101_2013_3_e

DESCRIPTION

facTRANSCRIPT

FAC1601/101/3/2013

DEPARTMENT OF FINANCIAL ACCOUNTING

FAC1601: FINANCIAL ACCOUNTING REPORTING 1

TUTORIAL LETTER 101/3/2013 (SEMESTERS 1 and 2)

This tutorial letter contains important information about this module

FAC1601/101/3/2013

2

CONTENTS

1. Introduction and welcome ...................................................................................................... 3

2. Purpose and outcomes of the module ..................................................................................... 3

3. Communication with your lecturers ......................................................................................... 4

4. Communication with the university .......................................................................................... 4

5. Study material ......................................................................................................................... 4

5.1 Inventory letter .................................................................................................................. 4 5.2 Study material .................................................................................................................. 5

6. Student support services......................................................................................................... 5

6.1 Contact with fellow students ............................................................................................. 5 6.2 Discussion classes........................................................................................................... 6

7. Assessment

7.1 Assignments and learning ................................................................................................ 6 7.2 General remarks .............................................................................................................. 6 7.3 Feedback on assignments ............................................................................................... 7 7.4 Study process .................................................................................................................. 7 7.5 Important aspects regarding assignments ........................................................................ 8 7.6 Finality of the due dates ................................................................................................... 9 7.7 Assessment of assignments ............................................................................................ 9

8. Examinations

8.1 Examination admission .................................................................................................... 9 8.2 Year-mark and final examination mark ............................................................................. 9 8.3 Examination period ........................................................................................................ 10 8.4 Examination paper ......................................................................................................... 10 8.5 Previous examination paper ........................................................................................... 11 8.6 Tutorial letter with information on the examination ......................................................... 11

9. Proposed study programme for 2013 .................................................................................... 11

9.1 First semester ................................................................................................................ 11 9.2 Second semester ........................................................................................................... 11

ANNEXURE A: COMPULSORY ASSIGNMENT ....................................................................... 13

ASSIGNMENT 01: (FIRST SEMESTER 2013) .................................................................... 13

ANNEXURE B: COMPULSORY ASSIGNMENT ....................................................................... 20

ASSIGNMENT 02: (FIRST SEMESTER 2013) .................................................................... 20

ANNEXURE C: COMPULSORY ASSIGNMENT ....................................................................... 28

ASSIGNMENT 01: (SECOND SEMESTER 2013) ............................................................... 28

ANNEXURE D: COMPULSORY ASSIGNMENT ....................................................................... 36

ASSIGNMENT 02: (SECOND SEMESTER 2013) ............................................................... 36

FAC1601/101/3/2013

3

1. Introduction and welcome

We are pleased to welcome you to this module and hope that you will find it both interesting and rewarding. We will do our best to make your study of this module successful. You will be well on your way to success if you start studying early in the semester and resolve to do the assignments

properly.

You will receive a number of tutorial letters during the year. A tutorial letter is our way of

communicating with you about teaching, learning and assessment.

This tutorial letter contains important information about the scheme of work, resources and assignments for this module. We urge you to read it carefully and to keep it at hand when working through the study material, preparing the assignments, preparing for the examination and

addressing questions to your lecturers.

Please read Tutorial Letter 301 in combination with this tutorial letter as it gives you an idea of

generally important information when studying at a distance and within a particular College.

In this tutorial letter, you will find the assignments and assessment criteria as well as instructions on the preparation and submission of the assignments. It also provides all the information you need with regard to the prescribed study material and other resources and how to obtain them. Please study this information carefully and make sure that you obtain the prescribed material as

soon as possible.

Right from the start we would like to point out that you must read all the tutorial letters you receive during the semester immediately and carefully, as they always contain important and,

sometimes, urgent information. You will also find useful information of a general nature in Tutorial Letter 301 and in the booklet mySTUDIES@Unisa. Having read through these, you should be

well prepared to begin.

We hope that you will enjoy this module and wish you all the best!

2. Purpose and outcomes of the module

The purpose of this module is to introduce students to financial accounting and reporting referring to some of the International Accounting Standards issued by the International Accounting Standards Board. In this course the focus of financial reporting and the analysis of financial statements are on partnerships and close corporations. You must also be able to record the accounting entries for the formation of, admittance to, retirement or death of a partner and the liquidation of partnerships. Further, you must be able to record the accounting entries to the capital structure of companies, be able to record the transactions relating to businesses with branches. Lastly, you must be able to prepare calculations relating to the time value of money.

FAC1601/101/3/2013

4

3. Communication with your lecturers

The lecturers responsible for this module:

Mr MT Hlongoane Mrs FM Osman Mr A Eysele Mr J van Staden Mrs B Ntoyanto-Ceki

Module Telephone Number: 012 429 4176 Module E-mail Address: [email protected]

All queries that are not of a purely administrative nature but are about the content of this module should be directed to us. Please have your study material with you when you contact us.

Email and telephone numbers are included above but you might also want to write to us. Letters should be sent to:

The module leader (FAC1601) Department of Financial Accounting PO Box 392 UNISA

0003

NB: Letters to lecturers may not be enclosed with or inserted into assignments.

4. Communication with the university

If you need to contact the university about matters not related to the content of this module, please consult the publication mySTUDIES@Unisa, which you received with your study material. This

brochure contains information on how to contact the university (e.g. to whom you can write for different queries, important telephone and fax numbers, addresses and details of the times certain facilities are open).

5. Study material

5.1 Inventory letter

You should have received an inventory letter telling you what you have received in your study

package and also showing items that are still outstanding. Also see the brochure entitled

mySTUDIES@Unisa.

Check the study material that you have received against the inventory letter. You should have

received all the items listed in the letter, unless there is a statement like “out of stock” or “not

available”. If any item is missing, follow the instructions on the back of the inventory letter without

delay.

FAC1601/101/3/2013

5

PLEASE NOTE

Your lecturers cannot help you with missing study material. For enquiries about your study

material, please contact the UNISA despatch department by sending an SMS to 43579 or by

e-mail at [email protected].

5.2 Study material

The Department of Despatch should supply you with the following study material for this module:

One study guide

Tutorial Letters 101 and 301 at registration and others later

Apart from Tutorial Letters 101 and 301, you will also receive other tutorial letters during the semester. These tutorial letters will not necessarily be available at the time of registration, but will be despatched to you as soon as they are available or needed (for instance, for feedback on assignments).

If you have access to the internet, you can view the study guides and tutorial letters for the modules for which you are registered on the university‟s online campus, myUnisa, at

http://myunisa.ac.za.

Prescribed textbook

Your prescribed textbook for this module is:

About Financial Accounting, Volume 2, 4th Edition by Berry PR, et al. LexisNexis

Butterworths. Durban. 2011.

Please consult the list of official booksellers and their addresses listed in mySTUDIES@Unisa. If you have any difficulty obtaining books from these bookshops, please contact the Prescribed Books Section.

6. Student support services

For information on the various student support systems and services available at Unisa (e.g. student counseling, tutorial classes, language support), please consult the publication mySTUDIES@Unisa, which you received with your study material.

6.1 Contact with fellow students

6.1.1 Study groups

It is advisable to have contact with fellow students. One way to do this is to form study groups.

The addresses of students in your area may be obtained from the following department:

Directorate: Student Administration and Registration PO Box 392 UNISA 0003

FAC1601/101/3/2013

6

6.1.2 myUNISA

If you have access to a computer that is linked to the internet, you can quickly access resources and information at the university. The myUnisa learning management system is Unisa's online

campus that will help you to communicate with your lecturers, with other students and with the

administrative departments of Unisa – all through the computer and the internet.

To go to the myUnisa website, start at the main Unisa website, http://www.unisa.ac.za, and then click on the “Login to myUnisa” link on the right-hand side of the screen. This should take you to

the myUnisa website. You can also go there directly by typing http://my.unisa.ac.za.

Please consult the publication mySTUDIES@Unisa, which you received with your study material,

for more information on myUnisa.

6.2 Discussion classes

Group discussions, offered by the lecturers of module FAC1601, will be held at predetermined venues during each semester. You will be notified of the dates, times and venues of these

classes.

The abovementioned discussion classes are the only official lectures offered by the lecturers of module FAC1601. Lectures offered by private organisations or persons are not the responsibility of the Department of Financial Accounting at Unisa. Lecturers (or the Department of Financial Accounting) should not be consulted with enquiries in this regard.

7. Assessment

7.1 Assignments and learning

Assignments are seen as part of the learning process for this module. As you do the assignment, study the reading text, consult other resources, discuss the work with fellow students or tutors or do research, you are actively engaged in learning. Looking at the assessment criteria given for each assignment will help you to understand what is required of you more clearly.

7.2 General remarks

Enquiries about assignments (e.g. whether or not the university has received your assignment or the date on which an assignment was returned to you) must be directed to the assignments department. This department can be reached by sending an SMS to 43584 or by e-mail at [email protected]. You might also find information on myUNISA. To go to the myUnisa

website, start at the main Unisa website, http://www.unisa.ac.za, and then click on the „login to myUnisa link under the myUnisa heading on the screen. This should take you to the myUnisa

website. You can also go there directly by typing http://my.unisa.ac.za.

Assignments should be addressed to:

The Registrar (Assignments) PO Box 392 UNISA 0003

You may submit written assignments and assignments done on mark-reading sheets either by post or electronically via myUNISA. Assignments may not be submitted by fax or email. For detailed

information and requirements as far as assignments are concerned, see the brochure mySTUDIES@Unisa, which you received with your study material.

FAC1601/101/3/2013

7

To submit an assignment through myUNISA:

Go to myUnisa.

Log in with your student number and password.

Select the module.

Click on assignments in the menu on the left.

Click on the assignment number you want to submit.

Follow the instructions on the screen.

7.3 Feedback on assignments

You will receive the correct answers automatically for multiple-choice questions. Feedback on compulsory assignments will be sent to all students registered for this module in a follow-up

tutorial letter, and not only to those students who submitted the assignments. The tutorial letter number will be 201, 202, etc.

As soon as you have received the feedback, please work through it. The assignments and the feedback on these assignments constitute an important part of your learning and should help you to be better prepared for the next assignment and the examination.

7.4 Study process

You may encounter fewer problems when you work as follows:

Paragraph 8 of this tutorial letter sets out the suggested study programme for semester 1 and 2. First semester students: refer to paragraph 8.1 and second semester students: refer to paragraph 8.2.

Study the relevant study units of the Study Guide for assignment 01. Do all the exercises in the study guide and make sure that you understand the contents of the study material.

Do assignment 01 and send it to UNISA for marking. Remember, the submission of assignment 01 is compulsory for examination admission and contributes to your year

mark (refer to paragraph 6).

Study the relevant study units of the Study Guide for assignment 02 and do the assignment. Remember, the submission of assignment 02 is compulsory and

contributes to your year mark (refer to paragraph 6).

After completing an assignment, carry on with the study programme. Do not wait for the

suggested solution or for the return of the marked assignment.

Students often fail to plan their studies properly in order to achieve specific study goals at predetermined dates. This leads to a haphazard approach to studying and the use of ineffective study techniques.

The study programme for each semester is herein provided to assist you in this regard. The programme indicates the dates during which certain sections of the study material should be studied, as well as the dates by which the compulsory assignments should be completed.

FAC1601/101/3/2013

8

The study programme is based on the following assumptions:

That study will commence on either 15 January 2013 for the first semester or 1 July 2013 for the second semester and that the course should be completed leaving sufficient time for revision.

That you should study at least 6 hours per week. We are of the opinion that this is within your reach.

We are convinced that, if you adhere to the suggested programme, you should be able to master the subject. It is very important that the subject matter covered in the study units should be mastered and not just be skimmed. If you happen to register late or fall behind with this

programme, extra effort on your part will be necessary.

Appendix A and B contains the compulsory assignment 01 and 02 for students who are registered for FAC1601 in the first semester.

Appendix C and D contains the compulsory assignment 01 and 02 for students who are registered for FAC1601 in the second semester.

Please note that these assignments are not the same. You must ensure that you submit the

assignments which pertain to the semester that you are registered in for FAC1601.

IF YOU ARE REGISTERED FOR FAC1601 IN THE SECOND SEMESTER YOU CANNOT SUBMIT ANY ASSIGNMENTS DURING THE FIRST SEMESTER.

ASSIGNMENTS INCORRECTLY SUBMITTED WILL RETURNED UNMARKED

7.5 Important aspects regarding assignments

There are 4 assignments for this module:

Assignment 01 is a multiple choice assignment that is compulsory and contributes 50% towards your year mark. It is important to note that if you do not submit this assignment you will not be admitted to the examination;

Assignment 02 is a multiple choice assignment that is also compulsory, and contributes 50% towards your year mark;

Assignments 03 and 04 are long question assignments. These assignments must NOT be submitted to UNISA for marking but forms an important part of your study material and exam questions will definitely be set on these sections.

Please keep copies of assignments submitted through myUnisa as this is proof that you submitted

the assignment.

Assignments constitute an integral part of the tutorial matter. Study material on which assignments are based is given in Annexure A (for students registered for the first semester) or Annexure C (for students registered for the second semester). Assignments and tutorial letters must also be studied for examination purposes.

FAC1601/101/3/2013

9

7.6 Finality of the due dates

The receipt of assignments after the due date disrupts our marking programme and the uncontrolled submission of assignments creates administrative problems. No extension will be granted for the submission of assignments and regrettably requests for the extension of the due date will NOT be considered.

7.7 Assessment of assignments

Although students may work together when preparing assignments, each student must submit his or her own individual assignment. It is unacceptable for students to discuss the answers on myUnisa. That is copying (a form of plagiarism) and you may be penalised or subjected to

disciplinary proceedings by the university.

8. Examinations

For general information and requirements as far as assignments are concerned, see the brochure mySTUDIES@Unisa, which you received with your study material.

8.1 Examination admission

For students to fully benefit from our formative tuition and assessment, the Management of the university has taken a decision to introduce two compulsory assignments in all modules to be submitted by set due dates. Submission of the first compulsory assignment by its due date will give a student admission to the examination in the particular module and the mark obtained for that assignment will contribute towards the final mark for that module. The second assignment is also

compulsory and contributes equally to the final mark.

Please ensure that the compulsory assignments reaches the University before the due date as

late submission of assignment 01 will result in you not being admitted to the examination.

8.2 Year-mark and final examination mark

The year-mark contribution towards the final examination mark is calculated as follows:

50% of the mark obtained for assignment 01

Plus

50% of the mark obtained for assignment 02

If you only submit assignment 01, your year mark will be 50% of the mark obtained for this assignment. This will then be your year mark out of a possible 100%. If, for example, you obtain

80% for assignment 01 and 0% for assignment 02, your year mark will be 40%.

According to university policy you require a sub-minimum of 40% in the examination before your year mark is taken into consideration. In other words, if you do not obtain at least 40% in the examination, you will automatically fail, and your final mark will be the mark you obtained in the

examination.

FAC1601/101/3/2013

10

A final mark of 50% is required to pass this module. This final mark is calculated as follows:

(10% x of the year mark) + (90% x mark obtained in the examination)

Example:

A B C D

Average of marks for

assignment 1 & 2

(Year mark)

Year mark contribution to

final mark at 10%

Exam mark

contribution required to pass

(50% minus year mark

contribution)

Minimum exam mark required to

pass

(C 0,9)

Student 1 100% 10% 40% 45%

Student 2 70% 7% 43% 48%

Student 3 50% 5% 45% 50%

Student 4 30% 3% 47% 52%

Student 5 20% 2% 48% 53%

Student 6 10% 1% 49% 54%

Student 7 0% 0% 50% 56%

If you obtain between 40% and 49% as a final mark, you will be allowed to write a supplementary examination. The supplementary examination will be written at the end of the next semester. This means that if you qualify for a supplementary examination in May/June, you will write the FAC1601 paper in October/November. Similarly, students who qualify for a supplementary examination in October/November will write this paper in May/June of the following year. A student may,

however, write only one supplementary examination per enrolment.

If, for any reason, you transfer your exam period for FAC1601 to a following semester, you need to submit Assignment 01 and 02 before the due date in the semester for which you originally registered for the course. The year mark you obtain will then be carried forward to the next semester because you will not be allowed to submit any assignments in the semester to which you have changed. By applying to have your semester changed to a following semester, in effect, you are applying for an aegrotat examination. However, you still need a year mark that will be taken into account as explained above – hence the need to submit the compulsory assignments in the

semester for which you originally registered.

8.3 Examination period

This module is offered in a semester period of 15 weeks. This means that if you are registered for the first semester, you will write the examination in May/June 2013 and the supplementary examination will be written in October/November 2013. If you are registered for the second semester, you will write the examination in October/November 2013 and the supplementary examination will be written in May/June 2014.

During the semester, the Examination Section will provide you with information regarding the examination in general, examination venues, examination dates and examination times. This information can also be obtained from the myUnisa site. Click on Examinations when you are

logged into the site.

8.4 Examination paper

At the end of the semester you will be required to write a two hour examination paper. No theoretical or multiple choice questions will be asked. You will only be required to apply the theoretical knowledge acquired in the questions asked. Exam questions are set on the content of the whole course – not only on assignments 1 and 2.

FAC1601/101/3/2013

11

You are advised to consult the examination time-table timeously in order to plan your revision programme accordingly. Please start early to avoid cramming at the last moment.

8.5 Previous examination paper

The May/June 2012 examination paper will be included in one of the tutorial letters that will be issued for this module. We advise you, however, not to focus only on this examination paper as your only source in your preparation for the examination as the content of examination paper changes from year to year. You may, however, accept that the type of questions that will be asked in the examination will be similar to those asked in the activities in your study guide and in the assignments.

8.6 Tutorial letter with information on the examination

To help you in your preparation for the examination, you will receive a tutorial letter that will explain the format of the examination paper and set out what and how to study for examination purposes.

9. Proposed study programme for 2013

9.1 First semester

DATE STUDY MATERIAL AND ASSIGNMENTS

± 14/1 to 15/2 Study: Study units 1 to 4 ± 16/2 to 18/2 Do Assignment 01 (compulsory assignment): Due date 11/03/2013 ± 18/2 Submit Assignment 01 (NB: DO NOT WAIT UNTIL 11/03/2013) ± 18/2 to 11/3 Study: Study units 5 to 7 ± 12/3 to 18/3 Do and mark Assignment 03 (do not submit this assignment) ± 19/3 to 21/3 Do Assignment 02 (compulsory assignment): Due date 08/04/2013 ± 25/3 Submit Assignment 02 (NB: DO NOT WAIT UNTIL 08/04/2013) ± 25/3 to 15/4 Study: Study units 8 to 10 ± 16/4 to 19/4 Do and mark Assignment 04 (do not submit this assignment) The solutions to Assignments 03 and 04 are provided in the same tutorial letter

20/4 to examination Revision

During May/June 2013: EXAMINATION

9.2 Second semester

DATE STUDY MATERIAL AND ASSIGNMENTS

± 1/7 to 31/7 Study: Study units 1 to 4 ± 1/8 to 3/8 Do Assignment 01 (compulsory assignment): Due date 19/08/2013 ± 5/8± Submit Assignment 01 (NB: DO NOT WAIT UNTIL 19/08/2013) ± 5/8 to 18/8 Study: Study units 4 to 7 ± 19/8 to 25/8 Do and mark Assignment 03 (do not submit this assignment) ±26/8 to 29/8 Do Assignment 02 (compulsory assignment): Due date 09/09/2013 ± 30/8 Submit Assignment 02 (NB: DO NOT WAIT UNTIL 09/09/2013) ±31/8 to 20/9 Study: Study units 8 to 10 ±21/9 to 25/9 Do Assignment 04 (do not submit this assignment) The solutions to Assignments 03 and 04 are provided in the same tutorial letter

26/9 to examination Revision

During October/November 2013: EXAMINATION

FAC1601/101/3/2013

12

We hope that you will enjoy this module and we wish you success with your studies.

Kind regards

Mr M Hlongoane Mrs FM Osman Mr A Eysele Mr J van Staden Mrs B Ntoyanto-Ceki

LECTURERS: FINANCIAL ACCOUNTING REPORTING 1 - MODULE 2 (FAC1601)

FAC1601/101/3/2013

13

ANNEXURE A: COMPULSORY ASSIGNMENT

ASSIGNMENT 01: (FIRST SEMESTER 2013)

UNIQUE NO: 678304

DUE DATE: 11 MARCH 2013

1. This assignment must be answered on a mark-reading sheet if submitted by post. It can also be submitted electronically through myUnisa.

2. Before answering this assignment, please read paragraphs 7 and 8 of this tutorial letter.

3. This assignment covers study units 1 – 4 of the study guide.

4. We cannot grant any extension for the late submission of this assignment since the due date is set in accordance with the marking date of this assignment. Regrettably, no correspondence or telephone conversations will be conducted in this regard.

5. Important aspects regarding multiple-choice assignments answered on a mark-reading sheet

For detailed information and requirements as far as assignments are concerned, see mySTUDIES@Unisa which you received with your study package.

Work carefully through the relevant tutorial matter before you do the assignment.

Calculate your answer on a separate piece of paper before completing the mark-reading sheet.

REMEMBER:

There is only one correct answer for each question. Do not make more than one

mark per question.

All questions are equal in value.

Indicate your student number correctly.

Indicate the assignment number correctly.

Indicate the unique assignment number for Assignment 01 correctly. Every

assignment which is marked by the computer is given a unique number. The number contains information on the course code and the assignment number. When the computer reads the unique number, it classifies it as Assignment 01 for FAC1601 – first semester.

FOR HARD COPY SUBMISSION:

Only the provided mark-reading sheets may be used.

Colour in the correct block clearly with a HB pencil.

Do not colour outside the block, or colour in the block with a pen.

Do not make corrections with correction fluid.

Do not tear or fold the mark-reading sheet. Do not try to repair a torn mark-reading sheet with sticky tape – use another one.

Do not staple the mark-reading sheet to another piece of paper.

Do not submit answers on a written sheet of paper.

Send only your mark-reading sheet to the Assignments Division in the appropriate

envelope.

FAC1601/101/3/2013

14

ASSIGNMENT 01 - FIRST SEMESTER (continued)

Given information for questions 1 and 2 The following balances appeared in the accounting records of Tera Traders at 31 December 2012, the end of the financial year: Land and buildings at cost (land R700 000; buildings R500 000) R1 200 000 Vehicle at cost R 110 000 Equipment at cost R 106 000 Accumulated depreciation: Vehicle R 30 900 Accumulated depreciation: Equipment R 51 000

Additional information

1. Land and buildings were acquired on 1 February 2012.

2. On 30 June 2012, the business purchased a new vehicle at a cost of R65 000. This transaction is still to be recorded in the accounting records of the business.

3. On 31 October 2012, equipment purchased on 30 April 2010 was sold for R2 500 cash. A replacement equipment was purchased at a cost of R33 000 on 1 November 2012. Total depreciation for the year written off on equipment amounted to R10 474.

4. It is the accounting policy of Tera Trader to provide depreciation as follows:

Vehicles: According to the straight-line method, at 20% per annum, Equipment: According to the diminishing-balance method, at 25% per annum, Buildings: According to the straight-line method, at 2% per annum.

QUESTION 1

Which one of the following alternatives represents the correct amount of accumulated depreciation on equipment on 1 January 2012?

1. R33 673 2. R46 283 3. R46 303 4. R53 156

5. None of the above

QUESTION 2

Which one of the following alternatives represents the correct amount that must be disclosed as property, plant and equipment in the statement of financial position of Tera Traders as at 31 December 2012?

1. R1 309 433 2. R1 318 600 3. R1 361 433 4. R1 370 600 5. None of the above

FAC1601/101/3/2013

15

ASSIGNMENT 01 - FIRST SEMESTER (continued)

Given information for questions 3 and 4:

Straw and Berry are in a partnership trading as Strawberry Traders with a capital contribution of

R100 000 and R125 000 respectively. The financial year end of the partnership is 31 December.

In terms of the partnership agreement Straw and Berry are each entitled to R10 000 salary per month. Berry is also entitled to a commission calculated at 8% of total sales of the first eight months. Interest is calculated at 8% and 9% on the partner‟s capital and drawings accounts respectively. During the year the partnership recorded interest on drawings to the amount of

R4 530 and R6 470 for Straw and Berry respectively.

During the year the following amounts were withdrawn by the partners as salaries:

Straw R45 300

Berry R64 700

Current account balance as at 1 January 2012 amounted to R40 000 (Dr) for Straw and R30 000 (Cr) for Berry. The total comprehensive income for the year amounted to R800 000. Annual sales of Strawberry Traders amounted to R1 450 000 after a 50% increase in the last five

months of the year.

QUESTION 3

Which one of the following alternatives represents the correct amount available as partner‟s share

of total comprehensive income for the year ended 31 December 2012?

1. R420 304 2. R615 900 3. R636 633 4. R766 633 5. None of the above

QUESTION 4

Which one of the following alternatives represents the correct closing balance of the current account of Berry as at 31 December 2012? 1. R429 474 2. R467 248 3. R522 548 4. R594 770 5. None of the above

FAC1601/101/3/2013

16

ASSIGNMENT 01 - FIRST SEMESTER (continued)

Given information for questions 5 to 7:

Mell and Joey are in a partnership trading as MelJ Traders with a profit sharing ratio of 3:2 respectively. They decided to admit Lisa from 1 July 2013 and that the new partnership will trade as Mellisa J Traders. The following information is extracted from the accounting records of the

partnership on 30 June 2013, the end of the financial year:

R

Capital: Mell .................................................................................................................... 70 000 Capital: Joey ................................................................................................................... 65 000 Current account: Mell (Dr) ............................................................................................... 15 000 Current account: Joey ..................................................................................................... 30 000 Asset replacement reserve ............................................................................................. 60 000 Vehicles at cost ............................................................................................................... 125 000 Accumulated depreciation: Vehicle (1 July 2012) ............................................................ 31 000 Furniture at cost .............................................................................................................. 120 000 Accumulated depreciation: Furniture (1 July 2012) ......................................................... 27 600 Inventory ......................................................................................................................... 44 000 Bank ............................................................................................................................... 88 000

Additional information:

1. On 1 July 2013 Mell and Joey decided that they would relinquish a third of interest in the profits/losses to Lisa in the ratio of 6:4 respectively. Lisa contributed a vehicle worth R100 000, equipment worth R20 000 and R40 000 cash and thereby acquire a third interest in the equity of the new partnership.

2. The partnership provides depreciation as follows:

Vehicles: According to the straight-line method, at 20% per annum Furniture: According to the diminishing balance method, at 15% per annum

3. In preparation for Lisa‟s admission an appraiser made the following valuation on 1 July 2013:

Vehicles R 90 000 Furniture R100 000

Inventory R 24 000 QUESTION 5

Which one of the following alternatives represents the profit/loss made on the valuation adjustments? 1. R16 400 (Loss) 2. R21 460 (Profit) 3. R22 460 (Profit) 4. R31 600 (Loss) 5. None of the above

FAC1601/101/3/2013

17

ASSIGNMENT 01 - FIRST SEMESTER (continued)

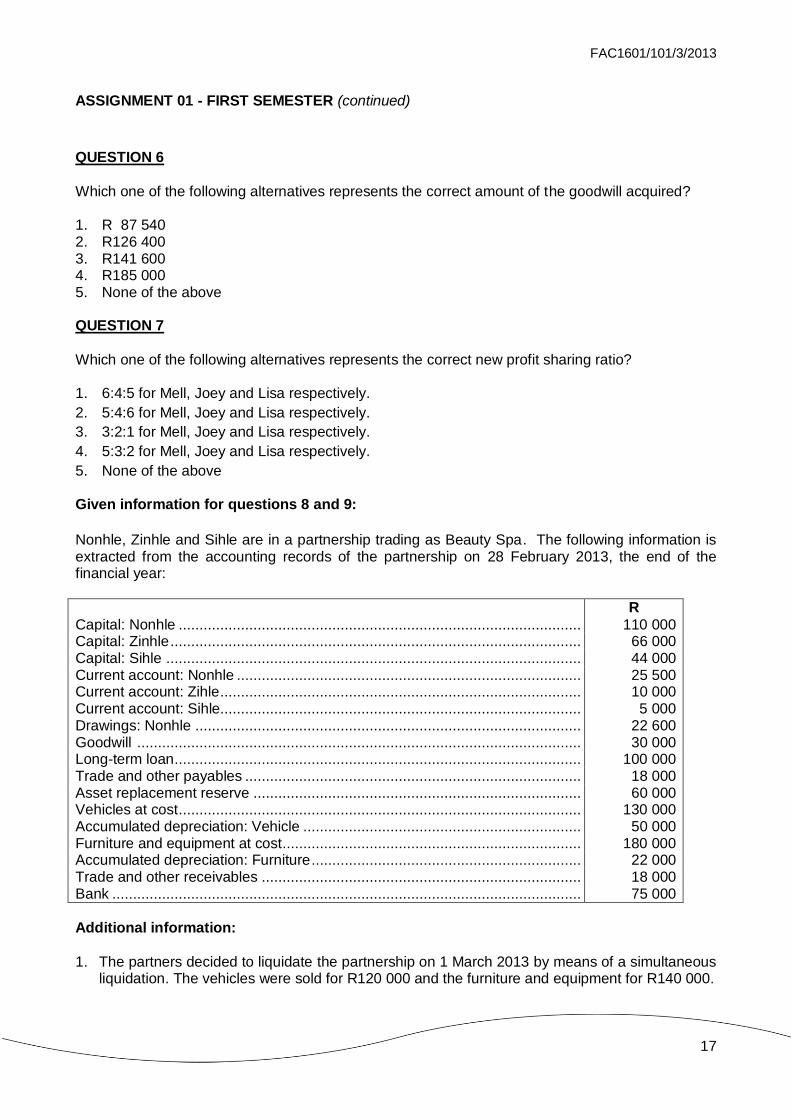

QUESTION 6

Which one of the following alternatives represents the correct amount of the goodwill acquired? 1. R 87 540 2. R126 400 3. R141 600 4. R185 000 5. None of the above

QUESTION 7

Which one of the following alternatives represents the correct new profit sharing ratio? 1. 6:4:5 for Mell, Joey and Lisa respectively.

2. 5:4:6 for Mell, Joey and Lisa respectively.

3. 3:2:1 for Mell, Joey and Lisa respectively.

4. 5:3:2 for Mell, Joey and Lisa respectively.

5. None of the above

Given information for questions 8 and 9:

Nonhle, Zinhle and Sihle are in a partnership trading as Beauty Spa. The following information is extracted from the accounting records of the partnership on 28 February 2013, the end of the financial year:

R

Capital: Nonhle ................................................................................................. 110 000 Capital: Zinhle ................................................................................................... 66 000 Capital: Sihle .................................................................................................... 44 000 Current account: Nonhle ................................................................................... 25 500 Current account: Zihle ....................................................................................... 10 000 Current account: Sihle....................................................................................... 5 000 Drawings: Nonhle ............................................................................................. 22 600 Goodwill ........................................................................................................... 30 000 Long-term loan .................................................................................................. 100 000 Trade and other payables ................................................................................. 18 000 Asset replacement reserve ............................................................................... 60 000 Vehicles at cost ................................................................................................. 130 000 Accumulated depreciation: Vehicle ................................................................... 50 000 Furniture and equipment at cost ........................................................................ 180 000 Accumulated depreciation: Furniture ................................................................. 22 000 Trade and other receivables ............................................................................. 18 000 Bank ................................................................................................................. 75 000

Additional information:

1. The partners decided to liquidate the partnership on 1 March 2013 by means of a simultaneous

liquidation. The vehicles were sold for R120 000 and the furniture and equipment for R140 000.

FAC1601/101/3/2013

18

ASSIGNMENT 01 - FIRST SEMESTER (continued)

2. Liquidation costs amounted to R2 000.

3. The loan and payables were settled at 5% discount.

4. Debtors settled their accounts at 10% discount.

QUESTION 8 Which one of the following alternatives represents the profit or loss on the liquidation account on

1 March 2013?

1. R24 100 2. R32 500 3. R42 300 4. R55 000

5. None of the above

QUESTION 9

Which one of the following alternatives represents the correct amount that must be recorded as the

settlement of the capital account of Nonhle?

1. R 67 500 2. R 90 000 3. R112 500 4. R139 950 5. None of the above

QUESTION 10

Johnny, Walker and Black were in partnership sharing profits or losses in the ratio of 5:3:2. The following information is extracted from the statement of financial position of the partnership as at

30 November 2012, the end of the financial year.

R

Capital: Johnny ............................................................................................................... 8 000 Capital: Walker ............................................................................................................... 7 000 Capital: Black .................................................................................................................. 4 400 Furniture ......................................................................................................................... 20 000 Equipment....................................................................................................................... 15 400 Loan: Johnny .................................................................................................................. 10 000 Creditors ......................................................................................................................... 8 000 Bank ............................................................................................................................... 2 000

The partners decided to dissolve the partnership on 1 December 2012 and to realise the assets at the best prices over a period of three months. Johnny agreed that his loan would only need to be repaid at the end of the third month together with interest at the rate of 12% per annum, provided that distributions were to be made monthly if possible but in such a way as to ensure that no partner would be called upon to make a refund.

FAC1601/101/3/2013

19

ASSIGNMENT 01 - FIRST SEMESTER (continued)

Assets sold and expenses incurred were as follows:

Carrying amount

Proceeds Realisation expenses incurred

R R R

At 31 December 2012 16 200 12 000 500 At 31 January 2013 12 400 9 900 400 At 28 February 2013 6 800 6 000 -

Which one of the following alternatives represents the correct amount that must be paid to Walker as cash distribution on 31 January 2013?

1. R2 590 2. R2 620 3. R2 680 4. R2 890 5. None of the above

END OF ASSIGNMENT 01 – FIRST SEMESTER

FAC1601/101/3/2013

20

ANNEXURE B: COMPULSORY ASSIGNMENT

ASSIGNMENT 02: (FIRST SEMESTER 2013)

UNIQUE NO: 810726

DUE DATE: 8 APRIL 2013

1. This assignment must be answered on a mark-reading sheet if submitted by post. It can also be submitted electronically through myUnisa.

2. Before answering this assignment, please read paragraphs 7 and 8 of this tutorial letter.

3. This assignment covers study units 5 – 7 of the study guide.

4. We cannot grant any extension for the late submission of this assignment since the

due date is set in accordance with the marking date of this assignment. Regrettably, no correspondence or telephone conversations will be conducted in this regard.

5. Important aspects regarding multiple-choice assignments answered on a mark-reading sheet

For detailed information and requirements as far as assignments are concerned, see mySTUDIES@Unisa which you received with your study package.

Work carefully through the relevant tutorial matter before you do the assignment.

Calculate your answer on a separate piece of paper before completing the mark-reading sheet.

REMEMBER:

There is only one correct answer for each question. Do not make more than one mark per question.

All questions are equal in value.

Indicate your student number correctly.

Indicate the assignment number correctly.

Indicate the unique assignment number for Assignment 01 correctly. Every assignment which is marked by the computer is given a unique number. The number contains information on the course code and the assignment number. When the computer reads the unique number, it classifies it as Assignment 01 for FAC1601 – first semester.

FOR HARD COPY SUBMISSION:

Only the provided mark-reading sheets may be used.

Colour in the correct block clearly with a HB pencil.

Do not colour outside the block, or colour in the block with a pen.

Do not make corrections with correction fluid.

Do not tear or fold the mark-reading sheet. Do not try to repair a torn mark-reading sheet with sticky tape – use another one.

Do not staple the mark-reading sheet to another piece of paper.

Do not submit answers on a written sheet of paper.

Send only your mark-reading sheet to the Assignments Division in the appropriate

envelope.

FAC1601/101/3/2013

21

ASSIGNMENT 02 - FIRST SEMESTER (continued)

Given information for questions 1 to 3:

Spring and Sommers are the only members of Vacation Rentals CC. They have an equal interest in the corporation and distribute profits accordingly. The following information is extracted from the accounting records of the CC as at 28 February 2013, the financial year-end of the corporation.

R

Member‟s contribution: Spring 60 000 Member‟s contribution: Sommers 40 000 Retained earnings (1 March 2012) 315 000 Land and buildings at cost 373 500 Equipment at cost 270 000 Accumulated depreciation: Equipment (1 March 2012) 97 200 Loan from member: Spring (1 March 2012) 46 900 Loan to member: Sommers 35 250 Inventory 49 656 Debtors control 265 300 Creditors control 252 050 Bank (Dr) 36 200 Mortgage 95 000 Investment (fixed deposit at FNZ Bank) 57 500 Interim profit distribution paid to members 21 000 Income received in advance 7 330 Prepaid expenses 2 500 Allowance for credit losses 24 515 SARS (Income tax) (Dr) 58 548 Profit before tax (before taking any applicable additional information into account) 249 459

Additional information: 1. Depreciation on equipment is calculated at 20 % per annum on the diminished balance and

must still be brought into account. 2. The mortgage was obtained on 31 May 2011 from ABC Bank at 25% interest per annum.

The interest payable has been paid and recorded correctly up to date. 3. A debtor who owed the business R15 000 was declared insolvent on 28 February 2013. It

was decided to write off his debt as irrecoverable. 4. The actual income tax for the financial year amounted to R86 500 and must still be recorded. 5. Provision must still be made for interest on loan from Spring. Interest is calculated at 20%

per annum on the opening balance of the loan and is payable on 1 March 2013.

6. On 20 February 2012, the members decided that an amount of R22 400 must be equally distributed to them on 28 February 2012 as a further profit distribution.

It was further agreed that these amounts will not be paid out in cash, but will remain in the

close corporation as loans from members. Forty percent of all the loans from the members must be repaid on 1 May 2012. The

balances of these loans are repayable in February 2017. All these loans are unsecured.

FAC1601/101/3/2013

22

ASSIGNMENT 02 - FIRST SEMESTER (continued)

7. Interest must be recorded on the loan accounts to members at 10% per annum on the opening balance of any existing loans as well as on any additional loans granted. On 31 August 2012, an additional loan of R12 500 was granted to Sommers and correctly accounted for in the books. Interest on the loans to members is capitalised. All loans are unsecured and immediately callable.

QUESTION 1

Which one of the following alternatives represents the correct amount that must be disclosed as retained earnings in the statement of financial position of Vacation Rentals CC as at 28 February 2013? 1. R375 565 2. R378 519 3. R384 945 4. R384 999 5. None of the above QUESTION 2

Which one of the following alternatives represents the correct balance of Loans to members of Vacation Rentals CC as at 28 February 2013? 1. R27 413 2. R35 250 3. R38 150 4. R38 663 5. None of the above

QUESTION 3 Which one of the following alternatives represents the correct amount to be disclosed as non–current liability of loans from members of Vacation Rentals CC as at 28 February 2013? 1. R27 720 2. R34 860 3. R41 580 4. R69 300 5. None of the above

FAC1601/101/3/2013

23

ASSIGNMENT 02 - FIRST SEMESTER (continued)

Given information for questions 4 and 5:

The following information pertains to Potter Ltd:

Potter Ltd was formed on 1 January 2012 with an authorised share capital of 55 000 ordinary

shares.

On 1 February 2012, the incorporators of the company subscribed to 5 000 ordinary shares at a deemed value of R5 000 and paid it in full. On 15 February 2012, the remaining shares were offered to the public. The board of the company deemed that a fair consideration for these share is

R62 500.

The full public issue is underwritten by Hogwarts Underwriters Ltd for a 1% underwriter‟s commission. The public subscribed to 45 000 shares and the full amounts payable were received on the closing date of 15 March 2012. All the shares were allotted on 18 March 2012 and all

transactions with the underwriter were concluded by 31 March 2012.

QUESTION 4

Which one of the following alternatives represents the correct balance of the Share Capital: Ordinary Shares account in the general ledger of Potter Ltd on 31 March 2012. 1. R61 250 2. R67 500 3. R78 320 4. R92 800 5. None of the above

QUESTION 5 Which one of the following alternatives represents the final amount paid to/by Hogwarts Underwriters Ltd on 31 March 2012 as final settlement of all underwriting transactions? 1. R 625 payable to Hogwarts Underwriters Ltd 2. R5 625 payable by Hogwarts Underwriters Ltd 3. R6 250 receivable by Hogwarts Underwriters Ltd 4. R5 625 payable to Hogwarts Underwriters Ltd

5. None of the above

FAC1601/101/3/2013

24

ASSIGNMENT 02 - FIRST SEMESTER (continued)

QUESTION 6

Penang Ltd had an issued share capital of 15 000 10% preference shares and 45 000 ordinary shares. Furthermore it had a credit balance in the retained earnings account of R15 000.

During a board meeting of Penang Ltd, it was decided that the company will issue capitalisation shares to the shareholders in the ratio of one capitalisation share for every five preference shares held, and one additional capitalisation share for every six ordinary shares held. The board of the company deemed that a fair consideration for the preference shares would be R3 000 and that of

the ordinary shares would be R7 500.

Which one of the following alternatives represents the correct number of capitalisation shares to be

issued of each class?

1. 600 preference share; 1 250 ordinary shares 2. 1 500 preference share; 4 500 ordinary shares 3. 2 000 preference share; 5 500 ordinary shares 4. 3 000 preference share; 7 500 ordinary shares 5. None of the above

QUESTION 7

The financial year of Guduza Ltd ends on the last day of February. The company has the following

share capital structure:

Authorised share capital:

200 000 ordinary shares

100 000 10% preference shares

Issued share capital:

90 000 ordinary shares, valued by the board of directors at R90 000 (75 000 of these shares remained unchanged for the full year while the remainder was allotted and issued on 1 July 2012); and 25 000 10% preference shares, issued at R2 per share (15 000 of these shares remained

unchanged for the full year while the remainder was allotted and issued on 1 September 2012).

On 15 February 2013, the board of Guduza Ltd declared an ordinary dividend of R0,25 per share payable during March 2013. The company‟s profit for the year ended 28 February 2013 amounted to R175 000. According to the company‟s solvency and liquidity test, it had sufficient cash

resources to pay the dividends to ordinary and preference shareholders.

FAC1601/101/3/2013

25

ASSIGNMENT 02 - FIRST SEMESTER (continued)

Which one of the following alternatives represents the correct amount of dividends payable by

Guduza Ltd as at 28 February 2013?

1. R22 500 2. R25 250 3. R26 500 4. R27 500 5. None of the above

Given information for questions 8 to 10:

The following information pertains to Spider CC:

SPIDER CC STATEMENT OF FINANCIAL POSITION AS AT 28 FEBRUARY 2013

2013 2012 ASSETS R R Non-current assets 129 300 50 000 Property, plant and equipment 129 300 50 000 Current assets 38 400 36 000 Inventories 12 000 10 200 Trade and other receivables 10 000 10 400 Prepayments (Insurance) 400 - Other financial assets 12 000 14 000 Cash and cash equivalents 4 000 1 400 Total assets 167 700 86 000

EQUITY AND LIABILITIES Total equity 152 000 69 800 Members‟ contributions 52 000 47 200 Retained earnings 100 000 22 600 Total liabilities 15 700 16 200

Non-current liabilities 5 200 4 200 Long-term borrowings 5 200 4 200 Current liabilities 10 500 12 000 Trade and other payables 8 000 10 000 Current tax payable 2 500 2 000 Total equity and liabilities 167 700 86 000

FAC1601/101/3/2013

26

ASSIGNMENT 02 - FIRST SEMESTER (continued)

SPIDER CC STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 2013

R Revenue 262 000 Cost of sales (130 000) Gross profit 132 000 Other income 6 600 138 600 Distribution, administrative and other expenses (30 800) Depreciation 2 000 Credit losses 4 500 Insurance expenses 2 600 Water and electricity 1 250 Salaries and wages 20 450 Finance costs (400) Interest on long-term loan 400 Profit before tax 107 400 Income tax expense (30 000) Profit for the year 77 400 Other comprehensive income for the year, net of tax – Total comprehensive income for the year 77 400

Additional information:

1. All sales and purchases are on credit.

2. The balance of the allowance for credit losses amounted to R2 000 and R1 800 for the financial year ending 2012 and 2013 respectively.

3. Other financial assets consists of shares purchsed in Mango Ltd.

4. An interim profit distribution of R2 800 was paid during the year.

5. Spider CC uses the direct method to prepare their statement of cash flows.

QUESTION 8

Which one of the following alternatives represents the amount that must be disclosed as cash receipts from customers in the statement of cash flows of Spider CC at 28 February 2013?

1. R257 700 2. R261 600 3. R262 000 4. R262 400 5. None of the above

FAC1601/101/3/2013

27

QUESTION 9

Which one of the following alternatives represents the amount that must be disclosed as cash paid to suppliers and employees in the statement of cash flows of Spider CC at 28 February 2013?

1. R154 250 2. R154 650 3. R155 050 4. R158 500 5. None of the above

QUESTION 10

Which one of the following alternatives represents the correct amount that must be disclosed as net cash generated from/(used in) operating activities in the statement of cash flows of Spider CC

at 28 February 2013?

1. R64 500 2. R71 400 3. R71 600 4. R80 300 5. None of the above

END OF ASSIGNMENT 02 – FIRST SEMESTER

FAC1601/101/3/2013

28

ANNEXURE C: COMPULSORY ASSIGNMENT

ASSIGNMENT 01: (SECOND SEMESTER 2013)

UNIQUE NO: 843058

DUE DATE: 19 AUGUST 2013

1. This assignment must be answered on a mark-reading sheet if submitted by post. It can also be submitted electronically through myUnisa.

2. Before answering this assignment, please read paragraphs 7 and 8 of this tutorial letter.

3. This assignment covers study units 1 – 4 of the study guide.

4. We cannot grant any extension for the late submission of this assignment since the

due date is set in accordance with the marking date of this assignment. Regrettably, no correspondence or telephone conversations will be conducted in this regard.

5. Important aspects regarding multiple-choice assignments answered on a mark-reading sheet

For detailed information and requirements as far as assignments are concerned, see mySTUDIES@Unisa which you received with your study package.

Work carefully through the relevant tutorial matter before you do the assignment.

Calculate your answer on a separate piece of paper before completing the mark-reading sheet.

REMEMBER:

There is only one correct answer for each question. Do not make more than one

mark per question.

All questions are equal in value.

Indicate your student number correctly.

Indicate the assignment number correctly.

Indicate the unique assignment number for Assignment 01 correctly. Every

assignment which is marked by the computer is given a unique number. The number contains information on the course code and the assignment number. When the computer reads the unique number, it classifies it as Assignment 01 for FAC1601 – second semester.

FOR HARD COPY SUBMISSION:

Only the provided mark-reading sheets may be used.

Colour in the correct block clearly with a HB pencil.

Do not colour outside the block, or colour in the block with a pen.

Do not make corrections with correction fluid.

Do not tear or fold the mark-reading sheet. Do not try to repair a torn mark-reading sheet with sticky tape – use another one.

Do not staple the mark-reading sheet to another piece of paper.

Do not submit answers on a written sheet of paper.

Send only your mark-reading sheet to the Assignments Division in the appropriate

envelope.

FAC1601/101/3/2013

29

ASSIGNMENT 01 - SECOND SEMESTER (continued)

Given information for questions 1 to 4 The following information appeared in the accounting records of Mali Traders at 31 December 2012, the end of the financial year:

R

Investment at cost 100 000 Buildings at cost 220 000 Furniture at cost 80 000 Accumulated depreciation: Buildings (1 January 2012) 20 000 Accumulated depreciation: Furniture (1 January 2012) 25 000 Debtors control 80 000 Allowance for credit losses 3 000 Credit losses 1 500

Additional information:

1. On 30 June 2012, the business purchased a new building at cost of R100 000.

2. On 30 September 2012, furniture with a cost price of R10 000 was traded in for a new one. The accumulated depreciation thereon was R6 000 on 1 January 2012. A replacement furniture was purchased for R35 000 on 1 October 2012 and a trade-in value of R4 000 on the old equipment was allowed for the purchase of the new furniture.

3. Depreciation must be provided for as follows:

Furniture: 20% per annum according to the diminishing balance method; and Building: 2% per annum according to straight line method.

4. A discount of 5% has been offered to Mr Moosa, a debtor owing the business R38 000, provided he settles his account on or before 31 January 2012.

5. The allowance for credit losses reflected a balance of R2 000 on 1 January 2012.

6. During the year the business received an amount of R1 500 in respect of a debt that had previously been written off as irrecoverable. The bookkeeper was unsure as to how to handle the matter and the transaction must still be recorded in the books of the business.

7. On 31 December 2012 the partnership learnt that a debtor owing the business R2 500 cannot be traced and it was decided to write off his debt as irrecoverable.

8. The investment consist of the following:

15 000 shares in Zama-Zama Ltd purchased at R4,00 per share. On

31 December 2012, it was established that the market value of these shares was

R4,06 per share.

10 000 shares in Super (Pty) Ltd purchased at R0,90 per share;

Fixed deposit at ABC Bank.

FAC1601/101/3/2013

30

ASSIGNMENT 01 - SECOND SEMESTER (continued)

QUESTION 1

Which one of the following alternatives represents the correct amount that must be disclosed as credit losses in the statement of profit or loss and other comprehensive income of Mali Traders for

the year ended 31 December 2012?

1. R2 000

2. R2 500

3. R3 500

4. R5 000

5. None of the above

QUESTION 2

Which one of the following alternatives represents the correct amount that must be disclosed as other income in the statement of profit or loss and other comprehensive income of Mali Traders for

the year ended 31 December 2012?

1. R1 500

2. R2 100

3. R2 400

4. R3 000

5. None of the above

QUESTION 3

Which one of the following alternatives represent the correct amount that must be disclosed as property, plant and equipment in the statement of financial position of Mali Traders as at 31 December 2012? 1. R249 650

2. R250 650

3. R255 000

4. R270 850

5. None of the above

QUESTION 4

Which one of the following alternatives represent the correct amount that must be disclosed as a total of current assets in the statement of financial position of Mali Traders as at 31 December 2012?

1. R134 100 2. R135 000 3 R136 000 4. R136 900 5. None of the above

FAC1601/101/3/2013

31

ASSIGNMENT 01 - SECOND SEMESTER (continued)

Given information for questions 5 and 6:

J&J Dealers is a partnership with partners James and Joel, who share profits and losses equally. The following information pertains to the business activities of the partnership for the year ended 28 February 2013:

R Capital: James 50 000 Capital: Joel 60 000 Current account: James (Dr) 2 000 Current account: Joel (Cr) 5 000 Long-term loan 40 000 Bank (Dr) 53 400 Inventory (1 March 2012) 80 500 Purchases 201 000 Profit on sale of equipment 105 General expenses 14 675

Additional information:

1. It is the policy of J&J Dealers to apply a mark-up of 20% on the selling price.

2. The partnership agreement provides for the following:

Interest on capital at 9% per annum,

Interest on current accounts at 7% per annum,

Salaries amount to R6 000 per annum for both partners,

A special bonus of 10% on the comprehensive income for the financial year after the adjustments of interest on capital and current accounts; and salaries is to be provided and shared by partners equally.

3. On 27 February 2013, defective inventory with a cost price of R500 was returned to the supplier. The supplier undertook to replace the inventory on 1 March 2013. This information must still be recorded in the books of the business.

4. The long-term loan bears an interest at a rate of 12% per annum payable on 30 June every year.

5. During the year each partner received R4 500 as a salary.

6. Inventory on hand at 28 February 2013 amounted to R61 000.

QUESTION 5

Which one of the following alternatives represents the correct amount of total comprehensive income for the year ended 28 February 2013?

1. R24 630 2. R24 730 3. R33 230 4. R35 630 5. None of the above

FAC1601/101/3/2013

32

ASSIGNMENT 01 - SECOND SEMESTER (continued)

QUESTION 6

Which one of the following alternatives represents the correct balance of the current account of James at 28 February 2013?

1. R12 560 2. R13 620 3. R14 060 4. R15 120 5. None of the above

Given information for questions 7 and 8:

Thembi and Lebo were in a partnership and traded as T&L Computers. They decided to admit Kgomotso to the partnership as from 1 January 2013. Kgomotso had to pay R60 000 for a 20% share in the fair value of the net assets of the new partnership that Thembi and Lebo will relinquish to Kgomotso according to their existing profit-sharing ratio. Kgomotso would also obtain a 20%

interest in the profit/loss of the new partnership that will trade as TLK Notebooks.

At 31 December 2012 the books of T&L Computers were closed off. At this date the following items appeared in the preliminary statement of financial position of the partnership of T&L Computers:

R

Capital: Thembi .......................................................................................................... 120 000

Capital: Lebo .............................................................................................................. 80 000

Current account: Thembi (Dr) ..................................................................................... 20 000

Current account: Lebo (Cr) ......................................................................................... 5 000

Asset replacement reserve ......................................................................................... 50 000

Land and buildings at cost .......................................................................................... 180 000

Accumulated depreciation: Buildings (1 January 2012) ............................................. 20 000

Inventory .................................................................................................................... 36 000

Debtors control ........................................................................................................... 24 000

Creditors control ......................................................................................................... 18 000

Bank (favourable) ....................................................................................................... 33 000

Additional information:

1. On 31 December 2012 a trade debtor who owes R3 000 was declared insolvent and his account must be written off as irrecoverable.

2. It is the policy of T&L to depreciate buildings at 5% per annum on straight line basis.

3. In preparation for the change in the ownership structure of the partnership, the following values were attached to the assets of T&L Computers:

Land and buildings - R152 000,

Inventory - R22 000.

FAC1601/101/3/2013

33

ASSIGNMENT 01 - SECOND SEMESTER (continued)

QUESTION 7

Which one of the following alternatives represents the correct balance of the capital account of Thembi prior to the formation of a new partnership and admission of Kgomotso?

1. R115 000

2. R118 600

3. R125 800

4. R133 000

5. None of the above

QUESTION 8

Which one of the following alternatives represents the correct new profit sharing ratio after the

admission of Kgomotso?

1. 4 : 4 : 2

2. 5 : 3 : 2

3. 6 : 4 : 3

4. 12 : 8 : 5

5. None of the above

QUESTION 9

Chris, Brown and Usher are partners in a music production firm, trading as CBU Music Factory, and they share profits and losses in the ratio of 5:2:1 respectively. They have considered to liquidate the partnership for quite some time, and received various offers for the land and buildings as well as for the furniture and equipment. Since they have decided to accept the most favourable of these offers, they planned to liquidate the partnership simultaneously on 1 July 2013. Mr David Cochrane a specialist lawyer on partnership was hired by the partners at a cost of R22 500 to handle the legal matters pertaining to the dissolution of the partnership. Before the liquidation entries were made, the trial balance of the partnership was prepared as follows:

CBU MUSIC FACTORY TRIAL BALANCE AT 1 JULY 2013

Debit Credit

R R

Capital - Chris ........................................................................................ Capital – Brown ...................................................................................... Capital – Usher ...................................................................................... Current account - Chris .......................................................................... Current account – Brown ........................................................................ Current account – Usher ........................................................................ Long-term loan at R&B Bank .................................................................. Creditors control ..................................................................................... Land and buildings at cost ...................................................................... Furniture and equipment at cost ............................................................. Accumulated depreciation: Furniture and equipment .............................. Bank .......................................................................................................

30 000

10 000

800 000 290 000

25 000

450 000 250 000 140 000

20 000

180 000

60 000

55 000

1 155 000 1 155 000

FAC1601/101/3/2013

34

ASSIGNMENT 01 - SECOND SEMESTER (continued)

On 1 July 2013 the following transactions with regard to the liquidation took place:

The land and buildings were sold for cash, R800 000; estate agent commission amounting to R35 000 was paid by the CBU Music Factory. Furniture and equipment with a carrying amount of R50 000 was taken over (not paid for immediately) by Brown at an agreed amount of R45 000, and the remaining furniture and equipment was sold at a profit of R25 000, cash. A discount of R5 000 was received on full settlement of the creditor‟s accounts. The long-term loan at R&B Bank was

settled in full and an early settlement fee of R2 500 was charged by the bank.

QUESTION 9

Which one of the following alternatives indicates the correct amount of profit/loss made on the

liquidation of CBU Music Factory?

1. R35 000 loss 2. R52 500 profit 3. R55 000 loss 4. R57 500 profit 5. None of the above

QUESTION 10

Maggie and Jiggs were in partnership sharing profits and losses in the ratio of 6:4. The following

information is extracted from the accounting records of the partnership on 30 June 2013:

R

Capital: Maggie 150 000 Capital: Jiggs 60 000 Inventory 180 000 Debtors control 39 000 Creditors control 45 000 Bank 36 000

On 1 July 2013 they decided to dissolve the partnership piecemeal. During the first two weeks of July 2013 inventory standing in the books at R120 000 was sold for R135 000 cash and the balance was donated to a local retirement home. An amount of R27 000 was collected for debtors

and expenses amounting to R7 500 were paid.

It was known that the maximum legal fees, payable once all assets have been liquidated, will not

exceed R4 500.

On 14 July 2013 each partner wishes to draw the maximum possible amount form the available cash but under no circumstances do they wish to risk having to make a refund.

FAC1601/101/3/2013

35

Which one of the following alternative represents the correct amount of settlement paid to Maggie

on 14 July 2013?

1. R108 600 2. R111 300 3. R115 800 4. R144 600 5. None of the above

END OF ASSIGNMENT 01 – SECOND SEMESTER

FAC1601/101/3/2013

36

ANNEXURE D: COMPULSORY ASSIGNMENT

ASSIGNMENT 02: (SECOND SEMESTER 2013)

UNIQUE NO: 869893

DUE DATE: 9 SEPTEMBER 2013

1. This assignment must be answered on a mark-reading sheet if submitted by post. It can also be submitted electronically through myUnisa.

2. Before answering this assignment, please read paragraphs 7 and 8 of this tutorial letter.

3. This assignment covers study units 5 – 7 of the study guide.

4. We cannot grant any extension for the late submission of this assignment since the

due date is set in accordance with the marking date of this assignment. Regrettably, no correspondence or telephone conversations will be conducted in this regard.

5. Important aspects regarding multiple-choice assignments answered on a mark-reading sheet

For detailed information and requirements as far as assignments are concerned, see mySTUDIES@Unisa which you received with your study package.

Work carefully through the relevant tutorial matter before you do the assignment.

Calculate your answer on a separate piece of paper before completing the mark-reading sheet.

REMEMBER:

There is only one correct answer for each question. Do not make more than one

mark per question.

All questions are equal in value.

Indicate your student number correctly.

Indicate the assignment number correctly.

Indicate the unique assignment number for Assignment 01 correctly. Every

assignment which is marked by the computer is given a unique number. The number contains information on the course code and the assignment number. When the computer reads the unique number, it classifies it as Assignment 01 for FAC1601 – second semester.

FOR HARD COPY SUBMISSION:

Only the provided mark-reading sheets may be used.

Colour in the correct block clearly with a HB pencil.

Do not colour outside the block, or colour in the block with a pen.

Do not make corrections with correction fluid.

Do not tear or fold the mark-reading sheet. Do not try to repair a torn mark-reading sheet with sticky tape – use another one.

Do not staple the mark-reading sheet to another piece of paper.

Do not submit answers on a written sheet of paper.

Send only your mark-reading sheet to the Assignments Division in the appropriate

envelope.

FAC1601/101/3/2013

37

ASSIGNMENT 02 - SECOND SEMESTER (continued)

Given information for questions 1 to 3:

The following information relates to Jimmy Shoe CC, a fashion retailer:

JIMMY SHOE CC TRIAL BALANCE AS AT 31 DECEMBER 2012

R

Member‟s contribution: Jimmy .................................................................................... 360 000

Member‟s contribution: Shoe ...................................................................................... 465 000

Asset replacement reserve – 1 January 2012 ............................................................ 150 000

Retained earnings – 1 January 2012 .......................................................................... 112 500

Long-term loan ........................................................................................................... 337 500

Land and buildings at cost .......................................................................................... 1 080 000

Machinery at cost ....................................................................................................... 600 000

Vehicles at cost .......................................................................................................... 225 000

Accumulated depreciation: Machinery ........................................................................ 120 000

Accumulated depreciation: Vehicles ........................................................................... 81 000

Investments at cost .................................................................................................... 120 000

Inventory .................................................................................................................... 75 000

Debtors control ........................................................................................................... 96 300

Creditors control ......................................................................................................... 48 000

Bank overdraft ............................................................................................................ 3 000

SARS (Income tax) (Cr) ............................................................................................. 37 800

Distribution to members ............................................................................................. 75 000

Profit for the year (before additional information) ........................................................ 556 500 Additional information:

1. The long-term loan was obtained on 30 April 2012 from MFL Bank. The interest on this loan is charged at a rate of 10% per annum payable on 30 June every year. The loan is unsecured and is repayable in five equal annual instalments, starting on 1 July 2013.

2. During a meeting held on 28 December 2012, the members approved that R90 000 of the profit for the year must be transferred to the asset replacement reserve.

3. On 1 September 2012, Jimmy, one of the members, made an additional capital contribution to the CC by transferring a vehicle with a carrying amount of R135 000 to Jimmy Shoe CC. On 1 October 2012 Mr Versace, the bookkeeper, was dismissed due to his incompetence. As a result no entries were made to record this transaction.

4. Jimmy Shoe CC offered a discount of 10% on an amount of R3 000 owed by a debtor provided the amount owing is paid before 31 January 2013.

FAC1601/101/3/2013

38

ASSIGNMENT 02 - SECOND SEMESTER (continued)

5. Depreciation (except for 5.2.2) was provided for as follows:

5.1 Machinery at 10% per annum according to the straight-line method. 5.2 Vehicles at 20% per annum according to the diminishing-balance method. 5.2.1 The only depreciation still to be provided for is the depreciation pertaining to the

vehicle that was acquired from Jimmy. 6. Investments consist of:

10 000 ordinary shares in Prada Ltd, purchased for R90 000 on 1 March 2011. On 31 December 2012 Prada Ltd declared a dividend of 30 cents per share, payable on 15 January 2013. On 31 December 2012, the fair value of shares held in Prada Ltd was determined at R10,00 per share.

R30 000 fixed deposit at Coastal National Bank. QUESTION 1

Which one of the following alternatives represents the correct amount to be disclosed as total equity in the statement of financial position of Jimmy Shoe CC as at 31 December 2012? 1. R1 625 200 2. R1 685 200 3. R1 747 200 4. R1 760 200 5. None of the above QUESTION 2 Which one of the following alternatives represents the correct amount to be disclosed as current assets in the statement of financial position of Jimmy Shoe CC as at 31 December 2012? 1. R164 000 2. R174 000 3. R274 000 4. R304 000 5. None of the above QUESTION 3

Which one of the following alternatives represents the correct amount to be disclosed as current liabilities in the statement of financial position of Jimmy Shoe CC as at 31 December 2012? 1. R111 300 2. R156 300 3. R173 175 4. R178 800 5. None of the above

FAC1601/101/3/2013

39

ASSIGNMENT 02 - SECOND SEMESTER (continued)

QUESTION 4