105 financial analysis for in-house counsel analysis for in-house lawyers financial statement...

TRANSCRIPT

ACC Europe’s 2007 Corporate Counsel University

This material is protected by copyright. Copyright © 2007 various authors, the Association of Corporate Counsel (ACC), and ACC Europe. Materials may not be reproduced without the consent of ACC.

Reprint permission requests should be directed to Julienne Bramesco at ACC: +1202.293.4103, ext. 338; [email protected]

105 Financial Analysis for In-house Counsel

Christopher C. King Vice President & General Counsel Hunter Douglas N.V

Peter J. Schimmel Partner Ernst & Young Fraud Investigation & Dispute Services

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Christopher King, Hunter Douglas N.V.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 2

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Financial Statement Analysis„Kölner Funktionslehre“ – Method of analysis and the statements that arerelevant depend on the purpose for which the statements are used.Reasons for Corporate Counsel to analyze financial statements

• Acquisitions / Joint Ventures– Financial statements form part of the basis of valuation– Balance sheet and related notes may point to problems, opportunities, risks

» Potential need for further investigation» Correction of Valuation» Additional warranties or indemnities

– Income Statement / Cash Flow Statement» Relevance is usually based on the assumption of path dependency» Although accountants don’t like to hear it, in an ever-faster changing world, this

assumption gets weaker and weaker.» In particular, the path dependency assumes continuity in strategic planning.

– Statement of Changes in Shareholders Equity – particular importance for legal side

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 3

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Financial Statement AnalysisReasons for Corporate Counsel to analyze financial statements

• Structuring of Earn-Outs, Shareholder Agreements with Buy-Sell provisions– Frequently, parties want to use simplified valuation methods for these purposes– Objectivity of the method is particularly important, where the parties can influence the

results through accounting treatment:» Note continuity problem» Awareness of opportunities for elections, judgments, changes in accounting

treatment» High need for objectivity (internal accounts may not have sufficient quality to merit

use for these purposes)» Always consider alternatives that are less subject to manipulation (auctions,

Texas shoot-outs), due both to problems of objectivity and the low relevance ofthe simplified valuation methods, particularly in light of the weak assumption ofpath-dependency.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 4

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Which Financial Statements are appropriate foranalysis

General Considerations for all forms of statements• Relevance (i.e. date, segment or other information)• Quality (external audit, internal audit, internal policies,

standard bookkeeping schemes)• Objectivity (possibility for elections, whether first time

using a particular format, etc.)Particular importance of impairment test under USGAAP and IFRS

• Difference between impairment and fixed amortization /depreciation

• Valuation methods for impairment; objectivity questions

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 5

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Which Financial Statements are appropriate foranalysis

External financial statements• IFRS

• US GAAP

• 4th Directive

• Other Local (e.g. FER in Switzerland)• Financial statements on tax returns (ties between tax and

financial accounting differs widely)

Consolidated Statements and companystatements

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 6

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Which Financial Statements are appropriatefor analysis

Internal financial statements• Divisional Statements• Statements directly from ledger• Other management reports (i.e. on productivity

or other metrics)

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 7

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Importance of maxims in the differentsystems

Continuity of presentationConservatismGoing Concern PremiseTrue and Fair View

• Generally more rules based approach underUS GAAP

• However, a correction under SOX

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 8

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Getting trapped by forms into reinventingfinancial accounting

Pitfalls are very significant; financial accounting isadapted to a much wider range of industries andconditions than are legal formsConsider particular adjustments based oncompany policy or experience, e.g. inobsolescence reserves, discount rate for pensionsor other long-term liabilities

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 9

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Always relate the financial statements to theproblem at hand

Financial statements tell a story; they needto be “unraveled”If you are trying to assure your companygets what it pays for, look for (and askabout) the value drivers (e.g. differentvaluations of different divisions in anacquisition)

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 10

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Look at both sides of every balance sheetand income statement

It is not the lawyer’s role to look only atliabilities; assets are just as importantThere is nothing per say wrong with anyclass of liabilities, yes, that includesenvironmental or pension, so long as theyare properly valued. Beware of the“agency” trap!

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 11

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Financial Analysis for In-House Lawyers

Tips for In-House LawyersCarefully read the notesCarefully read the MD&ASpecial sensitivity for

• Accounting changes• Classification as discontinued operations• Consolidation issues

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 12

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

105 Financial Analysis for In-House Lawyers

Getting the basics right to avoid making the wrong decision

Peter Schimmel, Ernst & YoungFraud Investigation & Dispute Services (FIDS) Netherlands

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 13

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

The importance of a financial statement

Many stakeholdersShareholdersFinancial InstitutionsVendorsClients(Future) EmployeesPotential BuyersTax AuthoritiesRegulatorsUnionsCompetitorsOther

All these stakeholders have to be served, whilehaving a very different perspective or interest

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 14

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

The importance of a balance sheet

Tell me: what does a balance sheet balance?The balance between what you own (assets) and what youowe (liabilities) now (current) and in the foreseeable future(deferred). If you have more assets than liabilities yourequity is positive.It is all about timing (when and for how long somethingbecomes an asset or liability) and valuation (money spentor current/future earning capacity)Responsibility of company, not auditor or shareholdersScreen shot: one moment. Date may prove important!

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 15

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

The importance of an income statement or P&L

Tell me what is income?What do you consider costs?What do you consider revenue?Should you include extraordinary costs andproceeds?Should you include tax or depreciation?Again, a matter of timing and valuationCovers financial year, 365 daysWhile considered the household book, be carefulto agree to that

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 16

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

The importance of cash flow

Add depreciations, write down to the net profit and subtract upwardrevaluation and you have the cash flow over a periodMaybe the most objective element to be considered, less easy tomanipulateIn theory a company’s value is the capitalized stream of future cashflows (discounted cash flow method of valuation)Without money to pay, expenses cannot be covered, vendors stopdelivering and personnel is no longer willing to workIn that respect, be sensitive to a positive working capital (cash plusaccounts receivables minus current liabilities)Cash flow statement may indeed been seen as the household book,however, just as in private life, always keep in mind your liabilities!

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 17

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

The threat: bankruptcy

The mix up of cash and profit: why do profitablecompanies go bankrupt?A company like Enron showed profit for all last quarters ofit’s existence, because it was accounting for income.However, it was not getting paid for it. Plus it kept a lot ofdebt off balance by not consolidating heavy financedinterestsAlso, when analyzing watch out for expensive debt that isfinancing non interest baring receivables. Bycompensating, balancing those balance postings you canvery much smarten up your financials

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 18

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Ratio analyses

Ratios as a solution for analyzing financialsolidity, the companies health or how yourinvestment is doing

Ratios are the diagnostics of finance

To make companies comparable:benchmarking

Beware: rubbish in is rubbish out

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 19

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Cooking the Books: eight ways to improve yourfinancials

Account for revenue/income too early

Account for costs/expenses too late

Slow down depreciation of assets

Do not write down worthless assets

Book costs as investments

Book loans as income

Compensate receivables and payables

Forget about provisions

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 20

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Create a receivable of 1 M to create 1 of revenueBased on financial statements including new revenue you go toa bank and borrow 1M, using the 1M receivable as collateralYou create fake costs for 1M and allegedly settle them bypaying 1M to your private bank accountYou settle the 1M receivable from your private bank accountBingo: you have just have added 1M revenue to your P&L(or: you have just wrongfully transferred a loan into revenue)and have 1 to your avail.

Creatively creating revenue

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 21

ACC Europe 2007 Corporate Counsel University 4-6 March 2006 NH Barbizon Palace Hotel, Amsterdam

Tips for analyses

Split up balance sheets and income statements inpercentages. That way you can more easily compare fromyear to year and from top to bottom.Do not speculate but try to understand and always askadditional questions(Financial) specialists should be so expert that they canexplain in basic language what they meanAn auditors opinion is only saying that a financialstatement is a fair representation of the financial situationof an organization, but not saying that the organization assuch is okay. It is not a declaration of good health.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 22

To: files ACCE Financial Analyses From: Peter Schimmel Date: February 21, 2007 Subject: Why Enron never reported a loss and still went bankrupt. What to look for in

Numbers

Suggested contribution Peter Schimmel of 30 minutes plus some time for discussion

• Getting the basics right on financial statement analyses • What is really important to know about balance sheets, income statements and cash flow? • How do you cook the books? • How do you analyze financials statements

Basic theory

mBalance Sheet.doc mBreaking down the balance sheet.doc

mReading Balance Sheet.doc

mOff Balance Sheet Entities.doc

mCash Flow Statements.doc

mEssentials of Cash Flow.doc

mIncome Statement.doc

mRatios.doc mRatio Benchmarks.doc

mCooking up BalanceSheets.doc

It is advisable to have all material in print out versions available.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 23

From: www.investopedia.com Date: February 4, 2007 Subject: The purpose of the Balance Sheet

Balance Sheet Knowing how to work with the numbers in a company's financial statements is an essential skill for stock investors. The meaningful interpretation and analysis of balance sheets, income statements and cash flow statements to discern a company's investment qualities is the basis for smart investment choices. However, the diversity of financial reporting requires that we first become familiar with certain general financial statement characteristics before focusing on individual corporate financials. In this article, we'll show you what the financial statements have to offer and how to use them to your advantage.Financial Statements are Scorecards There are millions of individual investors worldwide, and while a large percentage of these investors have chosen mutual funds as the vehicle of choice for their investing activities, a very large percentage of individual investors are also investing directly in stocks. Prudent investing practices dictate that we seek out quality companies with strong balance sheets, solid earnings and positive cash flows.

Whether you're a do-it-yourself or rely on guidance from an investment professional, learning certain fundamental financial statement analysis skills can be very useful - it's certainly not just for the experts. Over thirty years ago, businessman Robert Follet wrote a wonderful little book entitled "How To Keep Score In Business" (1987). His principal point was that in business you keep score with dollars, and the scorecard is a financial statement. He recognized that "a lot of people don't understand keeping score in business. They get mixed up about profits, assets, cash flow and return on investment." The same thing could be said today about a large portion of the investing public, especially when it comes to identifying investment values in financial statements. But don't let this intimidate you; it can be done. As Michael C. Thomsett says in "Mastering Fundamental Analysis" (1998):

"That there is no secret is the biggest secret of Wall Street - and of any specialized industry. Very little in the financial world is so complex that you cannot grasp it. The fundamentals - as their name implies - are basic and relatively uncomplicated. The only factor complicating financial information is jargon, overly complex statistical analysis and complex formulas that don't convey information any better than straight talk."

What follows is a brief discussion of twelve common financial statement characteristics to keep in mind before you start your analytical journey.

What Financial Statements To Use For investment analysis purposes, the financial statements that are used are the balance sheet, the income statement and the cash flow statement. The statements of shareholders' equity and

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 24

retained earnings, which are seldom presented, contain nice-to-know, but not critical, information, and are not used by financial analysts. A word of caution: there are those in the general investing public who tend to focus on just the income statement and the balance sheet, thereby relegating cash flow considerations to somewhat of a secondary status. That's a mistake; for now, simply make a permanent mental note that the cash flow statement contains critically important analytical data.

Knowing What's Behind the Numbers The numbers in a company's financials reflect real world events. These numbers and the financial ratios/indicators that are derived from them for investment analysis are easier to understand if you can visualize the underlying realities of this essentially quantitative information. For example, before you start crunching numbers, have an understanding of what the company does, its products and/or services, and the industry in which it operates.

The Diversity of Financial Reporting Don't expect financial statements to fit into a single mold. Many articles and books on financial statement analysis take a one-size-fits-all approach. The less-experienced investor is going to get lost when he or she encounters a presentation of accounts that falls outside the mainstream or so-called "typical" company. Simply remember that the diverse nature of business activities results in a diversity of financial statement presentations. This is particularly true of the balance sheet; the income and cash flow statements are less susceptible to this phenomenon.

The Challenge of Understanding Financial Jargon The lack of any appreciable standardization of financial reporting terminology complicates the understanding of many financial statement account entries. This circumstance can be confusing for the beginning investor. There's little hope that things will change on this issue in the foreseeable future, but a good financial dictionary can help considerably.

Accounting is an Art, Not a Science The presentation of a company's financial position, as portrayed in its financial statements, is influenced by management estimates and judgments. In the best of circumstances, management is scrupulously honest and candid, while the outside auditors are demanding, strict and uncompromising. Whatever the case, the imprecision that can be inherently found in the accounting process means that the prudent investor should take an inquiring and skeptical approach toward financial statement analysis.

Two Key Accounting Conventions Generally accepted accounting principles (GAAP) are used to prepare financial statements. The sum total of these accounting concepts and assumptions is huge. For investors, a basic understanding of at least two of these conventions - historical cost and accrual accounting - is particularly important. According to GAAP, assets are valued at their purchase price (historical cost), which may be significantly different than their current market value. Revenues are recorded when goods or services are delivered and expenses recorded when incurred. Generally, this flow

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 25

does not coincide with the actual receipt and disbursement of cash, which is why the cash flow becomes so important.

Non-Financial Statement Information Information on the state of the economy, industry and competitive considerations, market forces, technological change, and the quality of management and the workforce are not directly reflected in a company's financial statements. Investors need to recognize that financial statement insights are but one piece, albeit an important one, of the larger investment information puzzle.

Financial Ratios and Indicators The absolute numbers in financial statements are of little value for investment analysis, which must transform these numbers into meaningful relationships to judge a company's financial performance and condition. The resulting ratios and indicators must be viewed over extended periods to reflect trends. Here again, beware of the one-size-fits-all syndrome. Evaluative financial metrics can differ significantly by industry, company size and stage of development.

Notes to the Financial Statements It is difficult for financial statement numbers to provide the disclosure required by regulatory authorities. Professional analysts universally agree that a thorough understanding of the notes to financial statements is essential in order to properly evaluate a company's financial condition and performance. As noted by auditors on financial statements "the accompanying notes are an integral part of these financial statements." Take these noted comments seriously.

The Auditor's Report Prudent investors should only consider investing in companies with audited financial statements, which are a requirement for all publicly traded companies. Before digging into a company's financials, the first thing to do is read the auditor's report. A "clean opinion" provides you with a green light to proceed. Qualifying remarks may be benign or serious; in the case of the latter, you may not want to proceed.

Consolidated Financial Statements Generally, the word "consolidated" appears in the title of a financial statement, as in a consolidated balance sheet. Consolidation of a parent company and its majority-owned (more that 50% ownership or "effective control") subsidiaries means that the combined activities of separate legal entities are expressed as one economic unit. The presumption is that a consolidation as one entity is more meaningful than separate statements for different entities.

The financial statement perspectives provided in this overview are meant to give readers the big picture. With these considerations in mind, beginning investors should be better prepared to cope with learning the analytical details of discerning the investment qualities reflected in a company's financials.

4 February 2007

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 26

From: www.investopedia.com Date: February 4, 2007 Subject: Breaking Down the Balance Sheet

A company's financial statements - balance sheet, income statement and cash flow statement - are a key source of data for analyzing the investment value of its stock. Stock investors, both the do-it-yourselfers and those who follow the guidance of an investment professional, don't need to be analytical experts to perform financial statement analysis. Today, there are numerous sources of independent stock research, online and in print, which can do the "number crunching" for you. However, if you're going to become a serious stock investor, a basic understanding of the fundamentals of financial statement usage is a must. In this article, we help you to become more familiar with the overall structure of the balance sheet.The Structure of a Balance Sheet A company's balance sheet is comprised of assets, liabilities and equity. Assets represent things of value that a company owns and has in its possession or something that will be received and can be measured objectively. Liabilities are what a company owes to others - creditors, suppliers, tax authorities, employees etc. They are obligations that must be paid under certain conditions and time frames. A company's equity represents retained earnings and funds contributed by its shareholders, who accept the uncertainty that comes with ownership risk in exchange for what they hope will be a good return on their investment.

The relationship of these items is expressed in the fundamental balance sheet equation:

Assets = Liabilities + Equity

The meaning of this equation is important. Generally sales growth, whether rapid or slow, dictates a larger asset base - higher levels of inventory, receivables and fixed assets (plant, property and equipment). As a company's assets grow, its liabilities and/or equity also tends to grow in order for its financial position to stay in balance.

How assets are supported, or financed, by a corresponding growth in payables, debt liabilities and equity reveals a lot about a company's financial health. For now, suffice it to say that depending on a company's line of business and industry characteristics, possessing a reasonable mix of liabilities and equity is a sign of a financially healthy company. While it may be an overly simplistic view of the fundamental accounting equation, investors should view a much bigger equity value compared to liabilities as a measure of positive investment quality, because possessing high levels of debt can increase the likelihood that a business will face financial troubles.

Balance Sheet Formats

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 27

Standard accounting conventions present the balance sheet in one of two formats: the account form (horizontal presentation) and the report form (vertical presentation). Most companies favor the vertical report form, which doesn't conform to the typical explanation in investment literature of the balance sheet as having "two sides" that balance out.

Whether the format is up-down or side-by-side, all balance sheets conform to a presentation that positions the various account entries into five sections:

Assets = Liabilities + Equity

• Current assets (short-term): items that are convertible into cash within one year • Non-current assets (long-term): items of a more permanent nature

As total assets these =

• Current liabilities (short-term): obligations due within one year • Non-current liabilities (long-term): obligations due beyond one year

These total liabilities +

• Shareholders' equity (permanent): shareholders' investment and retained earnings

Account PresentationIn the asset sections mentioned above, the accounts are listed in the descending order of their liquidity (how quickly and easily they can be converted to cash). Similarly, liabilities are listed in the order of their priority for payment. In financial reporting, the terms current and non-current are synonymous with the terms short-term and long-term, respectively, and are used interchangeably.

It should not be surprising that the diversity of activities included among publicly-traded companies is reflected in balance sheet account presentations. The balance sheets of utilities, banks, insurance companies, brokerage and investment banking firms and other specialized businesses are significantly different in account presentation from those generally discussed in investment literature. In these instances, the investor will have to make allowances and/or defer to the experts.

Lastly, there is little standardization of account nomenclature. For example, even the balance sheet has such alternative names as a "statement of financial position" and "statement of condition". Balance sheet accounts suffer from this same phenomenon. Fortunately, investors have easy access to extensive dictionaries of financial terminology to clarify an unfamiliar account entry.

The Importance of Dates

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 28

A balance sheet represents a company's financial position for one day at its fiscal year end, for example, the last day of its accounting period, which can differ from our more familiar calendar year. Companies typically select an ending period that corresponds to a time when their business activities have reached the lowest point in their annual cycle, which is referred to as their natural business year.

In contrast, the income and cash flow statements reflect a company's operations for its whole fiscal year - 365 days. Given this difference in "time", when using data from the balance sheet (akin to a photographic snapshot) and the income/cash flow statements (akin to a movie) it is more accurate, and is the practice of analysts, to use an average number for the balance sheet amount. This practice is referred to as "averaging", and involves taking the year-end (2004 and 2005) figures - let's say for total assets - and adding them together, and dividing the total by two. This exercise gives us a rough but useful approximation of a balance sheet amount for the whole year 2005, which is what the income statement number, let's say net income, represents. In our example, the number for total assets at year-end 2005 would overstate the amount and distort the return on assets ratio (net income/total assets).

Since a company's financial statements are the basis of analyzing the investment value of a stock, this discussion we have completed should provide investors with the "big picture" for developing an understanding of balance sheet basics.

4 February 2007

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 29

From: www.investopedia.com Date: 4 February 2007 Subject: Reading the Balance Sheet

A balance sheet, also known as a "statement of financial position", reveals a company's assets, liabilities and owners' equity (net worth). The balance sheet, together with the income statement and cash flow statement, make up the cornerstone of any company's financial statements. If you are a shareholder of a company, it is important that you understand how the balance sheet is structured, how to analyze it and how to read it.

How the Balance Sheet WorksThe balance sheet is divided into two parts that, based on the following equation, must equal (or balance out) each other. The main formula behind balance sheets is: assets = liabilities + shareholders’ equity.

This means that assets, or the means used to operate the company, are balanced by a company's financial obligations along with the equity investment brought into the company and its retained earnings.

Assets are what a company uses to operate its business, while its liabilities and equity are two sources that support these assets. Owners' equity, referred to as shareholders' equity in a publicly traded company, is the amount of money initially invested into the company plus any retained earnings, and it represents a source of funding for the business.

It is important to note, that a balance sheet is a snapshot of the company’s financial position at a single point in time.

Know the Types of Assets Current AssetsCurrent assets have a life span of one year or less, meaning they can be converted easily into cash. Such assets classes are: cash and cash equivalents, accounts receivable and inventory. Cash, the most fundamental of current assets, also includes non-restricted bank accounts and checks. Cash equivalents are very safe assets that can be are readily converted into cash such as U.S. Treasuries. Accounts receivable consists of the short-term obligations owed to the company by its clients. Companies often sell products or services to customers on credit, which then are held in this account until they are paid off by the clients. Lastly, inventory represents the raw materials, work-in-progress goods and the company’s finished goods. Depending on the company, the exact makeup of the inventory account will differ. For example, a manufacturing firm will carry a large amount of raw materials, while a retail firm caries none. The makeup of a retailers inventory typically consists of goods purchased from manufacturers and wholesalers.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 30

Non-Current AssetsNon-current assets, are those assets that are not turned into cash easily, expected to be turned into cash within a year and/or have a life-span of over a year. They can refer to tangible assets such as machinery, computers, buildings and land. Non-current assets also can be intangible assets, such as goodwill, patents or copyright. While these assets are not physical in nature, they are often the resources that can make or break a company - the value of a brand name, for instance, should not be underestimated.

Depreciation is calculated and deducted from most of these assets, which represents the economic cost of the asset over its useful life.

Learn the Different LiabilitiesOn the other side of the balance sheet are the liabilities. These are the financial obligations a company owes to outside parties. Like assets, they can be both current and long-term. Long-term liabilities are debts and other non-debt financial obligations, which are due after a period of at least one year from the date of the balance sheet. Current liabilities are the company’s liabilities which will come due, or must be paid, within one year. This is comprised of both shorter term borrowings, such as accounts payables, along with the current portion of longer term borrowing, such as the latest interest payment on a 10-year loan.

Shareholders' EquityShareholders' equity is the initial amount of money invested into a business. If, at the end of the fiscal year, a company decides to reinvest its net earnings into the company (after taxes), these retained earnings will be transferred from the income statement onto the balance sheet into the shareholder’s equity account. This account represents a company's total net worth. In order for the balance sheet to balance, total assets on one side have to equal total liabilities plus shareholders' equity on the other.

Read the Balance Sheet Below is an example of a balance sheet:

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 31

Source: http://www.edgar-online.com

As you can see from the balance sheet above, it is broken into two sides. Assets are on the left side and the right side contains the company’s liabilities and shareholders’ equity. It also can be seen that this balance sheet is in balance where the value of the assets equals the combined value of the liabilities and shareholders’ equity.

Another interesting aspect of the balance sheet is how it is organized. The assets and liabilities sections of the balance sheet are organized by how current the account is. So for the asset side, the accounts are classified typically from most liquid to least liquid. For the liabilities side, the accounts are organized from short to long-term borrowings and other obligations.

Analyze the Balance Sheet with Ratios With a greater understanding of the balance sheet and how it is constructed, we can look now at some techniques used to analyze the information contained within the balance sheet. The main way this is done is through financial ratio analysis.

Financial ratio analysis uses formulas to gain insight into the company and its operations. For the balance sheet, using financial ratios (like the debt-to-equity ratio) can show you a better idea of the company’s financial condition along with its operational efficiency. It is important to note that some ratios will need information from more than one financial statement, such as from the balance sheet and the income statement.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 32

The main types of ratios that use information from the balance sheet are financial strength ratios and activity ratios. Financial strength ratios, such as the working capital and debt-to-equity ratios, provide information on how well the company can meet its obligations and how they are leveraged. This can give investors an idea of how financially stable the company is and how the company finances itself. Activity ratios focus mainly on current accounts to show how well the company manages its operating cycle (which include receivables, inventory and payables). These ratios can provide insight into the operational efficiency of the company.

There are a wide range of individual financial ratios that investors use to learn more about a company.

Conclusion The balance sheet, along with the income and cash flow statements, is an important tool for investors to gain insight into a company and its operations. The balance sheet is a snapshot at a single point in time of the company’s accounts - covering its assets, liabilities and shareholders’ equity. The purpose of the balance sheet is to give users an idea of the company’s financial position along with displaying what the company owns and owes. It is important that all investors know how to use, analyze and read one.

4 February 2007

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 33

From: www.investopedia.com Date: February 4, 2007 Subject: Off Balance Sheet Entities

Companies have used off-balance-sheet entities responsibly and irresponsibly for some time. These separate legal entities were permissible under generally accepted accounting principles (GAAP) and tax laws so that companies could finance business ventures by transferring the risk of these ventures from the parent to the off-balance-sheet subsidiary. This was also helpful to investors who did not want to invest in these other ventures.

Since the Enron scandal, however, companies that have any kind of off-balance-sheet items, whether justifiably or not, are being branded with a scarlet letter "E". This article will define some typical off-balance-sheet items and discuss whether they are "good" or "bad".

The term "off-balance-sheet" can refer to many things. Typically, it refers to separate legal entities (separate companies of which the parent holds less than 100% ownership) or contingent liabilities such as letters of credit or loans to separate legal entities that are guaranteed by the parent. GAAP allows these items to be excluded from the parent's financial statements but usually they must be described in footnotes.

The GoodOff-balance-sheet companies were created to help finance new ventures. Theoretically, these separate companies were used to transfer the risk of the new venture from the parent to the separate company. This way, the parent could finance the new venture without diluting existing shareholders or adding to the parent's debt burden. These separate legal entities could be privately held partnerships or publicly traded spin-offs.

Sometimes the separate companies were created to pursue a business project that was a part of the parent's main line of business. For example, oil-drilling companies established off-balance-sheet subsidiaries as a way to finance oil exploration projects. These subsidiaries were jointly funded by the parent and outside investors who were willing to take the exploration risk. The parent company could have sold shares or borrowed the money directly, but the accounting and tax laws were designed to allow the project funding come from investors who were interested in investing in specific explorations rather than investing in the parent company.

Other times these separate companies were created to house businesses that were decidedly different from the parent's line of work (in order to unlock "value"). For example, Williams Co's, created Williams Communications to pursue the communications business. Williams Companies spun off Williams Communications, but the bankers required the parent to guarantee the debt of Williams Communications. Because Williams Communications was a new company, this is not an unusual request.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 34

This use of off-balance-sheet entities is good in that it transfers risk from the parent's shareholders to others that were willing to take the business risk. Investors in Williams Companies (an energy resource company) may not have wanted to invest in a communications company, so management created a separate entity to house that business. Likewise, oil companies used off-balance-sheet entities to remove the exploration risk from their business to share it with others that wanted a bigger piece of the potential return from exploration.

The BadWhile GAAP and tax laws allow off-balance-sheet entities for valid reasons noted above, bad things happen when economic reality differs significantly from the assumptions that were used to justify the off-balance-sheet entity. Problems also occur when egos get too big.

In Williams's case, the decision to spin off the communications business was reasonable at the time. The parent had the infrastructure on which to build a communications network, but it was an energy company. By spinning off the subsidiary, it was not forcing its investors to take on the risk of a communications company, and it was able to take advantage of the market's demand for communication stocks. At the same time, the need to guarantee the debt of a new subsidiary is a reasonable request that bankers make in this type of transaction.

What went "wrong" was that economic reality differed from the assumptions that were used to justify the spin off. Dotcom mania resulted in over-capacity, causing problems for all telecommunications companies. The loan guarantee, which is never expected to be triggered, is now an issue for the company because of the recession and the slump in the telecommunications sector.

Enron exemplifies how ego can be the basis for the misuse of off-balance-sheet items. Here, off-balance-sheet vehicles appear to have been used to pump up financial results rather than for legitimate business purposes. What started as a plan to legitimately use off-balance-sheet vehicles morphed into ways to manufacture earnings as trades went bad. While one could argue that this is also a case of economic reality differing from expectations, the way management reacted to the situation allows us to classify it as an ego thing.

This financial engineering is usually fueled by the need to reach certain operating targets established by Wall Street or compensation plans. Once management succumbs to this "Dark Side", more time is spent on trying to game the system than trying to manage the core business. It is then only a matter of time before the house of cards falls.

The UglyIt gets ugly when the markets start to punish a stock just because it has an off-balance-sheet item. Granted, it is not always easy to read a company's SEC filings, let alone dig into the footnotes and figure out how the off-balance-sheet items might impact results. But the companies that provide full disclosure will probably be the better investments.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 35

ConclusionThe loss of faith in accounting's ability to provide full disclosure could have a bigger impact on the stock market than the events of September 11th. The attacks were an exogenous factor and we bounced back nicely. The loss of confidence in financial statements is an attack on one of the core elements of investment decision making. To quote Johnny Cochran, "If the statements aren't true, what will we do?"

However, the focus on off-balance-sheet accounting will have two major benefits. First, it will result in new regulations that will hopefully prevent future Enrons. Some of these changes will likely be the following: Prevention of officers of the parent from being officers of the off-balance-sheet subsidiary Increasing the percentage ownership by outside and non-affiliated companies Enforcing disclosure rules so that investors can clearly understand the risk (if any) posed by off-balance-sheet companies Second, market over-reaction creates a buying opportunity. Markets always overreact, causing panic in the Street. Uncertainty created by the loss of faith in financial disclosures could even cause more damage to the market than extreme events like September 11th.

4 February 2007

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 36

From: www.investopedia.com Date: February 4, 2007 Subject: Cash Flow Statements

One of the quarterly financial reports any publicly traded company is required to disclose to the SEC and the public. The document provides aggregate data regarding all cash inflows a company receives from both its ongoing operations and external investment sources, as well as all cash outflows that pay for business activities and investments during a given quarter

Because public companies tend to use accrual accounting, the income statements they release each quarter may not necessarily reflect changes in their cash positions. For example, if a company lands a major contract, this contract would be recognized as revenue (and therefore income), but the company may not yet actually receive the cash from the contract until a later date. While the company may be earning a profit in the eyes of accountants (and paying income taxes on it), the company may, during the quarter, actually end up with less cash than when it started the quarter. Even profitable companies can fail to adequately manage their cash flow, which is why the cash flow statement is important: it helps investors see if a company is having trouble with cash.

4 February 2007

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 37

From: www.investopedia.com Date: 4 February 2007 Subject: The essentials of cash flow

If a company reports earnings of $1 billion, does this mean it has this amount of cash in the bank? Not necessarily. Financial statements are based on accrual accounting, which takes into account non-cash items. It does this in an effort to best reflect the financial health of a company. However, accrual accounting may create accounting noise, which sometimes needs to be tuned out so that it's clear how much actual cash a company is generating. The statement of cash flow provides this information, and here we look at what cash flow is and how to read the cash flow statement.

What Is Cash Flow?Business is all about trade, the exchange of value between two or more parties, and cash is the asset needed for participation in the economic system. For this reason - while some industries are more cash intensive than others - no business can survive in the long run without generating positive cash flow per share for its shareholders. To have a positive cash flow, the company's long-term cash inflows need to exceed its long-term cash outflows.

An outflow of cash occurs when a company transfers funds to another party (either physically or electronically). Such a transfer could be made to pay for employees, suppliers and creditors, or to purchase long-term assets and investments, or even pay for legal expenses and lawsuit settlements. It is important to note that legal transfers of value through debt - a purchase made on credit - is not recorded as a cash outflow until the money actually leaves the company's hands.

A cash inflow is of course the exact opposite; it is any transfer of money that comes into the company's possession. Typically, the majority of a company's cash inflows are from customers, lenders (such as banks or bondholders) and investors who purchase company equity from the company. Occasionally cash flows come from sources like legal settlements or the sale of company real estate or equipment.

Cash Flow vs IncomeIt is important to note the distinction between being profitable and having positive cash flow transactions: just because a company is bringing in cash does not mean it is making a profit (and vice versa).

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 38

For example, say a manufacturing company is experiencing low product demand and therefore decides to sell off half its factory equipment at liquidation prices. It will receive cash from the buyer for the used equipment, but the manufacturing company is definitely losing money on the sale: it would prefer to use the equipment to manufacture products and earn an operating profit. But since it cannot, the next best option is to sell off the equipment at prices much lower than the company paid for it. In the year that it sold the equipment, the company would end up with a strong positive cash flow, but its current and future earnings potential would be fairly bleak. Because cash flow can be positive while profitability is negative, investors should analyze income statements as well as cash flow statements, not just one or the other.

What Is the Cash Flow Statement?There are three important parts of a company's financial statements: the balance sheet, the income statement and the cash flow statement. The balance sheet gives a one-time snapshot of a company's assets and liabilities (see Reading the Balance Sheet). And the income statement indicates the business's profitability during a certain period (see Understanding The Income Statement).

The cash flow statement differs from these other financial statements because it acts as a kind of corporate checkbook that reconciles the other two statements. Simply put, the cash flow statement records the company's cash transactions (the inflows and outflows) during the given period. It shows whether all those lovely revenues booked on the income statement have actually been collected. At the same time, however, remember that the cash flow does not necessarily show all the company's expenses: not all expenses the company accrues have to be paid right away. So even though the company may have incurred liabilities it must eventually pay, expenses are not recorded as a cash outflow until they are paid (see the section "What Cash Flow Doesn't Tell Us" below).

The following is a list of the various areas of the cash flow statement and what they mean: Cash flow from operating activities- This section measures the cash used or provided by a company's normal operations. It shows the company's ability to generate consistently positive cash flow from operations. Think of "normal operations" as the core business of the company. For example, Microsoft's normal operating activity is selling software. Cash flows from investing activities- This area lists all the cash used or provided by the purchase and sale of income-producing assets. If Microsoft, our example, bought or sold companies for a profit or loss, the resulting figures would be included in this section of the cash flow statement. Cash flows from financing activities - This section measures the flow of cash between a firm and its owners and creditors. Negative numbers can mean the company is servicing debt but can also mean the company is making dividend payments and stock repurchases, which investors might be glad to see.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 39

When you look at a cash flow statement, the first thing you should look at is the bottom line item that says something like "net increase/decrease in cash and cash equivalents", since this line reports the overall change in the company's cash and its equivalents (the assets that can be immediately converted into cash) over the last period. If you check under current assets on the balance sheet, you will find cash and cash equivalents (CCE or CC&E). If you take the difference between the current CCE and last year's or last quarter's, you'll get this same number found at the bottom of the statement of cash flows.

In the sample Microsoft annual cash flow statement (from June 2004) shown below, we can see that the company ended up with about $9.5 billion more cash at the end of its 2003/04 fiscal year than it had at the beginning of that fiscal year (see "Net Change in Cash and Equivalents"). Digging a little deeper, we see that the company had a negative cash outflow of $2.7 billion from investment activities during the year (see "Net Cash from Investing Activities"); this is likely from the purchase of long-term investments, which have the potential to generate a profit in the future.Generally, a negative cash flow from investing activities are difficult to judge as either good or bad - these cash outflows are investments in future operations of the company (or another company); the outcome plays out over the long term.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 40

The "Net Cash from Operating Activities" reveals that Microsoft generated $14.6 billion in positive cash flow from its usual business operations - a good sign. Notice the company has had similar levels of positive operating cash flow for several years. If this number were to increase or decrease significantly in the upcoming year, it would be a signal of some underlying change in the company's ability to generate cash.

Digging Deeper into Cash FlowAll companies provide cash flow statements as part of their financial statements, but cash flow (net change in cash and equivalents) can also be calculated as net income plus depreciation and other non-cash items.

Generally, a company's principal industry of operation determine what is considered proper cash flow levels; comparing a company's cash flow against its industry peers is a good way to gauge the health of its cash flow situation. A company not generating the same amount of cash as competitors is bound to lose out when times get rough.

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 41

Even a company that is shown to be profitable according to accounting standards can go under if there isn't enough cash on hand to pay bills. Comparing amount of cash generated to outstanding debt, known as the operating cash flow ratio, illustrates the company's ability to service its loans and interest payments. If a slight drop in a company's quarterly cash flow would jeopardize its loan payments, that company carries more risk than a company with stronger cash flow levels.

Unlike reported earnings, cash flow allows little room for manipulation. Every company filing reports with the Securities and Exchange Commission (SEC) is required to include a cash flow statement with its quarterly and annual reports. Unless tainted by outright fraud, this statement tells the whole story of cash flow: either the company has cash or it doesn't.

What Cash Flow Doesn't Tell UsCash is one of the major lubricants of business activity, but there are certain things that cash flow doesn't shed light on. For example, as we explained above, it doesn't tell us the profit earned or lost during a particular period: profitability is composed also of things that are not cash based. This is true even for numbers on the cash flow statement like "cash increase from sales minus expenses", which may sound like they are indication of profit but are not.

As it doesn't tell the whole profitability story, cash flow doesn't do a very good job of indicating the overall financial well-being of the company. Sure, the statement of cash flow indicates what the company is doing with its cash and where cash is being generated, but these do not reflect the company's entire financial condition. The cash flow statement does not account for liabilities and assets, which are recorded on the balance sheet. Furthermore accounts receivable and accounts payable, each of which can be very large for a company, are also not reflected in the cash flow statement.

In other words, the cash flow statement is a compressed version of the company's checkbook that includes a few other items that affect cash, like the financing section, which shows how much the company spent or collected from the repurchase or sale of stock, the amount of issuance or retirement of debt and the amount the company paid out in dividends.

ConclusionLike so much in the world of finance, the cash flow statement is not straightforward. You must understand the extent to which a company relies on the capital markets and the extent to which it relies on the cash it has itself generated. No matter how profitable a company may be, if it doesn't have the cash to pay its bills, it will be in serious trouble.

At the same time, while investing in a company that shows positive cash flow is desirable, there are also opportunities in companies that aren't yet cash-flow positive. The cash flow statement is simply a piece of the puzzle. So, analyzing it together with the other statements can give you a more overall look at a company' financial health. Remain diligent in your analysis of a company's cash flow statement and you will be well on your way to removing the risk of one of your stocks falling victim to a cash flow crunch.

4 February 2007

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 42

From: www.investopedia.com Date: February 4, 2007 Subject: Income Statement

A financial statement that summarizes the revenues, costs and expenses incurred during a specific period of time - usually a fiscal quarter or year. These records provide information that shows the ability of a company to generate profit by increasing revenue and reducing costs. The P&L statement is also known as a "statement of profit and loss", an "income statement" or an "income and expense statement".

The statement of profit and loss follows a general format that begins with an entry for revenue and subtracts from revenue the costs of running the business, including cost of goods sold, operating expenses, tax expense and interest expense. The bottom line (literally and figuratively) is net income (profit).

The balance sheet, income statement and statement of cash flows are the most important financial statements produced by a company. While each is important in its own right, they are meant to be analyzed together.

4 February 2007

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 43

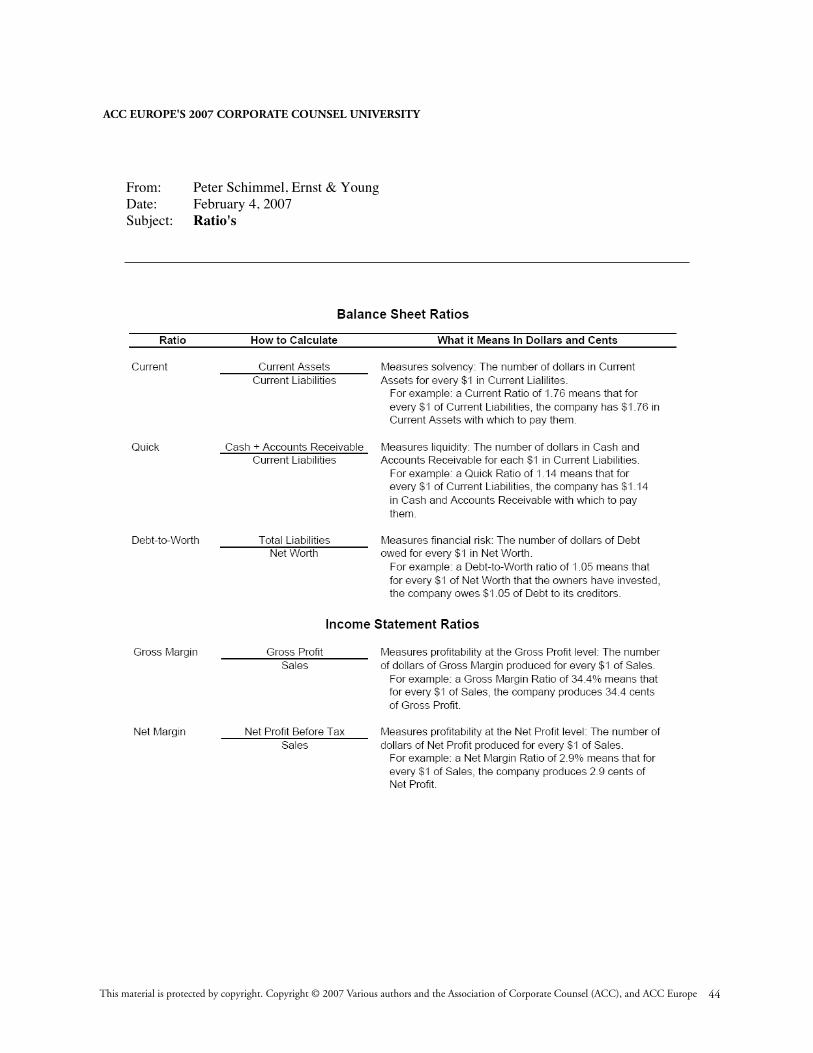

From: Peter Schimmel, Ernst & Young Date: February 4, 2007 Subject: Ratio's

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 44

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 45

4 February 2007

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 46

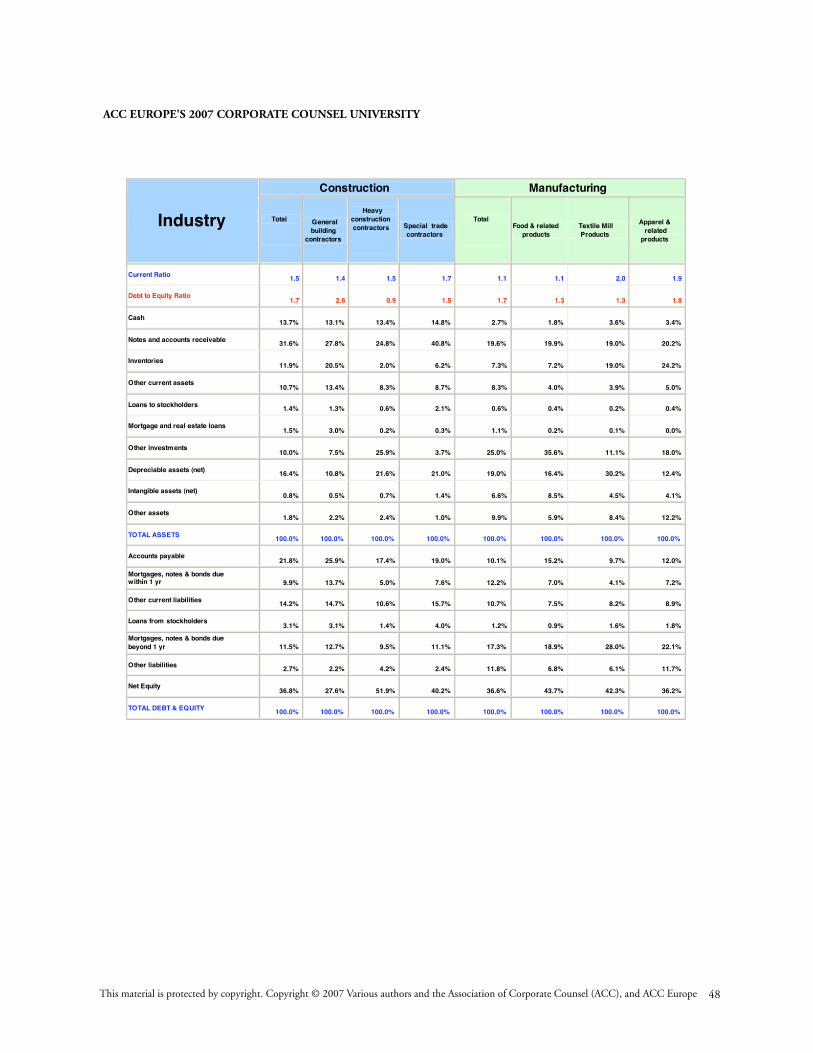

From: www.bizstats.com Date: February 4, 2007 Subject: Ratio Benchmark Info

BizStats.com

useful business statistics

Current Ratios & Other Balance Sheet Ratios National Averages for profitable U.S. Corporations

The following table reports current ratios, debt to equity ratios and composition of corporate balance sheets based on most recent data compiled from approximately 2.7 million corporate income tax returns reporting profits. Caution: Be careful if using this data for benchmarkingpurposes, since these are nationwide averages of corporate entities of various ages and capitalization, often employing differing methods of accounting, with differing fiscal year ends, and offering divergent product lines - factors which materially impact balance sheet ratios andcomposition

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 47

Construction Manufacturing

Industry Total General building

contractors

Heavy construction contractors Special trade

contractors

TotalFood & related

products Textile Mill Products

Apparel & related

products

Current Ratio 1.5 1.4 1.5 1.7 1.1 1.1 2.0 1.9

Debt to Equity Ratio1.7 2.6 0.9 1.5 1.7 1.3 1.3 1.8

Cash13.7% 13.1% 13.4% 14.8% 2.7% 1.8% 3.6% 3.4%

Notes and accounts receivable 31.6% 27.8% 24.8% 40.8% 19.6% 19.9% 19.0% 20.2%

Inventories11.9% 20.5% 2.0% 6.2% 7.3% 7.2% 19.0% 24.2%

Other current assets10.7% 13.4% 8.3% 8.7% 8.3% 4.0% 3.9% 5.0%

Loans to stockholders 1.4% 1.3% 0.6% 2.1% 0.6% 0.4% 0.2% 0.4%

Mortgage and real estate loans1.5% 3.0% 0.2% 0.3% 1.1% 0.2% 0.1% 0.0%

Other investments10.0% 7.5% 25.9% 3.7% 25.0% 35.6% 11.1% 18.0%

Depreciable assets (net) 16.4% 10.8% 21.6% 21.0% 19.0% 16.4% 30.2% 12.4%

Intangible assets (net)0.8% 0.5% 0.7% 1.4% 6.6% 8.5% 4.5% 4.1%

Other assets1.8% 2.2% 2.4% 1.0% 9.9% 5.9% 8.4% 12.2%

TOTAL ASSETS 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Accounts payable21.8% 25.9% 17.4% 19.0% 10.1% 15.2% 9.7% 12.0%

Mortgages, notes & bonds due within 1 yr 9.9% 13.7% 5.0% 7.6% 12.2% 7.0% 4.1% 7.2%

Other current liabilities 14.2% 14.7% 10.6% 15.7% 10.7% 7.5% 8.2% 8.9%

Loans from stockholders3.1% 3.1% 1.4% 4.0% 1.2% 0.9% 1.6% 1.8%

Mortgages, notes & bonds due beyond 1 yr 11.5% 12.7% 9.5% 11.1% 17.3% 18.9% 28.0% 22.1%

Other liabilities 2.7% 2.2% 4.2% 2.4% 11.8% 6.8% 6.1% 11.7%

Net Equity36.8% 27.6% 51.9% 40.2% 36.6% 43.7% 42.3% 36.2%

TOTAL DEBT & EQUITY 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 48

Manufacturing (continued)

Manufacturing Lumber & Wood

Products

Paper & related

products

Printing & Publishing

Chemicals & related

products

Petroleum & coal products

Rubber & plastic

products

Leather & leather

products

Stone, clay & glass

products

Current Ratio 1.2 1.0 1.3 0.9 1.2 1.6 2.4 1.4

Debt to Equity Ratio 1.4 1.3 1.2 1.8 1.1 1.5 1.0 1.3

Cash 3.3% 1.8% 3.0% 2.1% 0.9% 4.4% 6.8% 4.1%

Notes and accounts receivable 9.9% 10.1% 15.1% 15.5% 13.7% 19.7% 25.2% 17.0%

Inventories 11.8% 7.1% 3.8% 6.4% 2.9% 15.3% 29.6% 10.5%

Other current assets 8.6% 7.8% 5.3% 4.2% 4.2% 3.2% 7.1% 3.0%

Loans to stockholders 0.2% 0.1% 0.4% 2.2% 0.8% 0.4% 0.0% 0.4%

Mortgage and real estate loans 1.9% 4.3% 0.0% 5.2% 0.0% 0.1% 0.0% 1.3%

Other investments 13.3% 23.9% 26.4% 28.6% 39.9% 15.2% 9.9% 14.2%

Depreciable assets (net) 35.4% 35.7% 15.8% 17.8% 23.7% 32.9% 15.2% 38.1%

Intangible assets (net) 1.9% 3.1% 23.7% 7.0% 2.4% 4.6% 3.1% 8.0%

Other assets 13.8% 6.0% 6.5% 10.9% 11.5% 4.3% 3.0% 3.5%

TOTAL ASSETS 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Accounts payable 7.6% 7.8% 8.3% 10.3% 9.1% 10.5% 14.4% 8.8%

Mortgages, notes & bonds due within 1 yr 4.3% 6.7% 3.9% 7.8% 5.1% 5.8% 5.0% 6.4%

Other current liabilities 15.8% 12.1% 9.2% 13.2% 4.4% 10.7% 9.6% 9.8%

Loans from stockholders 1.3% 0.5% 2.6% 2.0% 0.9% 2.3% 0.0% 2.9%

Mortgages, notes & bonds due beyond 1 yr 23.5% 19.0% 22.2% 17.6% 16.5% 20.4% 14.8% 22.3%

Other liabilities 5.6% 10.5% 9.2% 13.0% 16.3% 10.8% 2.7% 6.1%

Net Equity 42.0% 43.4% 44.6% 36.2% 47.7% 39.6% 50.9% 43.4%

TOTAL DEBT & EQUITY 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 97.4% 99.9%

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 49

Manufacturing (continued)

Manufacturing Primary metal

industries

Fabricated metal

products

Machinery except

electrical

Electrical & electronic

equipment

Motor vehicles &

Equipment

Transportation equipment

except motor vehicles

Instruments & related

products

Miscellaneous manufacturing

Current Ratio1.7 1.7 1.5 1.1 0.9 1.0 1.4 1.7

Debt to Equity Ratio1.5 1.1 2.0 2.4 3.7 2.8 1.5 1.2

Cash 3.6% 5.4% 5.3% 4.3% 1.3% 1.4% 5.1% 7.3%

Notes and accounts receivable17.7% 20.7% 26.1% 19.6% 33.7% 15.8% 24.7% 19.8%

Inventories13.3% 15.0% 11.5% 6.4% 3.1% 17.8% 10.8% 16.8%

Other current assets 3.5% 4.0% 7.2% 24.5% 6.6% 8.2% 8.3% 6.6%

Loans to stockholders 0.2% 0.7% 0.2% 0.1% 0.0% 0.6% 0.2% 0.5%

Mortgage and real estate loans0.0% 0.1% 0.0% 0.0% 1.0% 0.2% 0.1% 0.1%

Other investments17.8% 16.9% 16.9% 17.5% 18.0% 16.6% 20.7% 14.2%

Depreciable assets (net)34.0% 24.1% 17.9% 13.1% 16.3% 18.4% 15.3% 18.4%

Intangible assets (net)3.4% 7.2% 5.8% 6.1% 1.5% 11.0% 7.4% 9.4%

Other assets 6.4% 5.9% 9.0% 8.3% 18.5% 10.1% 7.4% 6.8%

TOTAL ASSETS100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Accounts payable 11.3% 11.2% 15.4% 6.5% 11.0% 7.7% 14.0% 9.2%

Mortgages, notes & bonds due within 1 yr 4.1% 5.7% 9.4% 31.5% 21.3% 11.6% 6.1% 5.7%

Other current liabilities7.3% 9.0% 9.2% 11.2% 14.2% 22.2% 13.9% 14.0%

Loans from stockholders1.9% 2.4% 0.9% 0.4% 0.1% 0.3% 1.1% 1.3%

Mortgages, notes & bonds due beyond 1 yr 17.4% 17.1% 19.1% 12.4% 16.8% 18.4% 14.3% 16.9%

Other liabilities17.3% 7.7% 13.2% 8.9% 16.0% 13.7% 10.9% 6.9%

Net Equity40.7% 46.9% 32.8% 29.1% 20.6% 26.0% 39.7% 45.9%

TOTAL DEBT & EQUITY100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 50

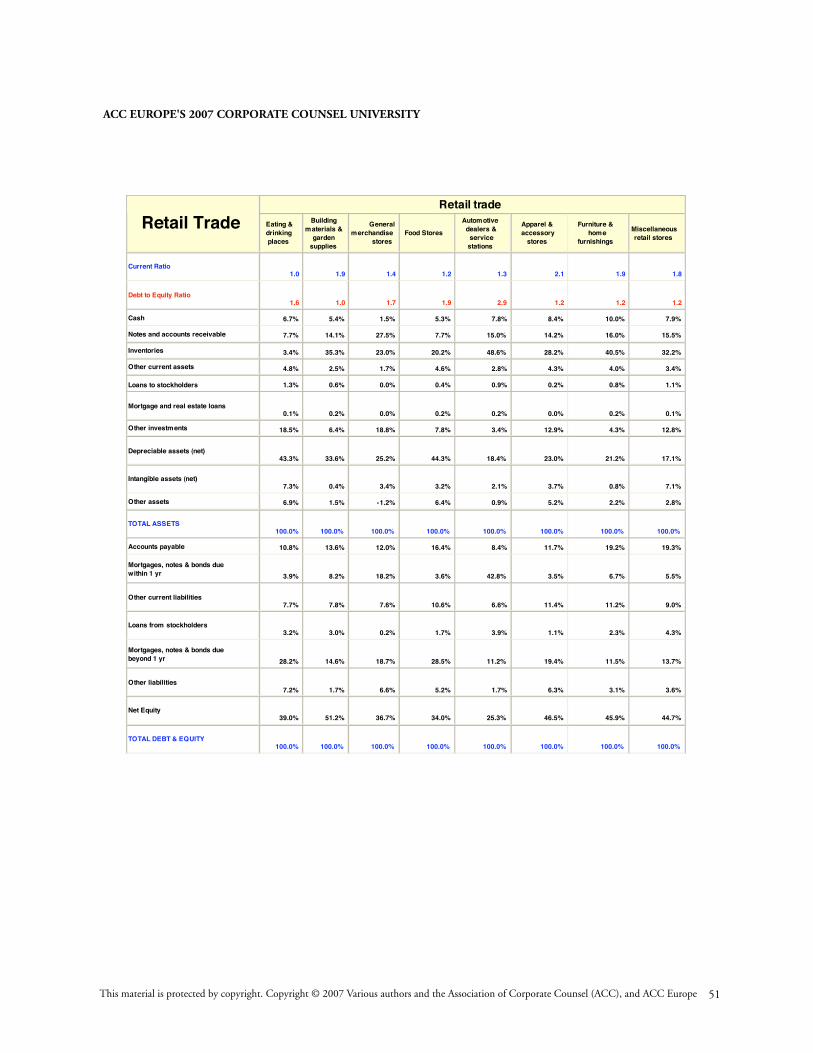

Retail trade

Retail Trade Eating & drinking places

Building materials &

garden supplies

Generalmerchandise

storesFood Stores

Automotive dealers &

service stations

Apparel & accessory

stores

Furniture & home

furnishings

Miscellaneous retail stores

Current Ratio1.0 1.9 1.4 1.2 1.3 2.1 1.9 1.8

Debt to Equity Ratio1.6 1.0 1.7 1.9 2.9 1.2 1.2 1.2

Cash 6.7% 5.4% 1.5% 5.3% 7.8% 8.4% 10.0% 7.9%

Notes and accounts receivable 7.7% 14.1% 27.5% 7.7% 15.0% 14.2% 16.0% 15.5%

Inventories 3.4% 35.3% 23.0% 20.2% 48.6% 28.2% 40.5% 32.2%

Other current assets 4.8% 2.5% 1.7% 4.6% 2.8% 4.3% 4.0% 3.4%

Loans to stockholders 1.3% 0.6% 0.0% 0.4% 0.9% 0.2% 0.8% 1.1%

Mortgage and real estate loans0.1% 0.2% 0.0% 0.2% 0.2% 0.0% 0.2% 0.1%

Other investments 18.5% 6.4% 18.8% 7.8% 3.4% 12.9% 4.3% 12.8%

Depreciable assets (net)43.3% 33.6% 25.2% 44.3% 18.4% 23.0% 21.2% 17.1%

Intangible assets (net)7.3% 0.4% 3.4% 3.2% 2.1% 3.7% 0.8% 7.1%

Other assets 6.9% 1.5% -1.2% 6.4% 0.9% 5.2% 2.2% 2.8%

TOTAL ASSETS100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Accounts payable 10.8% 13.6% 12.0% 16.4% 8.4% 11.7% 19.2% 19.3%

Mortgages, notes & bonds due within 1 yr 3.9% 8.2% 18.2% 3.6% 42.8% 3.5% 6.7% 5.5%

Other current liabilities7.7% 7.8% 7.6% 10.6% 6.6% 11.4% 11.2% 9.0%

Loans from stockholders3.2% 3.0% 0.2% 1.7% 3.9% 1.1% 2.3% 4.3%

Mortgages, notes & bonds due beyond 1 yr 28.2% 14.6% 18.7% 28.5% 11.2% 19.4% 11.5% 13.7%

Other liabilities7.2% 1.7% 6.6% 5.2% 1.7% 6.3% 3.1% 3.6%

Net Equity39.0% 51.2% 36.7% 34.0% 25.3% 46.5% 45.9% 44.7%

TOTAL DEBT & EQUITY100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 51

Finance & InsuranceTransportation Communication &

Utilities

Industry BankingCredit

agencies

Security & commodity

brokers

Insurance companies

Insurance agents,

brokers & services

Transportation services

Communication services

Electric, gas & sanitary

services

Current Ratio0.9 0.6 0.8 1.1 1.3 1.1 0.9 0.9

Debt to Equity Ratio7.3 10.9 16.5 3.7 1.7 1.7 1.5 1.9

Cash 7.5% 2.3% 2.6% 1.5% 15.3% 4.7% 1.9% 1.4%

Notes and accounts receivable 45.2% 25.5% 25.4% 3.4% 21.0% 12.0% 14.9% 6.8%

Inventories 0.0% 0.0% 0.0% 0.0% 0.0% 1.2% 1.1% 1.4%

Other current assets 16.0% 14.8% 36.7% 19.0% 13.7% 5.3% 3.5% 4.1%

Loans to stockholders 0.0% 0.4% 0.1% 0.1% 1.4% 0.4% 0.4% 0.1%

Mortgage and real estate loans8.3% 39.1% 0.7% 4.9% 0.5% 0.2% 0.0% 0.0%

Other investments 14.4% 14.6% 25.6% 58.6% 30.1% 21.1% 24.3% 15.8%

Depreciable assets (net)1.3% 0.7% 0.7% 1.2% 7.1% 47.7% 36.8% 57.8%

Intangible assets (net)1.0% 0.4% 0.5% 0.3% 4.5% 2.6% 11.9% 1.4%

Other assets 6.4% 2.2% 7.6% 11.0% 6.6% 4.9% 5.2% 11.2%

TOTAL ASSETS100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Accounts payable 3.1% 5.1% 17.8% 1.1% 22.9% 7.6% 6.6% 4.6%

Mortgages, notes & bonds due within 1 yr 6.4% 23.0% 4.2% 1.5% 3.3% 3.4% 8.9% 5.3%

Other current liabilities67.6% 39.8% 57.3% 19.4% 11.8% 10.8% 7.1% 5.8%

Loans from stockholders0.1% 0.7% 0.1% 0.1% 0.9% 1.1% 0.6% 0.1%

Mortgages, notes & bonds due beyond 1 yr 6.4% 19.5% 6.9% 2.4% 8.7% 24.3% 22.8% 30.2%

Other liabilities4.5% 3.5% 8.1% 54.4% 14.8% 15.8% 14.2% 19.2%

Net Equity12.0% 8.4% 5.7% 21.1% 37.6% 37.0% 39.8% 34.8%

TOTAL DEBT & EQUITY100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 52

Services Services All

services Hotels &lodging places

Personalservices

Business services

Auto & miscellaneous

repair services

Amusement & recreation services

Other ServicesAgriculture,

forestry andfishing

Current Ratio1.4 0.8 1.9 1.4 1.0 1.4 1.5 1.5

Debt to Equity Ratio1.5 1.8 1.4 1.7 2.2 1.3 1.4 1.1

Cash 8.8% 4.5% 8.1% 10.9% 8.7% 5.3% 10.4% 8.0%

Notes and accounts receivable16.5% 5.8% 15.6% 24.7% 13.3% 5.4% 17.6% 10.3%

Inventories2.4% 1.1% 7.6% 2.0% 9.6% 2.8% 1.3% 10.1%

Other current assets7.8% 2.7% 3.4% 10.2% 3.4% 4.0% 10.3% 4.5%

Loans to stockholders 1.2% 1.0% 1.0% 0.8% 1.6% 0.9% 2.0% 2.7%

Mortgage and real estate loans0.3% 1.4% 1.3% 0.2% 0.8% 0.2% 0.1% 0.9%

Other investments22.4% 18.7% 12.6% 17.6% 7.4% 37.1% 23.4% 12.5%

Depreciable assets (net) 22.3% 51.4% 31.5% 13.0% 50.7% 20.1% 20.4% 46.4%

Intangible assets (net)9.2% 7.3% 10.4% 7.7% 2.4% 13.2% 10.0% 0.9%

Other assets9.1% 6.1% 8.4% 13.0% 2.2% 10.9% 4.6% 3.8%

TOTAL ASSETS100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Accounts payable6.8% 6.7% 5.5% 9.4% 8.2% 3.0% 6.0% 5.3%

Mortgages, notes & bonds due within 1 yr 7.0% 4.9% 6.5% 7.5% 19.6% 3.4% 7.9% 12.2%

Other current liabilities12.4% 6.2% 5.9% 18.2% 8.5% 5.7% 13.0% 5.0%

Loans from stockholders2.2% 2.6% 2.5% 2.1% 5.3% 1.1% 2.6% 5.6%

Mortgages, notes & bonds due beyond 1 yr 23.2% 41.0% 28.0% 12.5% 23.3% 36.0% 21.5% 19.5%

Other liabilities8.9% 3.1% 10.5% 13.4% 3.8% 6.6% 7.2% 4.5%

Net Equity39.4% 35.6% 41.1% 37.1% 31.3% 44.2% 41.7% 47.9%

TOTAL DEBT & EQUITY100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

ACC EUROPE'S 2007 CORPORATE COUNSEL UNIVERSITY

This material is protected by copyright. Copyright © 2007 Various authors and the Association of Corporate Counsel (ACC), and ACC Europe 53

Wholesale Trade Mining

Industry TotalWholesale Groceries

& related products

Machinery, equipment &

supplies

Miscellaneous wholesale

tradeMetal mining Coal mining Oil and gas

extractionNonmetallic

minerals

Current Ratio1.5 1.4 1.6 1.5 1.9 1.2 2.3 1.2

Debt to Equity Ratio1.9 2.0 1.8 1.9 1.2 0.8 0.8 0.8

Cash 6.1% 5.9% 6.9% 5.9% 5.6% 2.6% 3.0% 4.6%

Notes and accounts receivable28.8% 27.2% 27.8% 29.0% 5.3% 22.3% 8.5% 20.5%

Inventories24.2% 24.1% 31.7% 23.1% 5.8% 1.8% 2.1% 3.7%

Other current assets5.7% 3.5% 5.4% 5.9% 3.7% 2.7% 12.6% 5.0%

Loans to stockholders0.6% 0.9% 0.6% 0.5% 0.2% 0.4% 0.4% 0.1%

Mortgage and real estate loans0.2% 1.1% 0.1% 0.1% 0.0% 0.0% 0.0% 0.2%

Other investments11.3% 5.7% 10.2% 11.9% 23.6% 44.2% 35.1% 34.9%

Depreciable assets (net) 16.9% 22.7% 13.3% 16.9% 47.3% 19.3% 31.1% 25.3%

Intangible assets (net)3.7% 7.1% 1.2% 3.8% 1.5% 2.3% 2.7% 2.6%

Other assets2.7% 1.7% 2.7% 2.7% 7.0% 4.5% 4.5% 3.1%

TOTAL ASSETS100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Accounts payable23.6% 23.7% 19.6% 24.2% 6.1% 7.3% 4.6% 17.6%

Mortgages, notes & bonds due within 1 yr 12.7% 10.0% 18.2% 12.1% 1.5% 1.4% 1.8% 7.1%

Other current liabilities7.8% 9.3% 7.9% 7.6% 3.3% 15.4% 5.0% 3.7%

Loans from stockholders3.2% 2.1% 1.9% 3.5% 1.7% 1.0% 0.5% 0.2%

Mortgages, notes & bonds due beyond 1 yr 13.9% 19.3% 13.1% 13.6% 29.8% 7.0% 23.1% 10.8%

Other liabilities3.9% 2.7% 3.6% 4.0% 12.7% 11.3% 8.8% 6.4%

Net Equity34.9% 32.9% 35.7% 35.0% 44.8% 56.5% 56.2% 54.2%