116th meeting of state level bankers’ committee … old meetings/slbc old data...1 the 116th...

TRANSCRIPT

1

The 116th meeting of State Level Bankers’ Committee (Punjab) will be held on 11.05.2011 at 3.00 PM at Hotel Shivalik View, Sector 17, Chandigarh. Following issues shall be taken up for discussions in the

meeting:-

Item No. 1 Confirmation of minutes of 115th Meeting of State

Level Bankers' Committee (Punjab) held on 28.02.2011

Last Meeting of SLBC 115th

Held On 28.02.2011

Minutes e-mailed/Circulated

On

11.03.2010

Comments Received NIL

As such, the house may confirm the circulated minutes.

Item

No. 2

Status report of Issues flagged in the 115th meeting of SLBC held on 28.02.2011.

2.I Incentive Scheme for Quicker Adoption of Electronic Benefit Transfer (EBT) for Government Schemes

Following districts/ blocks were allocated on 05.10.2010 on “One District One Bank” basis to banks mentioned against the names

of respective Blocks for implementation of EBT Scheme on pilot basis in the State.

Sr. No. District Block Bank

1. Amritsar Jandiala Guru PNB

2. Ferozepur Abohar SBI

116th Meeting of State Level Bankers’

Committee (Punjab)

2

3. Jalandhar Shahkot OBC

4. Ropar Chamkour Sahib UCO Bank

5. Patiala Bhuner Kheri SBOP

6. Ludhiana Samrala ICICI Bank

7. Mansa Mansa Axis Bank

The Department of Social Security (Punjab) convened a meeting of all the concerned banks on 13.11.2010 wherein

certain amendments in the MOU to be signed between the Banks and the Department were suggested. Banks requested that they needed some time for approval of the draft MOU at

their corporate level. In the meantime the process for implementation of EBT started on the basis of letter of intent

issued by the State Government.

During the deliberations in the 115th meeting of SLBC, Sh. KBS Sidhu,

IAS, Principal Secretary, Finance informed the house that progress in the Samrala & Mansa blocks in Ludhiana and Mansa districts was very good and it was decided to cover all the blocks in both districts for the purpose of EBT.

He further apprised that the progress in the other blocks was very slow. Sh S S Bhatia, FGM, PNB apprised that there was no problem in enrolment, PNB

has already enrolled 40000 pensioners however, one of the reasons for slow progress was that the banks were implementing EBT in those villages which were allotted under FIP as well. Sh. Bhatia made a reference to a letter dated

12.11.2010 from the Secretary, Department of Financial Services, Ministry of Finance, Govt. of India wherein it was requested that State Government should help to resolve the issue of overlap in EBT and FIP by conferring with

SLBC Banks.

Sh. G K Singh, IAS, Director, Deptt. Of Social Security Women & Child

Development apprised the house that the pension accounts opened under EBT are in the joint names of Government and the individual Pensioners. The account cannot be operated for any purpose other than for payment of

pension, thus the account cannot be converged with an account opened under FIP. Shri Jasbir Singh, Regional Director, Reserve Bank of India,

Chandigarh apprised that if that be the position then FIP and EBT are to run independently and cannot converge.

3

It was decided that the matter may be sorted out in the meeting of Sub Committee already constituted for the purpose under the Chairmanship

of Sh K B S Sidhu Principal Secretary (Finance) Government of Punjab.

The representative of IF&B has informed in the 1st Steering committee meeting held on 26.04.2011, that the issue will first be discussed in the Cabinet only then the meeting of sub-committee can be convened.

The representative of DIF&B may apprise the latest progress to the

House.

2.II Debt Swap Scheme – Raising the Limit of loan under the Scheme

In the 114th meeting of SLBC held on 30.11.2010 the above issue was thoroughly discussed and the house approved the proposal of raising the limit under Debt Swap Scheme from Rs. 50,000/- to Rs. 1,00,000/- . At the

same time controlling heads of banks were requested to get the same approved from their respective boards. The Boards of PNB, OBC, Union Bank

of India & SBI have approved the raised limit under Debt Swap. During the 1st Steering committee held on 26.04.2011,the

representative of SBOP,Corporation Bank, Satluj Gramin Bank & Punjab Gramin bank has confirmed that their boards has raised the limit.

Other member Banks are requested to apprise the house of the decision of their respective boards on the issue.

Item No. 2.III Progress under Debt Swap Scheme

It was decided in Hon’ble Finance Minister’s meeting that at least 3% of

disbursement of agriculture credit during the year is to be earmarked for

giving loans under “Debt Swap Scheme”. Accordingly it was desired that banks provide 3% of the targeted flow under agriculture sector for “Debt Swap Scheme”.

4

The progress achieved up to March 2011 is as follows:

(Amount Rs. in Lakh)

Target for Debt Swap (on the basis of 3% of Agri.)

Ach. Under Debt Swap 2010-11 up to March

2011

%age Ach.

91414 10011 10.95 (Bank wise progress is as per Annexure 1(a)

The achievement is 10.95% of the targets and needs

improvement.

The House may review.

2.IV Financial Literacy in School Curriculum During the deliberations in the 115th meeting of SLBC held on

28.02.2011, the Director IF&B apprised the house that the matter for inclusion of Financial Literacy in School Curriculum has been forwarded to the

Chairman, Punjab School Education Board, but nothing has been heard from their end. Chairman of the meeting requested the Director, IF&B to take up the matter at appropriate level so that financial literacy is included in the

school curriculum from the next session i.e. 2011-12 .

In this regard the Convener Bank also took up the matter with Deptt. Of Institution Finance & banking.

The representative of IF & B (Pb) may apprise the latest position in

this regard.

2.V Designating a Nodal Police Station for accepting complaints in relation to counterfeit notes received at the bank branches

It was decided in the meeting of Hon’ble Governor with State

Government officers & bankers on 15.10.2010, that a nodal Police Stations at

5

district level be designated for accepting complaints in relation to counterfeit notes received at the bank branches.

Director, IF&B apprised in 114th meeting of SLBC that the matter has

been taken up with the Home Department, Govt. of Punjab. It was resolved that Nodal Police Station at district level be got finalised at the earliest.

The Controlling Heads of Banks were also requested to convey the

name of the designated Nodal branch at the district level for reporting the

complaints of their branches in that district in relation to counterfeit currency notes. The information so far has been received by the Convener Bank from

SBI, PNB & Citizen Urban Coop. Bank. The Controlling Heads of the remaining Banks are again requested to convey the name of such branches to Convener Bank.

The representative of Department of IF&B apprised in the 1st Steering committee held on 26.04.2011that the matter is pending with the Home

Department of the State.

The representative of Department of IF & B (Pb) may apprise

the house of the latest status of designating the nodal police station

at each district in the State.

2.VI Allotment of Land for Establishment of RSETIs

During the deliberations in the 115th meeting of SLBC held on 28.02.2011,it was apprised by Sh. S S Johal, IAS, Joint Development Commissioner, IRD, Government of Punjab that land has been allotted in 15

districts, and in the remaining districts the matter is under consideration of Department.

The representative of SBOP apprised that the number of candidates sponsored for training in RSETI is not adequate. Shri Johal assured the house that the matter would be taken up with the DRDA in the next meeting

scheduled to be held shortly.

Convener bank vide its letter dated 15.03.2011 has taken up the matter with the Department of Rural Development requesting them to allocate

6

land in the remaining districts and also for sponsoring the adequate number of candidates for training.

The representative of Department of Rural Development may

apprise the house of the latest developments in the matter of allocation of land in remaining 5 Districts where land is yet to be allocated for setting up of RSETIs.

Execution of Lease Deed

The lease deed sent by Department of Rural Development (Pb) under

the cover of their letter dated 28.02.2011 was forwarded to corporate office of Convener Bank on 09.03.2011 who suggested minor changes, which have

been brought to the notice of Rural Development Department for their remedial action.

The representative of Department was also requested in the 1st meeting

of Steering Committee for approval of the changes in the lease deed at the earliest.

The representative of Rural Department is requested to apprise the latest position in this regard.

Functioning of RSETIs from Existing Buildings

In the following districts RSETIs have started functioning from the existing State Government / banks buildings till permanent arrangements for

raising/constructing the buildings are made :

Sr.No. District Lead Bank Name of Institution whose

building being used

1. Mohali PNB BDPO Office, Majri

2. Ferozepur OBC LDM Office, Ferozepur

3. Ludhiana PSB LDM Office, Ludhiana

4. Moga PSB LDM Office, Moga

5. Faridkot PSB LDM Office, Faridkot

6. F G Sahib SBOP BDPO Office, Fatehgarh Sahib

7

7. Bathinda SBOP Red Cross Bhawan, Bathinda

8. Sangrur SBOP Panchayat Bhawan, Sangrur

9. Mansa SBOP Sale cum Training Centre, Mansa

10 Muktsar SBOP Training cum Production Centre, Village Chak Bir Sarkar, Muktsar

11 Barnala SBOP ITI (Boys), Barnala

12 Patiala SBOP Panchyat Bhawan Building, Patiala

13 Jalandhar Canara Bank/ Syndicate Bank/

SDME

RUDSETI, Jalandhar

14 Ropar U co Bank Zila parishad building Ropar

RSETIs proposed to be started from Existing Buildings

The feedback available from Department of Rural Development / Lead District Managers reveals that in the following remaining districts RSETIs have been proposed to be started from the existing State Government / banks

buildings till permanent arrangements are made :

Sr.

No.

District Name of Institution whose building

would be used

1 Amritsar BDPO Office, Harsha Cheena

2 Gurdaspur Panchayat Building, Chawa

3 Hoshiarpur BDOP Office

4 Kapurthala Panchayat Bhawan

5 Nawanshahr DC Office

6 Tarn Taran Panchayat Building Village Sheron

The representative of Rural Development Department is

requested to apprise the house of the latest position.

8

Item

No.3.I

High Level Committee to Review Lead Bank Scheme-

Providing Banking Services in every Village having population of over 2000 by March 2012.

After the allocation of total 1576 unbanked villages in the State of Punjab with population of more than 2000, to different banks on the basis of

Service Area Approach for implementation of Financial Inclusion Plan in providing the banking services in these villages, the Controlling Heads of the Banks were requested to get approved the roadmap from the respective

boards specifically mentioning the time period (roadmap) and the mode of technology to be used in this regard.

Status of Financial Inclusion Plan-Road Map & Progress

The information in this regard, is summarized as under:

Year Model Proposed to be used

Brick &

Mortar Model

ICT

based BC Model

Others

( Mobile Banking)

Total

2010-11 37 645 0 682

2011-12 11 883 0 894

Progress

Achieved

31 794 - 825

(Bank wise roadmap is as per Annexure-1)

(Bank wise progress achieved is as per Annexure-11)

The bank wise detail are as under. The representatives of the Banks implementing the FIP in the State of Punjab are requested to apprise during discussions, the latest position of FIP in their bank.

Punjab National Bank (368): As per the FIP plan finalized by the bank,

the banking services in the allocated 368 villages are to be provided through ICT based BC model in 359 villages whereas 9 villages are to be covered by Brick & Mortar branches. The road map provides that 159 villages were to be

9

covered upto by March 2011 and all the 368 villages ( on cumulative basis) are to be covered during the year 2011-12.

After completing the process of approving, the Technology Service Provider (TSP) and Business Correspondents (BCs), banking services have been

provided in 160 villages besides deploying 159 BC agents and opening of 1 branch through brick and mortar model and imparting training to 119 to such BC agents.

State Bank of Patiala (265): Bank shall be implementing it through ICT based BC Model and Brick & Mortar branches. 115 villages were to be covered

by March 2011 and remaining in the next fiscal year. Further out of 265 villages, 15 villages will be covered through brick & mortar branch and the

remaining through BC Model.

Bank has opened branches in 15 allocated villages and completed the process of providing services through BC Model in 100 allocated

villages.

State Bank of India (175): Bank shall be implementing it through ICT based BC Model and brick and mortar branch . Out of 175 villages, 37 were to

be covered during first quarter, 32 in second quarter and remaining 82 in third & 24 in fourth quarter of 2010-11.

Bank has started providing banking services through BC Model in 138 allocated villages and in 7 other villages services have been provided by opening bank branches.

Punjab & Sind Bank (230): Bank shall implement it through ICT based BC

Model and Brick and mortar model. Out of 230 villages, 200 villages were to be covered by March-2011 and 10 through brick and mortar model and other 190 villages through ICT based BC/BF Model. Out of the remaining 30

villages 10 will be covered by brick and Mortal model and the remaining 20 by ICT based BC/BF model and it would be covered by March-2012.

Bank has started providing banking services by opening of branches in 10 allocated villages and in 190 villages the services have been

started through BC/BF Model.

Oriental Bank of Commerce(116): Bank shall be implementing it through

(ICT based BC Model). As per the revised plan bank was to provide services to

10

40% of villages by December 2010 and remaining villages was to be covered by March 2011.

Bank have started providing banking services through BC Model in 49 allocated villages.

UCO Bank (39): It is proposed to cover 40% of allocated villages during 2010-11 and remaining villages were to be covered in next year 2011-12

through Business Correspondent Model. It was also proposed to provide mobile branch banking services through a van which will cover at least 8-10 villages. Further the bank was to cover 4 villages by December 2010 and 5

villages in the last quarter of this 2010-11.

Bank has started providing banking services through BC Model in 39

allocated villages.

Allahabad Bank (12): As per the revised plan of the Bank all the 12 allocated villages will be covered upto March-2012, and it would be through

ICT based BC Model.

Bank of India (40): As per the revised plan of the Bank services to 5 allocated villages will be provided by March 2011 and the remaining 35

villages would be covered by March-2012, and it would be through ICT based BC Model in 32 villages and in remaining 8 villages in will be provide through

Brick and mortar model.

Bank has started providing banking services through IT based BC Model in 32 allocated villages and in 8 villages services have been

provided through Brick & mortar model

Bank of Baroda (19): The bank planned for providing services in 19 allocated villages by March-2011, and it would be through ICT based BC Model.

Bank has started providing banking services through BC Model in 2 allocated villages.

BOM (1): The services to the allocated village would be provided by ICT based BC Model by March 2012.

Canara Bank (30): Out of 30 allocated villages, services in the 17 allocated villages will be provided up to March-2011 and 12 villages would be covered by March-2012 and it would be through ICT based BC Model, services in

11

remaining 1 village will be provided up to march-2012 and it will be through brick & mortar model.

Bank has started providing banking services through BC Model in 17 allocated villages.

Central Bank of India (44): As per revised plan submitted by the Bank, out of 44 allocated villages, bank to cover all the allocated villages in the year 2011-12 and it would be through ICT based BC Model.

Corporation Bank (2): The services have been provided in the 2 allocated villages by the Bank through ICT based BC Model.

Indian Bank (8): Bank would implement it through ICT based BC Model and

out of 8 villages, 2 were to be covered by 31.03.2011, and remaining 6 by 31.3.2012.

Bank has started providing banking services through BC Model in 2

villages.

Indian Overseas Bank (18): All 18 allocated villages would be covered by ICT based BC Model & 75% of these villages were to be covered by Dec.

2010 and remaining 25% by March 2011.

Bank has covered all the allocated villages by providing banking

services through BC Model in 18 allocated villages.

Syndicate Bank (3): The services have been provided in the 3 allocated

villages through BC/ICT Model.

Vijaya Bank (2): As per the revised plan the services in the 2 allocated villages will be provided by Mar-2012 through BC/ICT Model.

Union Bank of India (27): The Bank would be implementing it through BC model and out of 27 villages, 2 villages were to be covered by September 2010, 5 villages (on cumulative basis) by December 2010, 9 by March 2011,

16 by June 2011, 20 by September 2011, 24 by December 2011 and 27 by March 2012.

Bank has covered all allocated 27 villages by providing banking services through BC Model in 27allocated villages.

12

Punjab Gramin Bank (94): As per revised plan submitted by the bank,

the services in all the 94 allocated villages will be provided by March-2012 and it will be through ICT based BC model.

Malwa Gramin Bank (42): The banking services were to be provided in 7 allocated villages by March-2011 and the remaining 35 villages will be covered by March-2012 and, through ICT based BC Model.

Satluj Gramin Bank (24): Bank would be implementing it through ICT based BC model and as per the revised plan all the allocated villages would

be covered by March-2012.

Local Capital Area Bank (1): The services were to be provided in 1 allocated village by march-2012 it would be through Brick & Mortar branch.

Bank has provided banking services in the village allocated to it under FIP.

ICICI Bank (3) & Bank of Rajasthan (1): The services would be provided in 3+1 allocated villages through ICT based Model. The services to 3 allocated

villages to ICICI Bank were to be provided by December 2010 and in 1 village allocated to erstwhile BOR would be completed by February 2011.

Bank has started providing banking services through BC Model in 3

allocated villages.

HDFC Bank (8): The services would be provided in 8 allocated villages

through ICT based BC/ Mobile Banking Model and 2 villages would be covered by March 2011 & remaining 6 by March 2012.

J & K Bank (1 village): The services would be provided in 1 allocated village by March 2011 through ICT based BC Model.

Axis Bank (4 villages): The bank would provide services to the allocated

villages by March 2012 through ICT based BC Model.

The controlling heads of banks are requested to implement the Financial

Inclusion Plan as per the approved roadmap and ensure that the services to the allocated unbanked villages are provided as envisaged by RBI.

13

Further, Monthly progress report on Financial Inclusion Plan(FIP) is

required to be submitted before 5th of every month to Ministry of Finance, New Delhi. Besides a quarterly statement on Financial

Inclusion consisting of annexure „A‟ & „B‟ is submitted to Reserve Bank of India before 10th day of the close of the quarter. It has been observed these statements are not submitted in time to Convener

Bank by the banks thereby leading to an avoidable delay in consolidation and submission to MoF/RBI. The Controlling Head of the banks are again requested to submit the progress reports/

statements within 3 days from the end of the month/quarter so that the consolidated progress is submitted to Ministry of Finance /

Reserve Bank of India.

FIP Misc. Issues:

1. Oriental Bank of Commerce has informed that village Taragarh in Amritsar District is already having branch of The Amritsar Central Cooperative Bank Ltd, Dharar

village in Amritsar District also has a branch of Punjab Gramin Bank Jehangir camp at Dharar. Further they

have informed that village Lalpura in Tarn Taran district is already having Branch of The Tarn Taran Central Cooperative Bank Ltd. Similarly village Matta in Faridkot

District is having of Central Coop. Bank.

Convener Bank took up the matter with respective LDMs and

they have confirmed that the bank branches were already existing in all these villages.

2. State Bank of India has informed that 3 villages viz

Banur, Kuraran and Gajju Majra in Patiala district allocated to them for Financial inclusion are already having their branches in these three villages.

Convener Bank vide its letter dated 07.02.2011 has taken up the matter with LDMs Patiala they have confirmed vide their

letter dated 16.02.2011 that the branches were already existing in all these villages.

3. State Bank Of Patiala has informed that their

sponsored Bank (Malwa Gramin Bank) has been allocated 43 villages under FIP. Keeping in view the

14

limited technology available with Malwa Gramin bank & constraint of manpower, SBOP has decided to cover

the villages allocated to Malwa Gramin Bank in the year 2011-12.

4. LDM SBS Nagar has reported that village Tansa allocated to Punjab National Bank is already banked. Similarily LDM Hosiarpur has reported that village

Jalalpur, & Dholwaha allocated to Punjab National Bank are already banked at the time of villages allocation of these under FIP.

Since all the above reported villages are reported

banked by the Bank/LDMs, so the above villages may be deleted from the FIP plan.

The unbanked village under FIP allocated to Malwa

Gramin Bank sponsored by SBOP, the matter may please be discussed at the level of DCC.

During the 1st Steering Committee meeting held on 26.04.2011, DGM Reserve Bank of India apprised the house that some banks have reported villages

allocated to them as covered, whereas on sample survey it has been observed that only enrollment has been done by some banks whereas the villages was reported as covered to SLBC. She advised all the controlling head of banks to

report the village as covered only when the whole process is completed.

House may discuss.

Item no. 3.I Allocation of all villages with a population of 1000

plus In the meeting held at Ministry of Finance in December 2010 for reviewing the

progress made in the implementation of Financial Inclusion Plans (FIPs) by the Public Sector Banks, one of the issues came up for discussion pertaining

to SLBC Convener Banks was that a plan to allocate all villages with population of 1000 plus be made in a honeycomb fashion around the FIP villages allocated to banks(and BCs) through the SLBC mechanism.

15

During the deliberation in the 1st Steering Committee held on 26.04.2011,the issue was discussed and the house was of the view that the process of

coverage of villages having population above 2000 be covered.

The house may discuss

3.II Credit Deposit Ratio – Implementation of the Recommendations of Expert Group on CD Ratio

As per the recommendations of an Expert Group constituted by GOI under the Chairmanship of Shri Y.S.P. Thorat, the then MD, NABARD a Special Sub-Committee (SSC) of District Level Consultative Committee (DLCC) was to

be constituted in districts with CDR of less than 40%, for drawing up “Monitorable Action Plans” (MAPs) to increase the CDR on a self set

graduated basis. Concerned LDM of the district will be convener of SSC with DCO, DDM, NABARD, LDO, RBI and District Planning Officer as its members.

SLBC (Pb) observed that CD Ratio as at September 2005 of 4 districts i.e. Hoshiarpur, Jalandhar, Kapurthala and Nawanshahr was below 40% and it

was decided that a Special Sub Committee (SSC) of District Level Consultative Committee (DLCC) be constituted. As per feedback available from concerned LDMs, the SSC of these districts were constituted and its meeting (s) have

been convened and the details of the Monitorable Actionable Points and other suggestions made are given below:

A) Conduct of meetings of SSC and Monitorable Action Plans (MAPs)

The conduct of the meetings of SSC alongwith the Monitorable Action Plan drawn up for increasing CD Ratio is as follows:-

District Date of Meeting Monitorable Action Plan

Jalandhar 10.01.2006 25% by 31.03.2006 40% by 31.03.2010 60% by 31.03.2015

Kapurthala 10.01.2006 23% by 31.03.2006 40% by 31.03.2010 60% by 31.03.2015

Nawanshahar 10.01.2006 18% by 31.03.2006 35% by 31.03.2009 60% by 31.03.2015

Hoshiarpur 11.01.2006 28% by 31.03.2006 40% by 31.03.2009 60% by 31.03.2012

16

B) Suggestions to improve the CD Ratio

The CD Ratio of a district/ region is dependent on various credit and non - credit inputs and during the meetings at various districts the following

suggestions have been given to improve the CD Ratio:-

B i) Credit Inputs Banks to formulate and implement area/ block specific credit schemes,

Investment credit under agriculture be strengthened and for which activities like dairy, poultry, bee keeping, fishery etc. should be

encouraged, NABARD has already prepared Project Reports of 140 activities, which

should be studied and entrepreneurs may be motivated to undertake

these activities and banks should provide financial assistance, Banks to make analysis and monitor CD Ratio of each branch and

initiate suitable measures to improve the same.

B ii) Non Credit Inputs

Special Economic Zones (SEZ) be set up to attract the establishment of

new medium/ big industrial units,

The level of infrastructure needs further improvement for smooth conduct of business.

Special fiscal incentives may be provided in line with the neighbouring

States like HP & J&K to attract new units and to retain the existing units,

Cluster approach may be adopted by providing special package for development of industry,

NRIs should be encouraged to make investments in establishment of

new units.

The Convener Bank has advised the LDMs of these districts requested controlling heads of banks to monitor the CD Ratio on continued basis as suggested by RBI.

17

C) CD Ratio of Identified Districts as at 31.03.2011

During 105th meeting of SLBC it was observed that emphasis should be on providing adequate credit by banks to all sectors of the economy.

Further, as NRI deposits have dual effect on CD Ratio i.e. these enhance the level of deposits being the denominator of the ratio and also do not create any fresh demand for credit as the activities from where these savings have

been generated are being performed in the countries where the NRIs are residing/ working and as such the numerator of the ratio is not influenced. In view of this, it was resolved that CD Ratio of these districts net of NRI

deposits should be calculated and reviewed vis– a- vis Monitor able Action Plan in the meetings of SLBC.

The comparative position of Monitorable Action Plan and CD Ratio (net of NRI deposits) as at March-10 & March-2011 of these four districts is given

below:- District CD Ratio

as per MAP CD Ratio %

(including NRI Deposits) as at

Mar.10

CD Ratio %

(including NRI Deposits) as at

Mar.11

Growth Mar11/

Mar.10 (PPs)

CD Ratio %

(Net of NRI Deposits) as at

Mar.10

CD Ratio %

(Net of NRI Deposits) as at

Mar.11

Growth Dec. 10/

Dec. 09 (PPs)

Jalandhar* 60 (Mar.15)

35.32 37.08 +1.76 49.50 45.86 -3.64

Kapurthala 60 (Mar.15)

31.67 33.28 +1.61 40.55 43.58 +3.03

Nawanshahr 60

(Mar.15)

24.77 29.57 +4.80 37.70 37.86 +0.16

Hoshiarpur 60 (Mar.12)

31.78 28.65 -3.13 40.25 47.00 +6.75

Observations:-

The CD Ratio (including NRI deposits has increased, as well as net of

NRI deposits is increased as at March-2011 over March-2010 in all the

three districts. The concerned LDMs are requested to continue to review the CD Ratio

in the meetings of Special Sub Committee of DCC so as to reach the next target of CD ratio as envisaged under Monitorable Action Plan.

During 115th meeting of SLBC, it was apprised that the economy of these districts was predominantly agrarian & new industrial units were not

coming up and resultantly the credit absorption capacity of the district is low.

18

Further the Credit growth is out weighted by growth in Deposits, thus restricting substantial growth in CD Ratio.

The House may review the CD Ratio vis a vis MAP to improve

CD Ratio of these identified districts. 3.III Non Availability of Insurance Cover for Construction of

Poly/Green House

During the deliberations of 112th & 113th Meeting of SLBC, while

analyzing the reasons of low-performance under LOI cases of NHB, it was observed that one of the reasons was non-availability of Insurance Cover from

any Insurance Company for construction of Poly Houses/ Green Houses due to which the farmers were hesitant to undertake such activities and bankers were also not coming forward to extend credit under this activity. After the

discussions, it was resolved that matter may be taken up with concerned authorities for exploring the feasibility of providing insurance cover to this upcoming activity.

The Convener Bank vide letters dated 23.08.2010 & 03.11.2010 took

up the matter with Insurance Regulatory & Development Authority (IRDA) Hyderabad requesting them to design a suitable insurance product for Poly/Green Houses.

The house was apprised that IRDA is a regulatory body, the matter

may be taken up with some non life insurance company to develop a product for this upcoming activity. Shri S C Agrawal, IAS, Chief Secretary, Govt. of Punjab advised the representative of ICICI bank to take up with ICCI Lambard

to devise a similar product for Poly/ Green Houses.

In this regard, Convener Bank took up the matter with ICICI Bank, vide

letter dated December 22,2010 to inform if ICICI LOMBARD can devise suitable scheme for coverage in raising of Poly/Green houses.

In the 115th SLBC Meeting of SLBC Punjab while deliberating upon

the issue it was informed by representative from ICICI Bank that ICICI

Lombard has devised an Insurance Product for providing cover for construction of Poly/ Green Houses. A copy of the letter dated 28-2-

2011 of ICICI Lombard containing the gist of the insurance cover for poly/ green house was also circulated among member banks vide dated 15.03.2011.

19

Now Convener Bank has been informed by Insurance Regulatory

and Development Authority that M/s New India Assurance Co. Ltd. has informed that their company has Comprehensive Floriculture Insurance

Product covering flower crops cultivated in Poly House. The Department of Horticulture is requested to consider issuance of LOI in respect of Poly/ Green Houses as farmers can avail the facility of insurance cover

from M/s New India Assurance Co. Ltd.

This is for information of the house.

3.IV Interest Subsidy Scheme for Housing the Urban Poor

(ISHUP) The Government of India, Ministry of Housing Urban Poverty Alleviation

has recently launched the Interest Subsidy Scheme of Housing for Urban Poor (ISHUP) to address urban housing shortage in the country. The scheme provides for interest subsidy of 5% per annum on loan amount upto Rs. 1

lakh for Economically Weaker Section (EWS) and Rs. 1.60 lakh for Low Income Group (LIG) segments in the urban areas for construction or

acquisition of a new house. It is expected to create additional housing stock of 3.10 lakh houses for EWS/LIG segments over next 4 years (2008-12).

The scheme is to be implemented by primary lending institutions (PLIs), viz, Scheduled Commercial Banks and Housing Finance Companies. The

National Housing Bank (NHB) and HUDCO have been designated as Nodal Agencies for administration & release of the subsidy.

The scheme was sent by NHB to RBI, IBA and all Scheduled Commercial Banks for implementation. The guidelines of the scheme have also been forwarded to member Banks by Convener Bank vide its letter dated

29.07.2009 for necessary action in the matter.

The National Housing Bank vide its letter dated 01.4.2010 has forwarded a specially designed common loan application form under ISHUP to be obtained from the applicant by the banks. As desired, a copy of the said

common loan application form has been sent by the Convener Bank to all controlling heads of banks vide its letter dated 15.04.2010.

20

However, in the absence of potential assessment and district – wise targets under ISHUP, banks are not able to make breakthrough in this

regard. The issue of slow pace of implementation of the scheme was discussed in detail during the 111th meeting of SLBC (Pb) held on 19th May

2010. After the deliberations, it was resolved that the SUDA/ Department of Local Bodies will work out the district wise potential of target beneficiaries and convey the same to the Convener Bank for further allocating the bank wise

targets. The Joint Secretary, Ministry of Housing & Urban Poverty Alleviation.

Government of India convened a meeting on 8th June 2010 of Conveners of SLBC of all States. In the meeting the chairman has expressed his concern

over NIL progress under the scheme in the State and emphasized that district wise potential of target beneficiaries may be worked out by the concerned State agencies. The Convener Bank vide its letter dated 10.6.2010 requested

SUDA & Department of Local Bodies accordingly so that district wise / bank wise targets can be allocated.

During the deliberation in the 1st Steering Committee meeting held on 26.04.2011,the representative of SUDA apprised the house that

PMIDC (Punjab Municipal Infrastructure Development Committee) has been designated as nodal agency for the state under the scheme. The representative of SUDA was requested to send a copy of the letter to the

convener bank for further circulation.

The representative of SUDA further informed that the potential survey is not yet completed.

The representative of SUDA may apprise the latest position in

this regard.

Item No. 4 Agriculture Debt Waiver & Debt Relief Scheme 2008 –

Fresh Lending

Fresh Lending – Progress up to Mar- 2011

During the meetings of SLBC it was observed that the ultimate objective of the Debt Waiver & Debt Relief Scheme is to provide fresh loan to the distressed farmers so that they can restart their farming/economic activity.

21

The progress of the same up to Mar., 2011 is given below;

(Amount Rs. in Lakh)

Agency Crystallization of Claims Under Waiver

& Relief

Fresh Loans Disbursed to beneficiaries of Waiver &

Relief

Accounts Amount Accounts Amount

Public Sector Banks

140557 42945 40550 56371

Private Sector

Banks

1517 2429 8 58

RRBs 8142 3008 3605 4935

Cooperative Banks 202298 45302 24919 13801

Total 352514 93684 69082

(19%)

75165

(80%)

(Bank wise information is as per Annexure III)

Observations

Banks in Punjab have provided fresh credit to the extent of Rs. 75165 lakh, which is 80.23% of total waiver & relief provided, covering 69082

accounts i.e.19%of farmers benefited under the scheme.

The Public Sector Banks have provided fresh loans to the extent of Rs.

56371 lakh which is 131.26% of the amount of waiver & relief covering 29% of farmers benefited under the scheme.

RRBs have provided fresh loans to the tune of 164.06% of the amount

of waiver & relief to 44% of farmers covered under the scheme.

The cooperative banks have given fresh loans to the extent of 30.46% of the amount of waiver & relief covering 12% of the farmers under

the scheme.

In the 108th meeting of SLBC it was observed that the performance of Cooperative banks in providing fresh assistance under the scheme was low. Reacting to this, the representative of Cooperative Bank apprised that most of

the farmers under the scheme were chronic defaulters and they had stopped making transactions with Primary Agriculture Credit societies (PACS) and may

22

have shifted to other banks for availing their fresh credit facilities. Further, Cooperative Banks are providing fresh credit to all those farmers who had

approached them under the scheme and their bank is not denying credit to such farmers.

The Controlling Heads of Banks are requested to ensure that fresh loans are disbursed to all the farmers who had received the

benefit of the Debt Waiver and Debt relief Scheme 2008.

Item No 5. Financial Literacy cum Credit Counseling Centre.

The consolidated performance of these FLCCs, up to March 2011, is

given below:-

(Amount Rs. in Lakh)

Particulars Number of persons who made enquiries

No. of persons who availed services

Amount mobilized/ disbursed/

Invested

Durin

g current

Quarter

Cumul

ative

During

current Quarter

Cumulative During

current Quarter

Cumul

ative

Deposit A/Cs 791 26066 318 19297 100 14739

Credit

Related

1061 22387 384 11069 559 21931

Education Loans

91 2554 28 1353 48 3549

Debt Swap 83 1204 7 610 306 530

Industrial

Loans

26 530 4 259 70 1191

Guidance on

investments other than banking

services

246 2299 167 966 56 337

Total 2298 55040 908 33554 1139 42277 (Center wise information is as per Annexure IV)

23

Observations

Up to March-2011, Financial Literacy cum Credit Counseling Centre in

Punjab have entertained enquiries from 2298 persons out of which 908persons have availed the services after getting counseling from the centers.

Out of the above,791persons made enquiries about Deposit Schemes

of banks, 1061 enquiries were credit related, 91 persons enquired

about the Education Loan Scheme, only 83 enquiries were made about the Debt Swap Scheme of Banks, 26 persons enquired about

Industrial loans and as many as 246 enquires were made in respect of investments & other than banking services.

Further individual centre wise analysis reveals that the functioning of

the centres at Fatehgarh Sahib, Ferozepur, Mansa & Patiala requires

more publicity.

The House may review the performance of FLCCs. Model Scheme of FLCC – RBI‟s Guidelines

After setting up FLCCs in all the 20 districts of the State the progress

achieved by these centers is being reviewed in the each meeting of SLBC. However, RBI vide circular dated 4.2.2009 has given Model Guidelines for functioning of FLCCs. A copy of the Model Guidelines has already been sent

by the Convener Bank to all the Lead Banks (which have established FLCCs ) for compliance.

The Corporate Office of PNB, taking cognizance of the Model Guidelines, has approved the plan for ensuring that all the FLCCs of the bank in 7 lead

districts of the State function as per the Model Guidelines of RBI. During the deliberations in the 114th meeting of SLBC, Regional

Director, Reserve Bank of India desired that the Controlling heads of banks

running FLCCs should confirm specifically that these are functioning as per the Model Scheme of RBI.

In the 4th meeting of Steering Committee held on 27th Janauary,2011 representative from member banks except OBC have confirmed that the

24

FLCCs under their control, are functioning as per the Model Scheme of RBI. In Oriental Bank of Commerce, FLCC is being headed by a permanent

employee of the Bank and the same is not strictly as per RBI Model Scheme.

Now OBC has also confirmed that their FLCC is functioning as per the Model Scheme of RBI.

This is for information of the house.

Item No. 6 Review of Performance of Banks (Excluding

Cooperative Banks) in Key Areas relating to Deposits, Advances & Priority Sector Advances.

The comparative position of key banking parameters is given below;

(Amount Rs. in crore)

Parameter As At Variation

March

2009

March

2010

March

2011

March. 2010 /

March. 2009

March. 2011 /

March. 2010

Absolute %age Absolute %age

Branches 3209 3429 3808 220 6.9 379 11.05

Agg. Dep. 119145 131759 154558 12614 10.6 22799 17.30

Advances 81807 98187 120705 16380 20.0 22518 22.93

PS Adv. 41547 50119 61671 8572 20.6 11552 23.04

Agri. Adv. 19780 25225 31966 5445 27.5 6741 26.72

Adv. to Small

Enterprises

13000 17510 22001 4510 34.7 4491 25.64

Weaker Sector

Adv.

8910 10765 14259 1855 20.8 3494 32.45

DRI Adv. 9 13 14 4 44.4 1 7.69 (Bank-wise position as at March 2011 is given in Annexure V)

6. I Branch Expansion

379 new branches of Commercial Banks were opened in the State

during the period from 1st April 2010 to 31st March 2011, thus raising the

25

network of branches from 3429 as at 31st March – 2010 to 3808 as at March - 2011.

Further, area wise analysis in regard to branch expansion is

summarized below:-

Number

of Branches

As At Variation

March. 2009

March 2010

March 2011

March 2010 / March 2009

March 2011/ March 2010

Absolute Absolute

Rural 1212 1278 1406 66 128

Semi Urban

964 1062 1209 98 147

Urban 1033 1089 1193 56 104

Total 3209 3429 3808 220 379

Observations

During the review period, increase in number of branches/ conversion of extension counters of banks in Semi Urban area of Punjab was of the order of 147

This is followed by rural areas, which registered an increase of

branches/ conversion of extension counters is 128

Whereas, the increase of branch network is 104 in urban areas.

This is for the information of the House.

6.II Deposit Growth

The aggregate deposits of the Banks in Punjab increased by Rs. crore, from Rs.131759 crore as at March 2010 to Rs. 154558 crore as at

March 2011, thus posting a growth of 17.30% as against an increase of 10.06 % during the corresponding period last year.

26

Further area wise analysis is summarized below:-

(Amount Rs. in Crore)

Aggregate

Deposits

As At Variation

March 2009

March 2010

March 2011

March 2010 / March 2009

March. 2011 / March. 2010

Absolute %age Absolute %age

Rural 27638 30865 35455 3227 11.7 4590 14.87

Semi

Urban

40994 45792 60040 4798 11.7 14248 31.11

Urban 50513 55102 59063 4589 9.1 3961 7.18

Total 119145 131759 154558 12614 10.6 22799 17.30

Observations

During the review period, the deposits in urban areas have grown by 7.18%,

Whereas, the same in semi urban areas have gone up by 31.11 % and in rural areas the deposit growth is 14.87 %.

This is for the information of the House. 6.III Credit Expansion

The gross credit in the State increased by Rs. 22518 crore, from Rs.

98187 crore as at March 2010 to Rs.120705 crore as at March 2011, thus exhibiting a growth of 22.93% as against an increase of Rs. 16380 crore or 20 % during the same period last year.

Further area wise analysis in regard to credit expansion is summarized

below:- (Amount Rs. in Crore)

Total

Advances

As At Variation

March 2009

March 2010

March 2011

March 2010 / March 2009

March 2011 / March 2010

Absolute %age Absolute %age

Rural 41310 15946 19994 1816 12.9 4048 25.38

Semi

Urban

22087 26578 39316 4491 20.3 12738 47.92

Urban 45590 55663 61395 10073 22.1 5732 10.29

Total 81807 98187 120705 16380 20.0 22518 22.93

27

Observations

During the review period, the growth in outstanding advances in urban

areas was10.29%, Whereas in semi urban & rural areas it was 47.92% &25.38%

respectively.

This is for the information of the House.

6. IV. i a) Overall CD Ratio

The comparative position of overall CD Ratio of Commercial Banks is as below:-

Period CD Ratio % Variation

March 2009 68.7

March 2010 74.5 +5.8

March 2011 78.1 +3.6 (Bank wise CD Ratio as at March-2011 is per Annexure VI .i).

Observations

During the period under review overall CD Ratio of Commercial Banks

for the State of Punjab witnessed an increase of 3.6 PPs from 74.5 % as at

March 2010 to 78.1 % as at March 2011. The incremental CD Ratio for the review period is 98.77 % which is a very healthy sign.

The House may review the overall CD Ratio.

6. IV. i b) CD Ratio - Rural Areas

The comparative position of CD Ratio of rural areas in Punjab is as follows,

(Amount Rs. in crore)

Period Rural Variation PPs Deposit Advances CD Ratio %

March 2009 27638 14130 51.13

March 2010 30865 15946 51.66 +0.53

March 2011 35455 19994 56.39 +4.73

28

Observations

During the review period, the CD Ratio of Rural areas has registered an increase of 4.73 PPs from 51.66% as at March 2010 to 56.39 % as at

March 2011. This is for the information of the House.

6. IV. i c) CD Ratio - Semi Urban Areas

The comparative position of CD Ratio of Semi Urban areas in Punjab is as follows,

(Amount Rs. in crore)

Period Semi Urban Variation

PPs Deposit Advances CD Ratio %

March 2009 40994 22087 53.88

March 2010 45792 26578 58.04 +4.16

March. 2011 60040 39316 65.48 +7.44

Observations

During the review period, the CD Ratio of Semi Urban areas has witnessed an increase of 7.44 PPs from 58.04 % as at March 2010 to 65.48

% as at March. 2011. This is for the information of the House.

6. IV. i d) CD Ratio - Urban Areas The comparative position of CD Ratio of urban areas in Punjab is as

follows, (Amount Rs. in crore)

Period Urban Variation PPs Deposit Advances CD Ratio%

March 2009 50513 45590 90.25

March 2010 55102 55663 101.00 +10.75

March 2011 59063 61395 103.94 +2.94

29

Observations

During the review period, the CD Ratio of Urban areas has witnessed an

increase of 2.94 PPs from 101 % as at March 2010 to 103.94 % as at March 2011.

This is for the information of the House.

6.IV.ii CD Ratio on the basis of credit as per utilization and

Resource support under Rural Infrastructure Development Fund of NABARD

As per the information available, NABARD has provided resource

support of Rs. 1950.14 crore up to March 2011 to Punjab Government under

RIDF for development of infrastructure. When we add this amount of Rs. crore to the credit provided by banks and calculate the CD Ratio on the basis of Credit Utilization (Cu) + RIDF, the same works to 79.40 %.

6. IV. iii) Credit plus Investment to Deposit Ratio

To work out the “Credit plus Investment to Deposit Ratio”,

investments made in the State Govt. bonds by the banks, Rs.884.26

crore have been added to the credit provided by banking system in the State and resultantly the flow of credit has gone up to Rs. 13882 crore. For the

period ended March 2011 the “Credit plus Investment to Deposit Ratio” is as follows:-

(Amount Rs. in crore)

Deposits Advances plus investments in State Government bonds

(C+I)/D Ratio

163106

132281 78.7

(77%) (% figures in brackets denote position as at March 2011)

6.IV. CD Ratio of Financial System

The CD Ratio of Financial System after inclusion of Deposits & Advances of the Cooperative Banks, Punjab Agriculture Land Development Banks and Financial Institutions comes to 81.17 % as per detail given as under:-

30

( Rs. in Crore) S.N. Particulars Deposits Advances CD

Ratio

1. Commercial Banks 154558 120705 78.09%

2. Including Cooperative Banks 163107 129479 79.38%

3. Including Punjab Agri. Dev. Banks*

163107 131660 80.72%

4. Including Financial Institutions**

163107 132406 81.17%

*Advances PADB (Rs. 2452 crore) **Financial Institutions PFC (Rs. 180 crore), PSIDC (Rs. 186 Crore), SIDBI (Rs. 380 crore).

The CD Ratio of Financial System as at March 2010 was 78.2%.

This is for information of the House.

6.V Priority Sector Advances

During the period under review, the Priority Sector Advances in Punjab grew by Rs.11552 crore, from Rs. 50119 crore as at March 2010 to Rs. 61671 crore as at March 2011 thus showing a growth of 23.04 % as against

an increase of Rs.8572 crore or 20.6 % during the corresponding period previous year.

The share of incremental PS advances to incremental advances during

the period under review is 51.30%.

6.VI Agriculture Advances

The Agriculture Advances in the State during the period under review witnessed an increase of Rs. 6741 crore, from Rs.25225 crore as at March

2010 to Rs.31966 crore as at March 2011 thus showing a growth of 26.72% as against an increase of Rs. 5445 crore or 27.5 % during the same period last year.

6.VII Advances to Micro & Small Enterprises

The advances to Micro & Small Enterprises during the period under review registered an increase of Rs. 4491 crore, from Rs. 17510 crore as at

31

March 2010 to Rs. 22001 crore as at March 2011, thus showing a growth of 25.64% as against an increase of Rs.4510 crore or 34.70% during the

corresponding period previous year.

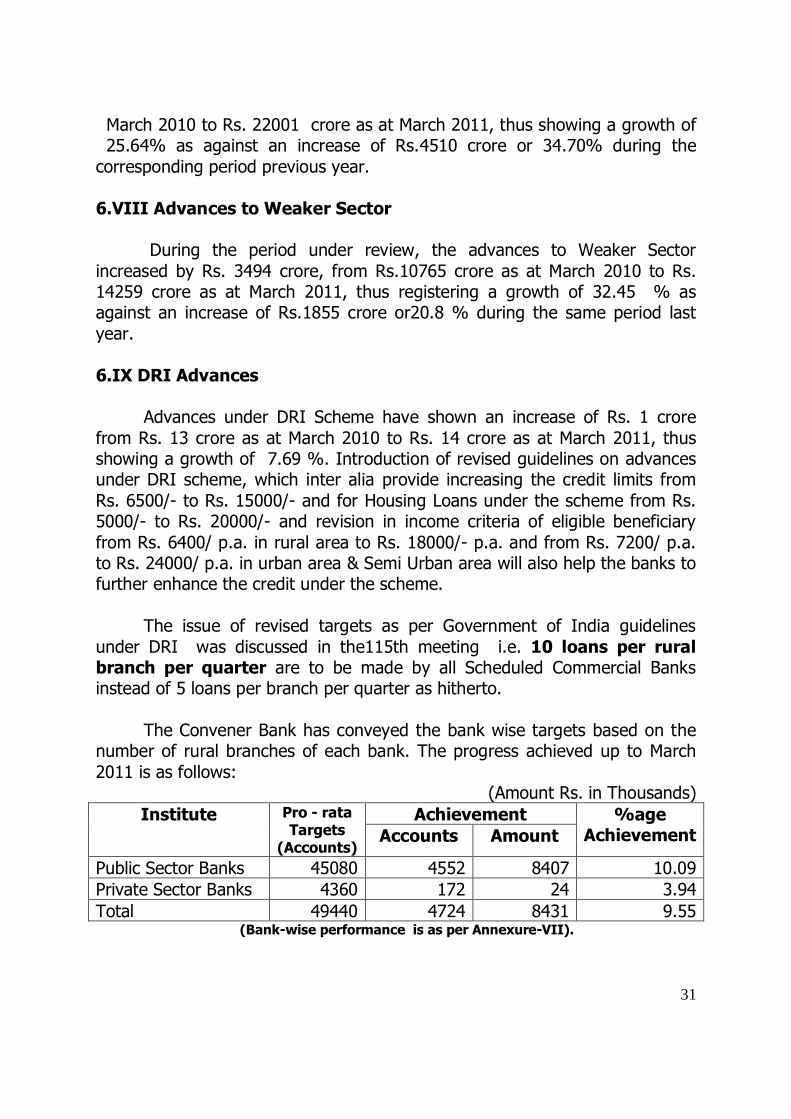

6.VIII Advances to Weaker Sector During the period under review, the advances to Weaker Sector

increased by Rs. 3494 crore, from Rs.10765 crore as at March 2010 to Rs. 14259 crore as at March 2011, thus registering a growth of 32.45 % as against an increase of Rs.1855 crore or20.8 % during the same period last

year.

6.IX DRI Advances

Advances under DRI Scheme have shown an increase of Rs. 1 crore

from Rs. 13 crore as at March 2010 to Rs. 14 crore as at March 2011, thus showing a growth of 7.69 %. Introduction of revised guidelines on advances under DRI scheme, which inter alia provide increasing the credit limits from

Rs. 6500/- to Rs. 15000/- and for Housing Loans under the scheme from Rs. 5000/- to Rs. 20000/- and revision in income criteria of eligible beneficiary

from Rs. 6400/ p.a. in rural area to Rs. 18000/- p.a. and from Rs. 7200/ p.a. to Rs. 24000/ p.a. in urban area & Semi Urban area will also help the banks to further enhance the credit under the scheme.

The issue of revised targets as per Government of India guidelines

under DRI was discussed in the115th meeting i.e. 10 loans per rural branch per quarter are to be made by all Scheduled Commercial Banks instead of 5 loans per branch per quarter as hitherto.

The Convener Bank has conveyed the bank wise targets based on the

number of rural branches of each bank. The progress achieved up to March

2011 is as follows: (Amount Rs. in Thousands)

Institute Pro - rata Targets

(Accounts)

Achievement %age Achievement Accounts Amount

Public Sector Banks 45080 4552 8407 10.09

Private Sector Banks 4360 172 24 3.94

Total 49440 4724 8431 9.55 (Bank-wise performance is as per Annexure-VII).

32

The controlling heads of banks are requested to initiate suitable steps for improving the progress and achieving the

targets for number of loans under DRI scheme.

6.X Review of National Goals

According to latest guidelines of RBI, the banks are to achieve the

National Goals on Adjusted Net Bank Credit (ANBC) as at the end of previous year instead of NBC and for calculation of ANBC the outstanding FCNR (B) and NRNR deposit balance will no longer be deducted for computation of ANBC,

which now will be Bank Credit plus investments made in non – SLR bonds HTM category. It may be difficult for banks to arrive at such figures at State

level and as such the review of National Goal is made on the basis of Net Bank Credit as at the end of previous year, which means gross credit minus inter bank credit.

The comparative position relating to achievement of National Goals in the State is given below:-

Sr. No

Particulars Goal %

%age Position as on

March 2009

March 2010

March 2011

a) Priority Sector Adv. to Net

Bank Credit

40 58 61 63

b) Agriculture Adv. to Net Bank

Credit

18 28 31 27

Out of above

i) Direct Agri. Adv. to Net Bank Credit

13.5

21

23

20

ii) Indirect Agri. Adv. to Net

Bank Credit

4.5 7 8 7

c) Weaker Sector Adv. to Net

Bank Credit

10 12 13 15

d) DRI Adv. to Total Adv. of Pre. Year

1 0.001 0.016 0.13

e) CD Ratio (Rural & Semi Urban) 60 53 55 62

f) Women Beneficiaries Advances

to NBC

5 5.8 6.3 6.80

[Bank-wise performance under National Goals is as per Annexure-VI (i) to (iii)].

33

Observations:

The ratio of Priority Sector Advances to Net Bank Credit as at March 2011 stands at 63% as against National Goal of 40%.

The share of Agriculture Advances to Net Bank Credit, as at March 2011 is 27% against the National Goal of 18%.

The share of Direct Agriculture Advances to Net Bank Credit is

20% against National Goal of 13.5% and share of Indirect Agriculture Advances is 7% against National Goal of 4.5%.

The advances to Weaker Sector are 15% of Net Bank Credit, as

against National Goal of 10%. In order to ensure achievements of sub targets of lending to weaker sector, RBI has advised banks to

contribute an aggregate amount of Rs. 2000 crore to Micro Small & Medium Enterprises (MSME) (Refinance) Fund with SIDBI in advance on the basis of the bank’s projected shortfall in achievement of targets of

10% for lending to weaker section category as on last Friday of March 2009.

The Ratio of DRI advances to total advances of previous year

although was below the level of 1%, yet it has shown improvement frm 0.016% as at March 2010 to 0.13% as at March 2011.

The CD Ratio of Rural & Semi Urban area is 62 % against the national goal of 60%.

The advances to Women Beneficiaries constitute 6.80 % of Net Bank

Credit, against the National Goal of 5%.

The House may review.

6.XI(a) Advances under Education Loan Schemes The comparative progress is as follows;

(Amount Rs. in Crore)

Year Accounts Balance O/S

Increase

Absolute %age

March 2009 26201 641.86

March 2010 32836 880.31 115.45 15.1%

March 2011 32312 1144.17 263.86 29.97% (Bank-wise position as at March 2011 is as per Annexure-VIII).

34

During the period under review, the advances under Education Loan schemes of banks witnessed an increase of Rs.263.86 crore from Rs. 880.31

crore as at March 2010 to Rs. 1144.17 crore as at March 2011, thus showing growth of 29.97 % as against increase of Rs. 115.45 crore or 15.1% during

the same period last year. The House may review the progress.

6.XI(b) Collateral Free Education Loans & Position of NPA

outstanding in Education Loans

As per RBI guidelines “…. Banks must not, mandatorily obtain

collateral security in case of education loans upto Rs. 4 lakh”.

As per RBI guidelines the banks are required to grant collateral free

education loan upto Rs. 4 lacs. The need to implement the guidelines of RBI was also emphasized in the 115th meeting of SLBC. Further, it was also

resolved that in the progress achieved by banks in this regard may also be reviewed in the meetings of SLBC. Accordingly, the Convener Bank has collected the data which is placed below in respect of quarter ended March

2011.

Amt . in lakhs

Number of Education Loan accounts outstanding as at quarter ended March 2011

Amount of Education Loan outstanding as at quarter ended March 2011

Out of 2, NPA outstanding as at quarter ended March 2011

%age of NPA under Education Loan as at quarter ended Dec 2010

Out of 2, education loan granted collateral free

Out of 5, NPA outstanding as at quarter ended March 2011

1 2 3 4 5 6

34012 1170.73 35.02 2.99 353.60 18.33 ( Bankwise detail as per annexure- VIII(i))

The house may discuss.

35

6.XII Advances to Minority Communities

The comparative position is given below:

(Amount Rs. in Crore)

Minority Community

March 2009

March 2010 %age Growth

March 2011 %age Growth

A/Cs Amt. O/S

A/Cs Amt. O/S

A/Cs Amt. O/S

Muslims 11977 182.38 13472 205.92 12.9 14059 229.29 11.3 Christians 6689 88.21 8071 123.27 39.7 8826 116.94 -10.5 Budhists 2221 7.66 2085 4.93 -35.6 2363 20.57 41.72 Zoroastrians 43 0.45 38 0.57 26.7 64 0.93 61.29

Total 20926 278.62 23666 334.68 20.1 25312 367.73 9.86 (Bank-wise position as at March 2011 is as per Annexure-IX).

The overall advances to minority communities have registered an increase of Rs. 33.05 crore, from Rs. 334.68 crore as at March 2010 to Rs.367.73 crore as at March 2011, thus showing a growth of 9.86 %.

During the quarter ended March 2011, banks disbursed advances to the tune of Rs. 25.43 crore to borrowers belonging to minority communities. The

bank-wise position is given as per Annexure X.

The House may review the performance.

6.XIII Advances to Women Beneficiaries

The comparative position of advances to women beneficiaries is given below:-

(Amount Rs. in Crore)

Year Accounts Amt. O/S Increase

%age to Net Bank Credit

Absolute %age

March 09 228784 4172.24 424.08 11.3 5.8

March 10 240589 5141.52 969.28 23.2 6.3

March 11 274255 6679.59 1538.07 29.91 6.8 (Bank-wise position as at March-2011 is as per Annexure- XI).

The overall advances to women beneficiaries witnessed an increase of Rs. 1538.07crore from Rs. 5141.52 crore as at March 2010 to Rs.6679.59

36

crore as at March 2011, thus registering a growth of 29.91 %. In the State of Punjab, the share of advances to women beneficiaries to Net Bank

Credit as at March 2011 stands at 6.80%, against the target of 5%. The bank-wise position in respect of advances to women beneficiaries to total advances

as at March 2011 is given as per Annexure VI (iii). During the quarter ended March 2011, banks disbursed advances to the

tune of Rs.445 crore to women beneficiaries. The bank-wise position is given at Annexure-XII.

The House may discuss please.

6.XIV Advances to SC Beneficiaries The comparative position of advances to SC beneficiaries is given as

under:- (Amount Rs. in Crore)

Year Accounts Balance Outstanding

Increase

Absolute %age

March 2009 173567 1368.11 153.58

March 2010 179395 1569.39 201.28 14.7%

March 2011 185890 1966.52 397.13 25.3%

[Bank-wise position as at March 2011 is given in Annexure- V (iii)].

The overall advances to SC beneficiaries witnessed an increase of

Rs. 397.13 crore during the period under review, from Rs.1569.39 crore as

at March 2010 to Rs. 1966.52 crore as at March 2011, thus showing a growth of 25.3%, as against an increase of Rs.397.13 crore or25.3% during the same

period last year.

The House may review please.

37

Review of Govt. Sponsored Schemes & Programmes

Item No. 7.1 Government Sponsored Schemes. A) Total Assistance

(Amt. Rs. in Lakh) Particulars 2009-10

March 10 2010-11

March 11

No. Amt. No. Amt.

Total number of Beneficiaries (both SHGs & Individual Swarozgaris) to

whom loans have been sanctioned

12775 - 10130

Out of which

SC Beneficiaries (Target being 50% of total)

9434 (74%)

- 7767 (76%)

Women Beneficiaries

(Target being 40% of the total)

6552 (51%)

- 6316 (62%)

Handicapped Beneficiaries

(Target being 3% of the total)

84 (0.7%)

- 54 (0.5%)

Target of Credit Disbursement - 2582 2970

Total Credit Disbursed - 4183 3147

% age Achievement - 162% 106%

B) Through Self Help Groups Particulars 2009-10

March 10 2010-11 March 11

No. Amt. No. Amt.

Number of Self Help Groups formed 1009 - 788 -

Number of SHGs undertaking economic

activities

785 - 590 -

Number of members of SHGs undertaking economic activities

5845 - 5112 -

Out of which

SC Beneficiaries

(Target being 50% of total)

4617

(79%)

- 4070

(79%)

Women Beneficiaries

(Target being 40% of the total)

5187

(89%)

- 4775

(93%)

Handicapped Beneficiaries

(Target being 3% of the total)

33

(0.6%)

- 27

(0.5%)

Loan disbursed - 1422 1204

Subsidy disbursed - 612 458

Total assistance - 2034 1662

Average assistance per member (Target)

- 0.25 0.25

Average assistance (Achievement) - 0.35 0.33

38

C) Individual Swarozgari Progress

(Amt. Rs. in Lakh)

Particulars 2009-10 March 10

2010-11 March 11

No. Amt. No. Amt.

Number of cases sponsored 8601 - 6784

Cases sanctioned 6930 - 5018

Out of which

SC Beneficiaries

(Target being 50% of total)

4817

(70%)

- 3697

(73%)

Women Beneficiaries

(Target being 40% of the total)

1365

(20%)

- 1541

(31%)

Handicapped Beneficiaries

(Target being 3% of the total)

51

(0.7%)

- 27

(0.53%

Loan disbursed - 2761 1943

Subsidy disbursed - 847 714

Total assistance - 3608 2657

Average assistance per member (Target)

- 0.25 0.25

Average assistance (Achievement) - 0.51 0.53 ( District wise progress is as per Annexure XIII)

( Progress upto 31.03.2011 is tentative as informed by the Deptt. Of Rural Development, Punjab)

The Department of Rural Development in consultation with SLBC (Pb) has chalked out the following quarterly schedule for disposal of cases under

SGSY:

Quarter Target for Disbursement

During the Qtr. Cumulative

I 15% 15%

II 20% 35%

III 30% 65%

IV 35% 100%

Observations:

As against annual target of Rs. 2970 lakh for credit disbursement, banks up to March 2011 have sanctioned loans amounting to Rs. 3147 lakh, the %age achievement works to

106%.

The targets of average assistance stand achieved both under individual swarozgaris as well as under SHGs.

39

Similarly the cumulative targets of assistance to SC & women beneficiaries also stand exceeded.

However, the benchmark for providing assistance to handicapped beneficiaries has been missed.

On cumulative basis, 76% SC beneficiaries have been sanctioned loan against target of 50% under the scheme and 62% women beneficiaries have been sanctioned loan against target of 40% under the scheme,

whereas the achievement of handicapped beneficiaries is 0.5% against the goal of 3%.

The House may discuss and review the progress please.

7.II Micro Financing – Self Help Groups

The summary of progress made in implementing the concept of Self Help Groups both under the Scheme of SGSY and Normal Lending up to 31.03.2011 is given below:

SHGs

As on 31.03.2010

SHGs

As on 31.03.2011

Gap

between formed & credit

linked as on

31.03.11

From 01.04.10

up to 31.03.2011

No. of

SHGs formed

No. of

SHGs credit linked

No. of

SHGs formed

No. of

SHGs credit linked

No. of

SHGs formed

No. of

SHGs credit linked

22779 [19128]

14777 [15349]

25446 [5326]

(22779)

16468 [15723]

(14777)

8978 [3529]

2667 [2260]

1691 [2510]

(Bank wise progress is as per Annexure XIV).

(District wise Progress is as per Annexure XV).

Figures in brackets [ ] denote amount Rs. in lakh - savings & credit linked

Figures in brackets ( ) denote position relating to the same period previous year

40

Observations

Up to 31.03.2011, 25446 Self Help Groups have been formed out of which 16468 Groups have been linked with the bank finance since

inception of the scheme. These groups include groups formed under SGSY (7786) of beneficiaries

living Below Poverty Line (BPL) and groups formed in general category

(17666 ), which also include beneficiaries other than living below BPL. Further, 6318 groups have been linked with bank credit under SGSY and balance 10150 groups linked with credit are under general scheme

of banks. The gap between the SHGs formed & linked with bank credit is 8978.

During the period ended upto March 2011, in all together 2667 Groups have been formed and 1691 have been credit linked.

The pace of formation & credit linkage of SHGs needs to be further

accelerated.

The House may discuss the bank wise progress.

7. III Prime Minister Employment Generation Programme

(PMEGP) Progress achieved Programme Year 2010-11 up to 31.03.2011.

KVIC has informed the following progress under PMEGP for the year 2010-11 up to 31.03.2011;

Particulars KVIC KVIB DIC Total

Rural Urban

Target

No. of Projects 282 282 188 188 940

Margin Money (Rs. in Lakh)

395.19 395.19 263.45 263.45 1317.28

Employment 2820 2820 1880 1880 9400

Progress*

Cases disbursed 159 209 455 823

Margin Money Released

615.81 448.02 711.69 1775.52

Employment 1550 1880 4150 7580

* The progress achieved pertains to cases carried over of previous year.

41

Observations:

As against annual target of release of Margin Money of Rs. 1317.28 lakh up to 31.03.2011 , banks have released Margin

Money to the extent of Rs. 1775.52 lakh. The % age achievement comes to 134.78 %.

The House may review the progress.

During the deliberation in the 1st Steering Committee meeting held on 26.04.2011,the representative of KVIC has informed the house that the scheme was initially launched by the Government of India for the 4 years. The

year 2011-12 is the last year as per the instructions of Govt. of India, he requested all the controlling heads of the banks that all the pending cases be

cleared so that there should not be any problem for claiming of subsidy and for settlement of cases sponsored.

The house agreed that up to 15.06.2011 all pending cases will be cleared and all the controlling heads of the Banks will submit a certificate in

this respect to the SLBC.

Action: Banks

7.IV Swarn Jayanti Shahari Rozgar Yojana (SJSRY)

As per the progress report received from SUDA, during the current Financial Year 2010-11, up to March 2011, Local Urban Bodies have

sponsored 72 cases out of which banks have sanctioned/disbursed loans in 64cases.

As the issue was pending with SUDA for a long time, during 113th meeting of SLBC (Pb) held on 22nd September 2010, Shri S. C. Agrawal, IAS, Chief Secretary, Government of Punjab & Chief Guest of the meeting desired

that the matter may be referred to Principal Secretary, Local Bodies for accelerating the process of appointing/designating coordinators at the district

level so that the sponsoring of cases under the scheme can be started.

42

The Convener Bank vide letter dated 14th October 2010 has requested The Principal Secretary, Local Bodies, Government of Punjab for getting

expedited the process of appointment of coordinators at the district level.

The representative of SUDA apprised that in the1st Steering committee held on 26.04.2011 that during last two year i.e. 2009-10 & 2010-11 no funds were released by the Government only tentative funds were released.

Now on 31st March-2011 Government of Punjab has released its share and Government of India will release the funds in due course. Further the Government of India has not fixed any target under the scheme.

DGM Reserve Bank of India has desired that steps be taken for implementation of the scheme and the matter should be taken up by the

department for the same. The representative of SUDA may apprise about the latest

position in this regard.

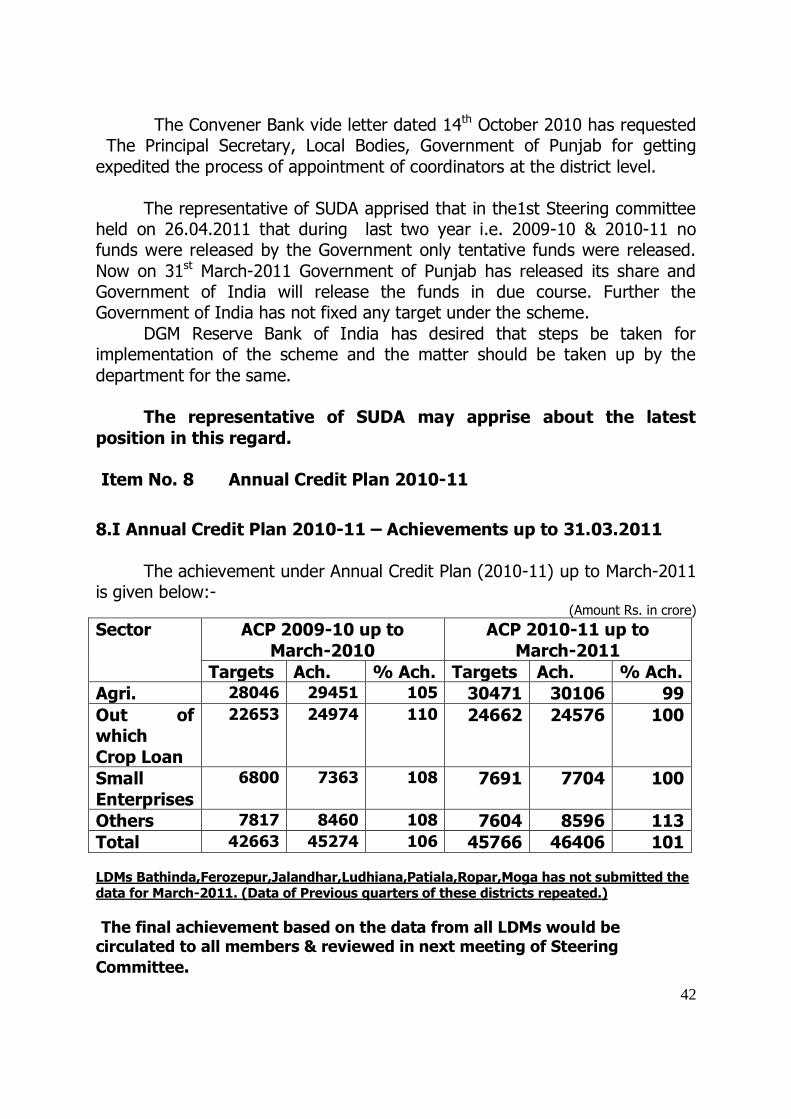

Item No. 8 Annual Credit Plan 2010-11

8.I Annual Credit Plan 2010-11 – Achievements up to 31.03.2011

The achievement under Annual Credit Plan (2010-11) up to March-2011

is given below:- (Amount Rs. in crore)

Sector ACP 2009-10 up to

March-2010

ACP 2010-11 up to

March-2011

Targets Ach. % Ach. Targets Ach. % Ach.

Agri. 28046 29451 105 30471 30106 99

Out of which

Crop Loan

22653 24974 110 24662 24576 100

Small

Enterprises

6800 7363 108 7691 7704 100

Others 7817 8460 108 7604 8596 113

Total 42663 45274 106 45766 46406 101

LDMs Bathinda,Ferozepur,Jalandhar,Ludhiana,Patiala,Ropar,Moga has not submitted the data for March-2011. (Data of Previous quarters of these districts repeated.)

The final achievement based on the data from all LDMs would be circulated to all members & reviewed in next meeting of Steering

Committee.

43

Observations:

As against overall targets of Rs. 45766crore, Banks have disbursed loans to the order of Rs. 46406 crore, The %age achievement

works to 101 %.

As against target of Rs.30471crore under agriculture & allied sector, Banks have disbursed loans to the order of Rs.30106

crore. The achievement comes to 99 % as against 105% for the same period last year. The disbursement under agriculture & allied agriculture activities under Annual Credit Plan 2010-

11 has also gone up by Rs 655 crore as compared to the disbursements made during the same period last year.

Banks disbursed crop loans amounting to Rs.24576 crore against target of Rs.24662 crore. The achievement comes to 100 %.

Banks disbursed loans amounting to Rs. 7704 crore against the

target of Rs. 7691 crore set forth for Small Enterprises Sector. The achievement comes to 100%. However, the disbursement under this sector has also gone up by Rs. 341

crore as compared to the corresponding period last year.

Banks disbursed loans to the tune of Rs8596 crore under Others Priority

Sector against the target of Rs.7604crore. The achievement comes to 113 %. The disbursement under this sector have also gone up by Rs. 136 crore as compared to the corresponding period last

year.

District wise Analysis

The perusal of district-wise progress up to March-2011 under ACP 2010-

11 is given at Annexure XVI reveals as under: -

The overall targets have been exceeded in 7 districts i.e. Amritsar, Fatehgar Sahib, Gurdapur, Hoshiarpur. Muktsar, , Nawanshahr & Mohali

and missed by varying margins in the remaining districts.

Similarly, the targets under Agriculture & Allied Sector have been achieved in 7 districts i.e. Amritsar, Gurdaspur, Hoshiarpur,Kapurthala, Muktsar, Nawanshahr & Mohali & missed by varying margins in the

remaining districts.

44

Likewise, the targets under Crop Loans have also been achieved in districts & missed by varying margins in Amritsar, Mansa, Sangrur,

Mohali, Barnala districts.

The targets under Small & Micro Enterprises have been exceeded in

Amritsar, FatehgarhSahib, Gurdaspur, Hoshiarpur, Kapurthala, Muktsar, Mohali districts & missed by varying margins in remaining districts.

The targets under Other Priority Sector have been achieved in Amritsar,

Fatehgarh Sahib, Faridkot, Gurdaspur, Hoshiarpur, Muktsar, Mohali & Barnala districts & missed by varying margins in remaining districts.

Bank wise Progress

The study of bank-wise progress given as per Annexure XVII reveals as follows:-

Agriculture & Allied Activities

As against target of Rs.30471/-crore under agriculture sector, the

Commercial Banks, have disbursed loans amounting to Rs.30105/- crore. The achievement works out to99 %.

The RRBs have disbursed loans amounting to Rs.1884/-crore under

agriculture sector as against target of Rs.1340/- crore, thus showing achievements of 141 %.

The Cooperative Banks have disbursed loans amounting to Rs.11745/- crore against targets of Rs.10702/- crore. The achievement comes to 91%.

Micro & Small Enterprises / Non Farm Sector

As against target of Rs.7393/- crore under this sector, the Commercial

Banks, have disbursed loans amounting to Rs.7549/-crore. The achievement comes to102 %.

The RRBs have disbursed loans amounting to Rs. 32/- crore under this

sector as against target of Rs.21/- crore, the achievement comes to 65 %.

Whereas, the Cooperative Banks have disbursed loans amounting to

Rs.238/- crore against target of Rs. 120/- crore.

Others Priority Sector

As against target of Rs.6285/- crore under this sector, the Commercial Banks, have disbursed loans amounting to Rs. 7255/-crore, the achievement comes to 115 %.

45

The RRBs have disbursed loans amounting to Rs.86/- crore under this sector as against target of Rs.140/- crore, thus achieving the target by

162%.

The Cooperative Banks have disbursed loans amounting to Rs. 1003/-

crore against target of Rs. 1078/- crore, thus achieving the target by 107%.

The house may review the progress under ACP 2010-11 up to March 2011.

8.II Flow of Investment Credit under Agriculture

The comparative position of achievement of targets for investment

credit under Annual Credit Plans up to period ended March 2011 is as under:

(Amount Rs. in crore)

Annual Credit Plan

Investment Credit under Agriculture

Annual Targets Achievement

2008-09 5761 4783 (83%)

2009-10 5393 4477 (83%)

2010-11 5808 5526(95.14) (Figures in parenthesis denote % age achievement over targets).

(Bank-wise progress is as per Annexure-XVIII).

Observations:-

As against pro-rata target of Rs.5808/- crore for Agri Investment credit

under ACP 2010-11, banks up to March 2011 have disbursed loans

amounting to Rs.5526/- crore, the achievement works out to 95.14 % .

The house may review please.

Item No. 9 Farmers‟ Club Programme

NABARD has been facilitating formation & nurturing of Farmers’ Clubs since 1982. With a view to making the farmers club programme sustainable and more vibrant, a comprehensive review of the programme was made and

a few changes have been evolved by NABARD, which are effective from April

46

2008. The mission of the programme is development through credit, technology transfer, awareness and capacity building.

The cumulative progress achieved in formation of Farmers’ Clubs in

Punjab is as follows:

Farmers‟ Clubs Formed Cumulative Position

2009-10 up to March 10

2010-11 up to March 11

As at March 2011

208 233 (12%)

839

During the financial year 2010-11 banks in Punjab, have

launched/established 233 new Farmers’ Clubs as against 208 such Clubs

formed during the same period last year, thus showing YoY growth of 12%.

The House may review the progress.

Item No. 10 National Horticulture Board & National Horticulture

Mission The summary of the progress achieved in LOI cases of National Horticulture Board is as follows;

(Amount Rs. in Lakh)

Year LOI

Issued

Cases

disbursed

Subsidy

Released

2008-09 108 33 43

2009-10 30 26 34

2010-11 5 0 0

As resolved in the last meeting of SLBC, the Convener Bank has also sought the performance data from Department of Horticulture regarding

implementation of National Horticulture Mission and the summary of the same is as follows;

Year Area Covered (in hec) Subsidy Released (Rs. in Lakh)

2009-10 4800 539

2010-11

5300 667

The House may review the progress.

47

Item No. 11 Advances to Industrial Sector

11.I Credit to Small & Medium Enterprises (SME)

India’s Small & Medium Enterprises (SMEs) manufacture about 8000

products, account for 6% of GDP, 34% of national exports and employ 30

million work force. Latest Guidelines

Reserve Bank of India vide circular RPCD.SME & NFS.NO.

BC.90/06.02.31/2009-10 dated 29th June 2010 has apprised that as per extant instructions contained in para 1.3 and para 2.1.3 of the Master Circular on lending to Micro, Small and Medium Enterprises (MSME) banks are advised to

ensure that: