109 of, risk best - member | soa · pdf filesession 109 of, risk management best practices in...

TRANSCRIPT

Session 109 OF, Risk Management Best Practices in Investments

Moderator:

Peter H. Sun, FSA, MAAA

Presenters: Dariush A. Akhtari, FSA, FCIA, MAAA

Samir Mathur Charles Nevins, CFA, FRM

SOA Antitrust Disclaimer SOA Presentation Disclaimer

© 2016 The Capital Group Companies, Inc.

Risk Management Best Practices

Monitoring Investment Strategies An Investment Perspective

Samir Mathur

Capital Group/American Funds

October 2016

1For financial professionals only. Not for use with the public.

© The Capital Group Companies, Inc.

Managed risk funds strategy monitoring – investment perspective

• Capital Research and Management Company (“Capital”) offers several managed risk funds in conjunction with Milliman as part of the American Fund Insurance Series (AFIS).

• The first such fund - AFIS Managed Risk Asset Allocation fund (VIMAA) - was launched end of September 2012.

• VIMAA consists of an underlying fund – AFIS Asset Allocation fund (VIAA) - and the managed-risk overlay provided by Milliman as a sub-advisor to VIMAA.

• Capital, as the investment adviser to the managed risk fund, monitors the managed risk strategy provided by Milliman.

• In this discussion I will address how we, at Capital, oversee such a strategy from an investment process perspective.

• Note, that there is an additional ongoing sub-advisor compliance and oversight process that Capital performs that will not be addressed in this presentation.

2For financial professionals only. Not for use with the public.

AFIS Managed Risk funds are designed for investors that seek to reduce their exposure to account fluctuations during periods of elevated equity market volatility. The managed risk funds pursue their investment objective by investing in shares of an underlying traditional AFIS funds and applying the managed risk strategy.

Managed Risk fund objectives:

• Seek to participate in the upside of the underlying traditional fund while lowering the risk of large account value drawdowns over equity market cycles. By the nature of the managed risk strategy and the cash component retained by the fund to implement the strategy, the managed risk fund will generally not participate in the full upside of the underlying fund and may not prevent large account value drawdowns in all market conditions.

Other considerations:

• The strategy should be scalable

• Only utilize highly liquid hedge instruments that trade under most market conditions

• Reduce the impact on the underlying AFIS funds

© The Capital Group Companies, Inc. For financial professionals only. Not for use with the public.

Managed Risk Strategy – objectives & trade-offs

Each of the American Funds Insurance Series (AFIS) Managed Risk funds has an investment objective consistent with that of its underlying fund, with the addition of “seeking to manage volatility and provide downside protection” – this leads to trade-offs which need to be kept in mind when analyzing the success of these funds

3

© The Capital Group Companies, Inc. For financial professionals only. Not for use with the public.

AFIS Managed Risk funds own shares in an underlying traditional fund, cash and hedge instruments.The AFIS managed risk strategy is designed to manage the risk associated with volatility and provide downside protection.

Managed risk funds – the basic structure

AFIS Managed Risk Funds own shares in the underlying traditional fund, cash and hedge instruments.

• The funds invest in an underlying traditional fund while maintaining a targeted level of cash to support the risk management strategy.

• The strategy incorporates two risk mitigation strategies; one to control volatility and the other to reduce downside account risk.

• Both risk management components are implemented using exchange-traded futures that are liquid, transparent and cash settle daily.

Managed risk fund

Shares of underlying traditional fund

Cash –5% to 10%

Hedge instruments

Volatility management

Capital protection

4

© The Capital Group Companies, Inc. For financial professionals only. Not for use with the public.

Source: Milliman Financial Risk Management. 1,000 stochastically generated scenarios . Each scenario contained thirty years of daily returns for indices and interest rates. The underlying portfolio consists of 58% S&P 500, 10% Russell 2000, 12% EAFE, 20% Barclays Aggregate, with 90 bps annual fee for both portfolios.

Traditional portfolio

Managed Risk portfolio

AverageReturn 9.3% 7.8%

AverageVolatility 18.7% 9.4%

Return/Vol 49.7% 83.6%

Managed risk strategy objective: more stable account values

The goal of the AFIS Managed Risk Strategy is to reduce the left tail and tighten the distribution of returns.

5

© The Capital Group Companies, Inc.

Managed risk funds strategy monitoring – investment perspective

6

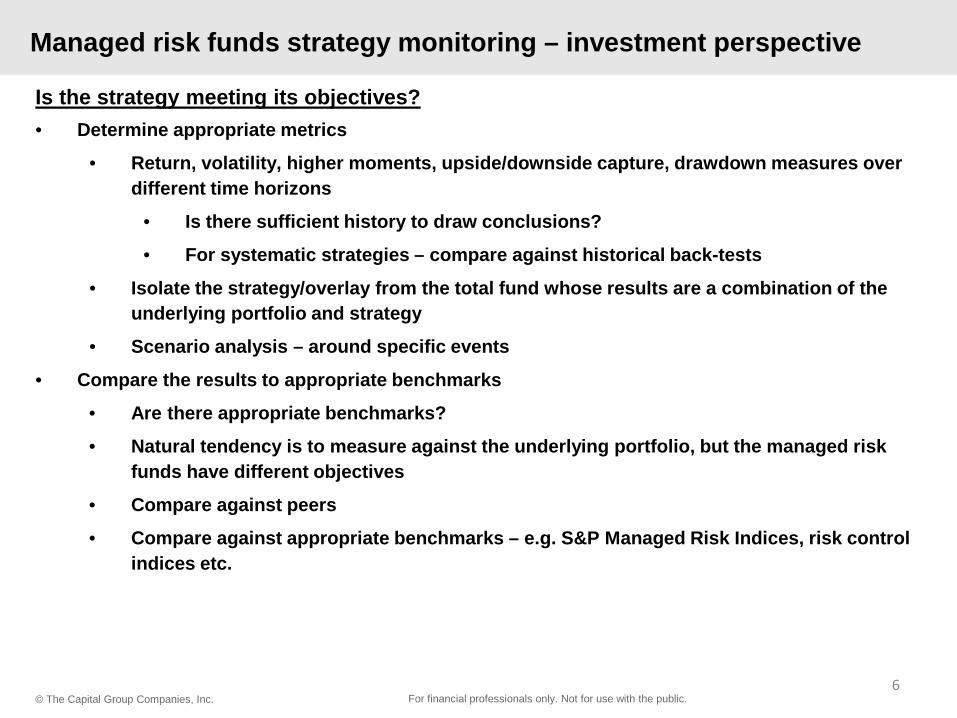

Is the strategy meeting its objectives?• Determine appropriate metrics

• Return, volatility, higher moments, upside/downside capture, drawdown measures over different time horizons

• Is there sufficient history to draw conclusions?

• For systematic strategies – compare against historical back-tests

• Isolate the strategy/overlay from the total fund whose results are a combination of the underlying portfolio and strategy

• Scenario analysis – around specific events

• Compare the results to appropriate benchmarks

• Are there appropriate benchmarks?

• Natural tendency is to measure against the underlying portfolio, but the managed risk funds have different objectives

• Compare against peers

• Compare against appropriate benchmarks – e.g. S&P Managed Risk Indices, risk control indices etc.

For financial professionals only. Not for use with the public.

© The Capital Group Companies, Inc.

Managed risk funds strategy monitoring – investment perspective

7

Is the strategy working as it is supposed to?For systematic strategies – it may be possible to replicate parts or the whole strategy

• Try to match the strategy components within tolerance bands

• Be careful about compounding the impact of strategy sub-components on the final results

• Resolve the input data issues – matching the data, dates, and pre-processing

• Determine the appropriate timing – daily/weekly/periodically

• Determine strategy advise incorporating intra-day market moves

• Address global timing considerations

• Whether to do this before the strategy trades or afterwards as a check

• Automated or manual

• Trading tolerances

• Internal and external reporting

• Determine the escalation process

• What happens when the strategy evolves?

For financial professionals only. Not for use with the public.

© The Capital Group Companies, Inc.

Managed risk funds strategy monitoring – organization & processes

8

How do you set up internal organization and processes?• Determine the multi-disciplinary group in charge of the monitoring process

• Set up regular monitoring and identify the resources

• Determine the points of contacts for regular dialog and escalation

• Set up periodic meetings with the larger group and the sub-advisor

• Have periodic internal meetings to discuss the results of the strategy and funds

• Have periodic due-diligence meetings

• Set up a process to investigate new ideas and evolution of the strategy

For financial professionals only. Not for use with the public.

Limitations and disclosures

Proprietary and confidential. Not for registered representative distribution.

Past performance is not indicative of future results. Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

Capital Group does not make any representations that products or services described or referenced herein are suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

Any discussion of risks contained herein with respect to any product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved. Investors should carefully consider investment objectives, risks, charges and expenses. This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

Capital Group does not ensure a profit or guarantee against loss.

© The Capital Group Companies, Inc. For financial professionals only. Not for use with the public.9

Chuck NevinsSenior Trader, Milliman Financial Risk Management LLCBest Practices in Investment ImplementationOCTOBER 25, 2016

FIDUCIARY: An individual in whom another has placed the utmost trust and confidence to manage and protect property or money. The relationship wherein one person has an obligation to act for another’s benefit.• Considerable Latitude• Judged by Prudence of the Process• Implementation is an Extension• Forms a Feedback Loop

2

3

Positive Impact of Technology

• Adds More Controls• Increases Speed• Lowers Transaction Costs• Allows Algorithmic Strategies• Assist in Compliance• Improves Data Dissemination

4

But Some Negative Repercussions

• Knight Capital software goes awry in 2012, results in $440m losses

• Michael Lewis bashes high-frequency trades in Flash Boys, released in 2014

• NYSE shuts down for four hours in July 2015 due to technology malfunction

5

Risk is a choice

• Effects of Prospect Theory

• The Black Swan viewpoint

• High Price of Gap Protection

• Willingness to endure the path

6

Product Choice Aligned with Strategy

• Cost• Liquidity • Collateral Requirements• Credit Risk• Tracking Error• Ability to Measure & Monitor Risk

7

8

Do you understand what it is and how it works?

9

10

Maybe it’s better than you think

BROKERS• Fees• Service (speed, completion, market impact)• Dedicated and Experienced Manpower• Purchasing Power• Assumption of Liability• Technology• Operational Efficiency• Financial Condition• Conclusion: It’s not all about explicit cost

11

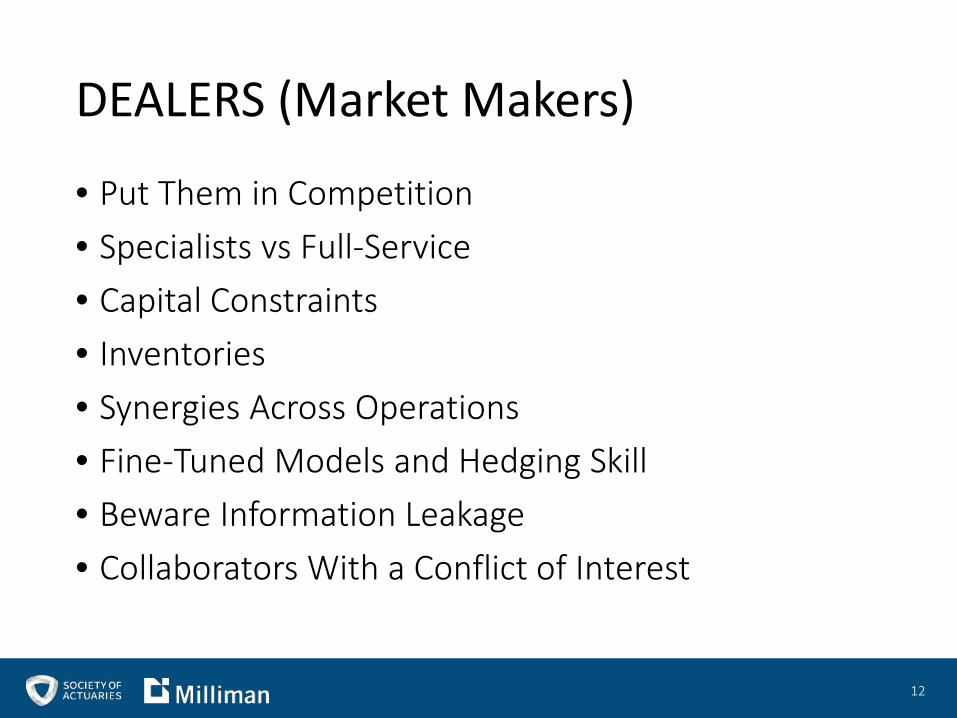

DEALERS (Market Makers)

• Put Them in Competition• Specialists vs Full-Service• Capital Constraints• Inventories• Synergies Across Operations• Fine-Tuned Models and Hedging Skill• Beware Information Leakage • Collaborators With a Conflict of Interest

12

BEST EX

• Impacts Portfolio Performance• Cannot Be Known With Certainty Ex Ante• Depends on Circumstances• Quality Assessed Over Time• Relationships and Practices Are Integral• Requires Ongoing Dedication to the Process• Provides Feedback For Strategy

13

Thank [email protected]

Session 109: Risk Management Best Practices in Investment

Dariush Akhtari

October 25, 2016

2

Agenda

Strategy

Execution/Implementation

Tracking

Governance

3

The Investment Strategy Is Determined at the Top of the House

Need to clearly define the objective of ALM

Capital appreciation

Capital preservation

• E.g., liability driven ALM in the low interest rate environment

Strategy Implementation Tracking Governance

4

An Insurance Liability-Driven Investment Strategy

Considerations for investment:

Liability characteristic

Embedded options in liabilities

Decision on hedging

Cash flows beyond liquid asset availability

What assets are used to back these?

Risk Constraints

Business Constraints

ALM

Firm’s Priority

Addressing Both Risk and Business Constraints The decision to match asset duration to that of liabilities depends on:

What is the goal?

Capital appreciation

Capital preservation

What duration to match to?

Effective duration or weighted average life?

What discount rate is used?

How are assets tagged to the insurance products?

Economic or statutory reserve

A

B

C

5

An Insurance Liability-Driven Investment Strategy

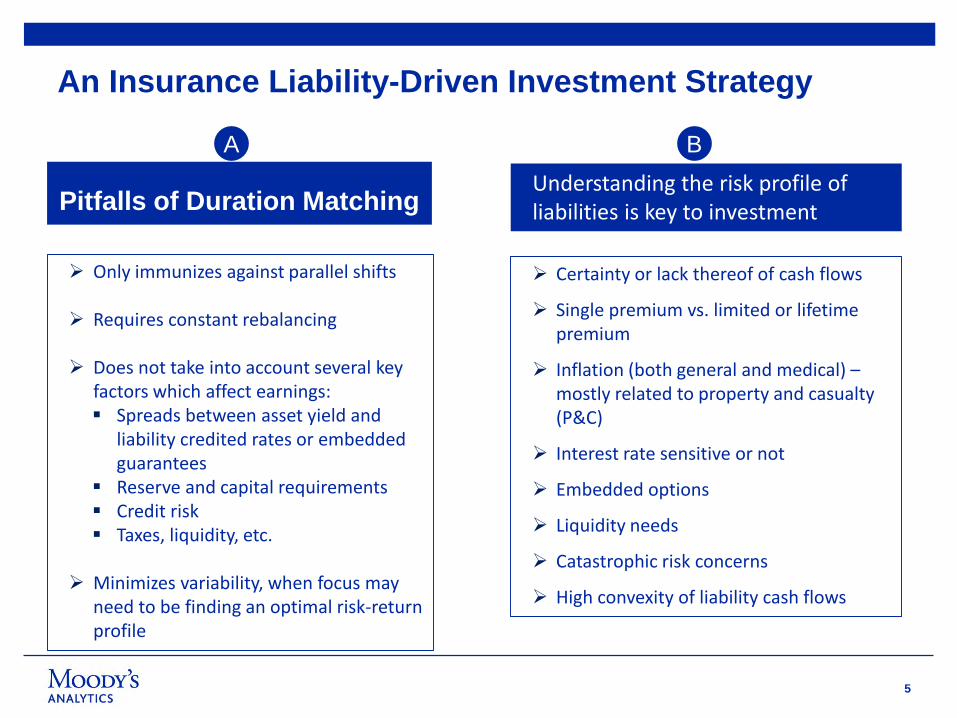

Pitfalls of Duration Matching

Only immunizes against parallel shifts

Requires constant rebalancing

Does not take into account several key factors which affect earnings: Spreads between asset yield and

liability credited rates or embedded guarantees

Reserve and capital requirements Credit risk Taxes, liquidity, etc.

Minimizes variability, when focus may need to be finding an optimal risk-return profile

A

Certainty or lack thereof of cash flows

Single premium vs. limited or lifetime premium

Inflation (both general and medical) –mostly related to property and casualty (P&C)

Interest rate sensitive or not

Embedded options

Liquidity needs

Catastrophic risk concerns

High convexity of liability cash flows

Understanding the risk profile of liabilities is key to investment

B

6

An Insurance Liability-Driven Investment Strategy

True ALM is about understanding and managing the volatility in the cash flow mismatch in all future periods (residual in the below graphs)

Common Practice Refinement

Independent discount rate

Time zero market value of asset (MVA0) (i.e., use assets’ ALM metrics for this portion of cash flows)

Independent discount rate

Eliminates the impact of the distortion of discount rate on liability’s ALM metrics

A > L A < L

Asse

t Cas

h Fl

ow (A

) Resid

ual

(L -

A)

Liab

illity

Cas

h Fl

ow (L

) Resid

ual

(L -

A)

Liab

illity

Cas

h Fl

ow (L

)

Asse

t Cas

h Fl

ow (A

)

A > L A < L

Asse

t Cas

h Fl

ow (A

) Resid

ual

(L -

A)

Liab

illity

Cas

h Fl

ow (L

) Resid

ual

(L -

A)

Liab

illity

Cas

h Fl

ow (L

)

Asse

t Cas

h Fl

ow (A

)

C

7

To Execute an Effective Strategy, One Needs to Consider the Organizational Alignment

Strategy Implementation Tracking Governance

8

Implementation Concern

In-force business

May not have an option

If possible, de-risk

Might be able through crediting rate, cost of insurance increase

Changing rider fees for VA (if possible)

New business

Not a clear cut situation – generally a bit of both

Consider competitive environment

Better to price based on available investment possibilities

Liability Investment?

9

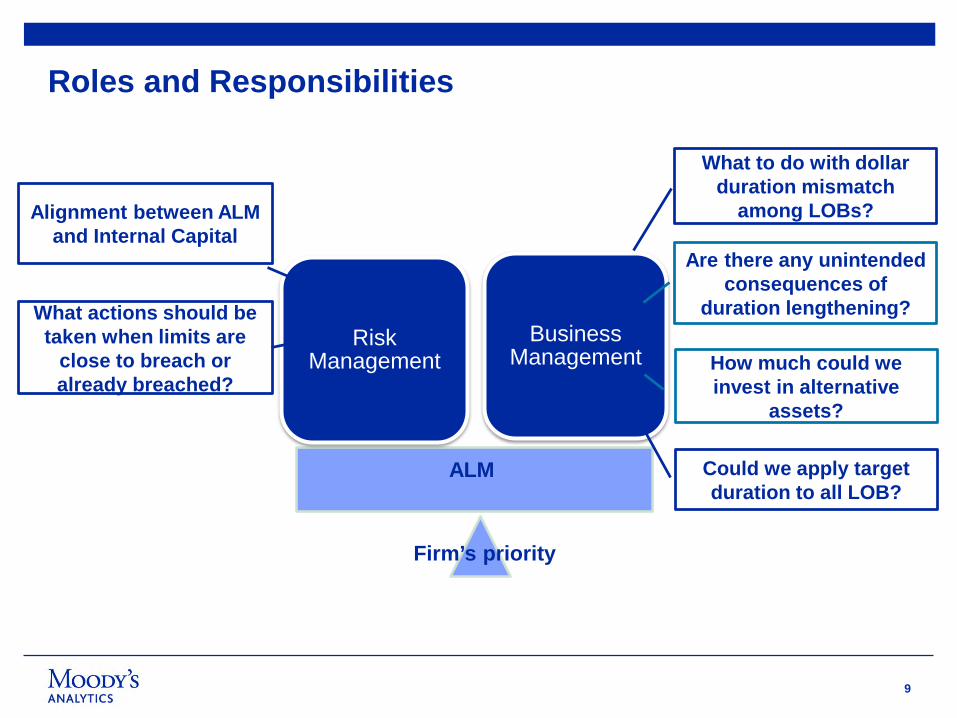

Roles and Responsibilities

Risk Management

Business Management

Firm’s priority

ALM

What to do with dollar duration mismatch

among LOBs?

Are there any unintended consequences of

duration lengthening?

How much could we invest in alternative

assets?

Could we apply target duration to all LOB?

What actions should be taken when limits are

close to breach or already breached?

Alignment between ALM and Internal Capital

10

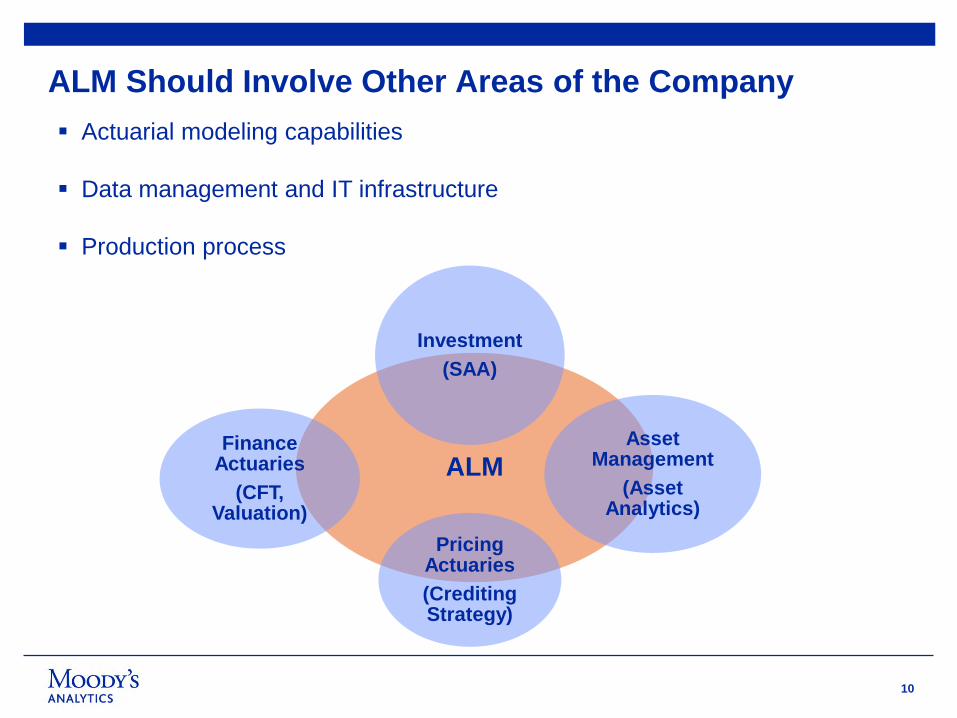

ALM Should Involve Other Areas of the Company

ALM

Investment(SAA)

Asset Management

(Asset Analytics)

Pricing Actuaries(Crediting Strategy)

Finance Actuaries

(CFT, Valuation)

Actuarial modeling capabilities

Data management and IT infrastructure

Production process

11

Strategic Asset Allocation (SAA)

Study (Brinson et al. 1986) concluded that asset allocation is the primary driver of a portfolio’s return variability1

Recent study (Vanguard 2012) found that active management has reduced a portfolio’s return and increased its volatility on average

Investment decision must take liability and other business requirements into consideration; this is an important component of ALM

SAA plays a key role in determining portfolio’s overall risk and return

Liability & Business

Requirements

SAA

Investment opportunity set; Expected return, variances, and correlation

across assets classes; Business constraints (liability cash flows) Risk constraints (duration, liquidity, and

diversification requirements) Investment return/risk target [e.g., total

return vs. net investment income (NII), book yield; variance vs value at risk (VAR)]

1 Determinants of Portfolio Performance

12

Efficient Frontier (EF) Analysis

Select investment strategy with the most attractive risk-return profileA point on the graph is superior to those below it,

which have lower returns, and those to its right, which have more risk

Select the portfolio on EF that allows for risk within the defined tolerance

Plot each strategy according to its risk-return profile

Return Measure: Average present value (PV) of distributable earnings (DE) across all scenarios

Risk Measure : Extreme percentile PV of DE among scenario results

Use ALM models to test various investment strategies

Strategy may include rebalancing current portfolio

For each investment strategy, run a set of stochastic real-world scenarios

Calculate PV of earnings for each scenario

13

Efficient Frontier Plot

1

3

4

56

7

10

11

12

15

20

30

650

700

750

800

850

900

950

1000

-50050100150200250300350400450500550600

Ret

urn

Mea

sure

Risk Measure

Average PV of distributable earnings (DE) (Y axis) vs. 5th Percentile (X axis) by Reinvestment Term

Unit of DE

Unit of DERisk Tolerance

Risk Increases

Accepted area

Min Return

14

Maintain Competitiveness While Matching Assets and Liabilities

Segment assets by insurance products

Define risk tolerance this is key

Use efficient frontier approach to allocate assets with optimal risk/reward profile

Consider various approaches to efficient frontier

Whole portfolio or a portion

Consider tax, deferred acquisition cost (DAC) unlocking, NII, etc.

Portfolio allocation vs. managing to the duration of optimal portfolio

15

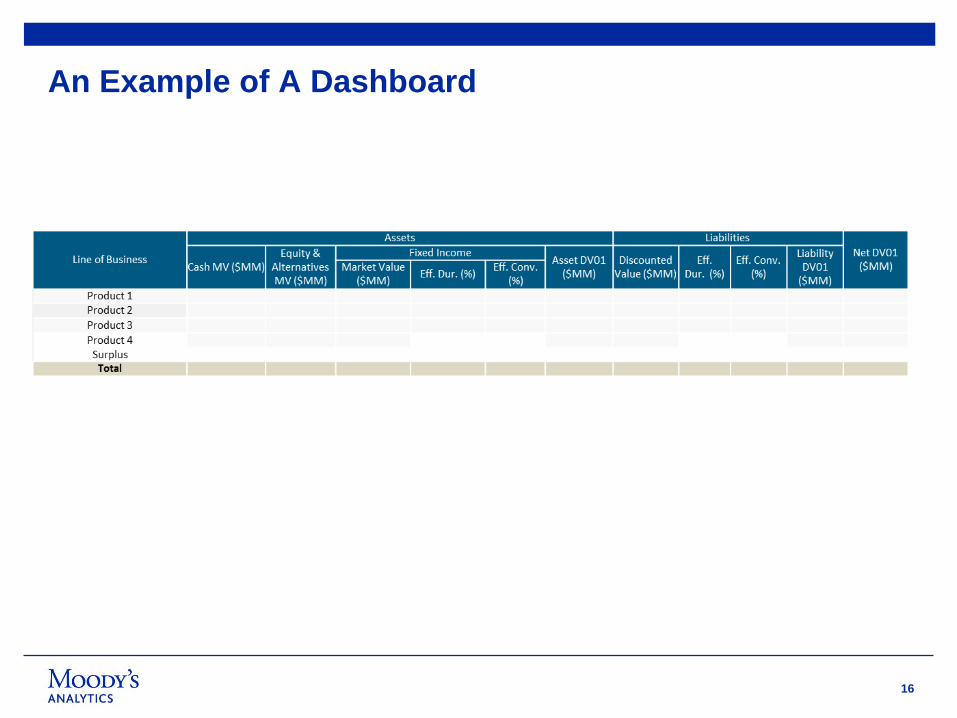

Need to Timely Track and Report Dashboards, Informing Senior Managements in Both BU and Corporate

Strategy Implementation Tracking Governance

16

An Example of A Dashboard

17

Controls Start at Every Stage of the Process

Strategy Implementation Tracking Governance

18

An Example of ALM Governance Approach

Financial actuaries review and sign-off

ERM review and challenge

ALCO

Improve governance and control process

Manage internal (actuarial) and external (non-actuarial) review and sign off

Facilitate reporting and discussions between BUs and Corporate

Document and provide governance for the key ALM activities

Enhance insight into value creation

Quantify value creation by the businesses both at issue and over time Improve ability to make investment risk-return

trade-offs

ALM

Enhance information consistency and transparency

Improve communication among relevant parties

Ensure consistent and reliable information is used across functions

Enhance operational efficiency

Streamlining production Review Reporting Process

Leverage resources and knowledge

19

Appendix

20

Matched vs. Mismatched Duration

If the goal is to manage the business through maximizing the economic surplus,

Choice of duration: matched or mismatched

• A duration mismatched method is recommended, as it provides maximum accumulated economic surplus. In fact, a naked position is even more desired.

Choice of liability discounting rate: dependent on or independent of assets backing liabilities

• Regardless of the choice of duration, results suggest that the liabilities’ discount rate should be dependent on the assets backing them

The choice of duration methodology is ultimately dependent on how the business is managed

21

Dependent vs. Independent Discount Rate

Choice of duration: matched or mismatched

• A matched duration (assuming values of assets and liabilities are equal) is desired as it lowers the standard deviation of hedge errors

Choice of liability discounting rate: dependent on or independent of assets backing liabilities• A discount rate that is dependent on the

assets backing the liabilities method is recommended, as it produces the lowest standard deviation of hedge errors

• discounting liabilities independent of the asset backing them could result in inappropriate investment

The choice of duration methodology is ultimately dependent on how the business is managed

• With the difference being that market yields of assets are used in place of book yields

• Consistent with market value of liabilities calculation under some international accounting regimes

Generally consistent with CFT method:

22

The objective of ALM framework needs to be refined to achieve an alignment with senior leadership’s expectation

If the objective is to maximize surplus using a risk/reward approach Use efficient frontier (EF) to set Target Asset Duration (TAD) Monitor DV01 and change in surplus under stress environments

If the objective is to minimize surplus volatility Align discounting of liabilities with those of assets Set Target duration to achieve DV01 and stress level tolerances

Is there a happy medium to address the above concerns?

Ultimately ALM metrics provided to the Investment team need to line up with ALM paradigm that aligns with pricing

23

© 2016 Moody’s Analytics, Inc. and/or its licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. Under no circumstances shall MOODY’S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Each rating or other opinion must be weighed solely as one factor in any investment decision made by or on behalf of any user of the information contained herein, and each such user must accordingly make its own study and evaluation of each security and of each issuer and guarantor of, and each provider of credit support for, each security that it may consider purchasing, holding, or selling.

Any publication into Australia of this document is pursuant to the Australian Financial Services License of Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569. This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001.