11.delta (part 3) - zerodha varsity

DESCRIPTION

sfdnsfTRANSCRIPT

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 1/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/

CHAPTER 11

Delta (Part 3)

11.1 – Add up the Deltas

Here is an interesting characteristic of the Delta – The Deltas can be added up!

Let me explain – we will go back to the Futures contract for a moment. We know for every point

change in the underlying’s spot value the futures also changes by 1 point. For example if Nifty

Spot moves from 8340 to 8350 then the Nifty Futures will also move from 8347 to 8357 (i.e.

assuming Nifty Futures is trading at 8347 when the spot is at 8340). If we were to assign a deltavalue to Futures, clearly the future’s delta would be 1 as we know for every 1 point change in the

underlying the futures also changes by 1 point.

Now, assume I buy 1 ATM option which has a delta of 0.5, then we know that for every 1 point

move in the underlying the option moves by 0.5 points. In other words owning 1 ATM option is as

good as holding half futures contract. Given this, if I hold 2 such ATM contracts, then it as good as

MODULES

SHARE

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 2/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 2

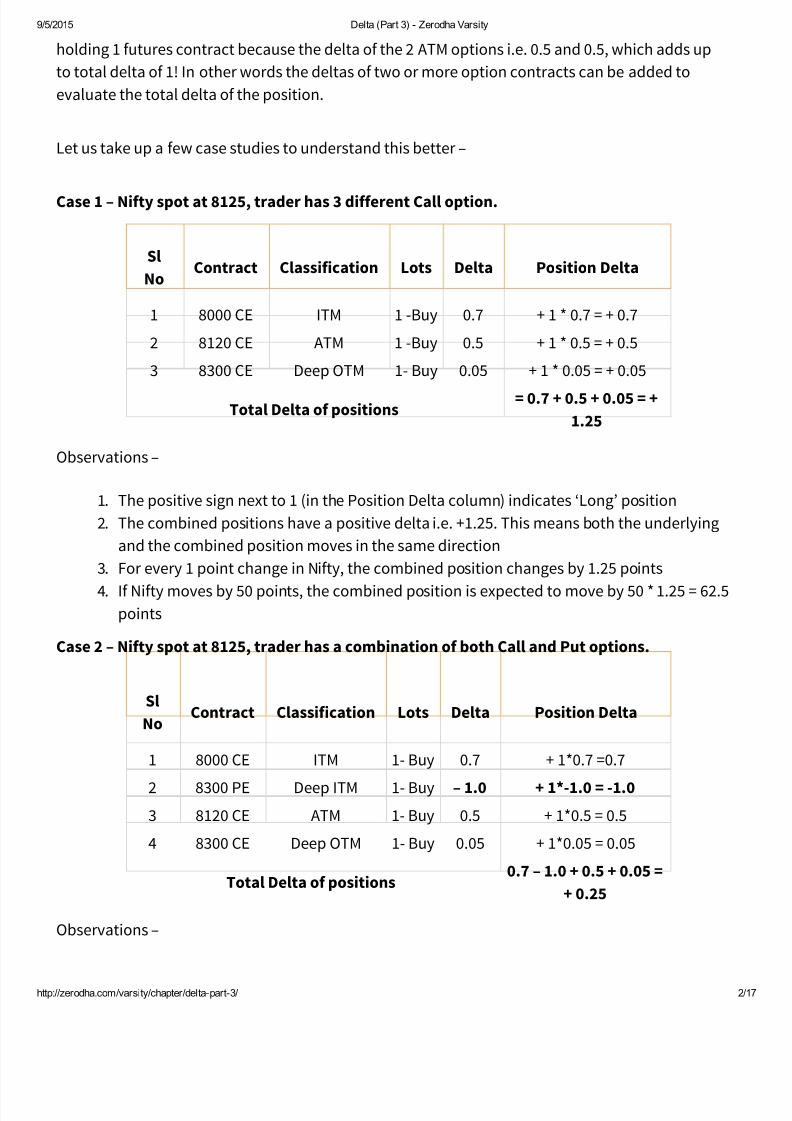

holding 1 futures contract because the delta of the 2 ATM options i.e. 0.5 and 0.5, which adds up

to total delta of 1! In other words the deltas of two or more option contracts can be added to

evaluate the total delta of the position.

Let us take up a few case studies to understand this better –

Case 1 – Nifty spot at 8125, trader has 3 different Call option.

Sl

NoContract Classification Lots Delta Position Delta

1 8000 CE ITM 1 -Buy 0.7 + 1 * 0.7 = + 0.7

2 8120 CE ATM 1 -Buy 0.5 + 1 * 0.5 = + 0.5

3 8300 CE Deep OTM 1- Buy 0.05 + 1 * 0.05 = + 0.05

Total Delta of positions= 0.7 + 0.5 + 0.05 = +

1.25

Observations –

1. The positive sign next to 1 (in the Position Delta column) indicates ‘Long’ position

2. The combined positions have a positive delta i.e. +1.25. This means both the underlying

and the combined position moves in the same direction

3. For every 1 point change in Nifty, the combined position changes by 1.25 points

4. If Nifty moves by 50 points, the combined position is expected to move by 50 * 1.25 = 62.5points

Case 2 – Nifty spot at 8125, trader has a combination of both Call and Put options.

Sl

NoContract Classification Lots Delta Position Delta

1 8000 CE ITM 1- Buy 0.7 + 1*0.7 =0.7

2 8300 PE Deep ITM 1- Buy – 1.0 + 1*-1.0 = -1.0

3 8120 CE ATM 1- Buy 0.5 + 1*0.5 = 0.5

4 8300 CE Deep OTM 1- Buy 0.05 + 1*0.05 = 0.05

Total Delta of positions0.7 – 1.0 + 0.5 + 0.05 =

+ 0.25

Observations –

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 3/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 3

1. The combined positions have a positive delta i.e. +0.25. This means both the underlying

and the combined position move in the same direction

2. With the addition of Deep ITM PE, the overall position delta has reduced, this means the

combined position is less sensitive to the directional movement of the market

3. For every 1 point change in Nifty, the combined position changes by 0.25 points

4. If Nifty moves by 50 points, the combined position is expected to move by 50 * 0.25 = 12.5

points

5. Important point to note here – Deltas of the call and puts can be added as long as it

belongs to the same underlying.

Case 3 – Nifty spot at 8125, trader has a combination of both Call and Put options. He has 2

lots Put option here.

Sl

NoContract Classification Lots Delta Position Delta

1 8000 CE ITM 1- Buy 0.7 + 1 * 0.7 = + 0.7

2 8300 PE Deep ITM 2- Buy -1 + 2 * (-1.0) = -2.0

3 8120 CE ATM 1- Buy 0.5 + 1 * 0.5 = + 0.5

4 8300 CE Deep OTM 1- Buy 0.05 + 1 * 0.05 = + 0.05

Total Delta of positions0.7 – 2 + 0.5 + 0.05 = –

0.75

Observations –

1. The combined positions have a negative delta. This means the underlying and the

combined option position move in the opposite direction

2. With an addition of 2 Deep ITM PE, the overall position has turned delta negative, this

means the combined position is less sensitive to the directional movement of the market

3. For every 1 point change in Nifty, the combined position changes by – 0.75 points

4. If Nifty moves by 50 points, the position is expected to move by 50 * (- 0.75) = -37.5 points

Case 4 – Nifty spot at 8125, the trader has Calls and Puts of the same strike, same

underlying.

Sl No Contract Classification Lots Delta Position Delta

1 8100 CE ATM 1- Buy 0.5 + 1 * 0.5 = + 0.5

2 8100 PE ATM 1- Buy -0.5 + 1 * (-0.5) = -0.5

Total Delta of positions + 0.5 – 0.5 = 0

Observations –

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 4/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 4

1. The 8100 CE (ATM) has a positive delta of + 0.5

2. The 8100 PE (ATM) has a negative delta of – 0.5

3. The combined position has a delta of 0, which implies that the combined position does

not get impacted by any change in the underlying

a. For example – If Nifty moves by 100 points, the change in the options positions

will be 100 * 0 = 0

4. Positions such as this – which have a combined delta of 0 are also called ‘Delta Neutral’positions

5. Delta Neutral positions do not get impacted by any directional change. They behave as if

they are insulated to the market movements

6. However Delta neutral positions react to other variables like Volatility and Time. We will

discuss this at a later stage.

Case 5 – Nifty spot at 8125, trader has sold a Call Option

Sl No Contract Classification Lots Delta Position Delta

1 8100 CE ATM 1- Sell 0.5 – 1 * 0.5 = – 0.5

2 8100 PE ATM 1- Buy -0.5 + 1 * (-0.5) = – 0.5

Total Delta of positions – 0.5 – 0.5 = – 1.0

Observations –

1. The negative sign next to 1 (in the Position Delta column) indicates ‘short’ position

2. As we can see a short call option gives rise to a negative delta – this means the optionposition and the underlying move in the opposite direction. This is quite intuitive

considering the fact that the increase in spot value results in a loss to the call option seller

3. Likewise if you short a PUT option the delta turns positive

a. -1 * (-0.5) = +0.5

Lastly just consider a case wherein the trader has 5 lots long deep ITM option. We know the total

delta of such position would + 5 * + 1 = + 5. This means for every 1 point change in the underlying

the combined position would change by 5 points in the same direction.

Do note the same can be achieved by shorting 5 deep ITM PUT options –

– 5 * – 1 = + 5

-5 indicate 5 short positions and -1 is the delta of deep ITM Put options.

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 5/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 5

The above case study discussions should give you a perspective on how to add up the deltas of

the individual positions and figure out the overall delta of the positions. This technique of adding

up the deltas is very helpful when you have multiple option positions running simultaneously and

you want to identify the overall directional impact on the positions.

In fact I would strongly recommend you always add the deltas of individual position to get a

perspective – this helps you understand the sensitivity and leverage of your overall position.

Also, here is another important point you need to remember –

Delta of ATM option = 0.5

If you have 2 ATM options = delta of the position is 1

So, for every point change in the underlying the overall position also changes by 1 point (as the

delta is 1). This means the option mimics the movement of a Futures contract. However, do

remember these two options should not be considered as a surrogate for a futures contract.

Remember the Futures contract is only affected by the direction of the market, however the

options contracts are affected by many other variables besides the direction of the markets.

There could be times when you would want to substitute the options contract instead of futures

(mainly from the margins perspective) – but whenever you do so be completely aware of itsimplications, more on this topic as we proceed.

11.2 – Delta as a probability

Before we wrap up our discussion on Delta, here is another interesting application of Delta. You

can use the Delta to gauge the probability of the option contract to expire in the money.

Let me explain – when a trader buys an option (irrespective of Calls or Puts), what is that he

aspires? For example what do you expect when you buy Nifty 8000 PE when the spot is trading at

8100? (Note 8000 PE is an OTM option here). Clearly we expect the market to fall so that the Put

option starts to make money for us.

In fact the trader hopes the spot price falls below the strike price so that the option transitions

from an OTM option to ITM option – and in the process the premium goes higher and the trader

makes money.

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 6/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 6

The trader can use the delta of an option to figure out the probability of the option to transition

from OTM to ITM.

In the example 8000 PE is slightly OTM option; hence its delta must be below 0.5, let us fix it to 0.3

for the sake of this discussion.

Now to figure out the probability of the option to transition from OTM to ITM, simply convert the

delta to a percentage number.

When converted to percentage terms, delta of 0.3 is 30%. Hence there is only 30% chance for the

8000 PE to transition into an ITM option.

Interesting right? Now think about this situation – although an arbitrary situation, this in fact is a

very real life market situation –

1. 8400 CE is trading at Rs.4/-

2. Spot is trading at 8275

3. There are two day left for expiry – would you buy this option?

Well, a typical trader would think that this is a low cost trade, after all the premium is just Rs.4/-

hence there is nothing much to lose. In fact the trader could even convince himself thinking that if

the trade works in his favor, he stands a chance to make a huge profit.

Fair enough, in fact this is how options work. But let’s put on our ‘Model Thinking’ hat and figure

out if this makes sense –

1. 8400 CE is deep OTM call option considering spot is at 8275

2. The delta of this option could be around 0.1

3. Delta suggests that there is only 10% chance for the option to expire ITM

4. Add to this the fact that there are only 2 more days to expiry – the case against buying this

option becomes stronger!

A prudent trader would never buy this option. However don’t you think it makes perfect sense to

sell this option and pocket the premium? Think about it – there is just 10% chance for the option

to expire ITM or in other words there is 90% chance for the option to expire as an OTM option.

With such a huge probability favoring the seller, one should go ahead and take the trade with

conviction!

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 7/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 7

(http://zerodha.com/varsity/chapter/delta-part-2/)

(http://zerodha.com/varsity/chapter/gamma-part-1/)

In the same line – what would be the delta of an ITM option? Close to 1 right? So this means there

is a very high probability for an already ITM option to expire as ITM. In other words the probability

of an ITM option expiring OTM is very low, so beware while shorting/writing ITM options as the

odds are already against you!

Remember smart trading is all about taking trades wherein the odds favor you, and to know if the

odds favor you, you certainly need to know your numbers and don your ‘Model Thinking’ hat.

And with this I hope you have developed a fair understanding on the very first Option Greek – The

delta.

The Gamma beckons us now.

Key takeaways from this chapter1. The delta is additive in nature

2. The delta of a futures contract is always 1

3. Two ATM option is equivalent to owning 1 futures contract

4. The options contract is not really a surrogate for the futures contract

5. The delta of an option is also the probability for the option to expire ITM

36 Responses to “Delta (Part 3)”

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14703#respond)

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 8/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 8

KHYATI VERDHAN

June 15, 2015 at 10:57 am

¶ htt ://zerodha.com/varsit /comment/14703

Hi kartik

Very very thanks for this chapter.This is very intresting chapter, but after reading this a no. of things running in my mind. Please

check this and correct me where I am wrong.

If delta (sum of all delta’s) is

1. +1.75

Profit- when market goes upLoss – when market goes down

2. +.025

Profit- when market goes up

Loss – when market goes down

3. 0

No profit , No loss at any market movement

4. -.075

Profit- when market goes down

Loss – when market goes up

I also think to calculate net p&l , I can do it mathematically-

Net P&L= total no. of shares of same underlying * change in underlying *total delta(sum of all delta’s)

• Profit- when market goes up and delta is +ve

Or

When market goes down and delta is –ve

• LOSS- when market goes up and delta is -ve

Or

When market goes down and delta is +ve

Is this formula correct??? Since delta is also variable , I am confused. Please clarify

KARTHIK RANGAPPA

June 16, 2015 at 4:46 am

¶ htt ://zerodha.com/varsit /comment/14734

You are absolutely right here –

1) If the deltas add up to a +ve number, this means you make money when the markets goes up2) If the deltas add up to a -ve number, this means you make money when the markets goes down

3) Net P&L = Change in underlying * Total Delta * Lot size —-> how ever please do bear in mind this is only an expected

P&L and not really the actual P&L. Remember an options contract is subjected to other variables…we will understand

this point in detail over the subsequent chapters.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14734#respond)

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 9/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 9

NARSIMHA

June 15, 2015 at 12:23 pm

¶ (http://zerodha.com/varsity/comment/14704)

sir,in tradinr intraday or swing what is definition of down &uptrenr i mean how many candeles down,up

Reply

(http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14704#respond)

KARTHIK RANGAPPA

June 16, 2015 at 4:48 am

¶ htt ://zerodha.com/varsit /comment/14735

Check for at least 6 to 8 prior candles.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?

replytocom=14735#respond)

JAGADEESH (HTTP://WWW.DISCRETIONARY-TRADING.COM)

June 15, 2015 at 3:45 pm

¶ htt ://zerodha.com/varsit /comment/14708

Yet another great article.. Thanks for this..

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14708#respond)

KARTHIK RANGAPPA

June 16, 2015 at 4:49 am

¶ (http://zerodha.com/varsity/comment/14736)

I must thank you for patiently reading all the articles on Varsity and constantly encouraging us

Reply

(http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14736#respond)

KIERON

June 15, 2015 at 7:36 pm

¶ htt ://zerodha.com/varsit /comment/14716

Thank you sir salute you for an great article

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?

replytocom=14716#respond)

KARTHIK RANGAPPA

June 16, 2015 at 4:56 am

¶ htt ://zerodha.com/varsit /comment/14738

Most welcome and I really hope you found the chapter useful and easy to understand.

Reply

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 10/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 10

(http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14738#respond)

KAVYASALUNKE

June 16, 2015 at 7:05 pm

¶ htt ://zerodha.com/varsit /comment/14756

sir i have doubt regarding stoploss of option order,if i want to place stop loss for option with repect to it’s underlying how can i

calculate it? also if option expiring as otm but if my premium is changed by 4-5 what should i consider it means profit or I had

paid premium after profit?

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14756#respond)

KARTHIK RANGAPPA

June 17, 2015 at 5:33 am

¶ htt ://zerodha.com/varsit /comment/14785

This is a very valid question – in fact I would explain this in detail when we take up the 3rd option Greek – Vega. So

request you to please stay tuned till then. Thanks.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14785#respond)

KHYATI VERDHAN

June 17, 2015 at 7:31 am

¶ htt ://zerodha.com/varsit /comment/14790

Hi kartik,

Thanks for clearing my confusions.I have read the chapter many times and develops a clear concept. Clearly, options are

superior than futures. But, thinks problems me is- if ‘X’ persons trade nifty futures, he has to trade at nifty future prices but if ‘Y’

persons trade nifty options and there are 10 strike prices available , then each strike price has only Y/10 volume. However, ATM

options are somehow more volume. Then is there any volume issue with options. Please clarify.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14790#respond)

KARTHIK RANGAPPA

June 18, 2015 at 5:29 am

I get your point here, in fact for this reason along with many others ATM options are always a good option to trade. You

will understand more on this as we progress.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14824#respond)

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 11/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 1

¶ htt ://zerodha.com/varsit /comment/14824

ADITYA GARG

July 14, 2015 at 6:29 am

¶ htt : zerodha.com varsit comment 15964

hi sir thanks for such a simplified version of greeks.

when we can expect article on option strategy?

Reply (http://zerodha.com/varsity/chapter/delta-

part-3/?replytocom=15964#respond)

KARTHIK RANGAPPA

July 15, 2015 at 5:21 am

¶ htt ://zerodha.com/varsit /comment/16001

Aditya, all I can say at this point is soon

Reply

(http://zerodha.com/varsity/chapter/delta-

part-3/?replytocom=16001#respond)

KESHAV

June 17, 2015 at 1:34 pm

¶ (http://zerodha.com/varsity/comment/14794)

I am eagerly waiting for option strategies.. When will u complete this module..?

When will u upload next chapter..?

Reply

(http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14794#respond)

KARTHIK RANGAPPA

June 18, 2015 at 5:33 am

¶ htt ://zerodha.com/varsit /comment/14826

Chapter 12 about Gamma (Part 1) should be up by t’row – it is a very different chapter and hopefully you will enjoy

reading it

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14826#respond)

ALOK

June 17, 2015 at 1:51 pm

¶ htt : zerodha.com varsit comment 14795

Worth it…Nice job i appreciate your efforts.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?

replytocom=14795#respond)

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 12/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 12

KARTHIK RANGAPPA

June 18, 2015 at 5:34 am

¶ htt : zerodha.com varsit comment 14827

Thanks Alok

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?

replytocom=14827#respond)

ARSHAD

June 17, 2015 at 9:41 pm

¶ htt : zerodha.com varsit comment 14801

I have spent lots of money for getting training about but all are worthless as compare to Varsity….u all did a great job..thanks..

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14801#respond)

KARTHIK RANGAPPA

June 18, 2015 at 5:38 am

¶ htt ://zerodha.com/varsit /comment/14828

Thanks Arshad.

There are many so called ‘market educators’ who in the pretext on teaching market finance fleece your hard earned

money. Keeping this in perspective we started Varsity with an objective of creating an online platform where we put up

meaningful content and make it available for everyone, for free.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14828#respond)

AJAY

June 20, 2015 at 3:12 pm

¶ htt : zerodha.com varsit comment 14918

Hello.

I recently read about the Adani enterprise demerger and the controversy surrounding it s the stock plunged 80% intraday. How

does it impact the a) market lot b) futures price c) premium?

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14918#respond)

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=14967#respond)

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 13/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 13

KARTHIK RANGAPPA

June 22, 2015 at 5:07 am

¶ htt ://zerodha.com/varsit /comment/14967

Adani was a mess – mostly attributable to people not reading the circular issued by NSE. The lot size/Future

Price/Premium all depends on the corporate action in perspective. However they all reduce or increase in proportion

to the spot value.

RAMESH

July 8, 2015 at 8:20 am

¶ htt ://zerodha.com/varsit /comment/15669

Hi Team,

Great articles/modules. I’ve learn’t a lot here than reading/attending classes. Very well writen with lots of examples. Thank you

very much.

A lay man question: In delta lesson modul, you’d mentioned that +5 delta moves by 5 points the underling movement of 1

point. Are you refering to points as in ‘premium change’? Pleae kindly clarify.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=15669#respond)

KARTHIK RANGAPPA

July 10, 2015 at 4:42 am

¶ htt ://zerodha.com/varsit /comment/15726

Thanks Ramesh, very happy to know that you appreciate the efforts. Please do stay tuned for more.

Yes, if an option has a Delta of 0.5, then for every 1 point change in the underlying then the premium changes by 0.5

points.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=15726#respond)

RAMESH

July 16, 2015 at 6:22 am

¶ htt ://zerodha.com/varsit /comment/16025

Thank You Karthik.

So if 5 contracts of 0.5 Delta then, the Delta adds up to 2.5. Then every 1 point move in underlying the position

will now move 2.5 times (premium points) – either side up or down.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=16025#respond)

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 14/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 14

KARTHIK RANGAPPA

July 16, 2015 at 7:09 am

¶ htt ://zerodha.com/varsit /comment/16033

Yes sir. Thats correct.

Reply

(http://zerodha.com/varsity/chapter/delta-

part-3/?replytocom=16033#respond)

SANATHARAM

July 8, 2015 at 6:41 pm

¶ htt ://zerodha.com/varsit /comment/15679

Can I use option strategies for intraday trading depending upon the situation? In intraday for example if am using bull spread,

the shorted OTM Option won’t have much impact due to non deterioration of theta.. Even the Usage of neutral strategy,

shorting 2ATM, Buying 1ITM & 1OTM won’t have much impact if my position is wrong.. Suggest the usage of options strategy for

intraday trading…

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=15679#respond)

KARTHIK RANGAPPA

July 10, 2015 at 4:56 am

¶ htt : zerodha.com varsit comment 15730

Sanatharam…I will be discussing options strategies in detail in the next module. Request you to kindly stay tuned.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=15730#respond)

SUSANTA

August 9, 2015 at 5:06 am

¶ htt : zerodha.com varsit comment 17296

Hi, thanks for the all teaching modules.. I understand that Delta for call option is +ve, and delta for Put option is -ve. I have a

question.. Can delta be a negative value for a only call option ? I assume not.. But still have a confusion.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=17296#respond)

KARTHIK RANGAPPA

August 10, 2015 at 6:40 am

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=17335#respond)

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 15/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 15

¶ htt ://zerodha.com/varsit /comment/17335

Call Delta per say is a +ve number, but when you short a call option the Delta is considered -ve. Similarly when you

short a put option the delta is considered +ve.

ANAND SINGH

August 26, 2015 at 7:20 am

¶ htt : zerodha.com varsit comment 18094

Hi Karthik, I didn’t understand the case no #5 in this chapter. Can you please elaborate this with premium, delta values for

better understanding. Thanks in advance

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=18094#respond)

KARTHIK RANGAPPA

August 27, 2015 at 5:32 am

¶ htt ://zerodha.com/varsit /comment/18140

Anand – Case 5 talks about a situation wherein you have a short ITM Call option. ITM options have a delta of 0.5, since

you are short call option the position delta would be 1 * (-0.5) = -0.5. The other position is a long ITM Put option. Put

option has a negative delta…but do remember when you short a put option, the delta is +ve.

So the overall delta of this position becomes -0.5 (from short ITM call) plus -0.5 (from long ITM Put), hence an over all

delta of -1.0.

Reply (http://zerodha.com/varsity/chapter/delta-part-3/?replytocom=18140#respond)

ANAND SINGH

August 27, 2015 at 7:20 am

¶ htt : zerodha.com varsit comment 18145

Sir, It is ATM position as delta is 0.5. Correct Sir.

Reply (http://zerodha.com/varsity/chapter/delta-part-

3/?replytocom=18145#respond)

KARTHIK RANGAPPA

August 28, 2015 at 5:33 am

¶ htt : zerodha.com varsit comment 18185

Yup….in and around 0.5.

Reply

(http://zerodha.com/varsity/chapter/delta-

part-3/?replytocom=18185#respond)

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 16/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

http://zerodha.com/varsity/chapter/delta-part-3/ 16

Logged in as mpsravitej (http://zerodha.com/varsity/wp-admin/profile.php). Log out »

(http://zerodha.com/varsity/wp-login.php?

action=logout&redirect_to=http%3A%2F%2Fzerodha.com%2Fvarsity%2Fchapter%2Fdelta-part-

3%2F&_wpnonce=d5ad7bfee0)

Submit

Select an image for your comment (GIF, PNG, JPG, JPEG):

No file chosenChoose File

Notify me of follow-up comments by email.

ANAND SINGH

August 28, 2015 at 8:44 am

¶ htt : zerodha.com varsit comment 18201

Thanks Karthik. I owe you a lot. Your gyan on technical analysis enriched my knowledge and

ignited passion for trading. Thanks a ton. After saying goodbye to long career in banking and

insurance I decided to become full time trader and was looking for authentic material on TA

and FA. Believe me your content is far more better than any book on share market in

circulation. Karthik tell me is it true that 95% people loose money in the market. If it is true

then who are the rest 5%. And how to increase the success rate in trading. Plz share your

thoughts.

KARTHIK RANGAPPA

August 29, 2015 at 6:30 am

¶ htt : zerodha.com varsit comment 18236

Thanks for the kind words Anand. Yes, it is true that most of the people lose money

‘attempting’ to trade. Think is mainly because the vast majority trade based on gut feel, and

random theories. Besides somewhere their egos take over their brains and they fail to evolve

themselves as traders. Most of them dont even bother to educate themselves.

My suggestion – Stay humble and constantly educate yourself. This alone will enhance your

odds of being successful in the markets.

Comment*

7/21/2019 11.Delta (Part 3) - Zerodha Varsity

http://slidepdf.com/reader/full/11delta-part-3-zerodha-varsity 17/17

9/5/2015 Delta (Part 3) - Zerodha Varsity

Copyright 2014 Varsity@Zerodha

(http://zerodha.com/varsity)

Chapter 11

Option Theory