⚫ Is due to be settled within 12 months after the end of the reporting period; or when

⚫ The entity does not have an unconditional right to defer settlement of the liability for at least 12

months after the end of the reporting period.

All other liabilities should be classified as non-current liabilities.

16

ACCA- FR 2021-2022 Part B-Chapter 2

2.2 Statement profit or loss and other comprehensive income

⚫ The revised IAS1 requires to present ‘other comprehensive income’ items (such as revaluation gains and

losses, and actuarial gains and losses), as well as the usual income statement items, on the face of the primary

financial statements.

⚫ Total comprehensive income: is the realized profit or loss for the period, plus other comprehensive income.

⚫ Other comprehensive income is the income and expenses that are not recognized in the profit or loss (i.e.

they are recorded in reserve rather than as an element of the realized profit for the period). For the purposes

of FR, other comprehensive income includes any change in the revaluation surplus.

XYZ Company

Statement of comprehensive income for the year ended 31 December 20X9

$ $

Revenue x

Cost of sales (x)

Gross profit x

Distribution cost (x)

Administrative expense (x)

Operating profit x

Finance cost (x)

Profit before tax (PBT) x

Tax (x)

Profit for the period x

Other comprehensive income

Revaluation surplus on property, plant and equipment x

Reversal of revaluation surplus on property, plant and equipment (x)

Revaluation gain or loss on investment in equity instrument

( FVTOCI financial asset) x

x

Total comprehensive income x 2.3 Statement of Changes in Equity

XYZ Company

Statement of Changes in Equity for the year ended 31 December 20X9

Share

capital

Share

premium

Revaluation

reserve

Retained

earnings

Total

$000 $000 $000 $000 $000

Opening balance X X X X X

Changes in accounting policies X X

Total comprehensive income X/(X) X X

Revaluation transfer to RE (X) X 0

Dividends paid (X) (X)

Issue of share capital X X X

Closing balance X X X X X

17

ACCA- FR 2021-2022 Part B-Chapter 2

3. Illustration of group financial statements

3.1 XYZ Group – Consolidated statement of financial position as at 31 December 20X9

20X9 20X8

$000 $000

ASSETS

Non – current assets Property, plant and equipment 350,700 360,020

Goodwill 80,800 91,200

Other intangible assets 227,470 227,470

Investment in associates 100,150 110,770

Investment in equity ( FVTOCI financial asset) 142,500 156,000

901,620 945,460

Current assets

Inventories 135,230 132,500

Trade receivables 91,600 110,800

Other current assets 25,650 12,540

Cash and cash equivalents 312,400 322,900

564,880 578,740

Total assets 1,466,500 1,524,200

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Share capital 650,000 600,000

Retained earnings 243,500 161,700

Other components of equity 10,200 21,200

903,700 782,900

Non-controlling interest 70,050 48,600

Total equity 973,750 831,500

Non-current liabilities

Long-term borrowings 120,000 160,000

Deferred tax 28,800 26,040

Long-term provisions 28,850 52,240

Total non-current liabilities 177,650 238,280

Current liabilities

Trade and other payables 115,100 187,620

Short-term borrowings 150,000 200,000

Current portion of long-term borrowings 10,000 20,000

Current tax payable 35,000 42,000

Short-term provisions 5,000 4,800

Total current liabilities 315,100 454,420

Total liabilities 492,750 692,700

Total equity and liabilities 1,466,500 1,524,200

18

ACCA- FR 2021-2022 Part B-Chapter 2

3.2 Consolidated statement of comprehensive income for the year ended 31 December 20X9

20X9 20X8

$000 $000

Revenue 390,000 355,000

Cost of sales (245,000) (230,000)

Gross profit 145,000 125,000

Other income 20,667 11,300

Distribution costs (9,000) (8,700)

Administrative expenses (20,000) (21,000)

Other expense (2,100) (1,200)

Financial costs (8,000) (7,500)

Share of profit of associates(a) 35,100 30,100

Profit before tax 161,667 128,000

Income tax expense (40,417) (32,000)

Profit for the year from continuing operations 121,250 65,500

Loss for the year from discontinued operations - (30,500)

PROFIT FOR THE YEAR 121,250 35,000

Other comprehensive income:

Gains on property revaluation 933 3,367

Investments in equity instruments (24,000) 26,667

Income tax 5,834 (7,667)

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 104,017 57,367

Profit attributable to:

Owners of the parent 97,000 25,900

Non-controlling interest 24,250 9,100

121,250 35,000

Total comprehensive income attributable to:

Owners of the parent 83,567 43,667

Non-controlling interest 20,450 13,700

104,017 57,367

Earnings per share (in currency units):

Basic and diluted 0.46 0.30

⚫ This means the share of associates profit attributable to owner of the associates, i.e. it is after tax and non-

controlling interests in the associates.

⚫ This illustrates the aggregated presentation, with disclosure of the current year gain or loss and

reclassification adjustment presented in the notes. Alternatively, a gross presentation can be used.

⚫ This means the share of associates other comprehensive income attributable to owners of the associates, i.e.

it is after tax and non-controlling interests in the associates.

⚫ The income tax relating to each component of other comprehensive income is disclosed in the notes.

19

ACCA- FR 2021-2022 Part B-Chapter 2

Example 1

Where equity dividends paid is presented in the financial statements?

A As a deduction from retained earnings in the statement of changes in equity.

B As a liability in the statement of financial position.

C As an expense in profit or loss.

D As a loss in ‘other comprehensive income’.

20

ACCA- FR 2021-2022 Part B-Chapter 3

Chapter 3 Non-Current Assets

Content

1.IAS16 Property, Plant and Equipment

2.IAS40 Investment property

3.IAS38 Intangible assets

4.IAS36 Impairment of assets

5.IAS23 Borrowing costs

6.IAS20 Government grant

7.IFRS5 Non-current asset held for sale and discontinued operations

Session Content

Tangible

Non-current Initial

IAS 40 assets costs

Investment

properties

Subsequent

expenditure

Finance

costs Depreciation

Revaluation

Indications

Impairment

CGU NRV &

Value in use

Treatment

Research & Recognition

Development

Problems

Criteria Treatment

Special : Non-current assets held for sale

Tangibles

Intangibles

21

ACCA- FR 2021-2022 Part B-Chapter 3

1. IAS 16 Property, plant and equipment

1.1 Definition

⚫ Property, plant and equipment are tangible assets held by an enterprise for more than one accounting period

for use in the production or supply of goods or services, for rental to others or for administrative purposes.

⚫ Owner occupied assets (used for ordinary business activities).

1.2 Recognition

⚫ Item of property, plant and equipment should be recognised as assets when:

It is probable that the future economic benefits associated with the asset will flow to the entity, and

The cost of the asset can be measured reliably. 1.3 Initial measurement

An item of property, plant and equipment shall be measured at its cost.

⚫ Purchase price, including import duties and non-refundable purchase taxes, after deducting trade discounts

and rebates.

⚫ Include all costs involved in bringing the asset into working condition

Site preparation cost

Initial delivery and handling costs

Installation costs

Testing costs whether the asset is functioning properly

Professional fees

Borrowing costs (Refer to IAS23)

⚫ Initial estimate of unavoidable costs of dismantling and removing the asset and restoring the site on which

it is located. Present value of these costs should be capitalized (Refer to IAS37 Provision, contingent assets

and liabilities).

⚫ Excluding:

Administration and general overheads

Set-up and similar pre- production costs

Initial operating losses before the asset reaches planned performance 1.4 Subsequent expenditure

Subsequent expenditure should be recognised in the carrying amount of an item of property, plant and

equipment if :

It enhances the economic benefits provided by the asset (this could be extending the asset’s life, and

expansion or increase the productivity of the asset).

It related to an overhaul or required major inspection of the asset- the costs associated with this should

be recognised in the carrying amount and depreciated over the time until the next overhaul or safety

inspection.

It is replacing a component of a complex asset. The replaced component will be derecognized. A complex

asset is an asset made up of a number of components, which each depreciate at different rates, Eg: an

aircraft would comprise body, engines and interior.

22

ACCA- FR 2021-2022 Part B-Chapter 3

⚫ All other subsequent expenditure should be recognized in the statement of profit or loss (expense), because

it merely maintains the economic benefits originally expected. Eg: the cost of general repairs should be

written off immediately.

1.5 Depreciation

⚫ Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life.

⚫ It is in essence a cost allocation process in compliance with the accruals / matching principle. Each

accounting period must bear a charge for depreciation to reflect the usage of the asset and benefit it helps

to generate.

⚫ Depreciable amount is the cost of an asset less its residual value.

⚫ All assets with a finite useful life must be depreciated. Land has no finite life, therefore excluded from

depreciation.

⚫ Depreciation must be charged from the date the asset is available for use. This may be earlier than the date

it is actually brought into use, for example when staff needs to be trained to use it.

⚫ Depreciation is continued even if the asset is idle.

1.5.1 Depreciation methods

The depreciation method used should reflect as fairly as possible the pattern in which the asset’s economic

benefits are consumed by the entity.

⚫ Straight line

Annual Depreciation =Cost-residual value

Useful life or (cost-residual value)*depreciation rate %

⚫ Reducing balance

Annual Depreciation = Net book value opening balance* depreciation rate %

1.5.2 Changes in useful life or method

⚫ The useful lives of assets or depreciation method should be reviewed at least at each financial year-

end and, when necessary, revised. When a material change becomes necessary, the depreciation

charge for the current and future periods should be adjusted.

⚫ Change of useful life or method is a change in accounting estimate not a change in accounting policy.

⚫ Apply new rate/method to existing NBV, previous year accounts unchanged.

Straight line

Cost $20,000 Residual value $2000 Useful economic life 4 years

Annual depreciation: (20000-2000)/4=4500

Reducing balance

Cost $20,000 Reducing balance% 25%

Annual depreciation:

Y1: 20000*25%=5000

Y2: (20000-5000)*25%=3750

23

ACCA- FR 2021-2022 Part B-Chapter 3

1.5.3 Separate components

Some items of property, plant and equipment comprise separate components with different useful lives.

For example, an aircraft might itself have a life of 30 years while the seats and fabrics in the interior only

have a life of five years. In such situations the separate components should be capitalized as separate

assets and each depreciated over their useful lives.

1.6 Subsequent measurement

⚫ IAS 16 allows a choice of accounting treatment for PPE:

The cost model

The revaluation model

⚫ Accounting treatment

Cost model Revaluation model

Initial

recognition

Initially measured at cost

Subsequent

measurement

Cost

–accumulative depreciation

–impairment losses

Revalued amount – accumulative depreciation

– impairment losses

Dr: Cost

Dr: Acc depreciation

Cr: Other

comprehensive

income(OCI)

Dr: Acc

depreciation

Cr: OCI

Cr: Cost

Dr: Acc

depreciation

Cr: OCI

Depreciation Based on historical cost

Dr: Depreciation

Cr: Acc depreciation

Based on revalued amount

Dr: Depreciation

Cr: Acc depreciation

Any difference between actual depreciation and

historical depreciation may be transferred from RR to

RE:

Dr: Revaluation reserve

Cr: Retained earnings

Disposal Profit or loss on disposal =

Net proceeds–CV of the asset

Recognized as income or

expense in I/S

Profit or loss on disposal =

net proceeds – CV of the asset

Recognized as income or expense in I/S

Remaining balance may be transferred from RR to RE or

left in equity under the heading revaluation surplus

Dr: Revaluation reserve

Cr: Retained earnings

1.6.1 Revaluations

⚫ If the revaluation alternative is adopted, two conditions must be complied with.

Revaluations must subsequently be made with sufficient regularity to ensure that the carrying

amount does not differ materially from the fair value at each balance sheet date.

When an item of property, plant and equipment is revalued, the entire class of assets to which the

item belongs must be revalued.

24

ACCA- FR 2021-2022 Part B-Chapter 3

⚫ Revaluation gains are credited to other comprehensive income and equity (revaluation reserve), the

increase shall be recognized in profit and loss to the extent that it reveres a revaluation decrease

previously recognized in profit and loss.

⚫ Revaluation losses should be recognized as an expense to profit and loss. However the decrease shall

be recognized in other comprehensive income to the extent of any credit balance existing in the

revaluation surplus.

1.6.2 Depreciation of revalued asset

⚫ Must charge, based on valuation less residual value, over remaining useful economic life (UEL).

⚫ Whole charge must go to income statement for year.

⚫ Make annual reserve transfer (Revaluation reserve →Retained Earnings) for extra depreciation on

revalued amount compared to cost.

⚫ Journals:

$ $

Dr P/L – depreciation charge X

Cr Non-current asset (NBV) X

Dr Revaluation reserve X

Cr Retained earnings X

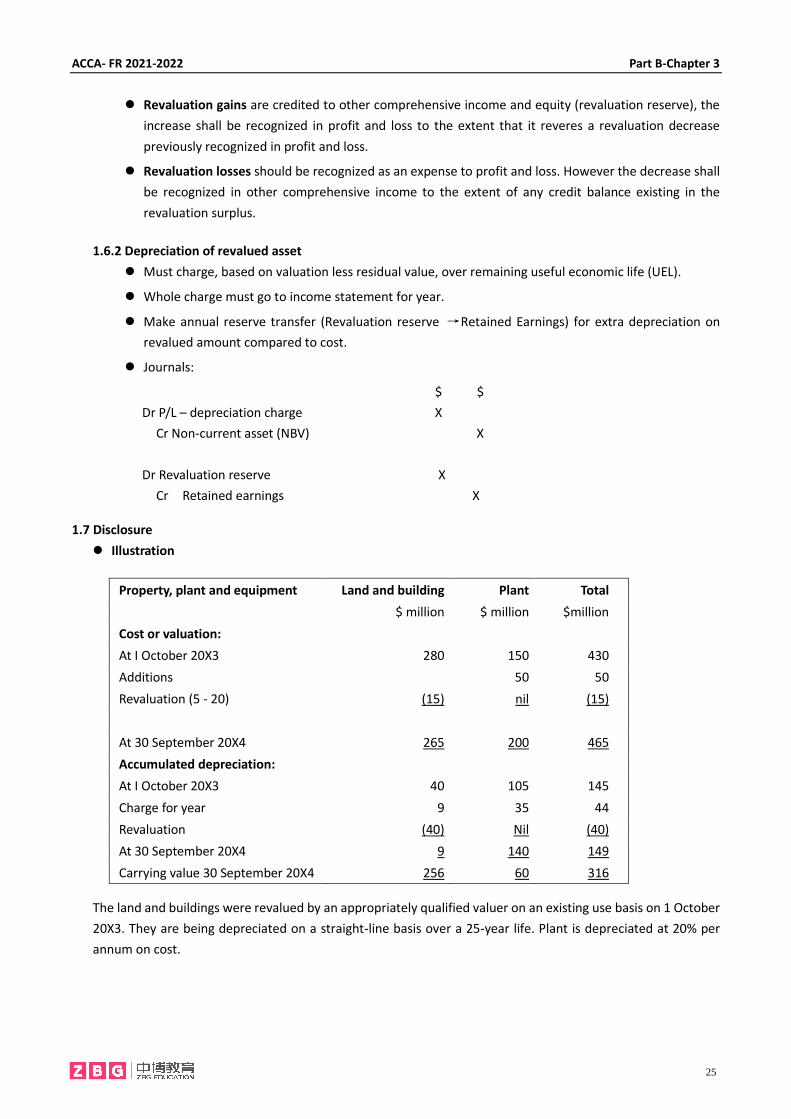

1.7 Disclosure

⚫ Illustration

Property, plant and equipment Land and building Plant Total

$ million $ million $million

Cost or valuation:

At I October 20X3 280 150 430

Additions 50 50

Revaluation (5 - 20) (15) nil (15)

At 30 September 20X4 265 200 465

Accumulated depreciation:

At I October 20X3 40 105 145

Charge for year 9 35 44

Revaluation (40) Nil (40)

At 30 September 20X4 9 140 149

Carrying value 30 September 20X4 256 60 316

The land and buildings were revalued by an appropriately qualified valuer on an existing use basis on 1 October

20X3. They are being depreciated on a straight-line basis over a 25-year life. Plant is depreciated at 20% per

annum on cost.

25

ACCA- FR 2021-2022 Part B-Chapter 3

Example 1 IAS 16 (Initial cost recognition)

Broadleaf company purchased a new machine during the year. The related costs were as follows:

$’000

List price 100

Installation 20

Pre-production testing 10

Insurance 2

Warranty 2

Maintenance 3 The company received a 10% trade discount on the list price. The installation should have cost $18,000 but Broadleaf

wasted $2,000 on installing the wrong machine supports at first. The maintenance occurred after the start of

production and was required by the warranty. Both the warranty and the insurance were for one year only. What is initial cost of new machine recognized by Broadleaf Co.

$

Example 2 IAS 16 (Revaluation)

On 1 Jan 20X8 Cheetah Ltd buys a non-current asset for $120,000. The asset has an estimated useful life of 20 years

with no residual value and is depreciated on a straight-line basis with a full year’s charge in the year of acquisition

and none in the year of disposal.

Cheetah Ltd’s year end is 31 Dec. On 31 Dec 20Y0, the asset will be included in the statement of financial position

at a cost of $120,000 with accumulated depreciation of $18,000.

On 1 Jan 20Y1, when the balance on the company’s accumulated profits was $500,000, the asset is revalued to

$136,000. The total useful life remains unchanged. Required:

1. Show the journal to record the revaluation.

2. Calculate the revised depreciation charge and show how it would be accounted for if reserve transfers as the

usage of the asset.

3. If the asset is revalued to $85,000, $102,000 on 1 Jan 20Y1, 1 Jan 20Y2 respectively, what are the double entries.

4. On 31 Dec 20Y0, the asset is sold for $127,000. Show how the disposal would be recorded.

Example 3 IAS 16 Past Exam Jun 2009 Q5

Flightline is an airline which treats its aircraft as complex non-current assets. The cost and other details of one of its

aircraft are:

$’000 estimated life

Exterior structure – purchase date 1 April 1995 120,000 20 years

Interior cabin fittings – replaced 1 April 2005 25,000 5 years

Engines (2 at $9 million each) – replaced 1 April 2005 18,000 36,000 flying hours

No residual values are attributed to any of the component parts.

At 1 April 2008 the aircraft log showed it had flown 10,800 hours since 1 April 2005. In the year ended 31 March

2009, the aircraft flew for 1,200 hours for the six months to 30 September 2008 and a further 1,000 hours in the six

months to 31 March 2009.

26

ACCA- FR 2021-2022 Part B-Chapter 3

On 1 October 2008 the aircraft suffered a ‘bird strike’ accident which damaged one of the engines beyond repair.

This was replaced by a new engine with a life of 36,000 hours at cost of $10·8 million. The other engine was also

damaged, but was repaired at a cost of $3 million; however, its remaining estimated life was shortened to 15,000

hours. The accident also caused cosmetic damage to the exterior of the aircraft which required repainting at a cost

of $2 million. As the aircraft was out of service for some weeks due to the accident, Flightline took the opportunity

to upgrade its cabin facilities at a cost of $4·5 million. This did not increase the estimated remaining life of the cabin

fittings, but the improved facilities enabled Flightline to substantially increase the air fares on this aircraft are: Required:

Calculate the charges to the income statement in respect of the aircraft for the year ended 31 March 2009 and its

carrying amount in the statement of financial position as at that date.

Note: the post-accident changes are deemed effective from 1 October 2008. (10 marks)

2. IAS 40 Investment property

2.1 Definition:

⚫ Investment property is defined by IAS 40 as land or a building held to earn rentals or for capital appreciation

or both, rather than for use in the enterprise or for sale in the ordinary course of business.

⚫ The following items are not investment properties

Accounted for under

Owner occupied property IAS 16

Property held for sale in the normal course of business IAS 2

Property being constructed for third parties IFRS 15 PART

2.2 Accounting treatment

⚫ Investment properties should initially be measured at cost.

⚫ IAS 40 then gives a choice between following a cost model or a fair value model.

2.2.1 Cost model--the asset should be accounted for in line with the benchmark treatment laid out in IAS 16.

2.2.2 Fair value model

⚫ The asset is revalued to fair value at the end of each year

⚫ The gain or loss is shown directly in the statement pf profit or loss (not OCI)

⚫ No depreciation is charged on the asset

Fair value is normally established by reference to current prices on an active market for properties in the

same location and condition.

If it is impossible to measure fair value reliably, then the cost-based model should be adopted.

It should not change from one model to the other unless the change will result in a more appropriate

presentation. IAS 40 states that it is highly unlikely that a change from the fair value model to the cost

model will result in a more appropriate presentation.

27

ACCA- FR 2021-2022 Part B-Chapter 3

2.2.3 Transfers

Transfer to or from investment property should only be made when there is a change in use.

⚫ Transfer from PPE to investment property and the fair value model for investment property

The asset must first be revalued per IAS 16 PPE and then transferred into investment property at FV

⚫ Transfer from investment to PPE, and the fair value model for investment property used.

Revalued the property first per IAS 40 and then transfer to PPE at FV

2.2.4 Disposal

Profit or loss on disposal = Net proceeds – Carrying amount of the asset, recognized as income or expense

in I/S.

Examples 1

Which of the following are examples of investment property?

(i) Land held for long-term capital appreciation rather than for short-term sale in the ordinary course of business;

(ii) A building that is vacant but is held to be leased out under one or more operating leases;

(iii) Land held for a currently undetermined future use;

(iv) Property occupied by employees;

A (i), (ii) and (iv)

B (i), (ii) and (iii)

C (i) and (ii)

D (i) and (iii)

Examples 2

Kingdom owns a building which it has been used as head office. At June 30 20X5, Kingdom let it out to a third party.

The building has an original cost on 1 January 20X0 at $ 500,000 and was being depreciated over 50 years. At 30

June 20X5, the fair value of this building is $480,000. At the year-end date of 31 December 20X5, the fair value of

this building is $510,000. Kingdom uses the fair value of investment property .

What amount will be shown in revaluation surplus at 31.December.20X5 in respect of this building?

A 35,000

B 45,000

C 55,000

D 65,000

3. IAS 38 Intangible assets

3.1 Introduction

⚫ When we considered IAS 16 Property, plant and equipment, we saw how businesses account for investment

in tangible assets. Many businesses invest significant amounts with the intention of obtaining future value

on areas such as:

Scientific/technical knowledge

Design of new processes and systems

Licenses and quotas

28

ACCA- FR 2021-2022 Part B-Chapter 3

Intellectual property e.g. Patents and copyrights

Market knowledge e.g. Customer lists, relationships and loyalty

Trademarks

The objective of IAS 38 is to prescribe the specific criteria that must be met an intangible asset can be recognized

in the accounts.

The standard covers all intangible assets other than those covered by another standard, which for our purposes

is Goodwill which is covered by IFRS 3.

3.2 Definition

⚫ An intangible asset is defined as, an identifiable non-monetary asset without physical substance. Therefore,

to meet the definition the asset must be:

Identifiable (is separable or arises from contractual /other legal rights);

Controlled by the entity as a result of past events;

A resource from which future economic benefits are expected to flow.

3.3 Recognition and measurement

To be recognized as an intangible asset must be meet

⚫ The definition of an intangible asset

⚫ The recognition criteria

It is probable that the future economic benefits attributable to the asset will flow to the entity

The cost of the asset can be measured reliably.

An intangible asset shall be measured initially at cost.

3.3.1 Acquired separately

⚫ If an intangible asset is purchased separately (such as a license, patent, brand name), it should be

recognized and initially measured at cost.

3.3.2 Acquisition as part of business combination

⚫ If an intangible is asset acquired as part of business combination, it should be recognized and initially

measured at fair value (and therefore the cost) as there is a rebuttable presumption that the fair value

of an intangible asset acquired in a business combination can be measured reliably.

⚫ However, an expenditure (included in the cost of acquisition) on an intangible item that does not meet

both the definition of and recognition criteria for an intangible asset should form part of the amount

attributed to the Goodwill recognized at the acquisition date.

3.3.3 Goodwill —IFRS 3 Treatment

⚫ Recognition and measurement of Goodwill. Goodwill is recognized by the acquirer as an asset from

the acquisition date;

⚫ No amortization of Goodwill. IFRS 3 prohibits the amortization of Goodwill. Instead Goodwill must be

tested for impairment at least annually in accordance with IAS 36 Impairment of Assets.

29

ACCA- FR 2021-2022 Part B-Chapter 3

⚫ Negative Goodwill. If the acquirer's interest in the net fair value of the acquired identifiable net assets

exceeds the cost of the business combination, that excess (sometimes referred to as Negative Goodwill)

must be recognized immediately in the income statement as a gain.

3.3.4 Internally Generated Goodwill

⚫ In some cases, expenditure is incurred to generate future economic benefits, but it does not meet the

recognition criteria of intangible asset. Such expenditure is often described as contributing to internally

generated goodwill. E.g.: advertising expenses.

⚫ Internally Generated Goodwill is not recognized as an asset because it is not an identifiable resource

(i.e. it is not separable nor does it arise from contractual or other legal rights) controlled by the entity

that can be measured reliably at cost.

3.3.5 Internally generated intangible assets

⚫ Generally, internally-generated intangible assets cannot be capitalised, as the cost associated with

these cannot be identified separately from the costs associated with running business.

The following internally generated items may never be recognized as assets:

Brands

Mastheads

Publishing titles

Customer lists

⚫ The production of internally generated assets is split into two phases: research and development.

Research costs: Original and planned investigation undertaken with the prospect of gaining new

scientific knowledge and understanding, which is charged to I/S as incurred.

Development costs: The application of research findings or other knowledge to a plan or design for

the production of' new or substantially improved materials, devices, products, processes, systems

or services before the start of commercial production or use.

Development costs are capitalized if they meet the criteria as follows:

• Technically feasible;

• Intention to complete;

• The availability of adequate technical, financial and other resources to complete;

• Ability to use or sell;

• Generation of future economic benefits: there must either be a market or an internal use for it;

• Ability to reliably measure the attributable expenditure on the project.

It is only expenditure incurred after the recognition criteria have been net which should be

recognized as an asset. Development expenditure recognized as an expense in P/L cannot

subsequently be reinstated as an asset.

30

ACCA- FR 2021-2022 Part B-Chapter 3

3.3.6 Acquisition in a Business Combination - In-process Research and Development

A research and development project acquired in a business combination is recognized as an asset at cost,

even if a component is research. Subsequent expenditure on that project is accounted for as any other

research and development cost (expensed except to the extent that the expenditure satisfies the criteria

in IAS 38 for recognizing such expenditure as an intangible asset).

3.3.7 Measurement after initial recognition

Two choices:

⚫ Cost model (more commonly used in practice): The accounting treatment is that intangible assets

should be carried at cost less amortization and any impairment losses.

⚫ Revaluation model: Intangible assets may be carried at a revalued amount (based on fair value) less

any subsequent amortization and impairment losses only if fair value can be determined by reference

to an active market. Such active markets are expected to be uncommon for intangible assets. Examples

where they might exist:

Milk quotas

Stock exchange seats

Taxi medallions

3.3.8 Amortisation

An entity must assess whether the useful life of an intangible asset is finite or indefinite.

With a finite useful life • Should be amortized on the pattern in which the asset's future

economic benefits are consumed.

• If such a pattern cannot be predicted reliably, the straight-line method

• Residual value assumed to be zero

With an indefinite useful

life

• Not amortized.

• Instead an impairment review must be carried out at least annually.

• The useful life of an intangible asset that is not amortized must be

reviewed each period to ensure that the life is still indefinite.

3.3.9 Disclosure

The same as IAS 16

Example 1

Which of the items will be recognized as intangible assets in the statement of financial position at the reporting

date?

(i) Licenses that are acquired from government;

(ii) Customer relationship that brings significant benefit to the business;

(iii) Self-owned trademarks;

(iv) Software that is acquired from outsiders and limited for 2-year use;

A (ii) and (iii)

B all four

C (i) and (ii)

D (i) and (iv)

31

ACCA- FR 2021-2022 Part B-Chapter 3

Example 2 (Referred to Jun 2015 Q2)

Which of the following statements relating to intangible assets is true?

(此题为综合考题,主体考核 IAS 38,穿插 IAS 36 内容(选项 D), 建议 IAS 36 学习后再次练习)

A All intangible assets must be carried at amortised cost or at an impaired amount; they cannot be revalued

upwards.

B The development of a new process which is not expected to increase sales revenues may still be recognised as

an intangible asset.

C Expenditure on the prototype of a new engine cannot be classified as an intangible asset because the prototype

has been assembled and has physical substance.

D Impairment losses for a cash generating unit are first applied to goodwill and then to other intangible assets

before being applied to tangible assets.

Example 3

Skyline is a company which commenced the development stage of a project to produce a new software on 1 October

20X4. The total expenditure of $60,000 incurred until the project was finished on 31 March 20X5 when the software

went into immediate production. The software became feasible on all aspects on 1 January 20X5. The software’s

estimated life span is five years. Skyline’s financial year end is 30 June. Time apportion is applicable when necessary.

What amount will be shown on Skyline’s statement of profit or loss for Development costs, including any

amortization for the year ended 30 June 20X5.

A $60,000

B $30,000

C $31,500

D $1,500

4. IAS 36 Impairment of assets

The objective of IAS 36 Impairment of assets is to set rules to ensure that the assets of an enterprise are carried

at no more than their recoverable amount (i.e. value to the business).

4.1 Definitions

⚫ Impairment: An asset has been impaired if its carrying value in the balance sheet exceeds its recoverable

amount.

⚫ Recoverable amount: It is the greater of fair value less cost to sell and value in use (future cash flows

generated by the asset discounted at a pre-tax market determined rate which allows for the risks specific to

the asset).

4.1.1 Measurement of FV less cost to sell / net selling price

⚫ Fair value is measured by following sequence:

Price in a binding sales agreement

Active market price

To estimate FV using best estimate (no active market)

⚫ Costs of disposal are the direct added costs only (not existing costs or overhead).

32

ACCA- FR 2021-2022 Part B-Chapter 3

4.1.2 Measurement of value in use

⚫ The discounted present value of estimated future cash flows expected to arise from the continuing use

of an asset, and from its disposal at the end of its useful life.

⚫ The calculation should reflect the following elements:

An estimate of the future cash flows;

Discount rate should be the pre-tax rate that reflects time value of money and the risks specific to

the asset. 4.2 Indications of impairment

The first step in applying IAS 36 is that at each balance sheet date, an enterprise should assess whether there

are any indications that the value of an asset may be impaired. You should think about any external or internal

factors that would affect either the selling price of the asset or the value that we can get out of it through using

it.

4.2.1 External sources of information

⚫ The asset's market value has declined more than expected.

⚫ Changes in the technological, market, economic or legal environment have had an adverse effect on

the enterprise.

⚫ Interest rates have changed, thus increasing the discount rate used in calculating the asset's value in

use.

⚫ The carrying amount of the net assets of the entity is more than its market capitalisation.

4.2.2 Internal sources of information

⚫ There is evidence of obsolescence or damage of the asset.

⚫ Changes in the way the asset is used have occurred or are imminent.

⚫ Evidence is available from internal reporting that indicates that the economic performance of an asset

is, or will be, worse than expected.

Even if there are no indications of impairment, the following asset must always be tested annually for

impairment.

⚫ Goodwill acquired in a business combination (see IFRS 3)

⚫ An intangible asset with an indefinite useful life (see IAS 38)

⚫ An intangible asset not yet available for use (see IAS 38)

4.3 Recognition and measurement of an impairment

⚫ If there is no indication of impairment then no further action need be taken. If there is an indication of

impairment, the recoverable amount should be calculated and any impairment loss should be immediately

recognized in the income statement.

⚫ The only exception to this is if the impairment reverses a previous gain taken to the revaluation reserve in

which case the impairment will be taken first to the revaluation reserve until the revaluation gain is reversed

and then to the income statement.

33

ACCA- FR 2021-2022 Part B-Chapter 3

4.4 Cash-generating units (CGUs)

⚫ In practice, cash flows belong to groups of assets rather than to individual assets. For example, a factory